Embed Size (px)

Citation preview

Recommending overweight commodities and long enhanced GSCI.

Historically, when the US and Chinese output gap closes and inflation begins to rise,

this has been a buy signal for commodities. We believe the recent reacceleration in

global PMIs suggests commodity markets are entering a cyclically stronger

environment. Supply restrictions from policy actions should benefit oil, coking coal

and nickel in the near term while economic reductions should boost natural gas and

zinc. Accordingly, we are upgrading our GSCI returns forecast to +9.0%

/+11.0%/+6.0% on a 3, 6 and 12 month basis from -2.0%/+1.7%/+8.3%.

The increased likelihood of an OPEC cut motivates our near-term forecast

upgrade. Stronger than expected demand growth and lower production from high-

cost countries increase our confidence that the global oil market will shift into deficit

by 2H17 even with OPEC production above current levels. Thus, there is now a

stronger incentive for OPEC producers to halt inventory growth in 1H17 and normalize

the current high level of inventories with a short-duration production cut. We think a

cut should generate backwardation – helping OPEC grow market share by sidelining

higher-cost producers – and reduce oil price volatility – increasing the valuation of

their debt and equity.

Higher commodity prices likely to improve financial conditions. Commodity

prices are correlated with the accumulation and de-accumulation of EM excess

savings. Unlike in the 1970s, more sophisticated financial markets in the 2000s were

able to transform the excess savings into greater global liquidity that increased asset

values, lowered interest rates and improved credit conditions that spanned the globe.

Weak commodity prices in 2015 and 2016 acted as a drag on financial conditions.

A bullish dollar view is not incompatible with a bullish commodity view. We

expect that the positive roll return from backwardation in commodities will offset the

Commodity Watch

Why high commodity prices can be good for the world: Upgradingto overweight commodities in 2017

A stronger cyclical backdrop

expect that the positive roll return from backwardation in commodities will offset the

downward pressure from a strengthening dollar, as has historically been the case.

We upgrade our 3/6/12-month iron ore price forecasts to $65/63/55 per tonne.

Steel consumption is more resilient than expected and demand for iron ore is likely to

be supported further by incremental restocking across the steel supply chain. Further,

the pace of supply growth has slowed as a result of delayed capital expenditure and

operational challenges.

We downgrade our 3/6-month gold price forecast to $1200/toz on stronger

cyclical outlook. Downside risks remain from potential physical ETF liquidation.

However, our 12-month outlook is unchanged at $1250/toz as it depends on how the

Fed responds to potential US stimulus and inflation as the economy reaches full

employment.

Cyclically driven commodity reflation. We recommend going long the enhanced

GSCI commodity index (number 139) indexed to 100 with a target of 112 and a stop

of 94. We prefer the enhanced structure to reduce the current negative carry on oil.

It is tempting to blame the sharp post-election rally in industrial metals prices on

President-elect Trump’s platform of lower taxation and higher public spending on

infrastructure. Instead, we would argue this rally was a continuation of a reflation

trend put in place at the start of 2016 by the Chinese through credit stimulus aimed at

infrastructure projects and policy driven supply curtailments in coal where they have

50% of global production. Although this was policy driven and a Trump victory

increases the odds of further fiscal policy stimulus, these policy actions all act as a

tailwind on a US economy in the later stages of a business cycle pushing near

capacity.

Historically, when the US and Chinese output gaps close and inflation begins to rise,

this has been a buy signal for commodities. While the knee jerk reaction of copper

and iron ore prices to a Trump victory was likely too much too quickly, we believe that

commodity markets are entering a cyclically stronger environment after a mid-cycle

pause as evidenced by the recent reacceleration in global PMIs . Near-term, oil,

natural gas, zinc, coking coal and nickel are all poised to benefit from a cyclically

stronger demand backdrop due to supply restrictions from either policy actions (oil,

stronger demand backdrop due to supply restrictions from either policy actions (oil,

coking coal and nickel) or economic reductions (natural gas and zinc). Accordingly,

we are upgrading our GSCI returns forecast to +9.0% /+11.0%/+6.0% on a 3, 6 and

12-month basis from -2.0%/+1.7%/+8.3%, and moving to an overweight

recommendation on commodities on a three and 12-month basis. We are also

initiating a 2017 Top 10 trading recommendation to go long the enhanced GSCI index.

It is often thought that commodity returns are linked to the rate of economic

expansion. Thus, the type of broad mid-cycle economic slowdown experienced during

2016 causes investors to assume commodity investments will perform poorly.

Historical evidence contradicts this traditional argument, as following a mid-cycle

pause, commodities have entered extended bull markets where they have

outperformed other asset classes (see Exhibits 1 and 2). The reason is that commodity

returns do not depend so much on the rate of economic growth as they do on the

level of demand relative to supply. Commodity production is characterized by limited

ability to expand capacity in the short run. Even for fast-cycle US shale it is 3-6

months. Thus, producers tend to “over” produce during business cycle lows, building

inventories and driving prices down. But as demand increases during the expansion

and supply is curtailed, demand eventually exceeds capacity and inventories are

drawn down and prices appreciate.

The mid-cycle pause tends to be a good marker of this transition from surplus to

insufficient capacity, as it follows from the central bank’s assessment that the

economy is running out of capacity and the need for a tightening of monetary policy.

This shift to a tighter policy creates a slowdown where the economy can move close

to a recession, perhaps with a single negative quarter or even a very mild recession

before the expansion reasserts itself. These brief slowdowns are usually accompanied

by some Federal Reserve easing, or as in the case of 2016 a more dovish stance. Such

pauses do not typically materially affect the level of commodity demand; rather, they

just slow the rate of growth. Thus, once growth is re-established after the mid-cycle

correction commodities are well positioned to produce sustained and significant

positive returns.

Exhibit 1: The mid-cycle pause is a goodmarker of transition from surplus toinsufficient capacity...

Exhibit 2: ...and commodities tend tooutperform other asset classes ascapacity constraints bite

An OPEC cut to normalize inventories makes economic sense

insufficient capacity...

GDP growth (%qoq, SA); Mid-cycle Pause toPeak of Cycle

Source: BEA, CBS, Goldman Sachs GlobalInvestment Research

capacity constraints bite

S&P GSCI performance relative to S&P 500(equities) and 10Y US Treasury (bonds) (%,total returns)

Source: S&P, Bloomberg, Goldman Sachs GlobalInvestment Research

Our upgrade to the near-term return forecasts is driven primarily by the increased

likelihood of an OPEC production cut that is aimed more at normalizing inventories to

reduce oil price volatility and create backwardation than to create sustainable price

increases (see Oil: Tactically bullish on stronger OPEC cut rationale). As a result, we are

not changing our 2017 WTI price forecast of $52.50/bbl, we are just shifting the

upside from late next year to the near-term, and moving some downside into late next

year.

Oil fundamentals have weakened sharply since OPEC announced a tentative

agreement to cut production in late September, pushing prices near our previous

target of $43/bbl, and absent such a cut we now expect a large surplus of 0.7 mb/d in

1Q17. Importantly though, the combination of stronger expected demand growth and

lower production from high-cost countries in decline, leave us more confident that the

global oil market will shift into deficit by 2H17 even at OPEC production above current

levels.

With greater certainty that deficits will finally materialize, there is now a stronger

economic incentive for OPEC producers to prevent a further rise in inventories in

1H17 and instead act to normalize the current high level of inventories through a short

duration production cut. We believe that such a cut will likely generate backwardation

The risk reward suggests getting long now

duration production cut. We believe that such a cut will likely generate backwardation

– helping them grow market share by sidelining higher-cost producers – as well as

reduce oil price volatility – which should increase the valuation of the debt and equity

they are issuing. In our view, the goal of normalizing inventories should however not

target elevated oil prices as the flattening of the cost curve and the unprecedented

velocity of the shale supply response would make such an endeavor rapidly self-

defeating above $55/bbl.

During 2H17, the key to investment returns in energy is the expected return to

backwardation driven by a successful OPEC cut. To understand why this would make

sense for OPEC to do in the New Oil Order where a flattening of the oil cost curve

incentivizes low-cost producers to grow revenues through increased market share, it

is important to emphasize that backwardation which is achieved though lower

inventories actually enables this strategy by removing the ability of higher-cost

producers to hedge their future production at a higher price. For example, looking at

three B+ rated US E&Ps, our HY energy analysts estimate that in a $45/bbl spot price

environment, a 1-yr contango of $5/bbl fully offsets the high cost of funding for that

period.

Should OPEC output average 33.0 mb/d in 1H17 before seasonally ramping up, we

expect OECD inventories (measured in days of demand coverage) to normalize to their

three-year average by 2Q17, at a level that warrants backwardation in the Brent crude

oil forward curve. Normalizing inventory levels leads us to raise our 3-month WTI price

forecasts to $55/bbl from $45/bbl. We are however reducing our 12-month WTI

forecasts to $50/bbl from $60/bbl on an expected resumption in OPEC production

growth, higher US shale supply response to the 1H17 rally as well as a further

strengthening of the US dollar.

If our assessment of the odds of a cut are wrong and OPEC fails to agree to a cut, we

would expect prices to decline from current levels as it implies greater sequential

production from the group in a battle for market share. The end outcome would

however likely still lead to our 2017 forecast of $52.50/bbl, with a path similar to what

we had previously published: low prices in 1Q17 generating a recovery in prices

through the year through further high-cost producer attrition. However, in this

environment the investment returns would likely be backend loaded as opposed to

front end loaded. Nonetheless, given today’s entry point and the now much higher

likelihood of an OPEC production cut, we believe the 9% expected near-term returns

Why higher commodity prices can be good for the world

likelihood of an OPEC production cut, we believe the 9% expected near-term returns

following an OPEC production cut more than offset the potential drag on returns from

a failed OPEC agreement of -2.0% on a 3-month horizon.

Exhibit 3: The risk reward from our current forecast now looks more attractive

Source: S&P, Goldman Sachs Global Investment Research

Not only does a production cut make economic sense for OPEC, but higher oil and

commodity prices also create better financial conditions for the world. We saw the

financial benefits that China derived this year from higher coal, iron ore and steel

prices by reducing default risks in the most leveraged industries, but we also saw this

year how low oil prices never provided the economic boost many thought would

materialize. Instead, we believe higher oil prices will give the US Federal Reserve more

runway in raising rates through improved financial conditions. This is the opposite of

what we saw in 2016 when lower oil prices weakened financial conditions as the Fed

tried to raise rates.

Going back to the early 2000s, despite warnings by economists that high oil prices

would slow growth, the global economy surged ahead even as oil prices climbed

above $100/bbl, and despite hopes of a growth tailwind due to lower oil prices since

above $100/bbl, and despite hopes of a growth tailwind due to lower oil prices since

2014, global growth slowed significantly when prices plunged toward $25/bbl earlier

this year. The experience from the 1970s created this deep rooted belief that, when oil

prices increased, the wealth transfer from the low-saving developed markets to the

high-saving emerging markets would slow growth due to the relatively lower marginal

propensity to consume in the emerging markets and do the opposite as oil prices

declined.

What this explanation failed to address was the high correlation between oil prices

and excess savings and the greater liquidity and credit availability that these excess

savings in the emerging markets created from 2002 to 2014 and eventually took away

post 2014. Unlike the 1970s, more sophisticated financial markets in the 2000s were

able to transform this excess savings into greater global liquidity that increased asset

values, lowered interest rates and improved credit conditions that spanned the globe.

The improved financial conditions generated from the excess savings that resulted in

part from higher oil prices more than offset the drag from a lower marginal propensity

to consume and vice versa as oil prices declined after 2014.

As oil prices surged and global trade boomed during the 2000s so did the size of

excess savings outside of the US (see Exhibit 4), growing from $1.0 trillion in 2001 to

a peak of $7.0 trillion in 2014 before oil prices rolled over in June of that year. Today,

excess savings stand at $5.8 trillion (this does not include at least another $3.5 trillion

which is held in sovereign wealth funds), and as a point of comparison, M2 in the US

is $13.0 trillion. These savings in turn drive asset values including homes and financial

assets which impacts a consumer’s assessment of their permanent income as well as

impacts their access to credit markets to borrow and smooth their consumption. In

other words, the difference between today and the 1970s is that oil creates global

liquidity through a far more sophisticated financial system.

Exhibit 4: EM excess savings peaked in June 2014 and have been decreasing since

bn $

Source: Haver, Goldman Sachs Global Investment Research

The key to this argument is twofold. First, oil prices are not simply a reflection of the

price of hydrocarbons, but rather on average the price of all traded goods (see Exhibit

5). The common denominator across nearly all traded goods is the US dollar due it

being the numeraire (currency of denomination) in global trade, and as the correlation

between the US dollar and oil rose in the 2000s, so did the correlation across the

prices of all commodities and traded goods. Driving this correlation between oil prices

and the US dollar was the excess savings itself. Higher oil prices led to more dollar

accumulation which put downward pressure on the dollar relative to other currencies

(see Exhibit 6).

Exhibit 5: Oil is highly correlated to theprice of all traded goods

index(lhs), $/bbl (rhs)

Source: CPB, Bloomberg, Goldman Sachs Global

Exhibit 6: Higher oil price leads togreater accumulation of excess savingsby EMs

Change in EM excess savings (%yoy, verticalaxis); Change in oil pirce (%yoy, horizontalaxis)

Source: CPB, Bloomberg, Goldman Sachs GlobalInvestment Research

Source: Haver, Bloomberg, Goldman Sachs GlobalInvestment Research

Although oil and commodities only represent 34% of global trade, the impact of

commodity prices on global savings is far larger than the commodity markets alone as

the prices of all traded goods denominated in dollars are correlated with the oil price

(see Exhibit 7). For example, the Korean export basket is priced relatively constant in

Korean Won, but because exports are transacted in US dollars and the price of oil is

correlated with the dollar, the dollar price of Korean exports are correlated with the

price of oil and so is their excess savings. Same goes for China and the rest of the EM.

As a result, oil prices are highly correlated with the accumulation and de-accumulation

of global excess savings, even in China (see Exhibit 8).

Exhibit 7: Dollar price of Korean exportsis correlated with oil

index (lhs), $/bbl (rhs)

Source: Haver, Bloomberg, Goldman Sachs GlobalInvestment Research

Exhibit 8: Even China's accumulation ofexcess savings is highly correlated withoil

Change in China excess savings (%yoy,vertical axis); Change in oil pirce (%yoy,horizontal axis)

Source: Goldman Sachs Global InvestmentResearch

Second, the credit multiplier on the excess savings (Eurodollar) is higher than the

Second, the credit multiplier on the excess savings (Eurodollar) is higher than the

domestic US credit multiplier (see Exhibit 9). Accordingly, higher oil prices amplify the

dollar liquidity outside of the US and vice versa. This implies that by creating credit

availability, higher oil prices improve global financial conditions while lower oil prices

tighten financial conditions (see Exhibit 10). In the current environment of lower oil

prices, slower global trade and weaker Chinese growth, this linkage between trade, oil

and liquidity would suggest that credit availability on a global basis is likely tighter

than what is commonly viewed. This is why higher oil and commodity prices from

current levels should be viewed as positive to global growth and that the Fed could

get more runway in raising rates from an OPEC production cut.

Exhibit 9: Ex-US (Eurodollar) moneymultiplier is currently higher than USdomestic multiplier

Source: BIS, Haver, Goldman Sachs GlobalInvestment Research

Exhibit 10: Higher oil price improvesdollar liquidity for EMs

bn $ (lhs), $/bbl (rhs)

Source: BIS, Haver, Goldman Sachs GlobalInvestment Research

Exhibit 11: Rising oil prices used to be adrag on US growth; now they have verylittle cumulative impact

VAR model impulse response of real GDP to 1SD oil price shock

Exhibit 12: Higher oil prices also nowease (not tighten) US financial conditions

VAR model impulse response of US FCI to 1SD oil price shock

We believe you can be both commodity and dollar bullish in 2017

Source: Goldman Sachs Global InvestmentResearch

Source: Goldman Sachs Global InvestmentResearch

Given the high negative correlation between commodity prices and the US dollar that

has existed since 2002 (see Exhibit 13) and given the bullish US dollar back drop post

the US election, it raises the question whether our FX strategists’ bullish dollar view is

consistent with our bullish commodity view. We believe so. To answer this question it

is useful to understand what drives the dollar-commodity correlations. At the core of

this correlation is once again the relationship between the price of oil and global

excess savings (see Exhibit 14).

Exhibit 13: Since 2002 there has been ahigh negative correlation betweencommodity prices and the US dollar...

USD Trade Weighted Index (LHS); BrentCrude Oil (RHS)

Source: ICE, Goldman Sachs Global InvestmentResearch

Exhibit 14: ...driven by global excesssavings

Global Excess Savings vs. USD vs Oilcorrelations

Source: CME, ICE

1. While we expect commodity prices to rise, we do not see them rising by enough to

significantly change the financial pressures on EM producers. In a world where

The underlying logic is quite simple. As the dollar is the numeraire for oil, commodities

and global trade, higher oil prices create excess savings in dollars which weigh on the

dollar and vice versa when declining oil prices reduce excess savings. We find that

statistically if the change in oil price leads to a change in excess savings, then there is

a negative correlation between the price of oil and the dollar (see Exhibit 15).

Exhibit 15: When oil is positively correlated with excess dollar savings it becomes negativelycorrelated with the dollar

Source: Goldman Sachs Global Investment Research, Haver, Bloomberg

Therefore, there are two ways to get positive commodity returns in a bullish dollar

environment. The first is to break the correlation between the dollar and oil by

breaking the correlation with oil and excess savings. The second is for returns to be

generated solely from backwardation without price changes, for which there is

precedent for in the late 1980s and mid 1990s, an environment that has been likened

to the upcoming environment. We believe that both forces will likely be at work in

2017:

$50/bbl to $55/bbl oil now looks to be the long-run equilibrium price, there are no

excessive windfall gains to be saved by commodity producers. Rather commodity

income is more likely to be seen as permanent income and hence spent

immediately, helping to finance both fiscal transfers (which remain much higher

than in the last phase of the commodity supply cycle) and efforts to diversify

excessively commodity-centric economies (see Exhibit 16);

2. Our more optimistic outlook for commodity returns during 2H17 is driven to a large

extent by “roll returns”. The benefit of this return is not seen by the commodity

producer (who sells longer dated options), or the commodity consumer (buying

near the front of the curve), but rather the investor who assumes the risk in

transferring between the two. Since roll returns are highly dependent on the level

of inventories, and the willingness to hold inventories is itself a function of the cost

of holding these inventories and hence funding costs, as interest rates rise with a

cyclically stronger backdrop the amount of inventory held should decline, boosting

commodity roll returns – even as the US dollar appreciates due to higher real

interest rate differentials. We expect that the positive roll return from

backwardation will offset the downward pressure from a strengthening dollar, as

has historically been the case (see Exhibit 17).

Exhibit 16: The correlation between oiland the trade weighted USD has alreadystarted to break down

Source: CME, Goldman Sachs Global InvestmentResearch

Exhibit 17: A stronger dollar hashistorically coincided with lower oilprices but not lower roll returns

WTI 1-yr return (spot or roll, % horizontal); 1-yr USD TWI return (% vertical), 1986-2016

Source: Goldman Sachs Global InvestmentResearch

Commodity returns depend more on supply and demand levels, not growth rates

A lesson for OPEC: How China benefited from supply management

Industrial metals markets are either already backwardated (aluminum and iron ore) or

very close (copper, zinc and nickel), which reduces the negative carry of being long

commodities. As the economic cycle matures next year higher demand levels will

likely stress the ability for some key industrial metals to meet demand and lead to a

decline in inventory and hence backwardation. The key is commodity returns do not

depend so much on the rate of economic growth as they do on the level of demand

relative to supply. So while property-related demand growth in China is slowing, the

level of demand is still very high requiring a high level of supply even if growth slows.

When commodity prices rallied in 2016, we learned a lot about the ability of

commodity supply to respond. In zinc and coking coal, sharply higher prices have

failed to create substantial new supplies. In oil, we gained confidence of a clear

delineation in global cost curve near $50/bbl given US drilling activity when prices

surged above that threshold, with $55/bbl or higher likely required to ramp up activity

for higher-cost producers. In copper, prices below $5000/t created supply

curtailments even as long-term price insensitive projects came online in late 2016.

Because we see near-term downside in copper and iron ore given the sharp rise in

these commodities post-election (see Metals' pricing of potential US infrastructure

spending: Too much too fast

(https://research.gs.com/content/research/en/reports/2016/11/12/1e221d6b-5ad9-

4bca-ac15-7145a656da4c.html)), we would view energy has the primary driver of

near-term returns with metals contributing more to returns in 2017H2 and beyond.

China demonstrated in 2016 the financial benefits of higher commodity prices. At the

beginning of the year, concerns about rising Chinese corporate debt levels and non-

performing loans were particularly acute. The potential macroeconomic policy

response of lowering interest rates was also concerning since this would create

downward pressure on the RMB and encourage capital outflows, potentially driving a

self-reinforcing negative loop for Chinese growth. The relatively blunt macroeconomic

action of lowering interest rates would also place further pressure on the balance

sheets of the banks carrying the non-performing loans.

Instead, China’s response was microeconomic and targeted. The government

Instead, China’s response was microeconomic and targeted. The government

implemented policies that stimulate the earnings of the corporates with the highest

credit risks – property and materials (Exhibit 18). It did this via supply side reforms

(coal mine working hour limitations, steel capacity closures) and property specific

credit easing (easier mortgage lending criteria), which drove coal, steel and housing

prices higher, which drove an improvement in both corporates' and the banks’

balance sheets, reducing non-performing loans and systemic risk (Exhibit 19). The

policies enacted have also at least temporarily ended a sustained period of producer

price deflation, and driven an increase in household wealth via property price

inflation.Although China’s still extremely high investment share of GDP and sharply

rising debt to GDP ratio and debt service burden remain concerning from a longer-

term macroeconomic perspective, these supply side reforms created runway for

growth in 2017.

Exhibit 18: The Chinese governmentimplemented policies to stimulateearnings of corporates with the highestcredit risks

Net debt/equity (vertical axis);EBITDA/interest expense (horizontal axis)

Source: Bloomberg, Goldman Sachs GlobalInvestment Research

Exhibit 19: In turn, this reduced non-performing loans and hence systemicrisk

Source: Goldman Sachs Global InvestmentResearch

For Chinese coal these production controls amount to an indirect bailout of the

Chinese coal industry that minimizes the impact on the government and the financial

sector, unlike more conventional methods such as subsidies and write-downs that

Upgrading iron ore forecast for 2017

sector, unlike more conventional methods such as subsidies and write-downs that

require direct injections of capital. In our view, active government intervention in the

domestic coal market may well continue until the end of decade given the significant

debt burden of the Chinese coal industry. Domestic production and inventory levels of

thermal coal are recovering following the gradual lifting of the 276-day limit on

operating hours, and recent contracts negotiated by state-owned miners at a

significant discount to spot prices increase our conviction that regulators are targeting

an equilibrium price in line with marginal cost. We expect inventories to normalize

during the first quarter of 2017, and the likely decline in Chinese demand for imported

coal should allow the Newcastle index to revert to US$60/t from 2Q onward. Although

the steep backwardation in the forward curve reflects market expectations of

restocking, we still see downward risks even after a c.15% sell-off in deferred prices.

We upgrade our 3/6/12-month iron ore price forecasts to $65/63/55 per tonne. In

particular, we believe the need for large cuts in seaborne supply has been postponed

to 2018 due to a combination of factors that moderate the surplus next year. First,

steel consumption is more resilient than expected and demand for iron ore is likely to

be supported further by incremental restocking across the steel supply chain. Second,

the pace of supply growth has slowed as a result of delayed capital expenditure and

operational challenges. Third, capital flows into the iron ore market are likely to

support prices as long as it provides speculative investors with a hedge against a

weaker CNY. We also revise our long-term equilibrium price to US$45/t on the back of

stronger commodity currencies. Rising inventories can offset the divergence between

supply and demand for the next twelve months, but this trend is unsustainable in the

long run and we still expect prices to revert back to the seaborne marginal cost of

production.

On the demand side, while real estate investment in China is expected

(https://research.gs.com/content/research/en/reports/2016/11/20/abb3205d-2385-

4a7a-a582-5ae4964b3150.html) to decelerate modestly in 2017 after the strong price

and sales gains in 2016, continued strength in infrastructure investment and heavy

machinery production are likely to persist. Our steel demand model, which takes

infrastructure investment, property investment, and excavator sales as inputs, predicts

a 2% year-over-year increase in Chinese steel consumption in 2017 (Exhibit 20). The

global macro backdrop is also supportive of steel demand. Our global economics

team projects

(https://research.gs.com/content/research/en/reports/2016/11/16/100ac98c-af5f-458a-

(https://research.gs.com/content/research/en/reports/2016/11/16/100ac98c-af5f-458a-

96a0-b8828627a838.html) global real GDP to growth 3.5% in 2017 vs. 3.0% in 2016.

More importantly, the pickup in fixed investment growth is more pronounced, from

1.5% in 2016 to 3.2% in 2017. Because fixed investment has a stronger link to capex

commodities, our global outlook further supports global demand for steel in 2017.

On the supply side, the Samarco disaster in late 2015 took 28Mt of iron ore

production out of the market and the timeframe for a resumption of operations

remains uncertain. The S11D project, which will have 90Mt annual capacity when fully

in production, is ramping up at a slower pace than anticipated. In China, domestic iron

ore production fell 10% in 2016. While we expect iron ore supply to rise in 2017, we

think this can be partly absorbed by inventory restocking. For example, steel inventory

held by traders and mills has remained at historically low levels in 2016 and we expect

it to return to historical normal levels. Iron ore port inventory has been rising in 2016

as the weakening of local currency drove steel mills to secure supply now for future

uses. As we expect RMB to depreciate another 5% in 2017, we think this dynamic can

continue and increases in port inventory also help take seaborne iron ore supply off

the market.

While the post-election rally appeared to be too much too fast to us and we expect

iron ore prices to decline from the current level of $73/t, the more favorable

fundamental demand and supply picture leads us to believe that iron ore prices can

stay above $60/t during the first half of 2017. In 2017 H2, however, rising supply

should begin to put downward pressure on iron ore prices as demand stays stable but

the inventory restocking process runs into physical constraints and market behavior

starts to reflect the downside price risk of an eventual contraction in Chinese steel

demand. Therefore, we forecast iron ore prices to fall to $55/t by the end of 2017

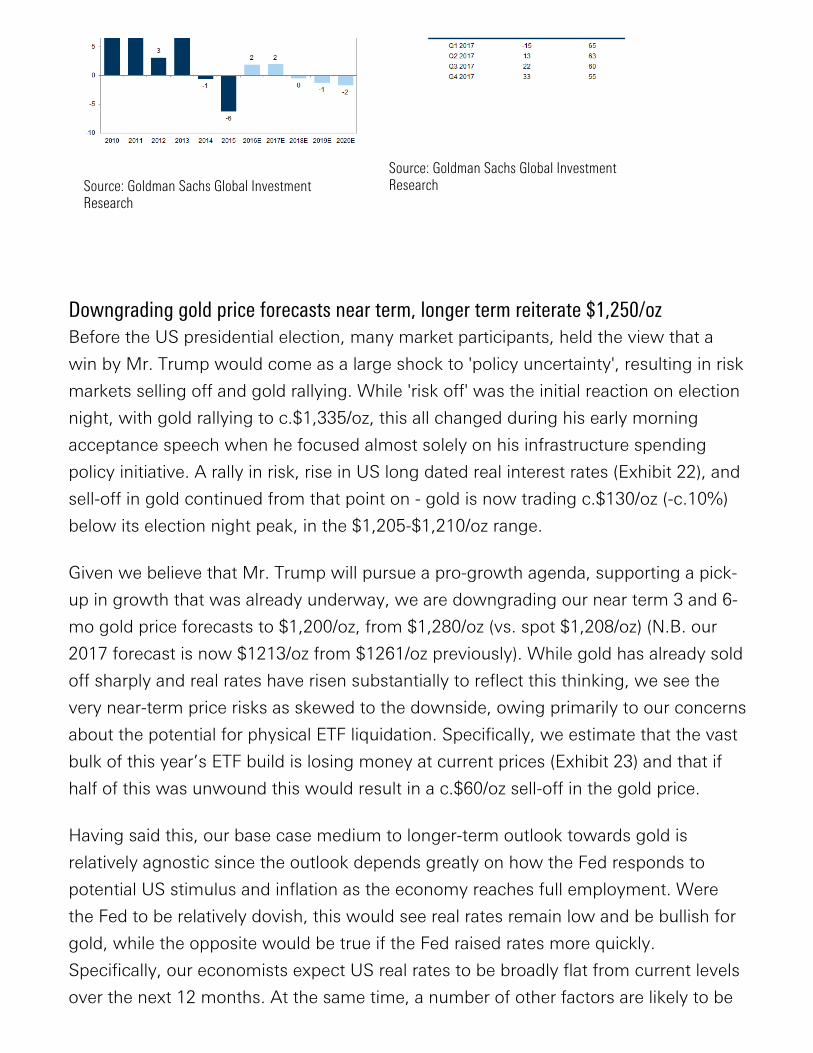

(Exhibit 21).

Exhibit 20: We predict a 2% year-over-year increase in Chinese steelconsumption in 2017

Exhibit 21: We see iron ore prices fallingto $55/t by end-2017

Downgrading gold price forecasts near term, longer term reiterate $1,250/oz

Source: Goldman Sachs Global InvestmentResearch

Source: Goldman Sachs Global InvestmentResearch

Before the US presidential election, many market participants, held the view that a

win by Mr. Trump would come as a large shock to 'policy uncertainty', resulting in risk

markets selling off and gold rallying. While 'risk off' was the initial reaction on election

night, with gold rallying to c.$1,335/oz, this all changed during his early morning

acceptance speech when he focused almost solely on his infrastructure spending

policy initiative. A rally in risk, rise in US long dated real interest rates (Exhibit 22), and

sell-off in gold continued from that point on - gold is now trading c.$130/oz (-c.10%)

below its election night peak, in the $1,205-$1,210/oz range.

Given we believe that Mr. Trump will pursue a pro-growth agenda, supporting a pick-

up in growth that was already underway, we are downgrading our near term 3 and 6-

mo gold price forecasts to $1,200/oz, from $1,280/oz (vs. spot $1,208/oz) (N.B. our

2017 forecast is now $1213/oz from $1261/oz previously). While gold has already sold

off sharply and real rates have risen substantially to reflect this thinking, we see the

very near-term price risks as skewed to the downside, owing primarily to our concerns

about the potential for physical ETF liquidation. Specifically, we estimate that the vast

bulk of this year’s ETF build is losing money at current prices (Exhibit 23) and that if

half of this was unwound this would result in a c.$60/oz sell-off in the gold price.

Having said this, our base case medium to longer-term outlook towards gold is

relatively agnostic since the outlook depends greatly on how the Fed responds to

potential US stimulus and inflation as the economy reaches full employment. Were

the Fed to be relatively dovish, this would see real rates remain low and be bullish for

gold, while the opposite would be true if the Fed raised rates more quickly.

Specifically, our economists expect US real rates to be broadly flat from current levels

over the next 12 months. At the same time, a number of other factors are likely to be

supportive for gold, at the margin, over the medium to long term. Valuation levels for

This past year was likely the mid-cycle pause, but patience is still required

supportive for gold, at the margin, over the medium to long term. Valuation levels for

alternative asset classes such as equities and bonds remain highly elevated by

historical standards, mine supply growth is likely to be weak over the next 12-24

months, and China's RMB is set to depreciate further, to 7.3 by year-end 2017 on our

FX team's forecast, potentially supporting gold ETF purchases (especially in the

context of a slowing growth in Chinese property prices). Overall, these considerations

result in us leaving our 12-mo and 2018 price forecasts of $1,250/oz unchanged.

Exhibit 22: Risk rallied after the USpresidential election

Source: Bloomberg

Exhibit 23: We estimate that the vastbulk of this year’s ETF build is losingmoney at current prices

Source: Bloomberg, Goldman Sachs GlobalInvestment Research

Despite the spring rally in commodity prices this past year, commodity returns have

been mostly flat in 2016, up 1.4% year to date. This suggests that despite the recent

cyclical improvement in macroeconomic data, investors have not missed the

opportunity to get long the reflation trade in commodities. However, we would

caution that although we currently have a significant number of signals that markets

are entering the third phase of the business cycle (above trend and growing) where

commodities perform the best relative to other asset classes, given the low economic

volatility we have experienced since the global financial crisis, we would remain

cautious. We have learned over the past eight years that markets have been slow to

react and that this reflation trade could take a while to play out. But most importantly,

Price action, Volatility and Forecasts

react and that this reflation trade could take a while to play out. But most importantly,

we view the risk reward today as now supporting a long position in commodities and

hence feel comfortable going overweight the asset class.

S&P GSCI® Enhanced Commodity Index and strategies’ total return and forecasts

Source: Goldman Sachs Global Investment Research

Performance of S&P GSCI® Enhanced Commodity Index and Strategies through Nov 18, 2016

Source: Goldman Sachs Global Investment Research

Price action, volatility and GS forecasts

Commodities in a Nutshell

Energy

Source: Goldman Sachs Global Investment Research

Crude Oil – 12m target $50/bbl

Oil fundamentals have weakened sharply since OPEC announced a tentative

agreement to cut production and we now expect a large surplus of 0.7 mb/d in 1Q17

in the absence of such a cut. Importantly though, data over the past two months leave

us more confident that the global oil market will shift into deficit by 2H17 even with

OPEC production above current levels, on the combination of stronger expected

demand growth and lower production from high-cost countries in decline.

With greater certainty that deficits will finally materialize, there is now a stronger

economic incentive for OPEC producers to prevent a further rise in inventories in

1H17 and instead act to normalize the current high level of inventories through a

short-duration production cut. In our view, the goal of normalizing inventories should,

however, not target elevated oil prices as the flattening of the oil cost curve and the

unprecedented velocity of the shale supply response would make such an endeavor

rapidly self-defeating above $55/bbl. Our base case is now that an OPEC production

cut will be announced and implemented and normalizing inventory levels will generate

backwardation by 2Q17. Political risks can still derail an otherwise economically sound

decision and we believe an outcome where OPEC does not agree to a cut is near-term

bearish – even from current price levels – as it implies greater sequential production

from the group in competition for revenues and market share.

RBOB Gasoline – 12m target $1.43/gal

Atlantic basin inventories have been drawing this year aided by strong growth in

global gasoline demand and higher than expected exports to Latin America – in

particular Mexico – due to persistent refinery issues in that region. Going forward, we

particular Mexico – due to persistent refinery issues in that region. Going forward, we

expect continued robust demand growth given our economists' forecast for strong

consumption expenditures growth. Furthermore, the current backwardation in

forward margins will incentivize too few runs to meet demand. As a result, we require

cracks to strengthen to lift margins to incentivize incremental refinery utilization. Given

our price outlook for crude oil and the requirement for margins to rise to incentivize

refinery runs, we expect summer 2017 gasoline cracks to average $20/bbl vs.

$15.50/bbl as the forward curve indicates. With our outlook for crude spreads to go

into backwardation by 2Q17 and with backwardated margins incentivizing too little

runs, we expect RBOB spreads to go into backwardation as barrels come out of

storage to meet short-term demand.

Heating Oil – 12m target $1.60/gal

Atlantic basin distillate stocks have remained high this year primarily because of weak

global demand, itself driven by the succession of a warm 1Q16 and lackluster global

industrial production. Going forward, however, an improved outlook for industrial

activity, higher commodity prices and the credit stimulus from China should drive

diesel demand higher next year. We see two upside risks to our forecasts: first, higher

metal and coal prices could support mining output with each 1% increase in global

mining activity raising diesel demand by 70 kb/d. Second, any incremental US

infrastructure spending beyond our US economists' base case of $50 bn would

increase US diesel demand, with our modeling pointing to a 10 kb/d demand increase

per $10 bn of infrastructure spending. Net, the current backwardation in forward

margins is incentivizing too few runs to meet improving demand. As a result, we

require cracks to strengthen to lift margins to incentivize incremental refinery

utilization. However, given higher starting inventory levels, we expect most of the

work to be done by gasoline with stronger than average RBOB-Heating oil differentials

keeping distillate cracks modestly higher than the current market. Given our outlook

for crude oil and the requirement for margins to increase to incentivize refinery runs to

meet demand, we expect 2017 cracks to average $1.50 / bbl higher than the forward

curve indicates.

Natural Gas – 12m target $3.00/mmBtu

Our expectation heading into 2017 was that low cost natural gas production growth

would be curtailed by a lack of new offtake capacity in Appalachia and low oil drilling

activity for associated gas. Mild temperatures so far this fall, record high gas

Industrial Metals

activity for associated gas. Mild temperatures so far this fall, record high gas

inventories and forecasts for continued above normal temperatures as a result pose

downside risk to our $3.30/mmBtu 3-mo forecast which was based on the need to

incentivize legacy shale gas drilling early next year. However, with four months of

winter weather still to play out, strong coal to gas switching on weaker gas and higher

coal prices and strong gas demand from exports (Mexico, LNG), we believe risks to

our 6-mo $3.00/mmBtu price forecasts are skewed to the upside, especially if

Northeast pipelines scheduled to come online in late 2017 get further delayed.

LNG – 12m forecast US$4.50/mmBtu

Power generation fuels have enjoyed a strong rally in the run-up to peak winter

demand. Although lower availability of nuclear plants and reduced hydro levels are

supporting conventional power generation in Europe and Asia, we believe that

Chinese policies to support domestic coal prices have created additional headroom for

the LNG market and are partly responsible for a rise to US$7.15/mmBtu in the JKM

index, up 30% in three months. We believe that further price upside is limited in the

short term because spot LNG is now close to parity with many oil-indexed contracts

that provide buyers with the option to increase deliveries. Moreover, the restart of US

exports following maintenance at Sabine Pass and the commissioning of new

liquefaction capacity in Australia and Malaysia should bring the global gas market

closer to surplus at a time when global coal prices are set for a sharp correction on the

back of rising Chinese coal output. The expansion of LNG capacity has another four

years to run and competition between fuels is therefore likely to intensify in 2017 –

particularly when hydro levels normalize in China and Scandinavia. We expect the

price premium of LNG over coal to shrink further in order to incentivize incremental

fuel switching, and spot prices should gradually converge towards the marginal cost

of supply set by Henry Hub.

Copper – 12m target $4,800/t

Copper prices have rallied sharply and net speculative positioning has reached its

highest level since 2005 over the past two months. We believe that while part of the

rally has been warranted, prices have rallied too much too soon, and we expect

copper will decline to c.$5,000/t on a 3-mo view. The market is, in our view,

positioned for a major acceleration in Chinese and/or global metals demand growth,

with our modelling estimates suggesting that the copper market is pricing a near-

tripling in global copper demand growth to c.6% in 2017. By contrast, we expect

Chinese copper demand growth will slow in the near term on Chinese property policy

tightening, and that Mr. Trump's stimulus is unlikely to impact metals demand directly

until it kicks in later in 2H17 or early 2018. Further, we are entering the seasonally

weak period for copper demand (1Q), during which period inventories normally build

to the tune of c.400kt even in a balanced market (and our base case is for a small-

moderate surplus market during 2017). For further details please see the following link

(https://research.gs.com/content/research/en/reports/2016/11/15/8d950326-3f0a-

4552-8cfa-035de2ccfad8.html).

Nickel – 12m target US$11,000/t

We continue to anticipate an announcement of large-scale Filipino mine suspensions

and resulting ore stocks drawdowns to low levels. We now expect this will drive

nickel prices up to c.$12,500/t over the next three months, relative to current pricing

of c.$10,800/t. The potential for nickel prices to rise more than our base case 3-mo

target of $12,500/t is high in our view, with upside in the bull case of larger and/or

more permanent than expected Philippines mine suspensions potentially driving

prices up to $15-16,000/t. The main downside risk is a substantial decline in Chinese

steel and coking coal prices, which could weigh on sentiment in the ferrous sector as

well as reduce costs of production. For further details please see the following link

(https://research.gs.com/content/research/en/reports/2016/11/15/8d950326-3f0a-

4552-8cfa-035de2ccfad8.html).

Aluminium – 12m target US$1,600/t

We continue to see the market in small deficit in 2016 and rebalancing in 2017. While

we do not forecast a surplus market in aluminium in 2017, we are modestly bearish

on prices taking a 3-12 month view, based on our forecast for Chinese production

cost deflation (our economists forecast the RMB to depreciate to 7.3 by year-end

2017) and on our view that thermal coal prices will decline from current levels.

Therefore, even if current margins in China were sustained, prices would likely

decline. Further, LME aluminium speculative positioning is at very high levels. For

further details please see the following link

(https://research.gs.com/content/research/en/reports/2016/11/15/8d950326-3f0a-

4552-8cfa-035de2ccfad8.html).

Zinc – 12m target US$2,800/t

Agriculture

Bulks

Zinc – 12m target US$2,800/t

We remain bullish on the outlook for cash zinc prices through 2017. We see zinc

rising to $2,800/t on a 12-mo view based on our forecast of a 500kt refined deficit for

2017, and our modelling of the inventory path on cash-5-year time spreads, and we

see the risks surrounding our 2017 zinc prices forecasts as skewed to the upside.

While net speculative length in zinc is significant, we believe it will be maintained

given our view that the forward fundamental will become incrementally bullish. The

mine supply tightness theme continues to play out on the back of price related supply

closures (Glencore and Chinese mines) and non-price related depletions (Century and

Lisheen mines) substantially tightening the market, and likely resulting in smelter

closures over the next three months. Environmental restrictions appear to be affecting

the ability of Chinese mines to respond to what are record high domestic mine prices.

Meanwhile, long dated (5 year forward) zinc prices are trading near their all-time

highs, which could be attractive from a producer hedging perspective. For further

details please see the following link

(https://research.gs.com/content/research/en/reports/2016/11/15/8d950326-3f0a-

4552-8cfa-035de2ccfad8.html).

Corn – 12m target $3.35/bu

Soybean – 12m target $8.85/bu

Despite concerns late last spring that La Nina weather conditions would weigh on

growing conditions, the US 2016/17 harvest ended up record large for both corn and

soybeans. Further, with only weak La Nina weather conditions currently, the

beginning of the South American growing season is so far taking place under

favorable conditions. As a result, we expect that under normal weather conditions

going forward corn and soybeans prices will decline back to their marginal costs of

production over the coming year to limit further inventory builds, with our 12-mo

forecast for both crops below the forward curve. Continued strong soybean demand

from China leaves us, however, forecasting that soybeans prices will continue to trade

at a historically elevated premium over corn prices to continue to incentivize acreage

allocation.

Iron Ore – 12m target $55/t

A combination of stronger Chinese steel demand, which was in turn driven by the

large credit injection earlier in the year, and lower-than-expected supply resulted in an

upward trend in iron ore prices in 2016. But demand and supply fundamentals cannot

explain all of the price run-up. Other factors such as surging coal and steel prices,

continued RMB depreciation, and optimism over President-elect Trump’s

infrastructure spending plan have also played a role. At $73/t, we think iron ore has

overshot its fair value implied by the supply and demand balance. For 2017, we see

the demand picture as supportive. Although there are downside risks in the Chinese

property market, steel demand should remain solid given the strong growth in

infrastructure investment. Outside of China, a cyclical recovery in investment globally

could also be supportive. However, we expect iron ore prices to fall over the next

several quarters for two reasons. First, a correction of the overvaluation mentioned

earlier should result in iron ore prices reverting towards marginal cost in the near

term. Second, as we look beyond 2017, a widening gap between stable to declining

demand and increasing mining capacity should drive inventories towards a historical

high and eventually force prices below marginal cost. At the same time, we expect

this downward trend to be anything but smooth, partly because a forward curve in

backwardation and a linkage to the USD has attracted speculative investors, and high

price volatility is likely to persist in 2017.

Metallurgical Coal – 12m target US$165/t FOB Australia

The steel sector has not been as fortunate as power utilities regarding its fuel supply.

Inventories remain low along the supply chain, and metallurgical coal production ex-

China is unlikely to fully offset the shortfall in the domestic market, partly because of a

lack of investment in the past five years and the risks associated with the financing of

mine restarts in a market with significant policy risk. We assume that inventories

continue to decline into the first quarter of 2017 due to the delayed response of

domestic mines and the focus of regulators on thermal coal supply. Healthy demand

and limited spot availability could drive prices for hard coking coal as high as

US$350/t in early 2017 before the eventual increase in Chinese coal production

reverses the significant de-stocking experienced this year. While our 2018 forecast of

US$125/t reflects normalized inventories and price parity with marginal cost in China,

production controls are a blunt policy instrument and the search for price stability in

the Chinese market may require successive tightening and loosening phases, causing

prices to over/undershoot repeatedly relative to the equilibrium price.

Thermal Coal – 12m forecast US$60/t FOB Newcastle

The market seems to have reached an inflection point: the global economy is not

short of mining capacity and the current windfall for producers was bound to be

short-lived. Chinese regulators have rolled back production limits in order to ensure

winter power and heating supply, and they have also provided clear guidance about

their price targets for 2017 via annual contracts signed recently by state-owned

producers at RMB 535/t. As inventories at Chinese power plants recover and a larger

number of domestic mines increase their operating hours, global coal prices have

declined across the curve and we believe that risks to Chinese demand for imported

coal in 2017 are skewed to the downside. Tightness in winter should therefore be

followed by sequentially stronger supply and weaker demand going into the

seasonally weaker second quarter of 2017, particularly given the growing competition

from LNG in both developed and emerging economies. Nonetheless, we believe that

Chinese policy will have a lasting impact on industry profitability because marginal

costs are higher in China than in other coal producing regions. However, policy risks

are significant. Potential measures to prioritize domestic coal at the expense of

imports would be likely to result in a price discount for seaborne coal relative to our

US$60/t estimate of the equilibrium price in an unconstrained market.

Investors should consider this report as only a single factor in making their investment

decision. For Reg AC certification and other important disclosures, see the Disclosure

Appendix, or go to www.gs.com/research/hedge.html

(http://www.gs.com/research/hedge.html).

Jeffrey Currie (/content/research/authors/f50f0e46-c1ae-11d5-8ba1-d5767450fa6b.html)+1 212 [email protected], Sachs & Co.

Damien Courvalin (/content/research/authors/9d1a3402-804b-11db-91b4-001185134607.html)+1 212 [email protected], Sachs & Co.

Michael Hinds (/content/research/authors/ea262e0a-b044-4ad5-8c29-ef70cdd73c3f.html)+1 212 357-7528

+1 212 [email protected], Sachs & Co.

Max Layton (/content/research/authors/3da678f2-0e7e-11e1-a4e6-00215acdb578.html)+44 20 [email protected] Sachs International

Christian Lelong (/content/research/authors/b487e668-41be-11e1-b4f9-00215acdb578.html)+1 212 [email protected], Sachs & Co.

Abhisek Banerjee (/content/research/authors/df20af82-d62a-4c68-a2ce-65e2cdb833b1.html)+44 20 [email protected] Sachs International

Hui Shan (/content/research/authors/5cc0436e-2740-11e1-8489-00215acdb578.html)+1 212 [email protected], Sachs & Co.

Yubin Fu (/content/research/authors/0a793db5-cfcd-42b8-8f0b-86c77b68902c.html)+44 20 [email protected] Sachs International

Amber Cai (/content/research/authors/e29f0d44-06c1-46da-8163-dd25a952930b.html)+852 [email protected] Sachs (Asia) L.L.C.

Chris Mischaikow (/content/research/authors/66db0b2c-6fab-4264-9ccf-8a5870914b8e.html)+1 212 [email protected], Sachs & Co.

Mikhail Sprogis (/content/research/authors/4b8fb3ca-789b-4f75-a8c7-96dde4b4b326.html)+44 20 [email protected] Sachs International

Huan Wei (/content/research/authors/c7efca6b-02e0-4409-8289-280b0d652039.html)+1 212 [email protected], Sachs & Co.

Callum Bruce (/content/research/authors/68097359-7334-493b-a4cb-d143ddad581e.html)+44 20 [email protected]