Embed Size (px)

Citation preview

What is New Hampshire? An overview of issues shaping the Granite State’s future

September 2015

If you found this report useful, consider supporting the Center today.

Any contribution works to help keep these reports coming! The Center’s continued independent and objective voice is only possible because of the

generosity of donors like you.

Authors Stephen Norton Executive Director Dennis Delay Economist Tyler Stoff Intern

About this paper The New Hampshire Center for Public Policy Studies compiled the information and analysis in this report for the use of Leadership New Hampshire, a program intended to introduce rising leaders to the people, strengths, and challenges of the Granite State. The Center is grateful for the opportunity to present this material to the Leadership New Hampshire participants and to all others seeking an overview of information about the state. The Center has produced this report with funds donated by individuals, foundations, and businesses from across New Hampshire. The Center’s supporters do not necessarily endorse, nor has the Center asked them to endorse, any of the materials included in this report. The Center, not Leadership New Hampshire, determined what to include in this report. This paper, like all of our published work, is in the public domain and may be reproduced without permission. Indeed, the Center welcomes individuals’ and groups’ efforts to expand the paper’s circulation. Copies are available at no charge on the Center’s web site: www.nhpolicy.org. Many of the pages that follow are excerpts from other Center reports, all of which are available at the same site. We have also prepared a selection of interactive maps and data sets that display much of the information detailed in this report. Those can be found on our website as well. Contact the Center at [email protected]; or call 603-226-2500. Write to: NHCPPS, 1 Eagle Square, Suite 510, Concord, NH 03301

WHAT IS NEW HAMPSHIRE?

2015 Edition

Table of Contents

INTRODUCTION: WHAT IS NEW HAMPSHIRE? .............................................................................................. 1

DEMOGRAPHIC CHANGE IN NEW HAMPSHIRE ............................................................................................ 2

NEW HAMPSHIRE’S ECONOMY .......................................................................................................................... 7

EDUCATION IN NEW HAMPSHIRE ................................................................................................................... 19

HEALTH CARE IN NEW HAMPSHIRE .............................................................................................................. 32

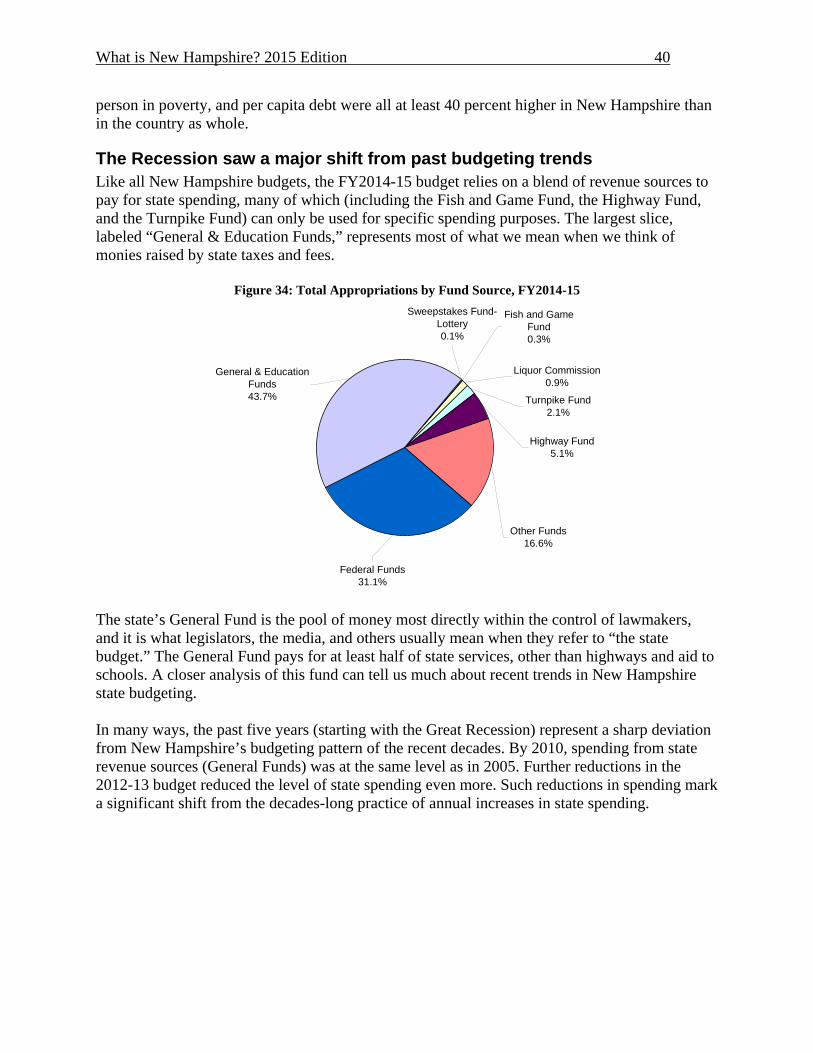

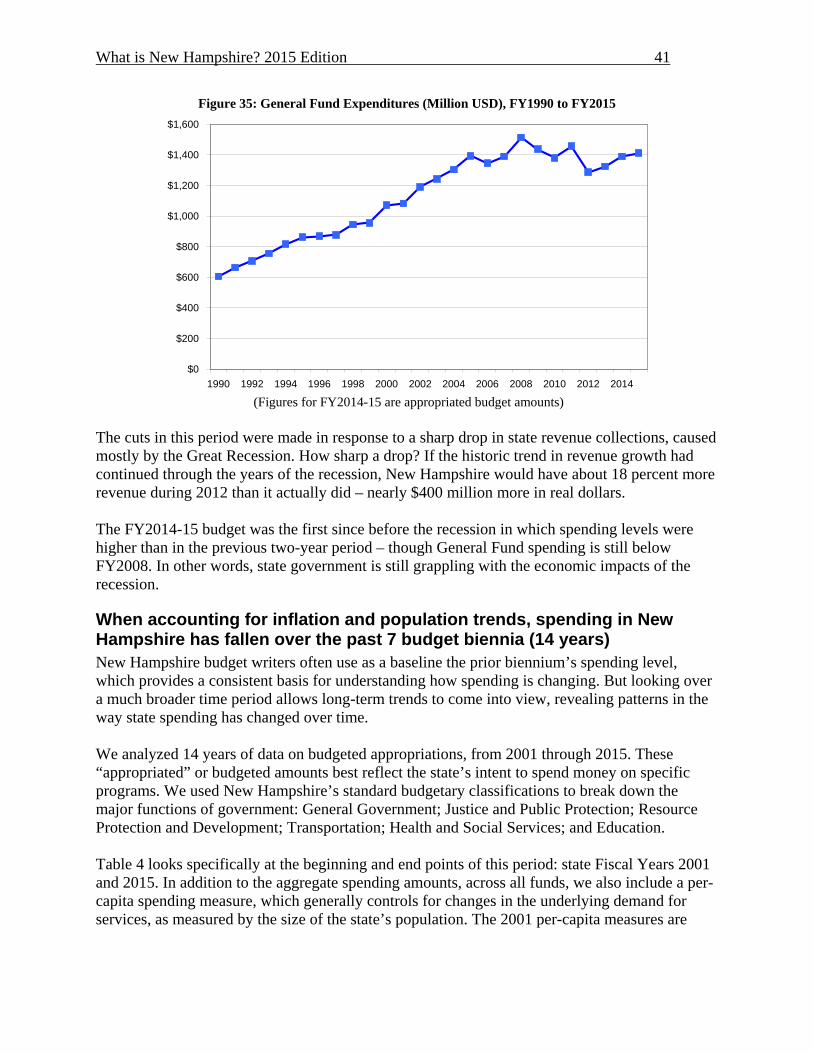

NEW HAMPSHIRE’S STATE BUDGET ............................................................................................................... 38

NEW HAMPSHIRE’S INFRASTRUCTURE ........................................................................................................ 48

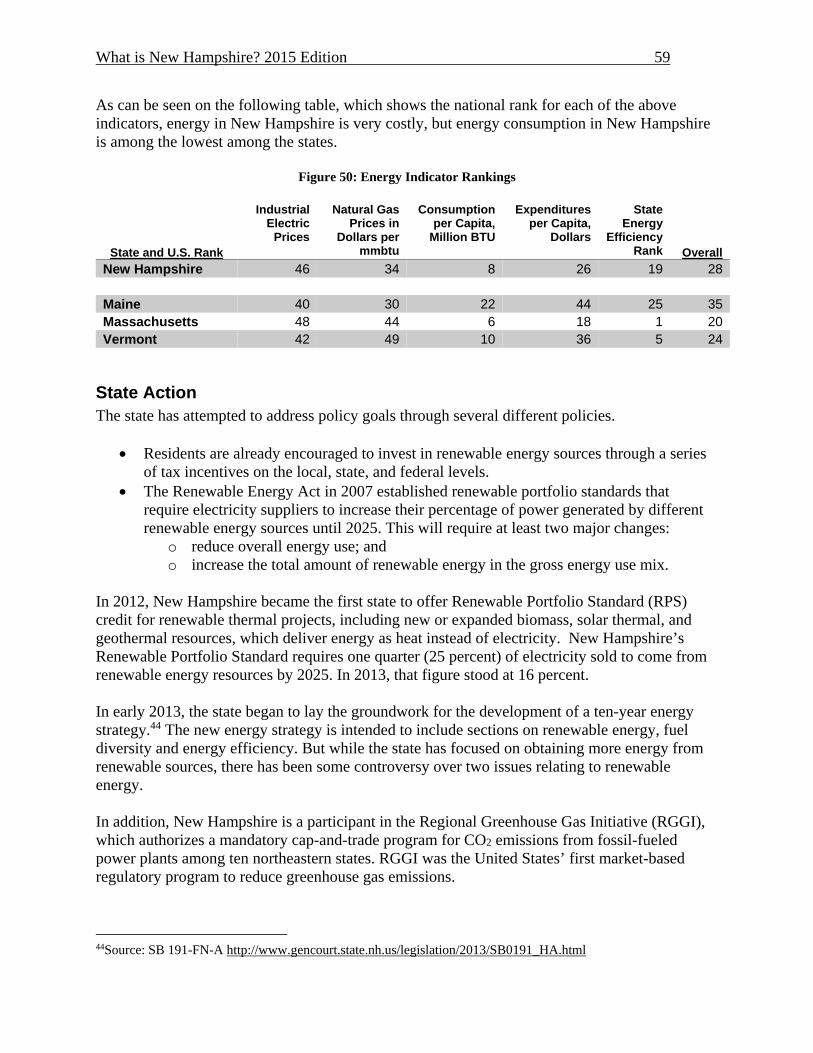

ENERGY IN NEW HAMPSHIRE ........................................................................................................................... 56

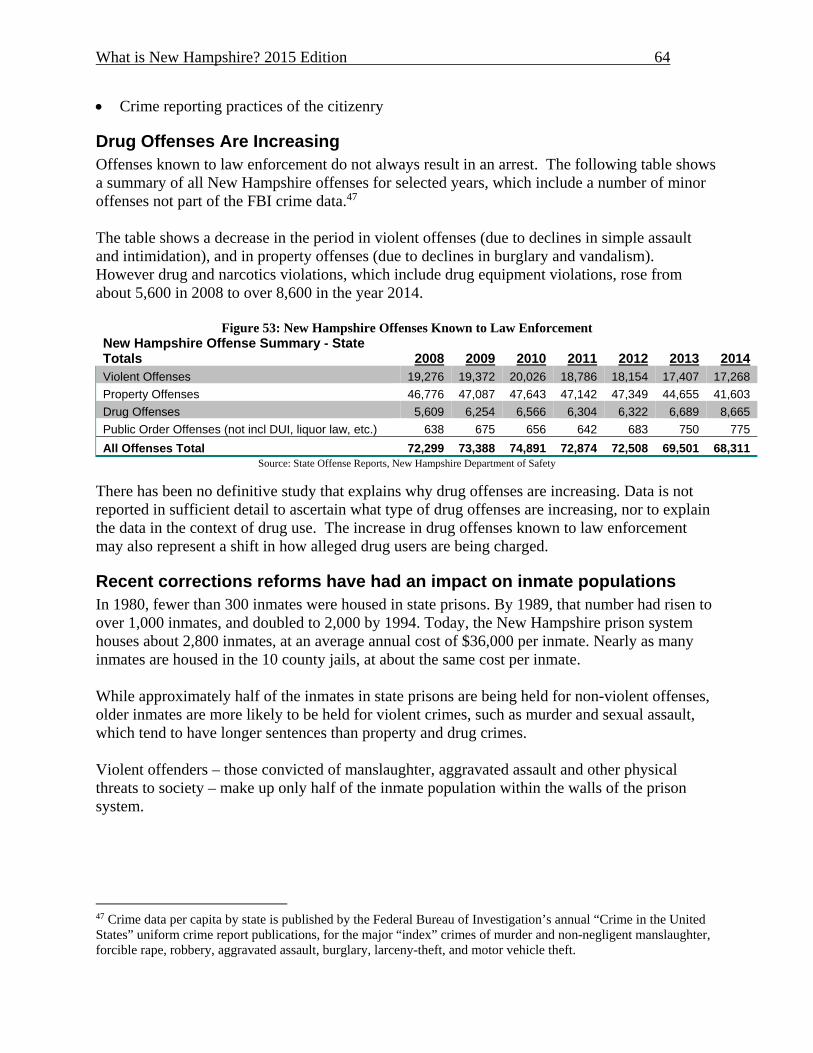

CRIME AND CORRECTIONS IN NEW HAMPSHIRE ...................................................................................... 62

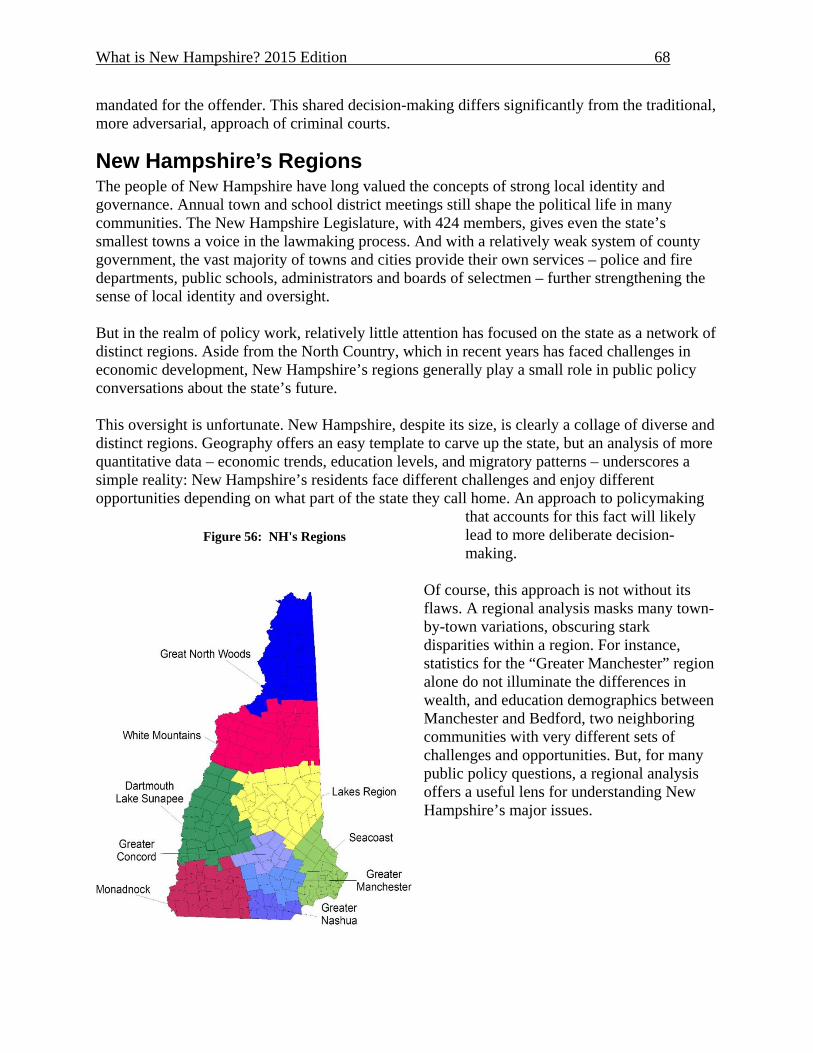

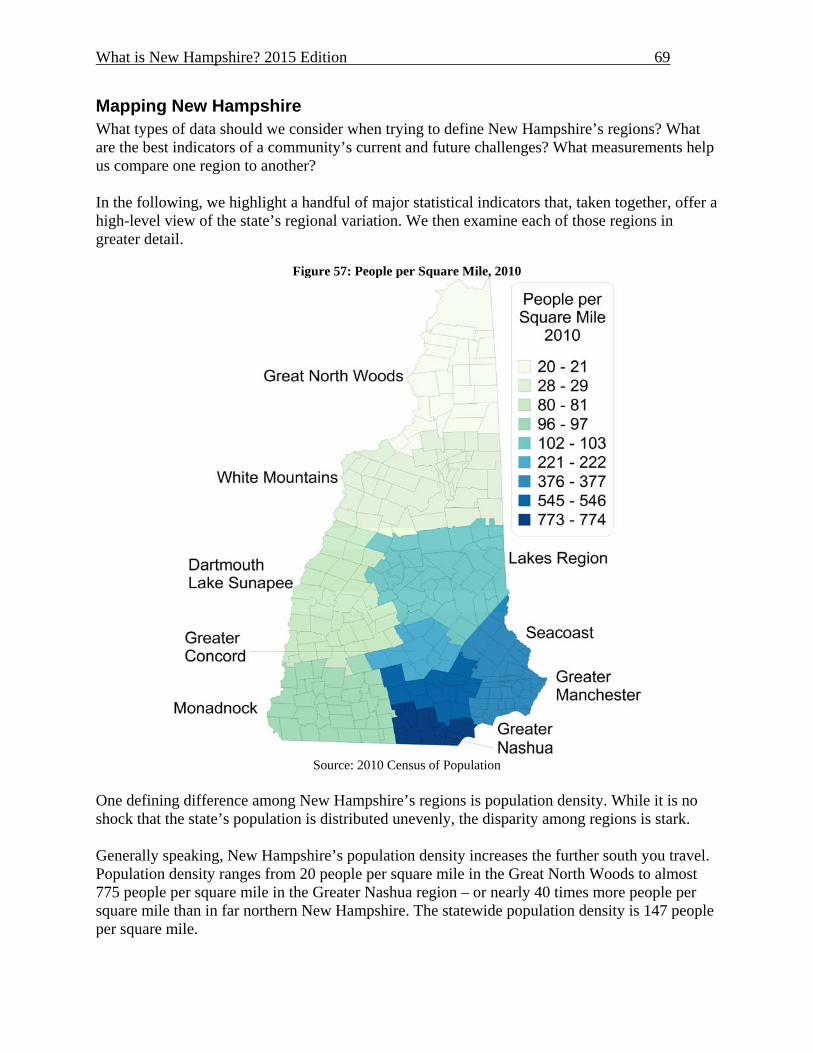

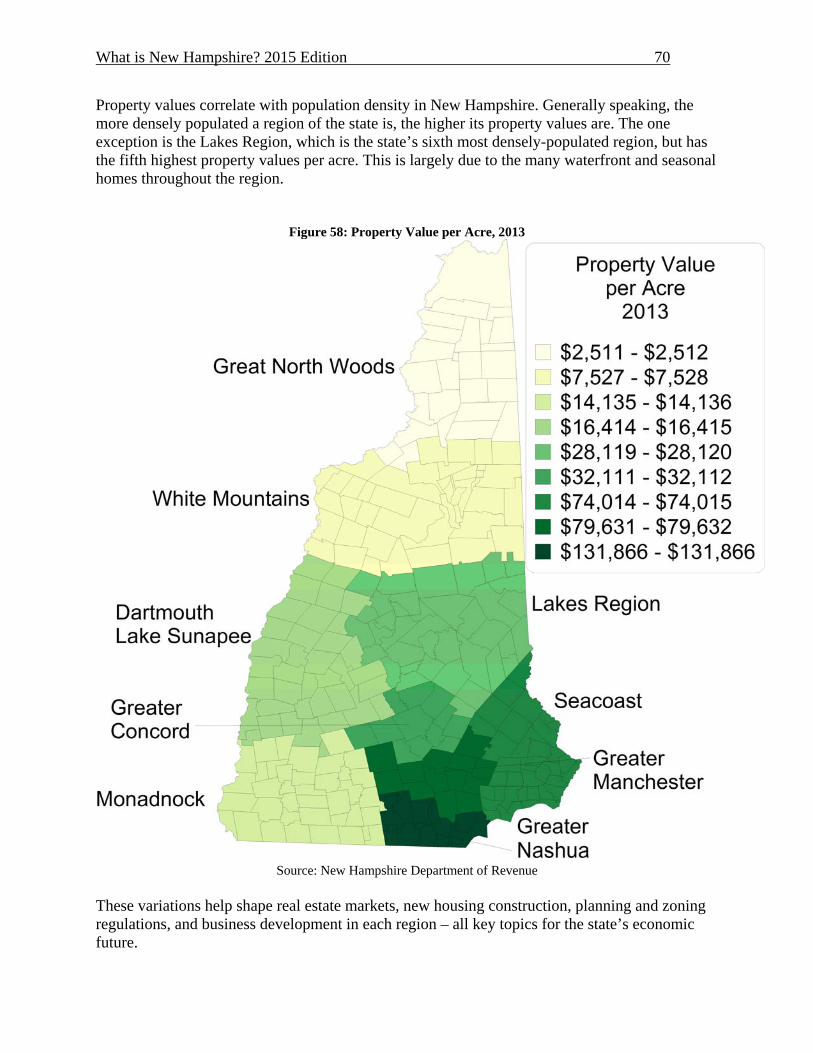

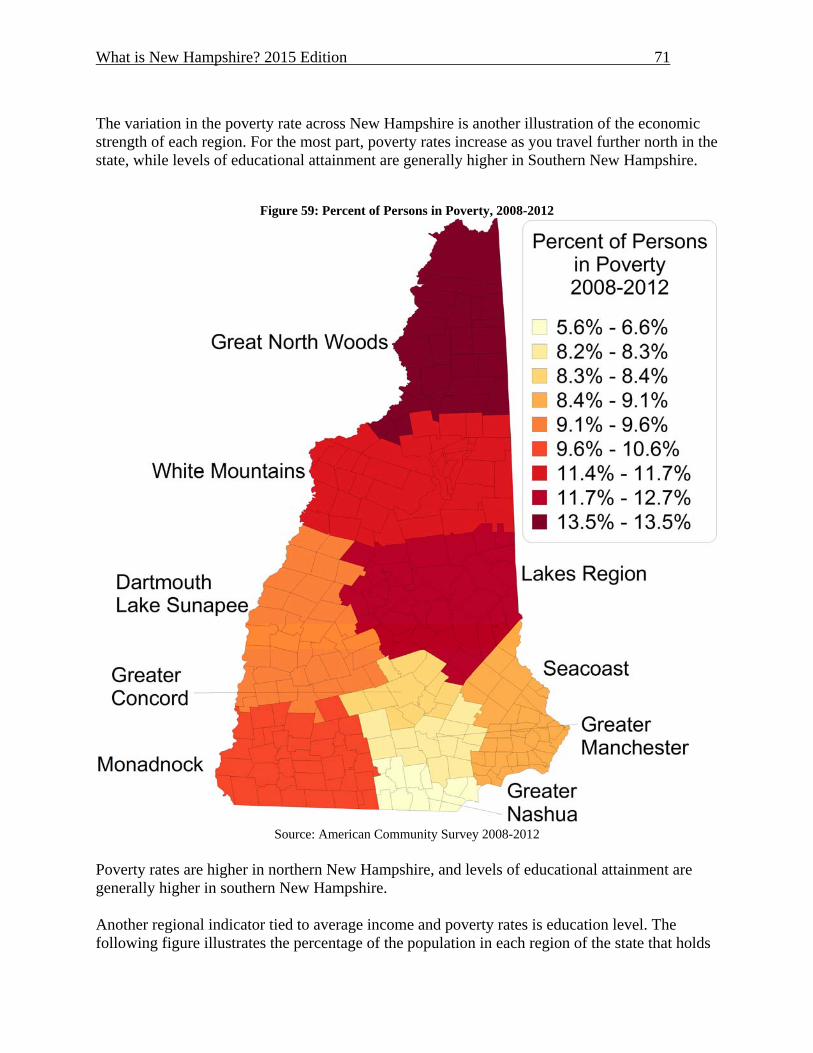

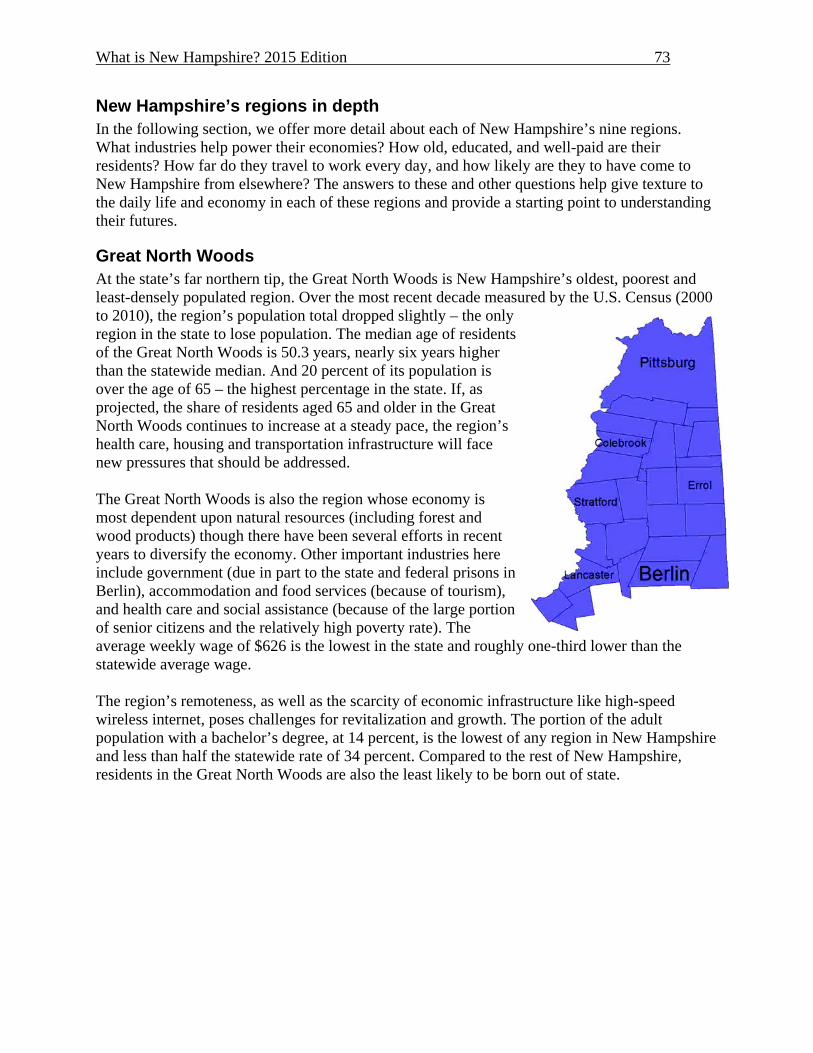

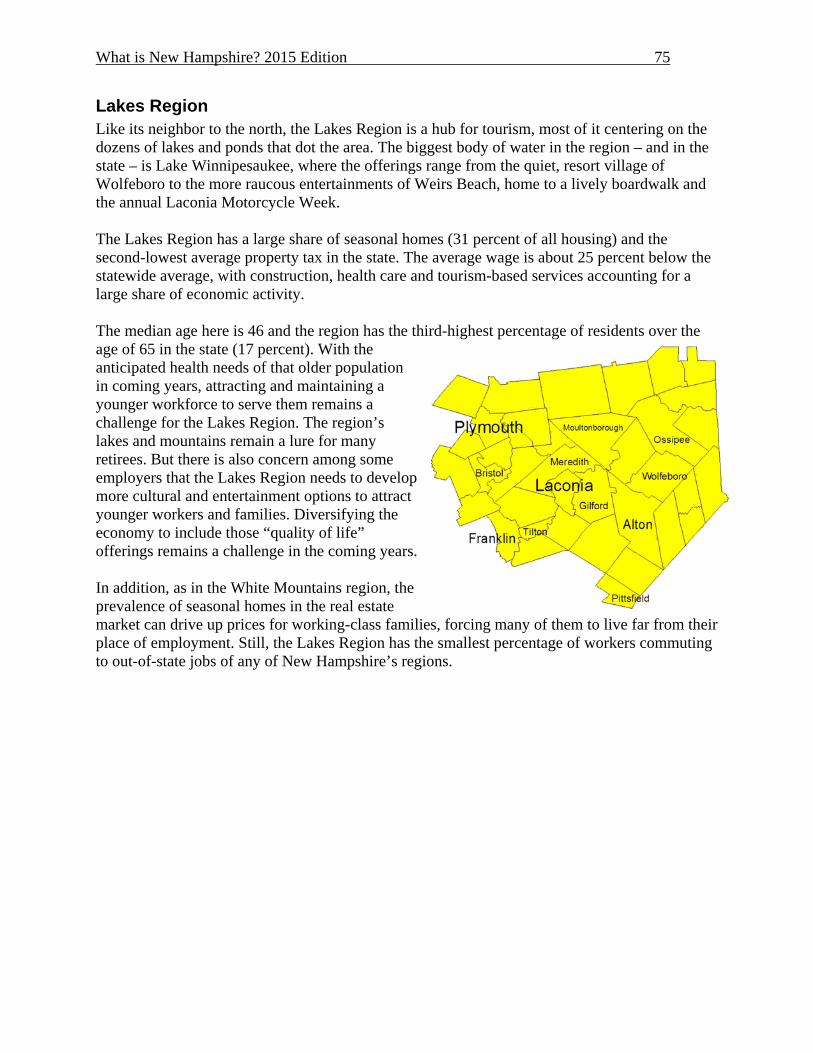

NEW HAMPSHIRE’S REGIONS ........................................................................................................................... 68

LIST OF TABLES Table 1: New Hampshire Employment and Wages by County Type, 2010 to 2013 .................... 11 Table 2: New Hampshire Economic Dashboard 2013 .................................................................. 16 Table 3: Administrative Costs for New Hampshire Districts by Enrollment ............................... 29 Table 4: Total state spending, 2001 and 2015 .............................................................................. 42 Table 5: General Fund Spending, 2001 and 2015 ......................................................................... 42 Table 6: 2023 New Hampshire Tax Revenue by Type ................................................................. 46 Table 7: Alternative - Deficit Assuming Historical Growth ......................................................... 47 Table 8: Infrastructure state indicators ......................................................................................... 49 Table 9: Estimated investment needs of water systems in selected states, including New Hampshire, over the next two decades. ........................................................................................ 53

LIST OF FIGURES Figure 1: Ten Year Percent Change in New Hampshire Population by Decade End ..................... 3 Figure 2: Net Migration in New Hampshire ................................................................................... 4 Figure 3: New Hampshire Population Age 65 and Over ................................................................ 4 Figure 4: Children in Poverty Growing ......................................................................................... 5 Figure 5: Average Annual Growth in Employment, 1970 to 2014 ................................................. 7 Figure 6: Change in New Hampshire Jobs from 2011 to 2013 by Average Wage ......................... 8 Figure 7: National, Regional, and State Unemployment Rates, 2005-2015 ................................... 8 Figure 8: United States and New Hampshire Real GDP Growth by Decade ................................. 9 Figure 9: Percent Change in Real GDP in BEA Regions ............................................................. 10 Figure 10: Percent Change of Labor Force in Regional Labor Market Areas, 2010 to 2014 ....... 10 Figure 11: Change in Employment by County Type, 2010 to 2013 ............................................. 11 Figure 12: Percent Change of Labor Force in National, Regional, and State Labor Markets, 2010 to 2014 .......................................................................................................................................... 12 Figure 13: New Hampshire Total Compensation Paid by Selected Industries (Thousands of Dollars) ......................................................................................................................................... 13 Figure 14: Projections of a Declining Workforce, Growth by Age Cohort .................................. 14 Figure 15: Regional Price Parities by State, 2013 (US = 100) ..................................................... 17 Figure 16: Percent of Students Scoring Proficient or Higher on State Reading Tests ................. 20 Figure 17: Third Grade Reading Scores by School District, 2013 ............................................... 20 Figure 18: Percent of High School Graduates Entering Post-Secondary Education, Class of 2014....................................................................................................................................................... 21 Figure 19: New Hampshire School District Revenue by Category, 2013-14 ............................... 21 Figure 20: Per-Pupil Education Spending by State, 2013-14 ....................................................... 22 Figure 21: State Support for Higher Education by System, FY2005 to FY2015 ......................... 23 Figure 22: State Support for Higher Education per $1,000 in Personal Income, FY2015 ........... 24 Figure 23: Average In-State Tuition and Fees at Public Four-Year Institutions by State, 2014-2015............................................................................................................................................... 24 Figure 24: Average Undergraduate Debt Load for In-State Students by Institution, 2007-2012 . 25 Figure 25: Three-Year Official Cohort Default Rates for New Hampshire Institutions .............. 26 Figure 26: New Hampshire Public Grade School Enrollment ...................................................... 27 Figure 27: Percent of Population Employed in Science and Engineering Fields, 2010 ............... 30 Figure 28: Growth in Medicaid Enrollment Associated with the Health Protection Act ............. 33

Figure 29: Share of New Hampshire GDP: Energy, Health Care, and the State Budget ........... 34 Figure 30: Annual Growth in Health Insurance Premiums .......................................................... 35 Figure 31: Average Family Health Insurance as a ........................................................................ 35 Figure 32: Per Capital Public Spending in 2013 .......................................................................... 38 Figure 33: Per Capita Spending in NH ........................................................................................ 39 Figure 34: Total Appropriations by Fund Source, FY2014-15 ..................................................... 40 Figure 35: General Fund Expenditures (Million USD), FY1990 to FY2015 ............................... 41 Figure 36: General Fund Revenues by Major Component 1988 Through 2013 .......................... 43 Figure 37: FY2013 General Fund Revenue Sources .................................................................... 44 Figure 38: General Fund Revenue as a Percentage of Gross State Product ................................. 44 Figure 39: State Appropriations by Category, 2014-15 (all fund sources) ................................... 45 Figure 40: State Spending by Category, 1982 (all fund sources) ................................................. 46 Figure 41: Per Pupil Primary and Secondary School Infrastructure Outlay for FY2013 ............. 50 Figure 42: Percent of Population without Household Broadband Internet Access by Region, 2010....................................................................................................................................................... 51 Figure 43: Percent of Population with Broadband Household Internet Access by County, 2015 51 Figure 44: Total Water Use Per Capita in Gallons/Day by State, 2010 ....................................... 52 Figure 45: Percent of Deficient Bridges by State, 2014 ............................................................... 54 Figure 46: Percent of Roads in Poor or Mediocre Condition, 2013 ............................................. 55 Figure 47: New Hampshire's Energy Use by Sector, 2013 ........................................................... 56 Figure 48: New Hampshire's Energy Consumption by Fuel Type, 1960 to 2013 (Millions of BTU) ............................................................................................................................................. 57 Figure 49: Energy Indicators ........................................................................................................ 58 Figure 50: Energy Indicator Rankings .......................................................................................... 59 Figure 51: Crime Rates per Hundred Thousand People by State, 2013 ....................................... 62 Figure 52: All Crime Rate, Crimes per 100,000 People, FBI Uniform Crime Reports ................ 63 Figure 53: New Hampshire Offenses Known to Law Enforcement ............................................. 64 Figure 54: New Hampshire State Prison Population by Major Offense ....................................... 65 Figure 55: New Hampshire State Prison Inmate Population under Justice Reinvestment ........... 66 Figure 56: NH's Regions .............................................................................................................. 68 Figure 57: People per Square Mile, 2010 ..................................................................................... 69 Figure 58: Property Value per Acre, 2013 .................................................................................... 70 Figure 59: Percent of Persons in Poverty, 2008-2012 .................................................................. 71 Figure 60: Percent of Adult Population with a Bachelor's Degree or Higher, 2008-2012 ........... 72

What is New Hampshire? 2015 Edition 1

Introduction: What is New Hampshire? Throughout its history, New Hampshire has worn many identities: agricultural outpost on the edge of New England; bustling engine of the Industrial Revolution; oasis for nature-seeking tourists; haven for tax-fleeing transplants. In the early years of the 21st Century, New Hampshire is still evolving amid shifting economic, demographic, social and political forces. Among the trends shaping the “new” New Hampshire: an aging population; increasing racial and ethnic diversity; a shift away from the high-growth economic model of the past; and continued demand on the state budget for public services. While the implications of these and other changes are still unclear, they do raise critical policy questions, including:

Economy: New Hampshire suffered the effects of the Great Recession less severely than many other states, but slow job growth continues to gnaw at the state’s economy. As of the summer of 2014, New Hampshire lagged behind the nation and the rest of New England in recovering jobs lost during the recession. What is the state’s economic development plan, especially in relation to demographic trends that show New Hampshire’s working age population actually declining in coming years? What specific industries or regions of New Hampshire will help shape the state’s economy in coming years? What regional approaches to economic development will find greatest success?

Demographic change: While New Hampshire is consistently rated one of the best places

in the country to raise children, our population as a whole continues to age. Meanwhile, our school enrollment continues on a decade-long decline, and several measures of youth well-being in the state show worrisome trends, including rising levels of childhood poverty. What are the implications of these developments on education policy, housing, public services and transportation?

Health care: New Hampshire’s health policy landscape faces great uncertainty amid

recent reforms at the national level, as well as continued rises in cost and the continued aging of the state’s population. What impact will the shifting health marketplace have on New Hampshire’s economy and the well-being of its residents?

Long-term planning: State policymakers face a long list of critical issues in coming

years: public infrastructure investment, education finance, corrections spending, health care, and energy policy, among others. Many of these require a long-term perspective and an understanding of multi-year trends. How will the state – which has a two-year budget cycle and a two-year term for all major state offices – manage to plan decades into the future?

This report is our annual survey of the major policy issues and critical questions shaping our future. The data explain where New Hampshire has been, forecast where it is heading, and explore how current trends and policy choices facing the state will affect the well-being of its citizens.

What is New Hampshire? 2015 Edition 2

Demographic change in New Hampshire New Hampshire had been the fastest growing state in the Northeast for years, fueled by high rates of domestic in-migration, largely from Massachusetts. With the arrival of these newcomers, the average educational attainment and income levels in New Hampshire increased over that period. Those trends, in turn, helped fuel the state’s strong economic growth of recent decades. But these migration patterns have changed over the course of the Great Recession, a fact that will have real implications for New Hampshire’s future. As we will see below, migration into New Hampshire has slowed considerably over the past decade, and the state is not expected to return to the past pattern of high growth for the foreseeable future.

New Hampshire’s people: By the numbers1 Compared to the rest of the country, New Hampshire’s population is older, less racially diverse, better educated, wealthier, and more likely to have moved here from another state.

Average age: o New Hampshire: 41.5 years o United States: 37.3 years

Percent of the population that is white: o New Hampshire: 96 percent o United States: 76 percent

Percent of the population with a high school diploma or higher: o New Hampshire: 91 percent o United States: 86 percent

Percent of housing units that are owner-occupied: o New Hampshire: 72 percent o United States: 65 percent

Median household income: o New Hampshire: $64,900 o United States: $53,000

Poverty rate: o New Hampshire: 8.4 percent o United States: 14.9 percent

Percent of state residents born in another state: o New Hampshire: 51 percent o United States: 27 percent

New Hampshire’s high growth years are in the past Through the 1970s, 1980s and 1990s, New Hampshire saw high rates of population growth, with three consecutive decades of growth of 20 percent or more. That pace of growth came in the middle of a period of economic expansion and rising wages.

1 Source: 2010 Census of Population and the American Community Survey 2009-2013

What is New Hampshire? 2015 Edition 3

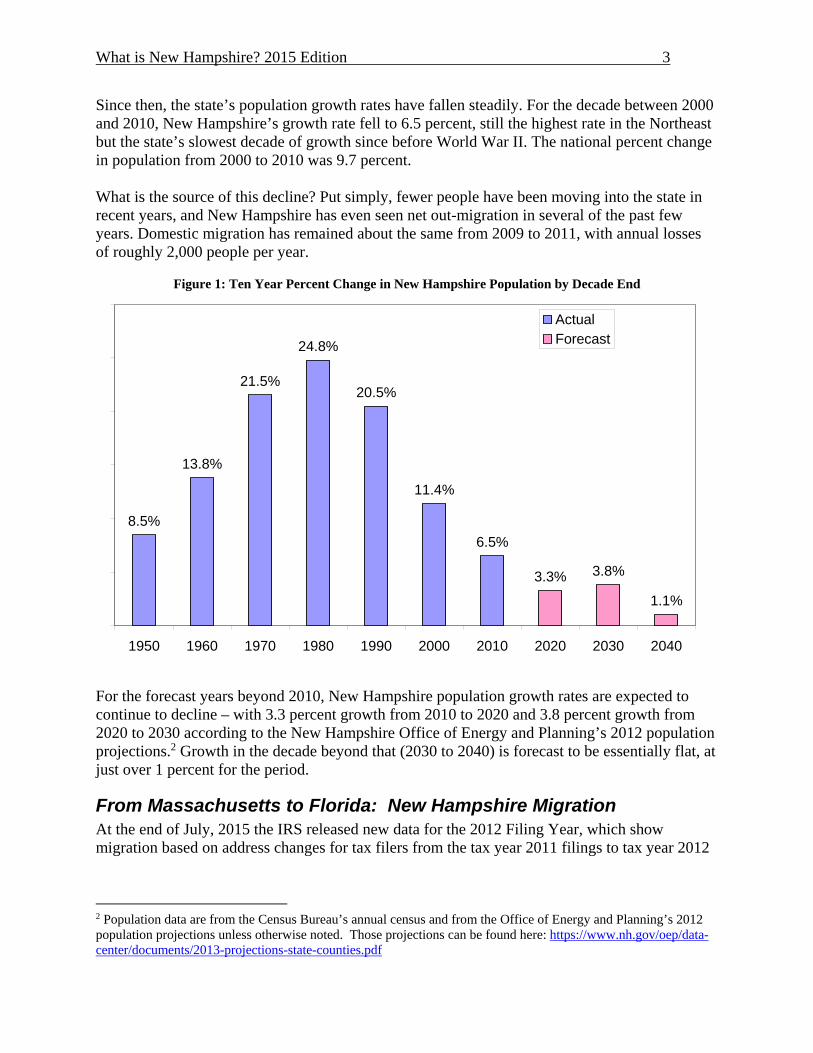

Since then, the state’s population growth rates have fallen steadily. For the decade between 2000 and 2010, New Hampshire’s growth rate fell to 6.5 percent, still the highest rate in the Northeast but the state’s slowest decade of growth since before World War II. The national percent change in population from 2000 to 2010 was 9.7 percent. What is the source of this decline? Put simply, fewer people have been moving into the state in recent years, and New Hampshire has even seen net out-migration in several of the past few years. Domestic migration has remained about the same from 2009 to 2011, with annual losses of roughly 2,000 people per year.

Figure 1: Ten Year Percent Change in New Hampshire Population by Decade End

For the forecast years beyond 2010, New Hampshire population growth rates are expected to continue to decline – with 3.3 percent growth from 2010 to 2020 and 3.8 percent growth from 2020 to 2030 according to the New Hampshire Office of Energy and Planning’s 2012 population projections.2 Growth in the decade beyond that (2030 to 2040) is forecast to be essentially flat, at just over 1 percent for the period.

From Massachusetts to Florida: New Hampshire Migration At the end of July, 2015 the IRS released new data for the 2012 Filing Year, which show migration based on address changes for tax filers from the tax year 2011 filings to tax year 2012

2 Population data are from the Census Bureau’s annual census and from the Office of Energy and Planning’s 2012 population projections unless otherwise noted. Those projections can be found here: https://www.nh.gov/oep/data-center/documents/2013-projections-state-counties.pdf

8.5%

13.8%

21.5%

24.8%

20.5%

11.4%

6.5%

3.3% 3.8%

1.1%

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040

ActualForecast

What is New Hampshire? 2015 Edition 4

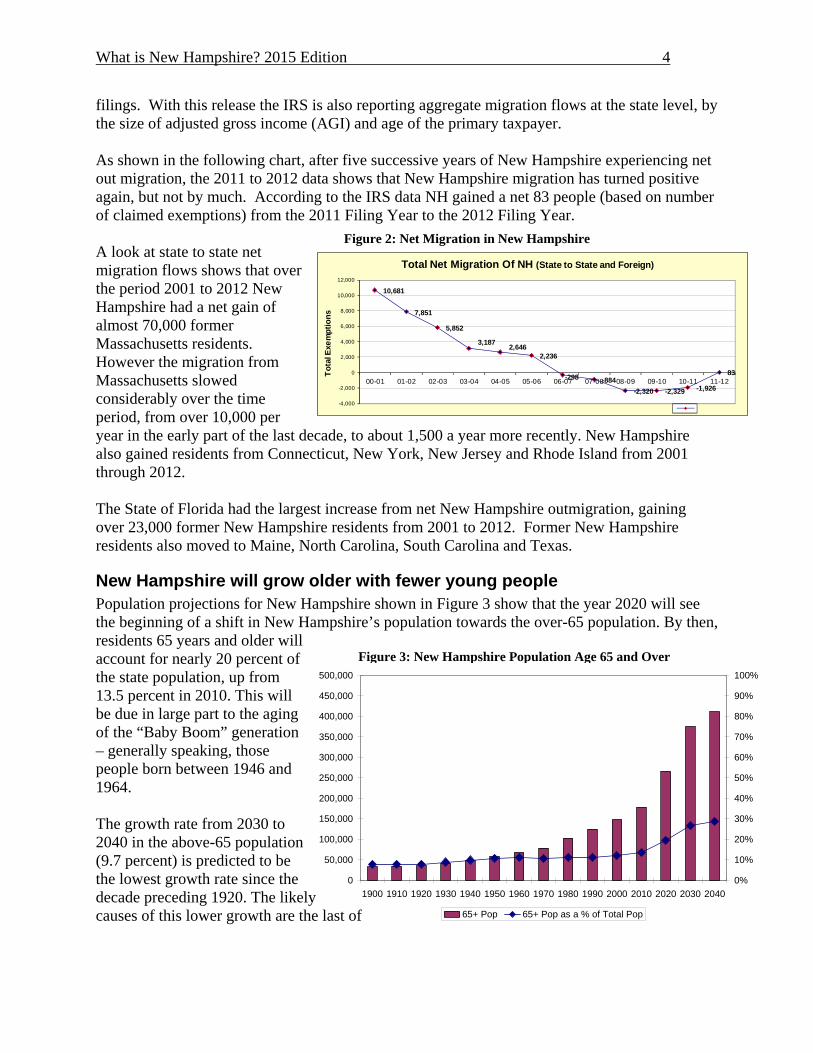

filings. With this release the IRS is also reporting aggregate migration flows at the state level, by the size of adjusted gross income (AGI) and age of the primary taxpayer. As shown in the following chart, after five successive years of New Hampshire experiencing net out migration, the 2011 to 2012 data shows that New Hampshire migration has turned positive again, but not by much. According to the IRS data NH gained a net 83 people (based on number of claimed exemptions) from the 2011 Filing Year to the 2012 Filing Year. A look at state to state net migration flows shows that over the period 2001 to 2012 New Hampshire had a net gain of almost 70,000 former Massachusetts residents. However the migration from Massachusetts slowed considerably over the time period, from over 10,000 per year in the early part of the last decade, to about 1,500 a year more recently. New Hampshire also gained residents from Connecticut, New York, New Jersey and Rhode Island from 2001 through 2012. The State of Florida had the largest increase from net New Hampshire outmigration, gaining over 23,000 former New Hampshire residents from 2001 to 2012. Former New Hampshire residents also moved to Maine, North Carolina, South Carolina and Texas.

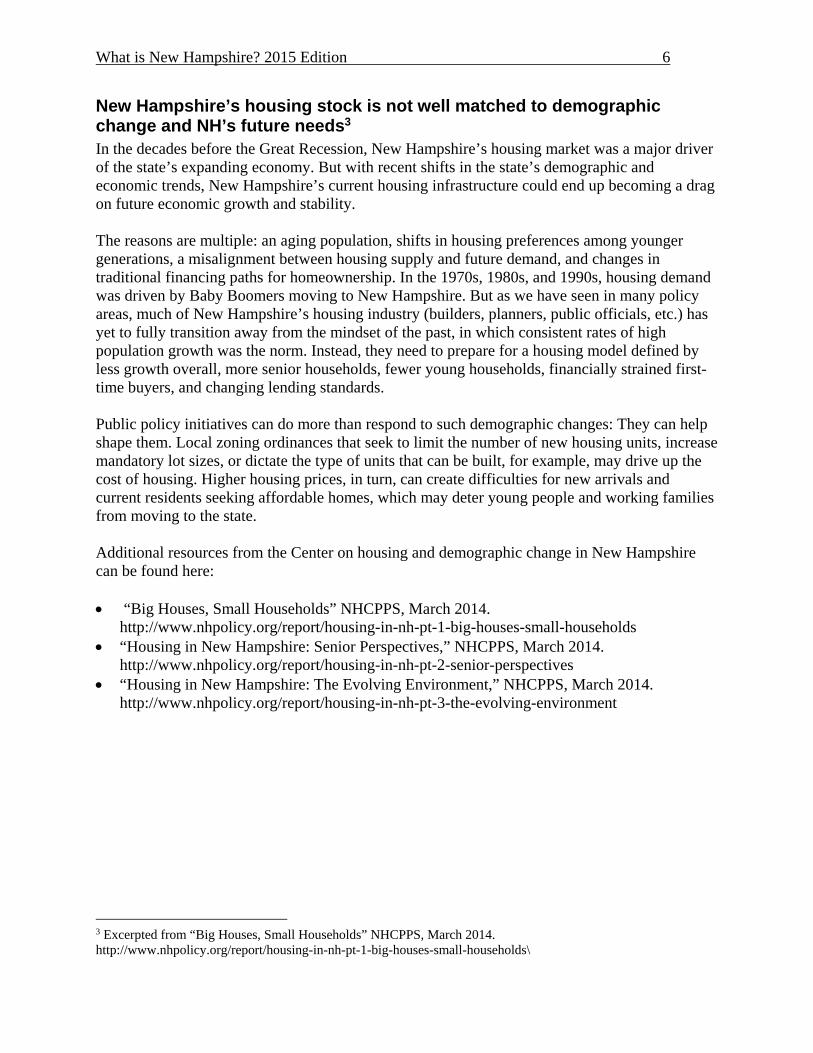

New Hampshire will grow older with fewer young people Population projections for New Hampshire shown in Figure 3 show that the year 2020 will see the beginning of a shift in New Hampshire’s population towards the over-65 population. By then, residents 65 years and older will account for nearly 20 percent of the state population, up from 13.5 percent in 2010. This will be due in large part to the aging of the “Baby Boom” generation – generally speaking, those people born between 1946 and 1964. The growth rate from 2030 to 2040 in the above-65 population (9.7 percent) is predicted to be the lowest growth rate since the decade preceding 1920. The likely causes of this lower growth are the last of

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

65+ Pop 65+ Pop as a % of Total Pop

Figure 3: New Hampshire Population Age 65 and Over

10,681

7,851

5,852

3,1872,646

2,236

-298 -884

-2,320 -2,329 -1,926

83

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

00-01 01-02 02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

To

tal E

xem

pti

on

s

Total Net Migration Of NH (State to State and Foreign)

Figure 2: Net Migration in New Hampshire

What is New Hampshire? 2015 Edition 5

the “Baby Boomer” generation having entered into the 65+ cohort during the preceding decade and the already significant amount of people age 65 and over.

Looking ahead

Measures of child well-being show troublesome trends Child poverty in New Hampshire has been growing over the past decade, and at a rate faster than the nation as a whole. According to data from the U.S. Census’s annual American Community Survey, the New Hampshire child poverty rate in 2013 was almost 11 percent, up from approximately 8% in 2003. This suggests that the child poverty rate is growing more quickly in New Hampshire. Other measures of childhood poverty, including the share of New Hampshire students eligible for free or reduced school lunches, also show steady increases in recent years. This trend is troubling for obvious reasons. Research indicates that growing up in poverty can impede a child’s cognitive development, and children from low-income households typically fare worse on measures of academic success, such as test scores and high school graduation rates.

An aging population will reshape the state’s healthcare system The aging of the population in New Hampshire will put pressure on virtually every dimension of the state’s health care system. If we assume that the elderly population in New Hampshire eligible for the state’s Medicaid program in 2020 will use services at the same rate as the elderly do today, the number of individuals participating in the program will increase rapidly, increasing slightly more than 30 percent over the next 10 years. These trends will put pressure on the state to rethink how it finances long term care services, including institutional and home and community-based services. Additional resources from the Center on aging in New Hampshire can be found here:

“New Hampshire's Silver Tsunami: Aging and the Healthcare System,” NHCPPS, Sept.

2011. http://www.nhpolicy.org/UploadedFiles/Reports/aging_and_the_healthcare_system_final.pdf “Aging and the Public Long Term Care System,” NHCPPS, Sept. 2012.

http://www.nhpolicy.org/UploadedFiles/Reports/Aging_and_the_LTC_Systemv5test.pdf

7.8

10.9

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

New Hampshire - Poverty RateThose Under 18

Figure 4: Children in Poverty Growing

What is New Hampshire? 2015 Edition 6

New Hampshire’s housing stock is not well matched to demographic change and NH’s future needs3 In the decades before the Great Recession, New Hampshire’s housing market was a major driver of the state’s expanding economy. But with recent shifts in the state’s demographic and economic trends, New Hampshire’s current housing infrastructure could end up becoming a drag on future economic growth and stability. The reasons are multiple: an aging population, shifts in housing preferences among younger generations, a misalignment between housing supply and future demand, and changes in traditional financing paths for homeownership. In the 1970s, 1980s, and 1990s, housing demand was driven by Baby Boomers moving to New Hampshire. But as we have seen in many policy areas, much of New Hampshire’s housing industry (builders, planners, public officials, etc.) has yet to fully transition away from the mindset of the past, in which consistent rates of high population growth was the norm. Instead, they need to prepare for a housing model defined by less growth overall, more senior households, fewer young households, financially strained first-time buyers, and changing lending standards. Public policy initiatives can do more than respond to such demographic changes: They can help shape them. Local zoning ordinances that seek to limit the number of new housing units, increase mandatory lot sizes, or dictate the type of units that can be built, for example, may drive up the cost of housing. Higher housing prices, in turn, can create difficulties for new arrivals and current residents seeking affordable homes, which may deter young people and working families from moving to the state. Additional resources from the Center on housing and demographic change in New Hampshire can be found here: “Big Houses, Small Households” NHCPPS, March 2014.

http://www.nhpolicy.org/report/housing-in-nh-pt-1-big-houses-small-households “Housing in New Hampshire: Senior Perspectives,” NHCPPS, March 2014.

http://www.nhpolicy.org/report/housing-in-nh-pt-2-senior-perspectives “Housing in New Hampshire: The Evolving Environment,” NHCPPS, March 2014.

http://www.nhpolicy.org/report/housing-in-nh-pt-3-the-evolving-environment

3 Excerpted from “Big Houses, Small Households” NHCPPS, March 2014. http://www.nhpolicy.org/report/housing-in-nh-pt-1-big-houses-small-households\

What is New Hampshire? 2015 Edition 7

New Hampshire’s Economy

The state’s economic model is changing significantly By many measures, New Hampshire’s economy rests on strong foundations. With high levels of educational attainment, a competitive tax structure, relatively low poverty rates, proximity to the Greater Boston economic market, and an overall high quality of life, the state has many enviable assets that boosted economic growth and prosperity over the past several decades. But New Hampshire faces considerable disadvantages in other areas, especially when compared to areas of the country that are seeing more robust economic growth. These challenges go beyond the economic disruption caused by the Great Recession. Recent developments such as declining rates of in-migration and an aging workforce are upending the model that defined the state’s economy since the 1980s – consistent population growth, increased productivity, and a more resilient economy than our competitors. The shift away from long-held assumptions of consistent growth will reshape the state’s policies on job creation, tax policy, land use, social services, and other areas.

Job growth has slowed New Hampshire’s job growth has declined considerably over the past decade. For instance, while the number of jobs in the state increased annually on average by 4.1 percent during the 1970s, the state actually saw small annual decreases in jobs from 2000 to 2010. That decrease was less than for New England and the nation as a whole (0.3 percent and 0.1 percent, respectively, in average annual job loss). However, over the past three years, New Hampshire has been regaining lost jobs at a slower pace than both the New England region and

the nation. Since 2010, annual job growth has

averaged just under 1 percent in New Hampshire, compared to 1.6 percent nationally and 1.2 for all of New England. The period since 2010 is the first in more than 40 years in which annual job growth in New Hampshire lagged behind the national and Economic Research Division regional rates. The United States and

The years since 2010 are the first period in more than 40 years in which annual job growth in New Hampshire has lagged behind the national and regional rates.

2.5%

1.9% 1.9%

-0.1%

1.6%1.9%

1.5%

1.0%

-0.3%

1.2%

4.1%

2.8%

2.0%

0.0%

0.9%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

1970-80 1980-90 1990-00 2000-10 2010-14

United States New England New Hampshire

Figure 5: Average Annual Growth in Employment, 1970 to 2014

What is New Hampshire? 2015 Edition 8

New England have recovered all of the jobs lost in the recession, while New Hampshire still lags in returning to pre-recession job levels. Most of the recent growth in employment, especially in the service sector, has been in industries that do not require highly skilled workers. Accommodation and food services industries added the most jobs from 2011 to 2013, and most of the positions in this industry require a high school diploma or less for employment. Low skill industries tend to pay wages that are below average. The quality of the jobs created has been mediocre, because two thirds of the jobs created pay below average wages.

Figure 6: Change in New Hampshire Jobs from 2011 to 2013 by Average Wage

Source: Quarterly Census of Wages and Employment

Over 7,000 of the jobs created in New Hampshire from 2011 to 2013 were below the average wage of jobs in the state, with only 5,803 jobs created at an above average wage.

Figure 7: National, Regional, and State Unemployment Rates, 2005-2015

Source: U.S. Bureau of Labor Statistics

5,803

7,089

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Above Average Wage Below Average Wage

0%1%2%3%4%5%6%7%8%9%

10%11%

Apr

il 20

05

Aug

ust 2

005

Dec

emb

er 2

005

Apr

il 20

06

Aug

ust 2

006

Dec

emb

er 2

006

Apr

il 20

07

Aug

ust 2

007

Dec

emb

er 2

007

Apr

il 20

08

Aug

ust 2

008

Dec

emb

er 2

008

Apr

il 20

09

Aug

ust 2

009

Dec

emb

er 2

009

Apr

il 20

10

Aug

ust 2

010

Dec

emb

er 2

010

Apr

il 20

11

Aug

ust 2

011

Dec

emb

er 2

011

Apr

il 20

12

Aug

ust 2

012

Dec

emb

er 2

012

Apr

il 20

13

Aug

ust 2

013

Dec

emb

er 2

013

Apr

il 20

14

Aug

ust 2

014

Dec

emb

er 2

014

Apr

il 20

15

United States New England New Hampshire

What is New Hampshire? 2015 Edition 9

Despite job growth lagging behind national and regional rates, New Hampshire continues to enjoy a lower unemployment rate than the nation or New England as a whole. The past ten years have seen fluctuations largely in line with national and regional trends, but with a narrowing over-performance compared to the rest of the nation.

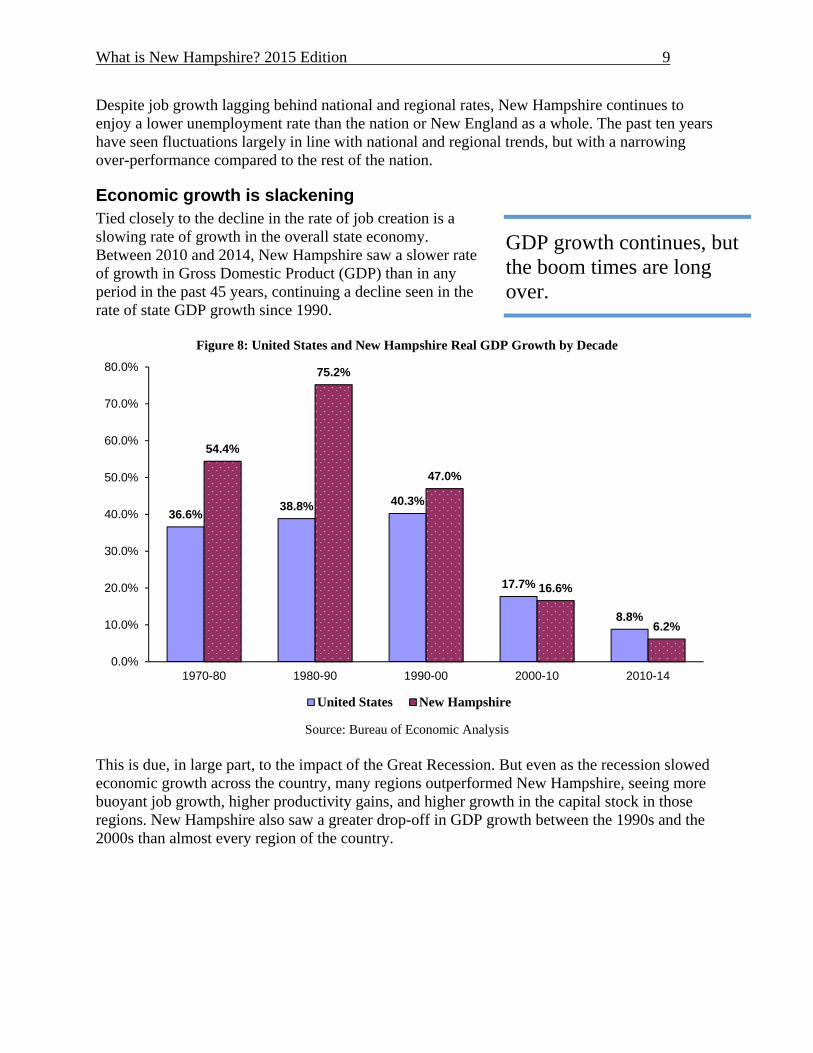

Economic growth is slackening Tied closely to the decline in the rate of job creation is a slowing rate of growth in the overall state economy. Between 2010 and 2014, New Hampshire saw a slower rate of growth in Gross Domestic Product (GDP) than in any period in the past 45 years, continuing a decline seen in the rate of state GDP growth since 1990.

Figure 8: United States and New Hampshire Real GDP Growth by Decade

Source: Bureau of Economic Analysis

This is due, in large part, to the impact of the Great Recession. But even as the recession slowed economic growth across the country, many regions outperformed New Hampshire, seeing more buoyant job growth, higher productivity gains, and higher growth in the capital stock in those regions. New Hampshire also saw a greater drop-off in GDP growth between the 1990s and the 2000s than almost every region of the country.

36.6%38.8% 40.3%

17.7%

8.8%

54.4%

75.2%

47.0%

16.6%

6.2%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

1970-80 1980-90 1990-00 2000-10 2010-14

United States New Hampshire

GDP growth continues, but the boom times are long over.

What is New Hampshire? 2015 Edition 10

Figure 9: Percent Change in Real GDP in BEA Regions4

Source: Bureau of Economic Analysis

Some New Hampshire metropolitan areas growing faster than others Employment growth in New Hampshire’s labor market areas is varied, though not quite as varied as a sampling of similarly-sized regions across New England. Though much is said about economic growth in Portsmouth on the seacoast, Manchester continues to have the fastest-growing employment among New Hampshire’s largest labor market areas, with 6.9% growth over the past four years versus Portsmouth’s 5.0% growth. This represents an increase of 7,800 jobs for Manchester from 2010 to 2014 and 4,300 jobs for Portsmouth. Nashua’s employment levels have grown by 3.8% in the same period. The state-leading growth in Manchester is driven primarily by increases in professional, education, and health services. Portsmouth’s growth, by contrast, has come from the manufacturing, finance, and

4 Source: U.S. Department of Commerce, Bureau of Economic Analysis

47.0%

33.0%30.0%

40.2% 41.1%

48.5%

62.4%

73.5%

39.5% 40.3%

16.6%13.0%

15.9%

3.1%

16.5% 16.8%

25.6%22.9%

19.7%17.7%

6.2% 4.8% 5.7% 6.6% 7.3%4.9%

18.0%

8.8% 8.4% 8.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

1990 to 2000 2000 to 2010 2010 to 2014

0.5%

2.0%

3.1%3.3%3.7%3.8%

4.7%4.8%5.0%

6.9%6.9%7.2%7.3%7.7%

0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

Figure 10: Percent Change of Labor Force in Regional Labor Market Areas, 2010 to 2014

What is New Hampshire? 2015 Edition 11

insurance industries. Manchester’s increases in educational and health employment may be a less visible growth in contrast to Portsmouth’s booming manufacturing trade. While New Hampshire’s metropolitan areas have seen employment growth across the board, it is necessary to note large declines in the numbers of federal, state, and local government employees statewide. Additionally, Nashua in particular has seen a large decline in its manufacturing sector, depressing that city’s economic recovery. The following table compares employment and wages for 2010 and 2013 in New Hampshire with a summary for metro counties and non-metro counties. Metro counties in New Hampshire are Hillsborough, Rockingham and Strafford, while the remaining seven counties are considered non-metro counties.5

Table 1: New Hampshire Employment and Wages by County Type, 2010 to 2013

2010 2010 2010 2013 2013 2013

Total, Private plus Government Units

Average Annual

Employment

Average Weekly Wage Units

Average Annual

Employment

Average Weekly Wage

Change in Employment, 2010 to 2013

Percent Change

Jobs

Percent Change Wages

Metro Counties 23,478 360,664 $920.73 23,777 373,452 $977.46 12,788 3.5% 6.2%

Non-Metro Counties

15,507 225,326 $779.77 15,385 229,382 $826.55 4,056 1.8% 6.0%

State 38,985 585,990 $866.53 39,162 602,834 $920.04 16,844 2.9% 6.2%

Source: Quarterly Census of Employment and Wages As can be seen in the above table, the metro counties in New Hampshire not only contain the majority of the jobs in the state, but employment growth has been faster in the metro counties than in the non-metro counties.

Figure 11: Change in Employment by County Type, 2010 to 2013

Source: Quarterly Census of Employment and Wages

5 Metro, non-metro and rural definition from the United States Department of Agriculture, Economic Research Service.

3.5%

1.8%

2.9%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Metro Counties Non-Metro Counties State

What is New Hampshire? 2015 Edition 12

When examining New Hampshire’s employment growth since 2010 in comparison to New England and the nation as a whole, it is clear that the economic recovery has been somewhat weaker in the Granite State than the region or the country with 3.7% statewide employment growth compared to 4.7% and 6.7% for New England and the United States respectively. This does not mean that New Hampshire is in a worse off state economically than the region or the nation. Rather, New Hampshire entered the recession from a place of much greater economic strength and lower unemployment, so lower job growth is to be expected with fewer people out of work and looking for jobs to begin with.

Figure 12: Percent Change of Labor Force in National, Regional, and State Labor Markets, 2010 to 2014

Source: U.S. Bureau of Labor Statistics, Federal Reserve Bank of St. Louis

Though New Hampshire’s economic growth no longer evokes memories of the boom times decades past, its post-recession recovery continues its respectability both within New England and the nation. Furthermore, cities like Manchester and Portsmouth are witnessing growth that outstrips both the New Hampshire and New England averages and circles the national employment growth average. New Hampshire added over 20,000 jobs in the past four years, with nearly half of that growth coming from the Manchester labor market area alone. As they push the state forward, New Hampshire’s cities continue to be centers of the state’s economic recovery.

Government and health care join manufacturing as NH’s largest sectors The dominant industry in New Hampshire for many years has been the manufacturing sector. Of particular importance for New Hampshire’s economic activity is the smart manufacturing/high

6.7%

4.7%

3.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

United States Average New England Average New Hampshire Average

The state’s cities are still hubs of growth, though New Hampshire’s best is just keeping in line with the national recovery.

What is New Hampshire? 2015 Edition 13

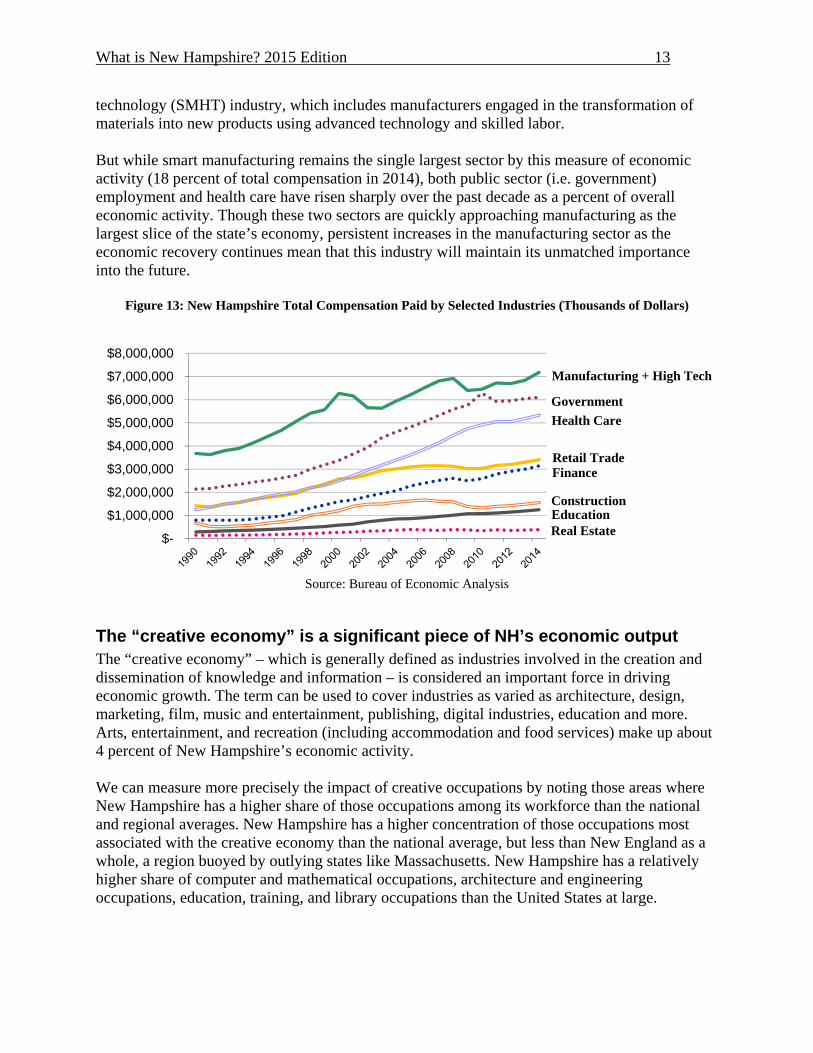

technology (SMHT) industry, which includes manufacturers engaged in the transformation of materials into new products using advanced technology and skilled labor. But while smart manufacturing remains the single largest sector by this measure of economic activity (18 percent of total compensation in 2014), both public sector (i.e. government) employment and health care have risen sharply over the past decade as a percent of overall economic activity. Though these two sectors are quickly approaching manufacturing as the largest slice of the state’s economy, persistent increases in the manufacturing sector as the economic recovery continues mean that this industry will maintain its unmatched importance into the future.

Figure 13: New Hampshire Total Compensation Paid by Selected Industries (Thousands of Dollars)

Source: Bureau of Economic Analysis

The “creative economy” is a significant piece of NH’s economic output The “creative economy” – which is generally defined as industries involved in the creation and dissemination of knowledge and information – is considered an important force in driving economic growth. The term can be used to cover industries as varied as architecture, design, marketing, film, music and entertainment, publishing, digital industries, education and more. Arts, entertainment, and recreation (including accommodation and food services) make up about 4 percent of New Hampshire’s economic activity. We can measure more precisely the impact of creative occupations by noting those areas where New Hampshire has a higher share of those occupations among its workforce than the national and regional averages. New Hampshire has a higher concentration of those occupations most associated with the creative economy than the national average, but less than New England as a whole, a region buoyed by outlying states like Massachusetts. New Hampshire has a relatively higher share of computer and mathematical occupations, architecture and engineering occupations, education, training, and library occupations than the United States at large.

$-

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,000

$8,000,000

Manufacturing + High Tech

Health Care

Retail TradeFinance

ConstructionEducationReal Estate

Government

What is New Hampshire? 2015 Edition 14

By contrast, agriculture and related industries that rely on natural resources make up a relatively small part of the New Hampshire economy. New Hampshire ranks 44th among the states in the portion of economic activity associated with agriculture, forestry, fishing and hunting. Though New Hampshire lags behind New England as a whole in its creative economy, it has become even more creative than the national average over the past decade. Though such a trend may seem like an increase for New Hampshire, here it indicates that the nation has been suffering a stagnation in the relative size of its creative class to a greater extent than the state and region at large. From 2004 to 2014, New Hampshire’s creative class increased from 15% to 16% of the population, a negligible change while the nation saw its creative class remain at 13% of the population.

Attracting the “creative class” With declining rates of in-migration, lower birth rates, and the resultant decline in young residents, New Hampshire must grapple with the challenge of attracting and developing a skilled workforce. The share of the state’s population between the ages of 35 and 44, arguably those in their period of highest productivity, declined by slightly more than 4 percent between 2000 and 2010. Only two states saw a bigger decline over the same period. This ongoing demographic shift must shape how policymakers think about coming workforce needs. As shown below, the traditional workforce cohort (those aged 20 to 64 years) in New Hampshire is projected to decline between 2010 and 2040. These same projections suggest a doubling in the population over 65 over the same time span.

Figure 14: Projections of a Declining Workforce, Growth by Age Cohort

Source: Office of Energy and Planning

0

100,00

200,00

300,00

400,00

500,00

600,00

700,00

800,00

900,00

2010 2015 2020 2025 2030 2035 2040

19 and under

New Hampshire appears strong as it develops a creative economy in a stagnant nation, but underlying problems remain.

20 to 64

65+

What is New Hampshire? 2015 Edition 15

These trends raise important questions for New Hampshire. First, what are the factors that will best attract a workforce to New Hampshire, and what does that mean for public policy? In addition, how can the state take advantage of the human capital associated with the aging of the Baby Boomers and incorporate that in the state’s economic growth?

Looking ahead

New Hampshire faces challenges in developing a future workforce While many of New Hampshire’s economic indicators reflect the decades-long period of growth and prosperity that began in the 1970s, some measures of future prospects are less promising. This can be seen in an analysis the Center developed to assist the Business and Industry Association of New Hampshire in its development of a strategic economic plan for the state. Each “indicator,” or measure of some aspect of the state’s economy, is placed into a broader category: healthcare, education and workforce, energy, infrastructure, etc.6 The table below ranks these measures according to New Hampshire’s position among the other 49 states, from best to worst. Viewed this way, we can divide many of the indicators into two broad categories: those that point to past or current conditions, and those that relate more to future growth. Many of the indicators where New Hampshire fares well, including high education levels and a robust science and engineering workforce, reflect the impact of past trends or current conditions. On the other hand, the table shows that in more “future-oriented” measurements – the change in the 35-to-44-year-old share of the population, average student debt, housing costs, and capital investment –New Hampshire fares quite poorly. These measures are directly linked to a state’s ability to attract and retain young people and arm them with the skills needed to compete for good jobs in coming years. Other areas in which the state ranks near the bottom of the country include many measures of business costs: industrial electric prices, corporate tax rate, health care costs, and land use restrictions. These, too, may constrain future economic growth, as other regions of the country can offer low-cost alternatives to organizations seeking a favorable businesses climate.

6 This is excerpted from “New Hampshire’s Economic Climate: Key Indicators,” NHCPPS, October 2013. http://www.nhpolicy.org/report/new-hampshireamp39s-economic-climate-key-indicators

What is New Hampshire? 2015 Edition 16

Table 2: New Hampshire Economic Dashboard 2013

Indicator New Hampshire Rank Homeownership Rates 2 Pollution Abatement / Dollar Value Added 3 Percent of Tree Cover Urban Areas 3 High School Graduation Rate 4 Voter Turnout Rate 4 Percent of Population in Science & Engineering workforce 5 Percent of Population with Associated Degree or Higher 6 Percent of Children Aged 3-4 in Preschool 6 Public Health and Welfare Spending Per Person in Poverty 7 Manufacturing Supercluster LQ 7 State Business Tax Climate Index 8 Consumption per Capita, Million BTU 8 Transportation Energy Expenditures as Percent of Personal Income 8 VC Investment Dollars per Capita 2011 8 Percent Uninsured 2011 9 R&D Performed per $GDP (Percent) 10 Business Churn 12 Domestic Tourism Spending per Capita 13 Manufacturing Contribution to Total Compensation 13 Creative Economy Jobs Concentration 14 2011 Age Adjusted Mortality Rates 15 Index of State Liability Systems 16 Volunteering Rate 19 State Energy Efficiency Rank 19 Percent of Mandated Health Benefits 20 Percent of State with Access to Broadband Speeds of 3mbps for Downloads, 768 kbps for 20 Water Infrastructure Needs per Capita 21 CEO Grades for State Taxation and Regulation 22 Percent of Jobs in Firms with 20 to 99 Employees 23 Public Government & Administration per $ Personal Income 24 Rate of HS Graduates Going to Degree-Granting Institution 24 Total Employment Percent Change 2007 to 2012 25 Expenditures per Capita, Dollars 26 Rent more than 30% of income 28 Total Health Care Expenditures as a Percent of Gross State Product (GSP), 2010 32 Ratio Median Housing Price to Median Income 34 Natural Gas Prices in Dollars per MMBTU 34 Portion of Unacceptable Rough Roads 35 State-Specific Standardized Infection Ratios (SIRs): 36 State Spending on Natural Resources per Capita 37 Top Marginal Corporate Tax Rate 38 Percent of Bridges Deficient or Obsolete 39 Owner Costs More than 30% of Income 43 State Debt per $ Personal Income 45 Industrial Electric Prices 46 Capital Investment Projects per 100,000 Population 46 Land Use Restriction 47 Change in 35-44 Year Old Share of Population, 2000 to 2010 48 Average Family Premium per Enrolled Employee For Employer-Based Health Insurance 49 Average Student Debt 50

These costs can be compared in detail across states through the use of Regional Price Parities (RPPs), the price levels of goods and services stated as a percentage of the national price level. Based on the costs of various items from the Consumer Price Index including food, transportation, and education, RPPs can be interpreted as the buying power of a dollar in different parts of the country. Using the United States as a baseline with 100, New Hampshire is

What is New Hampshire? 2015 Edition 17

one of a handful of states with a greater RPP (105.9) than the national average. This means that costs in New Hampshire are 5.9% higher than the mean of the United States.

Figure 15: Regional Price Parities by State, 2013 (US = 100)

Source: U.S. Department of Commerce, Bureau of Economic Analysis

Though New Hampshire frequently perceives itself as having an unusually business-friendly climate, this is mostly true in regards to costs only when compared to the rest of New England. Competition with states from other regions of the nation is significantly fiercer.

Policymakers need to prioritize economic development investments In the past, when considering economic development options, New Hampshire policymakers have focused on those areas where the state ranks high in state-by-state surveys: the creation of a low-tax environment, with a focus on high quality of life measures, such as a clean environment, low poverty and low crime. But in order to maintain a competitive advantage against other states, should policymakers here redirect their focus on areas where New Hampshire has typically fallen short, including healthcare and energy costs, infrastructure and public higher education spending?

New Hampshire, 105.9

86 88 90 92 94 96 98 100 102 104 106 108 110 112 114 116 118

MississippiArkansas

South DakotaAlabama

West VirginiaKentuckyMissouri

OhioOklahoma

IowaNebraska

South CarolinaTennessee

KansasLouisiana

IndianaNorth Dakota

North CarolinaGeorgia

IdahoWisconsinMichiganMontana

New MexicoWyoming

TexasArizona

UtahMinnesota

MaineRhode Island

NevadaPennsylvania

OregonFlorida

VermontIllinois

DelawareColorado

VirginiaWashington

New HampshireAlaska

MassachusettsConnecticut

MarylandCalifornia

New JerseyNew York

Hawaii

What is New Hampshire? 2015 Edition 18

Will investments in these or other areas yield better returns on economic growth? The answer, for now, is unclear. But what is clear is that New Hampshire can no longer rely on the demographic trends that have propelled it to economic prosperity over the past three decades. Should the state focus on certain regions of the state? For example, a pro-growth model might focus on the five communities with the highest level of economic productivity, which includes Nashua, Manchester, Concord, Portsmouth, and Rochester. Together, these cities accounted for more than 60 percent of the state’s wages in 2012. Encouraging continued growth in the existing manufacturing sector may provide additional returns to other parts of the state. There is no single, simple response to this new set of circumstances; policymakers will have to weigh various options. These include investing in human capital (an area where we rank relatively high, as measured by educational attainment), redesigning the state’s tax structure (where New Hampshire enjoys one of the lowest per-capita tax collection rates in the country but maintains high corporate taxes), or investing in improved infrastructure and transportation (an area in which the state ranks relatively poorly). The likely return-on-investment of these and other options should be part of that decision-making process, as well.

Additional resources “From Tailwind to Headwind: New Hampshire’s Shifting Economic Trends,” NHCPPS,

September 2012. http://www.nhpolicy.org/report/from-tailwind-to-headwind-new-hampshireamp39s-shifting-economic-trends

“New Hampshire’s Economic Climate: Key Indicators,” NHCPPS, October 2013. http://www.nhpolicy.org/report/new-hampshireamp39s-economic-climate-key-indicators

“Real Personal Incomes for States and Metropolitan Areas, 2013,” Bureau of Economic Analysis, July 2015. http://www.bea.gov/newsreleases/regional/rpp/rpp_newsrelease.htm

“New Hampshire’s Economy at a Glance,” Bureau of Labor Statistics. http://www.bls.gov/eag/eag.nh.htm

What is New Hampshire? 2015 Edition 19

Education in New Hampshire

New Hampshire’s education system remains strong, though shifting student demographics pose future challenges For many years, New Hampshire has had among the highest-performing public education systems in the country. On math and reading scores as reported by the National Assessment of Educational Progress, high school graduation rates, and high school dropout rates, New Hampshire ranks higher than the national figures and is among the top states in the country for overall education quality. However, as in every other state, New Hampshire sees gaps in student performance based on socio-economic status and race/ethnicity, with students from low-income households, black students, and Hispanic students generally faring worse than the statewide student population. There are also significant disparities in student achievement from school district to school district. Those disparities, too, often fall along socio-economic lines. Demographic changes in the state are also fueling the policy debate. Over the past decade, New Hampshire has seen a steady decline in its school-age population and student enrollments. This decline will likely prompt further discussions about education spending – including spending on school infrastructure – staffing levels, changes in curriculum, and regionalization of educational services across communities.

Student outcomes are high, but disparities in achievement persist New Hampshire has long enjoyed high rates of student success on a range of measures.7 But these statewide figures mask disparities across school districts and student subgroups, including racial/ethnic groups and those based on economic status, student disability and English-language learner status.

7 Unless otherwise noted, the data used in this section on student activity can be found on the NH Department of Education’s website: http://education.nh.gov/data/

As in every other state, New Hampshire sees gaps in student performance based on economic status, race and ethnicity.

What is New Hampshire? 2015 Edition 20

Figure 16: Percent of Students Scoring Proficient or Higher on State Reading Tests

Scores on the annual NECAP exams, the state’s standardized tests of student achievement, vary greatly across districts. For instance, the percent of 3rd grade students scoring “proficient” or higher for reading last year ranged from 50 percent in one district to 100 percent for several others, as shown in Figure 17.

Figure 17: Third Grade Reading Scores by School District, 2013 (Percent of Students Scoring "Proficient" or Higher)

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

2005 2006 2007 2008 2009 2010 2011 2012 2013

All students Asian

Black Hispanic

Low-income White

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

What is New Hampshire? 2015 Edition 21

Graduation rates also vary considerably across the state. While the overall state graduation rate is comparatively high, with the majority of New Hampshire high schools graduating between 77 percent and 95 percent of their students in 2011, a handful of schools show stubbornly low graduation rates – with nearly one-third of students in some high schools failing to graduate on time in 2011. College enrollment rates among high school graduates in 2014 ranged from less than 50 percent at some schools to 100 percent at one school.

Figure 18: Percent of High School Graduates Entering Post-Secondary Education, Class of 2014 (Each bar represents a school district in New Hampshire.)

Source: New Hampshire Department of Education

Education funding is largely a local affair School district revenue is raised through a number of different sources. The major source of district revenue is generated through property taxes.

Figure 19: New Hampshire School District Revenue by Category, 2013-148

8 Source: New Hampshire Department of Education, New Hampshire Department of Administrative Services

State Average, …

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Local Property …

Statewide Property …

State Foundation/ Adequacy

Aid, 19%

Federal Aid, 6%

Other State Aid, 3% Tuition, Food, …

What is New Hampshire? 2015 Edition 22

State education aid (not counting the statewide property tax) represents roughly 31 percent of total school district revenue. The share of state aid varies considerably from community to community across New Hampshire. This revenue model reflects the growing efforts to “target” state education aid to communities with less ability to generate school district revenue through local taxation. However, the extent to which targeting is allowed to drive state education spending remains a topic of considerable debate. Compared to the rest of the nation, New Hampshire ranks in the bottom third in terms of state contributions to education. In 2011-12 (the most recent year for which comparable national data is available), the state contributed 36 percent of total school district revenue (including the statewide property tax), compared to the national average of 45.5 percent. In terms of total spending, however, New Hampshire school districts spent more per pupil than the national average. Though as a percent of the overall economy, New Hampshire’s education spending has been below the national rate. During the 2013-14 school year, New Hampshire school districts spent an average of $13,721 per pupil, well above the national average of $10,700 per pupil.

Figure 20: Per-Pupil Education Spending by State, 2013-149

New Hampshire’s funding for higher education is the lowest in the country The past decade has witnessed significant changes in state fiscal support for higher education, much of it driven by financial pressures from the Great Recession. State funding for the University System of New Hampshire (USNH) fell by nearly 50 percent in FY2012, but has been

9 Annual Survey of School System Finances 2013

New Hampshire, $13,721

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

What is New Hampshire? 2015 Edition 23

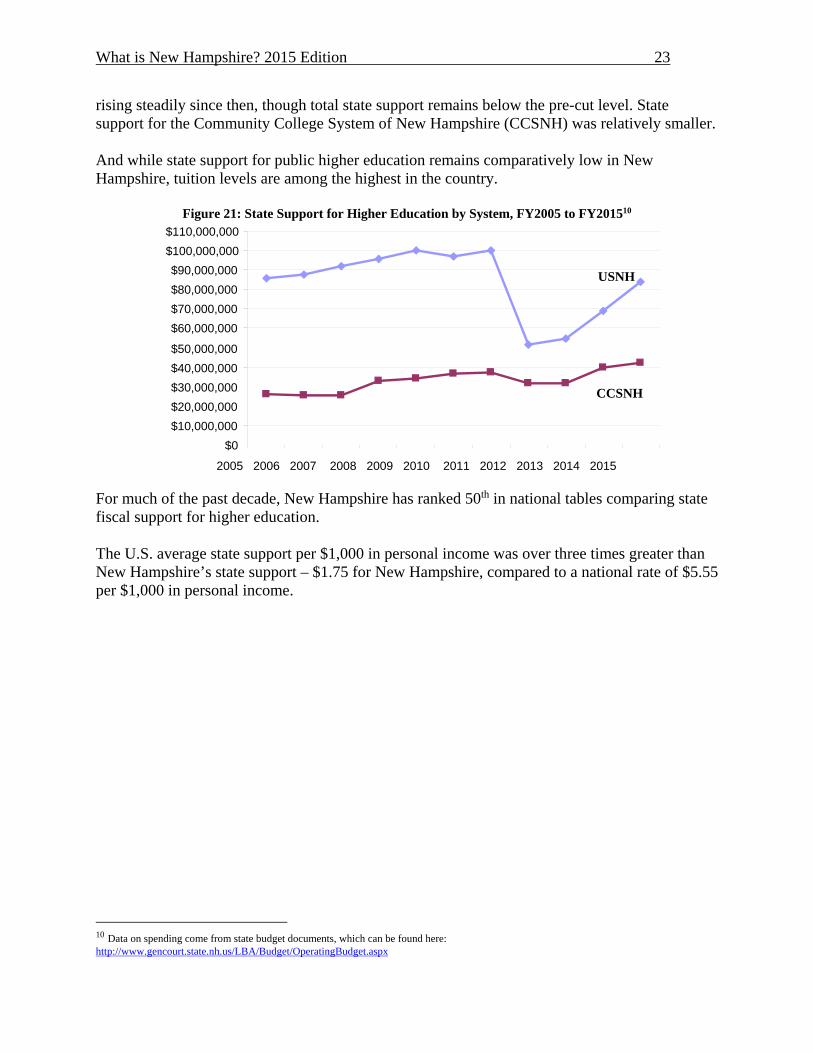

rising steadily since then, though total state support remains below the pre-cut level. State support for the Community College System of New Hampshire (CCSNH) was relatively smaller. And while state support for public higher education remains comparatively low in New Hampshire, tuition levels are among the highest in the country.

Figure 21: State Support for Higher Education by System, FY2005 to FY201510

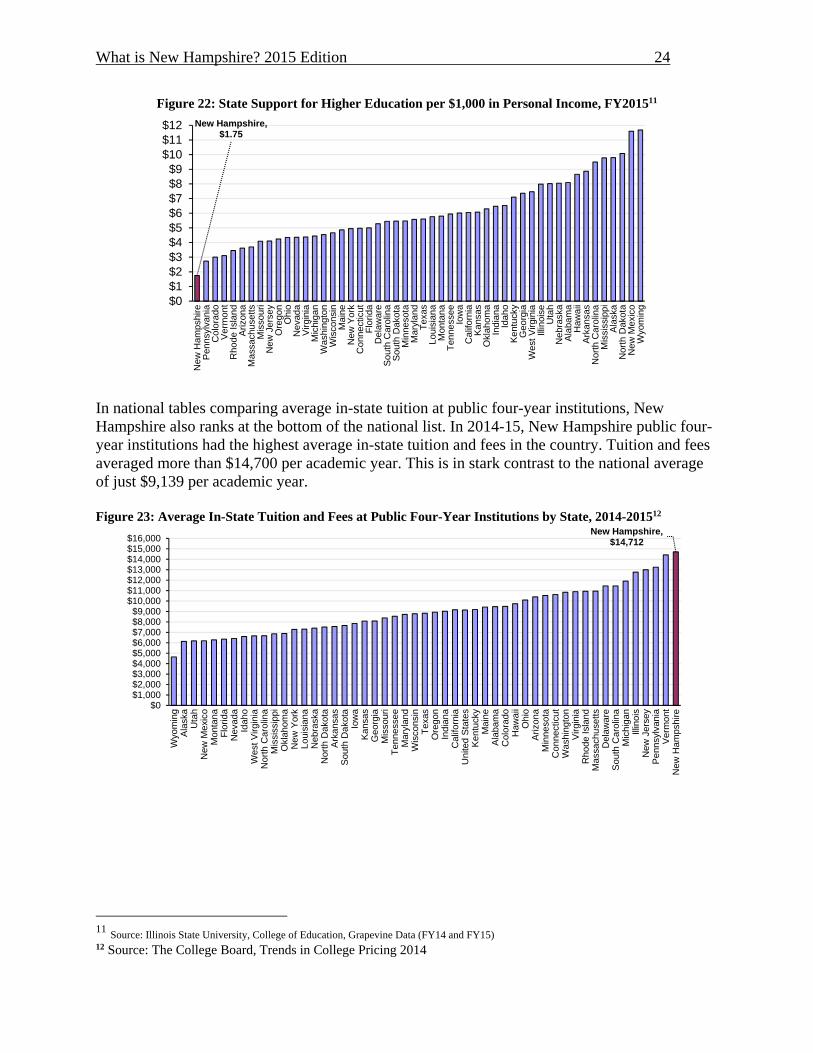

For much of the past decade, New Hampshire has ranked 50th in national tables comparing state fiscal support for higher education. The U.S. average state support per $1,000 in personal income was over three times greater than New Hampshire’s state support – $1.75 for New Hampshire, compared to a national rate of $5.55 per $1,000 in personal income.

10 Data on spending come from state budget documents, which can be found here: http://www.gencourt.state.nh.us/LBA/Budget/OperatingBudget.aspx

$0

$10,000,000

$20,000,000

$30,000,000

$40,000,000

$50,000,000

$60,000,000

$70,000,000

$80,000,000

$90,000,000

$100,000,000

$110,000,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

USNH

CCSNH

What is New Hampshire? 2015 Edition 24

Figure 22: State Support for Higher Education per $1,000 in Personal Income, FY201511

In national tables comparing average in-state tuition at public four-year institutions, New Hampshire also ranks at the bottom of the national list. In 2014-15, New Hampshire public four-year institutions had the highest average in-state tuition and fees in the country. Tuition and fees averaged more than $14,700 per academic year. This is in stark contrast to the national average of just $9,139 per academic year. Figure 23: Average In-State Tuition and Fees at Public Four-Year Institutions by State, 2014-201512

11 Source: Illinois State University, College of Education, Grapevine Data (FY14 and FY15) 12 Source: The College Board, Trends in College Pricing 2014

New Hampshire, $1.75

$0$1$2$3$4$5$6$7$8$9

$10$11$12

New

Ham

pshi

reP

enns

ylva

nia

Col

orad

oV

erm

ont

Rho

de Is

land

Ariz

ona

Mas

sach

uset

tsM

isso

uri

New

Jer

sey

Ore

gon

Ohi

oN

evad

aV

irgin

iaM

ichi

gan

Was

hing

ton

Wis

cons

inM

aine

New

Yor

kC

onne

ctic

utF

lorid

aD

elaw

are

Sou

th C

arol

ina

Sou

th D

akot

aM

inne

sota

Mar

ylan

dT

exas

Loui

sian

aM

onta

naT

enne

ssee

Iow

aC

alifo

rnia

Kan

sas

Okl

ahom

aIn

dian

aId

aho

Ken

tuck

yG

eorg

iaW

est V

irgin

iaIll

inoi

seU

tah

Neb

rask

aA

laba

ma

Haw

aii

Ark

ansa

sN

orth

Car

olin

aM

issi

ssip

piA

lask

aN

orth

Dak

ota

New

Mex

ico

Wyo

min

g

New Hampshire, $14,712

$0$1,000$2,000$3,000$4,000$5,000$6,000$7,000$8,000$9,000

$10,000$11,000$12,000$13,000$14,000$15,000$16,000

Wyo

min

gA

lask

aU

tah

New

Mex

ico

Mon

tana

Flo

rida

Nev

ada

Idah

oW

est V

irgin

iaN

orth

Car

olin

aM

issi

ssip

piO

klah

oma

New

Yor

kLo

uisi

ana

Neb

rask

aN

orth

Dak

ota

Ark

ansa

sS

outh

Dak

ota

Iow

aK

ansa

sG

eorg

iaM

isso

uri

Ten

ness

eeM

aryl

and

Wis

cons

inT

exas

Ore

gon

Indi

ana

Cal

iforn

iaU

nite

d S

tate

sK

entu

cky

Mai

neA

laba

ma

Col

orad

oH

awai

iO

hio

Ariz

ona

Min

neso

taC

onne

ctic

utW

ashi

ngto

nV

irgin

iaR

hode

Isla

ndM

assa

chus

etts

Del

awar

eS

outh

Car

olin

aM

ichi

gan

Illin

ois

New

Jer

sey

Pen

nsyl

vani

aV

erm

ont

New

Ham

pshi

re

What is New Hampshire? 2015 Edition 25

Student debt continues to climb Mounting student debt has become a critical policy issue on both the national and the state level. The total amount of student debt held by U.S. graduates is more than $1 trillion – with almost 40 million Americans carrying student debt.13 According to current estimates, the average New Hampshire college student graduates with more than $32,000 in student loan debt – the highest in the nation.14 If the cost of higher education continues to climb and loans remain one of the primary sources of self-funding, student debt will likely continue to climb. Average student debt is increasing at all USNH institutions.15 Figure 24: Average Undergraduate Debt Load for In-State Students by Institution, 2007-2012

Source: UNH, Keene, and Plymouth Office of Institutional Research

Despite increasing debt loads among in-state students attending New Hampshire institutions, students enjoy lower default rates on their student loans when compared to the national average. When examining the default rate on student loans of students cohorts three years after leaving their schools (a reasonable measure for a student’s ability to pay off their loans), New Hampshire’s private universities both eclipse and trail its public schools, highlighting the difficult decision students face in choosing between public and private post-secondary education.

13 Consumer Financial Protection Bureau, “Student Loan Affordability: Analysis of Public Input on Impact and Solutions”, May 8, 2013. 14 Institute for College Access & Success, The Project on Student Debt: http://projectonstudentdebt.org. The Project on Student Debt collects data from both private and public colleges and does not distinguish between resident and non-resident students. 15 Data may not include all private loans that students or their parents take out. This only includes loan information received or reported to the institution.

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

2007 2008 2009 2010 2011 2012

UNH KSC

PSU

What is New Hampshire? 2015 Edition 26

Figure 25: Three-Year Official Cohort Default Rates for New Hampshire Institutions16

The last three years of cohort data show student loan default rates generally remaining consistent within institutions, with the greatest variation occurring between institutions. The University of New Hampshire enjoys the lowest student loan default rate of New Hampshire’s public schools, just 2.9% in 2014, while Granite State College experiences among the worst student loan default rate in New Hampshire at 10.3% the same year. Business Administration and Management is the most popular major at both of these schools, so differing returns on investment from the selection of a major is not enough to account for this discrepancy in the student loan default rate. The amount in-state students pay for bachelor’s degrees at public schools in New Hampshire is similar between schools, averaging near $100,000, while private schools may be nearly twice that price. Even with higher costs, however, graduates of certain private universities may see a greater return on their investment depending on which institution they attend. Looking ahead

New Hampshire should expect continued declines in student population Over the past decade, New Hampshire has seen several changes in its student population, including a steady decline in public school enrollment, growth in the charter school and home school population17, and growing racial and ethnic diversity among school children, as well as increases in measures of economic hardship among young people.

16 Source: U.S. Department of Education 17 New Hampshire legalized the operation of charter schools, which are funded by tax dollars but have more leeway in administration and curricula than traditional schools, beginning with the 2004-05 school year.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2009 2010 2011

What is New Hampshire? 2015 Edition 27

These trends will help shape future education policy discussions at the state and local level, including conversations about staffing levels, funding formulas, investment in school facilities, curriculum offerings, and the achievement gap.

Figure 26: New Hampshire Public Grade School Enrollment

In 2002-03, total public school enrollment peaked at about 207,000 students. By the 2014-15 school year, total public school enrollment had decreased to 183,604 – a decline of 11.6 percent from the 2002-03 high. This decline raises questions for school districts about the possible need to consolidate functions across schools, including combining school districts and SAUs.

Considering cost reduction through school consolidation18 With demographic pressure, declining state aid, and increased pressure for reporting assessment, and accountability on districts from state and federal governments, arguments have been made for school consolidation. These arguments usually rest on a handful of assumptions. Most common is the basic concept of economies of scale, whereby adding students to a district will reduce per pupil costs if the additional students do not result in an increase in fixed costs. In addition, it is often argued that larger districts will be able to support more specialized teaching staff, thereby providing a wider, more diverse education to students. There are often, however, other factors which can undercut any potential savings or advantages assumed in the above arguments. For one, average transportation costs may increase through consolidation, as a district or SAU must transport more students over a larger geographic area. Consolidation may also result in higher personnel costs, especially if new salary agreements result in lower-paid staff from one district becoming newly eligible for higher wages and benefits once they are employed by a larger district.

18 Excerpted from: “School Consolidation in NH: Some Points for Consideration” NHCPPS, April 2015. http://www.nhpolicy.org/report/school-consolidation-in-nh-some-points-for-consideration

63,142 64,458 66,828 67,347 67,384 66,413 64,961 64,392 62,882 61,494 60,114 58,733 58,158

42,077 41,672 40,514 39,747 38,646 38,022 36,880 36,726 35,923 34,714 34,696 34,187 33,743

90,772 89,077 87,034 85,788 84,636 83,234 82,313 81,086 80,200 79,528 78,065 77,397 76,576

9,757 9,989 10,116 10,360 10,375 10,489 10,968 11,969 11,922 11,904 11,888 11,602 11,570

0

25,000

50,000

75,000

100,000

125,000

150,000

175,000

200,000

225,000

High School Middle School Elementary Kindergarten

What is New Hampshire? 2015 Edition 28

Still, it must be said: Research offers few firm conclusions about the impact of consolidation. In most instances, the impacts (whether financial, educational or community) of school/district consolidation vary widely according to the particular circumstances of each case. One important note: A distinction must be drawn between the consolidation of school districts, and consolidation of SAUs. A school district is a distinct political subdivision, with a single controlling school board. An SAU, on the other hand, can cover just a single school district or include multiple districts. School district costs include the usual things associated with education expenses: instruction, transportation, facilities maintenance, teacher salaries and benefits, etc. The costs associated with an SAU office are largely administrative, usually limited to the personnel costs associated with the superintendent office staff. In terms of cost savings from consolidation, this means that combining existing SAUs will likely result in lesser savings unless that shift is accompanied by a parallel consolidation, to some degree, among the member school districts. In addition, the fact that superintendents in multi-district SAUs must report to multiple school boards has been raised numerous times in past discussions as a barrier to streamlining administrative responsibilities in the state’s public schools. Attempts to quantify costs savings associated with consolidation typically cover the following areas:

Financial savings from consolidation are most likely when dealing with relatively small educational units. There is, however, wide disagreement about what constitutes a “small” school or district.19

Transition costs are often associated with consolidation, though they may decline over

time. These transition costs may include new construction costs to accommodate the shift in student population that results from consolidation.

Research indicates that increasing school size initially brings positive returns both on cost savings and student outcomes, but these trends are reversed as size continues to increase beyond a certain point. Defining that point with precision, however, is subject to disagreement within the research literature.20

Consolidation plans often overlook impacts beyond education costs, including residents’ connections with existing schools, housing prices and economic activity in the wider community associated with a local school.

19 Craig Howley, Jerry Johnson & Jennifer Petrie, “Consolidation of Schools and Districts: What the Literature Says and What it Means,” National Education Policy Center, February 2011, and Ulrich Boser, “Size Matters: A Look at School-District Consolidation,” Center for American Progress, 2013. 20 John Slate & Craig H. Jones, “Effects of School Size: A Review of the Literature with Recommendations,” Essays in Education, vol. 13, 2005. Joshua Barnett, Gary Ritter & Christopher Lucas, “Does Size Matter? School Consolidation Policy Issues in Arkansas,” University of Arkansas, Office for Education Policy,” 2004.

What is New Hampshire? 2015 Edition 29

Table 3: Administrative Costs for New Hampshire Districts by Enrollment

We see in New Hampshire that, as enrollment increases, general administrative expenses (those associated with district or SAU-wide functions) steadily decrease. In fact, general administration consumes more than twice as much of a district budget for districts with 100 students or fewer than it does for those districts with 3,000 students or more. However, school-level administration costs remain relatively similar regardless of district-wide enrollment, varying between 4.7 percent and 5.6 percent of each enrollment category. This seems to indicate that cost savings are most evident, not through combining individual schools, but by combining smaller districts into larger districts.

The Common Core is bringing big changes in curriculum and assessments The 2014-15 academic year marked the first year of full implementation of the Common Core State Standards (CCSS) in New Hampshire schools. These standards (often referred to simply as the “Common Core”) are a set of expectations about what students should know and be able to demonstrate at each grade level. The standards set goals for student learning and benchmarks against which to measure that learning. The CCSS were developed by education leaders across the country to provide a uniform set of standards from state to state. The goal is to have the same set of expectations for students, no matter where they go to school. The CCSS emphasize “higher-order” skills, such as critical thinking and problem-solving, that are supposed to better equip students for success in higher education and the workplace. The CCSS focus on two areas: mathematics and language arts. While New Hampshire has adopted its own state standards for other subject areas, those for math and language arts mirror those of the CCSS. Among the changes ushered in by the Common Core is a new set of standardized tests. New Hampshire is one of 24 states administering the SMARTER Balanced exams as part of the Common Core implementation. These new standardized tests, which replace the NECAP exams

District Enrollment

# of districts*

Gen. Admin expenses as

% of total expenses

School Admin expenses as %

of total expenses

Gen Admin

per pupil

School Admin

per pupil

<100 students 26 6.3% 5.6% $2,155 $1,923

100‐300 28 4.6% 4.7% $1,116 $1,141

300‐500 25 4.2% 4.7% $865 $979

500‐1,000 27 4.2% 5.3% $768 $971

1,000‐3,000 41 4.2% 5.4% $666 $862

3,000‐5,000 12 3.1% 5.2% $443 $751

5,000+ 2 2.7% 5.1% $325 $608

Statewide 161 3.8% 5.2% $605 $829

*14 New Hampshire districts that do not operate schools are not included here.

What is New Hampshire? 2015 Edition 30

that have been in place since 2005, were first administered to New Hampshire students in spring 2015. Students take these new exams online, with computers, and, because of quicker result turnaround times, are designed to provide more useful information to teachers to tailor instruction to meet the needs of each student. Dependent on approval of federal regulators, some New Hampshire schools may opt to replace administration of the SMARTER Balanced assessment with the SAT or ACT exams to satisfy testing requirements following recent changes to state law. The most visible issues in this first year of CCSS implementation has been the participation rates of students at higher grade levels. In Nashua, for instance, 99% of students in grades three through seven participated in this year’s SMARTER Balanced exams, but a mere 55% of eleventh graders took the exam, resulting in a district-wide participation level of 92%. This falls below the federal government’s required participation level by three percent. New Hampshire’s largest school district, Manchester, also did not meet federal requirements for participation levels. It is thought that beyond parental resistance to the new standards, students at higher grade levels may wish to avoid these stringent, additional tests. Beyond ensuring that new curricula and teaching methods align with these new exams, meeting desired participation levels among students will be among the challenges facing educators in the 2015-16 school year.

How can public education help address the needs of the future economy? New Hampshire has a higher share of its population employed in science and engineering fields than much of the rest of the country (3.9 percent compared to 2.5 percent nationwide), ranking the fifth-highest state in the country (and behind the District of Columbia).