Embed Size (px)

Citation preview

Wearable for the individual enterprise

Richard Jo,

16th June 2015,

Conference 2015, Seoul

11 June 20152

Table of contents

Where to find out opportunity

Implication for entry & growth strategy

Strategy direction for wearable players

11 June 20153

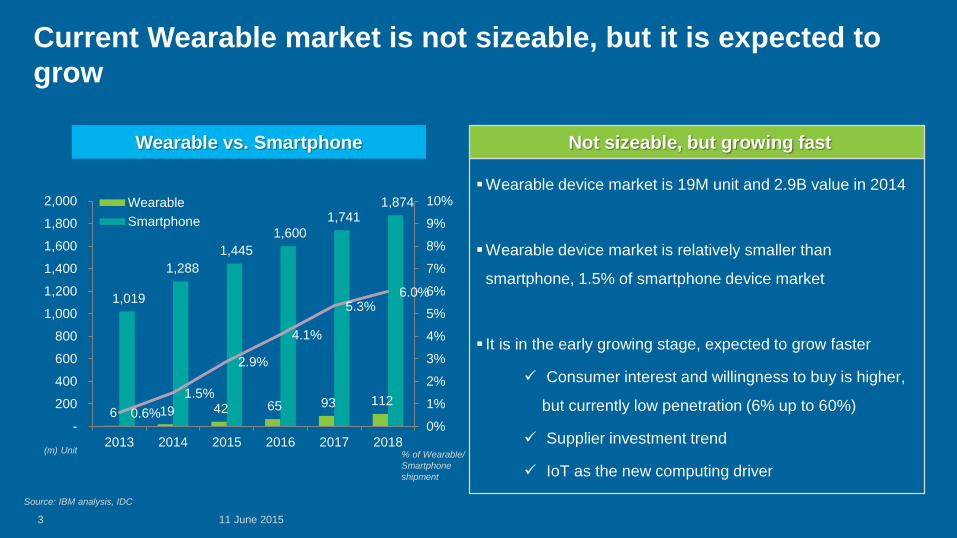

Current Wearable market is not sizeable, but it is expected to

grow

6 19 42 65 93 112

1,019

1,288

1,445

1,600

1,741 1,874

0.6%

1.5%

2.9%

4.1%

5.3%6.0%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2013 2014 2015 2016 2017 2018

Wearable

Smartphone

Wearable vs. Smartphone Not sizeable, but growing fast

Wearable device market is 19M unit and 2.9B value in 2014

Wearable device market is relatively smaller than

smartphone, 1.5% of smartphone device market

It is in the early growing stage, expected to grow faster

Consumer interest and willingness to buy is higher,

but currently low penetration (6% up to 60%)

Supplier investment trend

IoT as the new computing driver

Source: IBM analysis, IDC

(m) Unit % of Wearable/

Smartphone

shipment

11 June 20154

Wearable can be categorized into General Computing and

Specific Use

Specific UseGeneral Computing

Connectivity Mixed SyncingAlways Connected

Device mfg.Apparel Firms and

Smaller Tech FirmsTech Giants

Form FactorWristband, Clip-on,

EmbeddedWatch / Glasses

Functionality Single FunctionMulti-Function

Email Maps

User ConsumerConsumer/

Enterprise

Source: IBM analysis, IDC, Deloitte

11 June 20155

General Computing category will exceed Specific Use category

and to lead the market growth

Wearable device volume by category

5

15

30

41 48 50

2 4 12

24

45

62

-

10

20

30

40

50

60

70

2013 2014 2015 2016 2017 2018

Specific

General

Wearable device value by category

0.5 1.7

3.3 4.3 4.8 4.7

0.5 1.2 2.9

5.3

11.3

15.9

-

5.0

10.0

15.0

20.0

2013 2014 2015 2016 2017 2018

SpecificGeneral

Comment

Innovator’s wearable devices take the majority of the

market, which is mostly in Specific Use category

Value of General Computing will exceed that of Specific

Use in 2016, as the ASP is higher

General Computing category will grow faster than

Specific Use with the strategic focus from the tech giant,

including Smartphone manufacturers, IT service

providers, Telco, and App developers

Source: IBM analysis, IDC

(m) Unit

(b) USD

11 June 20156

While Consumer take more, Enterprise segment will grow

faster, because multiple functions will be used at work

Unit Share by user type93% 95% 93% 91% 88% 86%

7% 5% 7% 9% 12% 14%

0%

20%

40%

60%

80%

100%

2013 2014 2015 2016 2017 2018

Consumer

Enterprise

Value share by user type

86% 87% 86% 83%74% 70%

14% 13% 14% 17%26% 30%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2013 2014 2015 2016 2017 2018

ConsumerEnterprise

Comment

Multiple function support (e.g. email, scheduling) will be

adopted by the Enterprise as Smartphone used at work

Currently, smartphone using rate at work both employee

liable and corporate liable is about 25% from the total

(this figure considered for user type share calculation)

As the market grows led by General Computing category

and personal devices are encouraged to use at work

(e.g. BYOD), Enterprise will be the growing user type in

mid to long termSource: IBM analysis, IDC

11 June 20157

Mega trend is that Enterprise have integrated various devices

into the workplace and expanding rapidly

Key Fact Mega Trend

Smart Device

Computing

MobileApplications

for Enterprise

Bring

Your

Own

Device

While prices of smartphones and tablets are

declining1 (8%), their capabilities and

applications continue to increase

Market growing at CAGR 27%2 - $28b in

2013 to $58b in 2016

BYOD and Enterprise Mobility3 market will

grow from $72b in 2013 to $284b in 2019

Availability of this standard hardware and

software platform for variety of use cases is

fueling enterprise adoption

70% of enterprises4 are deploying

applications for businesses

Research states benefits from BYOD include

improved employee satisfaction, employee

productivity, and greater workforce mobility5

Source: Deloitte, IDC, VisionMobile, Greyhound Research, Capgemini

11 June 20158

Meanwhile, the emerging of On-demand economy and the

double technology revolution of Mobile and Analytics sparks

the Individual Enterprise

Systems of

Engagement

Systems of

Insight

Systems of

Records

Insightful Enterprise

Intelligent organizations

Automated processes

Empowered individuals

Individual Enterprise

Integrated ecosystems

Insight at the point of

engagement

Contextual actions in the

moment

Functional Enterprise

Efficient organizations

Streamlined processes

Focused individuals

Situational Enterprise

Networked organizations

Dynamic processes

Responsive individuals

Tablets, Phones,

and Wearable

Desktops and

LaptopsMainframes

and Minis

An

aly

tic

s

Mobile

Increase of Personal

contributor

Increase of Mobile

workers

Increase the real-

time business

Technology

development

Mobile Only

On demand

economy

Source: IBM analysis

11 June 20159

Individual Enterprise can add the innovative business value,

thus the enterprise will focus and invest its enabling systems

Create new business value

Mobility compresses time between situations and action

Mobility step changes productivity growth

Mobility allows enterprise redesign

Powered by analytics

Mobile analytics drive real-time situational understanding

Mobile analytics brings in-the-moment intelligence

Mobile analytics accelerates the ROI of information

Designed first for mobile

Mobility redefines operating models

Mobility is the foundation of new models of engagement

Mobility optimizes for the end-user

Unleash empowered employees

Mobility reconfigures individual workflows

Mobility stimulates skill acquisition

Mobility empowers individuals to create their own work experience

Characteristics of Individual Enterprise

Source: IBM analysis

11 June 201510

Strategic focus will need to be the General computing for

Enterprise, although Consumer watch market establishing firstM

ark

et

Att

racti

ven

ess (

Gro

wth

, S

ize)

Very High

Not at all

Moderate

High

Low

Technology Newness (Time to market)

Totally Not at allVery Moderately Slightly

Watch for

Consumer

1

Watch for

Enterprise

2

General Computing

Specific Use

Glass/ Helmet

for Enterprise

3

Band for

Consumer

Band for

Enterprise

Glass/ Helmet

for ConsumerEmbedded for

Enterprise

Embedded for

Consumer

Comment

General computing need to be the focus

area, from Watch to Glass

Consumer Watch segment can be the very

short term focus, while Enterprise Watch

segment need to be the top priority

For Enterprise segment it is critical to

provide the use case at work in order to take

the market opportunities

Offering-Market opportunity map

Source: IBM analysis

11 June 201511

Table of contents

Where to find out opportunity

Implication for entry & growth strategy

Strategy direction for wearable players

11 June 201512

Finance and Healthcare will be the most feasible vertical

market for Individual Enterprise General Computing

Comment

Market feasibility is higher in Finance and

Healthcare in terms of the revenue size, value

added impact, and the relationship with General

Computing

Financial market spans mainly Banks and

Insurance. With the proliferation of Sales Force

Automation in this area, the type of Individual

Enterprise increase rapidly. Watches for

supporting SFA will be used

Work at hospital requires wearable devices for

the accuracy, productivity and convenience. As

well Healthcare vertical is familiar with wearables

as it already started collect and analyse the data

from the patient’s wearable devices

Source: IBM analysis, IDC, Frost & Sullivan, Morgan Stanley

HighLow

Overall

Commercial

Industrial

Consumer

Related toGeneral Computing

Impact of valueadded by Display

Market feasibility assessment by industry

The size of each

circle represents the

business value

Feasibility by 2018

11 June 201513

As no one dominate the value chain, the Enterprise Specialist

will be the best revenue model providing end to end solutions

Value Chain structure

HW SW Contents Dist. Access

Processor Sensor Display Device OS NW proto. App. Media/Data Retailer Cloud CSP

General

Computing

Specific Use

Many Telco

N/A

Personal Data

N/A

HW SW Contents Dist. Access

Processor Sensor Display Device OS NW proto. App. Media/Data Retailer Cloud CSP

General

Computing

Specific Use

Many Telco

N/A

Personal Data

N/A

Health

careTBD N/A

Other

VerticalTBD TBD TBDEnterprise Specialist model

Enterprise

Specialist

As a service

model

Cu

rren

tN

ea

r Fu

ture

Source: IBM analysis, Deloitte

11 June 201514

Especially, sustainable and robust use case will be the key

success factor in the enterprise market entry & growth

Individual enterprise based on Smart Watch

Use case as the Key buying factor for Enterprise

Use cases for Smartwatch are definitely needed

(Watch 15% and Smartphone 14% are replaceable by Wearable purchases)

Definite needs of Use case at work

Healthcare

- Patient Care

Finance

- SFA w/ salesforce.com

19%

21%

47%

34%

Share health or other data

Monitor Health metrics

Keep track of exercise

Work Purpose

37%Track of everyday activities

61%

40%

12%

11%

Too expensive

Waiting to see new products

Uncomfortable to wear

Not useful

11%Design not discrete enough

Top wearable use case

Reasons for NOT purchasing Wearable

Source: Morgan Stanley 2014

11 June 201515

Quality use Case stems from Strong Eco-system (vertical), rich

experience (back-end service) and Always on technology

Strong Eco-

system

Rich Experience

Always-On

Platforms that can operate with a number

of devices, allowing customers to use

their smartphones for a growing array of

Wearable Technology

Integration of several sensors (such as

accelerometer, camera, etc.) allowing

rich customer experience.

Back-end services (Multidimensional

Analytics and connectivity with other

sensors) enhance customer experience

Technologies like Bluetooth 4.0 enable device to instantly connect, allowing

wearable device to work under time critical conditions such as healthcare

Key Attribute of Wearable use case

Source: Deloitte

11 June 201516

Table of contents

Where to find out opportunity

Implication for entry & growth strategy

Strategy direction for wearable players

11 June 201517

Three Strategic direction is recommended to the display

business

Strategic Alliance with Smart

device general computing

makers

Align closely with Enterprise

Killer Apps or IT service

provider both in technology

and business

Select vertical markets and

aggressively establish and

participate the eco system

Tech Giant, smart device

manufacturer will take the

HW leadership including OS

and other components

Eco play is the key to

success, component vendor

also can lead the eco system

by aligning with App

developers or IT service

providers

To choose the vertical is

critical because it defined

what to delivery and who to

work with

Healthcare, Field

maintenance, and Public

safety can be the candidate

11 June 201518

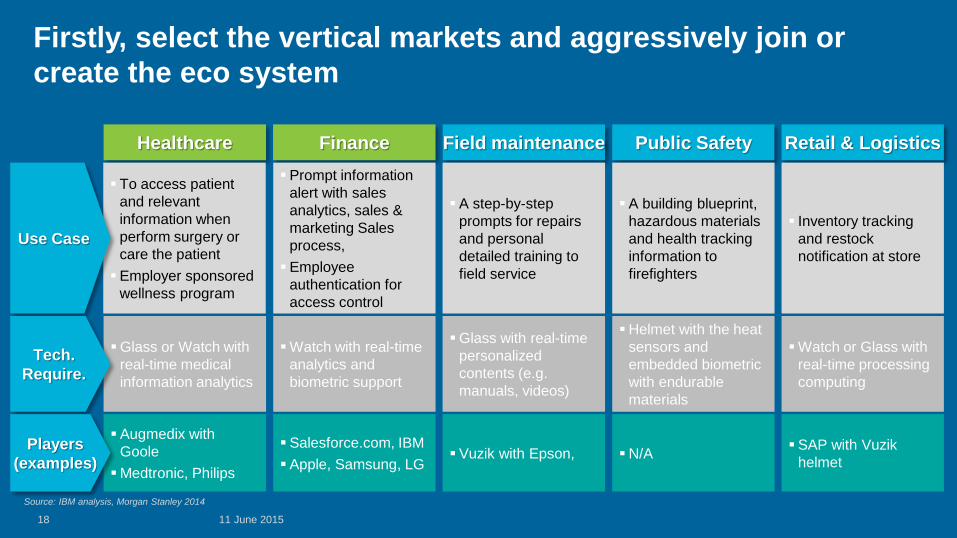

Firstly, select the vertical markets and aggressively join or

create the eco system

Field maintenance Public SafetyHealthcare

A step-by-step

prompts for repairs

and personal

detailed training to

field service

A building blueprint,

hazardous materials

and health tracking

information to

firefighters

To access patient

and relevant

information when

perform surgery or

care the patient

Employer sponsored

wellness program

Finance

Prompt information

alert with sales

analytics, sales &

marketing Sales

process,

Employee

authentication for

access control

Retail & Logistics

Inventory tracking

and restock

notification at store

Glass or Watch with

real-time medical

information analytics

Glass with real-time

personalized

contents (e.g.

manuals, videos)

Helmet with the heat

sensors and

embedded biometric

with endurable

materials

Watch with real-time

analytics and

biometric support

Watch or Glass with

real-time processing

computing

Augmedix with

Goole

Medtronic, Philips

Vuzik with Epson, N/ASalesforce.com, IBM

Apple, Samsung, LG

SAP with Vuzik

helmet

Use Case

Tech.

Require.

Players

(examples)

Source: IBM analysis, Morgan Stanley 2014

11 June 201519

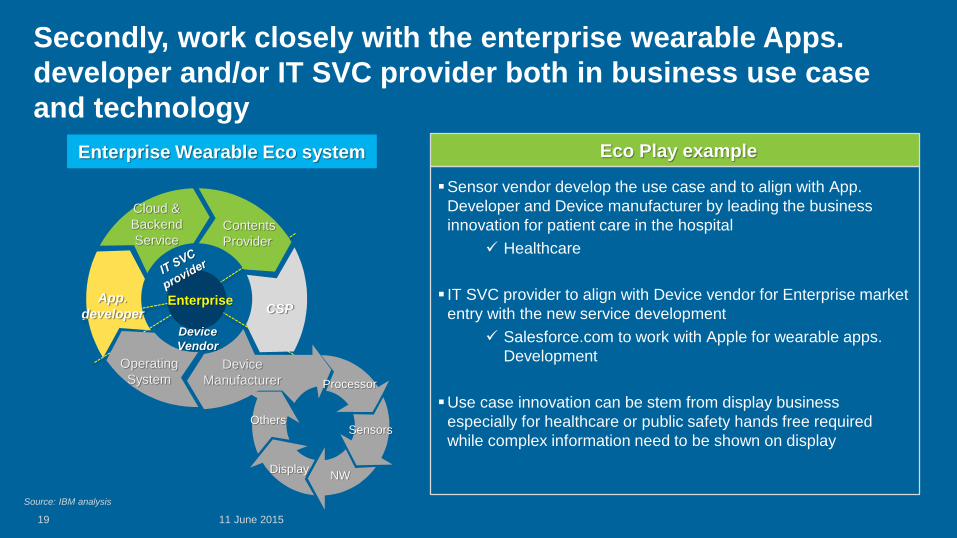

Secondly, work closely with the enterprise wearable Apps.

developer and/or IT SVC provider both in business use case

and technology

Cloud &

Backend

Service

CSP

Contents

Provider

App.

developer

Operating

System

Sensors

Processor

NWDisplay

Others

Device

Manufacturer

Enterprise

Device

Vendor

Enterprise Wearable Eco system Eco Play example

Sensor vendor develop the use case and to align with App.

Developer and Device manufacturer by leading the business

innovation for patient care in the hospital

Healthcare

IT SVC provider to align with Device vendor for Enterprise market

entry with the new service development

Salesforce.com to work with Apple for wearable apps.

Development

Use case innovation can be stem from display business

especially for healthcare or public safety hands free required

while complex information need to be shown on display

Source: IBM analysis

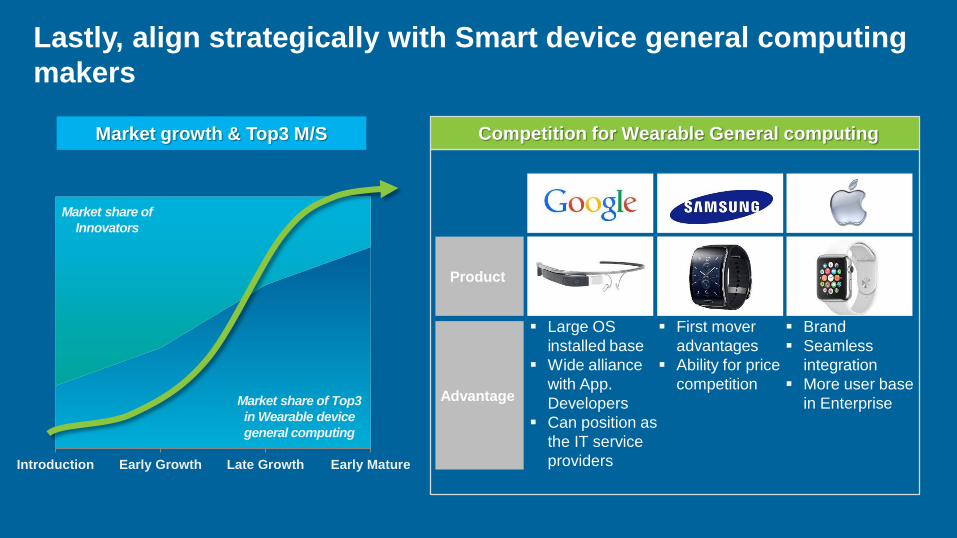

Lastly, align strategically with Smart device general computing

makers

Introduction Early Growth Late Growth Early Mature

Large OS

installed base

Wide alliance

with App.

Developers

Can position as

the IT service

providers

Market share of Top3

in Wearable device

general computing

Competition for Wearable General computingMarket growth & Top3 M/S

First mover

advantages

Ability for price

competition

Brand

Seamless

integration

More user base

in EnterpriseAdvantage

Product

Market share of

Innovators

Thank you

![Wearable [REDACTED]](https://img.dokumen.tips/doc/110x75/559f58221a28abf0078b482f/wearable-redacted.jpg)