Embed Size (px)

Citation preview

Options for Large Companies

WORKING WITH

STARTUPS

Bill Youstra

@youstra

The WhySITUATION

Accelerating advances in technologyExplosion of platforms, form factors &

APIsLow capital requirements for startupsEasy access to capitalCorporate imperative to experiment

(find a better model) is driving M&A exits

VELOCITY AND IMPACT OF EMERGING COMPANIES ARE

GROWING FAST

SourcingProductionPackagingTargetingDistributionMonetization

THIS EFFECTS ALL ASPECTS OF THE ECO-SYSTEM

Strategic advantages for early adoptersInstitutional awareness of experiments

& best practicesEnterprise value gain in core business

or equity share of partnerDistraction of engagement & dead-ends

with partner initiatives

CREATES BOTH OPPORTUNITIES & THREATS FOR LARGE CO’S CORE BUSINESS

Diffi cult for managers to monitor & assess all developments

Too many meeting requests & inbound calls

Decentralized – requests scattered across company w/ little shared learning

All compounded by FOMO - fear of missing out

BUT: DISCOVERY IS INEFFICIENT

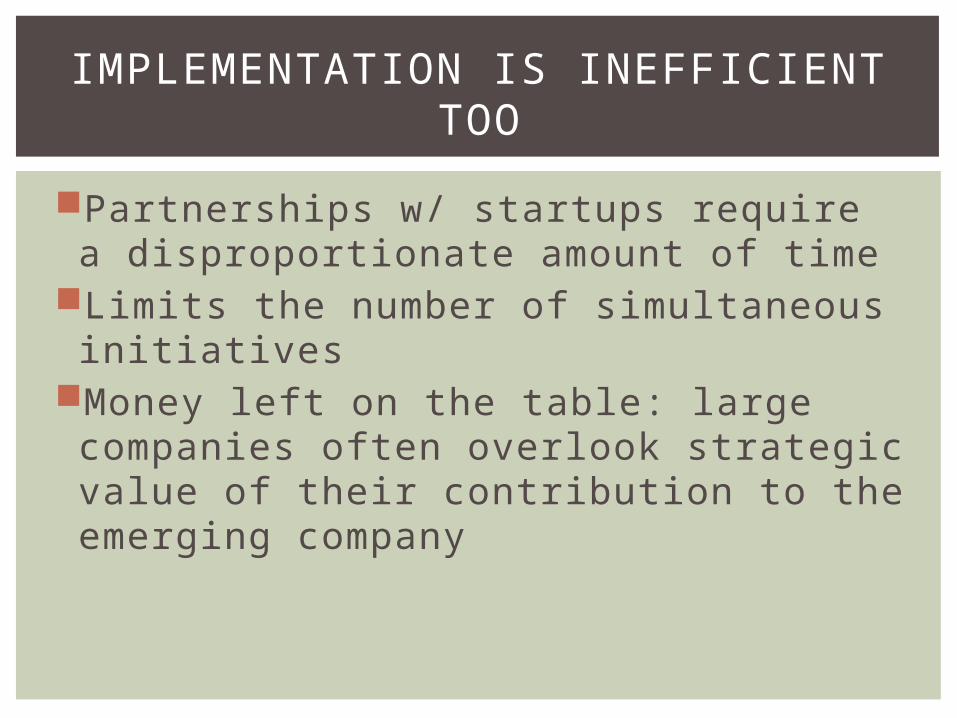

Partnerships w/ startups require a disproportionate amount of time

Limits the number of simultaneous initiatives

Money left on the table: large companies often overlook strategic value of their contribution to the emerging company

IMPLEMENTATION IS INEFFICIENT TOO

You need a centralized solution…

…to proactively scan & score

opportunities…

…and secure strategic & product benefits…

…with minimal distraction to operating

teams.

CONCLUSION

and what not to do…

WHAT TO DO

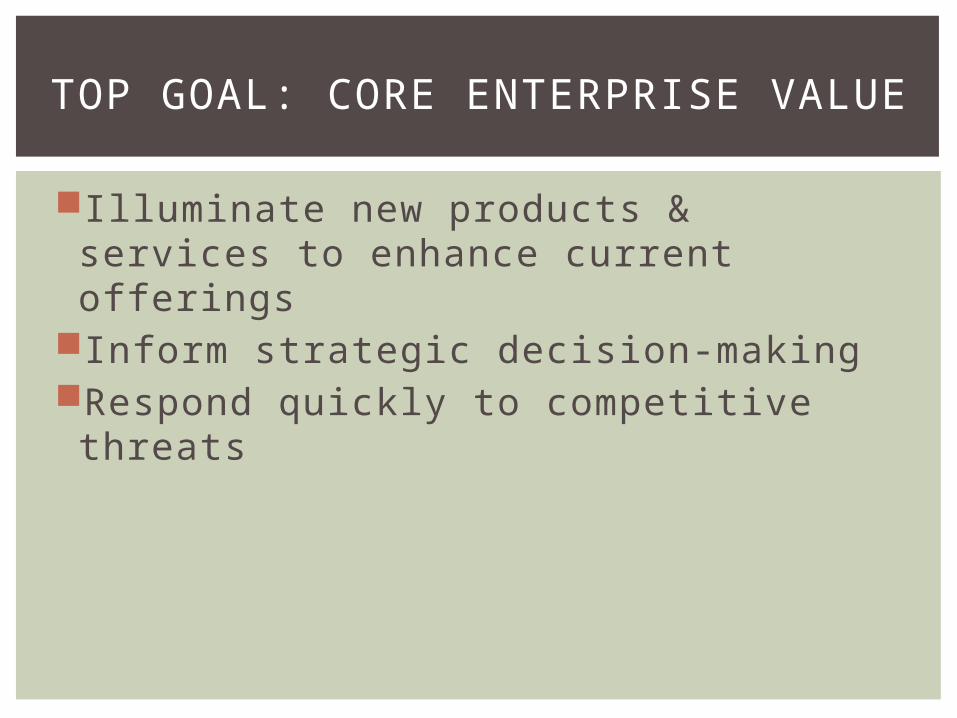

Illuminate new products & services to enhance current offerings

Inform strategic decision-makingRespond quickly to competitive threats

TOP GOAL: CORE ENTERPRISE VALUE

Trying to play VC (optimize for equity returns) is a mistake

There is significant potential financial upside

However: Emphasis is on “potential”Financial, time & opportunity costs are high

WHAT ABOUT EQUITY RETURNS?

VCs in aggregate do only a fair job picking winners

VCs have historically underperformed as an asset class, with a handful of exceptional huge outcomes for a handful of partnerships making the difference

Yet they enjoy superior deal flow, more capital, larger diversification and are much more attractive to entrepreneurs

Can you really do better?

PICKING WINNERS IS HARD

There is a natural conflict between investment returns and operational excellenceExampleGSI’s early investment in PowerReviews complicated the product manager’s ability to later switch to Bazaarvoice. Making the switch damaged the enterprise value of PowerReviews and the reputation of GSI as an attractive investor for startups.

FURTHER: OPERATIONAL CONFLICT

2-3 people focus on innovations for core business strategy and operations: “BD not VC”

Manage centralized intake to screen prospective early-stage partners

Liaise proactively with startup community, conferences & influencers

Understand priorities of internal operating units

Present “Innovation Seminars” and “Demo Days” of concepts or startups to operating groups

Establish boilerplate deal terms (warrants, exclusivity)

SUGGESTED APPROACH: INNOVATION GROUP

Conduct ad hoc research for execs & boardDeconstructing competitor’s innovationsPreliminary research on prospective initiatives

Serve as internal innovation lab, building prototypes for department initiatives

OPTIONAL: INNOVATION GROUP COULD

If you still want to play VC…

APPENDIX

Corporate InvestmentsIncubatorAccelerator

OTHER OPTIONS (NOT RECOMMENDED)

Establish “Media Co Ventures” armStaff with 2-3 investing professionals

with domain expertiseOperate as in-house VCFocus on Series A & B investments,

reserving 50% of capital for follow-on

CORPORATE INVESTMENTS

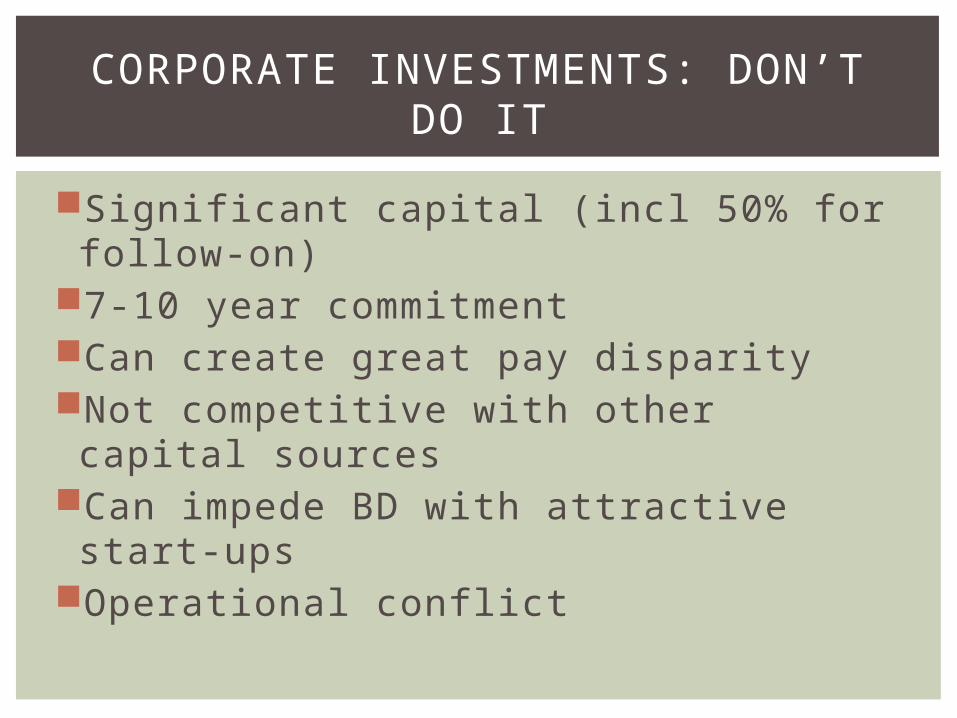

Significant capital (incl 50% for follow-on)

7-10 year commitmentCan create great pay disparityNot competitive with other capital

sources Can impede BD with attractive start-upsOperational conflict

CORPORATE INVESTMENTS: DON’T DO IT

You can attract uniquely attractive deal-flow

Your business is willing to aggressively embrace DNA transfers from startups

You have at least $200m available capital over 7 years

You anticipate initiating a second $200m fund in 4-5 years

You “firewall” the investing group (like Google Ventures)

CORPORATE INVESTMENTS: PROCEED IF

Cultivate cohorts of seed-stage ventures that are generated internally or externally

Offer cash, offi ces, overhead, support & expertise for 3-6 month sessions

Usually $15-80K for 5-20% equityStaff with 3-6 professionals and a network

of advisorsStage “Demo Day” to introduce hatchlings

to operating groups and external investors

INCUBATOR

Incubator structure limits the number of new ideas you’ll see

Generally too immature to integrate into core business for 12+ months

Very high risk; seed stage ventures have high mortality rate and pivot rate; they may easily pivot out of your interest range

On average, the most successful startups are from second-timers who eschew incubators

This model underperforms for all but the very top incubators (Y-Combinator)

INCUBATOR: DON’T DO IT

Don’t. It’s a seductive notion but ultimately makes no sense.

INCUBATOR: PROCEED IF

Similar to incubator, but with later stage seed ventures; all externally-generated

Ventures are beyond the napkin stage; have a concept, prototype and have engaged with customers

ACCELERATOR

Same downsides as incubators albeit with less risk

ACCELERATOR: DON’T DO IT

You can sponsor a third-party accelerator with terms that provide exclusive benefits

ACCELERATOR: PROCEED IF

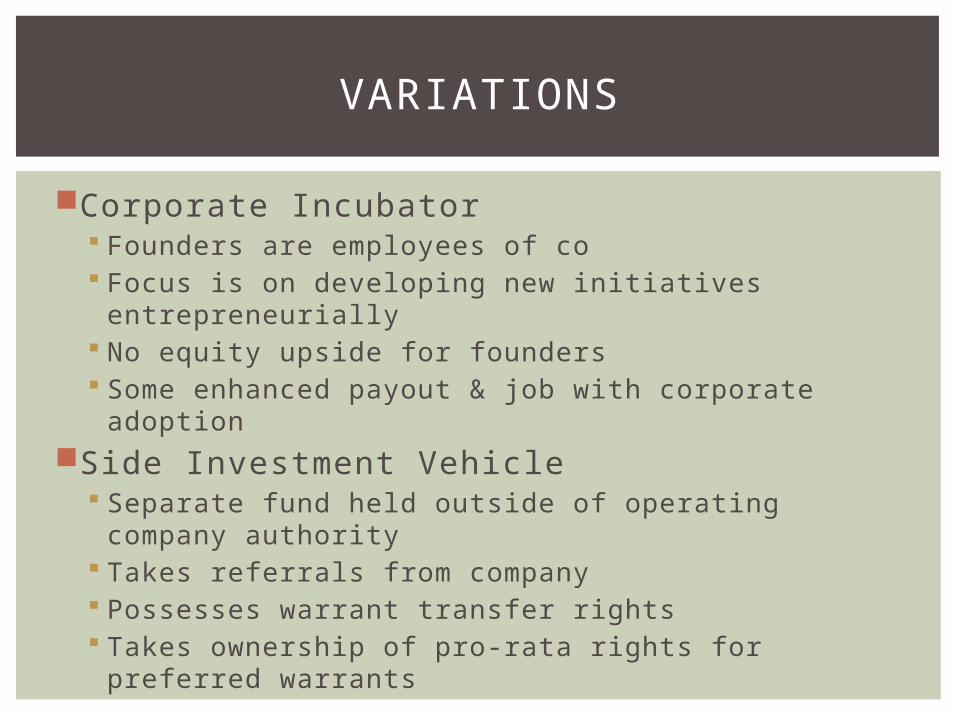

Corporate Incubator Founders are employees of co Focus is on developing new initiatives

entrepreneurially No equity upside for founders Some enhanced payout & job with corporate adoption

Side Investment Vehicle Separate fund held outside of operating company

authority Takes referrals from company Possesses warrant transfer rights Takes ownership of pro-rata rights for preferred

warrants

VARIATIONS