Embed Size (px)

Citation preview

Helping Clients Keep More of what they Earn

1

Advisory Services

Litigation Services

Compliance Services

BT ASSOCIATES

Pro

file

Ad

• Serv• Cent• Cust• Cros• Adv‘exp

dvisory serv

vice Taxtral Excisetomsss Credit Revisory Servicports’ and ‘im

ices

viewces onmports’

Litigati

•Indexingall transcdocumentand anydocumentimportant•Pickinginformatiodocumentthis informsummariedocument•Legal rese•Document

3

ion Services

and organiscripts, evidets, depositiy other lets thatt to a law firmup importon from lets and analyzmation to cres of lets.earchts drafting

WelitigWemarevtax seewel

singnceonsegalare

m.tantegalzingeateegal

• Vmft

• Sh

• RA

• Mc

Helping Client

e focus ongation and coe also assking represeenue autho

concessieking clarificll as federal

Compliance

VAT/CSTmonthly/quaf‐yearly depthe state invService taxhalf‐yearly.Refunds oAuxiliary DutMaintenancecenvat credit

ts Keep More o

n legal aompliance sist our clieentations beorities for oons, relie

cations at slevel.

Services

returnarterly/halpending onolvedreturn –

f Specialties (‘SAD’)e of thet registers

of what they E

dvisory, ervices. ents in fore the btaining

ef and state as

Earn

Thcuta

Urechthcl

Int

he impact oustoms dutieariff barriers

pfront identegulatory aphain. We ashat there areients assess

C

Ad

bo

ternation

of customs des in accordis changing

tification of pprovals thassist our cliee no hidden s and mitiga

ustoms class

dvisory & corelating

onding/ware

nal Transa

duties is signance with Wrapidly. Reg

the impact t may be re

ents in addrecosts or sute risks that

sification

mpliance g to ehousing

EvaluatingRegionaAgree

actions

nificant on cWTO commitgional Trade

of customsequired is cessing issuerprises. Wemay pose a

Va

Anti‐dsafeg

advisory/

g impact of al Trade ments

4

cross-borderments. How

e agreements

s duties as ritical if impes covering not only ide

a business c

aluation

umping andguard duty /representat

AdvIncenti

aAutho

r transactionwever, the na

s are increas

well as tarports are an

all these arentify plannihallenge.

ex(esc

ion

Comrevi

vice on varioive schemesas Advance orisation, EP

etc.

Helping Client

ns. The trenature and forsingly being

riff and non important p

reas in a hoing opportun

Incentive aemption sche.g. EOU, SEZchemes), pro

imports

mpliance/diaew for expo

us s such

PCG,

ts Keep More o

d today is rerm of tariff a entered into

n-tariff barriepart of your

olistic mannenities, but al

nd hemes Z, STP oject

agnostic rt units

of what they E

educing nd non-o India.

ers and r supply er, such lso help

Earn

Helping Clients Keep More of what they Earn

5

Procurement, manufacturing and distribution

In India, the indirect taxes applicable to the procurement, manufacturing and distribution functions are complex since they involve an inter-play of taxes that apply at different stages/transactions and at different levels i.e. central, state and local. A number of indirect taxes typically apply to transactions in the supply chain, including Excise duty, Sales tax (including works contract tax and lease tax), Service tax and VAT. We provide a range of services to our clients whose businesses involve procurement, manufacturing and /or distribution. These include:

• Assistance in establishing units, obtaining necessary government approvals

• Classification, valuation and dutiability

• Contract negotiation and structuring

• Identification of benefits and concessions

• Developing operating structures for tax optimisation

• National tax administration

• Due diligence and diagnostic review

• Cross credit review under integrated credit regime

• VAT impact analysis and pricing state

Vasaadfroonaceault VAnadiswaannebuanpo

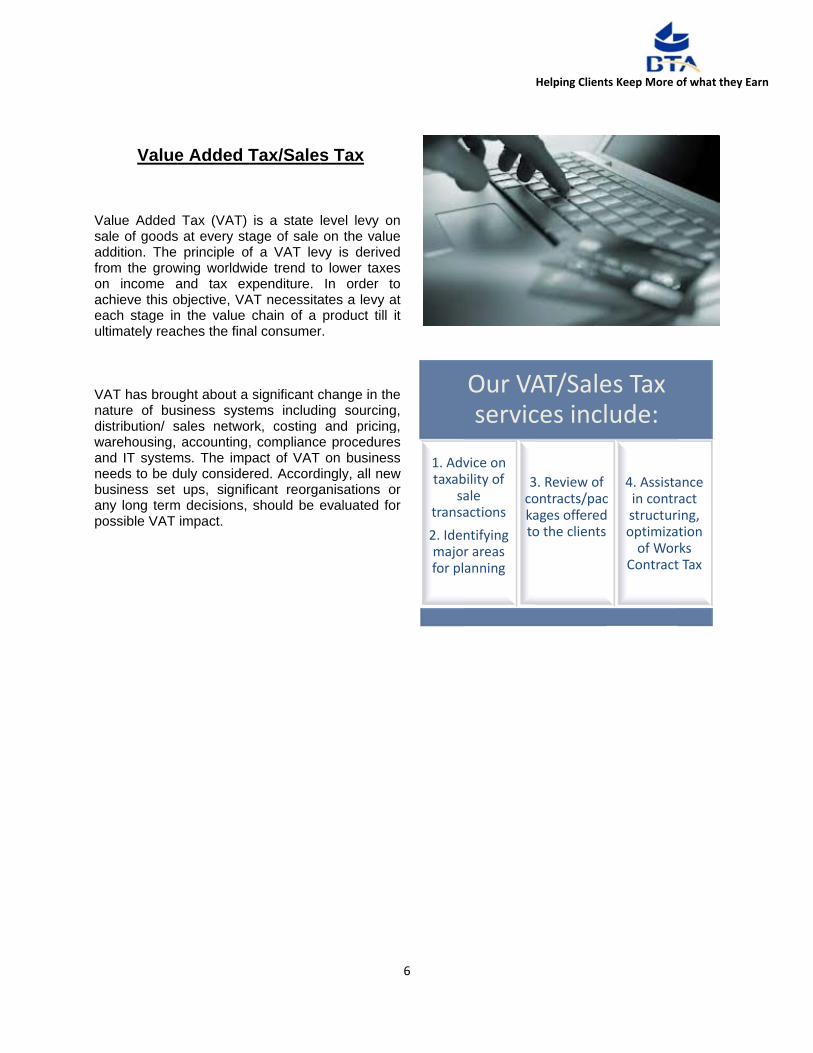

Value

alue Added ale of goodsddition. The om the grown income achieve this oach stage intimately reac

AT has brouature of busstribution/ sarehousing, nd IT systemeeds to be dusiness set ny long termossible VAT

e Added T

Tax (VAT) s at every st

principle owing worldwand tax exobjective, VAn the value ches the fina

ught about a siness systesales netwo

accounting,ms. The impduly conside

ups, signifm decisions,

impact.

Tax/Sales

is a state lage of sale f a VAT lev

wide trend toxpenditure. AT necessitachain of a

al consumer

significant cems includirk, costing , compliancepact of VAT red. Accord

ficant reorgashould be e

s Tax

level levy oon the valu

vy is deriveo lower taxe

In order tates a levy aproduct till

r.

change in thng sourcingand pricing

e procedureon busines

ingly, all newanisations oevaluated fo

6

on e d

es to at it

e g, g, es ss w or or

1. Advtaxab

satransa2. Idenmajofor pl

Our VAservic

vice on bility of ale actionsntifying r areas anning

3cokato

Helping Client

AT/Saleces incl

3. Review of ontracts/pacages offeredo the clients

ts Keep More o

es Tax ude:

c

4. Assistain contrstructurioptimizaof Wor

Contract

of what they E

ance act ing, tion rks t Tax

Earn

Helping Clients Keep More of what they Earn

7

Special Economic Zones

Special Economic Zones or SEZs are being created to provide an internationally competitive environment for export promotion and encouraging investment. SEZs have been provided various tax and duty exemptions and concessions. The importance of SEZs as a business model is evidenced by the fact that numerous business houses (both Indian and foreign) are setting up large SEZs in various parts of the country.

Our offerings with respect to the SEZ scheme are:

• Advisory assistance, identification of benefits and exemptions under the SEZ scheme

• Assistance in development of/setting up of SEZs/units in SEZs

• Assistance in liaison/representation before Central/State government officials for obtaining requisite approvals.

Engineering Procurement and Construction Contracts

An Engineering Procurement and Construction (EPC) contract in India is significantly impacted by indirect taxes. Customs duties, Sales tax/VAT including Works contract tax, Service tax, Research & Development cess, Octroi/Entry tax and Cenvat (Excise Duty) are all likely to impact these projects.

We help clients in managing and structuring their EPC contracts efficiently. The specific areas of assistance are enumerated below:

• Assistance in structuring tax efficient bid/notice inviting tender

• Review/restructuring of contracts for tax efficiency

• Advisory assistance pertaining to optimizing the impact of indirect taxes

• Assistance in obtaining registrations and approvals

• Comprehensive range of compliance services, including registrations and management of all tax related obligations

• Identification of benefits and exemptions

• Assistance in proceedings and litigation support

Helping Clients Keep More of what they Earn

8

Health checks and operational reviews

We provide a one-time review of the comprehensive indirect tax compliance and positions taken by our clients to ensure that their company’s indirect tax function operates with maximum efficiency. Our services not only include risk assessments and evaluations but also highlighting potential areas of exposure that may be encountered by business (compliance as well as structure of operations). We systematically share the best practices and industry knowledge to ensure our ideas and solutions address our clients’ concerns. The services which we provide in this area are:

• One-time review of the comprehensive indirect tax compliance and positions taken(Customs, Excise, Service Tax, Sales Tax and other ancillary indirect tax laws)

• Evaluation of existing business models in the context of optimising indirect taxes

• Risk assessment of practices (review of contracts, documents, declarations, processes) being followed by the company to identify areas of exposure

• Advice on corrective measures that could be adopted, to mitigate risks

• Identification of planning areas to optimize tax incidence

• Highlighting potential areas of exposure (compliance as well as current structure of operations) and providing assistance on resolution.

一椀渀攀琀攀攀渀

![[1] Teacher’s Profile Employee's Name BHOJAK HINABEN …[1] Teacher’s Profile Employee's Name BHOJAK HINABEN PANALAL Designation ASSOCIATE PROFESSOR Department SANSKRIT Address](https://img.dokumen.tips/doc/110x75/60686ea70b379d44154642ed/1-teacheras-profile-employees-name-bhojak-hinaben-1-teacheras-profile-employees.jpg)