Embed Size (px)

Citation preview

When a person responsible for paying any income deducts Income Tax on income at the

time of payment of income/credit, it is called ‘Deduction of Tax at source-TDS’ The provisions

related to TDS are covered under Chapter XVII-B of the Income Tax Act, 1961.

Coverage of the Chapter Deduction of tax on specified payment at specified rate

Deposit tax within the time limit as prescribed

File return of tax deducted at source

Issue certificate of deduction of tax at source

Processing of TDS return

Consequences of non-compliance

Introduction to TDS

The Tax on Total Income is collected in two ways1) Deduction of Tax at Source (TDS)

2) Advance Tax /Self assessment tax

1

The CBDT, in the light of the decision of the Hon'ble Rajasthan High Court in the case

of Commissioner of Income Tax(TDS) Jaipur Vs. M/S Rajasthan Urban Infrastructure,

examined the matter afresh and decided that wherever, in terms of the agreement/

contract between the payer and the payee, the service tax component comprised

in the amount payable to a resident is indicated separately, the tax shall be

deducted at source under Chapter XVII-B of the Act on the amount paid/ payablewithout including the service tax component.

Clarification on TDS on service tax component(CIRCULAR NO. 1/2014, DATED 13-1-2014)

2

In case of resident Payee /Deductee:

Payee/Deductee Applicability of Surcharge and Education

cess

1)Companies No surcharge or education cess shall be

added

2)Any other assessee No surcharge or education cess shall be

added to the prescribed rate of TDS except

salary in which surcharge @10% and

education cess @ 3% is required to be

deducted if salary exceed Rs. 1 crore.

Surcharge and education cess on rates of TDS prescribed

3

Payee/Deductee Applicability of Surcharge and Education cess

1)Foreign Companies Rate of TDS shall be increased by:1)Surcharge @ 2% (where payment made or to be made which is subject

to tax deduction during F/Y exceed 1 Crore but does not exceed 10

Crore).

2)Surcharge @ 5% (where payment made or to be made which is

subject to tax deduction during F/Y exceed 10 Crore

3)Education cess of 3% in all cases.

2)Any other assessee Rate of TDS shall be increased by:1)Surcharge @ 10% (where payment made or to be made which is

subject to tax deduction during F/Y exceed 1 Crore) .

3)Education cess of 3% in all cases.)

In case of non-resident Payee /Deductee:

Surcharge and education cess on rates of TDS prescribed

4

In case the deductee fails to submit the PAN to the Deductor, the Deductor shall beliable to Deduct TDS at the higher of the following Rates-

rate specified in the relevant provision of this Act; or

at the rate of twenty per cent.

Requirement to Furnish PAN (Section 206AA)

5

The time of Deduction in all the Sections shall be Payment or credit (whichever isearlier) of such Income to the account of the payee except the below mentioned

Section where the time of the deduction shall be payment to the payee-

Section 192 – TDS on salaries

Section 194B-TDS on winning from Lottery or Cross word puzzle

Section 194LA-TDS on payment of Compensation on Acquisition of Immovable

Property

Time of Deduction of TDS

6

No deduction of TDS shall be made on the payments of the nature specified below,

in case such payment is made by a person to a bank excluding Foreign Bank,

namely-

Bank Guarantee Commission

Cash Management Service Charges Depository Charges on maintenance of DEMAT Charges

Charges for warehousing services for Commodities

Underwriting Service Charges

Clearing Charges(MICR Charges)

Credit card or Debit card commission for transaction between merchantestablishment and acquirer Bank

No Deduction of TDS in certain cases(Section 197A(1F)

read with Notification No. 56/2012)

7

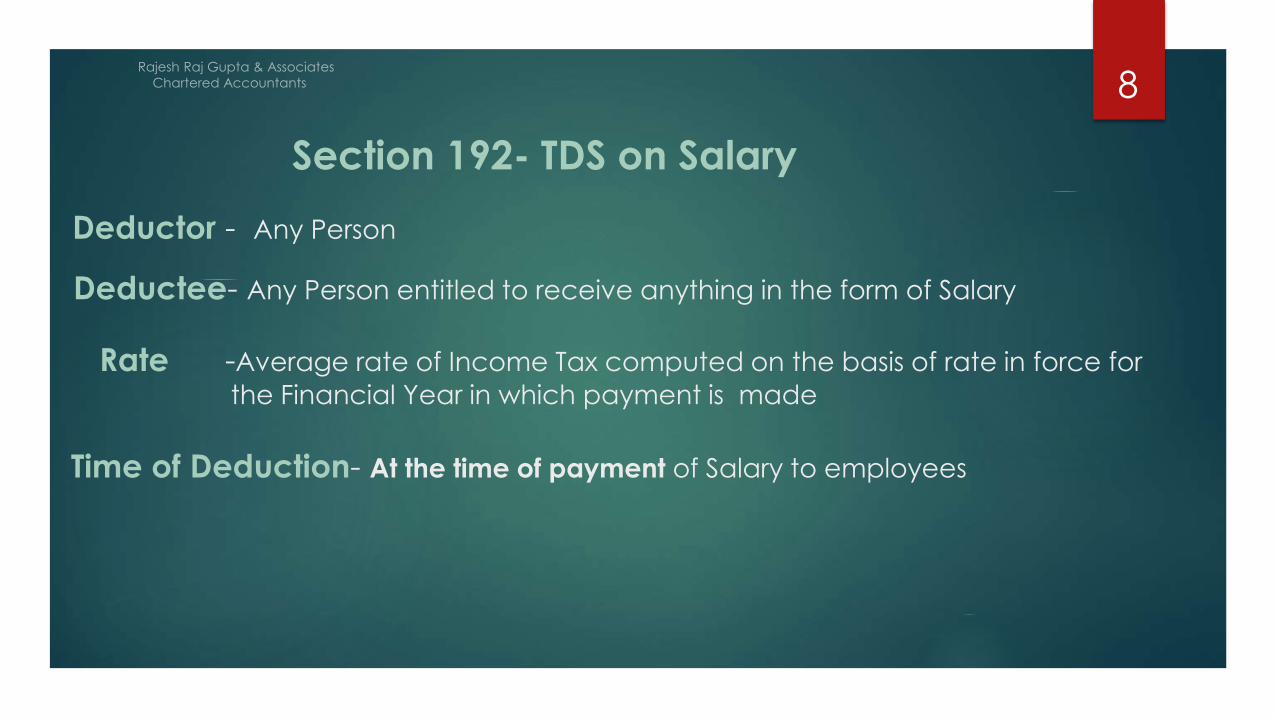

Section 192- TDS on Salary

Deductor - Any Person

Deductee- Any Person entitled to receive anything in the form of Salary

Rate -Average rate of Income Tax computed on the basis of rate in force for

the Financial Year in which payment is made

Time of Deduction- At the time of payment of Salary to employees

8

Computation of Monthly TDS deductible by the employer

Particulars Amount(Rs.)

Annual Salary X

Add: Value of Perquisites Y

Gross Salary (X+Y)

Add: Any other Income reported by employee Z

Less: Loss on House Property reported by Employee Z1

Gross Total Income (X+Y+Z-Z1)

Less: Deductions Under Chapter VIA(E.g. 80C, 80CCC,80D) P

Total Taxable Income (X+Y+Z-Z1-P)

Section 192- TDS on Salary

9

Computation of Monthly TDS deductible by the employer

Paticulars Amount(Rs.)

Tax on above A

Less: Rebate U/S 87A, if any (Note 1) B

Add: Surcharge, if any C

Add: Education Cess D

Total Tax (E) (A-B+C+D)

Less: Relief u/s 89(Note 2) F

Less: Tax deducted by other Institution and reported by the employee G

Balance Tax Payable (H) (E-F-G)

Monthly Tax Deductible H/12

Section 192- TDS on Salary

10

Special Points to be considered-

Note 1- As per Finance Act, 2013 An Assessee being an Individual Resident whose

Total Taxable Income does not exceed Rs. 5 Lac shall be entitled to

deduction ofRs. 2,000/-

or

Tax on Total Taxable Income, Whichever is lower

Note 2- In case the employee receives the arrear of earlier years then the Tax iscalculated on the income distributed according to which it relates to and

if after distribution of income in relevant years the tax due of all years is less

than the tax due by receipt Method then difference will allowed as

exemption under section 89(1)

Section 192- TDS on Salary

11

Section 193- TDS on Interest on Securities

Deductor - Any Person

Deductee- Any person being Resident only

Rate - 10% on Amount of Interest Payable

Exception to Section 193 No TDS liability upto Rs.5,000/- shall arise on Interest paid by a listed Company on

debentures(whether Listed or Not) in case of non dematerialized form to an

Individual or HUF by an account payee Cheque

No TDS liability on any Security issued in a dematerialized form and listed on a

recognized Stock change in India

No TDS on Interest payable on any Security of Central or State Government

12

Section 194- TDS on Dividends

Deductor - Any Person

Deductee- Any Person being Resident only

Rate -10% on dividend referred to in section 2(22)(e).

Exception to Section 194

Dividend referred to in section 115-O(Interim, Final, Deemed dividend) are exempt

in the hands of shareholder and consequently no TDS are required to be deducted

13

Section 194A- TDS on Interest other than “interest

on Securities”

Deductor - Any Person not being an Individual or HUF

Deductee - Any Person being Resident only

Rate - 10% on Income by way of interest other than Interest on Securities

Exception to Section 194A

An Individual or HUF is required to deduct TDS if he is carrying on any business or profession

and his sales , turnover or gross receipt from such business exceed 1crores and from

Profession 25 lakh during the F/Y immediately preceeding F/Y in which such interest is

credited or paid.

No TDS is required to be deducted if aggregate amount of such income credited or paid

during F/Y to payee does not exceed Rs.5000

14

Deductor - Any Person

Deductee - Any Person

Rate - 30% on Income by way of Winning from Lottery or cross

word puzzles and other game of any sort

The amount of Income paid should exceed Rs.10,000 for deducting TDS Lucky draw

schemes organized by any person shall attract TDS on distribution of prize since it is

in nature of lottery.

Section 194B- TDS on Winnings from Lottery and

Crosswords Puzzles

Special Points to be considered-

15

Deductor - Any Person

Deductee- Any Person being Resident only

Rate -1% where payment is made or credited to a person being an Individual or

HUF.

-2% where payment is made or credited to a person other than an

Individual or HUF

Exception to Section 194C

No TDS is required to be deducted on payment made or credited to Transport

operator during the course of business of plying, hiring or leasing goods carriage,

provided he furnishing of his permanent account number. However if the PAN is not

provided than tax @ 20% is required to be deducted.

Goods carriage” means any motor vehicle for carriage of goods.

Section 194C- TDS on Payment to Contractor

16

No TDS is required to be deducted when the amount to be paid or credited to

contractor does not exceed Rs.30,000 however if aggregate amount of payment

to be made to contractor in a F/Y exceed Rs.75,000 then TDS is required to be

deducted.

Section 194C- TDS on Payment to Contractor

Maximum Limit for Non Deduction of TDS

S.No Situations Whether TDS deductible

1 Single Contract of Rs. 30,000/- in a year No

2 Two Contracts of Rs. 30,000/-each in a year No

3 Three Contracts of Rs. 30,000 each in a year TDS deductible on s.90,000/-

4 Single Contract of Rs. 40,000 in a year Yes

5 Five Contracts of Rs. 15000 each in a year No

6 Single Contract of Rs. 75,000/- Yes

17

Contract shall include sub-contract.

General Points-

Definition of Work for the purpose of Section 194C

Work shall include advertising, broadcasting, including production of programs for

such broadcasting or telecasting, carriage of goods or passengers by any

mode of transport other than by railway catering, manufacturing or supplying a

product according to the requirement or specification of a customer by using

material purchased from such customer but does not include if material ispurchased from person other than customer.

Section 194C- TDS on Payment to Contractor

18

Section 194D- TDS on Insurance Commission

Deductor - Any Person

Deductee- Any Person being Resident only

Rate - 10% on any Income by way of remuneration or reward, whether by way of

commission or otherwise, for soliciting or procuring insurance business.

No TDS is required to be deducted when aggregate amount of such Income credited or paid

or likely to be credited or paid during the F/Y does not exceed Rs.20,000.

Maximum Limit for Non Deduction of TDS

19

Deductor - Any Person not being an Individual or HUF

Deductee- Any Person being Resident only

Rate -10% on Income by way of Commission or Brokerage not being an

Insurance Commission referred to in section194D

No TDS is required to be deducted when the amount to be paid or credited does not

exceed Rs.5,000 during a F/Y.

An Individual or HUF is required to deduct TDS if he is carrying on any business or profession

and his sales , turnover or gross receipt from such business exceed 1crores and from Profession

25 lakh during the F/Y immediately preceeding F/Y in which such interest is credited or paid.

Section 194H- TDS on Commission or Brokerage

Maximum Limit for Non Deduction of TDS

20

TDS on commission/ Supplementary commission received by Travel Agent fromAirlines - The commission received by the Travel Agent from the Airline shall be

subject to the TDS u/s 194 H and the TDS shall be deducted on the Commission

portion i.e. difference between the airfare fixed by the airlines and the price at which

agents are enabled to sell the tickets.

Commission to employees will form part of salary income and is liable to TDS u/s 192

and not under this section.

Section 194H- TDS on Commission or Brokerage

Special Points-

21

Deductor - Any Person not being an Individual or HUF.

Deductee- Any Person being Resident only

Rate -2% for use of any machinery or plant or equipment.

-10% for use of any land or building or land appurtenant to building (including

factory building) or furniture or fittings.

-

If the aggregate amount of such payments to be made in a F/Y exceed Rs.1,80,000 then TDS is

required to be deducted.

Maximum Limit for Non Deduction of TDS

Section 194I- TDS on Rent

22

-

An Individual or HUF is required to deduct TDS if he is carrying on any business or profession

and his sales , turnover or gross receipt from such business exceed 1crores and from

Profession 25 lakh during the F/Y immediately preceeding F/Y in which such interest is

credited or paid.

Where the share of each co-owner in property is definite and ascertainable, the limit of Rs.

1,80,000 will be applicable to each co-owner separately.

TDS on non refundable Security Deposit- No TDS is required to be deducted at the time of

payment of security deposit since it cannot be treated as advance rent however it is

required to be deducted when security deposit is to be adjusted.

TDS is required to be deducted on advance payment of rent.

TDS on Taxes borne by the Tenant- If Municipal tax, ground rent are born by tenant no tax

will be deducted on such sum.

Section 194I- TDS on Rent

General Points-

23

Deductor - Any Person

Deductee- Any Person being Resident only

Rate -1% on payment made for purchase of immovable property.

It is not necessary that the property should be situated in India.

In case section 194-IA is applicable the purchaser is not required to obtain TAN .

Every person purchasing property of Rs. 50 lakh or more would have to deduct TDS @1% of

payment made to seller on or after 01.06.2013.

Immovable property means Land (other than agricultural land) or any building or part of

building

If the sellers jointly owns a property and sells for a total consideration of Rs.50 lakh then this

section applies even if each co-owners consideration is less than Rs.50 lakh

Section 194IA-Payment on transfer of certain

immovable property other than agricultural land

General Points-

24

Deductor - Any Person not being an Individual or HUF

Deductee- Any Person being Resident only

Rate -10% on payment made as

fees for professional services, or

Fees for technical services, or

Royalty, or

Any sum referred to in clause(va) of Section 28, or

payment by whatever name called other than salary paid to Director

of company.

-

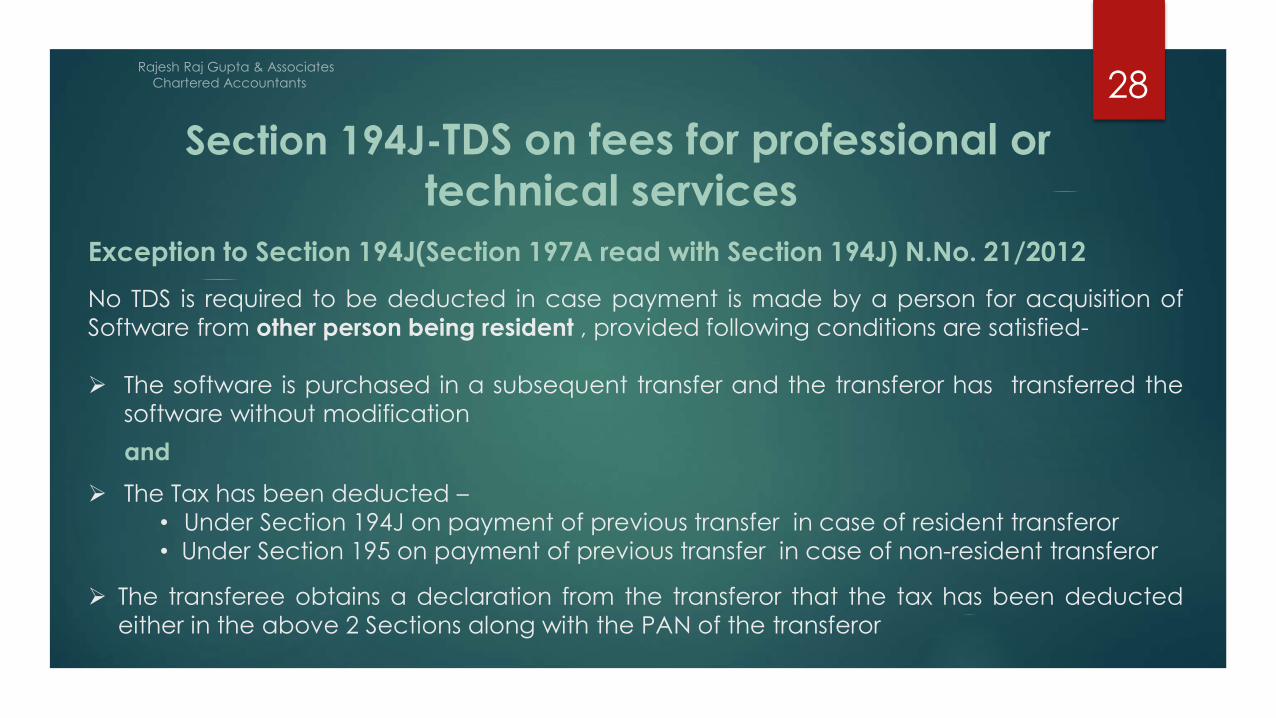

Section 194J-TDS on fees for professional or

technical services

25

-

An Individual or HUF is required to deduct TDS if he is carrying on any business or profession

and his sales , turnover or gross receipt from such business exceed 1crores and from

Profession 25 lakh during the F/Y immediately preceeding F/Y in which such interest is

credited or paid.

However such Individual or HUF shall not be liable to deduct TDS on sum by way of fees for

professional or technical services if such sum is paid exclusively for personal purpose.

Section 194J-TDS on fees for professional or

technical servicesMaximum Limit for Non Deduction of TDSNo TDS is required to be deducted when the amount to be paid or credited does not

exceed Rs.30,000 during a F/Y other than for payment made to director of company.

No threshold limit has been provided for the payments made to the Directors, even if the

sitting fees of Rs. 5,000/- is paid, the company is liable to deduct TDS on such payments.

General Points-

26

No TDS on professional fees paid by Non-Resident to the chartered

accountant, lawyers advocate or solicitor if non-resident does not

have any agent or business connection in India.

Royalty includes payment for purchase of computer software.

Section 194J-TDS on fees for professional or

technical services

General Points-

27

Section 194J-TDS on fees for professional or

technical services

Exception to Section 194J(Section 197A read with Section 194J) N.No. 21/2012

No TDS is required to be deducted in case payment is made by a person for acquisition of

Software from other person being resident , provided following conditions are satisfied-

The software is purchased in a subsequent transfer and the transferor has transferred the

software without modification

and

The Tax has been deducted –

• Under Section 194J on payment of previous transfer in case of resident transferor

• Under Section 195 on payment of previous transfer in case of non-resident transferor

The transferee obtains a declaration from the transferor that the tax has been deducted

either in the above 2 Sections along with the PAN of the transferor

28

Deductor - Any Person

Deductee- Any Person being Resident only

Rate -10% of any sum being in nature of compensation or enhanced compensation

on account of compulsory acquisition under any law for time being in force.

-

No TDS is required to be deducted when the amount to be paid or credited does not

exceed Rs.2,00,000 during a F/Y.

Section 194LA-Payment of compensation on

acquisition of certain immovable property*

Maximum Limit for Non Deduction of TDS

General Points-

*Immovable property means Land (other than agricultural land) or any building or part of

building.

29

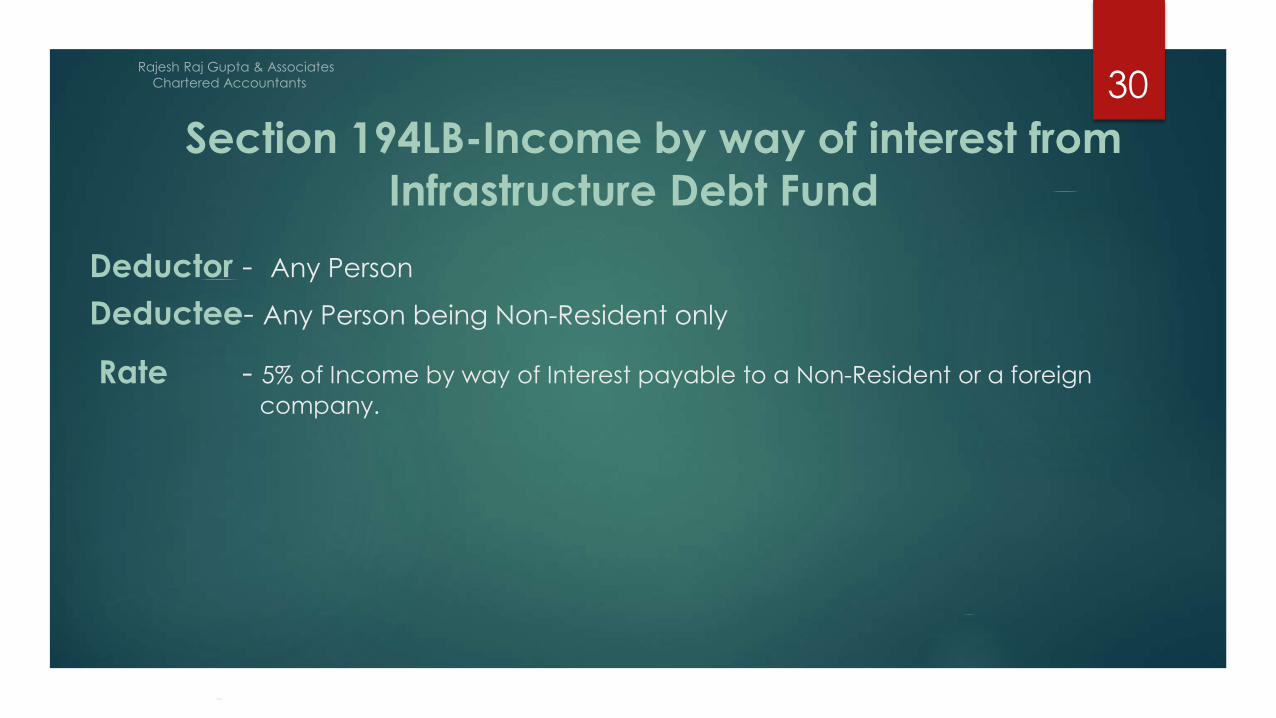

Deductor - Any Person

Deductee- Any Person being Non-Resident only

Rate - 5% of Income by way of Interest payable to a Non-Resident or a foreign

company.

-

Section 194LB-Income by way of interest from

Infrastructure Debt Fund

30

Deductor - Any Person

Deductee- Any Person being Non-Resident only

Rate -5% of Income by way of Interest payable to a Non-Resident or a foreign

company.

-

The Interest under this Section shall be the Income by way of Interest payable by Indian Co.

Interest payable on money borrowed at any time on or after 1st July, 2012 but before 1st day

of July, 2015, in foreign currency, from a source outside India under a loan agreement or by

way of issue of Long term Infrastructure bonds, as approved by Central Government in this

behalf.

The interest shall be Income to the extent it does not exceed the amount of interest

calculated at rate approved by Central Government in this behalf .

Section 194LC-Income by way of interest from Indian

company

Special Points-

31

Deductor - Any Person

Deductee- Any Person being Non-Resident only

Rate - Income by way of Interest, Royalty or any other sum payable to a foreign

company or Non- Resident not being Income chargeable under head salary or

interest covered under section 194LB, 194LC, 194LD shall be deductible at the

rate in force.

-

Any person responsible for paying to a Non-Resident or to Foreign Company Interest or any

other sum shall furnish the information regarding the same in such form and manner as may

be prescribed.(Form 15CA and 15CB).

Section 195-TDS on other sum(Paid to Non

resident)

Special Points-

32

No TDS is required to be deducted on payment made by a person to:

Government

Reserve bank of India

A corporation established by or under a Central Act which is, under any law for the time

being in force, exempt from income-tax on its income.

A mutual fund specified under section 10(23D).

Where such sum is payable by way of interest in respect of any securities owned by it or in

which it has full beneficial interest, or any other income accruing or arising to it.

Section 196-No TDS on Interest or other sum payable to

government, reserve bank or certain corporation

33

Every person, being a seller shall, at the time of debiting the amount payable by the buyer to

the account of buyer or at the time of receipt of such amount from the said buyer, which ever

is earlier, collect from buyer a sum equal to:

Nature of goods % of purchase price

Alcoholic liquor for human consumption 1%

Tendu leaves 5%

Timber obtained under a forest lease 2.5%

Timber obtained by any mode other than under a forest lease 2.5%

Any other forest produce not being timber or tendu leaves 2.5%

Scrap 1%

Minerals, being coal or lignite or iron ore 1%

Lease or license or contract or otherwise transfers any right or

interest in parking lot, toll Plaza, Mine, Quarry for use of such areas

2%

Section 206C-Tax collection at source

34

TDS is required to be paid to credit of central government within the time given below:

Different situation Time limit for deposit of tax

When payer is the Government or

when payment is made on behalf of

government

TDS is deposited without challan Same day

TDS is deposited with challan On or before 7 days from the end of

the month in which-

i) The deduction is made OR

ii) Income tax is due u/s 192(1A)

When tax is deducted by a person

other than Government

Where the income or amount is

credited or paid in the month of

March

On or before 30th April

In any other case On or before 7 days from the end of

the month in which-

i) The deduction is made OR

ii) Income tax is due u/s 192(1A)

Time limit for payment of TDS/ TCS

35

Credit of TDS under other Section even though the Challan related to a particular Section

Example: The challan used for payment of TDS relevant to Section 192 of the Act can also

be used for the purpose of reporting tax deposited under Section 194 of the Act also.

Credit of TDS admissible in Other Quarters also and if unutilized in the current year,

admissible in future years also

Example: If excess payment of Tax has been made in Quarter 1 of financial year 2013-14,

the same can be used for Quarter 2, 3 &4 of F.Y. 2013-14 as well as for Q1 to Q4 of F.Y.2014-

15. The excess amount of tax paid in Q1 of F.Y.2013-14 can also be used for payment of tax

default of Q1 to Q4 of F.Y.2012-13.

CPC (TDS) Clarification on Deposit of TDS through

multiple Challan

36

If a person fails to pay to the credit of the Central Government,

Tax Deducted at Source

Or

Tax Collected at Source

he shall be punishable with rigorous imprisonment for a term which shall not be less

than three months but which may extend to seven years

Failure to pay the tax collected at source(Sec 276B and

Sec 276BB)

37

Quarter Ending Due Date

30th June 15th July

30th September 15th October

31st December 15th January

31st March 15th May of F/Y immediately following F/Y in

which deduction is made.

Due date for filing TDS/TCS Return

38

Consequences for default in furnishing TDS/TCS Return

Fees for default in furnishing quarterly return of

TDS/TCS(Sec 234E)

Penalty for default in furnishing quarterly return

of TDS/TCS(Sec 271H)

Where a person fails to deliver the quarterly

return of TDS within the time prescribed, then

he shall be liable to pay Rs. 200/- day till the

default continues.

Points to be Noted

Such fees shall not exceed the amount of

TDS/TCS.

The fees shall be paid before furnishing

quarterly TDS/TCS return.

The penalty shall be a minimum of Rs.10,000

and it can extend upto Rs.1,00,000

Points to be Noted

The penalty shall be payable if assessee

Fails to deliver quarterly return of TDS/TCS, or

Furnish incorrect information in quarterly

returns of TDS/TCS.

No penalty shall be payable if the return has

been delivered within 1 year from the time

prescribed for filing the return along with

fees for default U/s 234E and Interest u/s 201

to credit of central government

39

Consequences of Failure to Deduct TDS or deposit TDS

Fails to Deduct TDSAfter Deduction fails to

Deposit the TDS

Assessee in Default

Interest u/s 220 Penalty u/s 221

1% p.m from the month the tax was

deductable/payable till the date of

passing of an order u/s 201(1)

Penalty u/s 221 can be maximum of

TDS not deducted/not paid.

Person Liable to Deduct TDS

40

Any person who fails to deduct the whole or part of the TDS on the sum paid or credited to the

account of a resident shall not be deemed to be an

Assessee in default in respect of such tax if such resident –

Has furnished his return of income u/s 139,

Has taken into account such sum for computing income in such return of Income.

Has paid the tax due on the income declared by him in such return of income.

And the person furnishes a certificate to this effect from a chartered Accountant in such form as

may be prescribed.

Interest leviable in case of non deduction of TDS for Resident Payee

The interest @ 1% per month per month or part of the month from the date the Tax was

deductible to the date of furnishing the return of income by the payee. The Interest shall be

levied on the amount of TDS not deducted/ short deducted by the Deductor.

Consequences of Failure to Deduct TDS or deposit

TDS(Sec201)

41

TDS deducted Late TDS Deposited Late

Interest @ 1% for every month or part of

month on amount of such tax from the

date on which such tax was deductible

to the date on which such tax is

deducted.

Interest @1.5% for every month or part of

month on amount of such tax from the date

on which such tax was deducted to the

date on which such tax is actually paid.

Consequences of Late deduction or late deposit of TDS

Person Liable to Deduct TDS

Such interest is required to be paid before furnishing quarterly return of TDS.

42

Every person liable to deduct tax shall within such period as may be prescribed , furnish a

certificate to the effect that tax has been deducted and specifying the amount so deducted ,

the rate as which tax has been deducted and such other particular as may be prescribed.

Particulars TDS on salary TDS on Non-salary

Form Form 16 Form 16A

Periodicity Annual Quarterly

Due date upto which

TDS certificate should

be issued

31st may of the following

relevant F/Y

15 days from the due date of furnishing

of TDS return i.e. 30th July, 30th October,

30th January, 30th May.

Issue of TDS certificate

43

The following are the various types of corrections that you can make to an accepted regular

TDS/TCS statement:

Update deductor details such as Name, Address of Deductor.

Update challan details such as challan serial no., BSR code, challan tender date, challan

amounts etc.

Update/delete /add deductee details.

Add / delete salary detail records.

Update PAN of the deductee or employee in deductee/salary details.

Add a new challan and underlying deductees.

Revision of TDS Return

44

Processing of Quarterly Returns of TDS(Section 200A)Where a statement of tax deduction at source has been made by a person deducting any

sum, such statement shall be processed in the following manner, namely:—

the sums deductible under this Chapter shall be computed after making the

following adjustments, namely:—

• any arithmetical error in the statement; or

• an incorrect claim, apparent from any information in the statement;

the interest, if any, shall be computed on the basis of the sums deductible as

computed in the statement;

An intimation under the Section 200A for the additional Demand or refund that arisedue to the Centralized processing of returns

Revision of TDS Return

45

Justification Reports-

It is a document which serves as an annexure to the intimation to be sent to the

deductor. Intimation will be sent to the deductor through mail / post but a justificationreport will have to be downloaded from the portal.

The Justification Report specifies the bifurcation of the Demand as stated in the

Intimation u/s 200A.

Conso File-

It is the consolidated data of the statements processed (regular & correction) for the

relevant Financial Year, Quarter and Form Type. It can be downloaded from theTraces Website.

Revision of TDS Return

46

Requirements of Conso File-

In order to download the Conso File following documents are required-

1.Token No. (Acknowledgement No of the Regular return filed)2.Challan No.

3.BSR code of the Bank

4.Challan Date

5.Challan Amount

6.3 Pan No. of the Deductees (Corresponding to the Challan whose revision is tobe done)

Revision of TDS Return

47

Any interest, commission or brokerage, rent, royalty, fees for professional services or fees for

technical services payable to a resident, or amounts payable to a contractor or sub-contractor,

being resident, on which TDS is deductible and such tax has not been deducted or after

deduction has not been paid on or before before 30th September following the year for which

the Return pertains

Provided that where in respect of any such sum, tax has been deducted in any subsequent

year, or has been deducted during the previous year but paid after the due date specified in

Section139(1), 30% such sum shall be allowed as a deduction in computing the income of the

previous year in which such tax has been paid(Amended by F.A. 2014)

Prior to Finance Act, 2014 whole of the expenditure was disallowed if the TDS was not

deposited before 30th Sep and allowed in the year in which it was actually paid.

But Post Finance Act, 2014 only 30% of the total expenditure shall be disallowed and shall be

allowed in the year in which it is actually deposited with the Department

Disallowance of the Expenditure in case of non Deposit of

TDS before the due date of filing of Return u/s 139(1)(As

amended by Finance Act, 2014)

48

49

Thank you

For Queries, Please Contact- CA Rajesh Gupta Email: [email protected]

CA Manoj Kumar Email: [email protected]

![[2014 ITB 8] Finance Act, 2014 - S.A. Salam updates/Finance Act, 2014... · Income Tax Ready Reference Finance Act, 2014 133 [2014 ITB 8] Finance Act, ... 2000) Finance Act, 2014](https://img.dokumen.tips/doc/110x75/5b4c8db67f8b9ab2668b4759/2014-itb-8-finance-act-2014-sa-updatesfinance-act-2014-income-tax.jpg)