Embed Size (px)

Citation preview

Tax Havens &

Recent Retrospective Amendments In Income Tax Act

Discussion On

Vodafone v/s Income Tax Authority

Tax Havens

What Does Tax Haven Means?

A tax haven is a state, country or territory where certain taxes are levied at a low rates or

not at all.

Advantages of Tax Havens

• Levy no significant taxes. Or very low tax rates

• Tax income earned in the country only.

• Some jurisdictions have tax treaties to avoid

double taxation

• Special Tax Incentive for offshore Business

setups

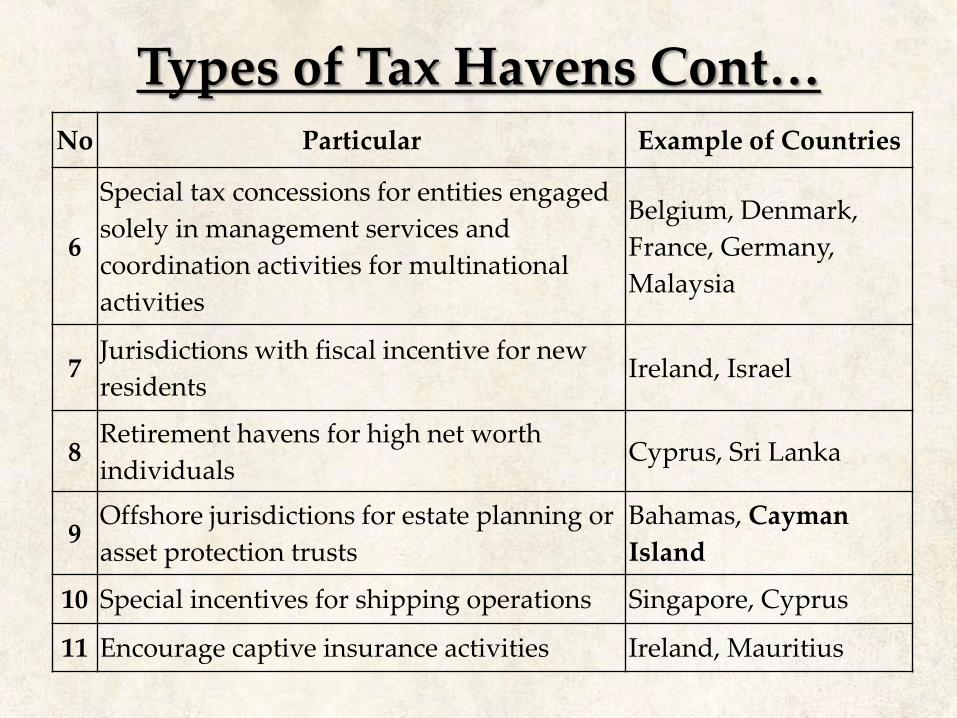

Types of Tax HavensNo Particular Example of Countries

1 No corporate tax Bermuda, Cayman

Island

2 Low-taxed Countries Hong Kong, Ireland,

Jersey

3

Jurisdictions with no (or very few) tax

treaties that offer nil (or very low) or

negotiated tax regimes for offshore entities

British Virgin Islands,

Cook Islands, US

Virgin Islands

4No or nil tax regimes for offshore

companies with the benefit of tax treaties

Cyprus, Malaysia,

Mauritius

5

Fiscally beneficial regimes for intermediary

holding finance or licensing companies

with full benefits of treaty network

Austria, Belgium,

Denmark, France,

Germany

No Particular Example of Countries

6

Special tax concessions for entities engaged

solely in management services and

coordination activities for multinational

activities

Belgium, Denmark,

France, Germany,

Malaysia

7Jurisdictions with fiscal incentive for new

residentsIreland, Israel

8Retirement havens for high net worth

individuals Cyprus, Sri Lanka

9Offshore jurisdictions for estate planning or

asset protection trusts

Bahamas, Cayman

Island

10 Special incentives for shipping operations Singapore, Cyprus

11 Encourage captive insurance activities Ireland, Mauritius

Types of Tax Havens Cont…

An Interesting Issue on Tax Haven !!!

Vodafone Union of India

HTIL

• Hutchison Telecommunications International Limited

• Situated in Hong Kong

• Holding 100% Shares in CGP Investments Holdings Ltd

CGP

• CGP Investments Limited

• Situated in Cayman Island, Mauritius (a tax haven country)

• Holding 67% Shares in HEL

HEL

• Hutch Essar Limited

• Situated in India

• Formed by Merger of HTIL and Essar Group

VIH

• Vodafone International Holdings

• Situated at Netherland

• Subsidiary of Vodafone Group Plc

The Deal – A Diagrammatic View

HTIL(Cayman Island Co.)

VELVodafone Essar Limited

HEL(Indian Co.)

VIH (Vodafone International

Holdings)

CGP(Cayman Island Co.)

Sold 100% holding of CGP to VIH

Renamed as

Apparent UnderstandingLook At Approach

Foreign Company 1

(HTIL)

Sold Foreign Company 2

(CGP)

To Foreign Company 3

(VIH)

Transaction Took Place Outside

India in Foreign Currency

There is no Territorial Nexus

Resultant Capital Gain can’t be taxed in India

Contention Of The Income Tax Dept.Contention 1

Offshore Share Transaction

Result in Transfer of Shares in HEL from HTIL to VIH

Indirect Transfer of Capital Asset Situated in India

Relevant Provision :- S. 9 (1) (i) L-4Income accrues/Arising, Directly/Indirectly through transfer of Capital Asset situated in India = Deemed to accrue/arise in India.

Contention 2

Controlling Interest In HEL is Capital Asset situated in India u/s 2(14)

On account of transfer of shares in CGP Inv Ltd by HTIL to VIH

Controlling Interest of HTIL in HEL gets extinguished

Extinguishment of Right = Transfer u/s 2(47)

Activates S.9(1)(i) L-4

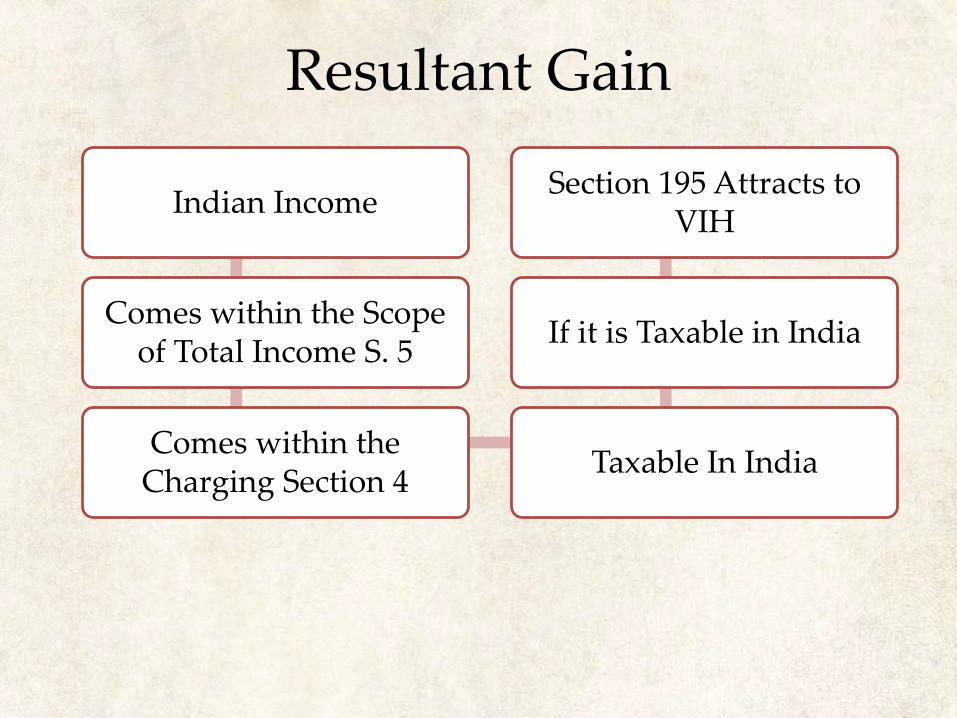

Indian Income

Comes within the Scope of Total Income S. 5

Comes within the Charging Section 4

Taxable In India

If it is Taxable in India

Section 195 Attracts to VIH

Resultant Gain

Action by Income Tax Dept.

Specifies as to why it should not be treated as an Assessee In Default

(AID) U/s 195?

Issued a Show Cause Notice u/s 201

Bombay HC

Filed a Writ Petition

Action By The Assessee

• Challenging the legal validity of the SCN

• Contending that the transaction was only in respect of shares of CGP in Cayman islands; and

• That being a capital asset situated outside India,

• No income had accrued or arisen in India

Decision of Bombay HC

• Bombay High Court Concurred with the Viewpoint of the department

• Bombay High Court refuses to Interfere

• SCN was not Quashed

• Vodafone was, therefore, liable to deduct TDS on the payment made to HTIL and therefore SCN is a Valid Notice.

Supreme Court

Aggrieved By the Order of HC. Files an Appeal to

Response to the Order By The Assessee

Decision Of Supreme Court

The word ‘Indirectly’ qualifies for ‘accruing/arising’ and doesn’t qualify for ‘transfer’

S.9(1)(i) cannot by a process of interpretation be extended to cover indirect transfer of CA situated in India

To do so would amount to changing the ambit of S.9(1)(i)

Therefore language employed in S.9 (1) (i) L-4, you cannot bring indirect transfer within its fold

Such Interpretation will make the words ‘…situated in India…’ meaningless or nugatory.

Contention 1

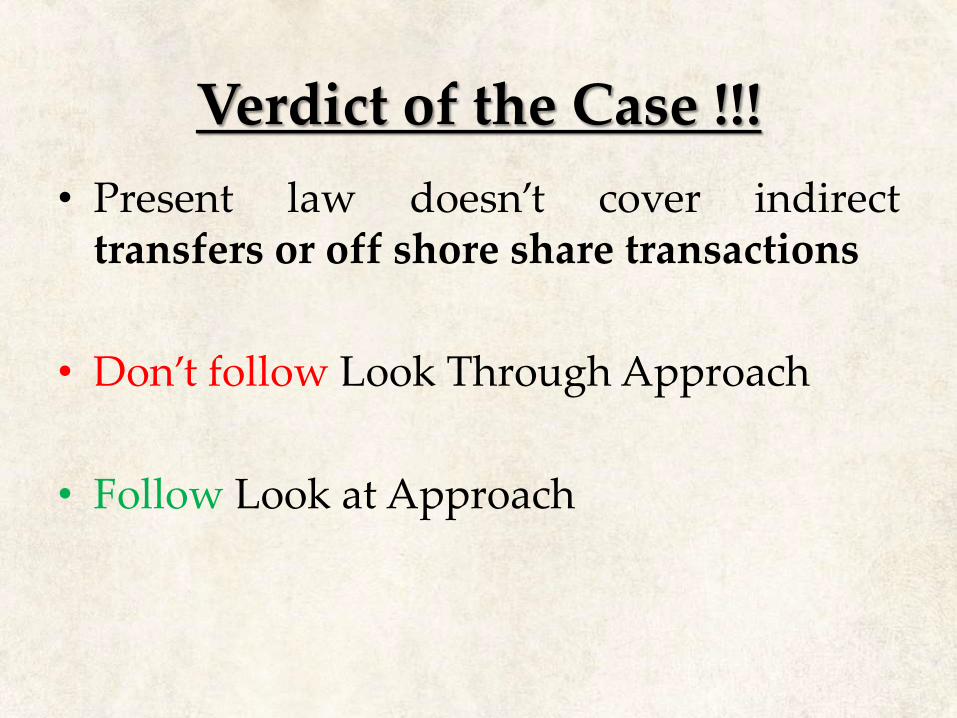

Verdict of the Case !!!

• Present law doesn’t cover indirecttransfers or off shore share transactions

• Don’t follow Look Through Approach

• Follow Look at Approach

Decision Of Supreme Court –Contention No.2

• Shares in a Company = Bundle of Shares

• One such Right = Voting Right

• If Share Holding Increases VR Increases then Controlling Interest also increases

• Control of a Company resides in Voting Power• Controlling Interest is a natural Incident of ownership of

share.• Controlling Interest is not Independent / Distinct

/Dissectable Capital Asset

• Shares and the right which eminate from them flow together and cannot be dissected.

• CI gets automatically shifted as a result of transfer of shares.

• Control and management is a facet of holding shares

• Conclusion: This is a Straight jacket case of transfer of Shares in a foreign Company between two non residence outside India .

• Therefore section 9(1)(i) L – 4 doesn’t apply• S.5 X S.4 4 – X, Not taxable, No TDS Deduction u /s 195.

SCN = Invalid• Note: S.195 applies only to a payment made by a

resident. If the Payer is NR s.195 doesn’t apply.

Major Amendments

No Section NameAmendment

Inserted

1 2(14) Capital Asset Exp.

2 2(47) Transfer of Capital Asset Exp. 2

3 9(1)(i) Income Deemed to

Accrue or Arise in India

Exp. 4

4 9(1)(i) Exp. 5

5 195(1) Other Sum paid to Non-

Resident Exp. 2

Retrospective Amendments To Supercede The Ruling Of

Supreme Court

Section Amended: Section 2 (14)

Segment of Ruling Superseded

Amendment – Explanation inserted to clarify that

Controlling interest is not anidentifiable or distinct capitalAsset independent of theholding of shares

“Property” includes anyright in or in relation to anIndian company , includingrights of management orcontrol or any other rightswhatsoever

Section Amended: Section 2 (47)

Off shore transfer ofshares in a foreignholding companydoes not result inextinguishment oftransferor’scontrolling interest inthe Indian subsidiaryand therefore, there isno element of transfer

Explanation – 2 is inserted below S.2(47)to clarify that “ transfer” includes

Disposing of or parting with an asset orany interest therein, or

Creating any interest in any asset in anymanner whatsoever,

Directly or indirectly, absolutely orconditionally, voluntarily orinvoluntarily, by way of anagreement(whether entered in to in Indiaor outside India or otherwise,

Notwithstanding that such transfer of rights has beencharacterized as being effected or dependent upon or flowingfrom the transfer of a share or shares of a company registered orincorporated outside India”

Section Amended: Section 9(1) (i)

Segment of Ruling Superseded

Amendment– Explanation 4 inserted to clarify that

Indirect transfer of capitalasset situated in India is notcovered by s. 9(1)(i). Theargument of look throughlacks merit

The expression “through”shall mean “ by means of” inconsequence of” or “byreason of”

Section Amended: Section 9(1) (i)

Segment of Ruling Superseded

Amendment – Explanation 5 inserted to clarify that

To read indirect transfer intoS.9(1)(i) would render thewords ‘capital Asset Situatedin India’ nugatory

Capital Asset situated inIndia will also cover share ofinterest in a foreigncompany/ entity registeredor incorporated outsideIndia if such share /Interestderives, directly or indirectly,its value substantially fromthe assets located in India

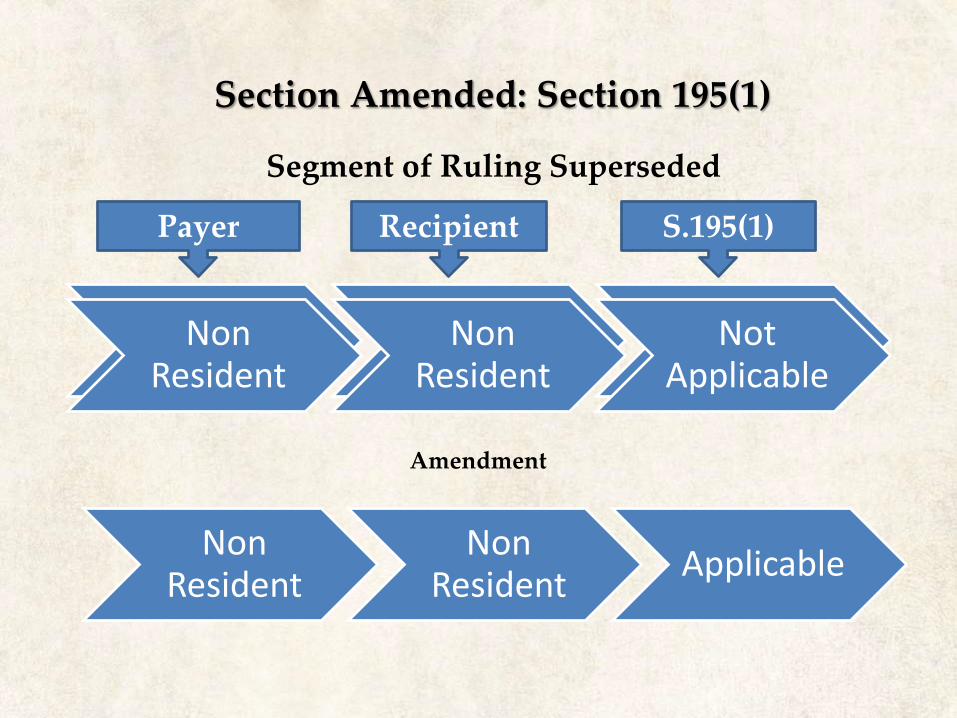

Section Amended: Section 195(1)

Segment of Ruling Superseded

Amendment

ResidentNon

ResidentApplicable

Payer Recipient S.195(1)

Non Resident

Non Resident

Not Applicable

Non Resident

Non Resident

Applicable

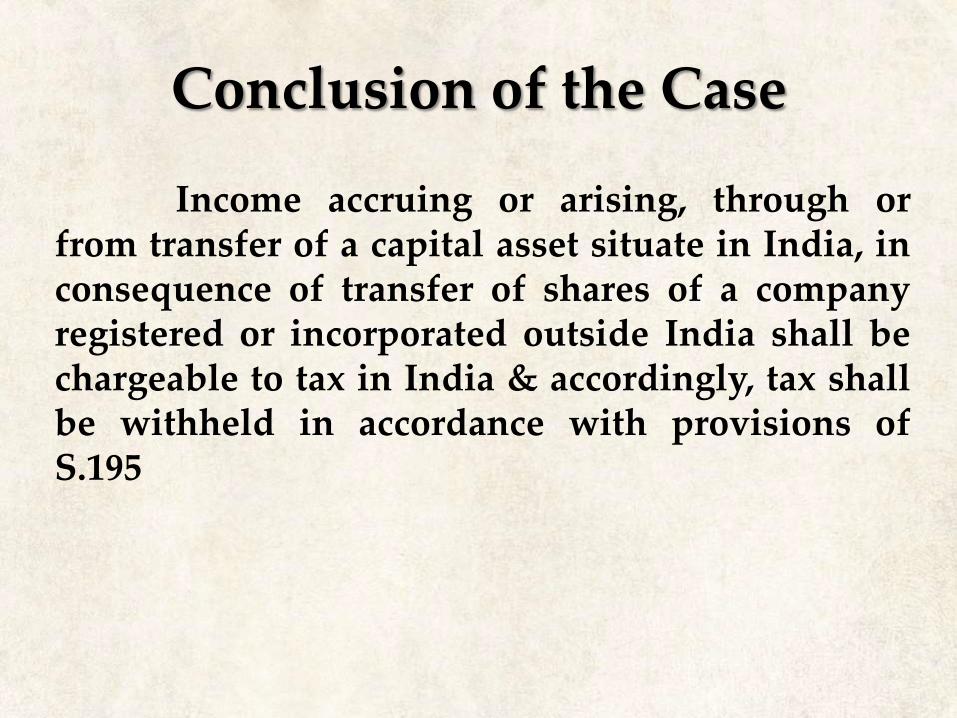

Conclusion of the Case

Income accruing or arising, through orfrom transfer of a capital asset situate in India, inconsequence of transfer of shares of a companyregistered or incorporated outside India shall bechargeable to tax in India & accordingly, tax shallbe withheld in accordance with provisions ofS.195

Thank You