Embed Size (px)

Citation preview

One Person Company [sec. 3(1)(c)];

Returns (u/s 92 & 93);

E- governance (sec. 120);

GDR (sec. 41);

Reduction of Share capital (u/s 63);

Valuation (sec. 247);

Company Secretary (203; & 205);

Concept of Corporate social responsibility (u/s 135);

Appointment of KMP (u/s 203);

Insider trading & forward dealing (u/s 194 & 195);

Enhanced accountability on part of companies;

Additional disclosures norms;

Audit accountability;

Audit Committee (u/s 177);

Register of Director & KMP and their shareholding (u/s 170);

Mergers and Amalgamation (sec. 230- 240);

Protection for minority shareholders;

Investor protection and relation;

Serious fraud investigation office (SFIO) [sec. 211];

Compounding under new legislation (u/s 441); and

Miscellaneous (fraud; penalty for fraud and false evidence) .

One Person Company

(OPC)The new legislation on Company Law has came out with new concept as cited

above and the same has been defined u/s 3 (1) (c) of the new legislation.

It refers to an lawful entity established by the one person by subscribing to the

memorandum of the OPC u/s 3 (1) (c)

The MoA of such co. shall indicate the “OPC” in the brackets below the name of

such company. e.g. Munjal Pvt. Ltd. (OPC).

The MoA of such Company shall also indicate the name of the person as the

nominee for such member by giving the prior written consent of such person and

same shall also be require to file with jurisdictional RoC at the time of incorporation

of such Co. along with MoA. Proviso to 3 (1)

The person, who appoint nominee for himself, having the following rights against

such nominee.

To bring the replacement, at any time, in the name of

nominee by given prior notice to such person &

To withdraw such written consent..

Provision Requirement

77 (2)

(certificate of regd. )

ROC shall issue a certificate of regd. in favour of Co

and , as the case may be, in favour of charge holder.

77 (3)

(effect of non regd. )

Notwithstanding anything contained in any other law for

the time being in force, Liquidator and Crs. shall not be

taken into a/c any charge unless there is a certificate of

regd.

77 (4)

[effect of 77 (3)]

77(3) shall not prejudice any obligation of Co towards

repayment.

Provision Requirement

77 (1)

(Registration of charge)

Every Company creating a charge- loan against

property, whether situated outside India, - within or

outside India, shall be bound by registration of such

charge with jurisdictional ROC by filing particulars and

instrument, if any, signed by creator and holder on

such payment and in such form as may be prescribed.

77(1)

(Time limit for regd.)

<= 30 days of creation of charge.

(What shall be the date considered for creation ?)

77 (1)

(type of Companies)

Every Company seeking finance against its property.

77(1)

(Condonation of delay)

If a Co. fails to get regd., <= 30 days from such

creation, then ROC, on app. by Co, may allow for

regd. <= 300 days from such creation. (Proviso- 1)

[procedure in rules for Condonation:- Co. shall file

app. for Condonation supported by declaration, signed

by Co. Secy, / Director, to the effect that such belated

delay shall not adversely affect rights of any other Crs.

of the Co.

-: Duty of the subscriber to MoA :-

To give intimation to the company with in such time and in such manner as may be

prescribe for change in name of the nominees indicating in the MoA of the Company.

The company shall give intimation to the concerned RoC about such change with in

such time and in such manner as may be prescribed i.e. by notifying the rules for the

same after the commencement of the new legislation.

Note:- the change in the name of nominee as indicating in the

Co’s MoA shall not be reckon as the alteration of the MoA.

Exemption available to new class of the Company:-

While filling the financial statement, such class of Companies not required to file.

cash flow statement. Proviso to clause 2 (40) (1)

The same company also not require to conduct AGM as the other company

require with in 9:00 a.m. to 6 p.m. u/s 96 (1)

The following section with which such company shall also not subject to :

Power of Tribunal to call meetings of members

Annual ReturnProvision Requirement

92 (1) Every Company shall require to file AR

which shall carrying the particulars as

on closing of F.Y.

92 (1) (k)

(signatory to AR)

1) AR shall be signed by a director

and Company Secretary, if there is

no CS then same shall be by PCS.

2) In case of listed entity: CS + D+

certified by PCS.

3) In case of OPC & Small Company:

CS of that Company and where

there is no CS then same shall be

signed by Director of that Co.

92 (2)

(Requirement w.r.t. certification)

1) AR filed by listed entity; and

2) Company having paid up Rs. >= 5

Cr. & turnover of >= 25 Cr.

then AR shall also be certified by PCS

92 (3)

( Extract of AR in BR)

Extract of AR shall form part of boards’

report

Provision Requirement

92 (4)

(time limit for filing)

Every Company shall require to file <=

60 days from the date of AGM; if there is

no AGM then <= 60 days from on which

date it should be held along with

reasons to that effect

Authority to whom AR shall be filed Concerned registrar of Companies

92 (5)

( Consequences of non compliances )

If any Company fails to comply 92 then

Company shall be liable to fine of not

less than 50K which may extend to 500k

and every officer, who is in default, shall

be liable for imprisonment maximum 6

months or 50K to 500k or both.

92 (6)

Penalty for wrong certification by PCS

If AR wrongly certified by PCS then he

shall be liable for fine which not be less

than 50 K but which may extend to 500

K.

Provision Requirement

93 (1) Every listed entity has require to file

with the ROC ; a return to the effect of

changes occur in shareholding of

promoter and top ten shareholders.

Who shall be covered under this return Promoter and top ten shareholders.

What shall be the basis of filing such

return

When changes occurred in nos. of

shares held by promoter and top ten

shareholders then that Company shall

abide by this.

Time limit for filing such return Company bound by this provision shall

require to file <= 15 days from the

occuurence of such change.

Return w.r.t. Change in

shareholding

Option of keeping books of account in electronic form

Maintenance and inspection of documents in electronic form

Placing of financial statements on co’s website [3rd proviso to 136(1)]

Holding board meetings through video conferencing [sec. 173(2)]

Offering securities to public in the dematerialized form (sec. 29)

E-governance

E-governance has been proposed for various

processes like :

Amendment proposed to clause 49 of listing agreement for bringing the listed cos

in line with new legislation and good corporate governance practices:

http://www.sebi.gov.in/cms/sebi_data/attachdocs/1357290354602.pdf

GDR (Global depository Receipt)

Q_ What is GDR ?

Ans_ It refers to receipt, denomination in foreign currency, created by the

overseas custodial body, on charging some fee for this, on behalf of the issuing

company, which is Indian company, and backed by the ordinary shares of the

issuer company . Or hitting the foreign market with new issue by Indian issuer

which already listed on recognized stock exchange of India.

u/s 41 of the new legislation, a company can issue the GDR by passing the

special resolution in its general meeting and by complying the condition as may

be prescribed.

Rules

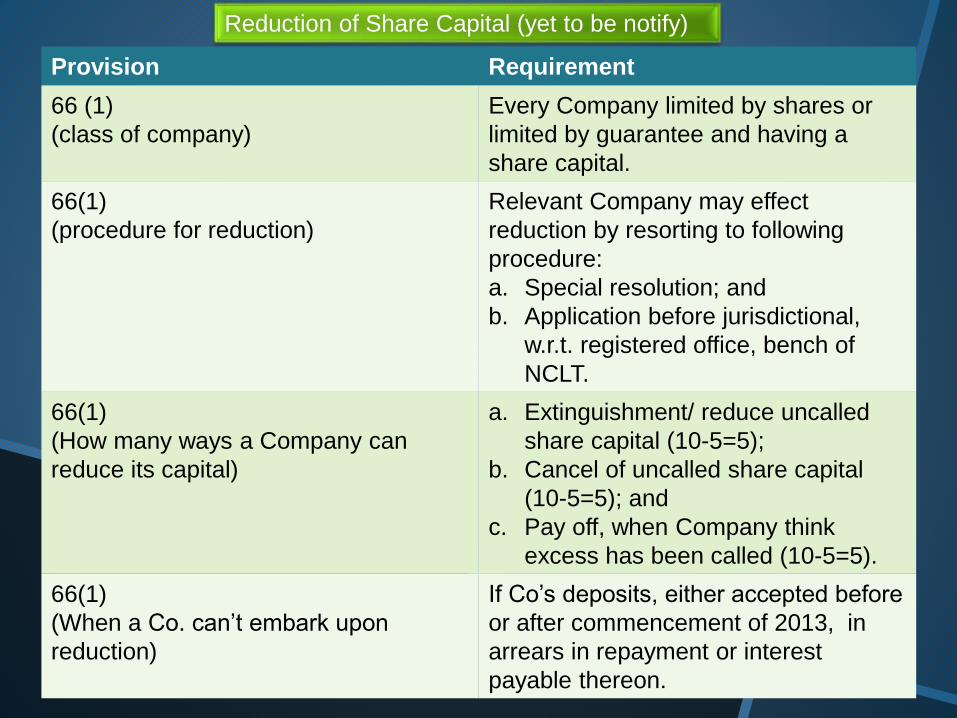

Reduction of Share Capital (yet to be notify)

Provision Requirement

66 (1)

(class of company)

Every Company limited by shares or

limited by guarantee and having a

share capital.

66(1)

(procedure for reduction)

Relevant Company may effect

reduction by resorting to following

procedure:

a. Special resolution; and

b. Application before jurisdictional,

w.r.t. registered office, bench of

NCLT.

66(1)

(How many ways a Company can

reduce its capital)

a. Extinguishment/ reduce uncalled

share capital (10-5=5);

b. Cancel of uncalled share capital

(10-5=5); and

c. Pay off, when Company think

excess has been called (10-5=5).

66(1)

(When a Co. can’t embark upon

reduction)

If Co’s deposits, either accepted before

or after commencement of 2013, in

arrears in repayment or interest

payable thereon.

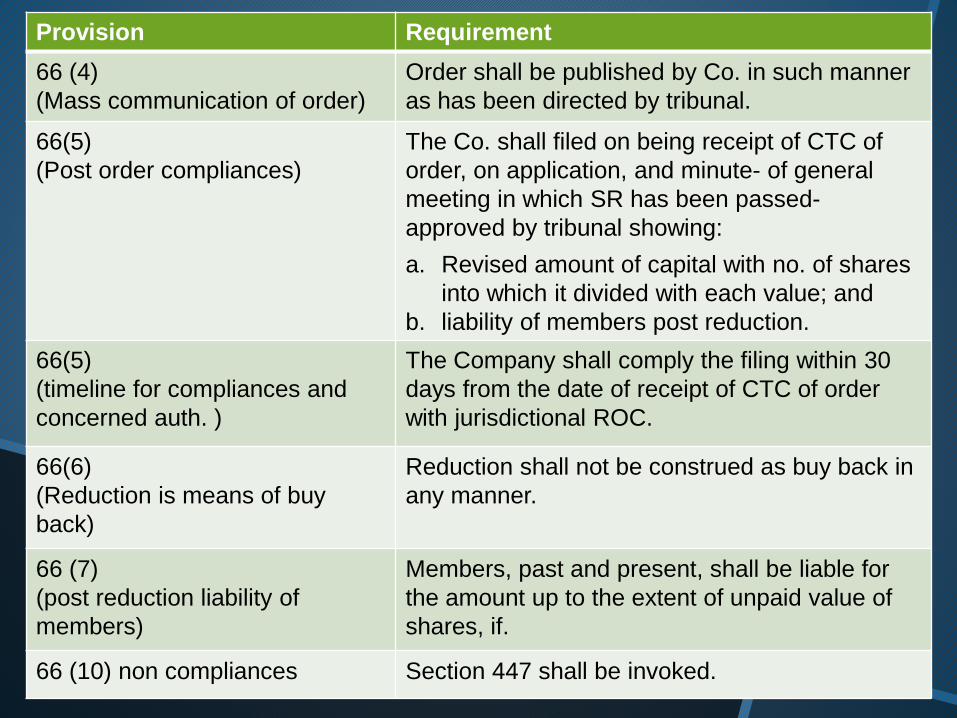

Provision Requirement

66 (2)

(procedure by NCLT)

The tribunal, on receipt of app, shall put into

knowledge of ROC; SEBI; IT etc. for receiving

their objection <= 3 months from the receipt of

notice.

66(2)

(presumption on non receipt of

objection)

If NCLT has not received any objection within 3

months , then same shall be considered that has

been approved by them. (proviso)

66(3)

(Order of reduction)

a. The tribunal may, on being confirmed that no

debt is outstanding by Co. or mechanism has

been devised for securing any debt in queue,

sanction such reduction.

66(3)

(when tribunal can block such

reduction)

If journal entry proposed by Co. w.r.t. reduction

of capital not in conformity with accounting

standard laid in sec. 133; and

A Certificate to that effect issued by PCA not

submitted with tribunal. (proviso)

Provision Requirement

66 (4)

(Mass communication of order)

Order shall be published by Co. in such manner

as has been directed by tribunal.

66(5)

(Post order compliances)

The Co. shall filed on being receipt of CTC of

order, on application, and minute- of general

meeting in which SR has been passed-

approved by tribunal showing:

a. Revised amount of capital with no. of shares

into which it divided with each value; and

b. liability of members post reduction.

66(5)

(timeline for compliances and

concerned auth. )

The Company shall comply the filing within 30

days from the date of receipt of CTC of order

with jurisdictional ROC.

66(6)

(Reduction is means of buy

back)

Reduction shall not be construed as buy back in

any manner.

66 (7)

(post reduction liability of

members)

Members, past and present, shall be liable for

the amount up to the extent of unpaid value of

shares, if.

66 (10) non compliances Section 447 shall be invoked.

ValuationNew Legislation come up with new chapter XVII carrying title “ Registered

Valuers”

Q_What is valuation and under which section it is specified ?

Ans_value of the property (moveable / immovable) for which valuation has

undergoing. and it is mentioned only u/s 247.

Q_How is to be valuation done in this legislation ?

Ans_ u/s 247 (2) (c) in accordance with the rules as may be prescribed.

Q_why and when we need of such ?

Ans_ To assessing the exact value of the property including the securities of the

Company and in following cases we require to resort to valuation.

Issue other than for cash consideration like Sweat

Equity ;

In Corporate strategy like :- mergers / takeovers /

amalgamation / Hiving-off of business

Issuing of Rights Issue i.e. proportionate allotment to

existing shareholders

Q_which covered under valuation?

Ans_ u/s 247 (1), Property of any kind, stocks, debenture, securities,

goodwill, assets, net worth and liabilities.

Appointment of valuer u/s 247 (1)

It shall be appointed by the audit committee / by the BoD of that Company in

absence of audit committee.

Who shall be valuer u/s 247(1)

He shall be the person possessed by such qualifications and experience and

registered as a valuer.

Role of valuer u/s 247 (2)

Penalty for contravention of rules, T&C by the valuer u/s 247 (3)

Makes the impartial , true & fair view;

Not to pursue for valuation of that property in which he

have direct / indirect interest;

Resorting to proper due diligence while valuation;

Abiding by the rules, T&C as may be prescribed.

Fine which shall not be less than 25000 but which may extend to 1 lac.

But where contravention of this 247 committed by the valuer for defraud the

company / its members then there shall be provision for imprisonment which

may extend to 1 yr and with fine 1 lac – 5 lac proviso to 247 (3) .

Where valuer is convicted then he shall repay the remuneration and pay for

losses which incurred by the Company u/s 247 (4) .

Contravention

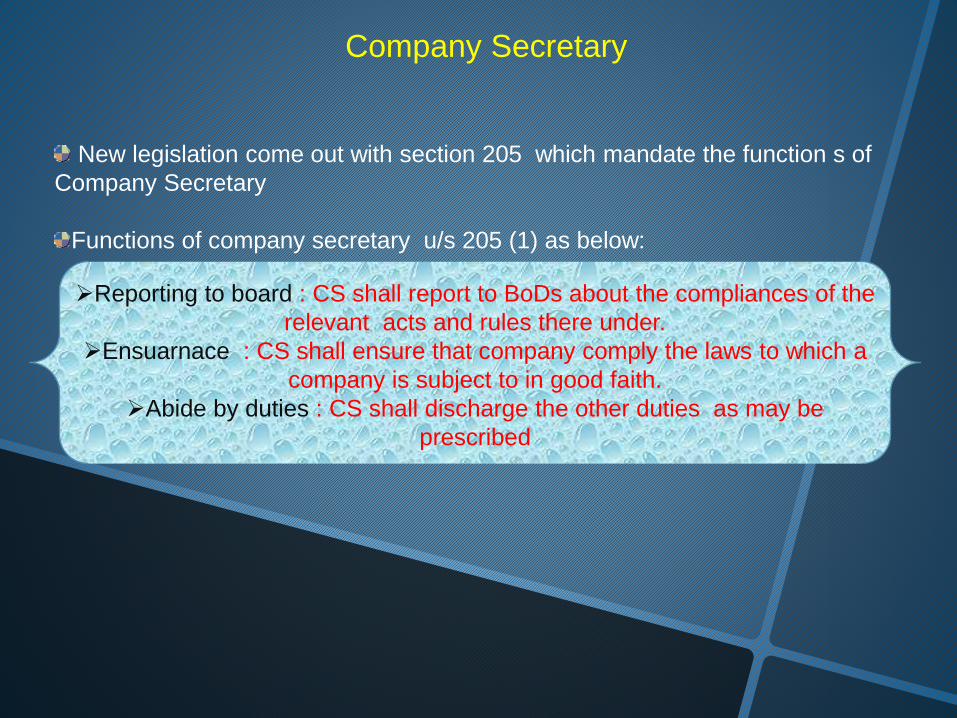

Company Secretary

New legislation come out with section 205 which mandate the function s of

Company Secretary

Functions of company secretary u/s 205 (1) as below:

Reporting to board : CS shall report to BoDs about the compliances of the

relevant acts and rules there under.

Ensuarnace : CS shall ensure that company comply the laws to which a

company is subject to in good faith.

Abide by duties : CS shall discharge the other duties as may be

prescribed

Q_What secretarial standard means ?

Ans_ it refers to standard issued by the Board on Secretarial Standard of

Institute of Company Secretary of India and duly approved by the Central

Government .

SS issued by the Board of SS till 18.01.2013 as below :

SS-1 Secretarial Standard on Meetings of the Board of Directors

SS-2 Secretarial Standard on General Meetings

SS-3 Secretarial Standard on Dividend

SS-4 Secretarial Standard on Registers and Records

SS-5 Secretarial Standard on Minutes

SS-6 Secretarial Standard on Transmission of Shares and Debentures

SS-7 Secretarial Standards on Passing Resolutions By Circulation

SS-8 Secretarial Standards on Affixing of Common Seal

SS-9 Secretarial Standards on Forfeiture of Shares

SS-10 Secretarial Standards on Board's Report

Concept of Corporate social responsibility

(I) What is CSR ?

Ans:- It refers to accountability of corporate towards social pertaining to

efficient utilization of their resources.

or

CSR means operating business in such a manner which strive the

environment of ethical and meet the expectation of society which they keep

from corporate .

or

It also said to be as introduce those line of products which do not affect the

environment and society as well.

or

In other way it also said to be as a implied contract between society and

corporate where later bearing responsibility since birth towards society.

(II) CSR (section-135) :-

If a company having during any financial year since 2014-15 :

Then that Company shall require to constitute a Committee designed as “CSR”

committee, constituting not less than three directors of which at least 1 shall be an

independent director.

And that company shall make every endeavor to spend 2 % of its avg. net profit before

tax earned in preceding 3 F.Y., in activities, schedule 7, approved by board on

recommendations of the said committee [135 (5)].

Note:_ While calculating PBT, profit arising from branches located outside India

shall not be taken into a/c.

Concerned Companies shall disclose the contents of its CSR policy in its board report

and also place the contents of its CSR policy on its website, if any,

[135 (4) (a)].

Company (ies) shall also state the composition of CSR committee in its board report.

[135 (2) ].

Net profit >= 5 crore/ 50 mn/ ; or.

Net worth >= 500 crore/ 5000 mn/ 5 bn; or

Turnover >= 1000 crore. [135 (1) ].

Q_; Functions of CSR committee [135 (3) ].

Ans:- Functions of this committee split into three parts:

1) Formulating the policy in line with sch. 7:

2) Recommendations of CSR activities to board; and

3) Recommendations about expenditure, on a/c of CSR activity (ies);

4) Monitoring the policy;

5) Specify the projects and programmes that are to be undertaken;

6) Compile a list of projects/ programmes plans to undertakeduring the

implementation yr. i.e, 2014-15;

Q_: How many ways a Company can undertake CSR projects ?

Ans: A Company can discharge the compliances by way of:

1) By formulating a division in Company;

2) By formulating a trust;

3) Through foundation;

4) By hiring a third party (NPO);

5) By pooling resources with other Company (ies) i.e,; in partnership with other

-: Draft Corporate Social Responsibility Rules:-

Commencement: These rules come into force from F.Y. 2014-15;

Net Profit: It refers to profit earned by a Company before tax i.e., PBT;

Spending: 2 % of its avg. PBT earned in preceding 3 F.Y. ending on 31.03.2014

Compliances: Concerned Cos has required to dedicate for compliances from

2014-15 on annual basis i.e, once these rules notified by MCA then those

Companies falling into the criterion provided in 135 (1) has required to spend 2

% of its avg. of PBT for 2013-14; 2012-13; and 2011-12.

CSR projects: A Company mar carry on brown fields or green fields project.

Social Activities conducted in normal course of biz. shall not be counted towards

CSR spending.

CSR v/s Corporate Sustainability

CSR includes corporate, social and its responsibility towards social on the

other hand later includes only environment

Corporate sustainability ensures traditional growth of social, economic, and

environment. Social, economic, environment provide opportunities.

Corporate sustainability increases stakeholders value.

PRINCIPLES:

Principal of Intergeneration

Principle of Sustainable use

Principle of Equitable use

.

Q:- What is it mean ?

Ans:- it refers to that class of persons which is possessed by high degree of

knowledge and ultimately bearing the responsibility for the failure / success of the

company .

Q:- What shall it comprise ?

Ans_ u/s 203 the following person shall form part of this category:

Q_ what section covers their appointment ?

Ans_ section 203 is introduced which covers the following :-

Every Company belonging to such class / class of companies which may be

prescribed shall be possessed by following members in their management at

every time:

Q_whether MD / CEO can take the charge of chairperson simultaneously ?

Ans_Proviso to 203 (1) (ii) unless AOA of company provides otherwise a person

can’t not enjoy the aforesaid positions at a time.

CFO / MD / Manager and in absence there shall be whole time director;

Company Secretary

CFO / MD / Manager and in absence there shall be Whole Time Director;

Company Secretary

Q_ How appointment of KMP shall be governed ?

Ans _ u/s 203 (2), Every whole time KMP shall be appointed by means of board

resolution with containing the t&C + remuneration as well.

Q_Whether there is provision for appointment of KMP in more than 1 company?

Ans_ u/s 203 (3), there is candid bar on KMP for assuming charge on such class

of designation in more than one company except that company categorised as its

subsy company .

However with the previous approval by passing board resolution, a person can

enjoy the position as KMP in more than 1 Company .

Q-Is there any requirement for making choice for number of designation as in

directorship after the commencement of new legislation ?

Ans_Yes, proviso (ii ) of 203 (3) stating that a person shall exercise his choice

with in 6 months from commencement of this act.

Q_whether a person can act as MD for > 1 Company ?

Ans_ Proviso (iii) to 203 (3) a company may go with same person who is already

enjoying such designation in another company already by passing board

resolution with the consent of all directors along with giving specific notice to that

effect . (note: but same person can’t hold office more than 1 at a time)

Q_ How vacancy will be fill for this class of designation (KMP) if any one

resign before his original terminal of tenure ?

Ans_ u/s 203 (4) the vacant post shall be fill by passing board resolution <= 6

months of such vacancy.

Q_ What will be the consequences for non compliances of this provisions ?

Ans_ u/s 203 (5), if contravention on the part of company then :-

If contravention on the part of the director:

Company shall be liable for fine which shall not be less than 1

Lac and which may extend to 5 lac

Then every director and KMP who is in default shall be liable for fine which

may extend to 50000 and for every day, in continuation, 1000 shall be liable

Forward TradingWhat is forward dealing ?

Ans:-

New legislation come up with a new section 194 , which confronted with

forward trading.

Aforesaid section mandate that no person including Director / KMP shall

enter into such trading in the securities of Company / associates / subsy (ies)

which gives any of the following right on a specified number of relevant shares /

specified amount of relevant debentures.

right to call for / make a delivery or Right , as he may elect, to call / make delivery.

Q:- What is relevant shares & relevant debentures ?

Ans:- Explanation to 194 - means that shares / debentures in which the

concerned person is a WTD / KMP / shares & debentures of its holding & subsy

(ies) cos.

Q:- Non compliances

Ans:- <= 2 years/ 1 lac – 5 lac/ both

Insider trading

There is new section 195 which dealt with insider trading.

Aforesaid section mandate that- No person including KMP / Director shall

enter into insider trading i.e, act of buying/ subscribing/ dealing/ selling/ agreeing

to subscribe, buy, sell or deal in any secs. Of Co.

If any person including KMP / Director enter in contravention to section 195

then he shall be liable for following :-

What insider trading means ?

Ans:- explanation “a” to proviso of 195 (1), an act of subscribing, buying,

selling, dealing or agreeing to subscribe, buy, sell or deal in any securities by

any director / KMP / any other officer of a company either as principal / agent if

such director / KMP / any other officer of a co. is reasonably expected to have

access to any UPSI in respect of securities of co. ; or

an act of counseling about procuring / communicating, directly / indirectly any

UPSI to any person

195 (2): Imprisonment which may extend to 5 years / fine shall not

be less than 5 lac but which may extend to 25 cr or 3 times of the

profit which earned through this transaction, whichever is higher or

both..

Tabulation of 194 & 195 underneath

Basis 194 195

Status Yet to be notify Yet to be notify

Dealt with Forward trading Insider trading

Community of persons

subject to

Any director or any of

KMP

No Person including any

director or KMP

Non Compliances 1) <= 2 years/ 1 lac- 5

lac/ both; and

2) The delinquent shall

surrender securities,

acquired under this

transaction, to the Co.

and Co. shall not

register the secs. in

favour of defaulter, if in

phy. form, or shall

inform to depository to

not to make entry w.r.t.

registration of said no.

secs.

<= 5 years/ 5 lac – 25 cr.

Or 3 times of the amount

earned, which ever is

higher, or both.

u/s 24 of SEBI act, 1992:

<= 10 years/ 25 cr. / with

both.

Norms in force N.A. SEBI (PIT) regulations,

1992

What is price sensitive information

Ans: Whch relates, directly / indirectly, to a b Co. & which if published is

likely to materially affect the price of securities of the Co.

Sebi rejects RIL companies' consent order plea in insider trading

http://economictimes.indiatimes.com/markets/regulation/Sebi-rejects-RIL-

companies-consent-order-plea-in-insider-trading/articleshow/17878717.cms

Reliance Industries approaches Tribunal against Sebi over alleged irregularities in

share dealings

http://economictimes.indiatimes.com/markets/regulation/Reliance-Industries-

approaches-Tribunal-against-Sebi-over-alleged-irregularities-in-share-

dealings/articleshow/17876201.cms

SAT adjourns RIL-SEBI case till January 24

http://economictimes.indiatimes.com/markets/regulation/sat-adjourns-ril-sebi-case-

till-january-24/articleshow/17980109.cms

Only a few controlling price-sensitive information a matter of concern: Sebi

http://economictimes.indiatimes.com/articleshow/18053378.cms?prtpage=1

Order against Reliance Petro Investment Ltd. in insider trading case

http://www.sebi.gov.in/cms/sebi_data/attachdocs/1367505894264.pdf

Enhanced accountability on the part of companiesConcept of independent directors, u/s 149(5), with their office term

& liability also have been laid in the act

Code of conduct for independent directors also been introduced by

specifying new schedule no. 4 r/w 149(5)

Duties of directors also prescribed u/s 166

The central govt. entrusted with powers to prescribe restrictions

w.r.t. layers of subsy (ies) for any class / classes of cos.

Concept for whistle blower also been provided and there is also a act,

Public Interest disclosures and protection to whistle blowers act, 2011 ,

which is waiting for clearance in parliament.

Please find the text of act:

http://www.prsindia.org/uploads/media/Public%20Disclosure/Public%20Interest%

20Disclosure%20act,%202010.pdf

New provisions for allowing re-opening of accounts on orders of central

government / court/ tribunal u/s 130

Brief about Section 130 as below :-

u/s 130(1):- A company shall not re-open it’s accounts unless order of competent

authority.

What is re-open of accounts ?

Inspection of accounts on orders of competent auth.

Who is competent auth. under section 130 ?

Court having jurisdiction over its, company, registered office.

When competent authority shall issue the order

If previous relevant accounts prepared in fraudulent manner;

If the affairs of company give the room for objection

Procedure for passing an order by said authority

Court / NCLT shall put the above facts into the knowledge of central government

and income tax auth. for representation and shall take into the consideration

before issuing the order.

Can accounts revised on account of this order ?

Yes, u/s 130 (2), order may carrying the provision for such revision of accounts, if

, revised on such re-open shall be final for that financial year.

What is independent director?

Who provides independent judgment, instill professional discipline, posses integrity,

monitor and ensure compliances and maintain the interest of the shareholders

Qualification for independent director u/s 149 (5)(e) ?

Not holds together with his relatives more than >= 2% of the voting rights of the

company u/s 149(5)(e)(iii) .

Neither himself or with his relative holds or held the designation of KMP or is or had

been an employee of holding / subsy (ies) / associate in any of the three preceding

financial year u/s 149 (5)(e)(i) .

who had not any pecuniary relationship with subsy(ies)/ holding/ promoters/

directors/ associate in any 2 preceding financial year or current year 149(5)©

None of whose relatives has or had pecuniary transaction with holding / subsy (ies)/

associate/ directors/ their promoters amounting to >= 2% of the income/ gross

turnover or 50 lac or higher amount which ever is lower u/s 149 (5)(d) .

Who neither himself nor his relatives appointed as CEO / director (by whatever

name called) of any organization for non profit and that organization received the <

25% of its total receipts from any company i.e. if received >= 25% of its receipt from

any company then said director, appointed as independent director, not said to be as

independent director u/s 149(5)(e)(iv) .

Additional disclosure normsDisclosures like development and implementation of risk management and

prohibition thereof in the board report u/s 134(3)(n) .

Board report of every listed companies shall carrying the disclosure about manner

of evaluations for its BoDs as well as individual directors performance u/s 134(3)(p)

.

Board report, u/s 134, shall include the detail of following :

related party transaction u/s 188,

statement on director’s remuneration,

auditor’s qualification on auditor report,

secretarial audit report,

cost audit report etc.

Every listed cos required to file return in prescribed form to concerned ROC

when change occurred in promoter’s stake and top 10 shareholders with in 15

days of such change.

Consolidation of a/cs i.e. a/cs of subsy (ies)+ foreign subsy (ies) + holding co

to be attached while filling with concerned ROC.

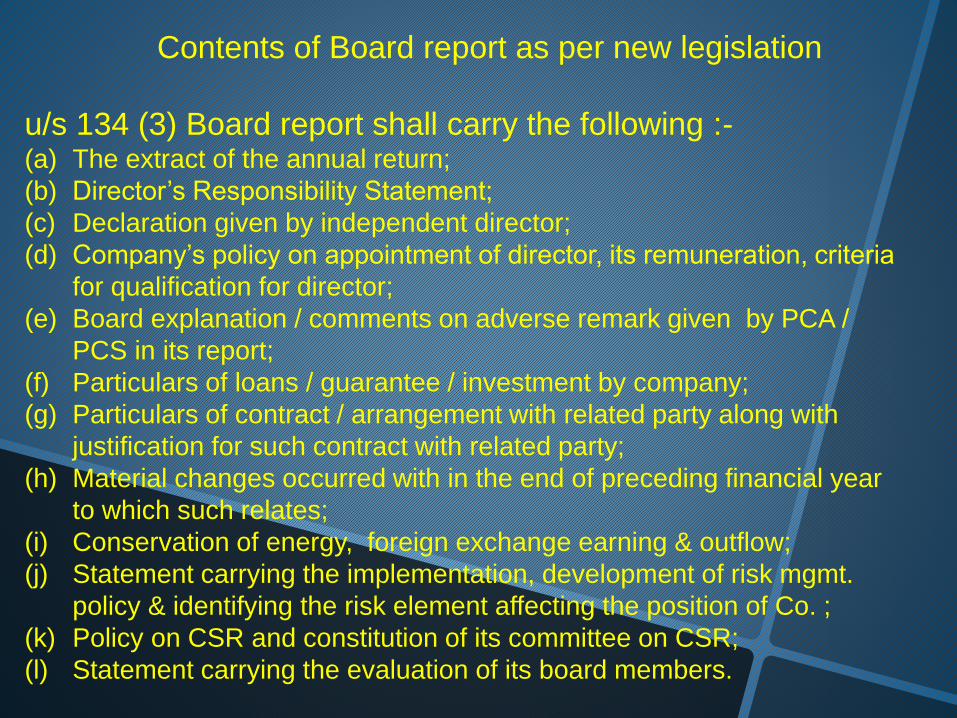

Contents of Board report as per new legislation

u/s 134 (3) Board report shall carry the following :-(a) The extract of the annual return;

(b) Director’s Responsibility Statement;

(c) Declaration given by independent director;

(d) Company’s policy on appointment of director, its remuneration, criteria

for qualification for director;

(e) Board explanation / comments on adverse remark given by PCA /

PCS in its report;

(f) Particulars of loans / guarantee / investment by company;

(g) Particulars of contract / arrangement with related party along with

justification for such contract with related party;

(h) Material changes occurred with in the end of preceding financial year

to which such relates;

(i) Conservation of energy, foreign exchange earning & outflow;

(j) Statement carrying the implementation, development of risk mgmt.

policy & identifying the risk element affecting the position of Co. ;

(k) Policy on CSR and constitution of its committee on CSR;

(l) Statement carrying the evaluation of its board members.

Signatories to the financial statement including consolidated financial

statement as per ne w legislation

Chairman ,if authorized by BoD or by two directors at

least one of them shall be MD; and

Company Secretary and;

CEO (if appointed as Director on its governing board);

CFO, where Co. appointed the same.

u/s 134(1)

Signatories to the Board report

u/s 134 (6)

Chairman, if he is authorize by BoD or by 2 directors (at

least one of them shall be MD)

Contravention to the 134

In case of company :- 50000 – 25 Lac and

In case of officer in default : 3 years / 50000 – 1 lac / Both

u/s 134 (8)

Attachment to financial statement

Auditor Report, Board Report and Secretarial Audit Report.

Section 188 at glance

Section 188 – Related party transaction “RPT”

Q: What related party consist ?

Ans: u/s 2 (76) of the act the following person party (ies) categorized as

related party :

i) Director or his relative.

ii) KMP or his relative.

iii) A firm, in which a director, manager or his relative is partner.

iv) A private Company in which a director or manager is a member or

director.

v) A public Company in which a director or manager is director or holds

along with his relatives more than two % of its paid up capital.

vi) Any body corporate whose board, MD or manager is accustomed to act

in accordance with the advice, directions or instructions of a director or

manager.

vii) Any person on whose advice, directions or instructions a director or

manager is accustomed to act.

viii) Any Company which is :

Holding, subsy or an associate Company of such Company

A subsy of a holding to which it is also a subsy

ix.) such other person as may be prescribed

.

Q: what is “ relative “ ?

Ans: relative with reference to any person, means any one who is related to

another, if:

1) They are members of HUF

2) They are husband and wife

3) One person is related to the other in such manner as may b prescribed

A company can not enter into such transaction (contract / arrangements)

unless there is resolution in its board meeting and conditions as may be

prescribed to be complied by the company.

If a company having such amount of paid up capital or transactions

exceeded the amount as may be prescribed then such transaction also

subject to special resolution in general meeting .

u/s 188 (1) what “RPT” may consist ?

sale, purchase and supply of material;

sale, purchase of property of any kind ;

leasing of property of any kind;

Underwriting the subscription of securities / derivatives

thereof;

Related party’s appointment in office / place for profit in

its subsy or associate company;

Appointment of any agent for sale, purchase or supply

of goods or services

Q:- what is associate company ?

Ans:- as defined in u/s 2(6) in relation to another company means that the

first company holds more than 20 % of its total share capital or of business

decisions under an agreement but it does not include subsy and JV.

Q:- what is office / place for profit ?

If such office / place for profit is held by Director then any

remuneration received by him, in respect of such holding, by way of

fee / commission / salary / otherwise exceeded the limit for which he

is entitled .

Where such office / place for profit is held by individual other than

director or by firm / private company then any remuneration receive by

way of salary / fee / commission / otherwise.

or

Q:- what shall be the effect of contract enter with related party without obtaining

the previous sanction of BoD / in general meeting ?

Ans- u/s 188(3), where the contract / arrangement entered without the sanction of

BoD / passing of special resolution at general meeting, as the case may be, by

any director or by employee shall be voidable ab initio at option of its board of

directors if not ratified by its BoD / by shareholders at general meeting <= 3

months of such contract / arrangement . where such contract / arrangement with

the related party of such contractor / authorize by such contractor then same

shall be liable for indemnify the Co. against any loss incurred by it.

u/s 188 (4), in addition a company may proceed against such defaulter for

recovering the loss incurred by it.

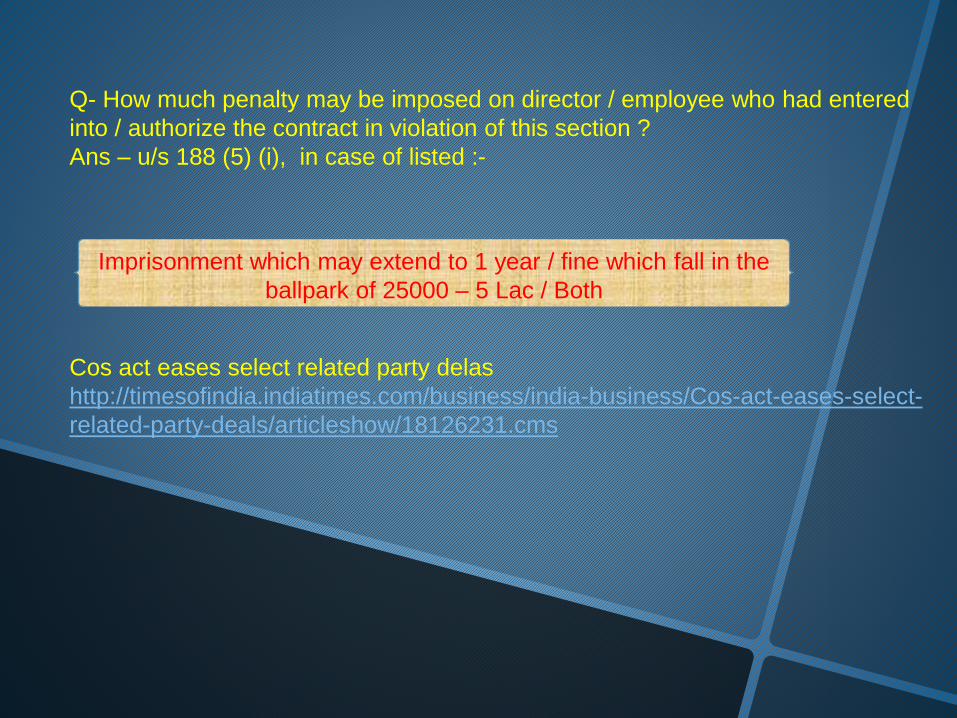

Q- How much penalty may be imposed on director / employee who had entered

into / authorize the contract in violation of this section ?

Ans – u/s 188 (5) (i), in case of listed :-

Cos act eases select related party delas

http://timesofindia.indiatimes.com/business/india-business/Cos-act-eases-select-

related-party-deals/articleshow/18126231.cms

Imprisonment which may extend to 1 year / fine which fall in the

ballpark of 25000 – 5 Lac / Both

Audit AccountabilityRotation of individual auditors after term of 5 consecutive years and audit

firms after 2 consecutive of 5 years.

Auditors prohibited from extending services other than as approved by Board

of Directors / Audit committee for maintaining its independence and

accountability [u/s 144].

Auditors (firms / individual) to report specifically on whether the company

has comply the directions issued by the SEBI.

Mandating NFRA (National Financial Reporting Authority) u/s 132 to ensure :

monitoring & compliance of accounting & auditing standards.

to monitor quality of service of professionals associated with

compliances.

to look into after the disclosures made by auditor.

Every listed entity require to engage PCS for secretarial audit of its

compliances and shall include a report of secretarial audit in board report.

Every listed entity require to comply the standards of ICSI issued for board

and general meeting i.e. shareholders meeting.

Audit Committee

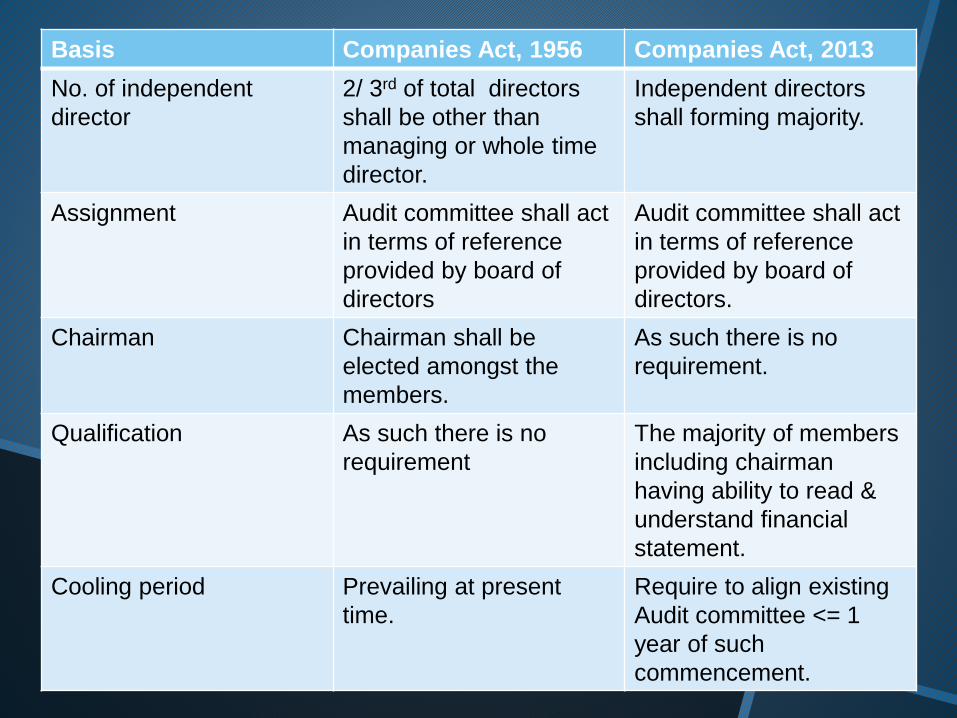

Basis Companies Act, 1956 Companies Act, 2013

Provision 292 177

Which Companies required

to constitute

Every Public Company

having paid up share

capital of >= Rs. 5 cr.

Every listed Company and

such other class as may be

*prescribed

a) Every other public

Company having paid

up capital >= Rs. 100

cr. Or turnover >=Rs.

100 cr, whichever is

more; or

b) Which have, in

aggregate, outstanding

loans or borrowings or

debentures or deposits

exceeding Rs. 200 cr.

No. of members Not less than three

directors

a) Minimum three

directors.

Basis Companies Act, 1956 Companies Act, 2013

No. of independent

director

2/ 3rd of total directors

shall be other than

managing or whole time

director.

Independent directors

shall forming majority.

Assignment Audit committee shall act

in terms of reference

provided by board of

directors

Audit committee shall act

in terms of reference

provided by board of

directors.

Chairman Chairman shall be

elected amongst the

members.

As such there is no

requirement.

Qualification As such there is no

requirement

The majority of members

including chairman

having ability to read &

understand financial

statement.

Cooling period Prevailing at present

time.

Require to align existing

Audit committee <= 1

year of such

commencement.

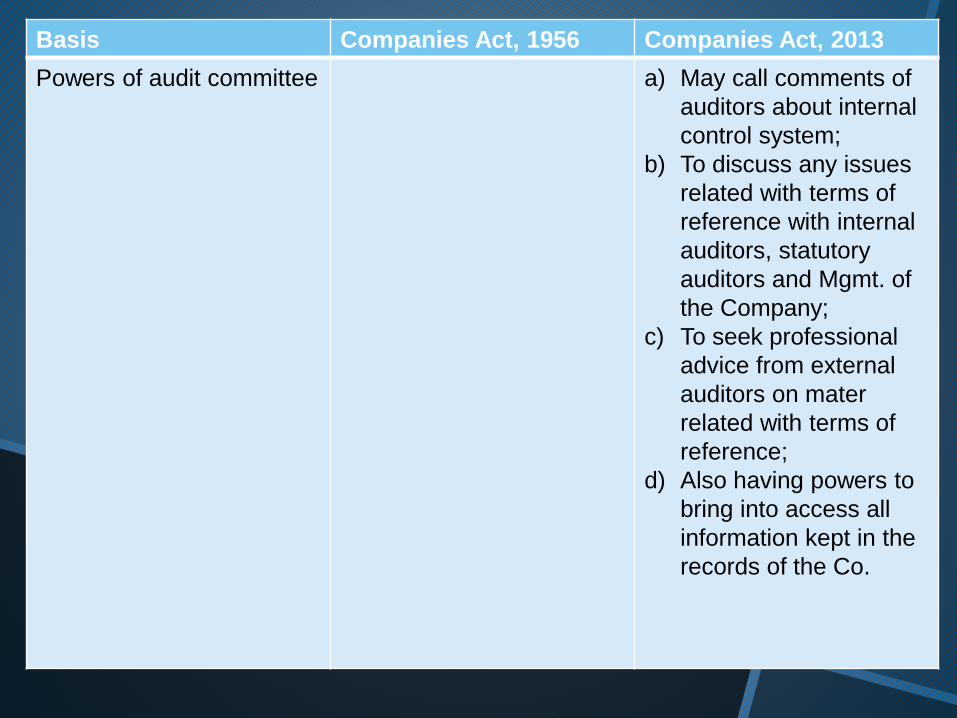

Basis Companies Act, 1956 Companies Act, 2013

Powers of audit committee a) May call comments of

auditors about internal

control system;

b) To discuss any issues

related with terms of

reference with internal

auditors, statutory

auditors and Mgmt. of

the Company;

c) To seek professional

advice from external

auditors on mater

related with terms of

reference;

d) Also having powers to

bring into access all

information kept in the

records of the Co.

Register of Director & KMP and their shareholding

Provisions Requirement

170 (1) Every Company shall keep at its

registered office in addition to other

registers, a register shall contain the

particular to the effect of Directors’ &

KMPs’ appointment and their

shareholding in Company, its subsidiary

& Associate Company if.

170 (2) Every Company shall require to file a

return before concerned ROC <= 30

days from the date of appointment of

every Director & KMP and also require

to file return <= 30 days from the date of

change thereof.

Status of provision as on 16th

December 2013

The said section yet not notified by MCA

SS-1 Secretarial Standard on Meetings of the Board of Directors

SS-1 Limited Revision of Secretarial Standard on Meetings of the Board of

Directors

SS-2 Secretarial Standard on General Meetings

SS-3 Secretarial Standard on Dividend

SS-4 Secretarial Standard on Registers and Records

SS-5 Secretarial Standard on Minutes

SS-6 Secretarial Standard on Transmission of Shares and Debentures

SS-7 Secretarial Standards on Passing Resolutions By Circulation

SS-8 Secretarial Standards on Affixing of Common Seal

SS-9 Secretarial Standards on Forfeiture of Shares

SS-10 Secretarial Standards on Board's Report

Secretarial Standards

:htt

p://w

ww

.icsi.edu/S

ecre

tarialS

tand

ard

s.a

sp

x

Protection for minority shareholders

Exit option to shareholders in case of dissent to change in object for which

public issue was made as well bring change in objective mention in its MOA.

Specific disclosure regarding effect of merger on following :

creditors,

KMPs, promoters &

Shareholders

The NCLT is being empowered for providing exit offer to dissenting.

shareholder in case of compromise / arrangements.

Valuation by registered valuers mandatory for certain corporate actions like

Issue other than right issues;

Issue for other than cash considerations;

Merger / Acquisitions / Dissolution / Demerger /

Takeovers

Investor Protection and relation

Central government has been empowered to prescribed class / class of

companies whose members shall not been auth. to appoint another person as

proxy [3rd proviso to 105 (1)];

Right of an investor to claim dividend even after unclaimed dividend

has been transferred to Investor Education & Protection Fund.

Provisions for applying in case of oppression which provide minimum number

of members

may apply before NCLT for safeguarding the provisions of this act i.e. 2013

In case of Co. having share capital :- 100 members or 1 / 10th

of total members or member / members holding >= 1 / 10th of

total issued share capital subject to condition that all calls have

been paid up. Or In case of Co. having not share capital 1 / 5th

of total membership.

-: Investor Relation (IR) :-

1) Encourage the whole board to get involved;

2) Explain investors the dynamics of your market;

3) Meet your performance target;

4) Attract more analyst coverage;

5) Provide a regular flow of information;

6) Target those investors who matter the most;

7) Hold a roadshow; and

8) Build social media into investor relations programmes.

like: Facebook, put Co’s profile on Facebook, LinkedIn and

Why a Company must look after this relationship ?

In very need of finance, public is only the source at first consider by a

Company So, we have to ensure such investor community remain healthy

i.e., increasing in value and in strong relationship.

So, it is imperative to look and take care of this, there are eight ways for

improvement……As below:-

Serious Fraud Investigation Office (Office)

Statutory status has been provided to SFIO by specifying the new sections

211, 212 of the act, 2011 .

SFIO shall have powers to arrest, u/s 212 (8), in respect of certain offences

stated in the act attracting the punishment for fraud.

What SFIO shall comprise ?

u/s 211(2) It shall be headed by Director, who shall be not below the grade of

joint secy. to the Government of India having knowledge and experience in

confronting the matters concerning to corporate affairs, and consist the such

number of experts appointed by Central Government possessing the ability of

and expertise in following areas:-

banking, corporate affairs,

taxation, forensic audit, capital market,

information technology, law .

Every person arrested u/s 212(6) shall be presented before the Judicial /

Metropolitan Magistrate with in clear 24 hours

Central Government is of opinion may order for investigation of the affairs of the

company on relying upon following inputs :-

On Court’s / NCLT ‘s order

On report by ROC

Suo moto

On intimation by company subject to

SR

Central

Government

210 (1) a

Section 210 (investigation into affairs into the Company) at glance

210 (2)

210 (1) c

210 (1) b

Section 210 (3) the Central Government may appoint one or more

persons as inspectors for the investigation the affairs of the company

under this section

In addition to Audit & Shareholders Investor Grievance Committees in every

listed company there should be a committee on :

CSR :- every listed entity shall constitute a committee- which based upon

achieving the criteria- known as “ CSR ” which shall comprise not less than

three executive directors at least 1 / 3rd shall be independent directors. u/s

135(1)

Nomination & Remuneration Committee :- every listed entity and such other

class of Companies as may be prescribed shall constitute a committee termed

as Nomination & Remuneration Committee which shall comprise of at least 3

non executive director at least half of them shall be independent director . u/s

178(1)

Stakeholders Relationship Committee :- every company which comprised of >

1000 shareholders; debenture holders; deposit holders and any other security

holder shall frame a committee said to be as SR committee which shall headed

by chairperson, who shall be non executive director, and such other number of

members which appointed by board of directors.

Corporate Social Responsibility;

Stakeholders Relationship Committee and

Nomination & Remuneration Committee .

New committees

Schedules

in Companies act, 2013

New Existing

MOA & AOA of the Company

(sch. I)

Useful lives to Compute

Depreciation (sch. II)

Preparation of final Accounts

(sch. III)

MD/ WTD appointment

(sch. V)

Projects or activities included

under the term ‘infrastructural

projects or facilities’ (sch. VI)

Code of Conduct for independent

Directors (sch. IV)

Activities which may be included by

the Companies in their Corporate

Social Responsibility Policies (sch. VII)

New Schedules at glance

Part I :- Guidelines of professional conduct;

Part II :- Role and functions;

Part III:- Duties;

Part IV:- Manner of appointment;

Part V:- Reappointment;

Part VI:- Resignation / Removal;

Part VII:- Separate meetings;

Part VIII: Evaluation mechanism.

Schedule IV Schedule VII

Eradicating extreme hunger and

poverty;

promotion of education;

promoting gender diversity;

Promoting gender morale;

Combating HIV, malaria and

other diseases;

Ensuring environment safety

and sustainability

To pursue social friendly

projects;

Contribution to fund set up by

CG / SG for :-

socio economic development

welfare of the SC / OBC /

women / minorities.

Activity which may form part of the

CSR policies of Cos.

Maximum strength laid down is 15 and a company may by passing special

resolution exceed its Board of Directors beyond 15 .

Prescribed class of companies is require to appoint one women director on the

governing board (there is already women director, Ms. Pallavi Shroff, on

governing Board of MSIL.

Every listed entity shall comprised with 1 / 3rd independent directors of its

board of directors.

Independent director covered u/s 149(5) r/w schedule IV.

tenure of independent director does not exceed 5 consecutive years and same

director can re-appoint after passing SR for another five years but if a company

want to go with same independent director on its governing board even after such

2 consecutive of five year then that company may do such only after expiration of

three years of such 10 years i.e. cooling period of 3 years shall be exist after 10

years.

Independent director shall at first meeting of the board, in which he is

participated, and thereafter at first meeting of such board meeting convene in

every financial year or whenever there is change in circumstances which may

affect his independency give its declaration to that effect.

There shall be a director on its governing board who resident, stayed at least for

182 days, in India preceding calendar year u/s 149 (2) .

u/s 161, appointment of additional / alternate / nominee director .

1) AOA of company may confer powers upon Board of Directors to appoint

additional director other than that who not succeeded in appointment as director

in general meeting who shall hold office up to the conclusion of next AGM from

conclusion of Ist AGM.

2) A company may appoint alternate director, if authorized by AOA , or even a

company may by passing of resolution in general meeting go for same which

shall take charge only when original director, in whose place he is appointed,

remain absent for a period >= 3 months from India.

whether a company can appoint alternate director to independent director ?

proviso to 161 (2) unless that person also eligible for designation of independent

director, a company cannot give him charge of alternate to independent director.

3) A company can appoint, only subject to AOA, any person as a director nominated

by institution / CG / SG or any other authority on its governing Board .

u/s 169, A company can remove director by passing ordinary resolution on being

specific notice given in writing at its registered office by

Director appointed by NCLT shall not be subject to section 169 i.e. Removal of

Director. and NCLT having power of such removal u/s 242 (2)(h) .

Where company go with section 163, principal of proportional representation,

then that company can not resort section 169 i.e. removal of director

section 163:- Company’s AOA may provide for appointment of 2 / 3rd of the total

numbers of directors by exercising principle of proportional representation by single

transferrable vote or by single cumulative voting/ otherwise and such principle is

open for once in every three years.

section 168 is about resignation of director, a director can resign from his

directorship after given notice to that effect to the company and shall also file a

return with statement carrying the reason for such resignation <=30 days to

concerned ROC . (MS Banga has retired from his office w.e.f. 26.10.2012)

in case company having share capital:- member or members

exercising 1 / 10th of the voting rights or holding shares on

which >=5 lac has been paid

in case company having no share capital:- by member /

members exercising 1 / 10th of total voting rights

What is independent director?

Who provides independent judgment, instill professional discipline, posses integrity,

monitor and ensure compliances and maintain the interest of the shareholders

Qualification for independent director u/s 149 (5)(e) ?

Not holds together with his relatives more than >= 2% of the voting rights of the

company u/s 149(5)(e)(iii) .

Neither himself or with his relative holds or held the designation of KMP or is or had

been an employee of holding / subsy (ies) / associate in any of the three preceding

financial year u/s 149 (5)(e)(i) .

who had not any pecuniary relationship with subsy(ies)/ holding/ promoters/

directors/ associate in any 2 preceding financial year or current year 149(5)©

None of whose relatives has or had pecuniary transaction with holding / subsy (ies)/

associate/ directors/ their promoters amounting to >= 2% of the income/ gross

turnover or 50 lac or higher amount which ever is lower u/s 149 (5)(d) .

Who neither himself nor his relatives appointed as CEO / director (by whatever

name called) of any organization for non profit and that organization received the <

25% of its total receipts from any company i.e. if received >= 25% of its receipt from

any company then said director, appointed as independent director, not said to be as

independent director u/s 149(5)(e)(iv) .

Board meeting as per Companies act 2013

u/s 173: Meetings of Board

As per section 173 of the Companies Act 2013 every Company has require to

conduct its first BM <= 30 days from the date of its incorporation besides this there

shall be minimum four meeting in every year (calendar / financial ?) and there shall

be maximum one twenty days gap b/w two BM

A meeting of the board shall be called by giving a notice of not less than seven

days (whether clear ?) of the meeting at all the address of directors registered with

Company either in hand writing/ post/ electronic means [173(3)]

The Company may convene its BM by serving a shorter notice subject to that one

independent director, if any, shall present in the BM. [proviso to 173(3)]

If in BM , convene on shorter notice ,

A director may participate in the meeting through audio visual means / video

conferencing/ in person, as may be prescribed, capable of recording the proceeding

[173 (2)]

The central government may by notification prescribed the matters which is not to

be transact with in meeting through video conferencing or audio visual means

[proviso to 173(2)]

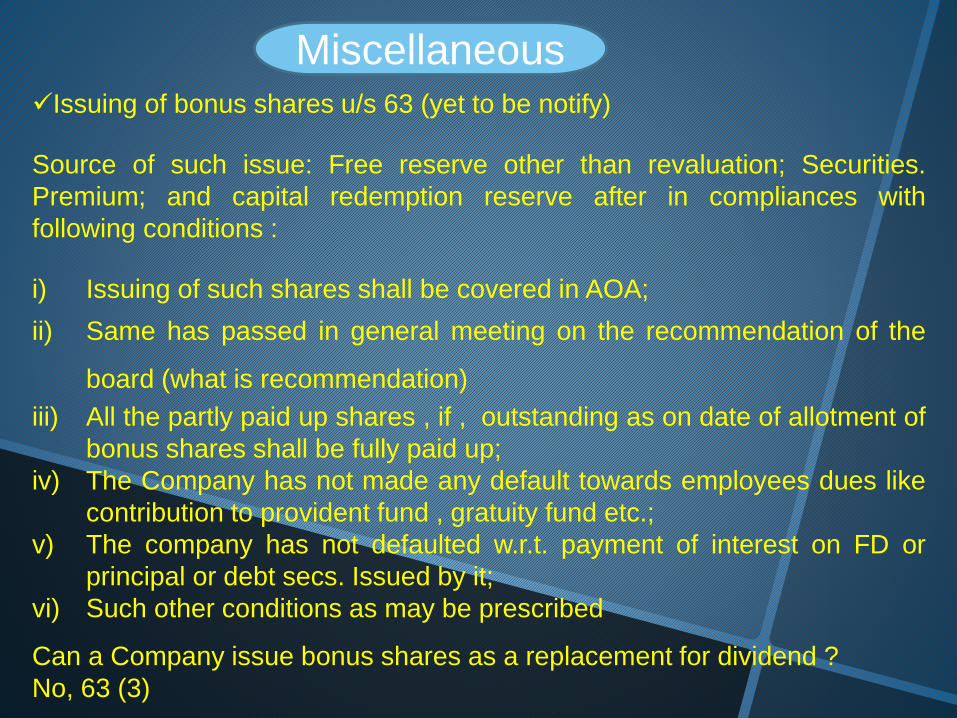

MiscellaneousIssuing of bonus shares u/s 63 (yet to be notify)

Source of such issue: Free reserve other than revaluation; Securities.

Premium; and capital redemption reserve after in compliances with

following conditions :

i) Issuing of such shares shall be covered in AOA;

ii) Same has passed in general meeting on the recommendation of the

board (what is recommendation)

iii) All the partly paid up shares , if , outstanding as on date of allotment of

bonus shares shall be fully paid up;

iv) The Company has not made any default towards employees dues like

contribution to provident fund , gratuity fund etc.;

v) The company has not defaulted w.r.t. payment of interest on FD or

principal or debt secs. Issued by it;

vi) Such other conditions as may be prescribed

Can a Company issue bonus shares as a replacement for dividend ?

No, 63 (3)

1. Punishment for Frauds u/s 447.

Every person , without prejudice to other liability, found guilty of fraud committed

fraud shall be liable for imprisonment not less than of 6 months which may

extend to 10 years and amount involved in fraud which may extend to 3 times of

such amount

If such fraud prejudicial to public interest then imprisonment shall not be less

than 3 years (proviso ).

2. Punishment for false statements u/s 448 (notified)

If any return, prospectus, financial statement, certificate , report & other

document carry the omission or containing the false statement which false in

nature than company otherwise provided in that section to which such offence

relate shall be subject to charges frame u/s 447.

3. Punishment where no specific penalty / punishment is else where provided u/s

450 (notified)

10000 and / or 1000 for every day after the first day of such contravention

continues

Can a Co. withdraw issue of bonus if once recommended by board ?

No (rule 4.12)

4. Punishment in case repeated default u/s 451

what is repeated default ?

same kind of offence , which subject to charges of imprisonment or with fine also,

committed on part of company / officer <= 3 years of previous occurrence of such

offence then such offence termed as repeated default.

penalty : twice the amount of fine laid in that section and imprisonment which

provided in that offence Non disclosure of information in certain cases u/s 457

5. Dissolution of CLB & consequential provisions u/s 466

6. Power of court to grant relief in certain cases u/s 463

7. Dormant Company, u/s 455 , means inactive Company which has not does any

significant accounting transaction or any operation in consecutively 2 F.Y. , such

Company may apply for this status and then ROC will issue a certificate to that

effect.

ROC may on suomoto give a notice to Company (ies) not filed financial statements

or annual returns for two consecutively 2 F.Y.

8. Punishment for false evidence u/s 449.

10 lac and 3 years – 7 years.

Compounding (not notified yet) of offences under new legislation

Q:- what offences eligible for compounding ?

Ans:- u/s 441, notwithstanding anything contained in Cr PC, 1973, any offences

which is subject to fine only shall be eligible for compounding either

committed by company / officer u/s 441 (1)

Q:- when same type of offence shall be eligible for compounding?

Ans:-u/s 441 (2) , if same kind of offence committed by any company / officers

after the expiry of 3 years of such date, when such offence was committed,

shall be treated as fresh offence so shall be eligible for same.

Q:- what is competent authority for compounding ?

Ans u/s 441 (1) (a & b )

Q- when can offender (company / officer) apply for compounding ?

Ans;- A company/ Person may apply for compounding either before institution

or after institution of prosecution by giving a intimation to that effect by filling an

application with in 7 days from the date when such offence is so compounded.

who shall forwarded the same before competent authority with its comments.

NCLT / if amount of fine not more than 5 lac then Regional director or

any other person appointed by Central Government.

Q-which type of offence require previous sanction of special court (fast tract

court) for amicably settlement under this act ?

Ans:- u/s 441 (6) (a & b) , Notwithstanding anything contained in Cr. PC,

1973, offences which involve the following charges shall require previous

sanction of fast track court :

imprisonment / fine;

imprisonment / fine / both; or

Q:- which offences totally debar from compounding ?

Ans- u/s 441 (6) (b), which involve the charges of imprisonment and fine also or

imprisonment only .

Q:- procedure of compounding ?

Ans – u/s 3 (a & b)

ROCCompetent Auth.

(NCLT/ RD)

Co /

officer

Application carrying

Intimation

<=7 days from

such date when

such offence is

committed

Who shall

forwarded the

same along with

its comments to

Q- what shall be the effect of application filled u/s 441(3)(a)

Ans- u/s 441 (3) (C) termination of prosecution resorted by ROC / shareholder /

central government ,where such compounding brought by ROC in writing before

court where prosecution is pending against offender in relation to which such

compounding is relate. or no such prosecution shall be taken in any other case .

Q:- Difference between consent mechanism / compounding mechanism ?

Ans:- Consent mechanism refers to settlement of a case dealing with alleged

flouting of securities laws without the individual or company involved admitting or

denying guilt. The alleged party gets absolved of the charges by paying a mutually

agreed penalty to the SEBI

Consent order guidelines

http://www.sebi.gov.in/cms/sebi_data/attachdocs/1291879532674.pdf

Frequently Asked Questions (FAQs) on consent & compounding mechanism

http://www.sebi.gov.in/faq/consentord-faq.pdf

Sebi comes out with new rules on consent orders

http://economictimes.indiatimes.com/articleshow/13492975.cms?prtpage=1

Sebi alters consent order mechanism norms; warns cos of stern action

http://articles.economictimes.indiatimes.com/2013-01-09/news/36237835_1_consent-

mechanism-market-misconduct-sebi-today

SEBI alters consent mechanism norms

http://www.moneylife.in/article/sebi-alters-consent-mechanism-norms/30653.html

Economic times articles on New legislation :

Corporate restructuring facilitated:

http://economictimes.indiatimes.com/opinion/guest-writer/corporate-restructuring-

facilitated/articleshow/17947788.cms

New Companies act to bestow more discretionary powers on government

http://economictimes.indiatimes.com/news/economy/policy/New-Companies-act-to-bestow-more-

discretionary-powers-on-government/articleshow/17933076.cms

Corporate governance: How new rules will change Indian companies

http://economictimes.indiatimes.com/news/news-by-company/corporate-trends/Corporate-governance-

How-new-rules-will-change-Indian-companies/articleshow/17932862.cms

Don't treat CSR as an additional tax: Govt to companies

http://economictimes.indiatimes.com/news/economy/policy/dont-treat-csr-as-an-additional-tax-govt-to-

companies/articleshow/17855335.cms

SFIO to get more powers, act as deterrent to frauds: Sachin Pilot

http://economictimes.indiatimes.com/news/economy/policy/sfio-to-get-more-powers-act-as-deterrent-to-

frauds-sachin-pilot/articleshow/17910958.cms

New intelligence unit to detect corporate frauds: Sachin Pilot

http://economictimes.indiatimes.com/news/news-by-company/corporate-trends/new-intelligence-unit-to-

detect-corporate-frauds-sachin-pilot/articleshow/17818050.cms

Satyam made us smarter; auditors can't get cosy with management: MCA Sachin Pilot

http://economictimes.indiatimes.com/news/news-by-industry/banking/finance/satyam-made-us-smarter-auditors-

cant-get-cosy-with-management-mca-sachin-pilot/articleshow/17755007.cms

Disclose CEO pay in perspective of staff salaries: Govt to companies

http://economictimes.indiatimes.com/news/news-by-company/corporate-trends/disclose-ceo-pay-in-perspective-

of-staff-salaries-govt-to-companies/articleshow/17767868.cms

SFIO asked to probe fraud by 83 companies since 2008: Sachin Pilot

http://economictimes.indiatimes.com/news/news-by-company/corporate-trends/sfio-asked-to-probe-fraud-by-83-

companies-since-2008-sachin-pilot/articleshow/17599206.cms

Over 100 cases of suspected frauds to overflow to 2013

http://economictimes.indiatimes.com/news/politics-and-nation/over-100-cases-of-suspected-frauds-to-overflow-

to-2013/articleshow/17704744.cms

Highlights of Companies act, 2011

http://economictimes.indiatimes.com/article show/17712030.cms

How India Inc can make their CSR spends count

http://economictimes.indiatimes.com/news/news-by-company/corporate-trends/how-india-inc-can-make-their-

csr-spends-count/articleshow/17865338.cms

Companies give employees a nudge for corporate social responsibility

http://economictimes.indiatimes.com/news/news-by-industry/jobs/companies-give-employees-a-nudge-for-

corporate-social-responsibility/articleshow/17975936.cms

Companies act made easy in 10 steps

http://www.business-standard.com/india/news/nvidia-iit-delhi-tie-up-to-build-supercomputer/200042/on