Embed Size (px)

Citation preview

www.duanemorris.com

MYANMAR Investment Opportunities

FOR DISCUSSION PURPOSES ONLY PRIVATE & CONFIDENTIAL

www.duanemorris.com

MINGALABAR!

2

www.duanemorris.com 3

• Official name: Republic of the Union of Myanmar • Strategically located between India, China and ASEAN • Capital: Nay Pyi Taw. Largest city: Yangon • Population of about 63 million (Male 49.7%, Female 50.3%). • Form of Government – Presidential Constitutional Republic (Current President: U Thein Sein) • Total area: 676,578 sq. km. • Total GDP: USD82,679 billion. • GDP per capita: USD1,324

Introduction

www.duanemorris.com

• Large population (60 million / 25% below 30 years old) • Huge potential for growth (only 4% population in consumer class) • Abundant natural resources (petroleum, natural gas, metals, and

precious stones) • Massive need for infrastructure development

www.duanemorris.com

Challenges

5

• Poor infrastructure, power shortages. • Legal system in state of flux and uncertainty • Political risks and uncertainty • Primitive banking system • Foreign exchange regulations • Weak educational system • Corruption and cronyism

www.duanemorris.com

• Myanmar Foreign Investment Law 2012 • US bans on most Myanmar imports lifted • US$6 billion (60% of total) worth of debt written off by foreign

creditors • 7 new proposed industrial zones • Hotel zones increased from 11 to 25. • SEA Games 2013 to be hosted in Myanmar • General Elections scheduled in 2015

www.duanemorris.com

MYANMAR

INVESTMENT REGULATORY FRAMWORK

7

www.duanemorris.com

Investment Framework

8

Foreign Investment

Entity Types • Incorporate a company (100% foreign-owned

or JV with Myanmar citizen or organisation)

• Register a branch office or representative office

Key Considerations • Intended business

activity • Taxation and

applicable incentives • Share capital

requirements • Shareholding structure

www.duanemorris.com

Investment Framework

9

MYANMAR COMPANIES ACT 1914

• 100% foreign-owned or JV with Myanmar entity

• Minimum of 2 shareholders • Minimum capital requirements US$150,000 for Manufacturing-

related business US$50,000 for Service-related

business

MYANMAR FOREIGN INVESTMENT LAW 2012 • 100% foreign-owned or JV with

Myanmar entity • Minimum capital requirements

may be determined by Myanmar Investment Commission (“MIC”)

• Due diligence conducted by MIC on the Investor – experience, financial standing and on investment project

www.duanemorris.com

Myanmar Foreign Investment Law (“MFIL”) 2012

10

• New MFIL 2012 (Law No. 21/2012) • Replaces previous MFIL 1988 • New improved investment incentives offered to foreign

investors • Restrictions on foreign investment on certain business

activities • Regulatory authority: Myanmar Investment Commission

(“MIC”)

www.duanemorris.com

MFIL 2012 Investment Incentives

11

• Right of Land Use / Lease (50 years +10 +10) • Tax incentives (5 years tax holiday, income tax relief on

profits from export etc) • Transferability of ownership • Foreign exchange • Dispute resolution and treaties

www.duanemorris.com

Myanmar Foreign Investment Rules (Jan 2013)

12

• Myanmar Foreign Investment Rules (Notification No. 11 of 2013) released in January 2013

• Foreign ownership in restricted business activities now allowed up to 80%

• MIC given more authority as government body • Directorate of Investment and Company Administration

(“DICA”) given more power over foreign investments

www.duanemorris.com

MIC Notification No. 1/2013 • Issued by the MIC on 31 January 2013 • Sets out list of prohibited and permitted activities for foreign

investors Mining: for large scale mining activities requires a local JV partner Real estate: Development of commercial and residential real

estate requires a local JV partner Oil & gas: Drilling for oil and gas from shallow wells of less than

1000 feet is generally not allowed Casino-related: special permission from the Govt and must follow

rules and regulations stipulated by Ministry of Hotel & Tourism

www.duanemorris.com 14

EMPLOYMENT

www.duanemorris.com

Employment

15

Foreigner • No work permit system implemented yet • Foreigners (MIC companies) may apply for a stay permit

(max. 9-month validity + special multiple re-entry visa) • Most foreigners usually enter and stay in the country on the

basis of business trips with business visas (max. 6/12 month validity / max. stay period: 70 days)

• No foreigners may be employed for jobs requiring no or low skills

www.duanemorris.com

Employment

16

Locals • 25% / 50% / 75% of an MIC company’s skilled employees

must be Myanmar citizens in the first and second / third and fourth / fifth and sixth year of operation

• Obligation to submit annual training plan • More practical than legal issues • Lack of skilled staff (e.g. marketing staff) • Job-hopping • Wildcat strikes (typically, more common in manufacturing

sector).

www.duanemorris.com

TAXES

www.duanemorris.com

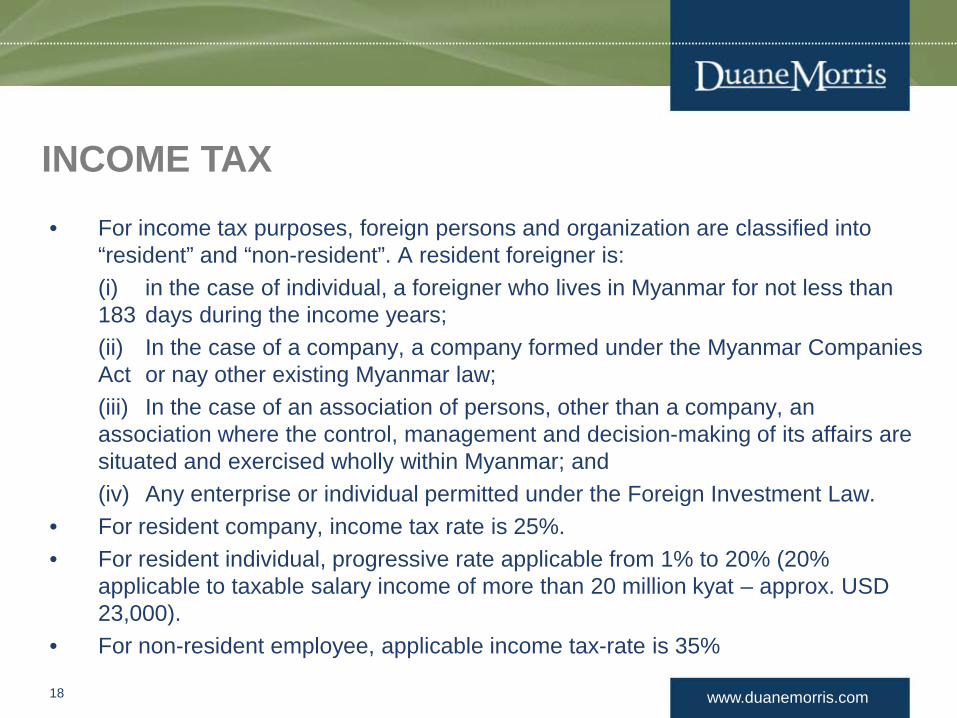

INCOME TAX

18

• For income tax purposes, foreign persons and organization are classified into “resident” and “non-resident”. A resident foreigner is:

(i) in the case of individual, a foreigner who lives in Myanmar for not less than 183 days during the income years;

(ii) In the case of a company, a company formed under the Myanmar Companies Act or nay other existing Myanmar law;

(iii) In the case of an association of persons, other than a company, an association where the control, management and decision-making of its affairs are situated and exercised wholly within Myanmar; and

(iv) Any enterprise or individual permitted under the Foreign Investment Law. • For resident company, income tax rate is 25%. • For resident individual, progressive rate applicable from 1% to 20% (20%

applicable to taxable salary income of more than 20 million kyat – approx. USD 23,000).

• For non-resident employee, applicable income tax-rate is 35%

www.duanemorris.com

WITHHOLDING TAX

19

• Dividends – No tax is levied on dividend paid to a resident or nonresident company.

• Interest – No tax is withheld on interest paid to a resident company; the rate is 15% on interest paid to a nonresident.

• Royalties – Royalties paid to a resident are subject to a 15% withholding tax; the rate is 20% for royalties paid to a nonresident.

• Other – Amounts paid to a resident for the procurement of goods within the country and services rendered (including technical services fees) are subject to a 2% withholding tax; the rate is 3.5% if paid to a nonresident company.

www.duanemorris.com

FOREIGN CURRENCY TRANSFER

20

www.duanemorris.com

FOREIGN CURRENCY TRANSFER • Right to Transfer Foreign Currency • A person who has brought in foreign capital can

transfer the following: - foreign currency entitlement of the person - net profit after deducting all taxes and provisions - foreign currency permitted for withdrawal by the MIC

which may include the value of assets on the winding up of business.

- A foreign employee can transfer its salary and lawful income after deducting taxes and other living expenses incurred domestically.

www.duanemorris.com

TRADEMARKS

22

www.duanemorris.com

TRADEMARKS

23

• No codified intellectual property law yet, but trademarks can as matter of practice be registered with the Registration of Deeds Office on the basis of the Registration Act of1908.

• Remedies against infringements: - Civil (temporary or perpetual injunction; damages); - Criminal (sections 478-489 of Penal Code) • New IP Law to be announced in 2014?

www.duanemorris.com 24

Kzeizu tin Badei!