Embed Size (px)

Citation preview

April 2014 Copyright - Anil Chawla Law Associates LLP 2

A. Meaning of CSR

B. Applicability & Spending

C. Constitution of CSR Committee

D. Implementation of CSR Strategy

E. CSR Activities

F. Mode of Carrying CSR Activities

G. Reporting Requirements

H. Analysis of CSR Spending

I. Penalties

J. Brainstorming Questions

3

A1. Companies Responsible for CSR

• Net Worth of Rs. 500 Crores (Rs. Five Billion) or more OR

• Turnover of Rs. 1000 Crores (Rs. Ten Billion) or more OR

• Net Profit of Rs. 5 Crores (Rs. Fifty Million) or more

April 2014Copyright - Anil Chawla Law Associates

LLP4

Every company (whether private or public) with:CRITERIA

Net Worth ≥ Rs. 500 Cr.

Turnover ≥ Rs. 1,000 Cr

Net Profit ≥ Rs. 5

Cr.

5

Every company that satisfies prescribed threshold is required to spend

at least 2% of its average net profit of 3 preceding financial years on

specified CSR activities

Section 3(d) of the proposed CSR Rules, defines Net Profit for

domestic company as: “Net profit before tax as per books of

accounts and shall not include profits arising from branches

outside India‘

“Net profit” for a foreign company means the net profit as per profitand loss account prepared in terms of section 381(a)(1) read with

section 198 of the Companies Act, 2013.

The ‘average net profit’ shall be calculated in accordance with

section 198 [i.e., calculation of net profit prescribed for the purpose of

determining the maximum managerial remuneration]

AMOUNT TO BE SPENT ON CSR ACTIVITIES

COMPUTATION OF PROFIT AS PER SEC 198

6

+/- Particulars Amount

Net profit after tax

XX

+ Allowed Credits

XX

- Credits Disallowed

X

+ Expenses Allowed

X

- Expenses Disallowed

XX

Allowed Credits

Expenses allowed

Expenses Disallowed

Credit Disallowed

Profit on sale of immovable property ( Original Cost – WDV )

Premium on shares or debentures ,Profit on sale of forfeited shares ,

Surplus in P&L on measurement of asset or liability at fair value

Usual Working Charges , Director’s Remuneration, Bonus or Commission paid to Staff , Interest on Loans, Depreciation.

Income Tax ,Compensations, damages or payments made voluntarily ,Capital Loss on sale ofundertaking or part thereof

CONSTITUTION OF CSR COMMITTEE

PRIVATE COMPANY

PUBLIC COMPANY

Composition of CSR committee should be 3 or more directors.

Out of which at least 1 director shall be an independent dIrector

Composition of CSR committee should be 3 or more directors;

If there is no independent director, then any 3 directors may be members of CSR committee.

Foreign COMPANY

Consist of atleast 2 Person

Out of which 1 shall be as specified u/s 380(d)(1)

Other nominated by foreign Company

CSR COMMITTEE ROLE OF THE BOARD

Formulate & Recommend a CSR Policy

Recommend CSR Initiatives

Monitor CSR expenditure

Form CSR Committee

Approve CSR Policy

Ensure Implementation

Disclose CSR Policy on the company’s website

Disclose reasons for not spending amount

STAGES EXPECTED OUTPUT

COMPLIANCE

CHECK

STRUCTURING

OPTIONS

CSR POLICY

DRAFTING

Program

implementation &

monitoring

Review &

Reporting

COMPLIANT LIST OF CSR PROJECT IDENTIFIED

CSR SPENDS IDENTIFIED

IMPLEMENTATION STRUCTURE STREAMLINED

NEW AREAS IDENTIFIED

CSR POLICY DRAFTED

TAX IMPLICATION IDENTIFIED

CREATING SOPS

REALIBLE DATA

IMPACT ASSESSMENT REPORT

ANNUAL CSR REPORT

Eradication of Hunger & Poverty

Protection of National

Heritage, Art & Culture

Environment Sustainability

Benefit of Armed Forces

Veterans

Training to Promote

Rural Sport

Contribution to PM

National Relief Fund

Rural Development

Project

Gender Equality &

Women Empowerment

SwachhBharat

Abhiyan

Restriction on Activities

Activities not mentioned in Company’s CSR Policy – Rule 4(1)

Activities conducted in normal course of business – Rule 4(1)

Activities conducted outside India – Rule 4 (4)

Activities benefitting only employees or families not allowed –

Rule 4 (5)

Building CSR capabilities of employees beyond 5% of CSR

expenditure – Rule 4(6)

Contribution to political party – Rule 4(7)

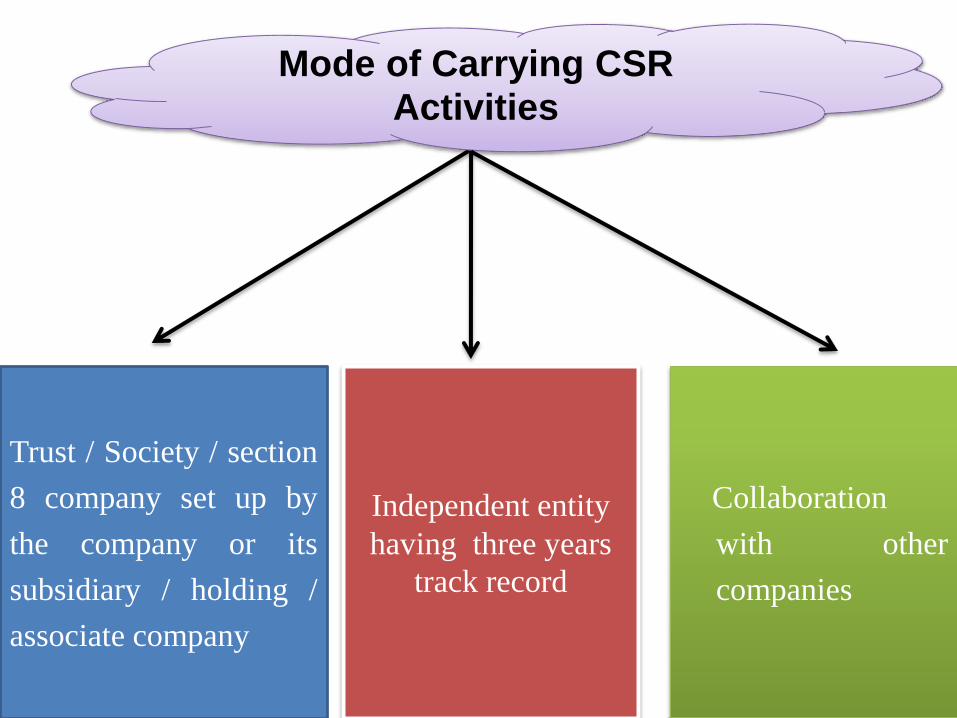

Mode of Carrying CSR Activities

Trust / Society / section

8 company set up by

the company or its

subsidiary / holding /

associate company

Independent entity

having three years

track record

Collaboration

with other

companies

ALTERNATE 1 ALTERNATE 2 ALTERNATE 3

COMPANY 1 COMPANY 2 COMPANY 1 COMPANY 2

In-house CSR Activity

Govt Schemes / Independent NGOs

Not For-profit arm of the group

CSR ACTIVITIES CARRIED OUT BY EMPLOYEES

Donation to government schemes / independent NGOs

Corporate group forms separate not-for Profit arm to carry out CSR activities

Directors’ Report to include contents of CSR Policy {Sec.

135(4)(a)}

Directors’ Report to General Meeting to include a report about

CSR initiatives as per format in Rule 8 { CSR POLICY RULES

2014 }

Company website to disclose company’s CSR Policy as per Rule

9 { CSR POLICY RULES 2014 }

If there is a failure to spend CSR amount, Board shall in its

report specify the reasons – Sec. 135(5)

1 2 3 4 5 6 7 8

SNO.

CSR PROJECT OR ACTIVITY IDENTIFI-ED

SECTOR IN WHICH THE PROJECT IS COVERED

PROJECT OR PROGRAMME1) LOCAL

AREA

2) SPECIFYTHE STATE AND DISTRICT

AMOUNT OUTLAY PROJECT OR PROGRAM WISE

AMOUNT SPENT ON THE PROJECTSOR PROGRAM

TOTALEXPEN-DITURE UPTO DATE

AMOUNTSSPENT : DIRECT OR THROUGH IMPLEM-ENTINGAGENCY

1

2

PENALTY ON NON REPORTING

COMPANY OFFICER IN DEFAULT

MAX FINE - 25 LACSMIN FINE - 0.50 LACS

IMPRISONMENT- UPTO 3 YEARS

FINE 50,000 TO 5 LACS

Section Deduction available for Deduction (AMOUNT)

35(1)(ii) Sum paid to research association university, college

or other institution to be used for scientific research

1.75 TIMES OF SUM

35(1)(iia) Sum paid to a scientific R&D company for scientific

research.

1.25 TIMES OF SUM

35(1)(iii) Sum paid to research association, university college

or other institution to be used in social science.

1.25 TIMES OF SUM

35(2AA) Any sum paid to National Laboratory or a University

or IIT or a specified person with a direction that such

sum is to be used for scientific research

2 TIMES OF SUM

35CCC Any expenditure on agricultural extension project

notified by CBDT

1.5 TIMES OF SUM

35CCD Any expenditure (not being expenditure in the nature

of cost of any land or building) on any skill

development project notified by CBDT

1.5 TIMES OF SUM

35AC Sum paid to public sector company/local authority/

Etc for carrying out any eligible notified project for

promoting social and economic welfare of the public

1TIME OF SUM

Section Deduction available for Deduction (AMOUNT)

35(1)(ii) Sum paid to research association university, college

or other institution to be used for scientific research

1.75 TIMES OF SUM

35(1)(iia) Sum paid to a scientific R&D company for scientific

research.

1.25 TIMES OF SUM

35(1)(iii) Sum paid to research association, university college

or other institution to be used in social science.

1.25 TIMES OF SUM

35(2AA) Any sum paid to National Laboratory or a University

or IIT or a specified person with a direction that such

sum is to be used for scientific research

2 TIMES OF SUM

35CCC Any expenditure on agricultural extension project

notified by CBDT

1.5 TIMES OF SUM

35CCD Any expenditure (not being expenditure in the nature

of cost of any land or building) on any skill

development project notified by CBDT

1.5 TIMES OF SUM

35AC Sum paid to public sector company/local authority/

Etc for carrying out any eligible notified project for

promoting social and economic welfare of the public

1TIME OF SUM

COMPANY SHOULD

PROVIDE DONATIONS

TO TRUST WHOSE ACTIVITIES ARE ALIGNED TO SOCIAL ACTIVIES CONTAINED IN SCHEDULE VII OF CA 2013

NO DEDUCTIONS U/S 37 OF IT ACT

1961

CSR RULES CEARLY DEFINES ACTIVITIES WHICH SHALL NOT BE CONDUCTED IN

REGULAR COURSE OF BUSINESS.

S.No. Name of Country

WhetherCSR spend / reporting mandatory

1 U.K Voluntary guidelines

2 U.S.A Voluntary guidelines

3 Germany Voluntary guidelines

4 France Mandatory reporting for listed companies in Annual reports

5 Denmark Investors and state owned companies to include information on CSR in their annual Financial reports

6 Sweden Mandatory reporting by state - owned companies

7 Indonesia Natural Resource based companies must allocate budgets for CSR programs and the programs must be run according to government regulations

8 Malaysia Compulsory for companies listed on Bursa Malaysia to disclose their CSR activities or practices

CSR applicable on group companies or individual holding/Subsidiary Company ?

Provision of CSR applicable on Section 8 Companies ?

Donation of money to a trust by a company be treated as CSR Expenditure?

In case multi-locational operations, What shall be area of “preferential locations” ?

Salary paid to staff for CSR activities included in CSR Activities?

CSR provision applicable on Foreign Company having only Project office

One off event like Marathon , Advertisement campaign be considered as CSR ?

Expenditure made by Foreign Holding eligible as expense for Indian Subsidiary co. ?