Embed Size (px)

Citation preview

THE SHARIA’AH AND LEGAL ISSUES ON ITS APPLICATION AS A FINANCING FACILITY :

THE MALAYSIAN EXPERIENCE

ADVANCE FIQH MUAMALAT (IFE705)

CONTENTS

1. INTRODUCTION

2. LEGAL EVIDENCE OF AL-BAI BITHAMAN AJIL

FROM AL-QURAN AND SUNNAH OF RASULULLAH SAW

3. THE OBJECTIVES OF AL-BAI BITHAMAN AJIL

4. PILLARS AND CONDITIONS OF AL-BAI BITHAMAN AJIL

5. TRANSACTION OF AL-BAI BITHAMAN AJIL

6. SHARI’AH ISSUE RELATING THE APPLICATION OF

AL-BAI BITHAMAN AJIL

7. AL-BAI BITHAMAN AJIL PRACTICE BY ISLAMIC BANK IN MALAYSIA

8. SHARI’AH ISSUES OF AL-BAI BITHAMAN AJIL AS

A FINANCING FACILITY IN MALAYSIA

9. CONCLUSION

2

INTRODUCTION

“Al Bai Bithaman Ajil” (BBA)

(i) Literally means “to make something into a known portion or

pieces”.

(ii) Technically, means“to defer the payment into several portions for a

different time period, and every portion that is due is called al-qist”.

BBA a sale of contract in which the payment of the purchase price is

payable at a certain particular time in the future.

BBA is also known as -

(i)Bay’ al-Nasiah which means as “waiting”;

(ii)Bay’ al-Taqsit which means as “installment”;

(iii) Bay’ Muajjal which means “deferred payment sale”; or

(iv) Al-Bay’ Li Ajal: If the payment is deferred as one lump sum towards

the end of a particular period.3

INTRODUCTION

In the middle east countries, the term used is Bay’ al-Taqsit

Bank Negara Malaysia defines :

“BBA as deferred payment sale whereby the property requested

by the client is bought by the financier, who subsequently sells the

goods to the client at an agreed price, including a mark-up

(profit) for the Islamic bank. The selling price is fixed and agreed by

both parties and will remain unchanged until the end of the

payment period. The ownership of the property purchased will be

under the claim of the financier and will be handed over to the

customer upon full payment.”.

4

LEGAL EVIDENCE OF AL-BAI BITHAMAN AJIL FROM AL-QURAN AND SUNNAH OF

RASULULLAH SAW

(i) Al-Quran from surah Al-Baqarah, 2: 282.:

ه البيع وحرم الر با وأحل اللـ

‘And Allah has permitted trade and forbidden riba’.’

ين آمنوا إ ذا تداينتم ب دين إ لى أجل مسمى ذ فاكتبوه يا أيها ال

‘O you who believe! Whenever you give or take credit (tadayantum)

for a stated term, set it down in writing.’

(ii) Al-Quran from surah Al-Nisa, 4: 29:

ل إ وا أموالكم بينكم ب الباط ين آمنوا ل تأكل نك يا أيها الذ ن ترا م ا م ل أ تكو ت

‘O you who believe! Eat not up your property among yourselves in

vanities; by way of trade based on mutual consent.’

5

LEGAL EVIDENCE OF AL-BAI BITHAMAN AJIL FROM AL-QURAN AND SUNNAH OF

RASULULLAH SAW

(a) It is reported in a Hadith by a Companion, Jabir, that the Rasulullah

SAW bought a camel from him outside the city of Madinah

whereby the payment was settled later on in Madinah.

(b) In another Hadith, it was narrated by Aisha RA that the Rasulullah

SAW bought a meal from one Jew with deferred payment, and

Rasulullah SAW mortgaged his iron shirt which is made from iron.

6

THE OBJECTIVES OF AL-BAI BITHAMAN AJIL

The objectives of BBA -

(i) providing financing for the purchaser who could not afford make thefull payment of the purchase price of the purchased goods upfront soas to reduce the hardship and burden for the purchaser in providingthe full payment of purchase price to purchase the goods;

(ii) attracting potential purchaser by offering payment by way of credit forthe purchaser to purchase the goods for the immediate usage andmake payment on affordable installment over an agreed period ofpayment which eventually lead to interest free sale transaction; and

(iii) providing flexible modes of payment as under BBA, the deferredpurchase price would be settled by the purchaser through variousmodes of agreed installment payment between the seller and thepurchaser and thus, leads to smooth business transaction between theseller and the purchaser.

7

PILLARS AND CONDITIONS OF AL-BAI BITHAMAN AJIL

Seller and purchaser, where both of them must be of sound mind,

attain age of puberty and intelligent;

Subject matter, exist during the time of purchase, known by the seller

and the purchaser, lawful and permissible or halal under Shari’ah, the

seller is the owner of the subject matter and the subject matter could

be delivered to the purchaser which include the transfer of

ownership; (BBA is subjected to the condition for transaction for non-

ribawi items only. If involve ribawi items, the ribawi items have to be

of different categories and types).

Price, must be known by the seller and purchaser where the payment

must be made in the currency agreed by both of them; and

Aqad which are ijab and qabul, must be absolute, decisive and

definite language to be made in one session.8

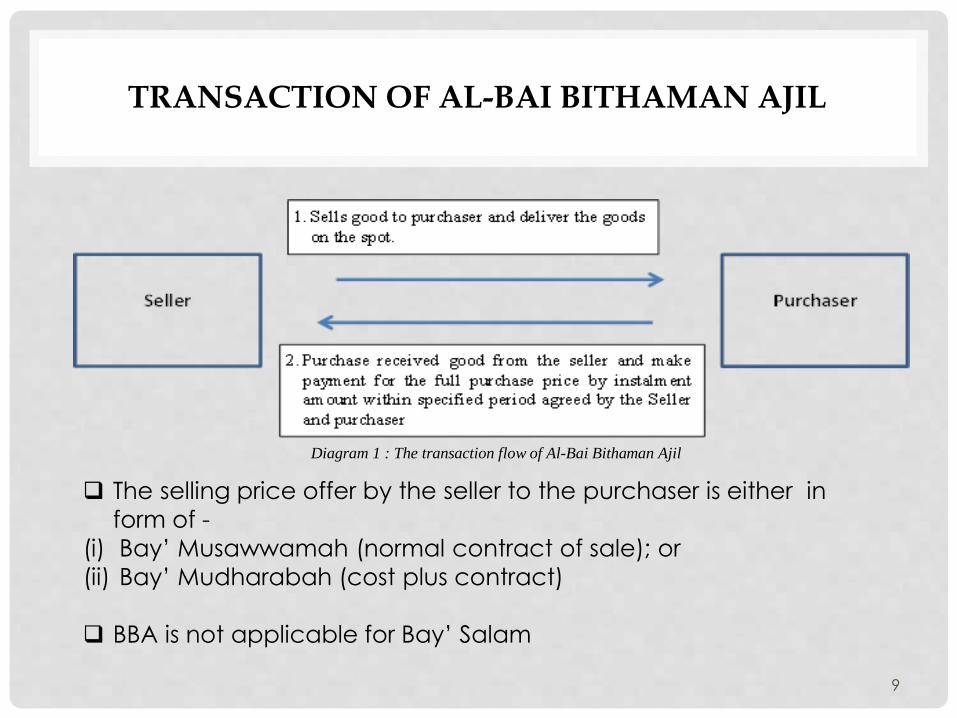

TRANSACTION OF AL-BAI BITHAMAN AJIL

The selling price offer by the seller to the purchaser is either in

form of -

(i) Bay’ Musawwamah (normal contract of sale); or

(ii) Bay’ Mudharabah (cost plus contract)

BBA is not applicable for Bay’ Salam

Diagram 1 : The transaction flow of Al-Bai Bithaman Ajil

9

SHARI’AH ISSUE RELATING THE APPLICATION OFAL-BAI BITHAMAN AJIL

Al-Bai Bithaman Ajil Resembles Riba Nasiah

The increment of the purchase price due to the delay in payment of full

purchase price of the goods, in the fixed future date as agreed between the

purchaser and the seller, which is by way of deferred payment of the full

purchase price by way of installment.

Majority of jurists, including the 4 mazhabs and Al-Kasani, Ibn Abidin and Al-

Nawawi were of the view that the price may be increased based on

deferment. Ibn Rushd of the opinion that the time has been given a share in

the price and hence, the increment of price is not a riba’ and is justifiable.

Hadith of Rasulullah SAW in one event where

“Rasulullah had ordered Amru Ibn Al-`As to prepare the army for a battle. He

then purchased a camel in exchange for a delayed payment of two camels”

The Majma` al-Fiqh al-Islamy (Academic Fiqh of OIC) has issued a resolution

number 7/2/65 stating that Bai’ al-Taqsid is permissible to be transacted as an

Islamic contract. 10

SHARI’AH ISSUE RELATING THE APPLICATION OFAL-BAI BITHAMAN AJIL

Issue on Guarantee

The seller is allow to request from the purchaser to provide and

appoint a guarantor in the event the purchaser defaulted in his

installment payment

Most of the Shari’ah scholars of the opinion that no fee could be

charged by the guarantor to the purchaser for providing the

guarantee services but the guarantor is permissible to claim actual

secretarial expenses incurred in offering the guarantee services.

The guarantor would only undertake to pay on behalf of the original

purchaser in the event he defaults of installment. If there is no default

on part of the purchaser. It would be unjust for the guarantor to

charge any fee for the guarantee service he provides for the

purchaser.

11

SHARI’AH ISSUE RELATING THE APPLICATION OFAL-BAI BITHAMAN AJIL

Rebate On Early Settlement

Discount or rebate to the purchase price when a purchaser make an

early settlement of the full purchase price. Would this early settlement

of the full purchase price amounting to breach of contract.The issue

is known as ‘da’ wa taajal’ or “give discount and receive soon”.

Some jurists of the opinion that this arrangement is permissible, but

the majority of the jurists, including the four schools of law, do not

allow it if the discount is held to be a condition for earlier payment.

Islamic Fiqh Academy of OIC took the same view.

12

SHARI’AH ISSUE RELATING THE APPLICATION OFAL-BAI BITHAMAN AJIL

Views Of Bank Negara Malaysia Shari’ah Advisory Council On Rebate –

Ibra`clause In Financing Agreement

The Shari’ah Advisory Council in its 24th meeting, held on 24th April

2002/11 Safar 1423 resolved that Islamic banking institution may

incorporate the clause on undertaking to provide ibra` to customers

who make early settlement in the Islamic financing agreement on

the basis of public interest (maslahah). This clause shall be stipulated

under the method of payment.

With the inclusion of ibra` clause in the financing agreement, the

bank is bound to honor that promise. This approach mirrors the

concept of giving discount on price or reducing the debt of the

customers who make early settlement based on the concept of dha`

wa ta`ajjal which is acceptable in Shari’ah. The confusion on the

issue of uncertainty in price (gharar) does not arise if the clause on

promise to give ibra` is stated clearly in the financing agreement.

•

13

SHARI’AH ISSUE RELATING THE APPLICATION OFAL-BAI BITHAMAN AJIL

Views Of Bank Negara Malaysia Shari’ah Advisory Council On Rebate –

Ibra` in Variable Rate Al-Bai Bithaman Ajil Product

The Shari’ah Advisory Council in its 32nd meeting on 27th February

2003/25th Zulhijjah 1423 resolved that granting of ibra` in a variable

rate BBA product is permissible. In this context, the bank is the party

who offered the ibra` (unilaterally promise to give ibra`) to the

customers and the bank may decide to give ibra` in any manner it

feels appropriate. If the bank has promised (binding promise) to give

ibra` to its customers, the bank bound to fulfill its promise.

Based on the mutual agreement in the contract, the financing

period for the customer can be extended without the need to

execute fresh contract provided that both parties fulfill all conditions

in the agreement and the final price charged on the customers shall

not exceed the original selling price (based on the ceiling profit rate)

contracted earlier.

•

14

AL-BAI BITHAMAN AJIL PRACTICE BY ISLAMIC BANKS IN MALAYSIA

BBA financing could be utilised by the Islamic bank to provide the

customers with medium and long term financing to acquire such

items as the following:

a) houses/shop houses;

b) land;

c) motor vehicles;

d) consumer goods;

e) shares;

f) overdraft facility;

g) education financing package;

h) personal financing;

i) other suitable and acceptable goods.

15

AL-BAI BITHAMAN AJIL PRACTICE BY ISLAMIC BANKS IN MALAYSIA

Agreements for BBA financing facility -

(a) The Property Purchase Agreement (PPA), Islamic bank purchase the property

from the purchaser at the purchase price, which usually the amount of

financial facility required by the purchaser.

(b) The Property Sale Agreement (PSA), the customer undertake and guarantee

to re purchase of the financed property for the Islamic bank at the agreed

selling price between the Islamic bank and the purchaser.

(c) Some other important documents to be executed by the purchaser for the

Islamic would be the security documents for securing the installment

payment of the facility amount are as follows –

(i) Legal Charge, for the property with individual titles; or

(ii) Deed of Assignment and Power of Attorney executed by the purchaser

in favour of the Islamic bank, for the property under master title and has

yet to be issued with individual titles; and

(ii) any other Islamic financing documents as required by the Islamic bank,

for instance, takaful on the property or the provision of guarantors by the

purchaser.

16

Diagram 2 : Al-Bai Bithaman Ajil flow for financing facility from Islamic bank in Malaysia. 17

AL-BAI BITHAMAN AJIL PRACTICE BY ISLAMIC BANKS IN MALAYSIA

SHARI’AH ISSUES OF AL-BAI BITHAMAN AJIL AS A FINANCING FACILITY IN MALAYSIA

Issue Of Ownership, Is Al-Bai Bithaman Ajil Is A Lending Transaction Disguise As A

Sale?

Issue of payment for stamp duty for the following agreements by the

purchaser only -

i. Sale and Purchase Agreement between the developer and purchaser;

ii. Property Purchase Agreement between the purchaser and the Islamic bank;

and

iii. Property Sale Agreement between the Islamic bank and the purchaser.

Dato’ Nik Mahmud b Daud (Appellant) v Bank Islam Malaysia Berhad

(Respondent) [1998] 3 CLJ 605.

Al-Bai Bithaman Ajil is actually does not involve of actual transfer of ownership

between the islamic bank and the purchaser but merely a right to registerable

interest of the Islamic bank in the property. All the agreements between the

Islamic bank with the purchaser is only a procedure required by the Islamic

bank to provide financial facilities to the purchaser. Thus, the whole

transaction is still a lending of money transaction rather than a sale

transaction as intended to be.

18

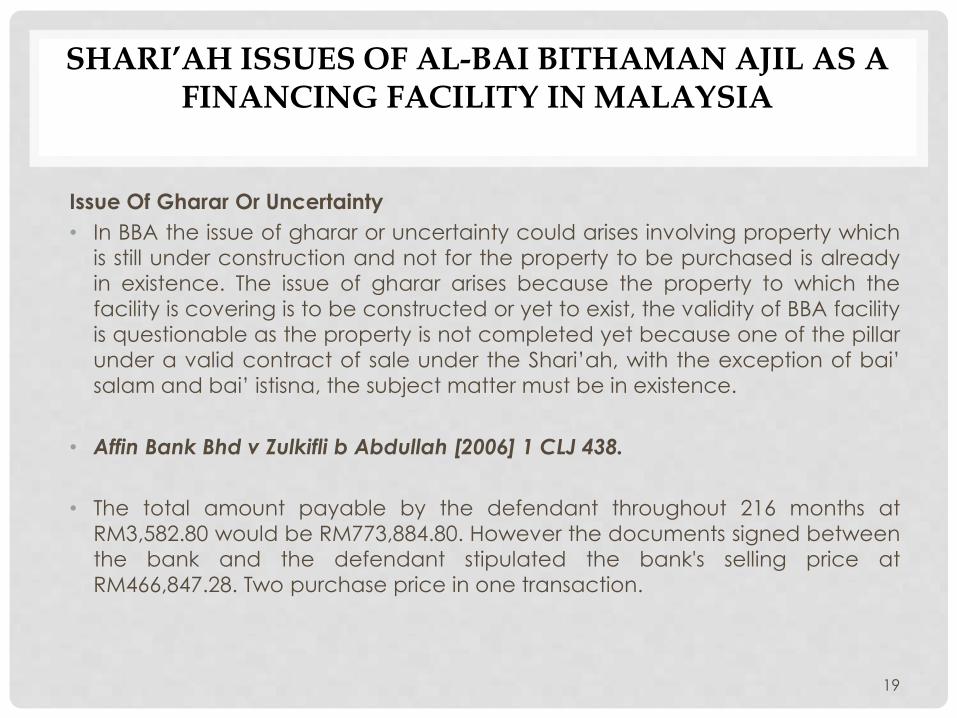

SHARI’AH ISSUES OF AL-BAI BITHAMAN AJIL AS A FINANCING FACILITY IN MALAYSIA

Issue Of Gharar Or Uncertainty

• In BBA the issue of gharar or uncertainty could arises involving property which

is still under construction and not for the property to be purchased is already

in existence. The issue of gharar arises because the property to which the

facility is covering is to be constructed or yet to exist, the validity of BBA facility

is questionable as the property is not completed yet because one of the pillar

under a valid contract of sale under the Shari’ah, with the exception of bai’

salam and bai’ istisna, the subject matter must be in existence.

• Affin Bank Bhd v Zulkifli b Abdullah [2006] 1 CLJ 438.

• The total amount payable by the defendant throughout 216 months at

RM3,582.80 would be RM773,884.80. However the documents signed between

the bank and the defendant stipulated the bank's selling price at

RM466,847.28. Two purchase price in one transaction.

19

SHARI’AH ISSUES OF AL-BAI BITHAMAN AJIL AS A FINANCING FACILITY IN MALAYSIA

The Of The Selling Price: Concept Of Justice

The primary principle of Shari’ah law is to provide justice. Any transactionthat is burdensome or oppressive to someone is absolutely prohibited.

Under BBA it could at some extent causing hardship to the customer. Thisissue is explained by the judgment of Arab Malaysian Finance Bhd vTaman Ihsan Jaya Sdn Bhd [2009] 1 CLJ 419; [2008] 5 MLJ 631 case, wherethe court found that, the facility given is far more burdensome in terms ofthe price of the property sold to the customer. This is because thepurchase price ascertained by the bank does not reflect the prevalentmarket value. It is in fact doubled or may be tripled than the amount thatthe customer received out of selling the property (the amount of facilitygiven) or even more than the amount that a customer of conventionalloan has to pay.

20

CONCLUSION

There are many legal and shari’ah issues arise in the BBA as to its

function as mode for financing facility because BBA in the first

instance is not a financing facility, it is a contract of sale. So many

aspects to be examined and studied, from the shari’ah and

Malaysian legal system, prior extending BBA function from a contract

of sale per se into a shari’ah compliance financing facility.

It is suggested that if BBA is to continue its role as a mode of

financing facility, the modus operandi and the standard operating

procedures for the application and management of BBA should be

reviewed by the Islamic banks or the authority so as to ensure that it is

in conformity with the true essence of Shari’ah principles and the

Malaysian legal system as well.

21

THANK YOU, FOR KIND ATTENTION

22