Embed Size (px)

Citation preview

0 1

Union Bank of Nigeria Plc

Annual Repo rt & Acco unts 31 December 20 15

0 2

Union Bank of Nigeria Plc

Annual Repo rt & Acco unts31 December 20 15

Table of Contents Page

No tice o f Annual General Meeting

Financ ial Highlights

Co rpo rate Pro file

Chairman's Statement

Chief Executive Officer's Statement

Directo rs, Officers and Pro fessio nal Adviso rs

Pro file o f Bo ard Members

Co rpo rate Governance

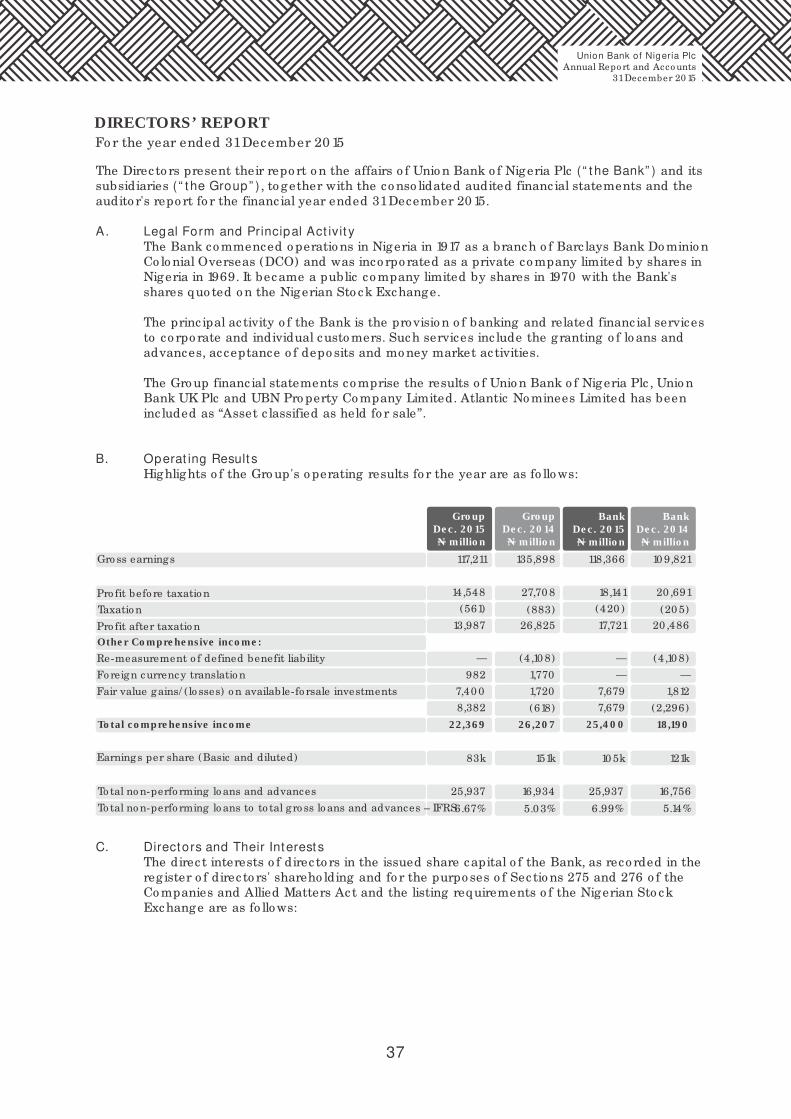

Directo rs' Repo rt

Statement o f Direc to rs' Respo nsibilities

Repo rt o f the Audit Co mmittee

Independent Audito r's Repo rt

Independent Bo ard Evaluatio n Repo rt

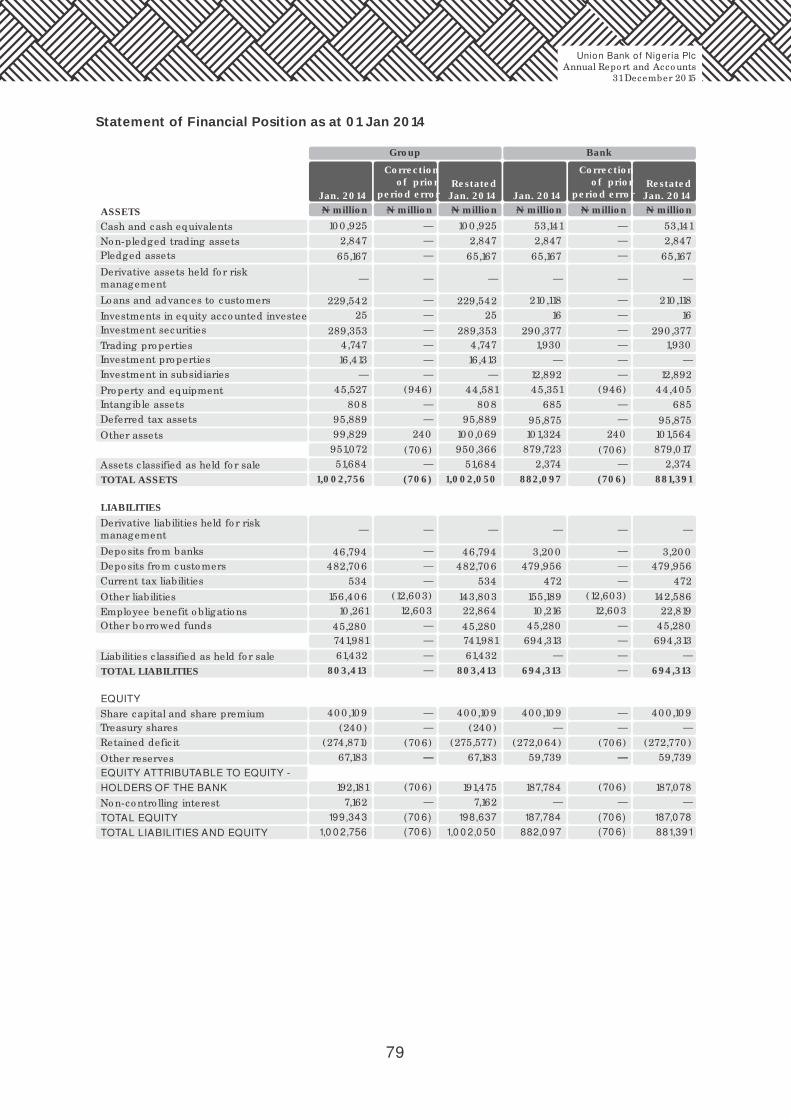

Co nso lidated and Separate Statements o f Pro fit o r Lo ss and Other Co mprehensive Inco me

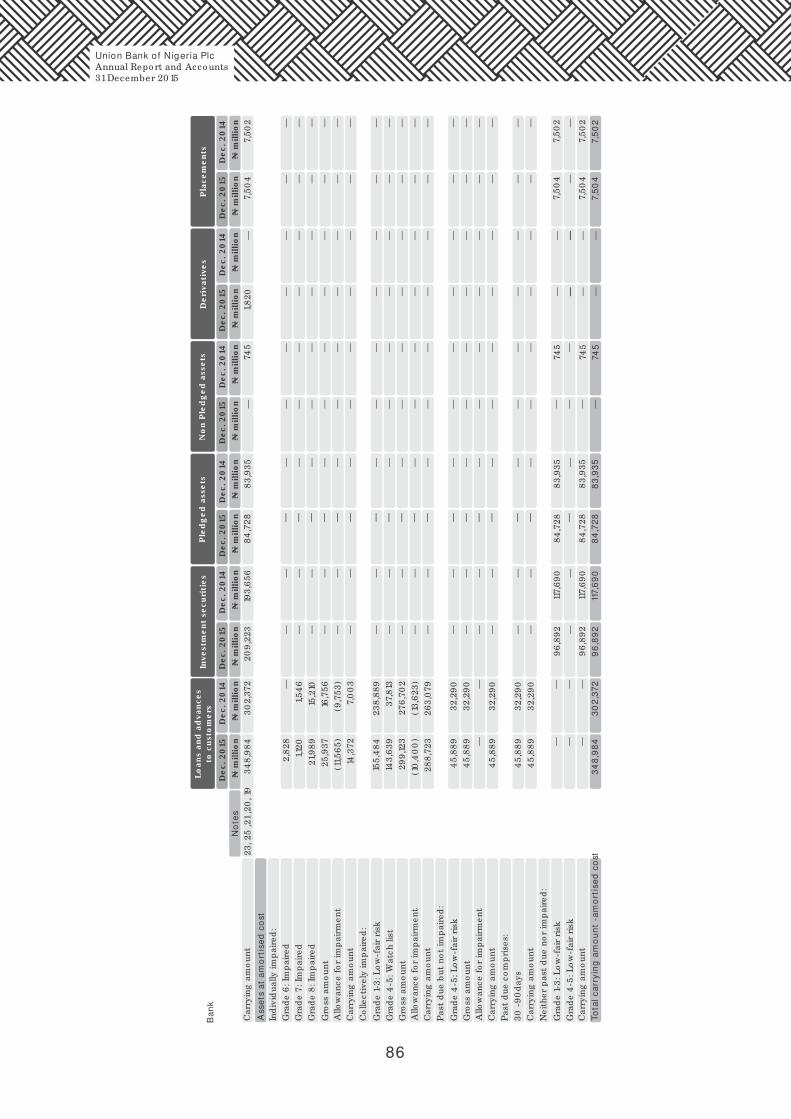

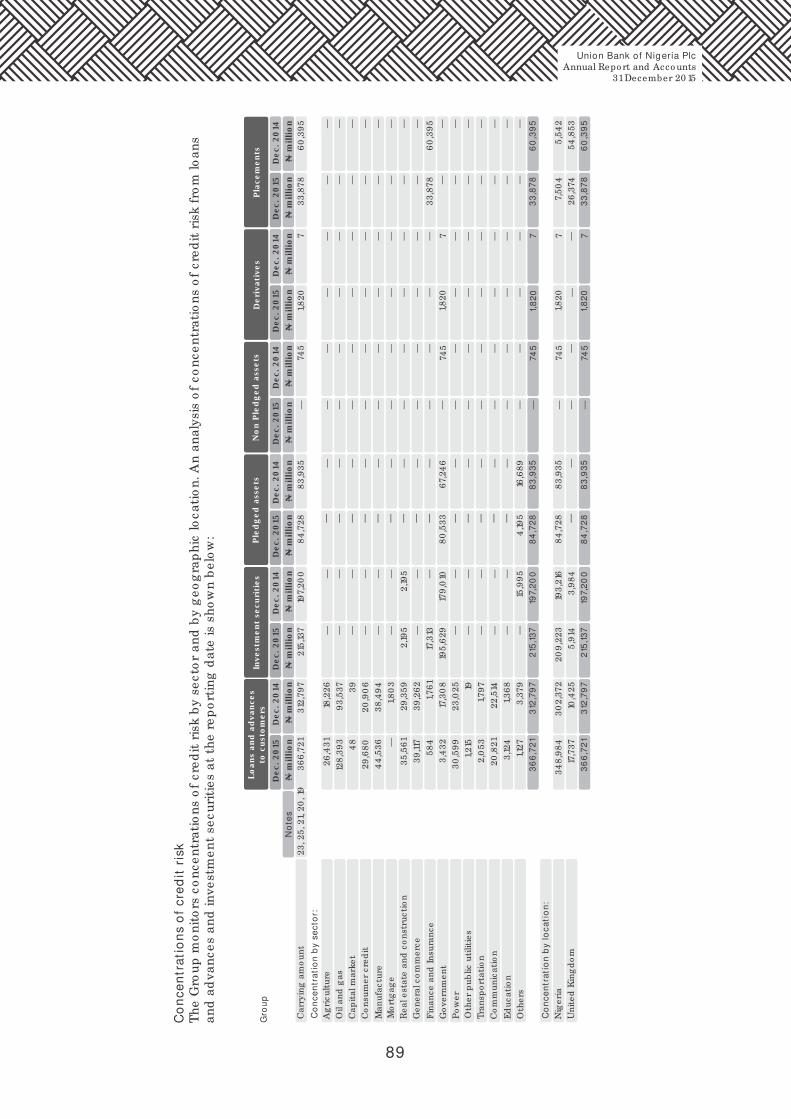

Co nso lidated and Separate Statements o f Financ ial Po sitio n

Co nso lidated and Separate Statements o f Changes in Equity

Co nso lidated and Separate Statements o f Cash Flows

No tes to the Co nso lidated Financ ial Statements

Value Added Statement

Financ ial Summary

Sales and Service Centre Lo catio ns

E-Dividend/ E-Bo nus Fo rm

Proxy Fo rm

0 3

10

11

12

16

18

20

26

37

48

49

50

52

53

54

55

57

59

142

143

145

146

156

0 3

NOTICE is hereby g iven that the 47th Annual General Meet ing (“AGM”) o f Unio n Bank o f Nigeria Plc will be held in the Ballro o m, Oriental Ho tel, 3 Lekki Ro ad, Vic to ria Island, Lago s o n Thursday, 2nd June, 20 16 at 11.0 0 a.m. to transact the fo llowing business:

ORDINARY BUSINESS

1. To receive and ado pt the Audited Gro up Financ ial Statements fo r the financ ial year ended 31st December, 20 15 to gether with the repo rts o f the Directo rs, Audito rs, Bo ard Appraiser and Audit Co mmittee.

2. To autho rize the Directo rs to fix the remuneratio n o f the Audito rs.3. To elec t/ re-elec t Direc to rs.4 . To elec t/ re-elec t members o f the Statuto ry Audit Co mmittee.

SPECIAL BUSINESS

Ord inary Resolut ion:

1. To approve the remuneratio n o f Direc to rs.

Special Resolut ions:

2. To amend the Bank's Memo randum and Artic les o f Asso c iatio n (“MEMART”) as hereinafter stated:

2(a) Alterat ion of t he MEMART

i. Deleting the Share Capital Histo ry attached to the MEMART and replac ing same with the fo llowing :

Share Capital History

1. On 7th July 1969 the autho rised share capital o f the Co mpany was increased to £10 ,0 0 0 ,0 0 0 divided into 10 ,0 0 0 ,0 0 0 o rdinary shares o f £1 each.

2. On 28th January 1971 by a Spec ial Reso lutio n, all the o rdinary shares were co nverted into 20 ,0 0 0 ,0 0 0 o rdinary shares o f N1 each (o ne Naira).

3. By a Spec ial Reso lutio n dated 10 th January 1977 the autho rised share capital o f the Co mpany was increased fro m N20 ,0 0 0 ,0 0 0 to N30 ,0 0 0 ,0 0 0 by the creatio n o f 10 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f N1 each.

4 . By a Spec ial Reso lutio n dated 23rd January 1978 the autho rised share capital o f the Co mpany was increased fro m N30 ,0 0 0 ,0 0 0 to N50 ,0 0 0 ,0 0 0 by the creatio n o f 20 ,0 0 0 ,0 0 0 o rdinary shares o f N1 each.

5. By a Spec ial Reso lutio n at the 13th AGM held o n 27th January 1982 the autho rised share capital o f the Co mpany was increased fro m N50 ,0 0 0 ,0 0 0 to N10 0 ,0 0 0 ,0 0 0 by the creatio n o f 50 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f N1 each.

6. By a Spec ial Reso lutio n passed at the 22nd AGM held o n 23rd January 1991 the autho rised share capital o f the Co mpany was further increased fro m N10 0 ,0 0 0 ,0 0 0 to N20 0 ,0 0 0 ,0 0 0 (80 0 ,0 0 0 ,0 0 0 o rdinary shares o f 25 ko bo each) by the creatio n o f 40 0 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f 25 ko bo each.

7. By a Spec ial Reso lutio n passed at the 23rd AGM held o n 29th o f January, 1992 the autho rised share capital o f the Co mpany was further increased fro m to N20 0 ,0 0 0 ,0 0 0 to N250 ,0 0 0 ,0 0 0 (1,0 0 0 ,0 0 0 ,0 0 0 o rdinary shares o f 25 ko bo each) by the creatio n o f 20 0 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f 25 ko bo each.

NOTICE OF ANNUAL GENERAL MEETING

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

0 4

8. By a Spec ial Reso lutio n passed at the 25th AGM held o n 23rd February 1994, the autho rised share capital o f the Co mpany was further increased fro m N250 ,0 0 0 ,0 0 0 to N50 0 ,0 0 0 ,0 0 0 (2,0 0 0 ,0 0 0 ,0 0 0 o rdinary shares o f 25 ko bo each) by the creatio n o f 1,0 0 0 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f 25 ko bo each.

9. By a Spec ial Reso lutio n passed at the 27th AGM held o n 27th March 1996, all the 2,0 0 0 ,0 0 0 ,0 0 0 o rdinary shares o f 25 ko bo each o f the Co mpany, were co nso lidated and divided into 1,0 0 0 ,0 0 0 ,0 0 0 o rdinary shares o f 50 ko bo each (i.e. an autho rised share capital o f N50 0 ,0 0 0 ,0 0 0 ).

10 . By a Spec ial Reso lutio n passed at the 29th AGM held o n 4th March, 1998 the autho rised share capital o f the Co mpany was increased fro m N50 0 ,0 0 0 ,0 0 0 to N1,0 0 0 ,0 0 0 ,0 0 0 by the creatio n o f 1,0 0 0 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f 50 ko bo each.

11. By a Spec ial Reso lutio n passed at the 32nd AGM held o n 8th August, 20 0 1 the autho rised share capital o f the Co mpany was increased fro m N1,0 0 0 ,0 0 0 ,0 0 0 to N3,0 0 0 ,0 0 0 ,0 0 0 divided into 6,0 0 0 ,0 0 0 ,0 0 0 o rdinary shares o f 50 ko bo each (by the creatio n o f 4 ,0 0 0 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f 50 ko bo each).

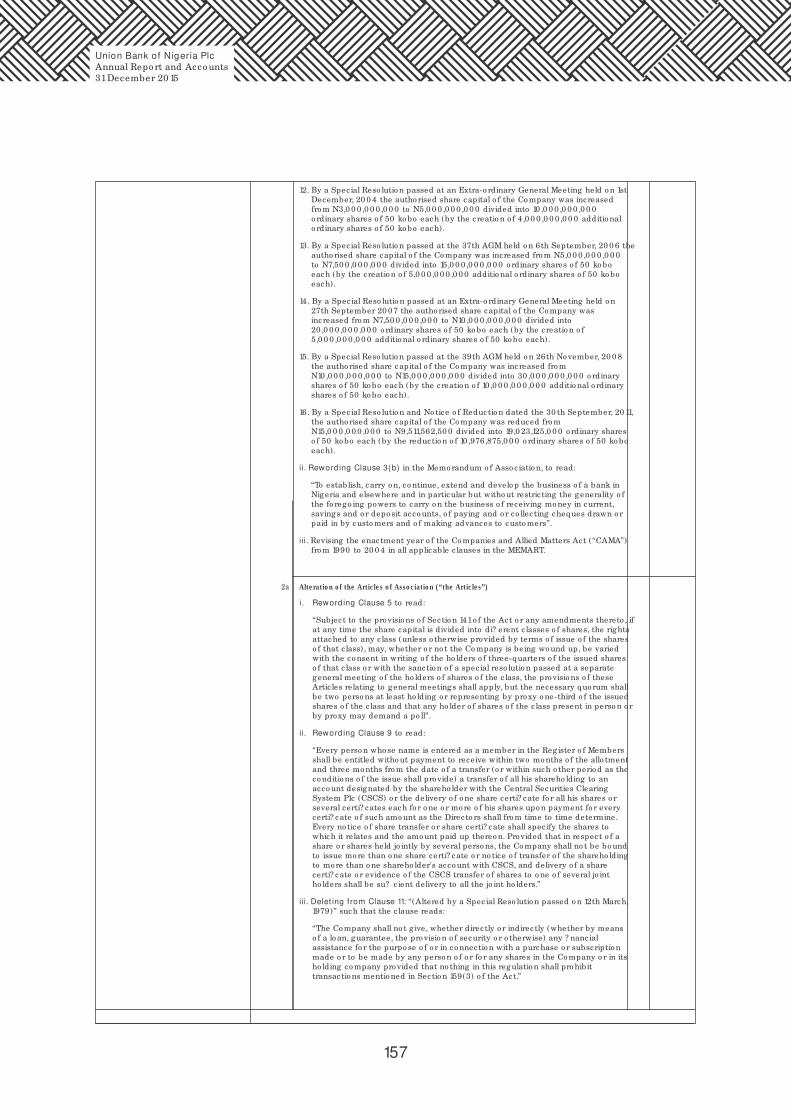

12. By a Spec ial Reso lutio n passed at an Extra-o rdinary General Meeting held o n 1st December, 20 0 4 the autho rised share capital o f the Co mpany was increased fro m N3,0 0 0 ,0 0 0 ,0 0 0 to N5,0 0 0 ,0 0 0 ,0 0 0 divided into 10 ,0 0 0 ,0 0 0 ,0 0 0 o rdinary shares o f 50 ko bo each (by the creatio n o f 4 ,0 0 0 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f 50 ko bo each).

13. By a Spec ial Reso lutio n passed at the 37th AGM held o n 6th September, 20 0 6 the autho rised share capital o f the Co mpany was increased fro m N5,0 0 0 ,0 0 0 ,0 0 0 to N7,50 0 ,0 0 0 ,0 0 0 divided into 15,0 0 0 ,0 0 0 ,0 0 0 o rdinary shares o f 50 ko bo each (by the creatio n o f 5,0 0 0 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f 50 ko bo each).

14. By a Spec ial Reso lutio n passed at an Extra-o rdinary General Meeting held o n 27th September 20 07 the autho rised share capital o f the Co mpany was increased fro m N7,50 0 ,0 0 0 ,0 0 0 to N10 ,0 0 0 ,0 0 0 ,0 0 0 divided into 20 ,0 0 0 ,0 0 0 ,0 0 0 o rdinary shares o f 50 ko bo each (by the creatio n o f 5,0 0 0 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f 50 ko bo each).

15. By a Spec ial Reso lutio n passed at the 39th AGM held o n 26th November, 20 0 8 the autho rised share capital o f the Co mpany was increased fro m N10 ,0 0 0 ,0 0 0 ,0 0 0 to N15,0 0 0 ,0 0 0 ,0 0 0 divided into 30 ,0 0 0 ,0 0 0 ,0 0 0 o rdinary shares o f 50 ko bo each (by the creatio n o f 10 ,0 0 0 ,0 0 0 ,0 0 0 additio nal o rdinary shares o f 50 ko bo each).

16. By a Spec ial Reso lutio n and No tice o f Reductio n dated the 30 th September, 20 11, the autho rised share capital o f the Co mpany was reduced fro m N15,0 0 0 ,0 0 0 ,0 0 0 to N9,511,562,50 0 divided into 19,0 23,125,0 0 0 o rdinary shares o f 50 ko bo each (by the reductio n o f 10 ,976,875,0 0 0 o rdinary shares o f 50 ko bo each).

ii. Reword ing Clause 3(b) in the Memo randum o f Asso c iatio n, to read:

“To establish, carry o n, co ntinue, extend and develo p the business o f a bank in Nigeria and, elsewhere and in particular but witho ut restric ting the generality o f the fo rego ing powers, to carry o n the business o f receiving mo ney in current, savings and o r depo sit acco unts, o f paying and o r co llec ting cheques drawn o r paid in by custo mers and o f making advances to custo mers”.

iii. Revising the enactment year o f the Co mpanies and Allied Matters Act (“CAMA”) fro m 1990 to 20 0 4 in all applicable c lauses in the MEMART.

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

0 5

2(b) A lterat ion of t he Art icles of Associat ion ( “ t he Art icles” )

i. Reword ing Clause 5 to read:

“Subjec t to the provisio ns o f Sectio n 141 o f the Act o r any amendments thereto , if at any time the share capital is divided into different c lasses o f shares, the rights attached to any c lass (unless o therwise provided by terms o f issue o f the shares o f that c lass), may, whether o r no t the Co mpany is being wo und up, be varied with the co nsent in writing o f the ho lders o f three-quarters o f the issued shares o f that c lass o r with the sanctio n o f a spec ial reso lutio n passed at a separate general meeting o f the ho lders o f shares o f the c lass, the provisio ns o f these Artic les relating to general meetings shall apply, but the necessary quo rum shall be two perso ns at least ho lding o r representing by proxy o ne-third o f the issued shares o f the c lass and that any ho lder o f shares o f the c lass present in perso n o r by proxy may demand a po ll”.

ii. Reword ing Clause 9 to read:

“Every perso n who se name is entered as a member in the Register o f Members shall be entitled witho ut payment to receive within two mo nths o f the allo tment and three mo nths fro m the date o f a transfer (o r within such o ther perio d as the co nditio ns o f the issue shall provide) a transfer o f all his shareho lding to an acco unt designated by the shareho lder with the Central Securities Clearing System Plc (“CSCS”) o r the delivery o f o ne share certificate fo r all his shares o r several certificates each fo r o ne o r mo re o f his shares upo n payment fo r every certificate o f such amo unt as the Directo rs shall fro m time to time determine. Every no tice o f share transfer o r share certificate shall spec ify the shares to which it relates and the amo unt paid up thereo n. Provided that in respect o f a share o r shares held jo intly by several perso ns, the Co mpany shall no t be bo und to issue mo re than o ne share certificate o r no tice o f transfer o f the shareho lding to mo re than o ne shareho lder's acco unt with CSCS, and delivery o f a share certificate o r evidence o f the CSCS transfer o f shares to o ne o f several jo int ho lders shall be suffic ient delivery to all the jo int ho lders.”

iii. Delet ing from Clause 11: “(Altered by a Spec ial Reso lutio n passed o n 12th March, 1979)” such that the c lause reads:

“The Co mpany shall no t g ive, whether direc tly o r indirec tly (whether by means o f a lo an, guarantee, the provisio n o f security o r o therwise) any financ ial assistance fo r the purpo se o f o r in co nnectio n with a purchase o r subscriptio n made o r to be made by any perso n o f o r fo r any shares in the Co mpany o r in its ho lding co mpany provided that no thing in this regulatio n shall pro hibit transactio ns mentio ned in Sectio n 159(3) o f the Act.”

iv. Delet ing from the Art icles:

1. Clauses 12 to 15 o n 'Lien o n Shares'. 2. Clauses 16 to 21 o n 'Calls o n Shares'. 3. Clauses 22 to 27 o n 'Transfer o f Shares'.

v. Reword ing Clause 28 to read:

“The Co mpany shall be entitled to charge a reaso nable fee o n the reg istratio n o f every pro bate, letter o f administratio n, certificate o f death o r marriage, power o f atto rney, no tice in lieu o f distringas, o r o ther instrument.”

vi. Reword ing Clause 29 to read:

“In case o f death o f a member, the survivo r o r survivo rs where the deceased was a jo int ho lder and the legal perso nal representatives o f the deceased where he was a so le ho lder shall be the o nly perso ns reco gnised by the Co mpany as having any title to his interest in the shares.”

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

0 6

vii. Reword ing Clause 30 to read:

“Any perso n beco ming entitled to a share in co nsequence o f the death o r bankruptcy o f a member may, upo n such evidence being pro duced as may fro m time to time pro perly be required by the Directo rs and subjec t as hereinafter provided, elec t either to be reg istered himself as ho lder o f the share o r to have so me perso n no minated by him reg istered as the transferee thereo f.”

viii. Reword ing Clause 31 to read:

“If the perso n so beco ming entitled shall elec t to be reg istered himself, he shall deliver o r send to the Co mpany a no tice in writing signed by him stating that he so elec ts. If he shall elec t to have ano ther perso n reg istered he shall testify his elec tio n by executing to that perso n a transfer o f the share.”

ix. Delet ing Clauses 33 to 39 on Forfeit ure of Shares.

x. Reword ing Clause 41 to read:

“The ho lders o f sto ck may transfer the same, o r any part thereo f in the same manner, and subjec t to the same regulatio ns, which the shares fro m which the sto ck aro se might prio r to co nversio n have been transferred, o r as near thereto as c ircumstances admit and the Directo rs may fro m time to time fix the minimum amo unt o f sto ck transferable but so that such minimum shall no t exceed the no minal amo unt o f the shares fro m which the sto ck aro se”.

xi. Delet ing “ or special” f rom Clause 44 such that t he Clause reads:

“The Co mpany may fro m time to time by o rdinary reso lutio n increase the share capital by such sum, to be divided into shares o f such amo unt, as the reso lutio n shall prescribe.”

xii. Delet ing Clause 45 on Pre-empt ive Rights of Shareholders.

xiii. Reword ing Clause 51 to read:

“An AGM and a meeting called fo r the passing o f a Spec ial Reso lutio n shall be called by at least twenty-o ne days' no tice in writing . A meeting o f the Co mpany o ther than an AGM o r a meeting fo r the passing o f a Spec ial Reso lutio n shall be called by at least twenty-o ne days' no tice in writing . The no tice shall be exc lusive o f the day o n which it is served o r deemed to be served and o f the day fo r which it is g iven and shall spec ify the place, the day, the ho ur o f meeting and the general nature o f the business to be transacted, and shall be g iven, in the manner hereinafter mentio ned o r in such o ther manner, if any, as may be prescribed by the Co mpany in General Meeting , to such perso ns as are under the regulatio ns o f the Co mpany, entitled to receive such no tices fro m the Co mpany.

Provided that a meeting o f the Co mpany shall, no twithstanding that it is called by sho rter no tice than that spec ified in this regulatio n, be deemed to have been duly called if it is so agreed by all the members entitled to attend and vo te thereat”.

xiv. Reword ing Clause 53 to read:

“All business shall be deemed spec ial that is transacted at an Extra-o rdinary General Meeting , and also that is transacted at an Annual General Meeting , with the exceptio n o f dec laring a dividend, the co nsideratio n o f the audited financ ial statements and the repo rts o f the Directo rs and Audito rs, the elec tio n o f Direc to rs in the place o f tho se retiring and the appo intment o f and the fixing o f the remuneratio n o f the Audito rs, which shall be deemed to be o rdinary business.”

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

0 7

xv. Reword ing Clause 56 to read:

“The Chairman, if any, o f the Bo ard o f Direc to rs shall preside as Chairman at every General Meeting o f the Co mpany, o r if there is no such Chairman, o r if he shall no t be present within thirty minutes after the time appo inted fo r the ho lding o f the meeting o r is unwilling to ac t, the Directo rs present shall elec t o ne o f their numbers to be the chairman o f the meeting”.

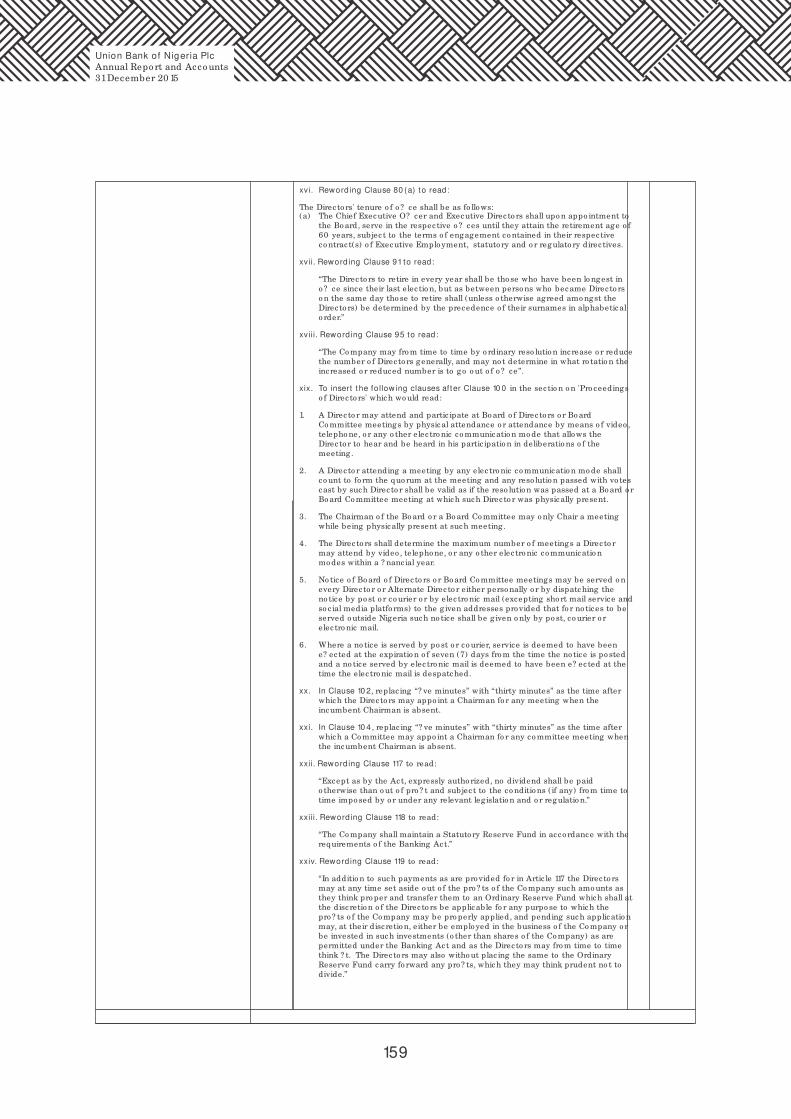

xvi. Reword ing Clause 80 (a) to read:

The Directo rs' tenure o f o ffice shall be as fo llows: (a) The Chief Executive Officer and Executive Directo rs shall upo n appo intment to the

Bo ard, serve in the respective o ffices until they attain the retirement age o f 60 years, subjec t to the terms o f engagement co ntained in their respective co ntract(s) o f Executive Employment, statuto ry and o r regulato ry direc tives.

xvii. Reword ing Clause 91 to read:

“The Directo rs to retire in every year shall be tho se who have been lo ngest in o ffice since their last elec tio n, but as between perso ns who became Directo rs o n the same day tho se to retire shall (unless o therwise agreed amo ngst the Directo rs) be determined by the precedence o f their surnames in alphabetical o rder.”

xviii. Reword ing Clause 95 to read:

“The Co mpany may fro m time to time by o rdinary reso lutio n increase o r reduce the number o f Direc to rs generally, and may no t determine in what ro tatio n the increased o r reduced number is to go o ut o f o ffice”.

xix. To insert t he fo llow ing clauses after Clause 10 0 in the sec tio n o n 'Pro ceedings o f Direc to rs' which wo uld read:

1. A Directo r may attend and partic ipate at Bo ard o f Direc to rs o r Bo ard Co mmittee meetings by physical attendance o r attendance by means o f video , telepho ne, o r any o ther elec tro nic co mmunicatio n mo de that allows the Directo r to hear and be heard in his partic ipatio n in deliberatio ns o f the meeting .

2. A Directo r attending a meeting by any elec tro nic co mmunicatio n mo de shall co unt to fo rm the quo rum at the meeting and any reso lutio n passed with vo tes cast by such Directo r shall be valid as if the reso lutio n was passed at a Bo ard o r Bo ard Co mmittee meeting at which such Directo r was physically present.

3. The Chairman o f the Bo ard o r a Bo ard Co mmittee may o nly Chair a meeting while being physically present at such meeting .

4 . The Directo rs shall determine the maximum number o f meetings a Directo r may attend by video , telepho ne, o r any o ther elec tro nic co mmunicatio n mo des within a financ ial year.

5. No tice o f Bo ard o f Direc to rs o r Bo ard Co mmittee meetings may be served o n every Directo r o r Alternate Directo r either perso nally o r by dispatching the no tice by po st o r co urier o r by elec tro nic mail (excepting sho rt mail service and so c ial media platfo rms) to the g iven addresses provided that fo r no tices to be served o utside Nigeria such no tice shall be g iven o nly by po st, co urier o r elec tro nic mail.

6. Where a no tice is served by po st o r co urier, service is deemed to have been effec ted at the expiratio n o f seven (7) days fro m the time the no tice is po sted and a no tice served by elec tro nic mail is deemed to have been effec ted at the time the elec tro nic mail is despatched.

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

0 8

xx. In Clause 10 2, replac ing “five minutes” with “thirty minutes” as the time after which the Directo rs may appo int a Chairman fo r any Bo ard o r o ther meeting when the incumbent Chairman is absent.

xxi. In Clause 10 4 , replac ing “five minutes” with “thirty minutes” as the time after which a Co mmittee may appo int a Chairman fo r any Bo ard co mmittee o r o ther meeting when the incumbent Chairman is absent.

xxii. Reword ing Clause 117 to read:

“Except as by the Act, expressly autho rised, no dividend shall be paid o therwise than o ut o f pro fit and subjec t to the co nditio ns (if any) fro m time to time impo sed by o r under any relevant leg islatio n and o r regulatio n.”

xxiii. Reword ing Clause 118 to read:

“The Co mpany shall maintain a Statuto ry Reserve Fund in acco rdance with the requirements o f the Banking Act.”

xxiv. Reword ing Clause 119 to read:

“In additio n to such payments as are provided fo r in Artic le 117 the Directo rs may at any time set aside o ut o f the pro fits o f the Co mpany such amo unts as they think pro per and transfer them to an Ordinary Reserve Fund which shall at the discretio n o f the Directo rs be applicable fo r any purpo se to which the pro fits o f the Co mpany may be pro perly applied, and pending such applicatio n may, at their discretio n, either be employed in the business o f the Co mpany o r be invested in such investments (o ther than shares o f the Co mpany) as are permitted under the Banking Act and as the Directo rs may fro m time to time think fit. The Directo rs may also witho ut plac ing the same in the Ordinary Reserve Fund carry fo rward any pro fits, which they may think prudent no t to divide.”

xxv. Reword ing Clause 120 to read:

“Subjec t to the rights o f perso ns, if any, entitled to shares with spec ial rights as to dividends, all dividends shall be dec lared and paid acco rding to the amo unts paid o r c redited as paid. All dividends shall be appo rtio ned and paid pro po rtio nately to the amo unts paid o r c redited as paid o n the shares during any po rtio n o r po rtio ns o f the perio d in respect o f which the dividend is paid; but if any share is issued in terms providing that it shall rank fo r dividends as fro m a particular date such share shall rank fo r dividend acco rding ly.”

xxvi. Delet ing Clause 121 o n “Unpaid Calls”.

xxvii. Deleting fro m Clauses 127, 128 and 129 all references to “Pro fit and Lo ss Acco unts” and “Balance Sheet” and replac ing same respectively with “Co nso lidated and Separate Statements o f Pro fit o r Lo ss and Other Co mprehensive Inco me” and “Co nso lidated and Separate Statements o f Financ ial Po sitio n”.

2(c) “That fo llowing the deletio n o f the above-stated c lauses fro m the Artic les o f the Co mpany, all the c lauses retained in the Artic les be renumbered acco rding ly and all typo graphical erro rs in the Artic les amended”.

2(d) “That all sec tio ns o f the CAMA c ited in the Co mpany's MEMART sho uld be reviewed and o r amended to ensure co rrectness”.

2(e) “That the Co mpany's MEMART inco rpo rating the above-listed amendments, be and are hereby approved and ado pted as the MEMART o f the Co mpany, in substitutio n fo r and to the exc lusio n o f all previo us editio ns thereo f”.

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

0 9

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

2(f) “That the Co mpany Secretary be and is hereby autho rised to file the amended MEMART o f the Co mpany at the Co rpo rate Affairs Co mmissio n”.

NOTES

a) PROXY

A member o f the co mpany entitled to attend and vo te is entitled to appo int a proxy to attend and vo te in its, his o r her stead. A proxy fo rm is supplied with the No tice. Executed proxy fo rms sho uld be duly stamped at the Stamp Duties Office and depo sited at the o ffice o f the Co mpany Registrar, GTL Registrars Limited, 2 Burma Ro ad, Apapa, Lago s no t less than fo rty-eight (48) ho urs befo re the meeting .

b) STATUTORY AUDIT COMMITTEE

Any member may no minate a shareho lder fo r elec tio n as a member o f the Statuto ry Audit Co mmittee by g iving no tice in writing o f such no minatio n to the Co mpany Secretary at least twenty-o ne (21) days befo re the Annual General Meeting .

c) CLOSURE OF THE REGISTER OF MEMBERS

The Register o f Members and Transfer Bo o ks o f the Co mpany will be c lo sed fro m Mo nday, 16th May 20 16 to Friday, 20 th May 20 16 (bo th days inc lusive).

d) RIGHT OF SHAREHOLDERS TO ASK QUESTIONS

Pursuant to Rule 19.12 (c ) o f the Nigerian Sto ck Exchange's Rulebo o k 20 15, kindly no te that it is the right o f every shareho lder to ask questio ns no t o nly at the meeting but also in writing prio r to the meeting . We urge that such questio ns be submitted to the Co mpany Secretariat no t later than two (2) weeks befo re the meeting date.

BY ORDER OF THE BOARD

Somuyiwa Adedeji SonubiCo mpany SecretaryFRC/ 20 13/ NBA/ 0 0 0 0 0 0 0 20 61Unio n Bank o f Nigeria PlcStallio n Plaza36 MarinaLago s

Dated the 9th day of May 20 16

10

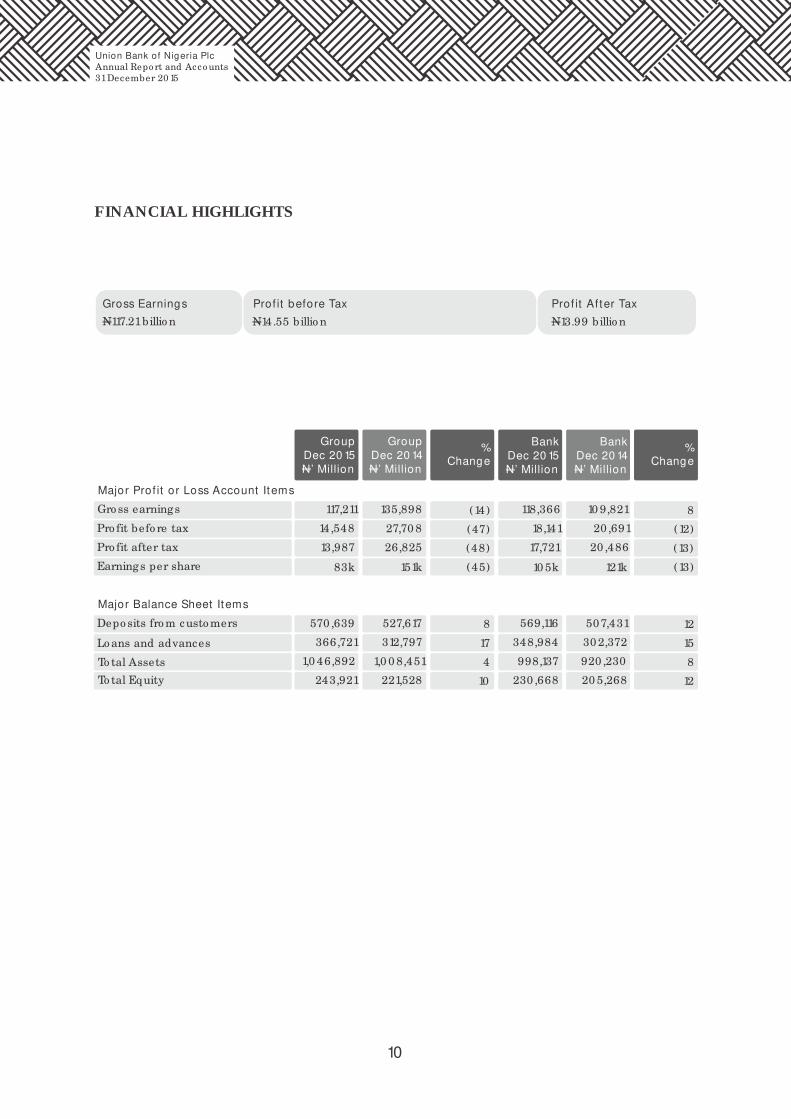

FINANCIAL HIGHLIGHTS

Gross Earnings Prof it before Tax Prof it After Tax

N117.21 billio n N14.55 billio n N13.99 billio n

Group

Dec 20 15

N’ Million

Group

Dec 20 14

N’ Million

%

Change

%

Change

Bank

Dec 20 15

N’ Million

Bank

Dec 20 14

N’ Million

Major Prof it or Loss Account Items

Gro ss earnings 117,211 135,898 (14) 118,366 10 9,821 8

Pro fit befo re tax 14,548 27,70 8 (47) 18,141 20 ,691 (12)

Pro fit after tax 13,987 26,825 (48) 17,721 20 ,486 (13)

Earnings per share 83k 151k (45) 10 5k 121k (13)

Major Balance Sheet Items

Depo sits fro m custo mers 570 ,639 527,617 8 569,116 507,431 12

Lo ans and advances 366,721 312,797 17 348,984 30 2,372 15

To tal Assets 1,0 46,892 1,0 0 8,451 4 998,137 920 ,230 8

To tal Equity 243,921 221,528 10 230 ,668 20 5,268 12

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

11

Unio n Bank o f Nigeria Plc (“UBN” o r “the Bank”) was established in 1917 and is o ne o f Nigeria's lo ng-standing and mo st respected financ ial institutio ns, o ffering a po rtfo lio o f banking services to individuals, SMEs, co mmerc ial and co rpo rate c lients.

Our o fferings inc lude current, savings and depo sit acco unt services, funds transfer, fo reign currency do mic iliatio n, lo ans, overdrafts, equipment leasing and trade finance. These services are provided thro ugh an extensive netwo rk o f over 325 sales and service centres, over 720 Auto mated Teller Machines (“ATMs”) spread acro ss Nigeria and alternate channels inc luding o nline banking , mo bile banking , debit cards and po int o f sale systems.

Fo llowing the banking refo rms initiated by the Central Bank o f Nigeria (“CBN”), UBN in September 20 12, co nc luded a successful recapitalisatio n pro cess with the injec tio n o f US$50 0 millio n by Unio n Glo bal Partners Limited (“UGPL”), a co nso rtium o f lo cal and internatio nal investo rs. UGPL acquired 65% o f the Bank's shareho lding while the Asset Management Co rpo ratio n o f Nigeria (AMCON) held 20 .0 4% with the remaining 14.96% held by a diverse gro up o f shareho lders. In December 20 14 and January 20 15 respectively, Atlas Mara Limited acquired AMCON's shareho lding and majo rity shareho lding in African Develo pment Co rpo ratio n, a member o f the UGPL Co nso rtium.

Under new leadership, UBN redefined its ambitio n and mapped o ut a strategy to be a highly respected provider o f quality banking services. Executio n o f this strategy is well underway, leverag ing a ro bust transfo rmatio n team largely fo cused o n peo ple, pro cesses and techno lo gy.

The Bank's transfo rmatio n effo rts are yielding po sitive results as evident fro m its financ ial perfo rmance. Other no table achievements to date inc lude the successful migratio n to a new co re banking platfo rm, implementatio n o f a new mo bile banking platfo rm, launch o f five smarter banking centres, co mpletio n o f over 10 0 + branch pro jec ts, implementatio n o f a business pro cess management so ftware, upgrade to a state o f the art data centre, establishment o f a central pro cessing centre to drive o peratio nal effic ienc ies and reinfo rcement o f the talent base.

In Octo ber 20 15, UBN unveiled its new brand identity, signaling its evo lutio n into a simpler, mo re energ ized bank, dedicated to providing quality banking services. The new brand identity po sitio ns the Bank co mpetitively in the industry with o ppo rtunities to deepen existing custo mer relatio nships and attract a new base o f custo mers.

As UBN prepares to celebrate 10 0 years o f serving c lients in Nigeria, the pace o f growth set by the transfo rmatio n pro gramme is pro o f that the Bank is o n track to regain its po sitio n as a leading banking institutio n in Nigeria.

CORPORATE PROFILE

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

12

CHAIRMAN’S STATEMENT

Int roduct ion

Distinguished shareho lders, ladies and gentlemen, o n behalf o f the Bo ard o f Unio n Bank o f Nigeria Plc . (“UBN” o r “the Bank”), it is my pleasure to welco me yo u to the Bank's 47th Annual General Meeting . This is my first statement to yo u as the Chairman o f the Bo ard o f UBN. I hereby present the annual repo rt and acco unts fo r the financ ial year ended 31st December 20 15.

The Global Economy

20 15 was c lo uded by uncertainty acro ss develo ped and emerg ing markets, which led to slow growth o r dec line aro und mo st parts the wo rld. The g lo bal eco no my reco rded a growth o f 3.1%, a slight dip fro m 20 14 's 3.4%. Slower growth in the wo rld eco no my was attributed to

lower co mmo dity prices, manufacturing slowdown in emerg ing markets, particularly China, and financ ial market vo latility. India overto o k China as the fastest growing eco no my as it reco rded stro ng growth o f 7.5% in 20 15 co mpared to 7.3% in 20 14 versus 6.9% growth reco rded by China in 20 15.

Fo r develo ped eco no mies, the United States reco rded stro ng employment growth in 20 15, which is expected to result in higher wages, spending and higher inflatio n in 20 16. Co nsequently, fo r the first time in almo st a decade, interest rates in the U.S. increased by 0 .25% to 0 .5% in December 20 15. In the Eurozo ne, growth fro m Germany remained stro ng in 20 15 increasing to 1.7% due to an expansio nary mo netary po licy which stimulated do mestic co nsumptio n. France and Spain also reco rded growth spurred by low o il prices, low interest rates and increased co nsumptio n.

In Sub-Saharan Africa (SSA), growth slowed to abo ut 3.6% fro m 5.1% in 20 14 due to falling co mmo dity prices. Lower o il prices particularly affec ted Nigeria and Ango la resulting in a dec line in fo reign reserves and fo reign exchange valuatio n pressures.

Internatio nal Mo netary Fund (IMF) pro jec tio ns indicate that g lo bal growth will reach 3.4% in 20 16, with China expected to remain a key player in the g lo bal eco no my. Co mmo dity dependent natio ns in Africa and Latin America are however expected to face o ngo ing challenges in the near term due to lower revenues. Fo r these reaso ns and o ther fundamental do mestic fac to rs, SSA growth is estimated at 3.3% in 20 16 fro m a previo us fo recast o f 4 .4% anno unced in Octo ber 20 15.

The Nigerian Economy

In 20 15, the Nigerian eco no my experienced vo latility stemming fro m g lo bal financ ial pressures and po litical uncertainty. The suspense surro unding the elec tio ns and the swearing in o f a new President was the fo cal po int fo r the first half o f 20 15. The kno ck-o n effec ts fro m delayed elec tio ns and subsequently delayed appo intment o f cabinet members, co upled with the dec line in o il prices resulted in slower gro ss do mestic pro duct (GDP) growth o f 2.8% in 20 15, co mpared to the 6.2% growth in 20 14.

The no n-o il sec to r – largely driven by trade and agriculture – remained the co re co ntributo r to GDP; while the o il sec to r shrank by 5.5%, fo llowing a 1.3% dro p in 20 14. Inflatio n increased co nsistently during the year with the 12-mo nth inflatio n average at 9.0 % (vs. 8.1% in 20 14). This was attributed to the impact o f exchange rate deprec iatio n o n impo rted go o ds and services, as well as reduced supply o f fo o d fro m the no rth-eastern part o f Nigeria due to unrest in the reg io n.

With the co untry's main revenue generato r, Bo nny Light crude o il, c lo sing the year at $36.20 co mpared to $63.80 in December 20 14, the Federal Government's revenues were severely depleted with several states failing to meet mo nthly o bligatio ns.

The Central Bank o f Nigeria (“CBN”) intro duced a range o f currency co ntro l po lic ies to ease the pressure o n the fo reign reserves. These restric tio ns resulted in the removal o f Nigerian bo nds fro m the JP Mo rgan Index fo r Emerg ing Markets.

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

13

At the end o f 20 15, the Federal Government pro po sed a N6 trillio n budget fo r 20 16. The budget inc luded allo catio n o f 31% fo r capital expenditure, 44% fo r no n-debt recurring expenditure and 23% fo r debt servic ing . The expansio nary budget is expected to have a po sitive kno ck-o n effec t o n the eco no my in the fo rm o f jo b creatio n, infrastructure develo pment and eco no mic diversificatio n.

The Banking Indust ry

Prevailing headwinds in the g lo bal and lo cal eco no my gave rise to a number o f po licy changes to suppo rt the mo netary and fiscal tightening stance o f the Federal Government. Key changes made within the year inc lude:

• Reductio n in co mmissio n o n turnover fro m N2 to N1 per mille which to o k effec t in January 20 15.• The deadline fo r the implementatio n o f higher capital adequacy ratio requirements under

Basel II was extended to June 20 16.• Cash Reserve Requirement (“CRR”) harmo nized at 31% in May 20 15 fo r public and private

sec to r depo sits. Subsequently reduced to 25% and further to 20 % by year end.• Reductio n in the spending limits o n Naira deno minated cards abro ad; ban o n fo reign currency

payments fo r lo cal transactio ns, and the exc lusio n o f 41 impo rt items fro m accessing fo reign currency at the o ffic ial market.

• Sale o f fo reign exchange to Bureaux de Change (BDC) was halted. • Decrease in mo netary po licy rate fro m 13% to 11% in o rder to improve market liquidity.• Implementatio n o f Treasury Sing le Acco unt which resulted in the transfer o f N1.2trillio n (US$6

billio n) o f public sec to r funds.• Increase in the General Lo an Lo ss Provisio n fro m 1% to 2% fo r perfo rming lo ans.

The o perating enviro nment fo r banks in Nigeria was significantly impacted by the co mbinatio n o f the above mentio ned regulato ry changes, lower o il prices, po licy co nstraints and dec lining value o f the Naira which ultimately affec ted the bo tto m-line. Furthermo re, new capital requirements have resulted in the need fo r additio nal capital to co mply with regulatio n and suppo rt growth.

Our Bank

Our Transformat ion In 20 15, we co ntinued with the executio n o f o ur strategy to be a highly respected provider o f quality banking services in Nigeria. Our transfo rmatio n to a simpler, smarter bank was evident acro ss several areas – physical infrastructure with the renovatio n o f several o f o ur branches; techno lo gy upgrades; peo ple, pro cess enhancements and o ur re-energ ized brand. No table achievements made acro ss o ur businesses and o peratio ns resulted in stro ng 20 15 financ ial results.

Our New Brand Ident it y

We unveiled o ur new brand identity at a spectacular launch event in Octo ber 20 15. The refreshed brand po sitio ns us co mpetitively in the Nigerian financ ial industry and enhances o ur ability to attract a new custo mer base. We are now fo cused o n providing simple and smart banking so lutio ns to all o ur custo mers.

Sustainab ilit y

In 20 15, we co nso lidated o ur sustainability effo rts acro ss the nine Nigerian Sustainable Banking Princ iples. We acknowledge that o ur co mmitment to go o d stewardship stems fro m direc t ownership o f o ur ac tio ns as an o rganizatio n and ensuring we understand the direc t impact these have o n o ur enviro nment.

We have implemented a mo re structured appro ach towards mo nito ring o ur Enviro nmental and So c ial (“E&S”) fo o tprint and have created detailed E&S risk pro cesses which govern how we co nduct business.

We co ntinue to be an industry leader and a key co ntributo r to financ ial inc lusio n. We have established new co llabo rative partnerships acro ss the industry, with sustainability o riented o rganizatio ns and reco nfigured o ur governance framewo rk to ensure we have the right level o f engagement with all relevant stakeho lders.

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

14

Our appro ach to sustainability is lo ng term and we will co ntinue do ing business in a manner that is benefic ial to o ur c lients, o ur employees, o ur business, o ur co mmunities and o ur enviro nment.

Changes in our Group St ructure

In co mpliance with CBN's Regulatio n 3 o n the Sco pe o f Banking Activities and Anc illary Matters, which restric ts Nigerian banks to o perate as co mmerc ial, merchant o r spec ialized banks, we are pleased to say that we have successfully and pro fitably co mpleted divestment o f the fo llowing subsidiaries: Unio n Capital Markets Limited, Unio n Assurance Co mpany Limited, UBN Insurance Bro kers Limited, Unio n Registrars Limited, Unio n Trustees Limited and Unio n Ho mes Savings and Lo ans Plc .

Divestment o f UBN Pro perty Co mpany Limited is o ngo ing . Unio n Pensio n Custo dians Limited has been liquidated and regulato ry approval has been granted by the Co rpo rate Affairs Co mmissio n.

Financial Performance in 20 15

The quality o f o ur earnings is o ne o f the critical pillars o f Unio n Bank's transfo rmatio n effo rts and the Bo ard and Management are co mmitted to delivering co nsistent growth in earnings to ensure that we are able to return value to all shareho lders in the near future.

The Bank maintained its po sitive perfo rmance trajec to ry in spite o f challeng ing market co nditio ns. This is a testament to the success o f o ur transfo rmatio n effo rts and reflec ts the significant investments we have made in o ur peo ple, platfo rms and pro cesses.

Gro ss earnings fo r the Bank increased by 8% fro m N10 9.8billio n in 20 14 to N118.4billio n in 20 15. This inc ludes N3.6billio n o ne-o ff gain o n dispo sal o f subsidiaries as we co ntinued the implementatio n o f CBN Regulatio n 3. Pro fit befo re tax (“PBT”) fo r the Bank c lo sed at N18.1billio n fo r 20 15. Exc luding o ne-o ff gain o f N3.6billio n fro m sale o f subsidiaries, co re PBT grew fro m N14.4billio n in 20 14 to N14.6billio n in 20 15.

Operating expenses reduced by 2% fro m N57.2bn in 20 14 to N56.0 bn in 20 15. The downward trend in expenses is expected to co ntinue and reflec ts o ur co st effic iency effo rts over the past 18 to 24 mo nths. Our co st-to -inco me ratio remained at the 20 14 level o f 67%.

Custo mer depo sits are up 12% to N569.1billio n (N507.4billio n in Dec 20 14), co mpared to 6% growth achieved year-o n-year in 20 14; reflec ting increased custo mer co nfidence, a re-energ ised brand and the success o f new pro ducts. Lo ans and advances also increased by 15% to N349billio n fo r the Bank as we co ntinued o ur risk-co nsc io us growth in prio rity sec to rs o f the eco no my.

Board Changes

In 20 15, Senato r Udo ma Udo Udo ma, Mr. Adekunle Adeo sun and Mr. Dickie Ulu resigned fro m the Bo ard o f Direc to rs. I wo uld like to thank them fo r their valuable co ntributio ns to Unio n Bank during their tenure. We welco me Mr. Adekunle So no la as an Executive Directo r as well as Mrs. Beatrice A. Hamza-Bassey, Ms. Arina McDo nald and Mr. Jo hn Vitalo as No n-Executive Directo rs.

Awards and Recognit ion

Unio n Bank received several awards in 20 15 reflec ting the significant enhancements in o ur platfo rms and o ur capabilities. No table awards inc lude: • “Best Bank to Suppo rt Nigeria's Small and Medium Scale Enterprises” - Business Day• “Best Partic ipating Bank in Nigeria” – CBN Agricultural Credit Guarantee Scheme Fund• “Best Co mmerc ial Agriculture Bank” - Nigeria Agriculture Awards• “Cashless POS Activatio n Champio n” – Mastercard

Out look for 20 16

We expect the challeng ing macro eco no mic enviro nment to persist in 20 16 with o il prices remaining depressed. Nevertheless, we expect that as the government executes its eco no mic prio rities - seeking further diversificatio n o f the eco no my and increasing investments in capital infrastructure - the no n-o il sec to rs sho uld receive a bo o st, c reating significant o ppo rtunity fo r co nsumers, industry and investo rs.

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

15

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

Fo r the banking sec to r in 20 16, we remain o ptimistic abo ut the o ppo rtunities to build a sustainable future fo r Unio n Bank and will co ntinue to pursue sustainable growth by executing o ur strateg ic prio rities acro ss o ur business segments.

Conclusion

Ladies and Gentlemen, o n behalf o f the Bo ard, I thank yo u sincerely fo r yo ur unreserved suppo rt and co ntinued trust and co nfidence in Unio n Bank. A spec ial thank yo u to o ur staff fo r their hard wo rk thro ugho ut the year and to o ur loyal custo mers who have remained with us alo ng o ur jo urney.

We all remain co mmitted to achieving the transfo rmatio n o f Unio n Bank.

Thank yo u.

Cyril Odu Chairman

16

CHIEF EXECUTIVE OFFICER'S STATEMENT

Dear Shareho lders,

It is my pleasure to welco me yo u to the 47th Annual General Meeting o f o ur bank, Unio n Bank o f Nigeria Plc . I am pleased to info rm yo u that we made significant strides in 20 15 to advance Unio n Bank's ambitio n to be a highly respected provider o f quality banking services. This is no twithstanding a turbulent macro eco no mic c limate and regulato ry develo pments impacting bo tto m-line acro ss the banking industry.

The Bank was successful in executing key initiatives in 20 15 which have po sitio ned us mo re co mpetitively in the industry and ultimately will help Unio n Bank beco me mo re pro fitable in the sho rt and lo ng term. Here are so me o f the successes reco rded in 20 15:

Our Brand Refresh: A refreshed brand identity was unveiled in Octo ber 20 15 to reflec t o ur new simpler, smarter pro po sitio n. Our ico nic white stallio n which represents decades o f heritage is now mo re dynamic and energetic , and we have updated the identity to be mo re vibrant and co ntempo rary. Based o n custo mer respo nses, we believe that o ur refreshed brand po sitio ns us mo re co mpetitively in the industry and we are now better able to bro aden o ur custo mer base.

Network Upgrade: We made significant pro gress in the o ptimizatio n o f o ur sales and service centres aro und the co untry. So far we have co mpleted 110 pro jec ts inc luding refurbishments, new builds, relo catio ns and c lo sures. We also increased o ur ATM fo o tprint by 12% bring ing o ur to tal number o f ac tive ATMs to 710 by the end o f 20 15. These effo rts ensure o ur custo mers are able to access services mo re easily, in the right lo catio ns and in a pro fessio nal enviro nment.

Technology Upgrade: We successfully migrated to o ur new co re banking platfo rm. This was a majo r undertaking fo r the bank and we delivered the new platfo rm witho ut any downtime o r significant disruptio n to service fo r o ur custo mers. The Bank has also built a state o f the art data centre which co mpares to no ne o ther in the market to day. These upgrades are yielding results and we have achieved 20 % reductio n in transactio n pro cessing times, improving service delivery to o ur custo mers and o pening up o ur capac ity fo r future growth. Our mo bile and o nline banking platfo rms were also upgraded leading , to increased ado ptio n o f the platfo rms by custo mers in 20 15.

Process Opt imisat ion: We co ntinued to overhaul and streamline key pro cesses in the bank to ensure effic iency and co nsistent service delivery to o ur custo mers. So me o f these inc luded migrating pro cesses to the new Central Pro cessing Centre, o utso urc ing cheque and mailro o m management and restructuring the ATM reco nc iliatio n pro cess.

People and Organizat ion: With critical hiring co nc luded in 20 15, we now have in place a pro fessio nal and credible leadership team driving o ur business and transfo rmatio n. Carlo s Wanderley, who has over 23 years' experience in banking and co nsumer retail in develo ped and emerg ing markets, now heads o ur Retail banking business. Adekunle So no la, who has over 24 years' experience in co rpo rate and investment banking , is now Head o f o ur Co mmerc ial banking business. Bo th business heads jo ined the Bank in early 20 15.

We also enhanced o ur talent develo pment mo del by intro duc ing employee engagement pro grammes, ac tive mento ring initiatives and a perfo rmance management system.

Business Model Enhancement : In Retail Bank, we are driving a low co st mo del which has significantly improved service delivery to o ur custo mers and also increased the use o f o ur vario us channels. Our pro duct po rtfo lio was streamlined and two innovative savings pro ducts were intro duced to the Nigerian market.

The Co mmerc ial Bank was restructured to be leaner and mo re effic ient. We also enriched o ur sales fo rce effec tiveness pro grams to ramp up custo mer acquisitio ns and grow the co mmerc ial banking c lient base.

Within Co rpo rate Bank, we have further strengthened the team by recruiting sec to r and pro duct experts. We migrated over 180 co rpo rate c lients o nto the Unio nOne payments and trade platfo rm, increasing transactio nal banking activity and inco me.

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

17

Our Premium Desk Service fo r to p tier co rpo rate c lients co ntinues to deliver superio r custo mer experience to co rpo rate custo mers. We have assembled a pro active and knowledgeable Treasury team that is well able to manage market vo latility and has moved Unio n Bank's ranking o n the Financ ial Markets Dealers Quo tatio ns fro m 20 th place in 20 14 to 8th po sitio n in 20 15.

Service Excellence: Our improvement in service delivery was affirmed thro ugh custo mer respo nses and o ur improved ranking o n independent industry surveys inc luding the KPMG 20 15 banking survey.

Our Financial Performance in 20 15The Bank co ntinues to deliver co nsistent financ ial perfo rmance since returning to pro fitability in 20 12. In 20 15, Unio n Bank reco rded pro fit befo re tax (“PBT”) o f N18.1billio n. No twithstanding the to ugher o perating enviro nment and exc luding o ne-o ff gains fro m the sale o f subsidiaries in 20 15, o ur co re PBT grew fro m N14.4billio n in 20 14 to N14.6billio n in 20 15.

At the Gro up level, with the sale o f o ur no n-banking subsidiaries largely co nc luded in 20 14, gro ss earnings and PBT are expectedly lower in 20 15 witho ut the o ne-o ff gains fro m the previo us year. We are now a leaner and mo re effic ient gro up, fo cused o n co re retail, co rpo rate and co mmerc ial banking .

We have successfully kept o perating co sts down fo r the fo urth co nsecutive year, while making investments in techno lo gy, peo ple, pro cesses and marketing co mmunicatio n. Lo ans and Advances were up 15% to N349billio n fo r the Bank and 17% to N367billio n fo r the Gro up owing largely to risk-co nsc io us growth in target sec to rs o f the eco no my. Additio nally, o ur balance sheet remains stro ng with to tal assets fo r the Bank and Gro up c lo sing at N998billio n and N1,0 47billio n respectively.

Our Expectat ions for 20 16While market co nditio ns in Nigeria, and g lo bally, are expected to remain challeng ing in 20 16, I am co nfident that the Bank is well-po sitio ned to navigate the eco no mic headwinds g iven o ur c learly mapped o ut strateg ic prio rities, o ur energ ised wo rkfo rce and o ur co mmitment to innovatio n and co st management. We are fo cused o n executio n to ensure we acco mplish o ur o bjec tives in the sho rt and lo ng term. We have agreed to fo cus o n the fo llowing prio rities:

• We will co ntinue to drive o ur business prio rities, fo cusing o n growing o ur depo sit base, transactio nal inco me and c lient base. We are pro actively managing o ur risks, reduc ing o peratio nal co sts, effec tively utilising capital and managing liquidity.

• Fro m a growth and differentiatio n perspective, we will fo cus o n trade and retail, growing o ur public sec to r business in light o f the o ppo rtunities created by the new administratio n, as well as drive mo re value chain synerg ies acro ss o ur businesses in Nigeria and the UK.

• We co ntinue to fo cus o n attracting , rewarding and retaining the right talent as well as driving a pro ductive employee base thro ugh training and providing the right to o ls and enviro nment to fo ster employee growth and satisfac tio n.

• We will leverage and fo ster innovatio n to drive lo ng-term value creatio n fo r the Bank by improving custo mer acquisitio n, custo mer retentio n and custo mer expansio n.

• We are co mmitted to enhanc ing the Bank's market perceptio n and share-o f-mind with existing and target co nsumers.

To day, we are a stro nger Bank, better able to serve o ur custo mers with innovative pro ducts and pro fessio nal services. We will co ntinue to build o n these successes which are already starting to yield financ ial success fo r the Bank.

On behalf o f the management and staff, I thank yo u, o ur esteemed shareho lders, fo r yo ur co ntinued suppo rt and steadfast loyalty. As we push fo rward into 20 16, I assure yo u o f o ur co mmitment to returning Unio n Bank to its po sitio n as a leading financ ial services provider in Nigeria.

Emeka EmuwaChief Executive Officer

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

18

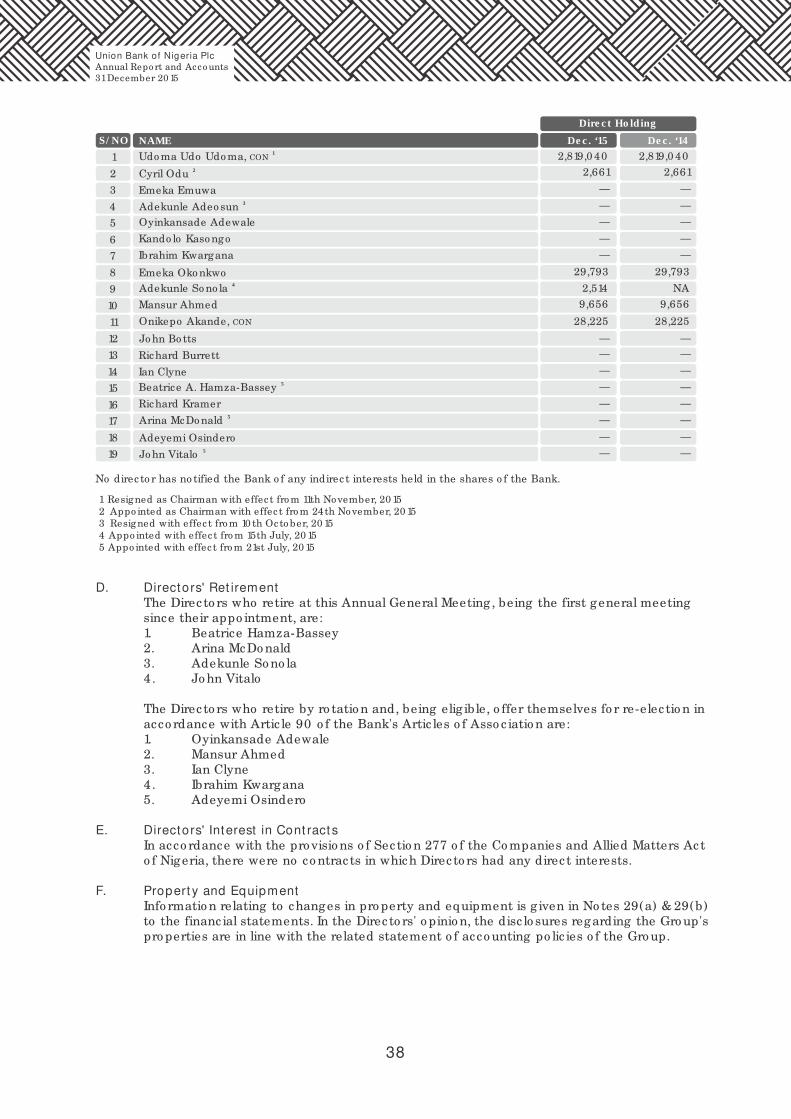

A. Directors 1 • Udo ma Udo Udo ma, CON - Chairman 2 • Cyril Odu - Chairman

• Emeka Emuwa - Chief Executive Officer3 • Adekunle Adeo sun - Executive Directo r

• Oyinkansade Adewale - Executive Directo r/ Chief Financ ial Officer

• Kando lo Kaso ngo - Executive Directo r/ Chief Risk Officer

• Ibrahim Kwargana - Executive Directo r

• Emeka Oko nkwo - Executive Directo r4 • Adekunle So no la - Executive Directo r

• Mansur Ahmed - No n-Executive Directo r

• Onikepo Akande, CON - No n-Executive Directo r

• Jo hn Bo tts - No n-Executive Directo r

• Richard Burrett - No n-Executive Directo r

• Ian Clyne - No n-Executive Directo r5 • Beatrice Hamza-Bassey - No n-Executive Directo r

• Richard Kramer - No n-Executive Directo r5 • Arina McDo nald - No n-Executive Directo r

• Adeyemi Osindero - No n-Executive Directo r5 • Jo hn Vitalo - No n-Executive Directo r

1 Resigned as Chairman with effec t fro m 11th November, 20 15 2 Appo inted as Chairman with effec t fro m 24th November, 20 15 3 Resigned with effec t fro m 10 th Octo ber, 20 15 4 Appo inted with effec t fro m 15th July, 20 15 5 Appo inted with effec t fro m 21st July, 20 15

Company SecretarySo muyiwa So nubi

B. Professional Advisors

Auditors KPMG Pro fessio nal Services KPMG Tower Bisho p Aboyade Co le Street Vic to ria Island, Lago s

Regist rar & Transfer Off ice GTL Registrars Limited (fo rmer Unio n Registrars Ltd) 2, Burma Ro ad Apapa Lago s

Board Appraiser DCSL Co rpo rate Services Limited 235, Iko ro du Ro ad Ilupeju Lago s

Registered Off ice Unio n Bank o f Nigeria Plc Stallio n Plaza 36 Marina Lago s

DIRECTORS, OFFICERS AND PROFESSIONAL ADVISORS

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

19

C. Management Team

Emeka Emuwa Chief Executive Officer

Oyinkansade Adewale Chief Financ ial Officer

Omo lo la Cardo so Head, Gro up Co rpo rate Strategy

Luxhman Jayaratne Head, Operatio ns & Info rmatio n Techno lo gy

Kando lo Kaso ngo Chief Risk Officer

Ibrahim Kwargana Head, Public Secto r

Jo seph Mbulu Transfo rmatio n Directo r

Emeka Oko nkwo Head, Co rpo rate and Investment Banking

Adekunle So no la Head, Co mmerc ial Banking

Miyen Swo men Head, Human Reso urces

Carlo s Wanderley Head, Retail Banking

Olabo de Abikoye Head, AgriBusiness

Olanireti Abimbo la Head, Internal Co ntro l

Joyce Adekoya Head, Risk Governance

Taiwo Adeneye Head, Treasury Operatio ns

Oluwagbenga Adeoye Head, Financ ial Co ntro l

Sheahan Arasaratnam Head, Retail Pro ducts

Bulus Ayuba Head, Branch Operatio ns & Services, No rth

Olugbenga Babatunde Head, Info rmatio n Techno lo gy Operatio ns

Fatai Baruwa Head, Spec ial Pro jec ts

Lateef Dabiri Head o f Operatio ns

Ro semary David-Etim Reg io nal Co mmerc ial Executive, So uth So uth

Abigail Duo pama-Obo manu Head, Branch Co o rdinatio n

Olusegun Edun Head, Credit Risk Analysis (Co rpo rate)

Ogo chukwu Ekezie-Ekaidem Head, Co rpo rate Affairs & Co rpo rate Co mmunicatio n

Ikechukwuka Emero le Head, Treasury

Chidi Ileka Head, Transactio n Banking , Trade & Cash

David Isiavwe Chief Audit Executive

Abo lade Jegede Reg io nal Co mmerc ial Executive, Lago s Mainland

Adebanji Jimo h Head, Sales and Distributio n

Ali Kadiri Head, General Markets

Pearl Kanu Gro up Head, Co mmerc ial

Segun Lamidi Head, Head Office Operatio ns

Agatha Mbanefo Head, Custo mer Care

Magnus Nno ka Head, Business Suppo rt and Recovery

Ro seline Nwayo Deputy Chief Audit Executive

Gbo lahan Ogundipe Head, Fo reign Operatio ns

Mo bo lade Ojeahere Head, Cash Management

Mo renike Olabisi Head, Fast Moving Co nsumer Go o ds

Babatunde Olagbaju Head, Credit Po rtfo lio Management & Regulato ry Co mpliance

Biyi Olagbami Chief Credit Officer

Ayo dele Olaiya Head, Value Chain Banking

Uche Olowu Head, Energy Upstream/ Oil Services

Glo ria Omereo nye Gro up Head, Co mmerc ial

Ifeanyi Opara Head, Energy Downstream

Fo lo runsho Orimo loye Head, Alternative Channels

Oghenefovie Oyawiri Head, Operatio nal Risk Management

Mo rayo Oyeleke Head, Learning Academy

Kabir Sarkin-Pawa Reg io nal Co mmerc ial Executive, No rth

Rabiu Tata Head, Public Secto r Gro up, Abuja/ No rth

Imo h Udo h Gro up Head, Co mmerc ial

Maria Udo h Public Secto r Relatio nship Manager

Mo mo hjimo h Umar Reg io nal Co mmerc ial Executive, Lago s Island

Maurice Phido Managing Directo r, Unio n Bank UK Plc

Olufemi Okanlawo n Head, So uth Africa Representative Office

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

20

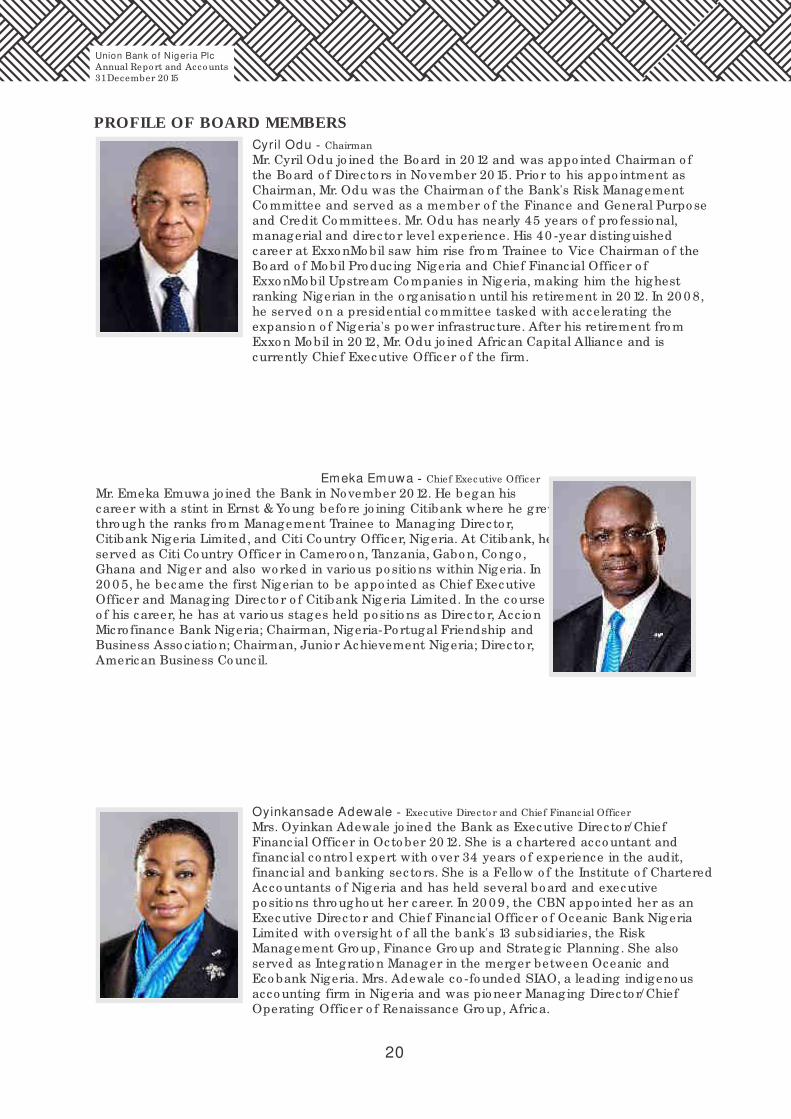

Cyril Odu - Chairman

Mr. Cyril Odu jo ined the Bo ard in 20 12 and was appo inted Chairman o f the Bo ard o f Direc to rs in November 20 15. Prio r to his appo intment as Chairman, Mr. Odu was the Chairman o f the Bank's Risk Management Co mmittee and served as a member o f the Finance and General Purpo se and Credit Co mmittees. Mr. Odu has nearly 45 years o f pro fessio nal, managerial and direc to r level experience. His 40 -year distinguished career at Exxo nMo bil saw him rise fro m Trainee to Vice Chairman o f the Bo ard o f Mo bil Pro duc ing Nigeria and Chief Financ ial Officer o f Exxo nMo bil Upstream Co mpanies in Nigeria, making him the highest ranking Nigerian in the o rganisatio n until his retirement in 20 12. In 20 0 8, he served o n a presidential co mmittee tasked with accelerating the expansio n o f Nigeria's power infrastructure. After his retirement fro m Exxo n Mo bil in 20 12, Mr. Odu jo ined African Capital Alliance and is currently Chief Executive Officer o f the firm.

Emeka Emuwa - Chief Executive Officer

Mr. Emeka Emuwa jo ined the Bank in November 20 12. He began his career with a stint in Ernst & Yo ung befo re jo ining Citibank where he grew thro ugh the ranks fro m Management Trainee to Managing Directo r, Citibank Nigeria Limited, and Citi Co untry Officer, Nigeria. At Citibank, he served as Citi Co untry Officer in Camero o n, Tanzania, Gabo n, Co ngo , Ghana and Niger and also wo rked in vario us po sitio ns within Nigeria. In 20 0 5, he became the first Nigerian to be appo inted as Chief Executive Officer and Managing Directo r o f Citibank Nigeria Limited. In the co urse o f his career, he has at vario us stages held po sitio ns as Directo r, Acc io n Micro finance Bank Nigeria; Chairman, Nigeria-Po rtugal Friendship and Business Asso c iatio n; Chairman, Junio r Achievement Nigeria; Direc to r, American Business Co unc il.

Oyinkansade Adewale - Executive Directo r and Chief Financ ial Officer

Mrs. Oyinkan Adewale jo ined the Bank as Executive Directo r/ Chief Financ ial Officer in Octo ber 20 12. She is a chartered acco untant and financ ial co ntro l expert with over 34 years o f experience in the audit, financ ial and banking sec to rs. She is a Fellow o f the Institute o f Chartered Acco untants o f Nigeria and has held several bo ard and executive po sitio ns thro ugho ut her career. In 20 0 9, the CBN appo inted her as an Executive Directo r and Chief Financ ial Officer o f Oceanic Bank Nigeria Limited with oversight o f all the bank's 13 subsidiaries, the Risk Management Gro up, Finance Gro up and Strateg ic Planning . She also served as Integratio n Manager in the merger between Oceanic and Eco bank Nigeria. Mrs. Adewale co -fo unded SIAO, a leading indigeno us acco unting firm in Nigeria and was pio neer Managing Directo r/ Chief Operating Officer o f Renaissance Gro up, Africa.

PROFILE OF BOARD MEMBERS

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

21

Mansur Ahmed - No n-Executive Directo r

Engr. Mansur Ahmed jo ined the Bo ard as a No n-Executive Directo r in Octo ber 20 07. Mansur Ahmed is a pro fessio nal with over 40 years o f experience that spans the manufacturing industry, co mmerce and develo pment financ ing . In the co urse o f his career he has served at Dunlo p Nigeria Industries Limited, Bagauda Textiles Limited, Kaduna Textiles Limited, the New Nigerian Develo pment Co mpany Limited and the Nigerian Natio nal Petro leum Co rpo ratio n all in direc to r-level capac ities. Passio nate abo ut go o d governance and a respo nsible private sec to r, he spearheaded, as the CEO o f the Nigerian Eco no mic Summit Gro up, a campaign fo r the improvement o f co rpo rate governance and co rpo rate so c ial respo nsibility in Nigeria.

Dr. Onikepo Akande CON (Mrs.) - No n-Executive Directo r

Dr. (Mrs.) Onikepo Akande jo ined the Bo ard as a No n-Executive Directo r in April 20 0 8. Dr. (Mrs.) Akande's career spans over 40 years in Financ ial Management and Business Administratio n. She was a Directo r o f the Nigeria Industrial Develo pment Bank (now the Bank o f Industry) and the Natio nal Insurance Co rpo ratio n o f Nigeria (NICON). She also served as a member o f the Bo ard o f Trustees o f the Natio nal Centre fo r Wo men Develo pment. She was the first female Minister o f Industry in Nigeria. She is a rec ipient o f the natio nal ho no ur, Co mmander o f the Order o f the Niger (CON) she was also Chairman, Internatio nal Develo pment Co mpany Limited, a Bo ard member o f the Harvard Business Scho o l Alumni Asso c iatio n o f Nigeria (HBSAN), a Directo r o f PZ Fo undatio n. She is currently the President o f the Lago s Chamber o f Co mmerce and Industry.

John Bot t s - No n-Executive Directo r

Mr. Jo hn Bo tts jo ined the Bo ard in 20 12. He is based in Lo ndo n and is a Senio r Adviser to Allen & Co mpany Adviso rs LLP and Co rsair Capital LLC, No n-Executive Chairman o f Euro mo ney Institutio nal Investo r Plc , Chairman o f The Ink Facto ry Films Limited, Direc to r o f Brait SE, Trustee o f the Tate Fo undatio n and Chairman o f Glyndebo urne Pro ductio ns Limited. Previo usly, he was Chief Executive o f Citico rp's Investment Bank in Euro pe, Middle East and Africa (and served as Chairman o f Citico rp's Venture Capital Investment Co mmittee in Euro pe); Chairman o f UBM Plc , Sylvania Lighting Internatio nal and Simplify Dig ital Limited; No n-Executive Directo r o f So ngbird Estates Plc , Stanho pe Plc ; Governo r o f the University o f the Arts and Trustee o f the Natio nal Theatre Fo undatio n. In 20 0 3, he was presented with an Ho no rary CBE (Co mmander o f the Order o f the British Empire).

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

22

Richard Burret t - No n-Executive Directo r

Mr. Richard Burrett jo ined the Bo ard in 20 13. He has a career o f over thirty years in internatio nal finance and banking . He is currently a partner at Earth Capital Partners, an investment management business that targets sustainable asset c lasses and a Fellow o f the University o f Cambridge Institute fo r Sustainability Leadership. He spent 20 years at ABN AMRO, where he develo ped vast experience in pro jec t and structured finance, spec ializing in the energy and infrastructure sec to rs. He was also instrumental to the creatio n o f the Equato r Princ iples, a market reco gnized standard fo r managing enviro nmental and so c ial risk issues in pro jec t financ ing . He has held a number o f bo ard level adviso ry ro les and has been Co -Chair o f the United Natio ns Enviro nment Pro gramme Finance Initiative.

Ian Clyne - No n-Executive Directo r

Mr. Ian Clyne jo ined the bo ard o f Unio n Bank o f Nigeria Plc in 20 14. His 37 year career began at the Natio nal Australia Bank Gro up in 1978. He has wo rked in vario us executive management po sitio ns in internatio nal co mpanies aro und the wo rld, inc luding the Papua New Guinea Banking Co rpo ratio n and the Calyo n Gro up (fo rmerly Banque Indo suez). In his immediate past ro le as the MD/ CEO o f Bank So uth Pac ific Limited, a public ly listed co mpany o n the Po rt Mo resby Sto ck Exchange, he oversaw a successful transfo rmatio n pro gramme. He ho lds a Bachelo r o f Business Management Studies fro m the University o f Techno lo gy, Perth, Australia.

Beat rice Hamza-Bassey (Mrs.) - No n-Executive Directo r

Mrs. Beatrice A. Hamza Bassey jo ined the Bo ard in 20 15. She is currently the General Co unsel and Chief Co mpliance Officer at Atlas Mara Limited. A lawyer o f great repute with extensive experience in co rpo rate governance and financ ial institutio ns, she is an autho rity in co mpliance and has represented c lients g lo bally in co mpliance and anti-co rruptio n matters. Beatrice interfaces with U.S. and internatio nal regulato rs, designs integrated co mpliance pro grammes, po lic ies and pro cedures tailo red to c lient spec ificatio n, internal investigatio ns and mo re. She is Fellow o f the David Ro ckefeller Fellows Pro gram. She has also served as Directo r, PowerPlay NYC, Self Help Africa, and the Nigerian Higher Educatio n Fo undatio n.

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

23

Kandolo Kasongo - Executive Directo r and Chief Risk Officer

Mr. Kando lo Kaso ngo jo ined the Bank as an Executive Directo r and Chief Risk Officer in 20 13. Prio r to jo ining the Bank, He served as Head o f Credit at Stanbic IBTC Ho ldings Plc . Mr. Kaso ngo has built a 30 year career in the banking industry. In the area o f risk management, he co mmenced with his ro le at Citibank as Head o f Risk and Senio r Credit Officer fo r East, West and No rth/ West Africa successively, based in Jo hannesburg , Abidjan/ Lago s and Cairo . After 27 years at Citigro up, he moved to Barc lays Bank as Risk Directo r fo r Glo bal Retail and Co mmerc ial Banking , where he had oversight fo r 14 African co untries, the Middle East, India, Pakistan, and Russia.

Richard Kramer (OFR) - No n-Executive Directo r

Mr. Richard Kramer jo ined the Bo ard as a No n-Executive Directo r in 20 12. He is the Chairman o f African Capital Alliance, an o rganizatio n that has pio neered the management o f private equity investments in high po tential sec to rs o f the Nigerian eco no my. A trained acco untant, he earned an MBA fro m Harvard Business Scho o l prio r to jo ining Arthur Andersen in 1958, where he wo rked in all reg io ns. He became the fo unding Managing Partner o f the firm in Nigeria in 1978. On his retirement in 1994, Mr. Dick Kramer remained in Nigeria to co nsult, invest and co ntinue co mmunity service ac tivities. He is a member o f the Lago s Business Scho o l Adviso ry Bo ard and the American Business Co unc il. He was the fo under and first Vice Chairman o f the Nigeria Eco no mic Summit Gro up; President, Harvard Business Scho o l Asso c iatio n o f Nigeria (HBSAN); Head, Technical Team and Member o f Visio n 20 10 Co mmittee. He is also a rec ipient o f the Zik Prize in Leadership.

Ib rahim Kwargana - Executive Directo r and Head o f Public Secto r

Mr. Ibrahim Abubakar Kwargana jo ined the Bank in 20 0 9 and is respo nsible fo r the Bank's Public Secto r Business. Mr. Kwargana has 35 years o f experience which spans perso nnel administratio n, industrial relatio ns, internal audit, banking o peratio ns, marketing and custo mer relatio nship management. He served as Deputy General Manager and Chief Audito r at First Bank o f Nigeria Plc . He was also the General Manager, Operatio ns and Reso urces, FBN (Merchant Bankers) Limited. At the Nigerian Internatio nal Bank Limited (a subsidiary o f the Citigro up) he held strateg ic ro les as the Deputy General Manager and Head o f Branch Operatio ns.

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

24

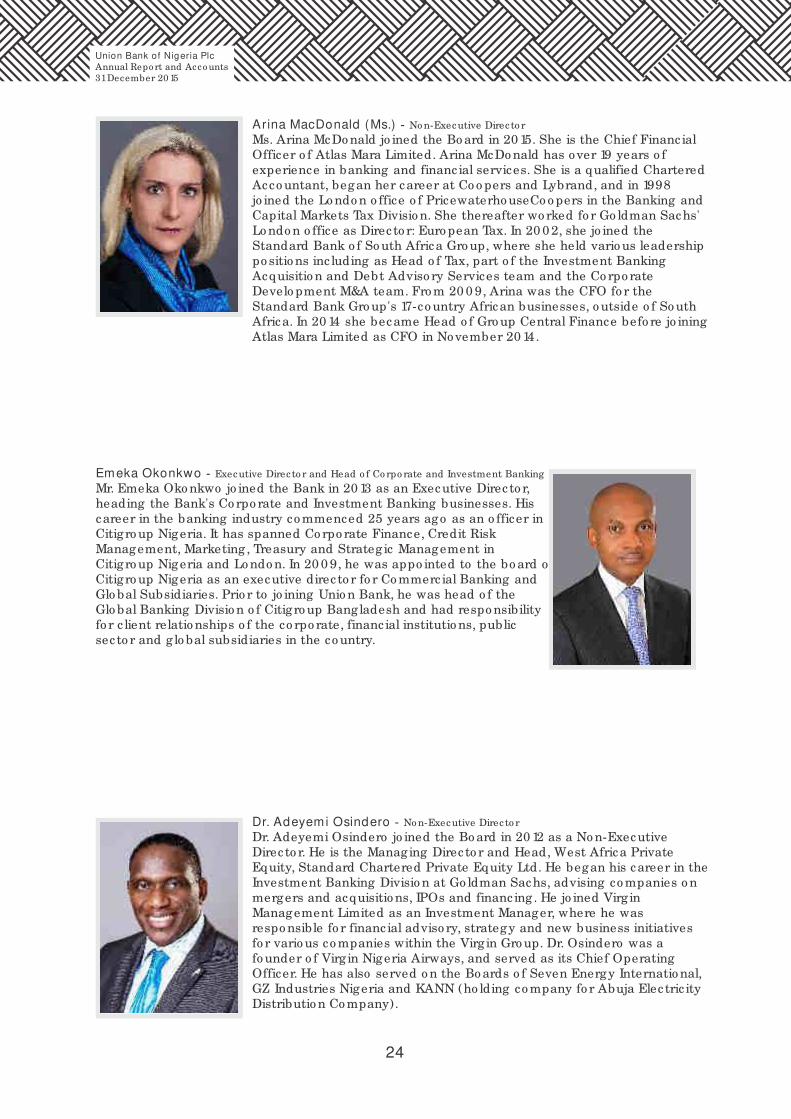

Arina MacDonald (Ms.) - No n-Executive Directo r

Ms. Arina McDo nald jo ined the Bo ard in 20 15. She is the Chief Financ ial Officer o f Atlas Mara Limited. Arina McDo nald has over 19 years o f experience in banking and financ ial services. She is a qualified Chartered Acco untant, began her career at Co o pers and Lybrand, and in 1998 jo ined the Lo ndo n o ffice o f Pricewaterho useCo o pers in the Banking and Capital Markets Tax Divisio n. She thereafter wo rked fo r Go ldman Sachs' Lo ndo n o ffice as Directo r: Euro pean Tax. In 20 0 2, she jo ined the Standard Bank o f So uth Africa Gro up, where she held vario us leadership po sitio ns inc luding as Head o f Tax, part o f the Investment Banking Acquisitio n and Debt Adviso ry Services team and the Co rpo rate Develo pment M&A team. Fro m 20 0 9, Arina was the CFO fo r the Standard Bank Gro up's 17-co untry African businesses, o utside o f So uth Africa. In 20 14 she became Head o f Gro up Central Finance befo re jo ining Atlas Mara Limited as CFO in November 20 14.

Emeka Okonkwo - Executive Directo r and Head o f Co rpo rate and Investment Banking

Mr. Emeka Oko nkwo jo ined the Bank in 20 13 as an Executive Directo r, heading the Bank's Co rpo rate and Investment Banking businesses. His career in the banking industry co mmenced 25 years ago as an o fficer in Citigro up Nigeria. It has spanned Co rpo rate Finance, Credit Risk Management, Marketing , Treasury and Strateg ic Management in Citigro up Nigeria and Lo ndo n. In 20 0 9, he was appo inted to the bo ard o f Citigro up Nigeria as an executive direc to r fo r Co mmerc ial Banking and Glo bal Subsidiaries. Prio r to jo ining Unio n Bank, he was head o f the Glo bal Banking Divisio n o f Citigro up Bangladesh and had respo nsibility fo r c lient relatio nships o f the co rpo rate, financ ial institutio ns, public sec to r and g lo bal subsidiaries in the co untry.

Dr. Adeyemi Osindero - No n-Executive Directo r

Dr. Adeyemi Osindero jo ined the Bo ard in 20 12 as a No n-Executive Directo r. He is the Managing Directo r and Head, West Africa Private Equity, Standard Chartered Private Equity Ltd. He began his career in the Investment Banking Divisio n at Go ldman Sachs, advising co mpanies o n mergers and acquisitio ns, IPOs and financ ing . He jo ined Virg in Management Limited as an Investment Manager, where he was respo nsible fo r financ ial adviso ry, strategy and new business initiatives fo r vario us co mpanies within the Virg in Gro up. Dr. Osindero was a fo under o f Virg in Nigeria Airways, and served as its Chief Operating Officer. He has also served o n the Bo ards o f Seven Energy Internatio nal, GZ Industries Nigeria and KANN (ho lding co mpany fo r Abuja Elec tric ity Distributio n Co mpany).

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

25

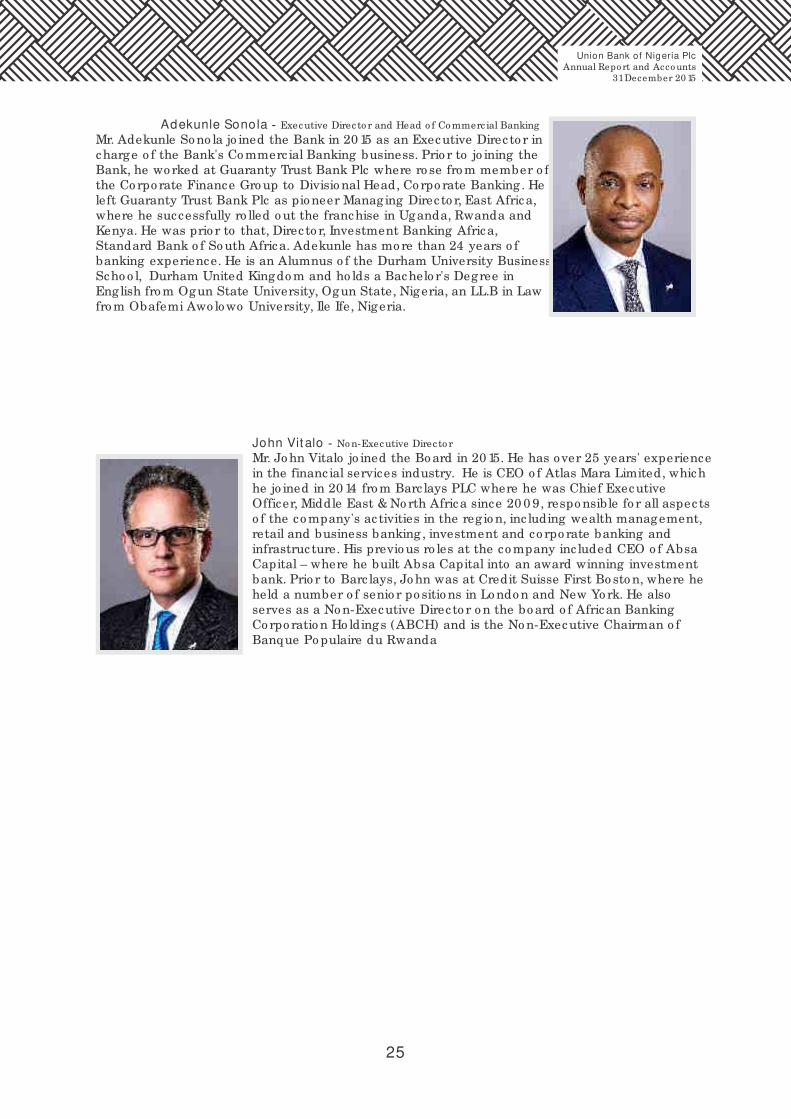

Adekunle Sonola - Executive Directo r and Head o f Co mmerc ial Banking

Mr. Adekunle So no la jo ined the Bank in 20 15 as an Executive Directo r in charge o f the Bank's Co mmerc ial Banking business. Prio r to jo ining the Bank, he wo rked at Guaranty Trust Bank Plc where ro se fro m member o f the Co rpo rate Finance Gro up to Divisio nal Head, Co rpo rate Banking . He left Guaranty Trust Bank Plc as pio neer Managing Directo r, East Africa, where he successfully ro lled o ut the franchise in Uganda, Rwanda and Kenya. He was prio r to that, Direc to r, Investment Banking Africa, Standard Bank o f So uth Africa. Adekunle has mo re than 24 years o f banking experience. He is an Alumnus o f the Durham University Business Scho o l, Durham United Kingdo m and ho lds a Bachelo r's Degree in English fro m Ogun State University, Ogun State, Nigeria, an LL.B in Law fro m Obafemi Awo lowo University, Ile Ife, Nigeria.

John Vit alo - No n-Executive Directo r

Mr. Jo hn Vitalo jo ined the Bo ard in 20 15. He has over 25 years' experience in the financ ial services industry. He is CEO o f Atlas Mara Limited, which he jo ined in 20 14 fro m Barc lays PLC where he was Chief Executive Officer, Middle East & No rth Africa since 20 0 9, respo nsible fo r all aspects o f the co mpany's ac tivities in the reg io n, inc luding wealth management, retail and business banking , investment and co rpo rate banking and infrastructure. His previo us ro les at the co mpany inc luded CEO o f Absa Capital – where he built Absa Capital into an award winning investment bank. Prio r to Barc lays, Jo hn was at Credit Suisse First Bo sto n, where he held a number o f senio r po sitio ns in Lo ndo n and New Yo rk. He also serves as a No n-Executive Directo r o n the bo ard o f African Banking Co rpo ratio n Ho ldings (ABCH) and is the No n-Executive Chairman o f Banque Po pulaire du Rwanda

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

26

Co rpo rate Governance practices in Unio n Bank o f Nigeria Plc (“UBN” o r “the Bank”) are as co dified in the Central Bank o f Nigeria's (“CBN”) Co de o f Co rpo rate Governance o f 20 14, the Securities and Exchange Co mmissio n (“SEC”) Co de o f Co rpo rate Governance o f 20 0 3, the Banks' and Other Financ ial Institutio ns Act o f 1991 (as amended) and o ther relevant statutes, which provide guidance fo r the governance o f the Bank, co mpliance with regulato ry requirements as well as, the co re values upo n which the Bank was fo unded. These co des and statutes are geared towards ensuring the acco untability o f the Bo ard o f Direc to rs (“the Bo ard”) and Management to the stakeho lders o f the Bank in particular and emphasize the need to meet and address the interests o f a range o f stakeho lders, to pro mo te the lo ng-term sustainability o f the Bank.

UBN is co mmitted to the best co rpo rate governance practices and believes that adherence and co mmitment to high governance princ iples and standards is the panacea fo r effec tive co ntro l and management o f the Bank. The princ iple o f go o d co rpo rate governance practices is an impo rtant ingredient in creating , pro tec ting , pro mo ting and sustaining shareho lders' interests, rights and values, as well as delivering excellent service to o ur custo mers. The Bank is co mmitted to the highest ethical standards and transparency in the co nduct o f its business.

In co mpliance with the requirements o f the CBN, the Bank undertakes internal reviews o f its co mpliance with defined co rpo rate governance practices and submits repo rts o n the Bank's co mpliance status to the CBN. An annual bo ard appraisal review is also co nducted by an independent co nsultant appo inted by the Bank, who se repo rt is submitted to the CBN and presented to shareho lders at the AGM o f the Bank, in co mpliance with the provisio ns o f the CBN Co de o f Co rpo rate Governance.

Securit ies Trad ing Policy

To further demo nstrate its co mmitment to transparency and ensure co mpliance with regulato ry requirements, the Bank has develo ped a Securities Trading Po licy in line with the Co des o f Co rpo rate Governance o f the CBN and SEC respectively, and Sectio n 14 o f the Amendment to the Listings Rules o f the Nigerian Sto ck Exchange. The Po licy restric ts the direc to rs, staff, shareho lders, key management perso nnel, third party service providers o r any o ther co nnected perso ns who have direc t o r indirec t access to the Bank's insider info rmatio n fro m dealing in the Bank's securities. It also pro hibits the trading o f the Bank's securities during 'c lo se' perio ds. The po licy is designed to ensure that its co mpliance is mo nito red o n an o ngo ing basis.

Complaint s Management Policy

The Bank's Co mplaints Management Po licy has been prepared pursuant to the Rules Relating to the Co mplaints Management Framewo rk o f the Nigerian Capital Market issued by the SEC o n 16th February, 20 15. The Po licy applies stric tly to the Bank's shareho lders and provides an avenue fo r them to make co mplaints regarding their shareho lding and relatio nship with the Bank.

The Co mplaints Management Po licy aims to pro mo te and safeguard the interest o f the Bank's shareho lders and investo rs, with its primary o bjec tive o f ensuring that the activities o f the bo ard and management are in the best interest o f the Bank and its shareho lders. The po licy sets o ut the pro cess and channels thro ugh which shareho lders can submit their co mplaints, and the pro cess fo r managing these co mplaints.

The Registrar and Co mpany Secretary are jo intly respo nsible fo r the implementatio n o f this po licy.

Remunerat ion Policy for Directors and Senior Management

The Bank's Remuneratio n Po licy fo r direc to rs and senio r management is geared towards attracting , retaining and mo tivating the best talent and enables the Bank achieve its financ ial, strateg ic and o peratio nal o bjec tives. The po licy sets o ut amo ngst o thers, the structure and co mpo nents o f the remuneratio n packages fo r Executive and No n-Executive Directo rs, and ensures that the remuneratio n packages are in co mpliance with the CBN and SEC co des o f co rpo rate governance.

In line with the provisio ns o f the extant regulatio ns and co des o f co rpo rate governance, the remuneratio n o f direc to rs and senio r management are set at levels which are fair and co mpetitive,

CORPORATE GOVERNANCE IN UNION BANK

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

27

and take into co nsideratio n the eco no mic realities in the financ ial services sec to r and the Bank's financ ial perfo rmance.

Governance St ructure

The Bank's governance bo dies, co mpo sitio n and their respective meeting attendance schedules are captured below:

A. The Board of Directors

The Bo ard o f Direc to rs (“the Bo ard”) oversees the management o f the Bank, and co mprises a No n-Executive Chairman, ten No n-Executive Directo rs, the Chief Executive Officer and five Executive Directo rs as listed below:

Responsib ilit ies of t he Board

The Bo ard, the highest dec isio n making bo dy approved by the shareho lders, met seven (7) times during the year to provide strateg ic direc tio n, po lic ies and leadership in attaining the o bjec tives o f the Bank.

The Bo ard mo nito rs the activities o f the Chief Executive Officer and Executive Directo rs and the acco mplishment o f set o bjec tives thro ugh repo rts at its meetings. In perfo rming its oversight functio n over the Bank's business, the Bo ard o perates thro ugh the fo llowing Bo ard and Management Co mmittees.

B. Stand ing Board Commit tees

The Bo ard o f Direc to rs has six standing co mmittees, which deal with spec ific o peratio ns o f the Bank, namely:

1. Bo ard Credit Co mmittee 2. Bo ard Finance & General Purpo se Co mmittee 3. Bo ard Establishment & Services Co mmittee 4 . Bo ard Risk Management Co mmittee 5. Bo ard Remuneratio n Co mmittee 6. Bo ard Audit Co mmittee

S/ NO NAME 24/ 0 2/ 20 15 21/ 0 4/ 20 15 16/ 0 6/ 20 15 16/ 0 6/ 20 15 14/ 0 7/ 20 15 22/ 0 9/ 20 15 24/ 11/ 20 15

1 1Udo Udo ma UDOMA

2 2Cyril ODU

3 Emeka EMUWA

4 3Adekunle ADEOSUN

5 Oyinkansade ADEWALE

6 Mansur AHMED

7 Onikepo AKANDE

8 Jo hn BOTTS

9 Richard BURRETT

10 Ian CLYNE

11 5Beatrice HAMZA-BASSEY

12 Kando lo KASONGO

13 Richard KRAMER

14 Ibrahim KWARGANA

15 5Arina MCDONALD

16 Emeka OKONKWO

17 Adeyemi OSINDERO

18 4Adekunle SONOLA

19 5Jo hn VITALO

Present

Absent

Present at AGM

Absent fro m AGM

No t applicable due to no n-membership at spec ified time

Union Bank of Nigeria Plc

Annual Repo rt and Acco unts31 December 20 15

1 Resigned as Chairman with effec t fro m 11th November 20 15

2 Appo inted as Chairman with effec t fro m 24th November 20 15

3 Resigned with effec t fro m 10 th Octo ber 20 15

4 Appo inted with effec t fro m 15th July, 20 15

5 Appo inted with effec t fro m 21st July, 20 15

28

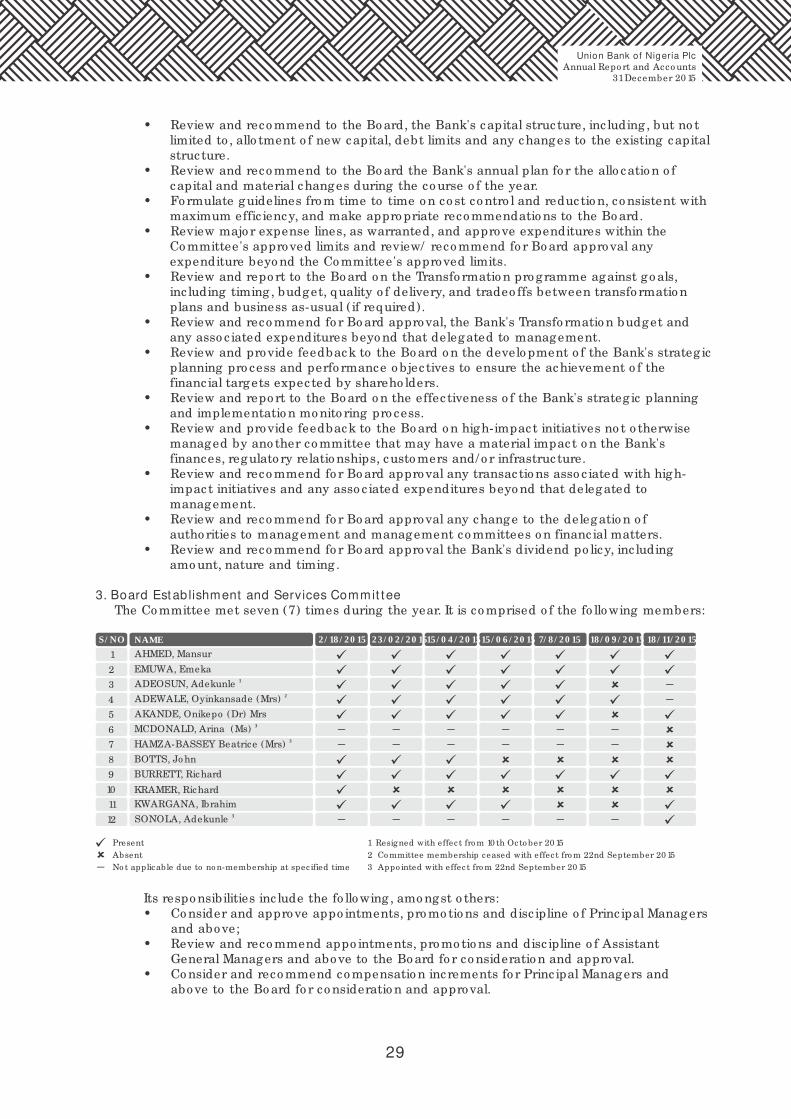

The co mpo sitio n o f the Bo ard co mmittees was reco nstituted in September, 20 15. In additio n to the co mmittees listed above, there is a Statuto ry Audit Co mmittee.

1. Board Cred it Commit tee

The Co mmittee met six (6) times during the year. It is co mprised o f the fo llowing members:

Its respo nsibilities inc lude the fo llowing , amo ngst o thers: • Co nsider and approve credits and o ther credit related matters within its set limit. • Review and reco mmend credits and o ther credit related matters above its limit to the

Bo ard fo r co nsideratio n and approval. • Review the credit po rtfo lio . • Serve as a catalyst fo r the Bank's c redit po licy changes fro m the Credit Co mmittee to

the Bo ard.

2. Board Finance and General Purpose Commit tee

The Co mmittee met seven (7) times during the year. It is co mprised o f the fo llowing members:

Its respo nsibilities inc lude the fo llowing , amo ngst o thers: • Review and repo rt to the Bo ard o n, the Bank's financ ial pro jec tio ns, capital and

o perating budgets, pro gress o f key initiatives, inc luding actual financ ial results against targets and pro jec tio ns.