Embed Size (px)

Citation preview

Canadian Tire Corporation

Investor Presentation

November 2016

This document contains forward-looking information that reflects management’s current expectations related to matters such as future financial performance and operating results of the Company. Forward-looking statements are provided for the purposes of providing information about Management’s current expectations and plans and allowing investors and others to get a better understanding of the Company’s financial position, results of operations and operating environment. Readers are cautioned that such information may not be appropriate for other circumstances.

All statements other than statements of historical facts included in this document may constitute forward-looking statements, including but not limited to, statements concerning Management’s current expectations relating to possible or assumed future prospects and results, the Company’s strategic goals and priorities, its actions and the results of those actions and the economic and business outlook for the Company. Often, but not always, forward-looking statements can be identified by the use of forward-looking terminology such as “may”, “will”, “expect”, “intend”, “believe”, “estimate”, “plan”, “can”, “could”, “should”, “would”, “outlook”, “forecast”, “anticipate”, “aspire”, “foresee”, “continue”, “ongoing” or the negative of these terms or variations of them or similar terminology. Forward-looking statements are based on the reasonable assumptions, estimates, analyses, beliefs and opinions of Management, made in light of its experience and perception of trends, current conditions and expected developments, as well as other factors that Management believes to be relevant and reasonable at the date that such statements are made

By their very nature, forward-looking statements require Management to make assumptions and are subject to inherent risks and uncertainties, which give rise to the possibility that the Company’s assumptions, estimates, analyses, beliefs and opinions may not be correct and that the Company’s expectations and plans will not be achieved. Examples of Management’s beliefs, which may prove to be incorrect, include, but are not limited to, beliefs about the effectiveness of certain performance measures, beliefs about current and future competitive conditions and the Company’s position in the competitive environment, beliefs about the Company’s core capabilities and beliefs regarding the availability of sufficient liquidity to meet the Company’s contractual obligations. Although the Company believes that the forward-looking statements in this document are based on information, assumptions and beliefs that are current, reasonable and complete, these statements are necessarily subject to a number of factors that could cause actual results to differ materially from Management’s expectations and plans as set forth in such forward-looking statements. Some of the factors, many of which are beyond the Company’s control and the effects of which can be difficult to predict, include: (a) credit, market, currency, operational, liquidity and funding risks, including changes in economic conditions, interest rates or tax rates; (b) the ability of the Company to attract and retain high quality employees for all of its businesses, Dealers, Canadian Tire Petroleum retailers and Mark’s and FGL Sports franchisees, as well as the Company’s financial arrangements with such parties; (c) the growth of certain business categories and market segments and the willingness of customers to shop at its stores or acquire its financial products and services; (d) the Company’s margins and sales and those of its competitors; (e) the changing consumer preferences toward eCommerce, online retailing and the introduction of new technologies; (f) risks and uncertainties relating to information management, technology, cyber threats, property management and development, environmental liabilities, supply chain management, product safety, changes in law, regulation, competition, seasonality, weather patterns, commodity prices and business disruption, the Company’s relationships with suppliers, manufacturers, partners and other third parties, changes to existing accounting pronouncements, the risk of damage to the reputation of brands promoted by the Company and the cost of store network expansion and retrofits; (g) the Company’s capital structure, funding strategy, cost management programs and share price; and (h) the Company’s ability to obtain all necessary regulatory approvals. Management cautions that the foregoing list of important factors and assumptions is not exhaustive and other factors could also adversely affect the Company’s results. Investors and other readers are urged to consider the foregoing risks, uncertainties, factors and assumptions carefully in evaluating the forward-looking statements and are cautioned not to place undue reliance on such forward-looking statements.

For more information on the risks, uncertainties and assumptions that could cause the Company's actual results to differ from current expectations, please refer to the "Risk Factors" section of our Annual Information Form for fiscal 2015 and our 2015 Management's Discussion and Analysis, as well as Canadian Tire's other public filings, available at www.sedar.com and at www.corp.canadiantire.ca.

Forward-looking statements do not take into account the effect that transactions or non-recurring or other special items announced or occurring after the statements are made, have on the Company’s business. For example, they do not include the effect of any dispositions, acquisitions, asset write downs or other charges announced or occurring after such statements are made.

The forward-looking statements and information contained herein are based on certain factors and assumptions as of the date hereof. The Company does not undertake to update any forward-looking statements, whether written or oral, that may be made from time to time by it or on its behalf, to reflect new information, future events or otherwise, unless required by applicable securities laws.

Forward looking information

2

$606.1

$429.6

$238.1

$1,612.5 $2,822.7

-0.1%

Retail Revenue by Banner4

4.3%

6.2%

3.5%

Q3 SAME-STORE

SALES

CANADIAN TIRE

FGL SPORTS

MARK’S

Recent Quarterly Results

Q3 RETAIL

SALES GROWTH

CANADIAN TIRE 4.9%

FGL SPORTS 8.5%

MARK’S 4.4%

Q3 DILUTED

EPS

$2.44 -6.7%1

Q3 RETAIL ROIC2,3

8.15%

Q3 FINANCIAL

SERVICES RETURN

ON RECEIVABLES2,3

7.40%

1,2

1 - Q3 2015 included a $0.33 per share gain from the sale of surplus property. Excluding this gain, diluted EPS increased 6.6 percent, year-over-year. 2 – Figures are calculated on

a rolling 12-month basis. 3 – Refer to Section 9.3.1 of the Q3 2016 MD&A for additional information on the Company’s key operating performance measures. 4 – Inter-segment

revenue within the retail banners of $63.6 million in the third quarter ( 2015 - $63.6million) has been eliminated at the Retail segment level. Revenue reported for Canadian

Tire, FGL Sports, Mark’s and Petroleum includes inter-segment revenue.

Q3 Operational Highlights

Aligned senior talent to strengthen our products and brands with the creation of new

Consumer Brands Division.

Focused on the lifecycle of our customer across all of our businesses and how, as

our businesses are all linked as one company, they form a marketplace.

“I am extremely encouraged by the strong performance in each of our core retail

banners this quarter. Our unique assortments and product development capabilities

are allowing us to bring our customers the products they need for the jobs and joys of

a lifetime in Canada”

-Stephen Wetmore, President & CEO, CTC

Implemented first phase of distributed order management system at Sport Chek,

allowing for a network view of real-time inventory and capabilities to efficiently

manage shipments.

Corporate Overview

Family of businesses Bringing our

customers the products they need for the jobs and joys of a lifetime in Canada.

Our strengths

Strong iconic brands that Canadians love

Market leadership and credibility in heritage categories

Financial flexibility / REIT / Scotiabank transaction

Strong balance sheet / credit rating

~1,700 bricks and mortar locations across Canada

Shared real estate, marketing, supply chain, support services

Our growth plan

Establish CTC as a world class leader in innovative uses of digital for

retailing

Growth and integration of in-store digital and e-commerce

Leading customer loyalty and reward programs

Engaging digital marketing, use of sponsorships and powerful

content

Continue to invest to strengthen our core businesses

Culture of productivity with a performance management focus

How we win

Exceeding customer expectations with best omni-channel retail

platforms

Conduit between customers and the best consumer brands in

the world

Building our brands and exclusivity

Family of CTC businesses – strong coalition

Sports and community partnerships

Financial highlights (2015) Growth (YoY)

Revenue* $12.3B -1.5%

Net Income (attributable to

shareholders of CTC)

$659.4M +9.2%

Adjusted Diluted Earnings Per

Share** $8.61 +8.4%

*Results for the full year 2015 (52 weeks ended January 2, 2016) are compared against results for the full year 2014 (53

weeks ended January 3, 2015)

**Refer to Section 11.3.2 of the Q4 and full-year 2015 MD&A for additional information on the Company’s Non-GAAP

financial measures

Market Leadership

Leadership position across heritage/core business categories:

Automotive, Living, Fixing & Playing

#1 in Men’s Industrial & Casual Apparel

1 in 5 Canadians hold a Canadian Tire credit card

5

Our Retail Network Across Canada

13

6

8

12

0

2

2

2

0

0

100

160

45

59

0

19

9

13

15

0

22

11

17

9

3

15

11

13

6

6

202

120

143

166

61

56

53

65

19

15

16

13

15

6

6

52

43

59

4

0

1

0

1

0

0

499

429

382

296

91

NEW

BRUNSWICK

NOVA SCOTIA

MANITOBA

ONTARIO

SASKATCHEWAN BRITISH

COLUMBIA

ALBERTA

NEWFOUNDLAND

AND LABRADOR

PRINCE EDWARD

ISLAND

QUEBEC

STORE TOTAL NORTHWEST

TERRITORIES

1

1

1

0

0

YUKON

4 CTR distribution centres

1 Mark’s distribution centres

1 Joint Mark’s and FGL Sports DC

3 Transload facilities

3 Auto parts distribution centres

3 FGL sports distribution centres

DISTRIBUTION FACILITIES

*Reflects store network as of the end of Q3 2016 6

Our Core Business is Retail

Six key business

categories

2015 REVENUE = C$12.3B C$8.1B C$2.0B C$1.1B C$1.1B

‣ Gas

‣ Auto Parts

‣ Tires & Power

Sports

‣ Auto Service

‣ Car Care &

Accessories

‣ Roadside

Assistance

‣ Home Cleaning

‣ Home Décor

‣ Home Org

‣ Kitchen

‣ Backyard Living

& Fun

‣ Gardening

‣ Outdoor Tools

‣ Seasonal

‣ Home Services

‣ Home Repair

‣ Paint

‣ Tools

‣ Hockey

‣ Golf

‣ Cycling

‣ Fitness

‣ Camping

‣ Hunting

‣ Fishing

‣ Industrial Wear

‣ Men’s Wear

‣ Women’s Wear

‣ Athletic Apparel

‣ Footwear

‣ Accessories

‣ Credit Cards

‣ Retail Deposits

‣ In-store

Warranties

‣ Insurance

‣ Deferred &

Installment

Payments

7

Financial highlights (2015) Banners

Revenue $6.4B

Sales growth * 2.4%

Same store sales growth ** 3.2%

Canadian Tire store count 498

*Results for the full year 2015 (52 weeks ended January 2, 2016) are compared against results for the full year

2014 (53 weeks ended January 3, 2015)

**Reported on a 52 week vs. 52 wk. period

Canadian Tire Retail

Our game plan Our strengths

One of Canada’s most trusted and iconic brands

Most knowledgeable retailer about Life in Canada

Market leader across core categories

Canada’s most read flyer – 12M / week

Local Dealer community presence and trust

Superior real estate locations and national store network

Our growth plan

Strengthen Canadian Tire brand and execute generational shift in

target customer

Revitalize and localize assortments, develop extended

assortments and grow new product pipeline

Build out private label and exclusive brands

Test innovative store concepts (Showroom and Showcase stores)

and refresh network

Analyze customer shopping data from new Canadian Tire Money

loyalty program

Create personalized customer connections and experiences

Expand e-commerce, supply chain and digital capabilities

How we win

Entrepreneurial Associate Dealer model

Offer the best, most relevant assortment and exclusive products

for Life in Canada

Tailored customer connections in-store, online and mobile

Sports partnerships and community engagement

How we fit in the CTC Family

Mature, healthy core business, cash generator

Flagship business, central to Corporate brand

Credibility in core categories

8

FGL Sports

Our game plan

Our strengths

Canada’s largest sporting goods retailer

Close relationships with elite vendor brands

Merchandising and store operations

Leader in digital marketing and concept/flagship stores

Best sports partnerships

Our growth plan

Network expansion: 2 million square feet of new retail space

from 2012 - 2017

Increase flagship stores and launch hero stores

Build unparalleled emotional connection with customers

Digitization of retail including stores, retail assortment,

promotions and brand

Hyper personalized customer experiences across digital and

physical channels

How we win

Conduit for all things sport and activity in Canadian communities

Premier real estate locations

Innovative and exciting in-store experience

Community engagement and sports partnerships activation

Seamless omni experience online, in-store and mobile

Financial highlights (2015) Banners

Revenue $2.0B

Sales growth* 2.7%

Same store sales growth ** 4.4%

Sport Chek same store sales

growth** 6.3%

Store Count 433

*Results for the full year 2015 (52 weeks ended January 2, 2016) are compared against results for the full year

2014 (53 weeks ended January 3, 2015)

**Reported on a 52 week vs. 52 week period

)

How we fit in the CTC Family

Growth driver

Engages younger customer throughout lifecycle

Leader in digital innovation

9

Mark’s

Our game plan

Our strengths

Industrial apparel, footwear and accessories

Product development, innovation and quality

Wholesale division – direct sourcing

Business to business (B2B)

Strong exclusive brands

National store network / ship from store to customer model

Our growth plan

Turbo-charging men’s casual apparel & footwear

Win with 30-50 year old Canadians

Re-invigorate Quebec network

Invest in targeted marketing to new customer demographic

Expanded and bi-lingual e-commerce capabilities – retail and

B2B

How we win

Building brand awareness and affinity

Utilize industrial credibility to grow in adjacent categories

Complement exclusive brands with select national brands

In-store digital improvement and e-commerce expansion

Leverage enhanced sourcing capabilities

Financial highlights (2015) Banners

Revenue $1.1B

Sales growth* -2.3%

Same store sales growth** -0.5%

Store count 380

*Results for the full year 2015 (52 weeks ended January 2, 2016) are compared against results for the

full year 2014 (53 weeks ended January 3, 2015)

**Reported on a 52 week vs. 52 week period

How we fit in the CTC Family

Reactivated growth driver

Strong customer alignment with Canadian Tire

Synergies with FGL Sports in sourcing,

merchandising, supply chain and real estate

10

CT REIT

Our game plan

Our strengths

Irreplaceable Canadian real estate portfolio of 287 properties

totaling approximately 21.5 million square feet of GLA

Durable portfolio features

Investment grade anchor tenant - CTC

Exceptional cash flow predictability and reliable monthly

distributions

Well-planned solid long-term growth

Our growth plan

Acquisition and intensification opportunities

Canadian Tire Corporation property pipeline

Contractual annual rent escalations

How we win

Highly diversified retail portfolio

Flexible design, configuration and dimension provides

capability of supporting a multitude of retail platforms

Actively pursuing third-party retail acquisition opportunities

CT REIT is structured for stability even in potentially volatile

markets

Financial highlights (2015) Growth (YoY)

Property revenue $378.2M +9.7%

Funds from operations $194.7M +10.1%

Adjusted funds from

operations $151.7M +14.1%

AFFO payout ratio 82%

How we fit in the CTC Family

CTC is a major retail tenant with strong brand recognition

Right of first offer on all CTC properties provides

referred access to captive pipeline

11

Canadian Tire Bank

Our game plan

Our strengths

$4.8B in receivables, 1.8M active accounts including over 500K of

Canadian Tire’s most loyal customers

Successful management of higher credit risk through the economic

cycle

Extensive customer data and strong analytics capability

Award winning customer service

Highly effective customer acquisition through retail channels

Our growth plan

Growing gross average accounts receivable (GAAR)

Increasing acquisition of loyal Canadian Tire customers and

generating higher profitability from these accounts

Increasing share of tender across all CTC banners

Strengthening digital/mobile capabilities

How we win

Reinvigorating the value proposition of credit cards

Tighter integration with retail banners and Dealers

Scotiabank partnership creating growth through co-marketing

opportunities

Financial highlights (2015)

Revenue $1.1B +2.4%

GAAR $4.8B +3.3%

Average number of accounts

with a balance (thousands) 1,840 +0.2%

Return on receivables 7.73%

How we fit in the CTC Family

Earnings generator

Supports core retail business

12

11,427 11,786

12,463 12,280

9,500

10,500

11,500

12,500

2012 2013 2014 2015

Consolidated Revenue (C$ in millions)1

Delivering Solid Results

1,138 1,236 1,376 1,519

0

1,000

2,000

2012 2013 2014 2015

Consolidated EBITDA (C$ in millions)1

6.45 7.02

7.94 8.61

$5

$7

$9

2012 2013 2014 2015

Adjusted Diluted EPS attributable to owners of CTC ($)1,2

27.3%

28.2%

28.9%

30.0%

25.0%

26.0%

27.0%

28.0%

29.0%

30.0%

31.0%

2012 2013 2014 2015

Retail gross margin (% of revenue)

6.76%

7.32% 7.36%

7.73%

6.2%6.4%6.6%6.8%7.0%7.2%7.4%7.6%7.8%8.0%

2012 2013 2014 2015

Financial Services Return on Receivables (%)

13 1 – Results for the full-year 2015 (52 weeks ended January 2, 2016) are compared against results for the full-year 2014 (53 weeks ended January 3, 2015) 2 – Refer to Section 11.3.2 and 10.3 of the Company’s Q4 and full-year 2015 and 2014 MD&A , respectively, for additional information on adjusted diluted EPS.

2016 Strategic Imperatives

14

Strengthen brands and enhance customer experiences

Transition to the new world of omni-retail where digital complements physical

Drive growth and productivity in core businesses

Create an agile and high-performing corporate culture

1

2

3

4

Balanced Capital Allocation

0.3 0.5 0.5

0.7 0.1

0.1 0.1

0.2

0.0

0.1

0.3

0.4

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

2012 2013 2014 2015

CAPEX* Dividends Share Repurchase**

$0.5B

$0.7B

$1.0B

$1.3B

1 2 3 4 Invest in the

business

Repurchase shares/

grow dividend (target payout ratio 25%-30%)

Maintain investment

grade credit rating Inorganic growth

opportunities

Since 2012, Canadian Tire Corporation has

returned in excess of $1.3B to shareholders1

while investing $2.1B in its store network2, IT

and distribution capacity3

Announced intention in November 2015 to

repurchase $550M Class A Non-Voting

shares in excess of anti-dilutive repurchases

by end of 20163

Canadian Tire Corporation maintains a BBB

(high) and BBB+ rating and a stable outlook

from both DBRS and S&P, respectively.

* Excluding REIT capital. ** Buybacks in excess of anti-dilutive buybacks 1 – Dividends and share buybacks in excess of anti-dilutive buybacks

2 – Excludes REIT capital

3 – See slide 18 for Q3 2016 dividend and share buyback announcements and slides 22 and 23 for

updated 2016 and 2017 guidance

15

39%

31% $0.3B

$0.5B $0.5B

21%

$0.7B

8%

3%

5% 4%

5%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

0

100

200

300

400

500

600

700

800

900

1,000

2012 2013 2014 2015

Store Network IT Supply Chain/DC Other

For 2016, forecast operating CAPEX of $475M to $500M (additional DC capacity CAPEX in the range of $100M to $125M)

2016 includes increased spend on retail network expansion, including the costs to open 12 former Target locations, the continuation of the

FGL Sports growth strategy, and for continued investments in digital and technology initiatives.

Capital Investments

CAPITAL INVESTMENTS (2012 – 2015)1

1 –Excludes REIT capital

% of Revenue

16

Shareholder Value Creation

CT REIT Initial Public Offering

CTC retained 83.1% majority interest in CT REIT allowing CTC to retain control over its real estate

properties

Surfaced the value of CTC’s real estate

Created a stand-alone vehicle for CTC’s real estate which will support continued real estate investment

Provide CTC with increased financial flexibility to pursue new opportunities to invest in and grow the

business

Scotiabank Partnership Transaction

Scotiabank purchased 20% minority interest in Canadian Tire’s Financial Services business for $500

million

Scotiabank provided committed funding facility of $2.25 billion to backstop funding of Financial Services’

credit card receivables

Partners identifying co-marketing opportunities to improve customer loyalty and generate incremental

sales through sponsorships and new products and services

Canadian Tire and Scotiabank aligned on community-based initiatives and sports partnerships

17

Returning Value to Shareholders

Q3 2016 – authorized the repurchase of up to $550M of Class A Non-Voting shares (beyond anti-dilutive)

through the end of 2017. In Q3 2016, $110M of Class A Non-Voting shares (beyond anti-dilutive) were

repurchased, leaving $110M of Class A Non-Voting shares to be repurchased in the balance of 2016.

Q2 2016 – repurchase of $110M of Class A Non-Voting shares (beyond anti-dilutive purchases)

Q1 2016 – repurchase of $110M of Class A Non-Voting shares (beyond anti-dilutive purchases)

Q4 2015 – repurchase of $110M of Class A Non-Voting shares (beyond anti-dilutive purchases)

Q3 2015 – authorized the repurchase of up to $550M of Class A Non-Voting shares (beyond anti-dilutive)

through the end of 2016.

2013 through Q2 2015 – cumulative repurchase of $700M of Class A Non-Voting share (beyond

anti-dilutive purchases)

Share Repurchases

Dividends

18

Q3 2016 – increased annual dividend to $2.60 per share, up 13.0%

Q3 2015 – increased annual dividend to $2.30 per share, up 9.5%

Q3 2014 – increased annual dividend to $2.10 per share, up 5.0%

Q1 2014 – increased annual dividend to $2.00 per share, up 14.3%

$0.56

$0.64

$0.72

$0.82 $0.84 $0.84

$1.10

$1.20

$1.40

$1.88

$2.10

$2.30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Returning Value to Shareholders

Policy to maintain dividend payments equal to 25% to

30% of the prior year’s normalized basic net earnings

Member of S&P/TSX Canadian Dividend Aristocrats index

Annual Dividends Paid

* In Q3 2016, CTC announced an annual dividend increase of 13.0% to $2.60 per share

19

13.7% CAGR

Canadian Tire – a Strong Investment Proposition

~490 Associate Dealers in local communities across Canada

Attracting and retaining world-class talent to grow businesses

Experienced leadership in key functions across the Company

Continued focus on brand-led organization

$12.3 billion in revenue

32.0 million retail square feet

Financial Services GAAR of $4.8B 20

Extensive reach and scale of business

90% of Canadians located 15 minutes from a Canadian Tire store

National presence with ~1,700 retail and gasoline outlets

One in five Canadians hold a Canadian Tire Options MasterCard

Differentiators

Delivering strong financial results

Clearly defined growth plan with underlying financial aspirations

Strong balance sheet and multiple funding sources

Committed to balanced approach for returning capital to shareholders

Delivering strong financial results

2016 & 2017 Outlook

21

2016 Outlook Update

22

Operating expense growth aligned with revenue growth

Effective tax rate estimate: 26.5% for 2016

In 2016, operating CAPEX estimated between $475 million and $500 million due primarily to Retail

store network investment, including the cost to open 12 former Target locations in 2016, and

investment in IT and digital initiatives.

Additional CAPEX:

Approximately $100 million to $125 million associated with future distribution capacity in 2016

Third-party property acquisitions by CT REIT

Expected three year (2015-2017) average annual CAPEX between $450 million and $500 million to

support significant investments in digital technology and Retail store network growth

2017 Outlook

23

Operating expense growth aligned with revenue growth

Effective tax rate estimate: 27.0% for 2017

In 2017, operating CAPEX estimated between $400 million and $425 million due primarily to Retail

store network investment, and investment in IT and in digital technology.

Additional CAPEX:

Approximately $25 million to $50 million associated with future distribution capacity in 2017

Third-party property acquisitions by CT REIT

Operational efficiency initiatives

Expected three year (2015-2017) average annual CAPEX between $450 million and $500 million to

support significant investments in digital technology and Retail store network growth

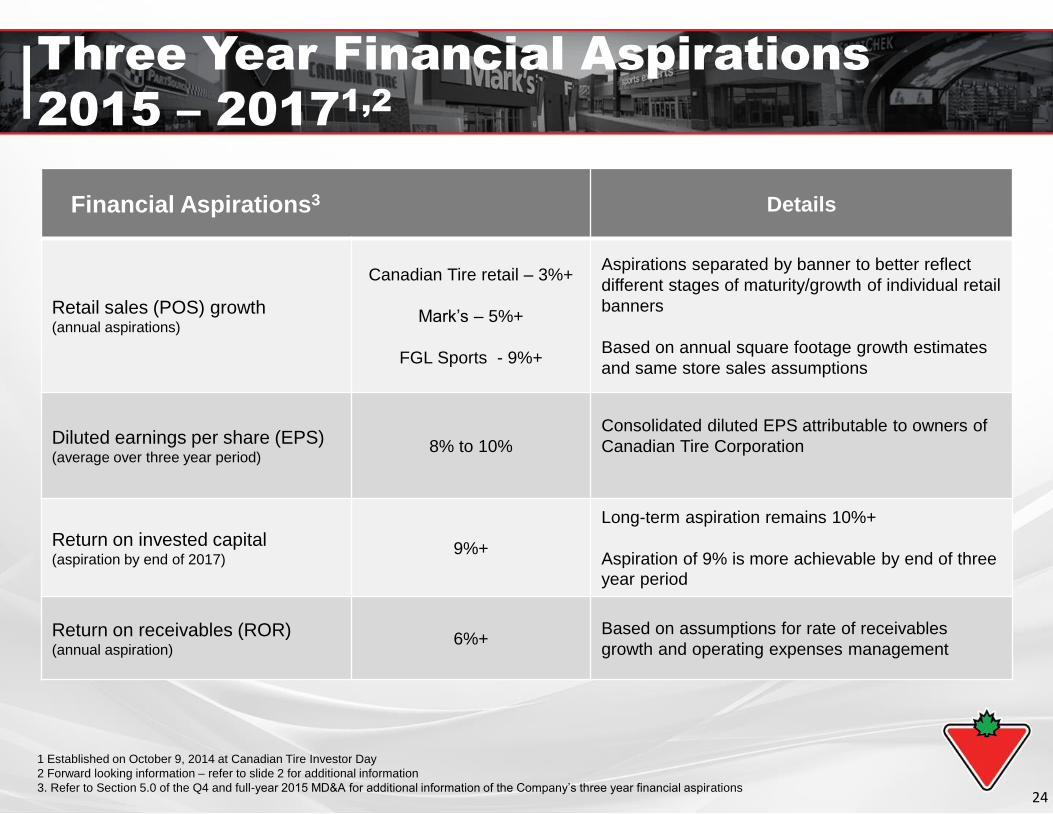

Three Year Financial Aspirations

2015 – 20171,2

Financial Aspirations3 Details

Retail sales (POS) growth (annual aspirations)

Canadian Tire retail – 3%+

Mark’s – 5%+

FGL Sports - 9%+

Aspirations separated by banner to better reflect

different stages of maturity/growth of individual retail

banners

Based on annual square footage growth estimates

and same store sales assumptions

Diluted earnings per share (EPS) (average over three year period)

8% to 10%

Consolidated diluted EPS attributable to owners of

Canadian Tire Corporation

Return on invested capital (aspiration by end of 2017)

9%+

Long-term aspiration remains 10%+

Aspiration of 9% is more achievable by end of three

year period

Return on receivables (ROR) (annual aspiration)

6%+ Based on assumptions for rate of receivables

growth and operating expenses management

1 Established on October 9, 2014 at Canadian Tire Investor Day

2 Forward looking information – refer to slide 2 for additional information

3. Refer to Section 5.0 of the Q4 and full-year 2015 MD&A for additional information of the Company’s three year financial aspirations 24

25

For more information http://investors.canadiantire.ca [email protected] or (416) 480-8725

Download our Investor Relations App

Follow us on twitter @CanTireCorp