Embed Size (px)

Citation preview

4Q16 Institutional

Presentation

2/37 Investor Relations | 4Q16 |

Profile and History

Pine

History

Business Strategy

Competitive Landscape

Focus Always on the Client

Corporate Credit

FICC

Pine Investimentos

Strategic Partnership

Corporate Governance

Organizational Structure

Corporate Governance

Social Investment and Responsibility

Economic Overview

Macroeconomic

Credit Growth

Expectations

Highlights and Results

Summary

3/37 Investor Relations | 4Q16 |

Profile and History

4/37 Investor Relations | 4Q16 |

Pine

Specialized in providing financial solutions for corporate clients…

Credit Portfolio by Annual Client Revenues Customer Profile

Bank Profile

Focused on establishing long-term relationships

Fast response | Specialized services

Customized products | Product diversity

R$ 6,445 million in Loan Portfolio

R$ 1,148 million in Shareholders’ Equity

Long-term National Rating at A by Fitch

Business is structured along three primary business lines:

Corporate Credit: credit and financing products

FICC: instruments for hedging and risk

management

Pine Investimentos: Capital Markets, Financial

Advisory, Project & Structured Finance and

Research

Large Corporate (> R$ 2.000 millions)

Corporate (R$ 500 - R$ 2.000 millions)

Companies (R$ 50 - R$ 500 millions)

Retail (PFs e small companies)

Balance sheets audited by third parties, corporate governance,

well defined hedging policies, and the lower risk profile Over R$2 billion38%

R$500 million to R$2 billion

25%

Up to R$500 million

36%

5/37 Investor Relations | 4Q16 |

...with extensive knowledge of Brazil’s corporate credit cycle.

History

1997

Noberto Pinheiro sell

his stake in BMC and

found Pine

1939

Pinheiro Family

founds

Banco Central do

Nordeste

1975

Noberto Pinheiro

becomes one of

BMC’s controlling

shareholders

Devaluati-

on of the

real

Nasdaq Sept. 11 Brazilian

Elections

(Lula) Subprime

Russian

Crisis European

Community

2007

Discontinuation of the payroll-deductible loan

business, with changes in the corporate business

strategy. Hence, there was a creation of Pine

Investimentos, besides the opening of the Cayman

branch

October, 2011 Subscription of Pine’s capital by DEG

August, 2012

Subscription of Pine’s capital by DEG, Proparco, Controlling Shareholder and Management

2015

Portfolio deleveraging strategy due to an political and economic scenario

March, 2007

IPO

May, 2016

19 years

2005

Noberto Pinheiro

became Pine’s

controller

2H2016

The turning point of the Bank’s portfolio

155 184 222 341 521 620 755 663 7611,214

2,854 3,108

4,195

5,763

6,963

7,911

9,920 9,826

6,9336,445

1862

121 126 140 136 152 171209

335

801827 825

867

1,015

1,220

1,272 1,256

1,163 1,148D

ec-9

7

Dec-9

8

Dec-9

9

Dec-0

0

Dec-0

1

Dec-0

2

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

Dec-1

3

Dec-1

4

Dec-1

5

Dec-1

6

Corporate Credit Portfolio (R$ Million)

Shareholders' Equity (R$ Million)

6/37 Investor Relations | 4Q16 |

Business Strategy

7/37 Investor Relations | 4Q16 |

Competitive Landscape

Pine serves a niche market of companies with few options for banks.

100% focused on providing complete service

to companies, offering customized products

100% Corporate

Large Multi-Services banks

Market

Consolidation of the banking sector has decreased

the supply of credit lines and financial instruments

for corporate

Foreign banks are in a deleveraging process

PINE

Full service Bank – Credit, Hedging, and Investment

Bank products – with room for growth

~15 clients per officer

Competitive Advantages:

Focus

Fast response: Strong relationship with

clients, with the credit committee meeting

once a week ensures rapid return to customer

needs

Specialized services

Tailor-made solutions

Product diversity

Foreign and

Investment Banks

SME & Retail

Corporate e SME

Retail

8/37 Investor Relations | 4Q16 |

Focus Always on the Client

Products tailored to meet the needs of each individual client.

In addition to the

headquarters located in the

city of São Paulo, Pine has 6

branches throughout Brazil , in

the States of Mato

Grosso, Paraná,

Pernambuco, Rio de Janeiro,

Rio Grande do Sul, and

São Paulo. The origination

network also counts with a

Cayman Branch, especially for

Trade Finance transactions.

9/37 Investor Relations | 4Q16 |

Corporate Credit

Actions Credit Committee

Strong track record and solid credit origination and approval process.

Credit Approval: Electronic Process

Origination

Officers

Credit origination

Credit analysis, visit to

clients, data updates,

interaction with internal

research team

Credit Analysts

Regional Heads of

Origination and

Credit Analysis

Presentation to the Credit

Committee

Directors and

Analysts of Credit

Centralized and

unanimous decision

making process

CREDIT

COMMITTEE

Meets once a week – reviewing on ~ 20 proposals

Minimum quorum: 4 members - attendance of CEO or

Chairman is mandatory

Committee Members:

CEO

Chief Financial Officer

Chief Administrative Officer

Credit Director

Corporate and Investment Banking Director

Superior Committee Members:

Two members of the Board

Participants:

FICC Director

Credit Analysts Team

Other members of the Corporate Banking origination

team

Personalized and agile service, working closely with clients and

keeping a low client to account officer ratio: each officer

handles ~15 economic groups

Geographic coverage of clients, providing the bank with local

and extremely up-to-date credit intelligence and information

Established long term relationships with more than 500

economic groups

Pine has approximately 20 professionals in the credit analysis

area, assuring that analysis is fundamentally driven and based

on industry-specific intelligence

Efficient loan and collateral processes, documentation, and

controls, which has resulted in a low NPL track record

Discussion on sizing,

collateral, structure etc.

Superior

Committee

Approval

Tickets over R$ 15 MM

10/37 Investor Relations | 4Q16 |

September 30rd, 2016

Currencies (74%): Dollar, Euro, Yen, Pound, Canadian

Dollar, Australian Dollar

Commodities (17%): Sugar, Soybean ( Grain, Meal and Oil),

Corn, Cotton, Metals, Energy

Fixed income (9%): Fixed, Floating, Inflation, Libor

FICC

Solid trackrecord.

Market Segments Competitive Advantages

One Stop Shop: credit and risk mitigation

Every transaction demands prior credit approval

Collaterals surpass approved derivative’s limits

Agility| Client Focused| Diversification

Average of 30 days to close a derivative transaction

(domestic large banks average - 90 days)

Sample Transaction

Trader prices the

transaction, including spread

Treasury hedges the

transaction

Transaction closed

Treasury informs the spot

price

Global Derivatives

Agreement

(ISDA Master Agreement)

• Limits

• Types of Derivatives

• Collaterals

• Market Risk: 100% Hedged

• Limits

PINE Credit Analysis

Process

FICC

• Credit Analysis

• Collaterals

• Cross-selling opportunity

• Credit Committee Approval

Client 1st

2nd

Margin Calls Management Derivatives

11/37 Investor Relations | 4Q16 |

Pine Investimentos

9th place in volume of short-term fixed income transactions, being the 5th player in the number of transactions

Operating Model

Selected Transactions

Pine Investimentos

Financial Advisory Capital Markets Project

Finance

Fixed Income (CRIs, CRAs)

Infrastructure Debentures

Equities

Securitization

Hybrid capital

transactions

Project & Structured

Finance

Investidores

Family Offices

Individuals

Companies

Asset Managers

Financial Institutions

Pension Funds

Foreign Investors

Hedge Funds

September, 2016

Structure CreditFacility

R$ 10,000,000

Lead Coordinator

September, 2016

Mortage Backed Securities

R$ 10,000,000

Lead Coordinator

September, 2016

Bond

R$ 469,000,000

October, 2016

NCE

R$ 30,000,000

Coordinator

October, 2016

Mortage Backed Securities

R$ 50,000,000

Lead Coordinator

November, 2016

Promissory Note

R$ 20,000,000

November, 2016

CRI

R$ 47,400,000

Lead Coordinator

December, 2016

Mortage Backed Securities

R$ 8,500,000

Lead Coordinator

December, 2016

CRI

R$ 50,000,000

Lead Coordinator

12/37 Investor Relations | 4Q16 |

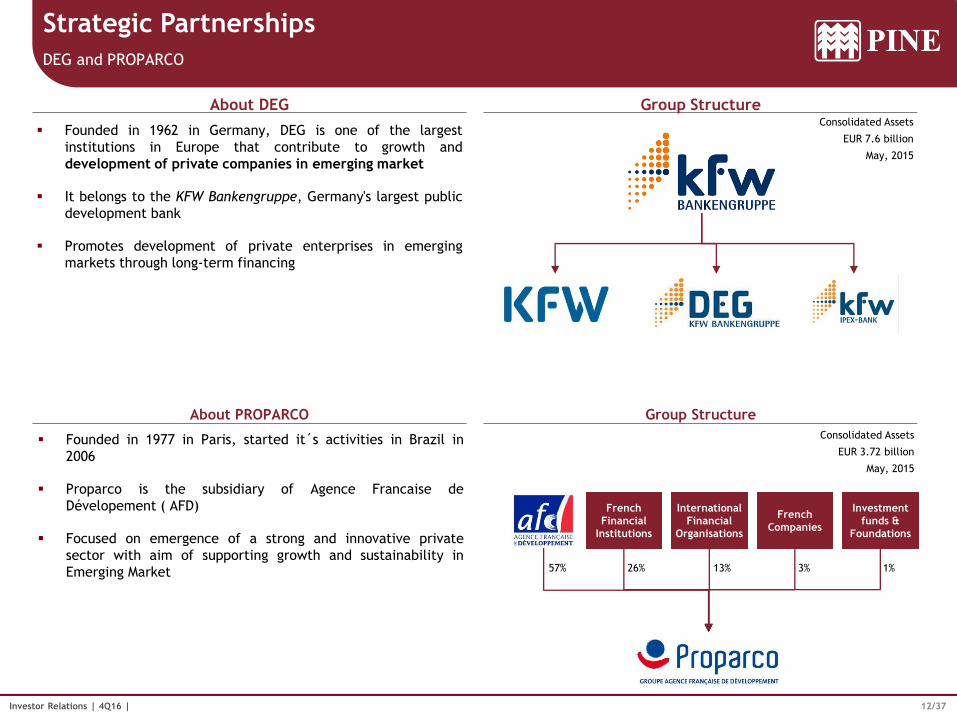

Strategic Partnerships

About DEG

About PROPARCO

Group Structure

Group Structure

DEG and PROPARCO

Founded in 1962 in Germany, DEG is one of the largest

institutions in Europe that contribute to growth and

development of private companies in emerging market

It belongs to the KFW Bankengruppe, Germany's largest public

development bank

Promotes development of private enterprises in emerging

markets through long-term financing

Consolidated Assets

EUR 7.6 billion

May, 2015

Founded in 1977 in Paris, started it´s activities in Brazil in

2006

Proparco is the subsidiary of Agence Francaise de

Dévelopement ( AFD)

Focused on emergence of a strong and innovative private

sector with aim of supporting growth and sustainability in

Emerging Market

Consolidated Assets

EUR 3.72 billion

May, 2015

57%

French

Financial

Institutions

International

Financial

Organisations

French

Companies

Investment

funds &

Foundations

26% 13% 3% 1%

13/37 Investor Relations | 4Q16 |

Corporate Governance

14/37 Investor Relations | 4Q16 |

Organizational Structure

Non-bureaucratic Culture, entrepreneurial and meritocratic with a flat hierarchy

CEO

Norberto Zaiet Jr.

INTERNAL AUDIT COMPENSATION

COMMITTEE AUDIT COMMITTEE

EXTERNAL AUDIT

PWC

Noberto N. Pinheiro Jr. Rodrigo Pinheiro Igor Pinheiro Noberto Pinheiro Norberto Zaiet Gustavo Junqueira Mailson de

Nóbrega Susana Waldeck

President Vice-President Vice-President Member Member Independent

Member

Independent

Member

External

Member

BOARD OF DIRECTORS

RISKS COMMITTEE

Corporate & IB

Mauro Sanchez

Finances

Welinton Gesteira

Operations

Ulisses Alcantarilla

Business

João Brito

Structuring- DCM

Investment Banking

Corporate Banking

Assets and Liabilities

Back-office

Legal

Compliance, Internal

Control and Security of

Information

Collaterals Management

Management Special

Assets

Middle Office

Exchange

Services

Sales & Trading

International

Research Macro /

Commodities/ Companies

Funding & Distribution

Marketing

Investor Relations

Structured Products

ALM e FLOW

Accounting and Tax

Planning

Market and Liquidity

Risks

Strategic Planning and

P&L

Commercial Planning and

Valuation

Credit

Marcelo Camargo

Credit

Register

RH

Camilla Suave IT

15/37 Investor Relations | 4Q16 |

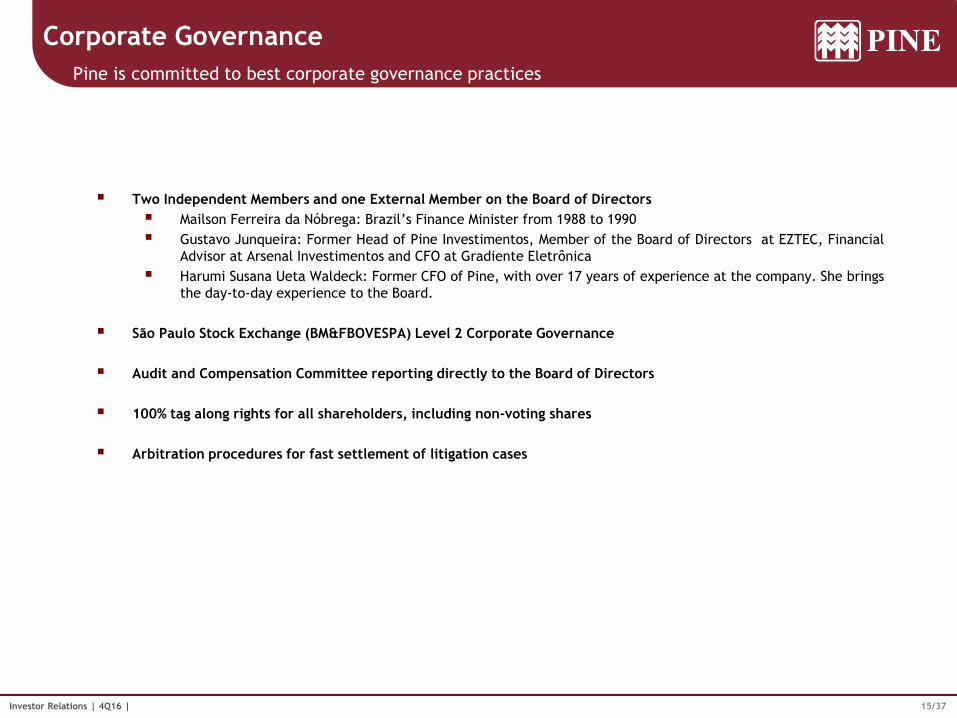

Corporate Governance

Pine is committed to best corporate governance practices

Two Independent Members and one External Member on the Board of Directors

Mailson Ferreira da Nóbrega: Brazil’s Finance Minister from 1988 to 1990

Gustavo Junqueira: Former Head of Pine Investimentos, Member of the Board of Directors at EZTEC, Financial

Advisor at Arsenal Investimentos and CFO at Gradiente Eletrônica

Harumi Susana Ueta Waldeck: Former CFO of Pine, with over 17 years of experience at the company. She brings

the day-to-day experience to the Board.

São Paulo Stock Exchange (BM&FBOVESPA) Level 2 Corporate Governance

Audit and Compensation Committee reporting directly to the Board of Directors

100% tag along rights for all shareholders, including non-voting shares

Arbitration procedures for fast settlement of litigation cases

16/37 Investor Relations | 4Q16 |

Social Investment and Responsibility

Focus on the short, medium and long term.

Social Investment Recognition

Partnerships

Most Green Bank

Recognized by the International Finance Corporation (IFC), private

agency programs of the World Bank as the most "green" bank as a result

of its transactions under the Global Trade Finance Program (GTFP) and

its onlending to companies focused on renewable energy and ethanol

Efficiency Energy

Recognition by World Bank for support in the Energy Efficiency sector.

Responsible Credit

“Lists of Exceptions”: the Bank does not finance projects or those

organizations that damage the environment, are involved in illegal

labor practices or produce, sell or use products, substances or activities

considered prejudicial to society.

System of environmental monitoring, financed by the IADB and

coordinated by FGV, and internally-produced sustainability reports for

corporate loans

Protocolo Verde – “Green Protocol”, an agreement

between FEBRABAN and the Ministry of the Environment

to support development that does not compromise future

generations.

Exhibition and sponsorship of Brazilian artists, for instance Paulo von Poser and

Miguel Rio Branco, in addition to sponsoring and supporting films and

documentaries such as Quebrando o Tabu (Fernando Henrique Cardoso on the

drug war), O Brasil deu certo, e agora? (idealized by Mailson da Nóbrega), Além

da Estrada (Charly Braun) and others.

Sustainability Annual Report

Seventh consecutive year disclosing the

Sustainability Report in the GRI

standard. The 2015 report, with its high

level of clarity, transparency and quality

was recognized with the fourth place in

the Abrasca Annual Report Award,

considering its category of companies

with net income to R$3 billion.

17/37 Investor Relations | 4Q16 |

Economic Overview

18/37 Investor Relations | 4Q16 |

17.617.519.2

23.5

16.4

19.1

15.3

12.0

12.5 10.19.911.8

8.6 8.3 11.0

13.514.1

10.9

9.5 9.8

10.0

5

10

15

20

25

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Forecast

Selic (interest rate, average) Média móvel 4 anos

Macroeconomic

Real GDP

SELIC

IPCA (CPI)

Gross Government Debt

Due to the challenging economic scenario...

Moving Avarage 4 years

4.4

1.4

3.1

1.1

5.8

3.24.0

6.15.1

-0.1

7.5

3.9

1.9

3.0

0.1

-3.8-3.5

0.5

3.0

1.5

1.5

-6

-4

-2

0

2

4

6

8

10

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Forecast

Real GDP growth rate (%) Média móvel 4 anosMoving Avarage 4 years

6.0

7.7

12.5

9.3

7.6

5.7

3.1

4.5

5.9

4.3

5.96.5

5.8 5.96.4

10.7

6.3

4.5 4.5 4.5 4.5

3

5

7

9

11

13

15

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Forecast

IPCA (CPI)

67

76

72

6867

55

57 5659

52

51

5452

57

6770

77

79

82

85

50

60

70

80

90

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Forecast

Gross government debt (% GDP)

19/37 Investor Relations | 4Q16 |

0

10

20

30

40

50

60

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total credit/GDP (%)

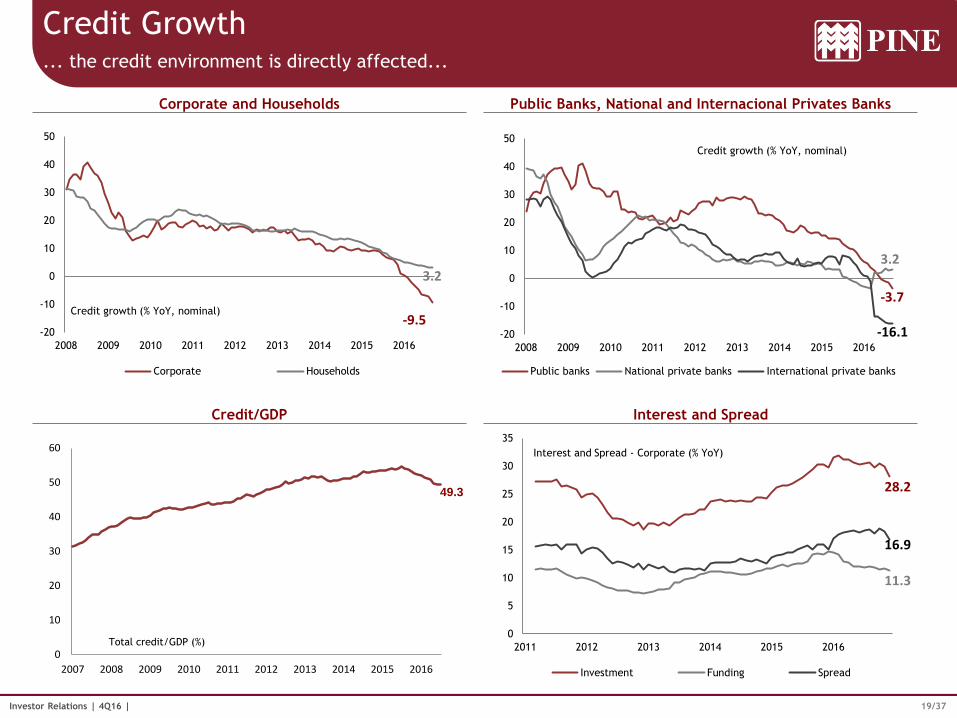

Credit Growth

Corporate and Households

Credit/GDP

Public Banks, National and Internacional Privates Banks

Interest and Spread

... the credit environment is directly affected...

49.3

-20

-10

0

10

20

30

40

50

2008 2009 2010 2011 2012 2013 2014 2015 2016

Credit growth (% YoY, nominal)

Corporate Households

-9.5

3.2

-20

-10

0

10

20

30

40

50

2008 2009 2010 2011 2012 2013 2014 2015 2016

Credit growth (% YoY, nominal)

Public banks National private banks International private banks

-3.7

3.2

-16.1

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015 2016

Interest and Spread - Corporate (% YoY)

Investment Funding Spread

28.2

11.3

16.9

20/37 Investor Relations | 4Q16 |

Expectations ...however, we expect that this scenario has a slight improvement in 2017.

Source: Pine Bank, December 2016

Brazil: Key Economic Indicators - PINE

INDICATORS 2011 2012 2013 2014 2015 2016E 2017E 2018E

Real GDP growth rate (%) 3.9% 1.9% 3.0% 0.1% -3.9% -3.5% 0.5% 3.1%

BRLUSD (eop) 1.83 2.08 2.35 2.65 3.87 3.35 3.40 3.60

BRLUSD (average) 1.67 1.95 2.16 2.35 3.33 3.49 3.30 3.50

IPCA (CPI) 6.5% 5.8% 5.9% 6.4% 10.7% 6.3% 4.5% 4.5%

IGP-M (PPI) 5.1% 7.8% 5.5% 3.5% 10.5% 7.2% 3.7% 5.0%

Selic (interest rate, eop) 11.00% 7.25% 10.00% 11.75% 14.25% 13.75% 9.50% 9.50%

Selic (interest, average) 11.71% 8.46% 8.44% 11.02% 13.58% 14.15% 10.92% 9.50%

Trade balance (USD bn) 29.8 19.4 2.6 -3.9 19.7 47.7 55.0 35.0

Current account (USD bn) -73.2 -78.4 -83.0 -103.6 -58.9 -23.5 -30.0 -45.0

Current account (% GDP) -2.8% -3.5% -3.8% -4.8% -3.3% -1.3% -1.5% -2.2%

FDI (US$bn) 101 87 69 97 75 78.9 80.0 90.0

Primary surplus (% GDP) 2.9% 2.2% 1.7% -0.6% -1.9% -2.5% -2.1% -1.5%

Gross government debt (% GDP) 51.3% 54.8% 53.3% 58.9% 66.4% 69.5% 76.5% 78.7%

21/37 Investor Relations | 4Q16 |

Highlights and Results

22/37 Investor Relations | 4Q16 |

Highlights

Liquid balance sheet with a cash position of R$ 1.8 bi, equivalent to 50% of time deposits.

Excess capital, with a BIS ratio of 15.8%, being 15.3% in Tier I Capital.

Loan portfolio coverage ratio surpassed 6% as a result of relevant provisions over the past quarters.

Retraction of approximately 8% in personnel and administrative expenses in the accumulated of 9 months.

Continuous liability management with a diversified portfolio and adequate terms.

23/37 Investor Relations | 4Q16 |

7,409 6,859

Sept-15 Dec-15

Total Funding

-7.4%

1,181 1,163

Sept-15 Dec-15

Shareholders' Equity

-1.5%

3.5% 3.6%

3Q15 4Q15

ROAE

0.1 p.p

2.9% 3.2%

3Q15 4Q15

NIM Evolution

0.33 p.p.

10 10

3Q15 4Q15

Net Income

Financial Highlights

1 Includes Stand by LCs, Bank Guarantees, Credit Securities to be Received and Securities (bonds, CRIs, eurobonds and fund shares)

R$ million

7,691 6,933

Sept-15 Dec-15

Total Loan Portfolio1

-9.9%

6,933 6,238 6,445

Dec-15 Sept-16 Dec-16

Total Loan Portfolio1

3.3%

-7.0%

6,859 5,908 5,692

Dec-15 Sept-16 Dec-16

Total Funding

-3.7%

-17.0%

1,163 1,152 1,148

Dec-15 Sept-16 Dec-16

Shareholders' Equity

-0.3%

-1.3%

3.2%

2.0%

1.0%

4Q15 3Q16 4Q16

NIM

-220 bps.

-100 bps.

3.4%

1.7%

2015 2016

NIM Evolution

-170 bps

10

-7-9

4Q15 3Q16 4Q16

-190.0%

-37.2%3.6%

-2.3%

-3.1%

4Q15 3Q16 4Q16

ROAE

-670 bps.

-80 bps.

3.4%

-1.2%

2015 2016

ROAE

-460 bps

41

-142015 2016

Net Income

-134.9%

24/37 Investor Relations | 4Q16 |

Revenue Mix Product and Revenue Diversification

Business Lines

Credit64.4%

FICC22.0%

Pine Investimentos

8.9%

Treasury4.7%

2016

Credit79.1%

FICC14.5%

Pine Investimentos

3.8%

Treasury2.6%

2015

25/37 Investor Relations | 4Q16 |

NIM and Efficiency Ratio

NIM

Expenses and Efficiency Ratio

Rigorous cost control.

2321 22

1917

18

60.0%77.6%

111.1%

-200%

-150%

-100%

-50%

00%

50%

100%

150%

0

5

10

15

20

25

30

35

40

4Q15 3Q16 4Q16

Personnel Expenses

Other administrativeexpenses

Recurring EfficiencyRatio (%)

3.2%

2.0%

1.0%

4Q15 3Q16 4Q16

NIM

-220 bps.

-100 bps.

3.4%

1.7%

2015 2016

NIM Evolution

-170 bps

26/37 Investor Relations | 4Q16 |

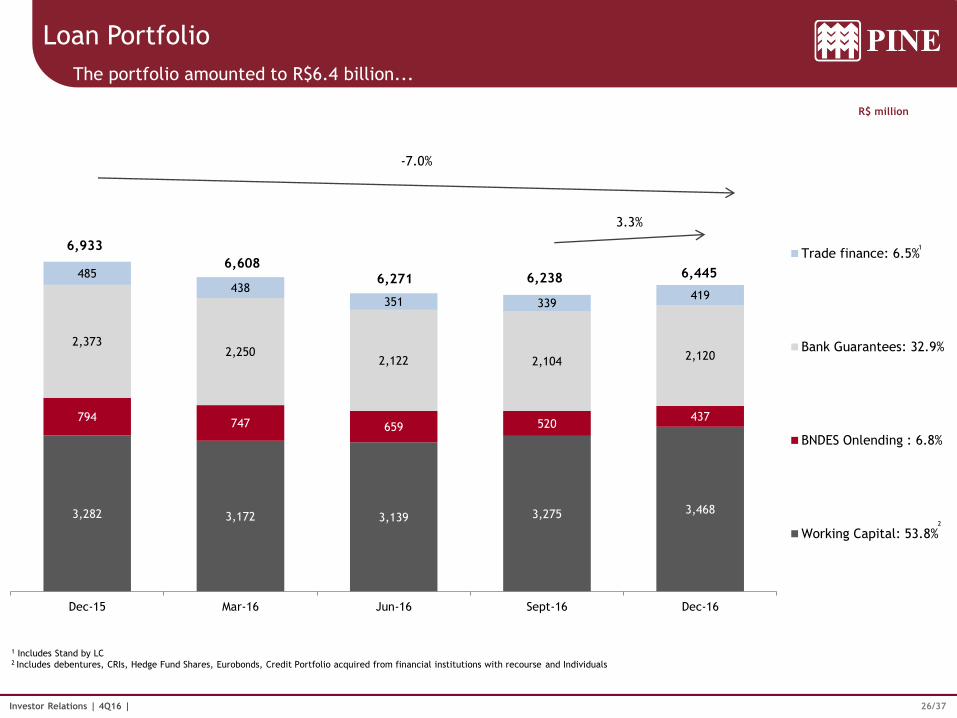

3,282 3,172 3,139 3,275 3,468

794747 659 520

437

2,3732,250

2,122 2,104 2,120

485

438351 339

419

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Trade finance: 6.5%

Bank Guarantees: 32.9%

BNDES Onlending : 6.8%

Working Capital: 53.8%

6,6086,271 6,238

6,933

6,445

1 Includes Stand by LC 2 Includes debentures, CRIs, Hedge Fund Shares, Eurobonds, Credit Portfolio acquired from financial institutions with recourse and Individuals

R$ million

Loan Portfolio

The portfolio amounted to R$6.4 billion...

1

-7.0%

3.3%

2

27/37 Investor Relations | 4Q16 |

Continuous Loan Portfolio Management

Sectors Rebalance

...with improved sector diversification...

The composition of the portfolio of the 20 largest clients changed by over 20% in the past twelve months;

The share of wallet of the 20 largest clients remained at around 30%, in line with market peers.

39%36%40%40%39%

6%6%

6%5%5%

9%10%8%9%7%

10%13%14%14%15%

11%10%10%9%9%

12%12%12%14%

12%

13%13%10%9%13%

Dec-16Dec-15Dec-14Dec-13Dec-12

Energy

Real Estate

Agriculture

Sugar and Ethanol

Engineering

Transportationand Logistics

Others

Energy13%

Real Estate12%

Agriculture11%

Sugar and Ethanol10%

Engineering9%

Transportation and Logistics

6%Telecom

5%

Foreign Trade4%

Specialized Services

4%

Retail3%

Metallurgy3%

Construction Material

2%

Mining2%

Vehicles and Parts2%

Meatpacking2%

Food Industry1%

Other10%

28/37 Investor Relations | 4Q16 |

Portfolio strategy

Active Groups Average Ticket per Group

...with the entry of new and active customers and a reduction of the average ticket...

The continuity of the current economic recovery process tends to support a diversified growth strategy focused on the cross-sell

of products and services

25,196

20,513

18,062

4Q14 4Q15 4Q16

390

338359

4Q14 4Q15 4Q16

29/37 Investor Relations | 4Q16 |

AA-A22.6%

B23.5%

C40.2%D-E

7.8%

F-H5.8%

9.3%

15.1%

13.7%

5.1%

6.1% 5.9%

00%

02%

04%

06%

08%

10%

12%

-01%

01%

03%

05%

07%

09%

11%

13%

15%

17%

Dec-15 Sept-16 Dec-16

D-H Portfolio Coverage of Total Portfolio

80%

193%

426%

50.0%

250.0%

450.0%

650.0%

Coverage of D-H Overdue Portfolio

1D-H Portfolio: D-H Portfolio / Loan Portfolio Res. 2,682 2Coverage of Total Portfolio: Provisions / Loan Portfolio Res. 2,682 3Coverage D-H Overdue Portfolio: Provisions / D-H Overdue Portfolio

December 31st, 2016

Contracts Overdue: total amount of the contracts overdue for more than 90 days / Loan Portfolio

excluding Bank Guarantees and Stand-by Letters of Credit.

Loan Portfolio Quality

86.3% of the loan portfolio is classified between AA-C ratings.

Loan Portfolio Quality – Res. 2,682

Credit Coverage

Non Performing Loans > 90 days (Total Contract)

Collaterals

1 2 3

Products Pledge

37%

Receivables14%

Properties Pledge

46%

Investments3%

1.1%

2.1%1.8%

1.2%1.7%

0.7%1.3% 1.5%

0.6%

Dec-14 Mar-15 Jun-15 Sept-15 Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

30/37 Investor Relations | 4Q16 |

R$ million

Funding

Diversified sources of funding...

53% 53% 52% 50% 31% Cash over Deposits

841 787 648 617 460

324 348261 376

384

1,570 1,662 1,939

2,600 2,980

336 218 156

13346

18 17 19

2917

806 759 668

530 454295 284 296

198 213751 761 734

259 247

279244

216 206 204

1,029777

680 665 416

113

6139 33

33

497

352

270 262239

6,859

6,270

5,925 5,9085,692

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Trade Finance: 4.2%

Private Placements: 0.6%

Multilateral Lines: 7.3%

International Capital Markets:3.6%

Financial Letter : 4.3%

Local Capital Markets: 3.7%

Onlending: 8%

Demand Deposits: 0.3%

Interbank Time Deposits: 0.8%

High Net Worth Individual TimeDeposits: 52.4%

Corporate Time Deposits: 6.7%

Institutional Time Deposits:8.1%

31/37 Investor Relations | 4Q16 |

45% 48% 51%64% 68%

55% 52% 49%36% 32%

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Total Deposits Others

Leverage: Expanded Loan Portfolio / Shareholders’ Equity

Expanded Loan Portfolio excluding Bank Guarantees and Stand-by Letters of Credit /

Shareholders’ Equity

Credit over Funding ratio: Loan Portfolio excluding Bank Guarantees and Stand-by Letters of

Credit / Total Funding

Asset & Liability Management

... matching assets’ and liabilities’ duration.

Leverage Credit over Funding Ratio

Total Deposits over Total Funding R$ million R$ billion

5,908 6,859 6,270 5,925 5,692

Asset and Liability Management (ALM)

66%69% 70% 70%

76%

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

6.0x5.6x 5.4x 5.4x 5.6x

3.9x 3.7x 3.6x 3.6x 3.8x

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.0 0

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Expanded loan Porfolio

Loan Portfolio excludingBank Guarantees

1.1

0.7

5.0

0.00.7

0.6

Assets

0.1

0.4

3.8

2.7

0.40.7

Liabilities

8.2 8.2

Coverage of 131%

Cash and cash equivalents

Assets financed through REPOs

Other assets

Credit Portfolio

Trading portfolio assets

Illiquid assets

Secured funding

Other liabilities

Unsecured funding

Demand deposits

Equity

REPO Financing

32/37 Investor Relations | 4Q16 |

Capital Adequacy Ratio (BIS), Basel III

BIS ratio of 15.4%, being 15.0% in Tier I Capital.

14.1% 14.7% 15.4% 15.3% 15.0%

0.9% 0.4%0.5% 0.5% 0.4%

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Tier II Tier IMinimum Regulatory Capital (10.5%)

15.0% 15.1%15.9% 15.8% 15.4%

33/37 Investor Relations | 4Q16 |

Rating

Foreig

n

an

d L

ocal

Cu

rren

cy

Long Term B+ BB- B1 -

Nati

on

al

Long Term BBB- A Baa2 9.09

34/37 Investor Relations | 4Q16 |

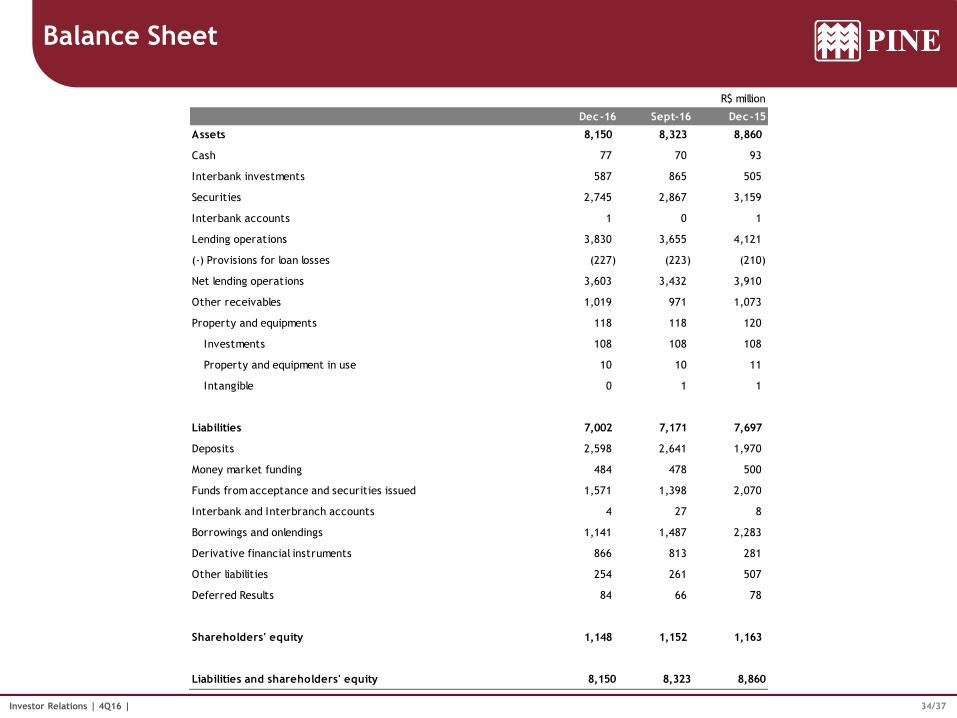

Balance Sheet

R$ million

Dec-16 Sept-16 Dec-15

Assets 8,150 8,323 8,860

Cash 77 70 93

Interbank investments 587 865 505

Securities 2,745 2,867 3,159

Interbank accounts 1 0 1

Lending operations 3,830 3,655 4,121

(-) Provisions for loan losses (227) (223) (210)

Net lending operations 3,603 3,432 3,910

Other receivables 1,019 971 1,073

Property and equipments 118 118 120

Investments 108 108 108

Property and equipment in use 10 10 11

Intangible 0 1 1

Liabilities 7,002 7,171 7,697

Deposits 2,598 2,641 1,970

Money market funding 484 478 500

Funds from acceptance and securities issued 1,571 1,398 2,070

Interbank and Interbranch accounts 4 27 8

Borrowings and onlendings 1,141 1,487 2,283

Derivative financial instruments 866 813 281

Other liabilities 254 261 507

Deferred Results 84 66 78

Shareholders' equity 1,148 1,152 1,163

Liabilities and shareholders' equity 8,150 8,323 8,860

35/37 Investor Relations | 4Q16 |

Managerial Income Statement

(overhedge effect and provisions reclassified)

R$ million

4Q16 3Q16 4Q15 2016 2015

Income from financial intermediation 208 236 215 609 1,785

Lending transactions 101 116 146 453 701

Securities transactions 76 99 93 331 325

Derivative financial instruments 15 12 (18) (112) 691

Foreign exchange transactions 15 10 (7) (63) 68

Expenses with financial intermediation (205) (224) (183) (590) (1,693)

Funding transactions (163) (180) (163) (554) (876)

Borrowings and onlendings (32) (26) 6 52 (638)

Provision for loan losses (11) (17) (26) (88) (180)

Gross income from financial intermediation 3 13 32 19 92

Other operating (expenses) income (19) (25) (37) (90) (158)

Fee income 22 19 18 72 90

Personnel expenses (22) (21) (23) (85) (89)

Other administrative expenses (18) (17) (19) (67) (74)

Tax expenses (4) (3) (6) (19) (23)

Other operating income 8 3 2 36 16

Other operating expenses (5) (6) (7) (29) (78)

Operating income (16) (12) (5) (72) (66)

Non-operating income 4 3 3 19 8

Income before taxes and profit sharing (12) (10) (2) (53) (59)

Income tax and social contribution 6 7 22 53 133

Profit sharing (4) (4) (9) (15) (33)

Net income (9) (7) 10 (14) 41

36/37 Investor Relations | 4Q16 |

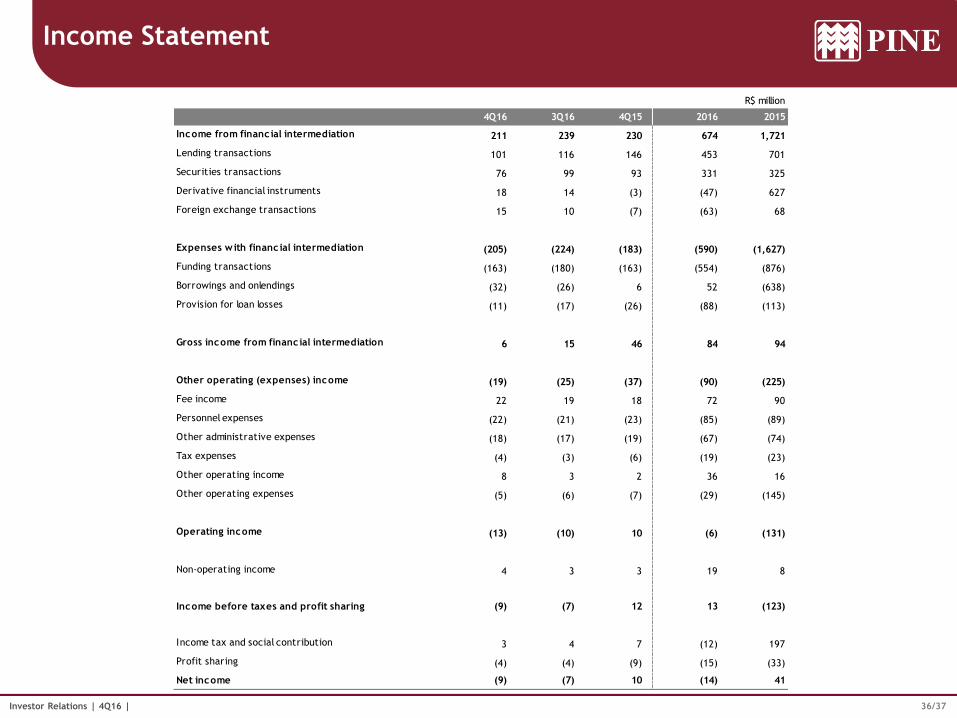

Income Statement

R$ million

4Q16 3Q16 4Q15 2016 2015

Income from financial intermediation 211 239 230 674 1,721

Lending transactions 101 116 146 453 701

Securities transactions 76 99 93 331 325

Derivative financial instruments 18 14 (3) (47) 627

Foreign exchange transactions 15 10 (7) (63) 68

Expenses with financial intermediation (205) (224) (183) (590) (1,627)

Funding transactions (163) (180) (163) (554) (876)

Borrowings and onlendings (32) (26) 6 52 (638)

Provision for loan losses (11) (17) (26) (88) (113)

Gross income from financial intermediation 6 15 46 84 94

Other operating (expenses) income (19) (25) (37) (90) (225)

Fee income 22 19 18 72 90

Personnel expenses (22) (21) (23) (85) (89)

Other administrative expenses (18) (17) (19) (67) (74)

Tax expenses (4) (3) (6) (19) (23)

Other operating income 8 3 2 36 16

Other operating expenses (5) (6) (7) (29) (145)

Operating income (13) (10) 10 (6) (131)

Non-operating income 4 3 3 19 8

Income before taxes and profit sharing (9) (7) 12 13 (123)

Income tax and social contribution 3 4 7 (12) 197

Profit sharing (4) (4) (9) (15) (33)

Net income (9) (7) 10 (14) 41

37/37 Investor Relations | 4Q16 |

This report may contain forward-looking statements concerning the business prospects, projections of operating and financial results and growth outlook of PINE. These are merely projections and as such

are based solely on management’s expectations regarding the future of the business. These statements depend substantially on market conditions, the performance of the sector and the Brazilian economy

(political and economic changes, volatility in interest and exchange rates, technological changes, inflation, financial disintermediation, competitive pressures on products and prices and changes in tax

legislation) and therefore are subject to change without prior notice.

Investor Relations

Norberto Zaiet Junior

CEO

João Brito

CFO

Raquel Varela Bastos

Head of Investor Relations, Local Funding and Communication

Luiz Maximo

Investor Relations Coordinator

Kianne Paganini

Investor Relations Analyst

Phone: (55 11) 3372-5343

ir.pine.com