Embed Size (px)

Citation preview

2014 results

Overview

• Outlook 2015

• Portfolio realignment

• Business review 2014

• Financial review 2014

• Questions

2

Umicore expects profitability to improve in 2015

Recycling Energy Materials Catalysis Performance Materials

Supply conditions are

anticipated to be

broadly similar to

2014. The expected

downtime due to the

expansion investments

in Hoboken should be

compensated by an

increased underlying

throughput

Revenues and

profitability are set to

increase further

reflecting the

contribution of recently

acquired activities as

well as demand growth

in all business units

The ramp-up of Heavy

Duty Diesel (HDD)

catalyst production in

Europe and China and

further growth in

demand for emission

abatement for light

duty vehicles should

drive revenues and

earnings higher for

Catalysis in 2015

Revenues are expected

to grow broadly in line

with GDP

3

Portfolio realignment

• Preparations underway for eventual divestment of Zinc Chemicals & Building Products:

• significant improvement of overall performance and recent investments placing them in a strong position

• better growth opportunities in an environment that is more aligned with their respective products, services and applications

• Looking for opportunities to accelerate growth in Electro-Optic Materials & Thin Film Products through alliances or strategic partnerships

• Intention to implement portfolio realignment by the end of 2016, subject to market opportunities

4

Businessreview2014

Catalysis

Revenues up 6% and recurring EBIT up 13%:

• Increases in Automotive Catalysts:

• ramp-up of HDD catalyst production in Europe and China

• Higher revenues for LDV catalysts, despite unsupportive mix

• Volume growth in line with global market

• Unsupportive mix in Europe and North-America

• Outperforming the growing Chinese market

• Lower order levels and earnings in Precious Metals Chemistry

H1 H2

399

275 33

9

391 45

3

453

467

314

311 35

9 424

407

414

45071

2

586 69

9 814

860

867

917

0

200

400

600

800

1,000

1,200

2

008

2

009

2

010

2

011

2

012

2

013

2

014

Revenues (excluding metal)(in million €)

57

-14

39

46 49 44 41

7

17

39

44 42

29

41

64

31

78

89 91

73

83

-20

0

20

40

60

80

100

120

Recurring EBIT

6

Catalysis

Nowa Ruda: H1 2016

New production facility

Hemaraj: H2 2016

New production facility

Incheon: H2 2015

New technology development center

Suzhou: H1 2014

New production capabilitiesfor HDD operational

Tulsa: H1 2014

New plant commissioned

Florange: H2 2014

Third SCR line for HDD operational

Precious Metals Chemistry

Automotive Catalysts

Pune: H2 2014

New plant commissioned

Hanau: H2 2014

Capacity expansion for metal deposition commissioned

7

Energy Materials

Revenues up 11% and recurring EBIT up 59%:

• Integration of recent acquisitions in Cobalt and Specialty Materials and higher sales volumes in ceramics & chemicals

• Strong volume growth in Rechargeable Battery Materials, mainly driven by demand for high-end portable electronics

• Higher sales volumes in Electro-Optic Materials and Thin Film Products

H1 H2

205

154

173

180

184

200 22

3

190

151 17

4

178

183 20

3 222

395

305 34

8

358

366 40

3 445

0

100

200

300

400

500

2

008

2

009

2

010

2

011

2

012

2

013

2

014

Revenues (excluding metal)(in million €)

36

7

24 21

14 12

20

21

17

20 20

4 13

20

57

24

44 41

18

25

39

0

20

40

60

80

Recurring EBIT

8

Energy Materials

Cheonan and Jiangmen: 2014

Production capacity expansions completed

Wickliffe: H2 2014

Acquisition of CP Chemicals

Rechargeable Battery Materials

Cobalt & Specialty Materials

Thin Film Products

Monza: 1 January 2015

Full ownership of Todini and Co

Qingyuan: H1 2014

JV with First Rare Materials

Olen: 2015

Expansion for Co fine powders

9

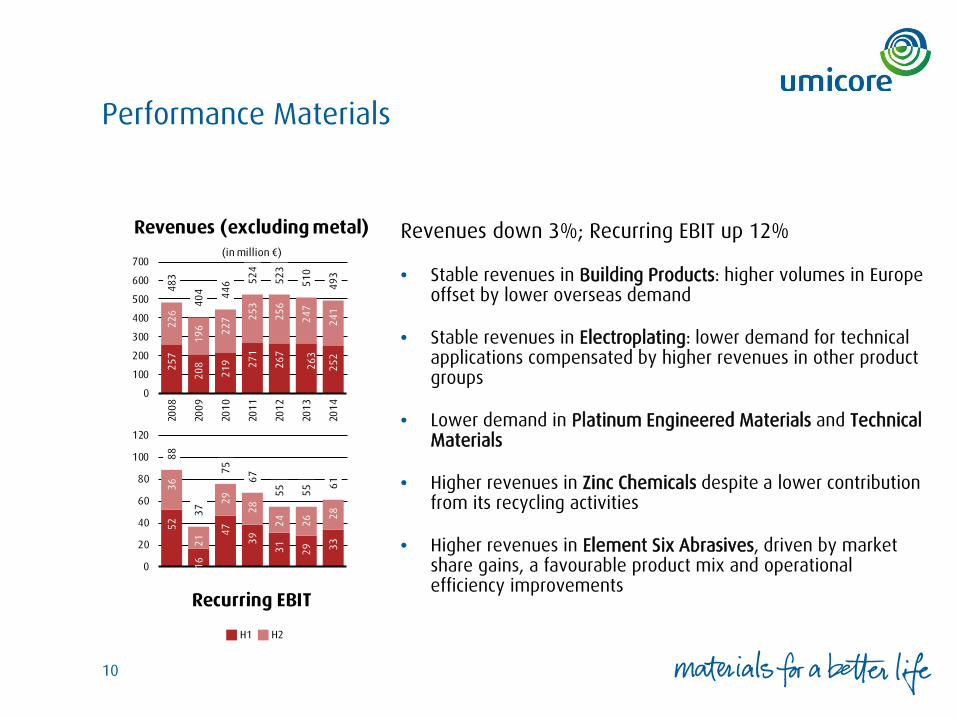

Performance Materials

Revenues down 3%; Recurring EBIT up 12%

• Stable revenues in Building Products: higher volumes in Europe offset by lower overseas demand

• Stable revenues in Electroplating: lower demand for technical applications compensated by higher revenues in other product groups

• Lower demand in Platinum Engineered Materials and Technical Materials

• Higher revenues in Zinc Chemicals despite a lower contribution from its recycling activities

• Higher revenues in Element Six Abrasives, driven by market share gains, a favourable product mix and operational efficiency improvements

H1 H2

257

208

219 27

1

267

263

252

226

196 22

7 253

256

247

241

483

404 44

6 524

523

510

493

0

100

200

300

400

500

600

700

2

008

2

009

2

010

2

011

2

012

2

013

2

014

Revenues (excluding metal)(in million €)

52

16

47

39

31 29 33

36

21

29

28

24 26

28

88

37

75

67

55 55

61

0

20

40

60

80

100

120

Recurring EBIT

10

Performance Materials

Pasir Gudang: H1 2014

Capacity expansion to serve Asia-Pacific completed

Changsha: H1 2015

New plant for Zn powders

Viviez: H1 2014

New plant for surface-treated products

commissioned

Electroplating

Zinc Chemicals

Building Products

Jiangmen : H1 2014

JV with JCX

11

12

Recycling

Revenues down 10% and recurring EBIT down 30% due to lower metal prices; ROCE at 40%

In Precious Metals Refining:

• Lower metal prices

• Robust availability of supply volumes although overall mix not as supportive

• Higher processed volumes after the first phase of expansion

Lower contribution from the recycling activities in Jewellery & Industrial Metals

Less favourable conditions for Precious Metals Management

H1 H2

95

66

102 13

3

122

103

68

106

52

93

134

137

97

71

202

118

195

267

259

200

139

0

50

100

150

200

250

300

350

Recurring EBIT

253

222

254 31

0

342

307

268

255

204 25

2 327 339

283

265

508

427 50

6 637 681

590

533

0

200

400

600

800

1,000

2

008

2

009

2

010

2

011

2

012

2

013

2

014

Revenues (excluding metal)(in million €)

12

Recycling

Pforzheim: H2 2014

Expansion of Ag recycling

Hoboken

1. 2nd phase of sampling facility expansion H1 20142. Commissioning of biological water treatment H1 20143. Expansion of capacity by 40% 2014 - 2016

Bangkok: 2014 - 2015

Ongoing expansion of Agrecycling

Precious Metals Refining

Jewellery & Industrial Metals

Manaus: H1 2014

Expansion of Ag recycling

13

Employees and Safety

Total number of employees increased by 17

• Increase in fully consolidated companies primarily in Catalysis and Energy Materials

• Decrease in associated companies mainly in the JV’s of Energy Materials and following the restructuring in Element Six Abrasives

Safety performance

• Two fatalities in January 2014

• Accident frequency rate at 2.16

• 84% of sites accident-free

In addition to existing safety initiatives, a process safety program has been launched

9.89

5

9.82

8

9.05

3

9.82

6

10.0

79

9.31

5

9.55

8

10.1

64

10.3

96

10.1

90

10.3

68

4.13

1

4.31

4

4.87

9

5.01

8

5.33

4

4.40

5

4.82

8

4.40

8

4.04

2

3.86

7

3.70

6

14.0

26

14.1

42

13.9

32

14.8

44

15.4

13

13.7

20

14.3

86

14.5

72

14.4

38

14.0

57

14.0

74

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

2

004

2

005

2

006

2

007

2

008

2

009

2

010

2

011

2

012

2

013

2

014

Fully consolidated Associates

People

14

2014 financials

Profitability impacted by lower Recycling margins

Recurring EBITDA down 4%

• Lower metal prices affecting Recycling margins

• Recurring EBITDA up in Catalysis, Energy Materials and Performance Materials

• Currency headwinds

Recurring EBIT down 10%

• Higher depreciation charges linked to the recent growth investments

ROCE at 12.2%

H1 H2

Restated in 2004, 2006 and 2008 for discontinued operations in following year

218

188 22

4 255

269

107

247 28

1

266

240

221

208

184 21

0 216

198

156

222 27

2

258

222

221

426

372 43

4 471

467

263

469 55

3

524

463

442

0

100

200

300

400

500

600

700

2

004

2

005

2

006

2

007

2

008

2

009

2

010

2

011

2

012

2

013

2

014

Recurring EBITDA(in million €)

155

122 17

0 199

215

50

186 21

5

192

163

138

126

111

159 16

0

140

97

156

202

181

141

135

280

233

329 35

9

355

146

343

416

372

304

274

0

100

200

300

400

500

Recurring EBIT

16

Resilient free cashflows

Further reduction of working capital

Operating cashflow at € 403 million

Substantial growth investments

• Capex of € 202m

• Acquisitions in Energy Materials

Net cashflow before financing at € 140 million

429

254

398

598

475

441

403

17

202

-247

-49

34

97

56

-300

-200

-100

0

100

200

300

400

500

600

700

2

008

2

009

2

010

2

011

2

012

2

013

2

014

Operatingcashflow

Workingcapitalchanges

Operating cashflow(in million €)

* Operating cashflow = cashflow generated from operations less change in working capital requirement plus dividend and grants received

17

Expenditures for growth

Capex € 202 million including significant growth projects:

• First phase of investments completed to expand capacity in Hoboken

• Ongoing expansions in Catalysis and Energy Materials

Acquisitions in Energy Materials: € 35 million

• CP Chemicals

• Todini and Co

R&D expenditures slightly up to € 143 million (6 % of revenues) with higher spending in Energy Materials and Recycling

216

190

172

213 23

6

280

202

1

11

22

35

0

50

100

150

200

250

300

350

2

008

2

009

2

010

2

011

2

012

2

013

2

014

Capex Acquisition of new subsidiaries

Capex & acquisitions(in million €)

18

Cash returns to shareholders

Stable dividend proposed at € 1.00 per share

Corresponds to 56% payout ratio based onrecurring EPS of € 1.79 per share

Purchased 2 million treasury shares in 2014, amounting to € 72 million

Total cash returned to shareholders (dividend + buybacks) of € 187 million or 43% of cashflowgenerated by operations

Cancellation of 8 million shares in September 2014

1.41

1.21

1.73 1.

80 1.93

1.24

1.40

2.69

2.47

1.96

1.79

0.33

0.37

0.42

0.65

0.65

0.65 0.

80

1.00

1.00

1.00

1.00

23%

31%

24%

36%34%

52%57%

37%41%

51%

56%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0.50

1.00

1.50

2.00

2.50

3.00

2

004

2

005

2

006

2

007

2

008

2

009

2

010

2

011

2

012

2

013

2

014

Recurring EPS Dividend Payout ratio

Data per share(in € / share)

Restated for discontinued operations in 2004, 2006 and 2008* Dividend proposed for 2014

19

Net financial debt

Net debt31/122013

Operatingcashflow

Workingcapital

changes

CapexDev Cap

Netacquisitions/ disposals

Taxes Netinterest

Dividends

Sharebuybacks Other

Net debt31/122014

-215

403

56 -202

-13 -58

-57

-3 -115

-64

-31

-298

-300

-250

-200

-150

-100

-50

0

50

100

150

200

250

300(in million €)

Net financial debt evolution

* Operating cashflow = cashflow generated from operations less change in working capital requirement plus dividend and grants received

20

Capital structure remains strong

585

515

813

140

333

177

360

267

222

215 29

8

31% 34

%

45%

10%

20%

11% 19

%

13%

11%

11%

15%

1.6

1.3

1.7

1.1

0.8

1.0

0.5 0.

6

0.5

0.4 0.

5

0

250

500

750

1,000

1,250

1,500

2

004

2

005

2

006

2

007

2

008

2

009

2

010

2

011

2

012

2

013

2

014

Net financial debt Gearing ratio (debt / debt+equity)

Average net debt / recurring EBITDA

Net financial debt

Restated for discontinued operations in 2004, 2006 and 2008

(in million €)

Net financial debt € 298 million

Corresponds to :

• 0.5 x Average net debt to recurring EBITDA ratio

• 15 % net gearing ratio

Average weighted net interest rate down to 1.56 %

21

Non-recurring elements

Non-recurring EBIT of € -22 million

Total negative impact on net result of€ 23 million

Non-recurring items (in million €) 2014

Restructuring charges & provisions (20.1) Environmental charges & provisions (7.1) Impairments on metal inventory 8.2 Other (2.6)

Non-recurring EBIT (21.6)

Non-recurring tax result 1.4 Non-recurring minority result 0.1

Net non-recurring result (21.8)

Net IAS 39 effect (0.7)

Total impact on net result (22.5)

22

Wrap-up

• 2014 earnings fully in line with guidance

• Long term growth investments on track

• Positive outlook for 2015

• Portfolio realignment process underway

23

Q&A

Financial calendar

28 April 2015 Annual General Meeting

30 April 2015 Ex-dividend trading date

4 May 2015 Record date for dividend

5 May 2015 Payment date for dividend

31 July 2015 Half Year Results 2015

2 September 2015 Capital Markets Day - London

22 October 2015 2015 third quarter trading update

Forward-looking statements

This presentation contains forward-looking information that involves risks and uncertainties, including statements about Umicore’s plans, objectives, expectations and intentions.

Readers are cautioned that forward-looking statements include known and unknown risks and are subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the control of Umicore.

Should one or more of these risks, uncertainties or contingencies materialize, or should any underlying assumptions prove incorrect, actual results could vary materially from those anticipated, expected, estimated or projected.

As a result, neither Umicore nor any other person assumes any responsibility for the accuracy of these forward-looking statements.

25