Embed Size (px)

Citation preview

News business in the age of platformsHow to respond strategically to digital disruption

Vincent Peyregne CEO WAN-IFRA, the World Association of News Publishers@vincentpeyregne

!"#$%&"'!"#$%&'()%$#*+(,-.(/%0$.)+$1

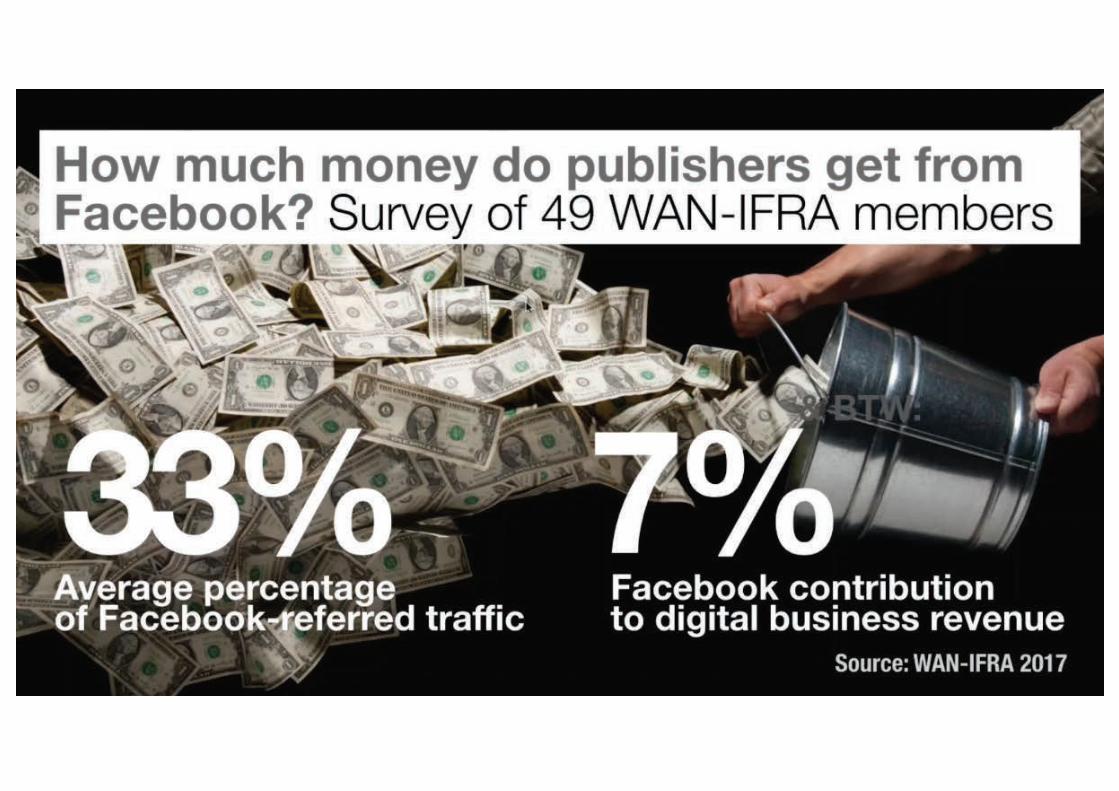

WAN-IFRA members can download the report here

wan-ifra.org/facebook_report

credit

Grzegorz PiechotaSenior research Fellow Green Templeton College & Reuters Institute, University of OxfordResearch Associate, Harvard Business School. Former news editor, Gazeta Wyborcza, Poland. Author of “Reality Check – making Money with Facebook”, WAN-IFRA 2017

OUR CONVERSATION

TODAY

vincentpeyregne

Publishersneed to have a strategywithplatform

Analysingpublishersbusiness model worldwide: 4 typicalapproaches

How publishersare takingdecisions

A Decade in the Driver’s Seat

Platforms have become the new mass mediaTopnetworksbymilionsofactivemonthlyusers

Source: Statista 2017, Company data 2017

1

2

3

4

5

6

7

8

9

10

1 860

1 200

4

1 200

Messenger

1 000877

846

600

550

500317

1 1 860

2

3

1 2002

3 11 200

MessengerMessenger 7 600

Publisher’scontentdrivesdailynewsconsumption,engagementonplatforms

Sources: Crowdynews, PEW Internet 2016

62%U.S. adults

got their newslast week on social

media

62%U.S. adults

got their newslast week on social last week on social

media

FAST FORWARD… in 2017 Google is sending more traffic than Facebook to publishers

Source Parse.ly from some2,500 publishers that use its analytics service, 2017

Winners of the attention economyaggregate largest audiences & capture

most of ad revenue

71% USA combined share in 2016

89% their share in new ad spend

2+3$!#45678/9:;75<=8>597?5

Who else captures $ in digital ad ecosystem?

Source: AEMII / Future Media Lab / European Magazine Media Association 2016

$1$0.10

$0.05

$0.15$0.12

$0.15$0.14

$0.29

Advertiser Agency Trading Desk DMP/Data provider

DSP Ad exchange SSP/Ad network

Publisher

companiesShare of ad tech 61%

Average monthlyrevenue

Source: Digital Content Next 2017

What’s the distributed content revenue?Benchmark 17 top U.S. publishers in 1H 2016

Share of paymentsin average total platform revenue

$1.3m60%

platform advertising revenue share +syndication + production fees

of paymentsin average total platform

$27.6bn / 50mFacebook’s ad revenue in2016

Let’s imagine Facebook shares it all

Pagepublishers

Source: Facebook 2017

= $552

What do publishers think and do with platforms?

1st wave of disruption: unbundling

News sites

Opinionsites

Niche verticals (around topics,

personalities, communities)

User generated content(blogs, boards)

Brand websites (product, service pages)

Marketplaces

… unbundling of individual stories

Headline of an article

Visual elements:e.g. picture,

video, graphics

Complements:e.g. comments,

reactions

Text of an article

Text elements:e.g. captions, sidebars

Recommended:e.g. related, earlier, similar stories

erodingValueeroding

Value Valueeroding

Value Valuecreating eroding

Forc

onsu

mer

Noticeads

Consume content

Visit a website Search/ an app for content

Choosemedium / brand

Forp

ublis

her

Value creating

Value creating

Value capturing

Decoupling Platforms, ad-blockers letconsumers avoid value eroding activities or minimise pains

XXXX

Strategic response?

Advocate on the regulatory framework?

Launch your own platforms?Form alliances on data,

technology, single user

sign-in?

Take for granted thatplatforms are not goingaway

Without reach,data & zero costcontent, it’s hard to competedirectly.

Consumers are not going to start loving displayads

1

2

What about chargingother parties

for content itself?

Who pays for digital content at the NY Times?

Consumers

Content marketeers

Retailers

Donors

Syndication

How much money may the Times make?

digital-onlysubscriptions (2016)

branded content (est)affiliatedmarketing (est)

donors (est)

Source: NYT Company, Q4 2016; estimates Greg Piechota based on data reported in trade press

syndication, events, e-commerce (est)

<$60m <$10m >$5m

$232m $77m

Platforms become fishing ponds for customers and expand reach of branded content campaigns

Design the new content portfolio

Optimised foracquisition, retention, upgrade

Contentwith differentbusiness models attached

Evaluation

Awareness & Trial on & off-platform

ContributionReferral

Repeated useon & off-platform

Customer’s need & attention Purchase

Loyalty

Consideration of the paid offer

Use continued on & off-platform

Visitor Subscriber

Customer journeys strongly influenced by newuser behaviour

How come the airlineindustry make record profits at a time when seatmargins are dwindlingthe grand vision of airlines as omni-channelretailers - Ancillary Revenue represents a 264% increase from the 2010

Source: IdeaWorksCompany 2017

Media are becoming shoppable and retailers media companies

How come majorsupermarket chains losemoney on actual sale ofgoods?

How come music revenue grows as digital downloads and CDs fadeStreaming grows and Live music thrives

Total revenue of the music industry USD Million source LSE

Platformsare not yourfriends,

nor enemiesHire them to work for you

Develop a platform strategy

What’s your business model?What’s your end game

on platforms

If you want to chase reachGo Beyond National Boarders

Go Beyond NewsGo Viral

If you accept that you are not mass media anymoreForget about Chasing Reach

Explore your Niche CommunitiesGrow ARPU

Source: GrzegorzPiechota based on NYT financial report

Data is keyBuild your own analytics

capability NOW

Make Better DecisionsTest Value vs. Viability

Customer vs. Business Value First and Foremost

Alignment with Brand & StrategyNot all Platforms Play the same Role

Calculate collateral costsDocumented Process

Guiding Principles A PRELIMINARY CHECK LIST

Ingestible cross-platform user dataPublishers need the platforms to do more to connect user activities across platforms and the publishers’ to understand path to engagement

Direct relationship with the customerPublishers need ownership of the relationship with the customer, including contact data, pricing, bundling, customer experience, customer support

Business drivers: branding, promotion, pricing, paywallControl over branding and promotion, messaging, pricing of the publisher’s bundles, levers that drive the business.

14 web properties35,4 M Unique Visitors 80% market reachRanks #4 after Google Facebook and Microsoft

44 Mio.unique users in Germany

85% of eComerce users

Many fragmented Domestic solutionsdo not reach the critical mass

Amazon portfolio DE First isolated single sign-in German Initiatives

vs. eCommerce

automotive

food retailer

media

logistics

mobile communications

44 Mio.unique users in Germanyunique users in Germanyunique users

85% of eComerce users

Many fragmented Domestic solutionsdo not reach the critical mass

Amazon portfolio DE First isolated single sign-in German Initiatives

vs.vs.vs. eCommerce

automotive

food retailer

media

logistics

mobile communications

vs.

vs.

vs.

vs.

vs.

Dominant global players use of central user accounts to harness their market reach

Amazon account Google-id Apple id Facebook-id Alibaba-id

237702 500

11 228

231237 300

22 482

500800

2281

22811 591

4070

750

1500

2250

3000

Amazon Google Apple Facebook Alibaba

+27%

+60%+64%

+30%

+254%

Amazon account for e-commerce. Cross industries

ID for access, identification, authorization of specific services

ID for access and authentification with a large numbers of other service providers

All-in-One account used to log in many Apple Inc. online services

Alibaba ID for e-commerce proviseur (BtoB, BtoC, CtoC), sales services, e-payment, search-engine, Cloud services

active global users (millions)

THE POWER OF MANYRethink your Alliances

….NEWS ….TV

….BLOGS

….TV ….NICHE

….NEWS

2+3$!#52*$+@@&#

MORE WAN-IFRA REPORTS wan-ifra.org/reports

MORE MARKET INSIGHTS blogs.wan-ifra.org

QUESTIONS ?Vincent PeyrègneCEO, [email protected]

vincentpeyregnevincent.peyregne@wan