Embed Size (px)

Citation preview

Industry Project-Healthcare

Group 9

Wasim, Abinandan, Hari, Ayushi 3/26/14

1

Index

S No Topic Page

Number

1

INDUSTRY OVERVIEW

2

2

INDUSTRY SIZE

4

3

TRENDS AND INVESTMENT

6

4

IMPACT OF BUDGET ON HEALTHCARE INDUSTRY

7

5

CONTRIBUTION TO INDIAN GDP

9

6

INFRASTRUCTURE

10

7

HEALTH INSURANCE INDUSTRY

11

8

HOSPITALS

13

9

PHARMACEUTICAL INDUSTRY

17

10

FUTURE TRENDS IN HEALTHCARE INDUSTRY

20

11

CHALLENGES

21

12

OPPORTUNITIES

22

13

CONCLUSION

25

2

Industry Overview:

The health care industry or medical industry is a combination of sectors within the economic

system that provides goods & services to treat patients. The modern healthcare industry is

divided into many sectors and depends on trained professionals to meet health needs of

individuals. The healthcare is one of the largest & fastest growing industries& contributes

10% to the GDP of most developed nations. It can form an enormous part of a country’s

economy.

The healthcare industry consists of various sub-sectors:

Hospitals

Medical Infrastructure

Medical Devices

Clinical trials

Outsourcing

Tele medicine

Health insurance &

Medical equipments

Over the past few years there has been a major change in the industry from paper files to

electronic mediums. India’s growing economy is driving urbanization & creating an

expanding middle class, with more disposable income to spend on healthcare. Another

factor which drives the growth of India’s healthcare sector isrise in both infectious & chronic

degenerative diseases. Indians in general, live more affluent lives and adopt unhealthy

western diets that are high in fat and sugar, the country is undergoing a rise in lifestyle

diseases such as diabetes, hypertension, cancer which is reaching epidemic proportions.

Over the next 5-10 years, lifestyle diseases are expected to grow at a faster rate than

infectious diseases in India, and to result in an increase in cost per treatment. India’s

healthcare infrastructure has not kept pace with the economy’s growth. The physical

infrastructure is woefully inadequate to meet today’s healthcare demands, much less

tomorrow. While India has several centers of excellence in healthcare delivery, these

facilities are limited in their ability to drive healthcare standards because of the poor

condition of the infrastructure in the vast majority of the country.

3

When it comes to healthcare, there are two India’s: the country that provides high-quality

medical care to middle-class Indians and medical tourists, and the India in which the

majority of the population live-a country whose residents have limited or no access to quality

healthcare. One of the main challenges that India faces is the lack of health insurance.

While public sector health insurance has not fared well, the market for private health plans

is expanding in India. In some cases, the government is partnering with the private sector to

provide coverage at a low cost. Clearly, there is an urgent need to expand the health

insurance net in India.

4

Industry Size:

The Indian healthcare assisted by IT market has been growing tremendously over the past

few years. It is expected to grow at a CAGR of around 22.7 per cent during the period 2013-

2015.

The hospitals and diagnostic centers in India received foreign direct investment (FDI) worth

US$ 1,914.28 million, while drugs & pharmaceuticals, medical & surgical appliances

industry registered FDI worth US$ 11,318.32 million and US$ 653.45 million, respectively

during April 2000 to June 2013, according to data provided by Department of Industrial

Policy and Promotion (DIPP).Moreso ever, the other related segments like genetic testing

market is expected to grow at a CAGR of around 9 per cent during 2012-2017 and that of

the diagnostic services market in India at a CAGR of around 26 per cent during 2012-2015.

All the growth is based on the foundation on huge investments, fast expansion into tier II &

III cities, and strong government support to strengthen the healthcare infrastructure in the

country.

5

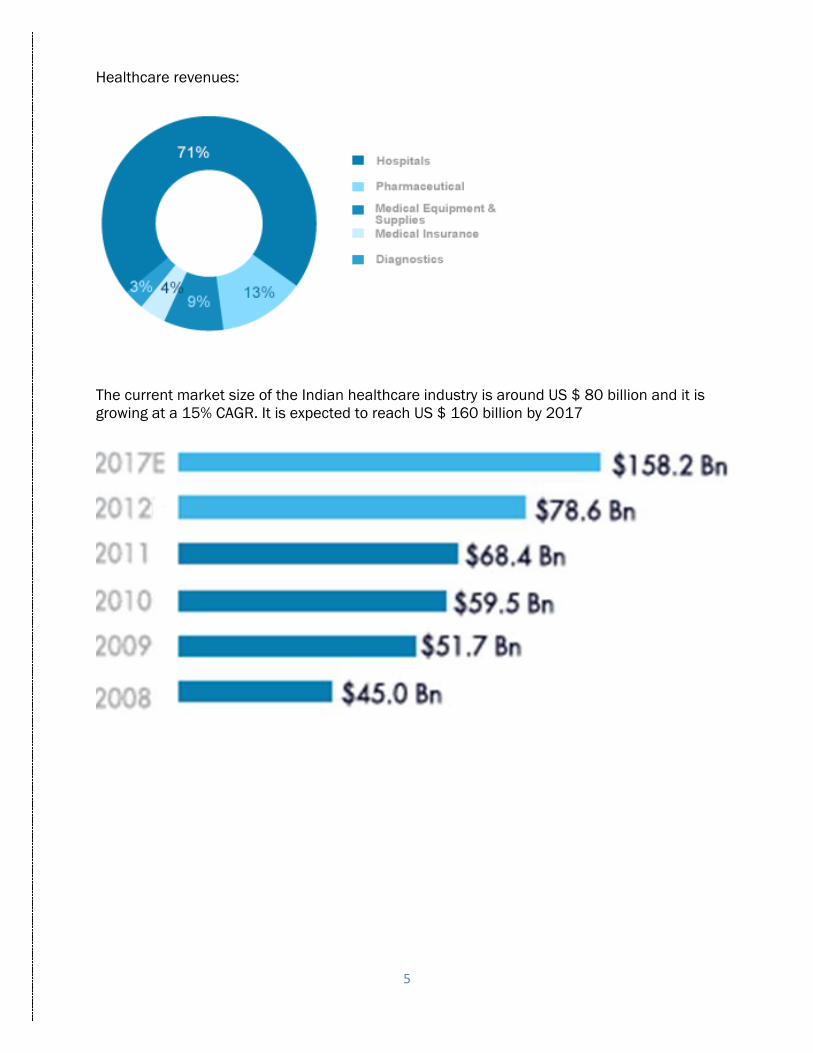

Healthcare revenues:

The current market size of the Indian healthcare industry is around US $ 80 billion and it is

growing at a 15% CAGR. It is expected to reach US $ 160 billion by 2017

6

Trends &Investments:

The Indian healthcare providers plan to spend ` 5,700 crore (US$ 897.64 million) on IT

products and services in 2013, a seven per cent rise over 2012 revenues of `5,300 crore

(US$ 834.65 million), as per a report by Gartner.

The Indian-American doctors’ community organized the "Global Healthcare Summit" in

Ahmedabad, Gujarat, from January 3-5, 2014, to bring affordable world class healthcare for

Indians. Global Healthcare Summit 2014 aims at advancing the accessibility, affordability

and quality of world-class healthcare to the Indian people. The Summit will also focus on

prevention, diagnosis, treatment options and share ways to truly improve healthcare

transcending global boundaries, as per Dr Jayesh Shah, President, Association of American

Physicians of Indian Origin (AAPI).

Some of the major investments in the sector include:

VLCC has bought controlling stake in Singapore-based Global Vantage Innovative

Group (GVig).

Apollo Hospitals has 1,500 beds capacity in the East and North East region and plans

to add another 1,500 beds. The firm plans to open four new hospitals – one each in

Kolkata, Patna, Raipur and Guwahati

Piramal’s healthcare plans to invest US$ 2.5 million at its FDA-approved Grange

mouth (UK) site to upgrade their antibody drug conjugate (ADC) manufacturing suites

ASK Pravi, a joint venture (JV) between ASK Group and Pravi Capital, has acquired a

minority stake in Hyderabad-based OMNI Hospitals for `60 crore (US$ 9.45 million)

Zydus Cadila plans to set up an injectable facility at Vadodara, Gujarat, at an

investment of `100 crore (US$ 15.75 million) by 2015. The company also plans to

expand its hospital business across Gujarat in the next three years

Dr Devi Shetty and Rudrabhishek Infrastructure Trust have entered into a JV to set up

a 300 bed multi speciality hospital worth `100 crore (US$ 15.75 million) in Lucknow,

Uttar Pradesh (UP)

CDC Group and Abraaj Group have jointly invested `107.3 crore (US$ 16.90 million)

in Hyderabad-based Rainbow Hospitals

7

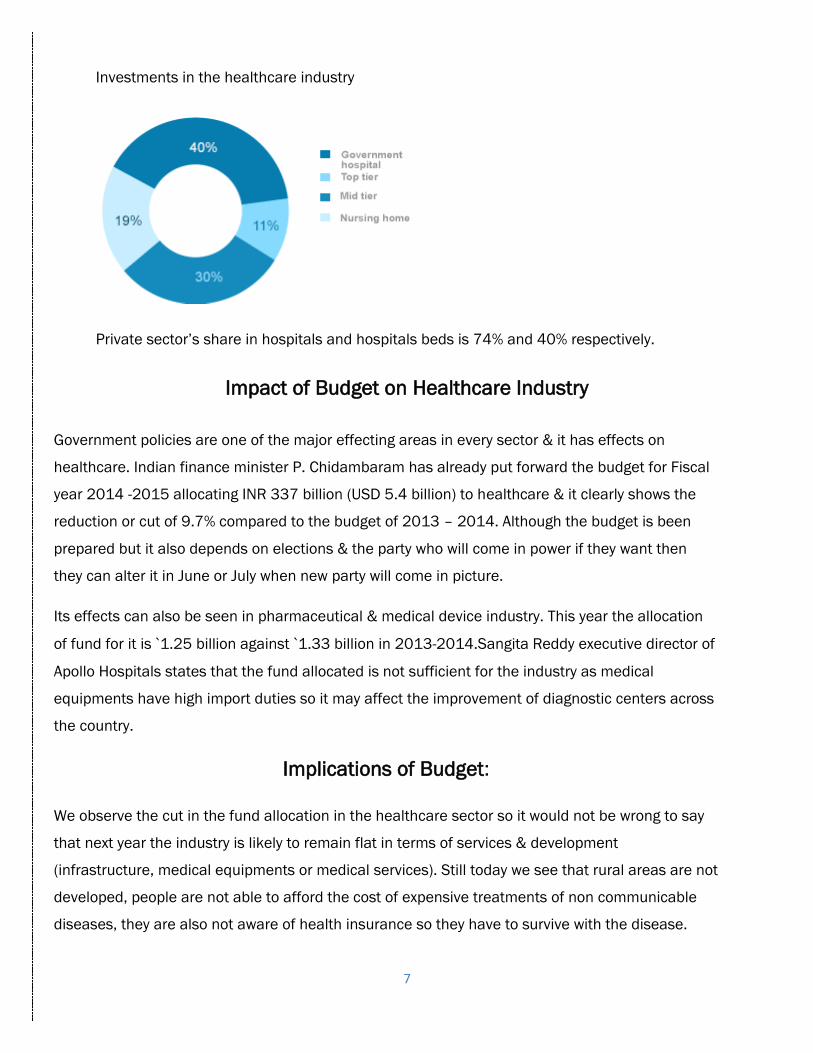

Investments in the healthcare industry

Private sector’s share in hospitals and hospitals beds is 74% and 40% respectively.

Impact of Budget on Healthcare Industry

Government policies are one of the major effecting areas in every sector & it has effects on

healthcare. Indian finance minister P. Chidambaram has already put forward the budget for Fiscal

year 2014 -2015 allocating INR 337 billion (USD 5.4 billion) to healthcare & it clearly shows the

reduction or cut of 9.7% compared to the budget of 2013 – 2014. Although the budget is been

prepared but it also depends on elections & the party who will come in power if they want then

they can alter it in June or July when new party will come in picture.

Its effects can also be seen in pharmaceutical & medical device industry. This year the allocation

of fund for it is `1.25 billion against `1.33 billion in 2013-2014.Sangita Reddy executive director of

Apollo Hospitals states that the fund allocated is not sufficient for the industry as medical

equipments have high import duties so it may affect the improvement of diagnostic centers across

the country.

Implications of Budget:

We observe the cut in the fund allocation in the healthcare sector so it would not be wrong to say

that next year the industry is likely to remain flat in terms of services & development

(infrastructure, medical equipments or medical services). Still today we see that rural areas are not

developed, people are not able to afford the cost of expensive treatments of non communicable

diseases, they are also not aware of health insurance so they have to survive with the disease.

8

Instead of these facts & falls in the budget still the government this year has not allocated the

proper funds to the industry for its improvements rather they tried to cut the expenses from it &

invest in some other sector. With funding remaining so tight it seems that government policy of

saving from pharmaceutical industry will continue.

With pharmaceutical price cuts & environment of cost saving now set to remain tight we can say

that Indian Healthcare sector will face a challenging phase until new government comes into

power & make any changes.

Government Initiatives:

The Government of India has decided to increase health expenditure to 2.5 per cent of gross

domestic product (GDP) by the end of the Twelfth Five Year Plan (2012-17). Dr Manmohan Singh,

the Prime Minister of India, also emphasized the need for increased outlay to health sector during

the Twelfth Five Year Plan. Moreover, 100 per cent FDI is permitted for health and medical

services under the automatic route.

In a recent initiative, 348 essential medicines will now come under price control in India. These

currently contribute `13,033 crore (US$ 2.05 billion) to the total annual sales of `72,762 crore

(US$ 11.46 billion), according to market research firm IMS Health’s analysis.

Some highlights of the Union Budget 2013-14 presented by Mr P Chidambaram, Minister of

Finance, Government of India, for the healthcare are as follows:

Health for all remains one of the priority sectors for the Government

The Ministry of Health & Family Welfare has been allocated `37,330 crore (US$ 5.87

billion). Of this, the new National Health Mission that combines the rural mission and

the proposed urban mission will get `21,239 crore (US$ 3.35 billion), an increase of

24.3 per cent over the Revised Estimates (RE)

`4,727 crore (US$ 744.41 million) for medical education, training and research

In addition, contributions made to schemes of Central and State Governments similar to Central

Government Health Scheme, eligible for section 80D of the Income Tax Act.

9

The federal government has begun taking steps to improve rural healthcare. Among other things,

the Government launched the National Rural Health Mission 2005-2012 in April 2005. The aim of

the Mission is to provide effective healthcare to India’s rural population, with a focus on 18 states

that have low public health indicators and/or inadequate infrastructure. India’s first medical

insurance scheme for the poor was launched in the 1996-97 budget. The “Janarogya Yojana”

scheme is marketed by the four subsidiaries of GIC, and covers people between the ages of 5 and

70 for pre– and post–hospitalization expenses, for up to 30 and 60 days, respectively. The

insurance coverage costs around $122 per annum.

Contribution to Indian GDP

In India has emerged as one of the largest service sectors with estimated revenue of around $30

billion constituting 5% of GDP and offering employment to around 4 million people. By 2025,

Indian population will reach 1.4 billion with about 45% constituting urban adult (15 years+). To

cater to this demographic change, the healthcare sector will have to be about $100 billion in size

contributing nearly 8 to 10% of the then GDP. By then, the 10 large national healthcare networks

would be able to absorb 30% of the market share. The leaders in the Indian healthcare sector will

be benchmarked to international quality and efficiency standards. Opportunities According to

Investment Commission of India, the sector has witnessed a phenomenal expansion in the last 4

years growing at over 12% per annum. As per a recent CII-McKinsey report, the growth of this

sector can contribute to 6-7% of GDP and increase employment by at least 2.5 million by 2012.

The key drivers for Indian Healthcare sector are: Medical Value Travel or Medical Tourism World

class treatment and benefits at a fraction of the Cost (almost 1/10th) with no waiting time for

surgeries as compared to advanced nations like UK and US where waiting period is substantially

longer have been instrumental in a large number of foreign arrivals to access healthcare services

in India. Medical tourism market is valued to be worth over $310 million with foreign patients

coming by every year, and the market is predicted to grow to $2 billion by 2012.

Diagnostics & Pathology Services

Outsourcing of Pathology and Laboratory tests by foreign hospital chains due

to the high cost differential in India. Clinical Trials

Availability of a Huge Patient Pool

Cost advantage with testing of drugs possible at 60% of the price.

10

Health Insurance with less than 10 per cent of the population having some sort of health

insurance, the potential market for health insurance is huge. McKinsey-CII estimates the number

of potential insurable lives at 315 million with a potential of US$ 7,700 million in health insurance

premium by 2015. Telemedicine Allows even the interiors to access quality healthcare and at the

same time, significantly improves the productivity of medical personnel. Telemedicine is one such

innovative technology, which if used effectively can double the utilization of scarce human

medical personnel.

Infrastructure

As the economy is growing but there is no much development in the infrastructure of

healthcare. There are hospitals, Diagnostic centre’s which have well equipped infrastructure but

still large percentage of it is the same. Therefore it is not possible for everyone to avail the

facilities as the infrastructure is not proper especially in the rural & semi – urban areas compared

to the urban areas.

Public health facilities are also not adequate. For example India needs 74000 health centers per

million populations it is not even half the number. There are still 11 states in our country which do

not have proper drug testing centre’s and the laboratories which exist either are not well equiped

or nursing problem

Healthcare Divide:

India is divided into two: one is high-quality medical care to middle-class Indians and medical

tourists, and other is in which the majority of the population lives—a country whose residents have

limited or no access to quality care. As per the research today only 25% of total population can

take allopathic medicines rest are still dependent on Ayurvedic or homeopathy medicines.

Health care in India:

India has 48 doctors per 100,000 persons which is fewer than in developed nations

Wide urban-rural gap in the availability of medical services

Poor facilities even in large Government institutions compared to corporate hospitals (Lack

of funds, poor management, political and bureaucratic interference, lack of leadership in

medical community)

11

So there is a huge need of changing the scenario as early as we can because these drawback will

not let us come out from it.

Indian Health Insurance Industry:

What is health Insurance?

Health insurance is an insurance against the risk of incurring medical expenses among individuals.

To cover the risk there is a pre planned financial structure in terms of monthly paid premium so

that they are relaxed if any emergency is to be faced then they need not worry about the monetary

terms. According to the Health Insurance Association of America, health insurance is defined as

"coverage that provides for the payments of benefits as a result of sickness or injury. Includes

insurance for losses from accident, medical expense, disability, or accidental death and

dismemberment”.

Industry gurus always have been suggesting the best governance when the government does

not deliver a product or service, but monitors its quality and ensures that the people get the

relevant service or product through able private players. In this case, government policies are seen

to be changing and their role in healthcare is seen shifting from healthcare delivery to financing

the delivery of care. With their launch of health insurance schemes like Rashtriya Swasthya Bima

Yojna, Aroygashree and other similar schemes has tremendously improved healthcare delivery

through private players, the schemes will cover millions of BPL patients in the years to come. The

government will save billions on the capital costs and HR costs by having the private player invest

in the same.

With opening of health insurance to private players, the insurance sector is booming.

Especially with rising disposable incomes, and the highest population being the earning age group

of 15-64 years (60 per cent of population), the insurance reach is bound to grow from the present

meager two per cent to 20 per cent as estimated by industry experts. This will bring in demand for

better quality care and a dominant role of insurer on choice of healthcare units for patients in

reference to quality and professionalism.

Patients will have a lot to shop around before choosing the 'right care provider' as he will be

armed with the vital medical insurance.

12

Major Players in Health Insurance Industry:

Aviva Life Insurance

Bajaj Allianz General Insurance

Max New York Life Insurance

HSBC health Insurance

Reliance Health

TATA AIG

Some points we would like to highlight about health Insurance:

Indian healthcare insurance industry is INR 60,497 corers from 2008-2015 compounded

annual growth rate of 42.3%.

The market penetration is 3 folds higher in 2015

According to world health report 95% of Indians will face a monetary crisis so health

insurance is a required

Less than 3% of population is covered by private insurance players & 22% by the

government organizations ( Reimbursements etc)

Technology in Industry:

Let it be any industry there is always the need of technology to take it forward. Better technology is

always the promoting factor in surgeries & ambulatory services. Both of these are the demand of

time so their supply needs to be perfect. If technology is proper used then it also promotes

telemedicine which will be of great help in rural areas.

There are various drivers for the implementation of technology in the industry:

Cost Pressure

Improving the quality of clinical care

Competitive & regulatory pressures

13

Reducing medical errors & evolving physician support tools

Investments & government policies play a big role in technology because if both of these are not

balanced then it will have a direct effect on the industry in terms of investment. Healthcare is a

growing demand as these days people are more conscious about their lifestyle & related diseases

in urban areas they go for a regular routine check up for their healthcare awareness & to be saved

from future diseases.

Annual per capita spending on healthcare:

“We Spend Like Misers”

HOSPITALS IN INDIA

Apollo Hospital

Vision: “'Touch a Billion Lives”.

Mission: Healthcare of International standards within the reach of every individual. We are

committed to the achievement and maintenance of excellence in education, research and

healthcare for the benefit of humanity.

Growth in Healthcare Spectrum: The Apollo Hospitals Group is the pioneer of integrated

healthcare delivery in India. This vision led the group to earmark time and resources to

strengthen each vital cog in the process of healthcare delivery. As a result of these efforts,

the group today is in a unique position to exponentially increase its healthcare cover.

India

China

Brazil

USA

14

a. Hospitals:

Apollo Reach Hospitals

General Multi Specialty

b. Health and Lifestyle:

Apollo Life Wellness Programs

The Cradle

The Apollo Clinic

Apollo Health and Lifestyle

Nurse Station.

c. Consulting and Solution

Global Project Consultancy.

Health Street Limited

Health Hiway

Apollo Telemedicine

d. Disease Management

Breath Eazy

Dialysis Clinic

Sugar Clinic

Health Heart Program

e. Insurance

Family Health Plan ltd

Apollo Munich Health Insurance

f. Education and Research:

Apollo Hospitals Education and Research Foundation

Health Knowledge city

15

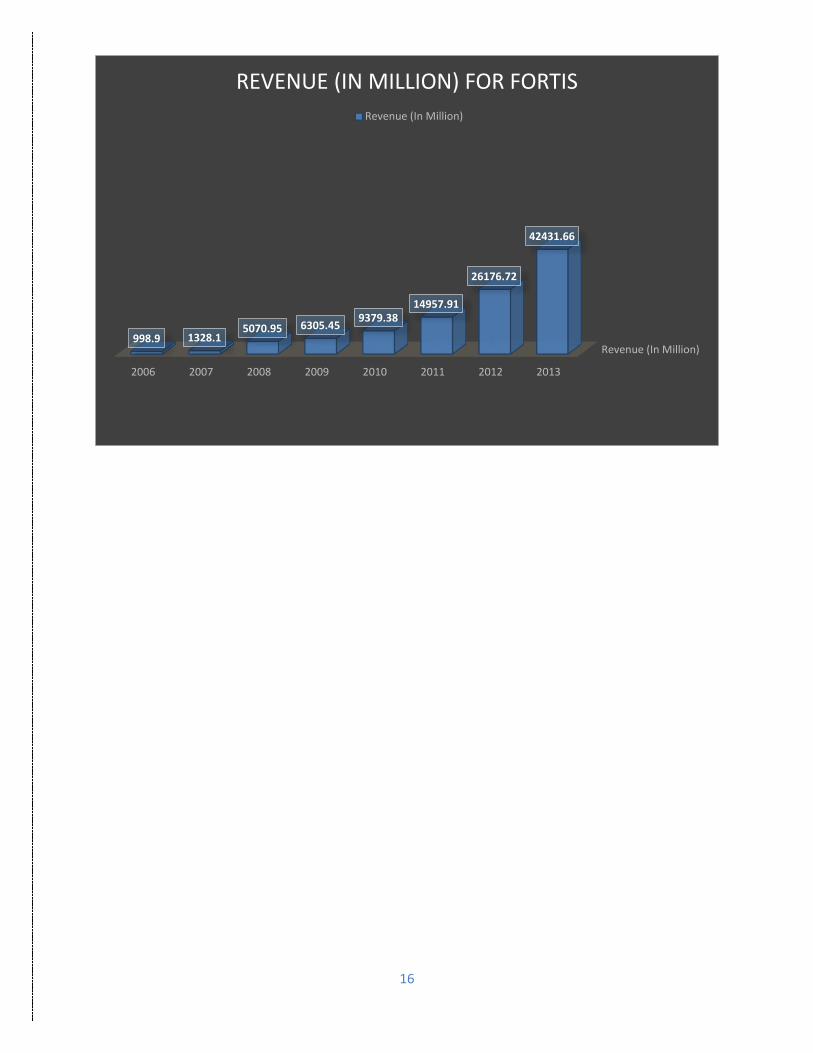

FORTIS HOSPITALS:

Fortis Healthcare Limited is a leading, pan Asia-Pacific, integrated healthcare delivery

provider.

The healthcare verticals of the company span diagnostics, primary care, day care specialty

and hospitals, with an asset base in 5 countries, many of which represent the fastest-

growing healthcare delivery markets in the world.

Currently, the company operates its healthcare delivery services in India, Singapore, Dubai,

Mauritius and Sri Lanka with 65 healthcare facilities (including projects under development),

over 10,000 potential beds, over 240 diagnostic centres and a team strength of more than

17,000 people.

Fortis Healthcare is driven by the vision of becoming a global leader in the integrated

healthcare delivery space and the larger purpose of saving and enriching lives through

clinical excellence.

Revenue (In Million)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

4485 4998 5956 7191 899511501

1480420265

2605428801

33178

APOLLO REVENUE (IN ` MILLIONS)

Revenue (In Million)

16

Revenue (In Million)

2006 2007 2008 2009 2010 2011 2012 2013

998.9 1328.15070.95 6305.45

9379.3814957.91

26176.72

42431.66

REVENUE (IN MILLION) FOR FORTIS

Revenue (In Million)

17

PHARMACEUTICAL INDUSTRY IN INDIA

Indian Pharma Industry is the third largest in terms of volume. The government started

encouraging the growth of drug manufacturing by Indian companies in the early 60s, and

with the Patents Act in 1970. Liberalization was the turning point in the history of Indian

Pharma Industry. It has the domestic market worth$12.26 billion and it holds market share

of about $14 billion is US market. There are about 4000 drug manufacturing units in India

employing approximately 3.45 lakh employees. In global market, Indian companies have

mere 1-2% share but the industry grows at a good pace about 10 % every year.

Below is the table showing top 10 Indian Pharmaceutical companies.

S. No Company Net Sales in 2013( in’bn)

1 Cipla 69.77

2 Dr.Reddy’s 66.86

3 Ranbaxy 63.03

4 Lupin 53.64

5 Aurobindo 42.84

6 Sun Pharma 40.15

7 Cadila Healthcare 31.52

8 Torrent Pharma 27.66

9 Jubilant Lifesciences 26.41

10 Wockhardt 26.50

18

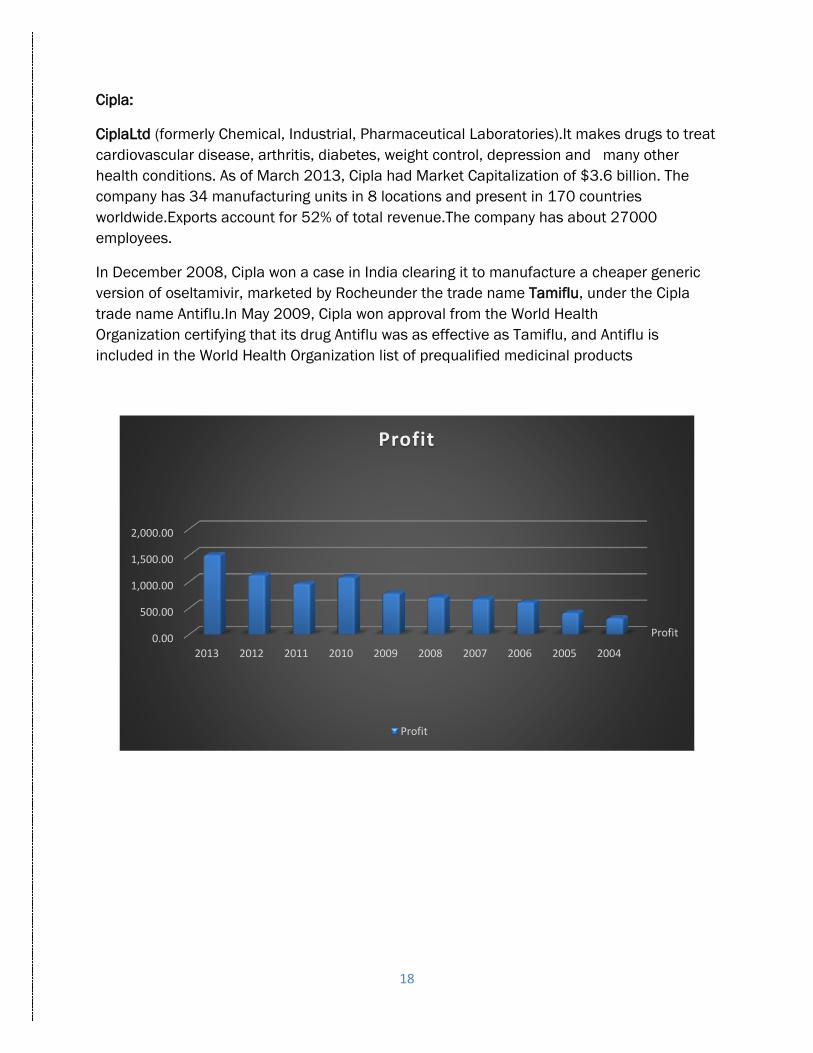

Cipla:

CiplaLtd (formerly Chemical, Industrial, Pharmaceutical Laboratories).It makes drugs to treat

cardiovascular disease, arthritis, diabetes, weight control, depression and many other

health conditions. As of March 2013, Cipla had Market Capitalization of $3.6 billion. The

company has 34 manufacturing units in 8 locations and present in 170 countries

worldwide.Exports account for 52% of total revenue.The company has about 27000

employees.

In December 2008, Cipla won a case in India clearing it to manufacture a cheaper generic

version of oseltamivir, marketed by Rocheunder the trade name Tamiflu, under the Cipla

trade name Antiflu.In May 2009, Cipla won approval from the World Health

Organization certifying that its drug Antiflu was as effective as Tamiflu, and Antiflu is

included in the World Health Organization list of prequalified medicinal products

Profit0.00

500.00

1,000.00

1,500.00

2,000.00

2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Profit

Profit

19

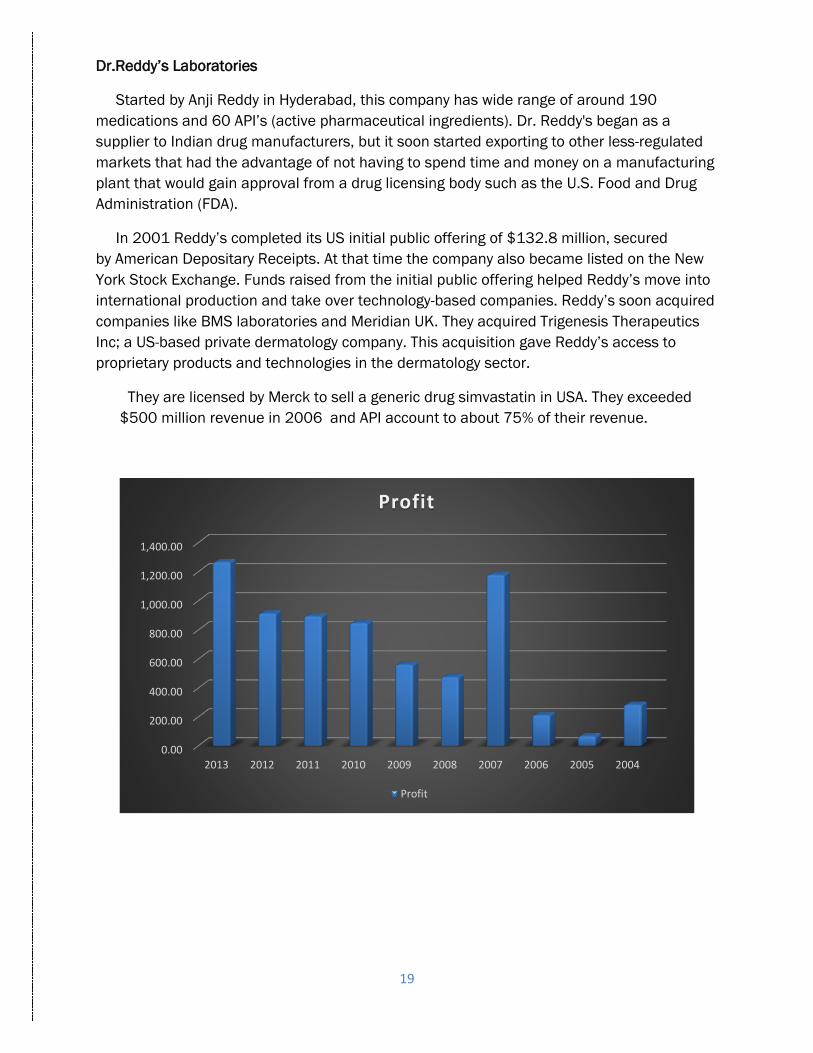

Dr.Reddy’s Laboratories

Started by Anji Reddy in Hyderabad, this company has wide range of around 190

medications and 60 API’s (active pharmaceutical ingredients). Dr. Reddy's began as a

supplier to Indian drug manufacturers, but it soon started exporting to other less-regulated

markets that had the advantage of not having to spend time and money on a manufacturing

plant that would gain approval from a drug licensing body such as the U.S. Food and Drug

Administration (FDA).

In 2001 Reddy’s completed its US initial public offering of $132.8 million, secured

by American Depositary Receipts. At that time the company also became listed on the New

York Stock Exchange. Funds raised from the initial public offering helped Reddy’s move into

international production and take over technology-based companies. Reddy’s soon acquired

companies like BMS laboratories and Meridian UK. They acquired Trigenesis Therapeutics

Inc; a US-based private dermatology company. This acquisition gave Reddy’s access to

proprietary products and technologies in the dermatology sector.

They are licensed by Merck to sell a generic drug simvastatin in USA. They exceeded

$500 million revenue in 2006 and API account to about 75% of their revenue.

0.00

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Profit

Profit

20

Future Trends in Healthcare Industry in India

According to recent studies conducted, the customer's (patient) aspirations are fast

changing. Customers are growing more aware of their health needs, demand quick

response, less waiting times, and above all - demand nearness of the healthcare unit to

them.

Customers though now demand better quality care; they however now do not want to travel

much as in earlier days.

And if you notice, the billing and pricing though important, is not a very high priority now as

insurance reach is getting stronger (to the tune of 40 per cent among patients visiting a

urban hospital).

If this is the window to the future of healthcare, then it leaves immense opportunity for

existing hospitals across the country to revamp and re-organise in order to woo back their

immediate local drainage population as the competition would heat up soon. The patients

would have a lot to choose from, now being insured.

As per various studies including a report by IDFC, and Mc Kinsey, Indian Healthcare industry

will be worth $125 billion in the next five years.

Public spending is likely to increase beyond 20 per cent, there is room for everyone in the

organized private healthcare sector.

The entities who have noted this advantage to name among the other few are Apollo and

Fortis with its cumulative market cap of around $ five billion and may be considered as a

reflection of the healthcare scenario of the present and future of Indian healthcare.

India presently has a bed deficit of approximately 30 lakh beds as per the WHO

recommendation of four beds per 1000 population. Considering even a 250 bedded

hospital on an average, the country would need 12000 hospitals in the near future. As

almost 80 per cent of this would be fulfilled by the private players, a huge rise in IPO's and

premium commanding players in the arena would flutter bringing in interesting times for the

healthcare industry.

Recent spurt in Public Private Partnership (PPP) projects, and thrust on quality by the

government sector and its demand (& mandate in some areas) on NABH and ISO, a lot of

consultancy business is abuzz with the projects galore in the accreditation and QMS field.

India to its credit already has one government hospital NABH accredited and many are in the

pipeline. With CGHS making NABH mandatory for care and hospitalization cost

reimbursements, there is hectic activity seen in hundreds of hospitals waking up to the long

due need for quality healthcare and applying for the coveted quality mark.

The trend is on a steep rise, and it is just a matter of time when the government launches

patient awareness on NABH quality in full swing. This would make the patient demand at

least an ISO QMS certified hospital if not NABH.

21

Good times ahead for healthcare consultants in every sphere be it new projects or existing.

There are various other trends observed which will be discussed in the article ahead, but

would discuss challenges and opportunities before embarking on the same which ultimately

is linked to the justification on the future trends seen.

Challenges in Indian Healthcare Industry:

The important challenges faced by Indian Healthcare Industry are

1. Inadequate human health resources.

2. Rise in non-communicable and infectious diseases especially in rural areas.

3. Access to health services is severely limited as health infrastructure is minimal.

Other challenges are:

High capital costs:

Depending on the region and real estate costs, an average hospital requires capital infusion

of `40 lakhs to a crore per bed (& even more). Industry estimates suggest that any hospital

with capital costs of more than 50 lakhs per bed has high gestation period and even may be

unviable. Land and building together account for almost 40 per cent of the total project cost

and affects the viability depending on the resulting per bed cost.

Medical equipment:

Contributing to almost 40 per cent costs in a tertiary setup, the medical equipment though

cutting edge at the time of purchase poses the threat of inevitable obsolescence within five

to seven years of setup. This problem is compounded by the fact the most of such

equipment is imported and very few local reputed manufacturers exist.

This will lead to apportioning to higher treatment costs and will further lead to lesser

competitive edges and low utilisation rates resulting in an undesired operating margins.

Human resources:

The fast-expanding domestic healthcare industry is the third largest employer, but is

severely short of manpower.

As per ministry of health, there is a shortage of approximately half a million doctors, a million

nurses and the deficit needs to be filled in the next five years. Such shortage will lead to

exponential salary hike demands, and further lead to high patient care costs.

With organized sector being the preferred choice now, there will be a huge demand even for

the skilled and quailed health administrators to run the show. Considering one skilled and

22

quailed administrator is required for every 50 employees, there would be a requirement of

almost 50000 such healthcare professionals in the near future.

Highly regulated environment and unrealistic stringent norms and restriction of entry to the

private entities in the field of medical education has led to further deficiencies in terms of

number of skilled professionals being released for intake by various hospitals.

Conventional models of business:

Rarely an out-of-the-box idea of running a healthcare business is seen. Recent niche

segments of single specialty centres (for e.g. - focused on OBGY or other specialties (Cradle

etc.) have been very few. Even in the public health sector, millions of square feet of space is

left unutilized, expensive equipment ill-maintained and lack of skilled professionals adding

to the -woe, still do not find adequate initiatives happening towards outsourcing or even

PPP.

Almost 90 per cent of private sector in India is run under the unorganized sector. The clinical

establishment bill also has faced immense opposition and a professional healthcare

consultancy firm guided healthcare business is not still seen frequently.

The conventional model would need to be broken to mitigate the presently seen long

gestation periods of five to 10 years of which almost three years are spent in project

conceptualization to commissioning.

The conventional model of healthcare business would need to change to bring in untapped

opportunities, operational efficiencies and better profitability. This would also attract better

private equity which is now diverted to more lucrative industries.

In the public healthcare sector the infrastructure is provided based on the size of the

population instead of epidemiological profile. This many time results in under-utilization of

infrastructure, and ultimately not meeting the demands of the local population and

drainage.

Opportunities

Population:

Many would consider that the massive population of India would be a bane. But it has

turned out to be an immense business opportunity across industries like telecom, broadcast

and healthcare.

The 1.17 billion population of 2009 is projected to reach 1.33 billion in the next 10 years. Of

which almost 60 per cent of population is in the 15-64 year age group - which is the active

earning population and will primarily drive the industry, especially the healthcare insurance

23

Industry which will make healthcare accessible over a period of time to majority of the

population.

As India 'shines', and we chant 'Jai ho', the disposable income of Indian families has

increased by a whopping 70 per cent since 2004 and is growing at a pace of 10 per cent

ever year.

This will lead to increased demand for good quality healthcare even at a premium.

Comparative low costs and Medical Tourism:

As per industry studies, almost five million foreigners had availed treatment in Indian

healthcare setups by 2008. With surgical cost almost one tenth in western worlds, the

estimated 15 billion dollar medical tourism industry will only grow further.

This has led to the creation of health cities and medical tourism hub. Now with immense

support of the Indian tourism ministry and its dedicated medical arm, the medical tourism

industry in India will grow leaps and bounds.

Looking Forward

With the personal disposable income rising by more than

70 per cent and over all income of the population rising,

the demand for better quality in healthcare is bound to

exponentially rise. With the CGHS mandating the

requirement of NABH for all reimbursements, and

hundreds of hospitals applying to get the coveted ISQua approved NABH-the mark of

international healthcare quality, this is just the beginning.

There is no doubt that the government too is focusing on improving the quality of healthcare

delivery in its own infrastructure and the promising beginning is seen with a public unit getting

the NABH accreditation in Gujarat and more on the anvil.

With only 20 per cent of healthcare delivery provided through public health units and the

government not intending to spend more on capital expenditure, more PPP projects and private

healthcare initiatives would see the light of the day.

24

To bridge the immense HR gap, especially in the clinical and professional side, the government

is mooting the idea of corporatizing medical education and it is just the matter of time when

private run non-trust based medical education on commercial lines will be seen across the

country.

Health insurance sector has never seen better days than today and with what is on the anvil.

With a population as strength, even the present two per cent penetration to a five per cent

penetration would mean millions and billions in business. The projected penetration in the next

five to 10 years is 20 per cent of the population, because the earning population of 15 to 64

year age group comprises of more than 60 per cent of the total population who can afford

health insurance. And with rising awareness and the acknowledgement that insurance is the

way to a healthy life, the demand for medical insurance will only rise further. Trend reveals that

at least in the large corporations and private organizations including public sector units,

insurance is provided as a norm to all employees. This trend will only substantiate in time to

come.

With the increase in population and to bridge the gap of number of beds, hundreds of quality

healthcare units will spring up. However, with economy growing, demand for real estate also

grows and further leads to making real estate capital investments for healthcare expensive and

making operational margins tighter. This will lead to (and already has) in unconventional model

of health care delivery by way of single specialty centres, life style units, retails clinics, to bring

in operational efficiencies and increase the EBITAs. A lot of earlier untapped models will be

tapped and the consumers will have plenty to choose.

With tax sops and other government incentives, more secondary and tertiary care units will

open in tier-2 /3 cities.

With quality standards coming on even in AYUSH and alternative medicine, and India's rich

heritage already attracting a lot of tourists, medical tourism will see a marked boom in years to

come. Health cities with an aim to woo medical tourist is on the rise, and the healthcare players

will leverage on the integrated medicine model by providing Ayurveda, Homeopathy, Unani,

Yoga and others along with the modern medicine.

25

This holistic approach will attract patients from far lands further, because the cost of care is

almost one tenth the western world’s costs.

Technology will play a major role in bringing quality in healthcare, be it better nursing

communication systems, patient monitoring devices or telemedicine to provide low cost

diagnosis to remote patients etc.

Companies like HCL, HP and Microsoft are already investing heavily in healthcare technology

and Google trying to ambitiously woo the consumers for a centralized healthcare database,

what is in store for the future of healthcare is limitless.

Pneumatic chutes, PACS, automated laboratories and other technologies are on the verge of

becoming norms in both public and private hospitals.

Conclusion

The Indian healthcare sector can be viewed as a glass half empty or a glass half full. The

challenges the sector faces are substantial, from the need to improve physical infrastructure to

the necessity of providing health insurance and ensuring the availability of trained medical

personnel. But the opportunities are equally compelling, from developing new infrastructure

and providing medical equipment to delivering telemedicine solutions and conducting cost-

effective clinical trials. For companies that view the Indian healthcare sector as a glass half full,

the potential is enormous.

Healthcare industry is the fastest growing industry but the gap between urban & rural is still

vast & that need to be filled because it will be the biggest sector to invest.

![Indian Health Care Industry[1]](https://img.dokumen.tips/doc/110x75/577d1d801a28ab4e1e8c6692/indian-health-care-industry1.jpg)