Embed Size (px)

Citation preview

Impact & performance AnalysisImpact & performance AnalysisImpact & performance AnalysisImpact & performance Analysis

of Women SHGsof Women SHGsof Women SHGsof Women SHGs

S.P.-24, Chetan Vihar, Sector

Ph : 0522- 4026249,

secretary.janhit

Impact & performance AnalysisImpact & performance AnalysisImpact & performance AnalysisImpact & performance Analysis

of Women SHGsof Women SHGsof Women SHGsof Women SHGs

24, Chetan Vihar, Sector-C, Aliganj, Lucknow-226024

4007845; E-mail : [email protected]

[email protected]; Website : www.janhit.net

Impact & performance AnalysisImpact & performance AnalysisImpact & performance AnalysisImpact & performance Analysis

226024

; Website : www.janhit.net

Page | 1

INDEX

Sl. No. Description Page

1 A. Background 2

B. Janhit Foundation 2

• Major Intervention 2

C. Performance Analysis of SHGs and Impact Assessment 3

• Objective 3

• Social 3

• Performance of SHGs 3

• Capacity Development 3

• Impact on SHG members’ household 3

D. Methodology 3

2 Findings 4

A. Social 4

• Caste Profile of members of sample groups 4

B. Performance of SHGs 4

B1. Size of Sample groups 4

B2. Members brought under financial inclusion and Life Insurance Cover 4

B3. Trend of total Savings Mobilized 4

B4. Trend of total loan of sample groups 4

B5. Dispersion of Loan among members 5

B6. Turnover/velocity of Internal lending 5

C. Capacity Development 6

C1. Expenditure reduction through debt swapping 6

C2. Investment towards Health & Education 6

C3. New Investment towards Livelihood 7

C4. New Investment towards Domestic Asset Creation & House Reconstruction 8

D. Impact/Benefits perceived by SHGs’ members 8

D1. Participation in family decision making process after joining group 8

D2. Mobility/Financial literacy 9

D3. Health (Medical treatment) 9

D4. Health(Living standard/fooding pattern) 9

D5. Education of Children 9

D6. Debt swapping from money lender to SHG 10

D7. Debt still to be repaid to Money Lender 10

D8. Income 10

D9. Livelihood 11

D10. House Reconstruction 11

D11. Domestic Assets Creation 11

3 Questionnaire (Sample) 12

Page | 2

A. Background: Like everyone else, poor people need and use financial and livelihood services all the time. The

financial services available to the poor, however, often have serious limitations in terms of cost,

security, and convenience. The poor rarely access services through the formal financial sector.

They address their need for financial services through a variety of financial relationships, mostly

informal. Credit is available from money-lenders but usually at a very high cost to borrowers.

Over the years the Community involvement and the concept of self-help were felt most required

for the success of efforts to mitigate poverty in the country. In other words, Self-Help Groups

(SHGs) are realized to be a proven model/methodology to address the issues of poverty

alleviation and women empowerment. To activate this model, micro-credit has been recognized

as a powerful tool in the struggle to end poverty and economic dependence. Microcredit program

extend small loans to poor people through their SHG for self-employment enterprise that

generate income, allowing them to care for themselves and their families. In most cases,

microcredit programs offer a combination of services and resources to their clients in addition to

credit for self-employment, these often include savings facilities, training, networking, and peer

support. Solutions to the alleviation of poverty lie in generation of self-employment/wage

employment opportunities. Such opportunities can be created by bringing at least one member of

every poor family into the fold of SHGs and enhancing access to micro-credit and livelihood

support services.

B. Janhit Foundation:

Janhit Foundation was formed by dedicated social workers and development professionals to

work as catalytic and facilitative agency for sustainable development and empowerment of poor

and underprivileged households in rural and urban areas. JANHIT FOUNDATION is registered

under society registration Act 1860 in Dec 2002.

Janhit Foundation's approach is enabling the poor to better their lives and achieve self-reliance.

Janhit strongly believes that what poor need is not charity, but hope, not sympathy but

entitlement, not delivery of services but an enabling environment to earn those services by

themselves. We hope that this enabling approach

will facilitate the poor to stand on their own by

earning a decent income with dignity.

Janhit achieves it by promoting self-reliant people

institutions, by organizing the poor. Thus creating

effective demand streams, where the poor have

an opportunity to access livelihood support

services i.e. Microcredit etc and improve income

generation and asset building capacity. Janhit is

actively working for last 4 years in 18 blocks of 4

districts of U.P. & M.P covering more than 60000

poor households.

Major Interventions:

• Targeting poor households from Poor/Small & Marginal farmers/SC/OBC/Minorities

households through its women members who are organized into self-help groups

• Capacity building of these SHGs on group management, financial literacy etc. through

formal/ informal learning sessions.

• Enabling poor household’s members to articu

empowerment.

• Ensuring in-situ availability of Agriculture/Business development service for improving

income generation through self

• Enhancing access to easy and timely availability of low cost microcredit through

with Banks.

• Risk mitigation measure like Life/Non

C. Performance Analysis of SHGs and Impact Assessment:

Objectives:

The objective of the study is to examine the performance of SHGs which have completed 3 years

of age and impact of Janhit’s Livelihood Improvement Program on SHG members’ household. It

would enable an understanding of the effects the program has on client

help in designing better financial and support services. Also it would lead to development of

complementary non-financial services at the household level to maximize the impact of program.

Under the performance of SHGs and impact of Ja

following aspects were studied:

• Social: Caste profile of members.

• Performance of SHGs:

and Life Insurance Cover, total saving mobilized, total loan dispersion

among members, turnover/velocity of internal ending.

• Capacity Development:

Investment towards health & education, livelihood intensification/diversification and

domestic asset creation.

• Impact on SHG members’ household:

decision making process, mobility/ self confidence, improvement in income and

capacity enhancement.

D. Methodology:

20% sample of total 118 groups

completing 3 years of age as on 30

September 2013, were randomly

selected and their secondary data

available in web based MIS was

analyzed to find out trend and

impact on livelihoods of groups

/members. In addition 25% of total

283 members of sample groups

were also randomly selected and

interviewed to find out perceived

benefits from their participation in

SHGs

Enabling poor household’s members to articulate their needs for livelihood

situ availability of Agriculture/Business development service for improving

income generation through self-employment.

Enhancing access to easy and timely availability of low cost microcredit through

Risk mitigation measure like Life/Non-Life Insurance.

Performance Analysis of SHGs and Impact Assessment:

The objective of the study is to examine the performance of SHGs which have completed 3 years

of age and impact of Janhit’s Livelihood Improvement Program on SHG members’ household. It

would enable an understanding of the effects the program has on client households and would

help in designing better financial and support services. Also it would lead to development of

financial services at the household level to maximize the impact of program.

Under the performance of SHGs and impact of Janhit’s Livelihood Improvement Program

following aspects were studied:

Caste profile of members.

Performance of SHGs: Size of groups, Members brought under financial Inclusion

Life Insurance Cover, total saving mobilized, total loan dispersion

among members, turnover/velocity of internal ending.

Capacity Development: Expenditure reduction through debt swapping, Enhanced

Investment towards health & education, livelihood intensification/diversification and

domestic asset creation.

on SHG members’ household: participation of SHG members in family

decision making process, mobility/ self confidence, improvement in income and

capacity enhancement.

20% sample of total 118 groups

completing 3 years of age as on 30th

September 2013, were randomly

selected and their secondary data

available in web based MIS was

analyzed to find out trend and

impact on livelihoods of groups

/members. In addition 25% of total

283 members of sample groups

were also randomly selected and

nterviewed to find out perceived

benefits from their participation in

Page | 3

late their needs for livelihood

situ availability of Agriculture/Business development service for improving

Enhancing access to easy and timely availability of low cost microcredit through linkages

The objective of the study is to examine the performance of SHGs which have completed 3 years

of age and impact of Janhit’s Livelihood Improvement Program on SHG members’ household. It

households and would

help in designing better financial and support services. Also it would lead to development of

financial services at the household level to maximize the impact of program.

nhit’s Livelihood Improvement Program

Size of groups, Members brought under financial Inclusion

Life Insurance Cover, total saving mobilized, total loan dispersion of loan

Expenditure reduction through debt swapping, Enhanced

Investment towards health & education, livelihood intensification/diversification and

participation of SHG members in family

decision making process, mobility/ self confidence, improvement in income and

Page | 4

Findings :

A. Social:

A1. Caste Profile of members of sample groups:

Out of 283 members in 20 sample groups, Schedule Caste, Schedule Tribe and OBC comprise

45%, 6% and 31% respectively.

B. Performance of SHGs

B1. Size of Sample groups :

Table-1 shows that average size of group is 14.15 with standard deviation of 2.41 that means

80% groups are having 12 to 17 women members.

Table-1

Sample Size 20 groups

Average number of members/group 14.15

Std deviation of number of members/group σ

2.41

% of group within + or – band of σ 80%

B2. Members brought under financial inclusion and Life Insurance Cover:

All sample groups have saving Bank account in Bank and all members of these groups have life

insurance cover.

B3. Trend of total Savings Mobilized:

Table-2 shows that average saving mobilized by sample groups was Rs 51,245.00 with standard

deviation of Rs 17, 475.00 by the end of Sept, 2013. 80% groups have followed normal trend of

savings

Table-2

Sample Size 20 groups

Average of total amount of cumulative Savings of

sample groups(Rs) by end of Sept,2013

51,245.00

Std deviation of total Saving σ

17,475.00

% of group within + or – band of σ 80%

B4. Trend of total loan of sample groups :

All groups have access to institutional credit from Bank in form of cash credit limits which is

revised as per RBI/NABARD guidelines by Bank. Accrued savings of Rs 10,24,900.00 and Bank

Page | 5

loan of Rs 91,50,727.00 availed by groups was used to lend to members to meet their livelihood

and other needs. Table E-1 indicates that 60% in year 2011 and subsequently 75% groups follow

normal trend while balance have some have extreme values of total cumulative loan(i.e.

extremely low or high).

Table-3

Sample Size 20 groups Average of total amount of

cumulative loan of sample groups

2011 2012 2013

Average of total amount of cumulative

loan of sample groups(Rs)

138,185 261,532 640,945

Std deviation of total loan σ

73,528 149,704 429,338

% of group within + or – band of σ 60% 75% 75%

B5. Dispersion of Loan among members:

Table-4 shows that in 70% of sample group, 81-100% members availed loan from their SHG

while in 20% group only 61- 80% of members availed loan.

Table-4

Sample Size

20 groups

Range of Dispersion of loan among members(x)

40%<x<=60% 60%<x<=80% 80%<x<=100%

% of group

under range

10% 20% 70%

B6. Turnover/velocity of Internal lending:

Turnover or velocity of internal lending is an indicator of efficiency of financial management of

group. Turnover=Total Internal Loan/(Total Savings + Total Bank Loan).Table-5 shows that all

sample groups have turnover of more than 1.0 which indicates that these groups/members have

acquired financial/group management skill through training and practice.

Table-5

Sample Size 20 groups Turnover(x)

X<=1.20 1.20<x<01.50 1.50<x<=2.0 x>2.0

% of groups 30% 45% 20% 5%

Page | 6

C. Capacity Development:

C1. Expenditure reduction through debt swapping:

Member Households of groups have done debt swapping by repaying high interest loan taken

from local money lender/MFI by taking loan from their SHGs thereby reducing monthly

expenditure liability. Table-6 shows that member households of majority of groups were debt

ridden in the network of money lender/MFI and they availed opportunity of debt swapping to

reduce monthly expenditure liability.

Table-6

Sample Size 20 groups % of groups availing Debt Swapping

Year 2011 2012 2013

Debt swapping

85%

90%

95%

Table-7 shows that as capacity of groups improved to due to enhanced access to institutional

credit and accrued savings, more and more members reduced their monthly expenditure

liability by repaying high interest loan. More than 100% growth in debt swapping amount in

subsequent year is a testimony of this fact.

Table-7

C2. Investment towards Health & Education:

Table-8 shows that % of groups investing towards health and education has increased year to

year. This clearly shows that members are slowly realizing that this investment will ultimately

have positive bearing on their livelihood and quality of life.

Table-8

Sample Size 20

groups

% of groups investing for Health &

Education

Year 2011 2012 2013

Health &

Education

70%

75%

85%

Sample

Size 20

groups

Debt Swapping Average

cumulative amount/group (Rs)

% growth of Debt Swapping

Year 2011 2012 2013 2011 2012 2013

Debt

swapping

22,425

67,210

159,826

NA

200%

138%

Page | 7

Table-9 shows that not only number of groups/members but amount of expenditure towards

health and education is also increasing yearly.

Table-9

C3. New Investment towards Livelihood:

Lack of access to institutional credit has been one of the main causes of unsustainable

livelihood. Once access to credit through SHGs is established, member household utilize major

amount of credit availed to improve their existing livelihood option. Table-10 shows almost all

groups have invested to improve their livelihood through intensification/diversification of

existing livelihood option.

Table-10

Sample Size 20

groups

% of groups investing for Livelihood

Year 2011 2012 2013

Livelihood 95% 100% 100%

Table-11 shows that not only number of groups/members but amount of investment towards

Livelihood is also increasing yearly which indicates that members are reaping benefits of

enhanced investment in livelihood.

Table-11

Sample

Size 20

groups

Average cumulative investment

amount/group on health &

Education(Rs)

% growth of Average

cumulative investment

amount/group on health &

Education

Year 2011 2012 2013 2011 2012 2013

Health &

Education

14,259 22,659 25,024 NA 59% 10%

Sample Size 20

groups

Average cumulative investment

amount/group on Livelihood (Rs)

% growth of Average

cumulative investment

amount/group on

Livelihood

Year 2011 2012 2013 2011 2012 2013

Livelihood 75,530 128,305 376,455 NA 70% 193%

Page | 8

C4. New Investment towards Domestic Asset Creation & House Reconstruction:

Table-12 shows that numbers of groups are increasingly investing for Domestic Asset

Creation/House Reconstruction which is an indicator of economic well being.

Table -12

Sample Size 20

groups

% of groups investing for Asset Creation

Year 2011 2012 2013

Domestic Asset

Creation & House

Reconstruction

95% 100% 100%

Table-13 shows the year wise cumulative amount of investment on asset creation and its

growth.

Table-13

D . Impact/Benefits perceived by SHGs’ members:

D1. Participation in family decision making process after joining group:

98.57% respondents have articulated that their role in decision making process of family,

have improved.

Table-14

Question Response % respondents

Are decisions in the family taken in

consultation with you, after joining

SHG?

1- Yes 98.57

2- No 1.43

3- Some Time 0.00

*Sample size 70 members.

Sample Size 20 groups Average cumulative

investment amount/group on

Asset Creation (Rs)

% growth of Average

investment amount/group on

Asset Creation

Year 2011 2012 2013 2011 2012 2013

Domestic Asset Creation

& House Reconstruction

10,466

23,978

37,270

NA

129%

55%

Page | 9

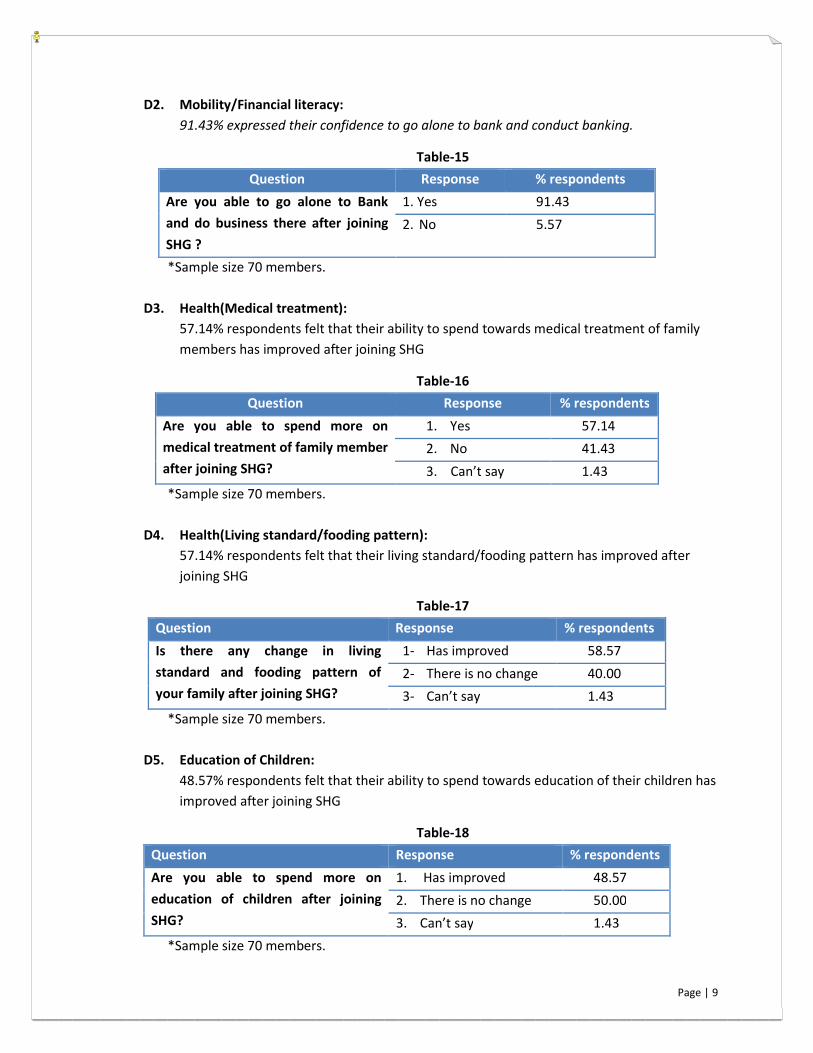

D2. Mobility/Financial literacy:

91.43% expressed their confidence to go alone to bank and conduct banking.

Table-15

Question Response % respondents

Are you able to go alone to Bank

and do business there after joining

SHG ?

1. Yes 91.43

2. No 5.57

*Sample size 70 members.

D3. Health(Medical treatment):

57.14% respondents felt that their ability to spend towards medical treatment of family

members has improved after joining SHG

Table-16

Question Response % respondents

Are you able to spend more on

medical treatment of family member

after joining SHG?

1. Yes 57.14

2. No 41.43

3. Can’t say 1.43

*Sample size 70 members.

D4. Health(Living standard/fooding pattern):

57.14% respondents felt that their living standard/fooding pattern has improved after

joining SHG

Table-17

Question Response % respondents

Is there any change in living

standard and fooding pattern of

your family after joining SHG?

1- Has improved 58.57

2- There is no change 40.00

3- Can’t say 1.43

*Sample size 70 members.

D5. Education of Children:

48.57% respondents felt that their ability to spend towards education of their children has

improved after joining SHG

Table-18

Question Response % respondents

Are you able to spend more on

education of children after joining

SHG?

1. Has improved 48.57

2. There is no change 50.00

3. Can’t say 1.43

*Sample size 70 members.

Page | 10

D6. Debt swapping from money lender to SHG:

30% members have repaid loan ranging from Rs5000/ to Rs 50000/ taken from money

lender

Table-19

*Sample size 70 members.

D7. Debt still to be repaid to Money Lender:

95.71% members have articulated that there is no outstanding loan from money ender

while balance 4.29% members still have to repay money lender loan.

Table-20

Question Response % respondents

Is there any loan still outstanding from

money lender?

1- Yes 4.29

2- No 95.71

*Sample size 70 members.

D8. Income:

54.29% respondents have perceived that their income has increased while balance 45.71%

expressed no change.

Table-21

Question Response % respondents

Is there any change in income of

your family, after joining SHG?

1- Income has increased 54.29

2- Income has decreased 0.00

3- No change 45.71

*Sample size 70 members.

Question Response % respondents /

Amount

Have you repaid loan of

money lender after joining

SHG?

1- Yes 30.00

2- If yes, how much Rs. 5000 to 50000

D9. Livelihood :

30% respondents have

11.43% respondents have diversified their livelihood. 8.57% respondents have started new

enterprise while there is no change in balance 50% respondents’ livelihood.

Question

Is there any change in

Livelihood of your family,

after joining SHG?

*Sample size 70 members.

D10. House Reconstruction:

15.71% respondents have repaired their old house while 12.86% respondents have

undertaken new construction in their house.

*Sample size 70 members.

D11. Domestic Assets Creation:

8.57% respondents have purchased domestic assets like

and Inverter etc.

*Sample size 70 members.

Question

Have you undertaken any

repair/construction in your

house, after joining SHG?

Question

Have you purchase any domestic asset?

30% respondents have articulated that they have intensified their existing livelihood while

11.43% respondents have diversified their livelihood. 8.57% respondents have started new

enterprise while there is no change in balance 50% respondents’ livelihood.

Table-22

Response

1- Expansion of existing enterprise

2- Started new enterprise

3- Started new enterprise in addition to existing enterprise

4- No change

*Sample size 70 members.

House Reconstruction:

15.71% respondents have repaired their old house while 12.86% respondents have

undertaken new construction in their house.

Table-23

*Sample size 70 members.

Creation:

8.57% respondents have purchased domestic assets like Refrigerator, Television, Solar light

Table-24

*Sample size 70 members.

Response % respondents

Have you undertaken any

repair/construction in your

1- Repaired old house 15.71

2- Some new construction done 12.86

3- Non of above 71.43

Response % respondents

Have you purchase any domestic asset? 1- Yes 8.57

2- No 91.43

Page | 11

articulated that they have intensified their existing livelihood while

11.43% respondents have diversified their livelihood. 8.57% respondents have started new

enterprise while there is no change in balance 50% respondents’ livelihood.

% respondents

30.00

8.57

Started new enterprise in addition to existing enterprise 11.43

50.00

15.71% respondents have repaired their old house while 12.86% respondents have

Refrigerator, Television, Solar light

% respondents

15.71

12.86

71.43

% respondents

8.57

1.43

Page | 12

QUESTIONNAIRE: