Embed Size (px)

Citation preview

Performance Budgeting: Current issues and ambitions

Ronnie Downes

Deputy Head, Budgeting and Public Expenditures OECD

Asian SBO

Bangkok, Thailand, 17-18 December 2015

Performance Budgeting – Simple in Theory…

€ ₩ $

…Difficult in Practice

1 1.5 2 2.5 3 3.5 4 4.5 5

Pay cut for head of programme/organisation

Programme transferred to other…

Negative consequences for leaders' evaluations

Programme eliminated

More staff assigned to programme/organisation

New leadership brought in

Budget freezes

Budget increases

More training provided to staff assigned

Budget decreases

More intense monitoring in the future

Poor performance made public

No consequences

2007 2011

What happens when performance objectives are not met?

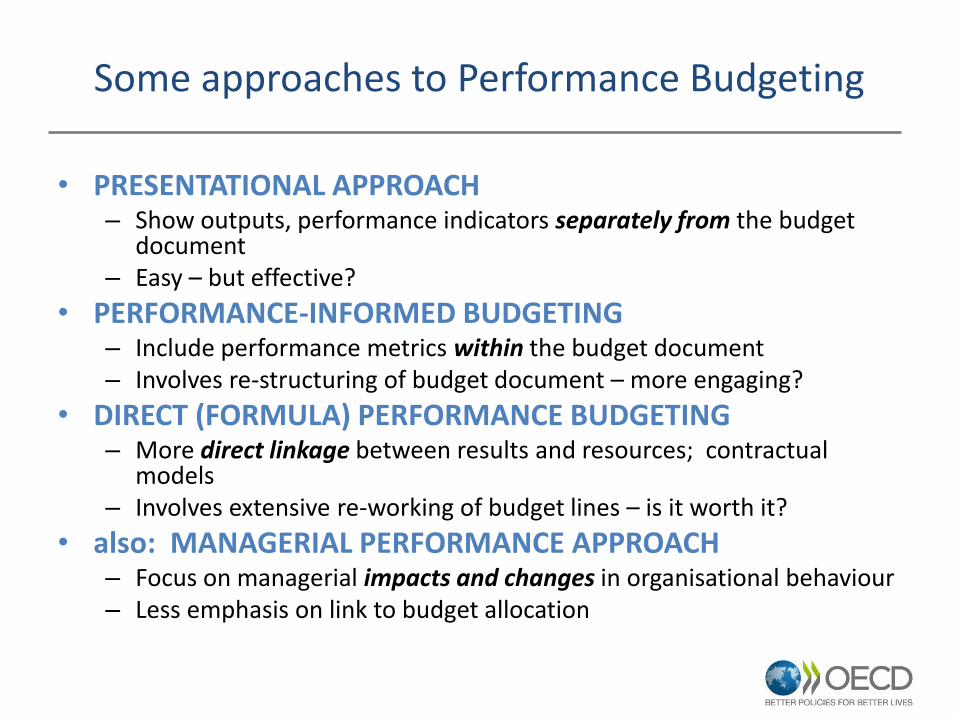

Some approaches to Performance Budgeting

• PRESENTATIONAL APPROACH – Show outputs, performance indicators separately from the budget

document – Easy – but effective?

• PERFORMANCE-INFORMED BUDGETING – Include performance metrics within the budget document – Involves re-structuring of budget document – more engaging?

• DIRECT (FORMULA) PERFORMANCE BUDGETING – More direct linkage between results and resources; contractual

models – Involves extensive re-working of budget lines – is it worth it?

• also: MANAGERIAL PERFORMANCE APPROACH – Focus on managerial impacts and changes in organisational behaviour – Less emphasis on link to budget allocation

The institutional and procedural context for Performance Budgeting is developing

• Link to KNIs?

• Standardised PB?

• Structures?

• PB Agreements?

• Transparency

• Accountability – Government (achieving strategic goals?)

– Organisational (delivering on our mandate?)

– Managerial (delivering my targets?)

• Austerity – Inform difficult government decisions, cuts

• Efficiency – Allocative (where resources have best effect)

– Operational (value-for-money, “more with less”)

• Culture-shift (focus on results and delivery)

Performance information is used for a variety of purposes

Information on outcomes and impacts is not (yet?) widely used

• Inputs?

• Outputs?

• Outcomes?

• Ratings?

• Efficiency?

• Horizontal themes?

Some challenges remain is using Performance Information; other challenges are being addressed

Accurate timely data

Relevance for budget

Info overload

Performance culture

Too bureaucratic

Lack of PB guidance

Some perennial problems

• Quality, relevance and objectivity of performance information

• What’s the proper response to Poor Performance?

– More resources, or fewer?

• “Gaming” of performance targets

– An issue where the target corresponds weakly to the public service objective

– “Outcomes” are better targets than “outputs” – but harder

• Engagement by politicians, public and bureaucrats

• Any real impact on policy-making and accountability?

Recent OECD-wide reforms: improving engagement

• Performance data should not be an internal, bureaucratic concern

• It could – and should – excite the interest of parliamentarians and the public

– Quality of debate, clearer political messages

– Emphasise continuum of policy-making: resources, activities, outputs, impacts

– Grounded in government-wide plans, strategies

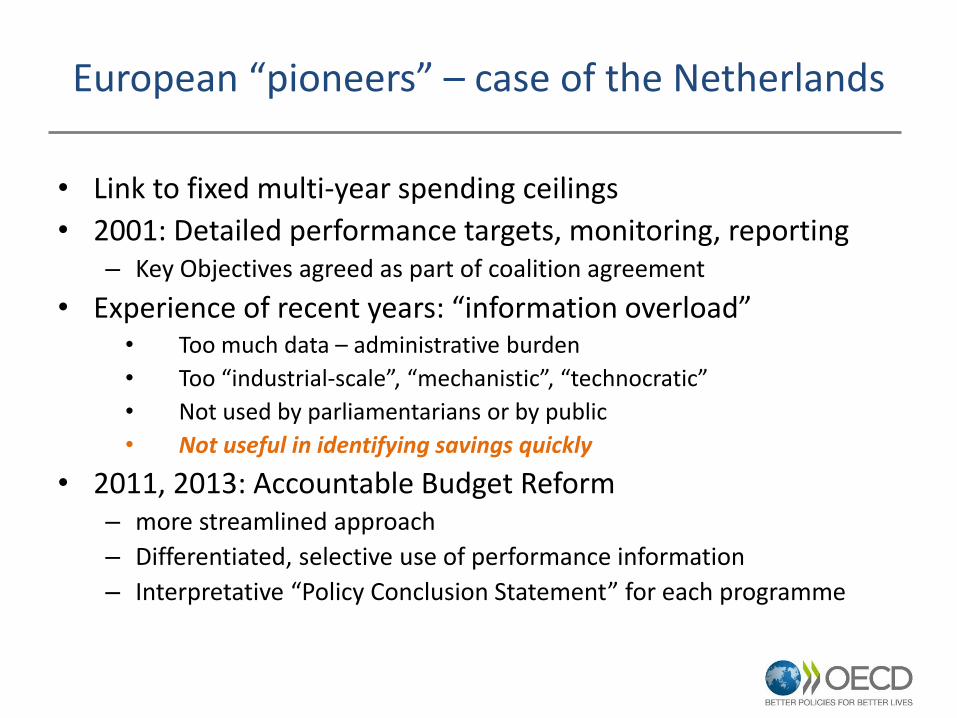

European “pioneers” – case of the Netherlands

• Link to fixed multi-year spending ceilings

• 2001: Detailed performance targets, monitoring, reporting – Key Objectives agreed as part of coalition agreement

• Experience of recent years: “information overload” • Too much data – administrative burden

• Too “industrial-scale”, “mechanistic”, “technocratic”

• Not used by parliamentarians or by public

• Not useful in identifying savings quickly

• 2011, 2013: Accountable Budget Reform – more streamlined approach

– Differentiated, selective use of performance information

– Interpretative “Policy Conclusion Statement” for each programme

Streamlining of performance indicators in France

46%

19%

35% Efficiency for the citizen

Quality of service

Efficiency for the taxpayer

Between 2014 and 2015 : -17% objectives, -19% indicators

US approach: Agency Priority Goals

• GPRA Modernization Act 2010

– Inspired in part by UK experience: PSAs

• Emphasis is primarily MANAGERIAL not BUDGETING

– Identification of Agency Priority Goals and Goal-Leaders

– Move to quarterly reporting

– Government-wide Performance Improvement Council and dedicated website

• Successful in creating internal ‘ownership’ and commitment to performance targets

Wellbeing indicators – “the Rule of Three?”

1. Economic indicators – Competitiveness – Potential growth

2. Social / Inclusive indicators – Poverty, inequality, relative income – Health, Education – Cultural life

3. Sustainability indicators – Environment – Human and physical capital – Fiscal and Societal Resilience

Examples: France, NZ, OECD

Lessons learned about good and bad practice?

a) use ready-made performance data from policy cycle

b) clear programme logic linking inputs, outputs, outcomes

c) seamless link to government-wide strategy and goals

d) avoid information overload – the “vital few” indicators

e) Include national and international benchmarks

f) organisational, managerial accountability for results

– Establish routines of behaviour within organisations

g) audited and auditable performance targets

h) citizen- and CSO-accessible data

Current Work by the OECD

• Develop a broader conception of “performance” – Whole-of-government concept – Centre of Government – leadership and coordination – HR: accountability of organisations and senior executives – Open government aspects: societal accountability

• Analysis of “what works” in OECD countries – 2016 Survey of Budgeting Practices and Government

Performance

• For discussion: What are the Asia-specific experiences of

performance budgeting successes and challenges?

Budgeting within fiscal objectives

OECD Recommendation on Budgetary Governance

Quality, integrity &

independent audit

Performance, Evaluation &

VFM

Comprehensive budget

accounting

Effective budget

execution

Alignment with medium-term strategic plans and priorities

Performance, evaluation &

VFM

Transparency, openness & accessibility

Participative, Inclusive

& Realistic Debate

Fiscal Risks & Sustainability

Capital budgeting framework

![Odrl downes-prez.ppt [repaired]](https://img.dokumen.tips/doc/110x75/58738b8d1a28ab272d8b6b95/odrl-downes-prezppt-repaired.jpg)