Embed Size (px)

Citation preview

Fraud!What you need to know!

The Fraud Triangle

Pressures and Incentives

Living beyond their meansOverwhelming desire for

personal gainHigh personal debt

Close association with customers

Feeling pay not commensurate with responsibility

Wheeler-dealer attitude

Strong challenge to beat the system

Excessive gambling habits Undue family or peer pressure

No recognition for job performance

Opportunity

Placing too much trust in key employees

Lack of proper procedures for authorization of transactions

Inadequate disclosures of personal investments and

incomes

No separation of authorization of transactions from custody of

related assets

Lack of independent checks on performance

Inadequate attention to details

No separation of custody of assets from the accounting for

those assets

No separation of duties between accounting functions

Lack of clear lines of authority and responsibility

Department that is not frequently reviewed by internal

auditors

Perception of detection is biggest deterrent to fraud

Rationalization

Not about justifying theft that has already occurred

Necessary component of crime before it takes place

Part of the motivation for the crime

After criminal act has taken place, rationalization will

often be abandoned

Once line is crossed, illegal acts become more or less

continuous

How is Fraud Detected?

0%

10%

20%

30%

40%

50%42%

16%14%

11%

7%3%

3% 2% 1% 1%

Who Commits Fraud?

19% - Owners/ Executives

42% -Employees

39% Managers

City of Dixon

Small Midwestern city with 16,000 residents

Childhood home of Ronald Reagan

General fund budget of $10 million

Audit and bookkeeping fees of $40,000

Small staff, part-time council, no City Manager

Rita Crundwell

Hometown resident

Began working at the city after high school in 1970

Named comptroller in 1983

Trusted employee and community member

Horse breeding employed a number of residents

The Fraud

Opened a non-authorized bank account in the name of the City in December 1990

Prepared fictitious invoices for infrastructure reimbursement to the State

Wrote checks for payment on fictitious invoices payable to “Treasurer”

Deposited those checks into unauthorized account

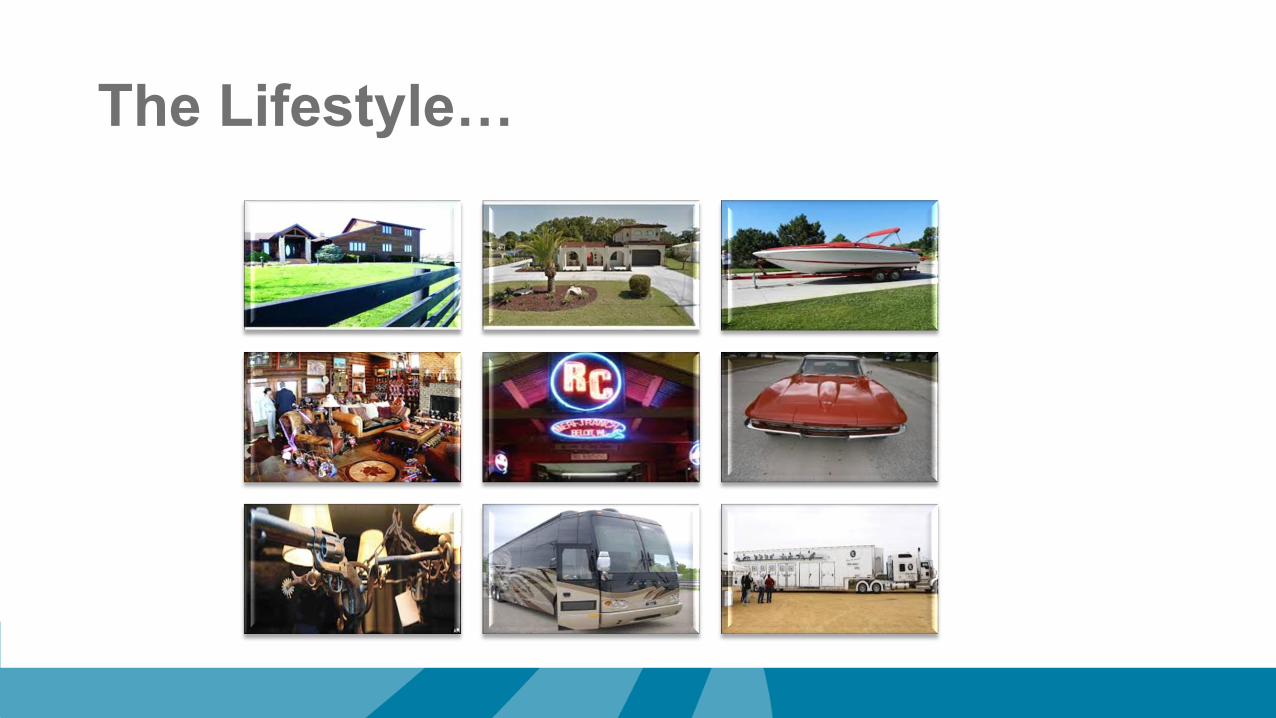

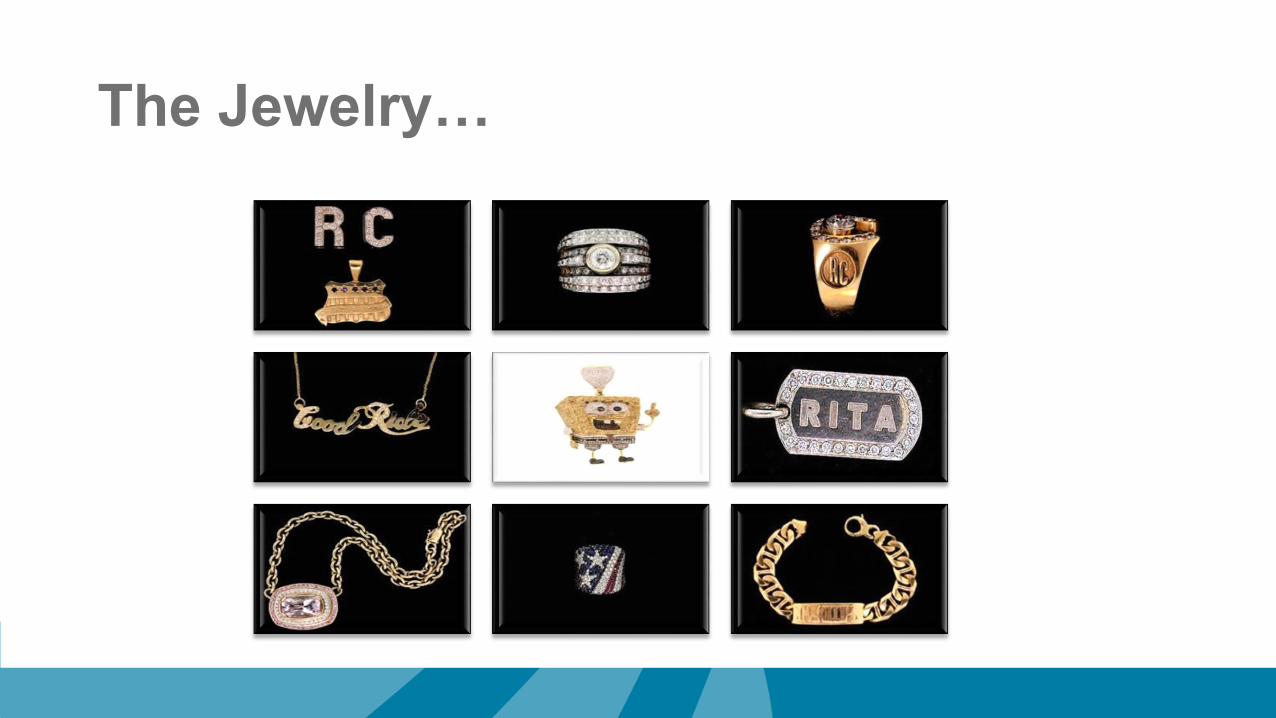

Went shopping for clothes, jewelry, cars, motorhomes, property, horses, and unusual home furnishings…

Rita Crundwell

The Lifestyle…

The Jewelry…

The Fraud

Total fraud exceeded $54.0 million

Fraud exceeded $5.6 million in 2008

179 fictitious invoices prepared

Most all fictitious invoices in even amounts

Fraud continued after initial identification until her arrest

Auditor Responsibilities

The auditor obtains reasonable assurance about whether the financial

statements as a whole are free from material misstatement, whether due

to fraud or error.

To obtain reasonable assurance, which is a high but not absolute, level

of assurance, the auditor identifies and assesses the risks of material

misstatement, whether due to fraud or error, based on an understanding of

the entity and it environment, including the entity’s internal control.

Due to the inherent limitations of an audit, an unavoidable risk exists that

some material misstatements of the financial statements may not be

detected, even though the audit is properly planned and performed in

accordance with GAAS

Responsibility for Prevention and Detection of Fraud

The primary responsibility for the prevention and detection of fraud rests with

both those charged with governance of the entity and management. It is

important that management, with the oversight of those charged with governance,

places a strong emphasis on fraud prevention, which may reduce opportunities

for fraud to take place, and fraud deterrence, which could persuade individuals

not to commit fraud because of the likelihood of detection and punishment.

This involves a commitment to creating a culture of honesty and ethical

behavior, which can be reinforced by active oversight by those charged

with governance. Oversight by those charged with governance includes

considering the potential for override of controls or other inappropriate

influence over the financial reporting process, such as efforts by management to

manage earnings in order to influence the perceptions of financial statement users

regarding the entity's performance and profitability.