Hanoi, April 2006

Prepared by Vietnam Textile and Apparel Association (Vitas) with assistance from the TradePromotion Agency (the Ministry of Trade), Trade Promotion Project VIE/61/94 (funded by theGovernments of Switzerland and Sweden and implemented by International Trade Centre),

and MCG Management Consulting

Contents

List of tables 4

List of figures 4

Abbreviations 5

Vietnam Textile and ApparelAssociation (Vitas)

Garment Export Strategy 2006 - 2010

Third Draft

Executive Summary 6

1 Part I - Introduction 81.1 Rationale 81.2 Principles of Analysis 81.2.1 Scope of Strategy 81.2.2 Framework for Strategy Design and

Management 91.2.3 Value Chain Analysis 9

2 Part II – Status Quo Analysis 102.1 New Challenges after the Phase-out of the Quota

System 102.2 Vietnam’s Garment Export Performance 112.3 Vietnam’s Current Textile and Garment Export

Value Chain 122.3.1 Qualitative Analysis of the Value Chain 132.3.2 Quantitative Analysis of the Value Chain 282.4 Critical Success Factors and Assessment of

Overall Competitiveness 302.4.1 Price 332.4.2 Long lead time 352.4.3 Customer services 372.5 SWOT Analysis 382.5.1 Strengths 382.5.2 Weaknesses 382.5.3 Opportunities 392.5.4 Threats 402.6 Government Policy and Strategy in Support of

the Sector 402.7 The Sector’s Trade Support Network 422.8 Summary of Conclusion 43

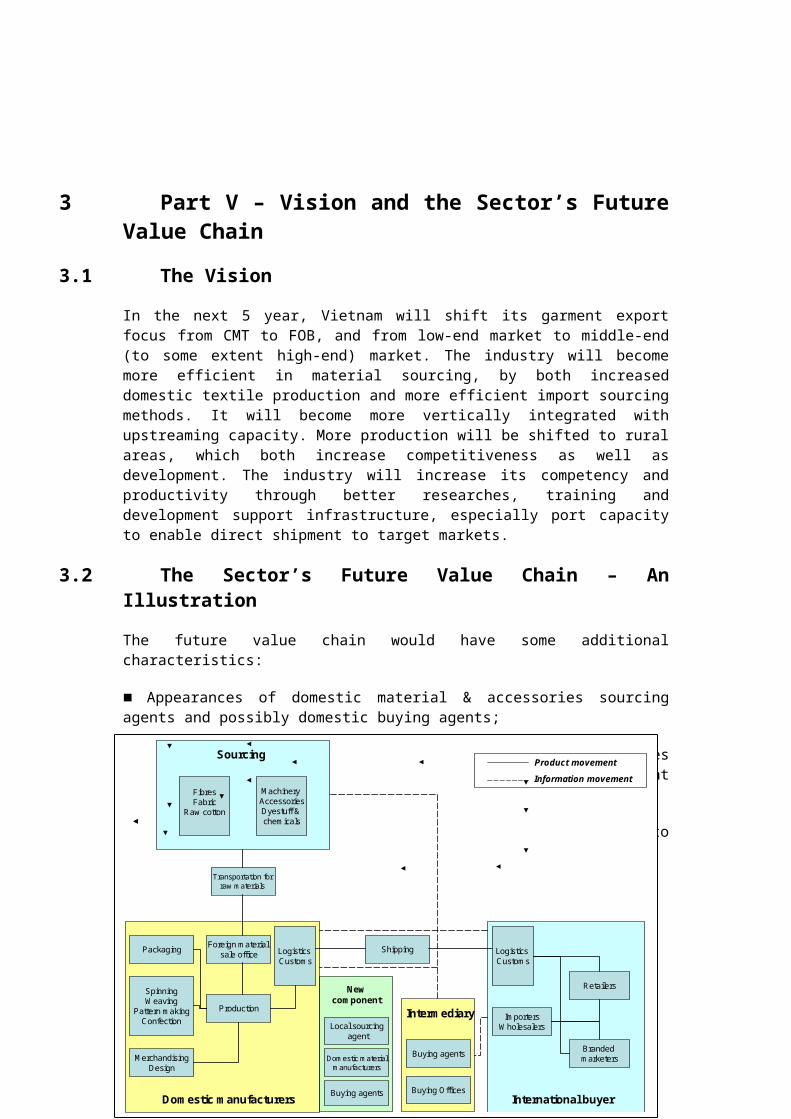

3 Part V – Vision and the Sector’s Future Value Chain 44

3.1 The Vision 44

3.2 The Sector’s Future Value Chain – An Illustration 44

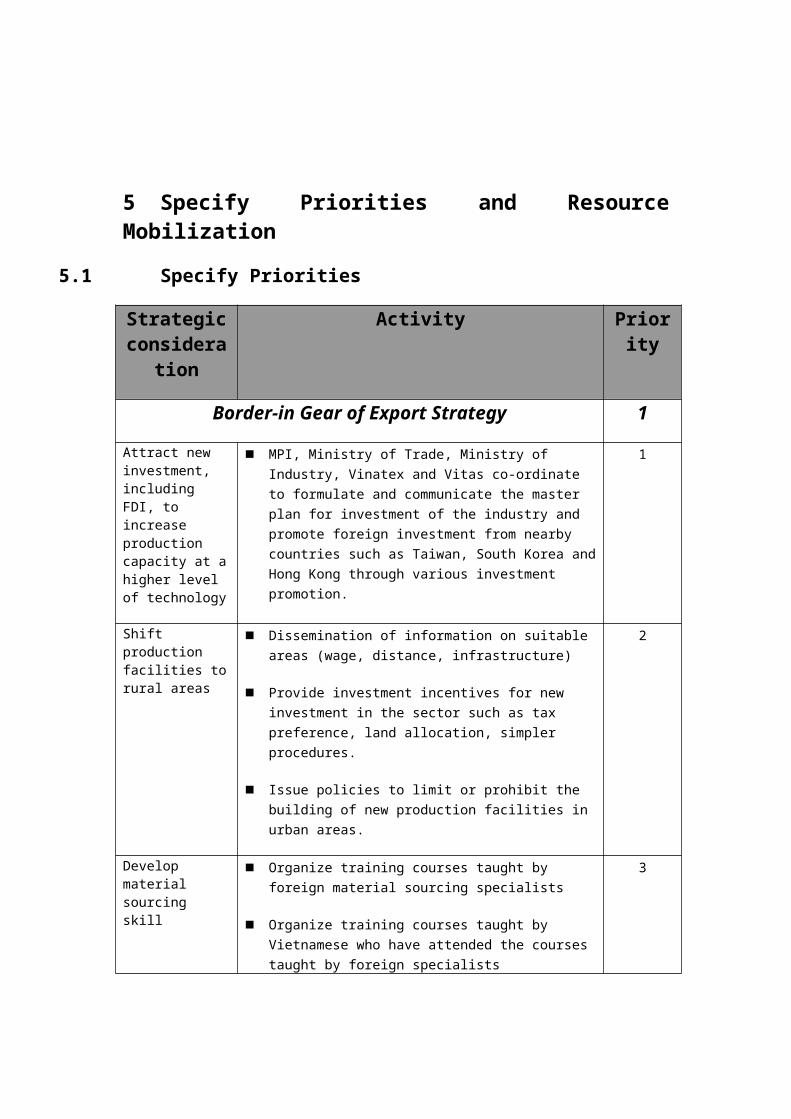

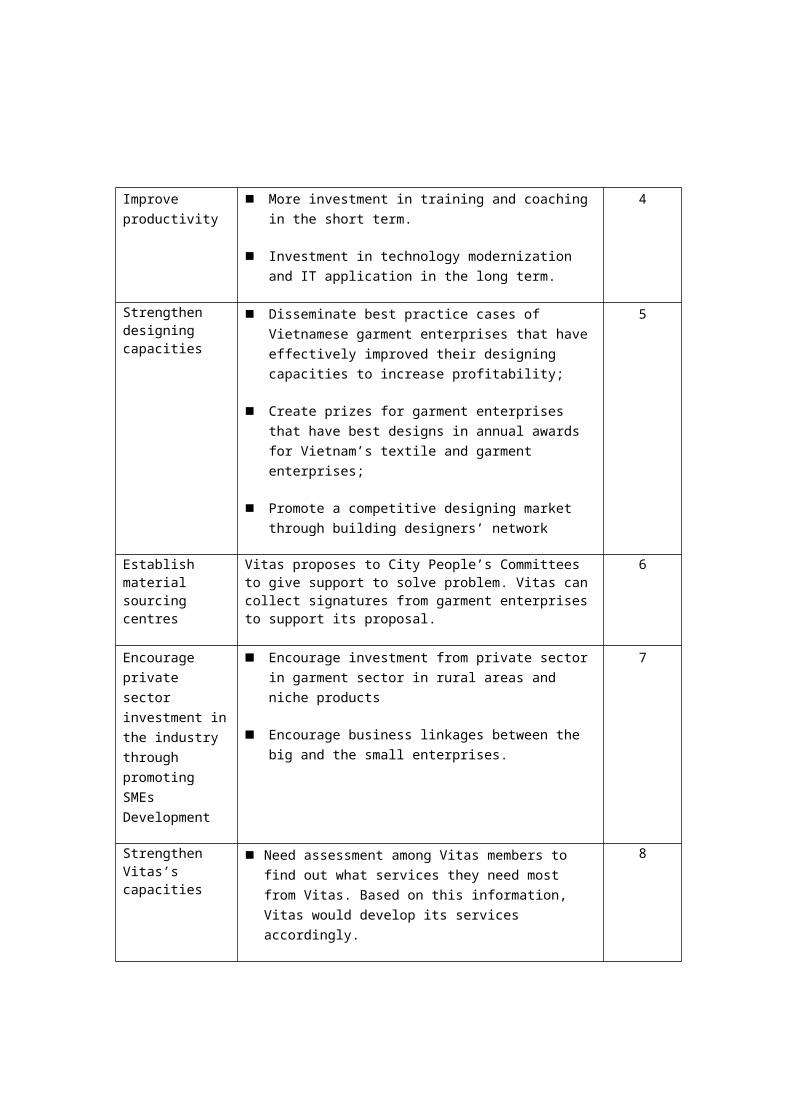

4 The Way Forward 454.1 Border-in Gear 454.1.1 Strategic Consideration 1: Attract new

investment, including FDI, to increase production capacity at a higher level of technology 45

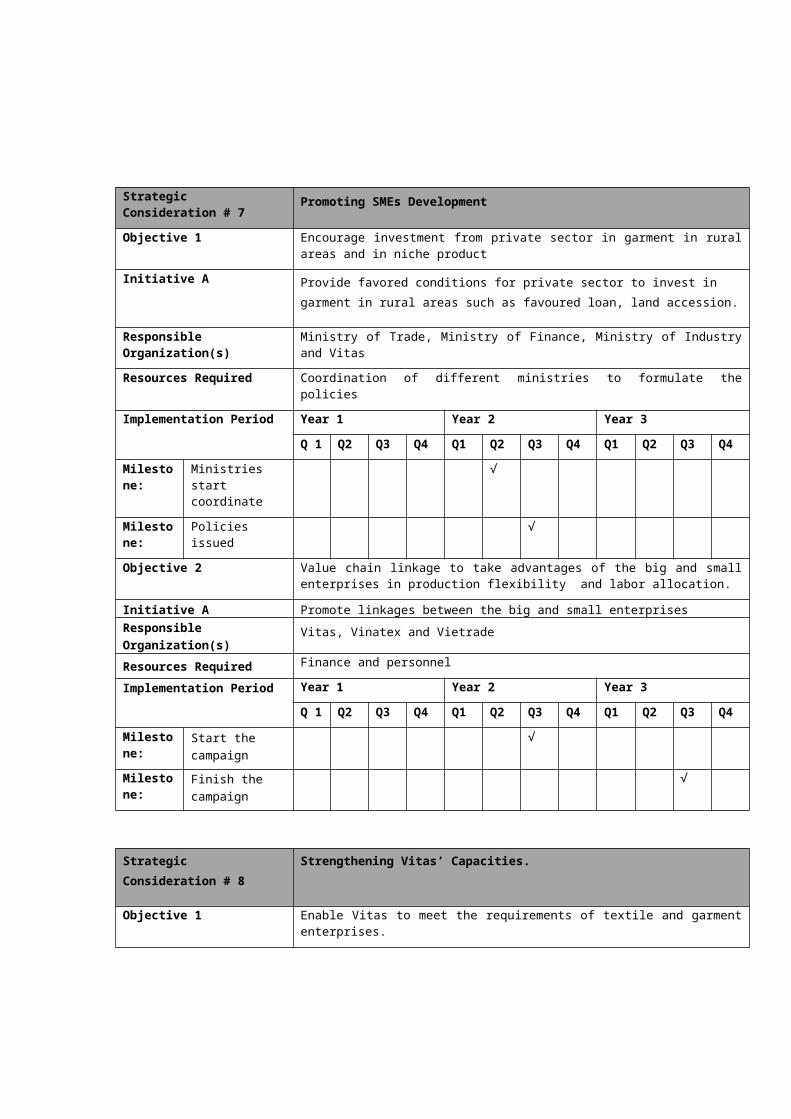

4.1.2 Strategic Consideration 2: Encourage private sector investment in the industry through promoting SMEs development 45

4.1.3 Strategic Consideration 3: Shift ProductionFacilities to Rural Areas 45

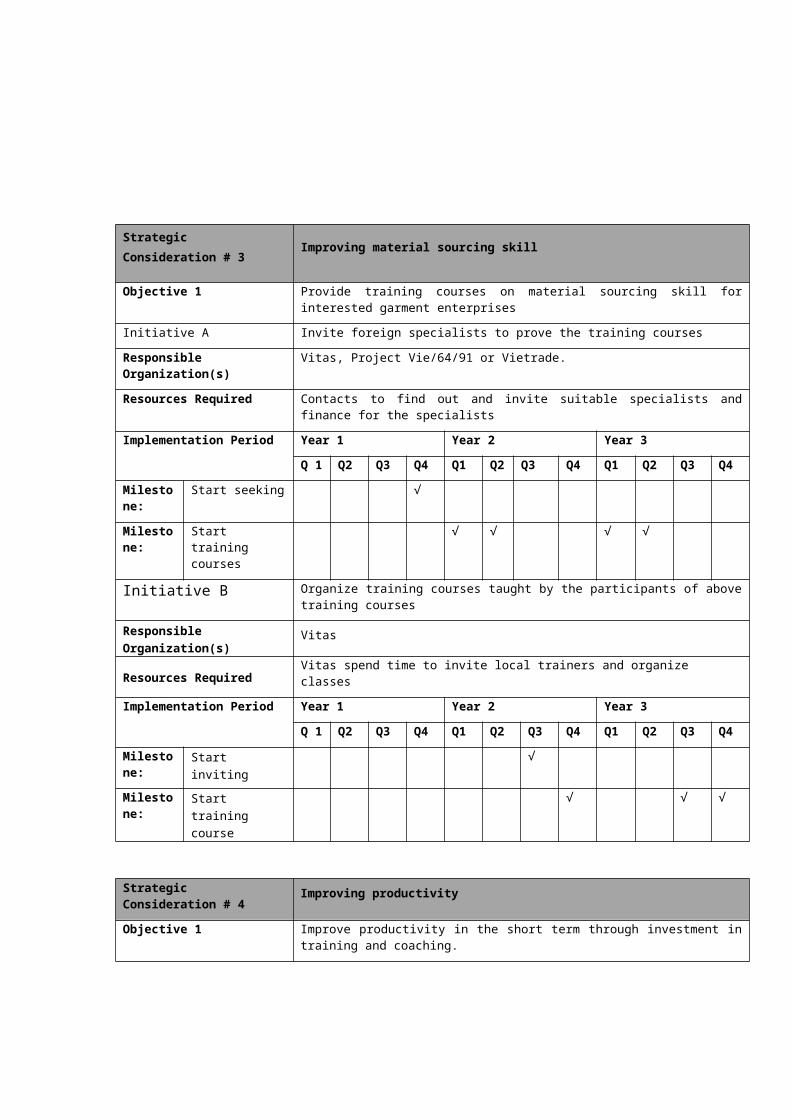

4.1.4 Strategic Consideration 4: Develop MaterialSourcing Skill 46

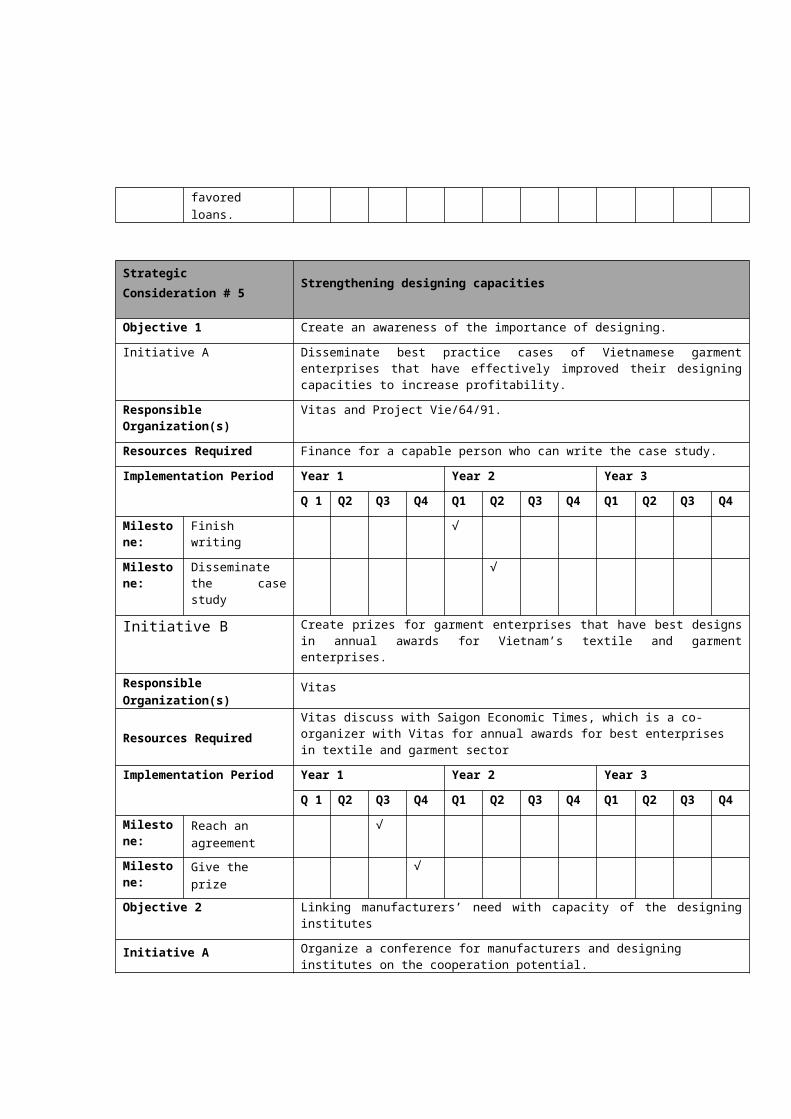

4.1.5 Strategic Consideration 5: Strengthen Designing Capacities 46

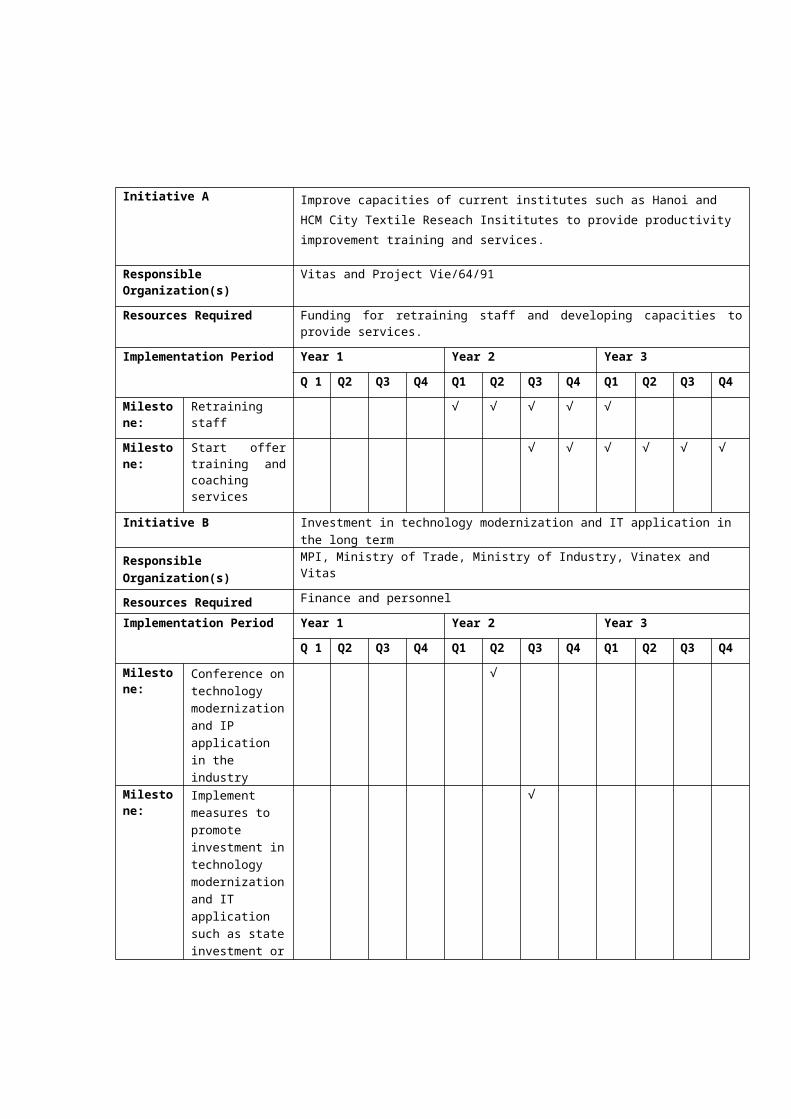

4.1.6 Strategic Consideration 6: Improve Productivity 46

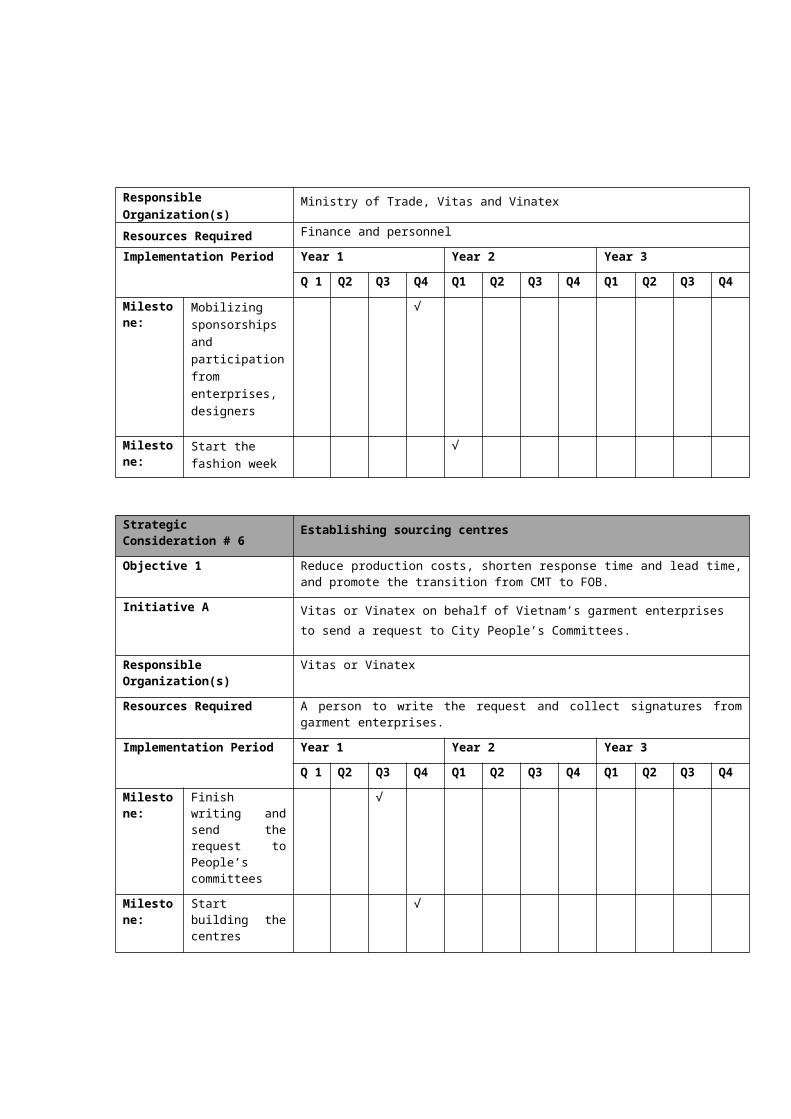

4.1.7 Strategic Consideration 7: Establish Material Sourcing Centres 47

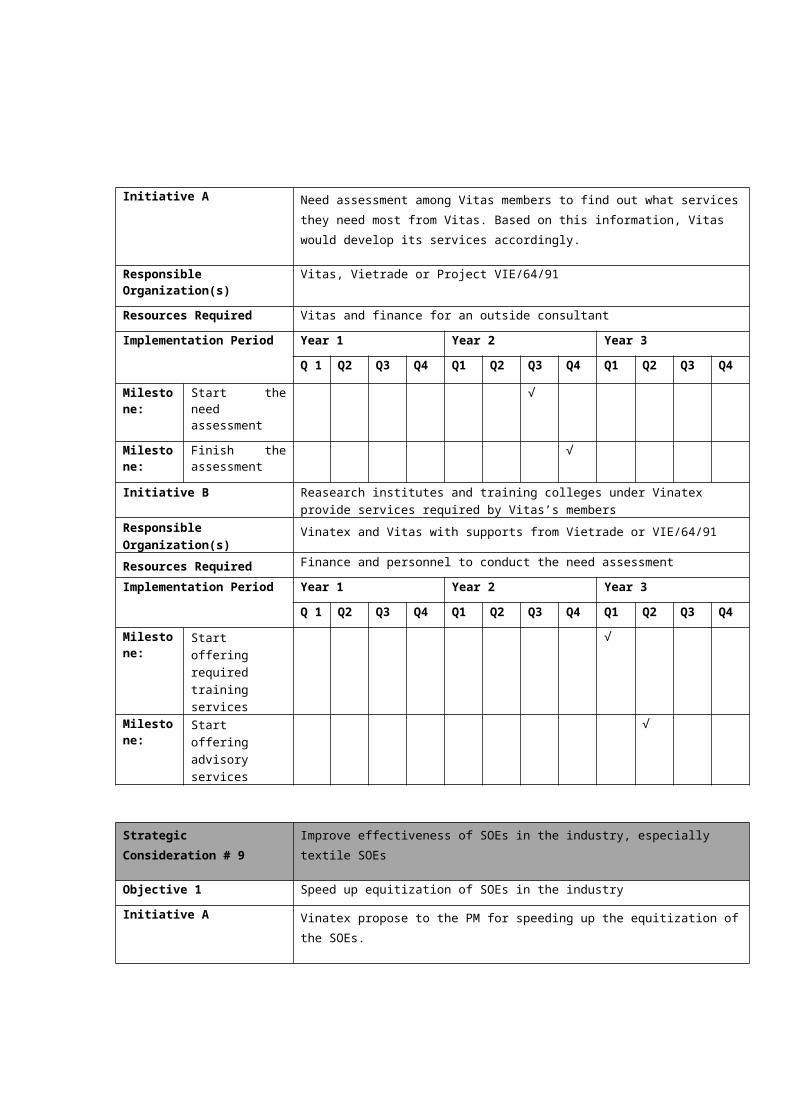

4.1.8 Strategic Consideration 8: Strengthen Vitas’ Capacities 47

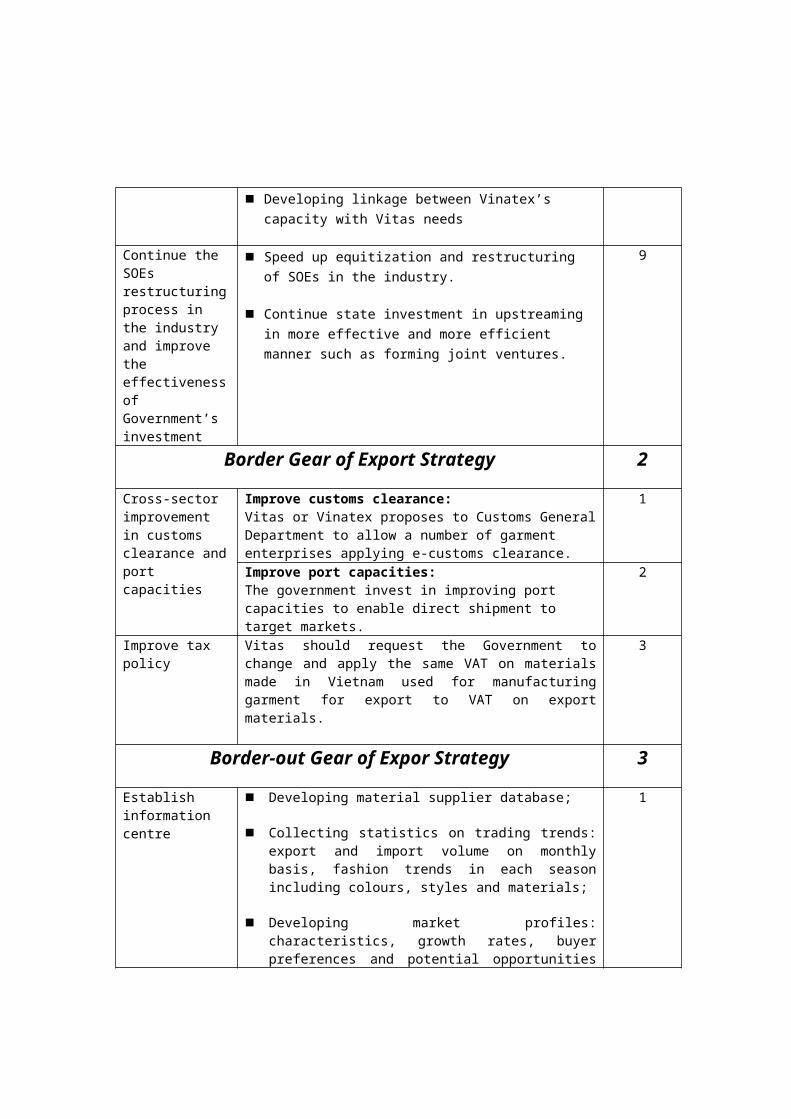

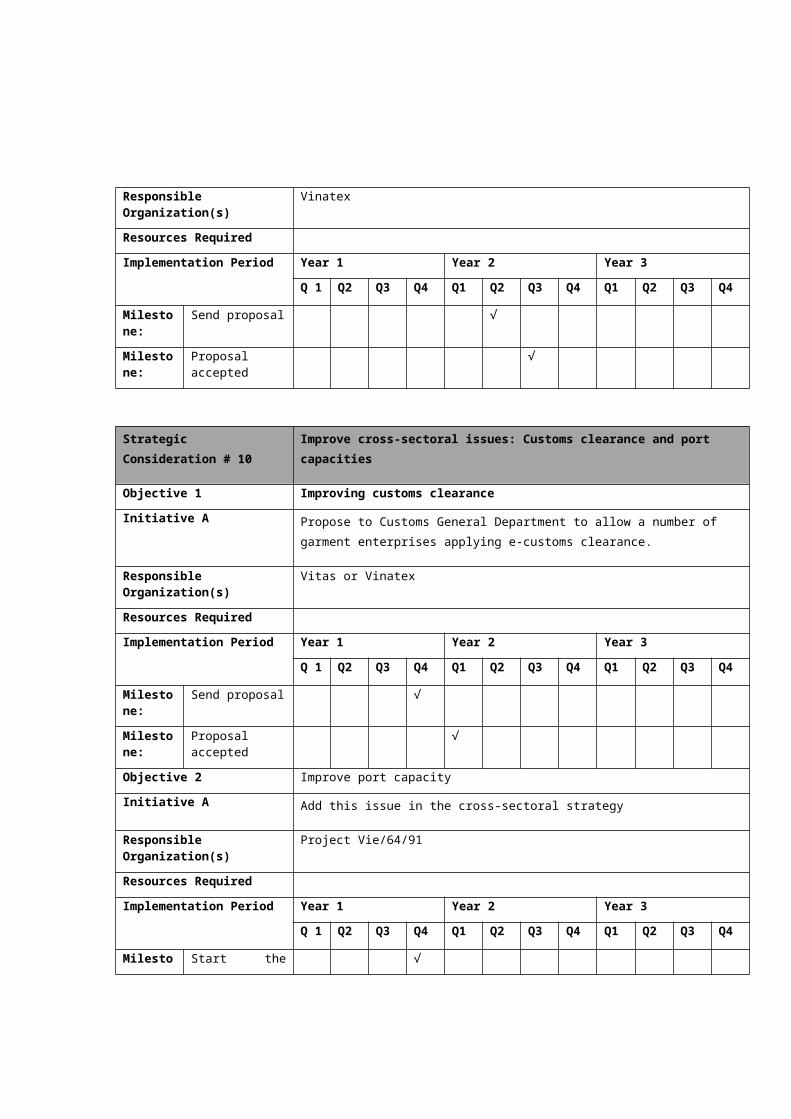

4.1.9 Strategic Consideration 9: Continue the SOEs restructuring process in the industry and improve effectiveness of Government’s Investment 48

4.2 Border Gear 484.2.1 Strategic Consideration 10: Cross-sector

improvement in customs clearance and port capacities 48

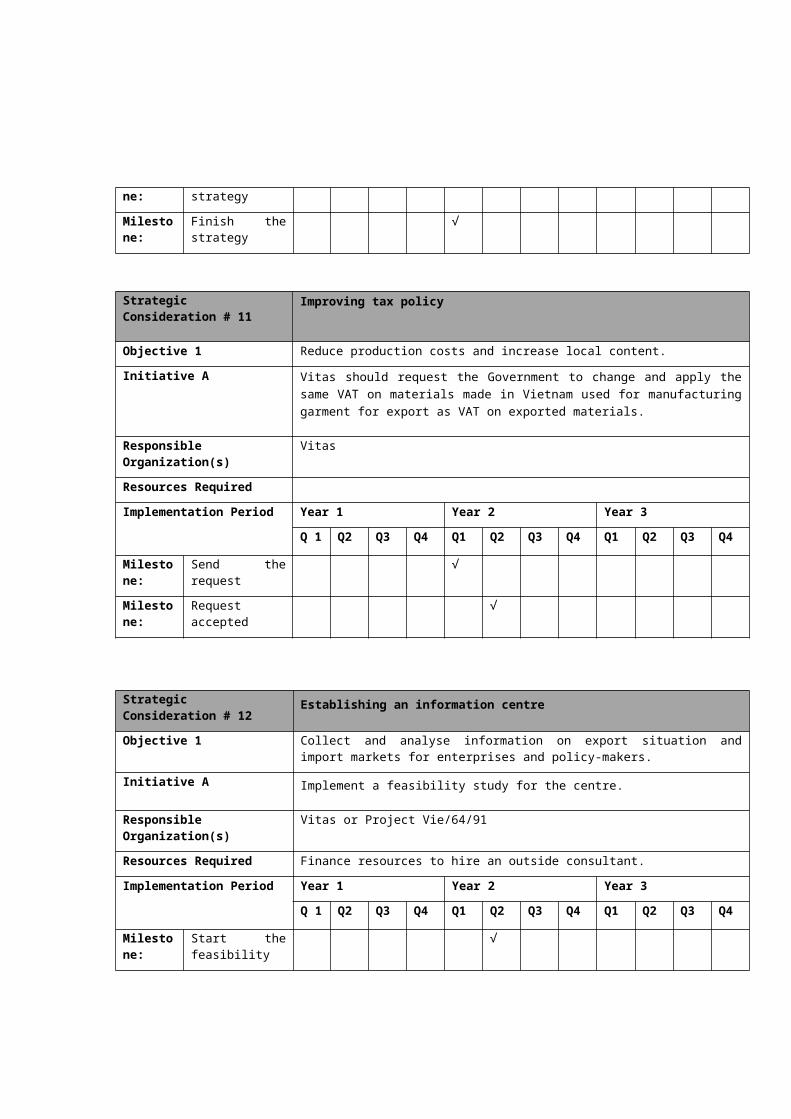

4.2.2 Strategic Consideration 11: Improve Tax Policy 48

4.3 Border-out Gear 49

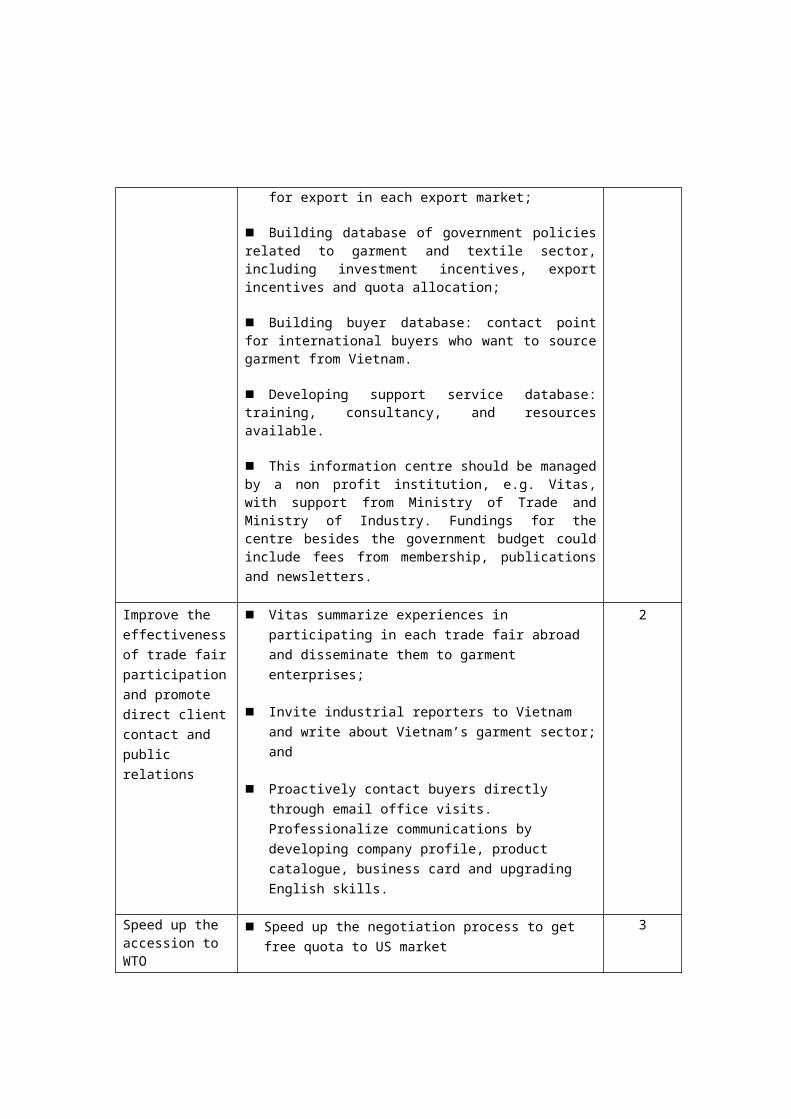

4.3.1 Strategic Consideration 12: Establishment of Information Centre 49

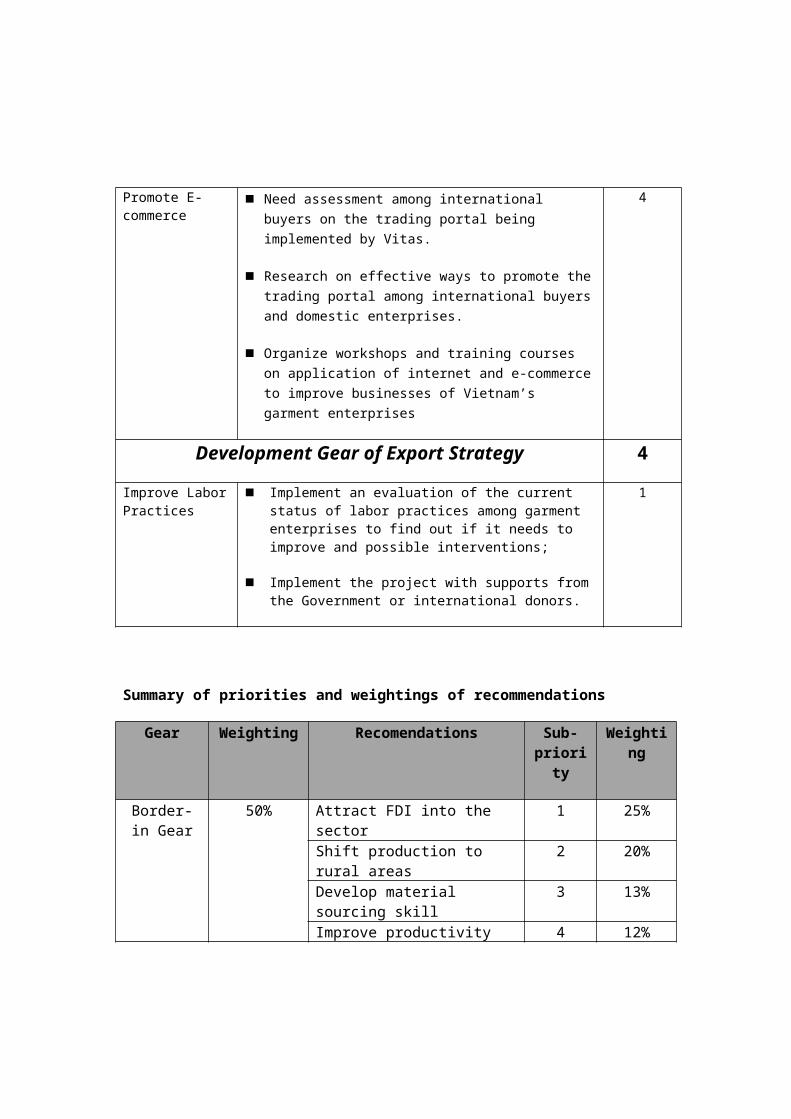

4.3.2 Strategic Consideration 13: Promote E-Commerce 49

4.3.3 Strategic Consideration 14: Improve the Effectiveness of Trade Fair Participation and Promote Direct Client Contact and Public Relations 50

4.3.4 Strategic Consideration 15: Speed Up the Accession to WTO 51

4.4 Development Gear 514.4.1 Strategic Consideration 16: Increase Labor

Practices 51

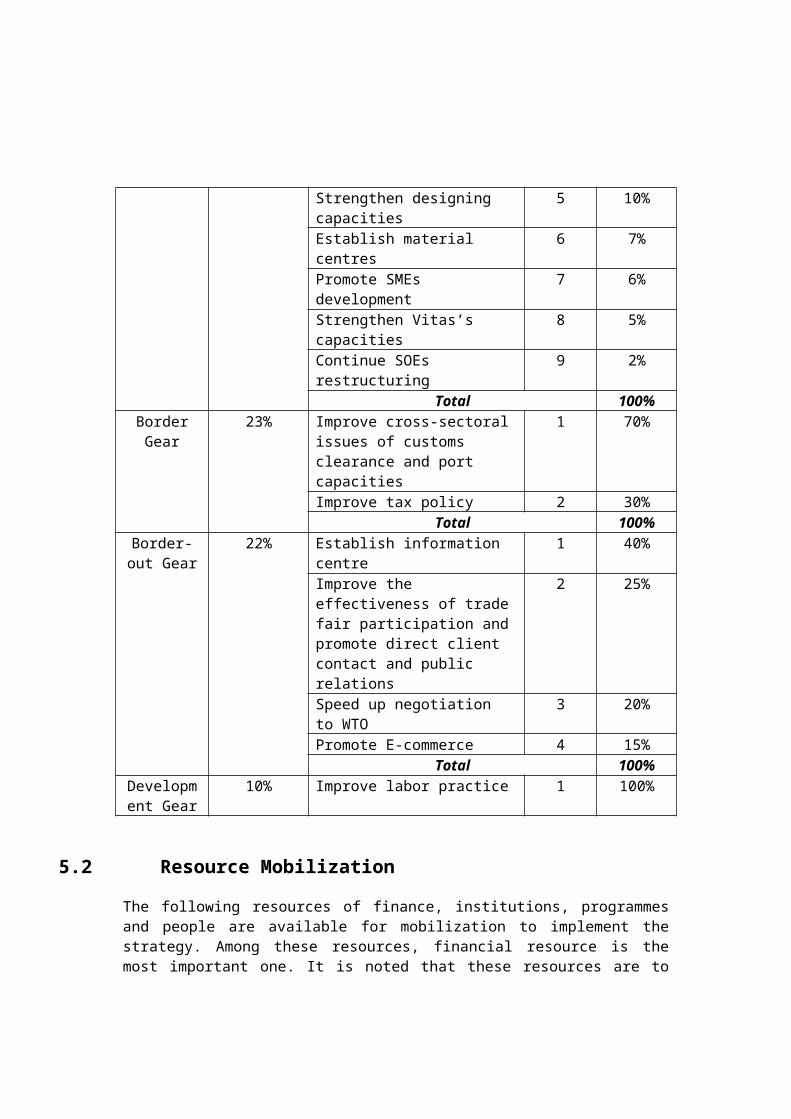

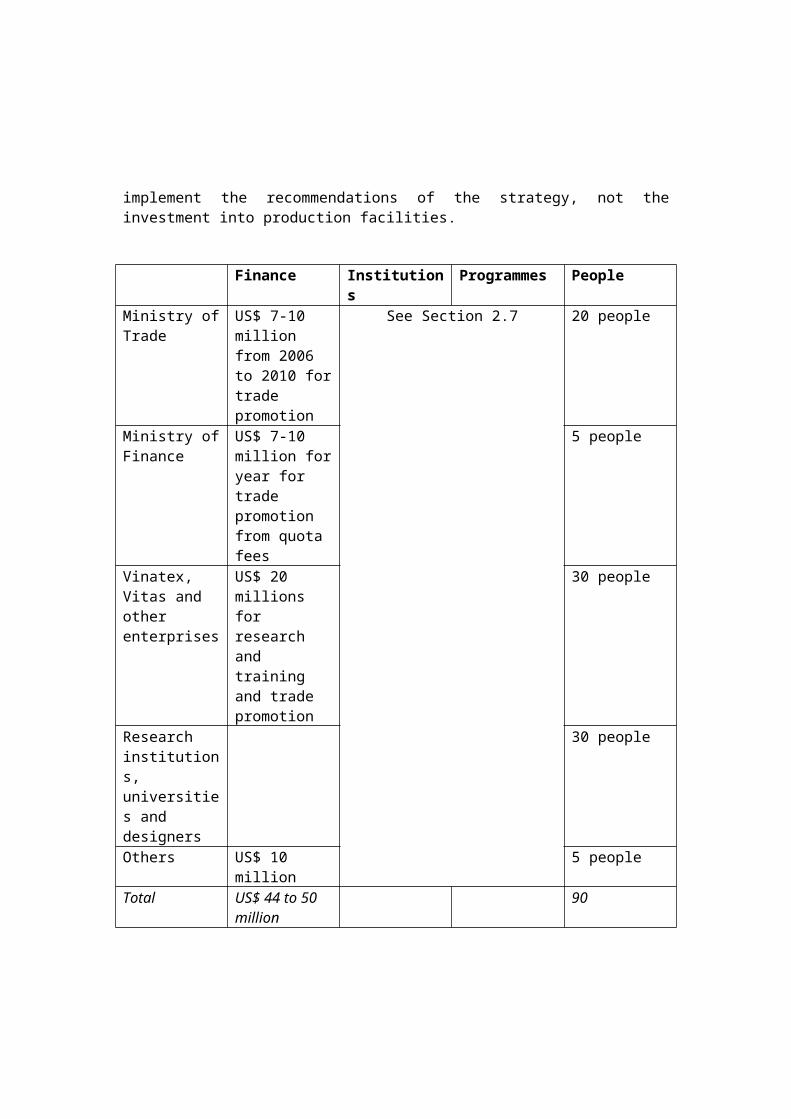

5 Specify Priorities and Resource Mobilization 52

5.1 Specify Priorities 525.2 Resource Mobilization 56

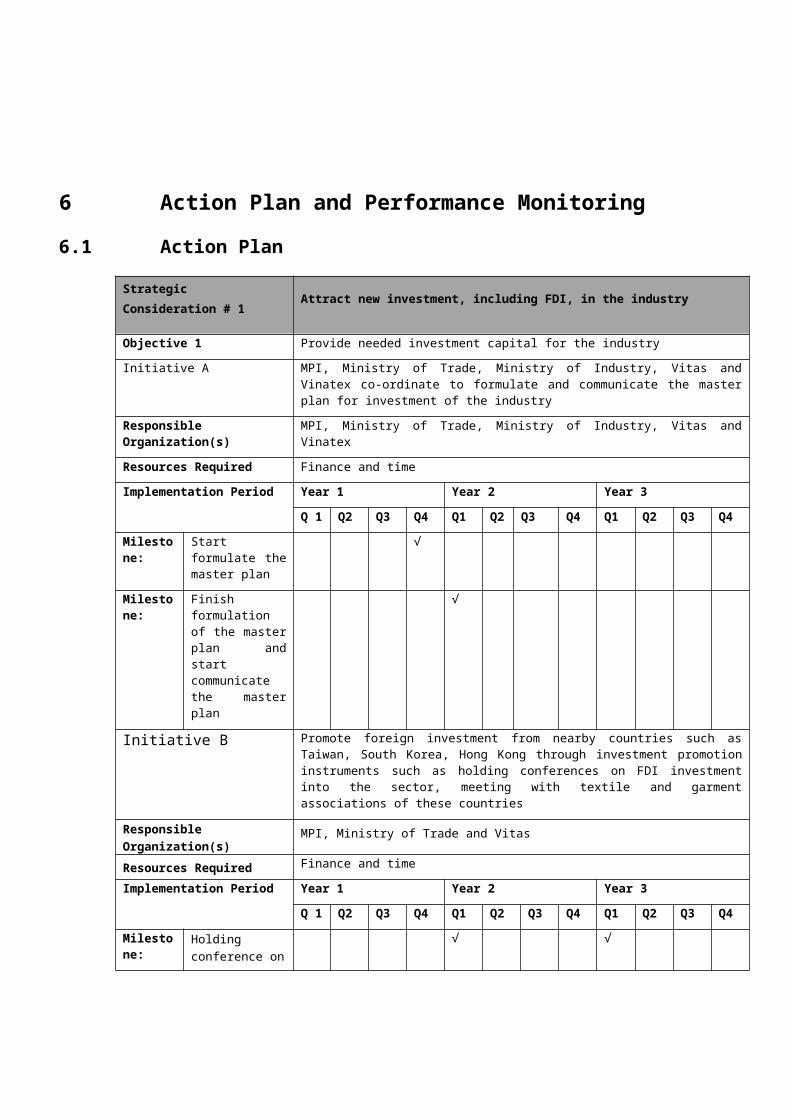

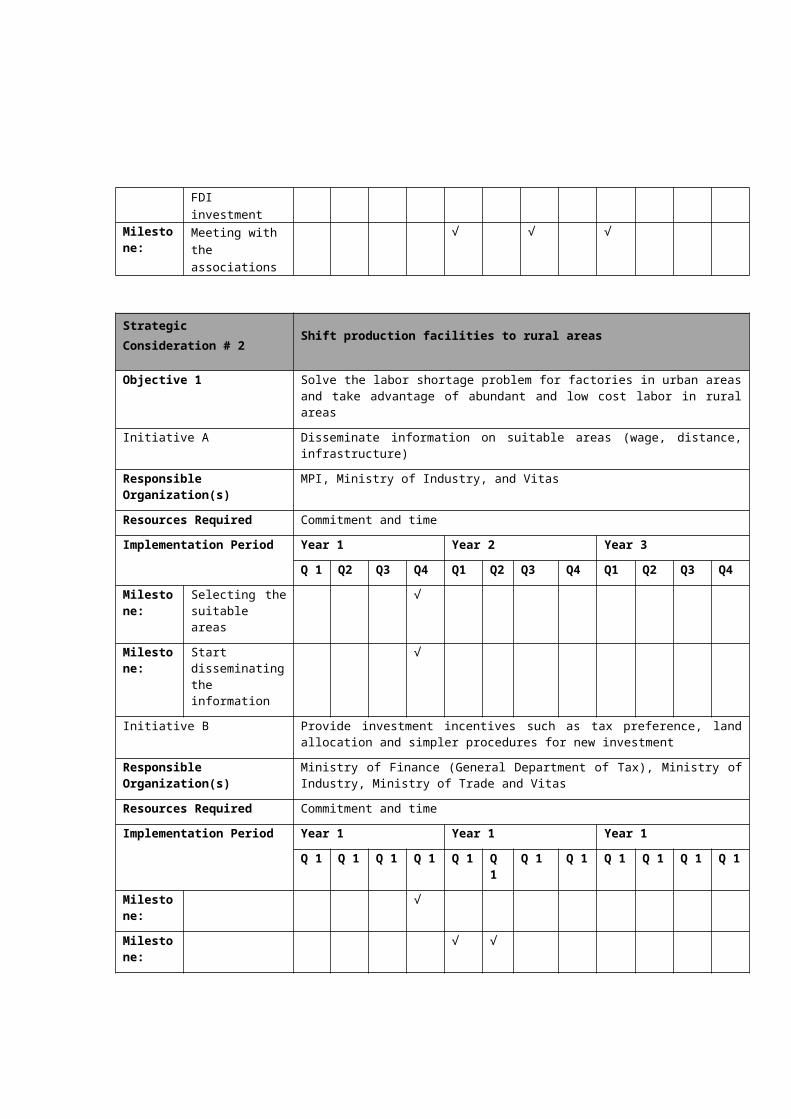

6 Action Plan and Performance Monitoring 586.1 Action Plan 586.2 Performance Monitoring 67

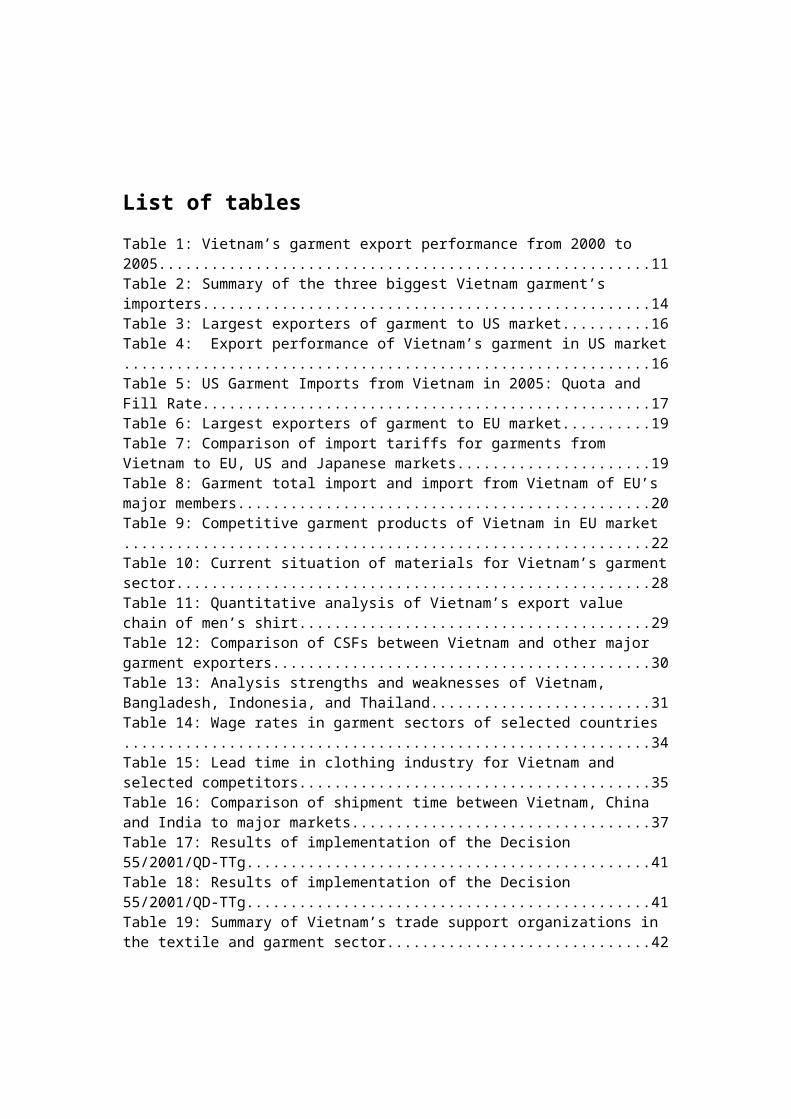

List of tablesTable 1: Vietnam’s garment export performance from 2000 to 2005........................................................11Table 2: Summary of the three biggest Vietnam garment’s importers...................................................14Table 3: Largest exporters of garment to US market..........16Table 4: Export performance of Vietnam’s garment in US market............................................................16Table 5: US Garment Imports from Vietnam in 2005: Quota and Fill Rate...................................................17Table 6: Largest exporters of garment to EU market..........19Table 7: Comparison of import tariffs for garments from Vietnam to EU, US and Japanese markets......................19Table 8: Garment total import and import from Vietnam of EU’s major members...............................................20Table 9: Competitive garment products of Vietnam in EU market............................................................22Table 10: Current situation of materials for Vietnam’s garmentsector......................................................28Table 11: Quantitative analysis of Vietnam’s export value chain of men’s shirt........................................29Table 12: Comparison of CSFs between Vietnam and other major garment exporters...........................................30Table 13: Analysis strengths and weaknesses of Vietnam, Bangladesh, Indonesia, and Thailand.........................31Table 14: Wage rates in garment sectors of selected countries............................................................34Table 15: Lead time in clothing industry for Vietnam and selected competitors........................................35Table 16: Comparison of shipment time between Vietnam, China and India to major markets..................................37Table 17: Results of implementation of the Decision 55/2001/QD-TTg..............................................41Table 18: Results of implementation of the Decision 55/2001/QD-TTg..............................................41Table 19: Summary of Vietnam’s trade support organizations in the textile and garment sector..............................42

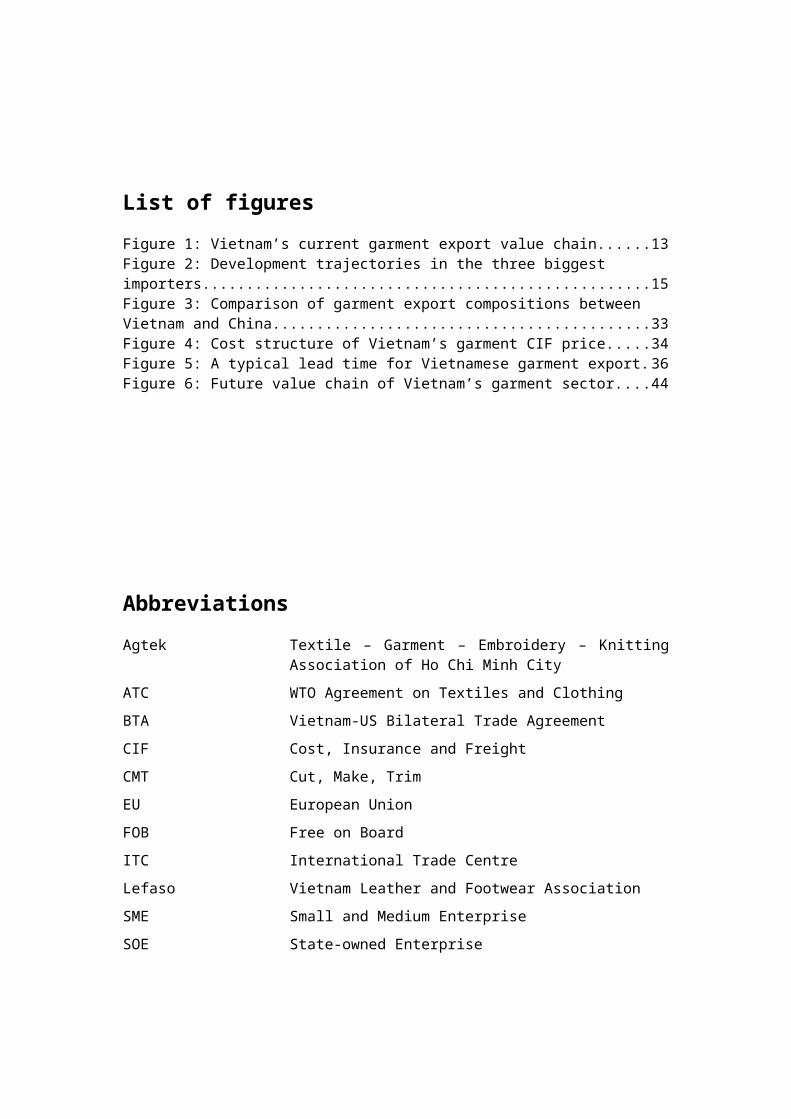

List of figuresFigure 1: Vietnam’s current garment export value chain......13Figure 2: Development trajectories in the three biggest importers...................................................15Figure 3: Comparison of garment export compositions between Vietnam and China...........................................33Figure 4: Cost structure of Vietnam’s garment CIF price.....34Figure 5: A typical lead time for Vietnamese garment export.36Figure 6: Future value chain of Vietnam’s garment sector....44

AbbreviationsAgtek Textile – Garment – Embroidery – Knitting

Association of Ho Chi Minh CityATC WTO Agreement on Textiles and ClothingBTA Vietnam-US Bilateral Trade AgreementCIF Cost, Insurance and FreightCMT Cut, Make, TrimEU European UnionFOB Free on BoardITC International Trade CentreLefaso Vietnam Leather and Footwear AssociationSME Small and Medium EnterpriseSOE State-owned Enterprise

TCA Textile and Clothing AgreeementUK United KingdomUS United States of AmericaVietrade Vietnam Trade Promotion AgencyVinatex The Vietnam National Textile and Garment

CorporationVitas Vietnam Textile and Apparel AssociationWTO World Trade Organization

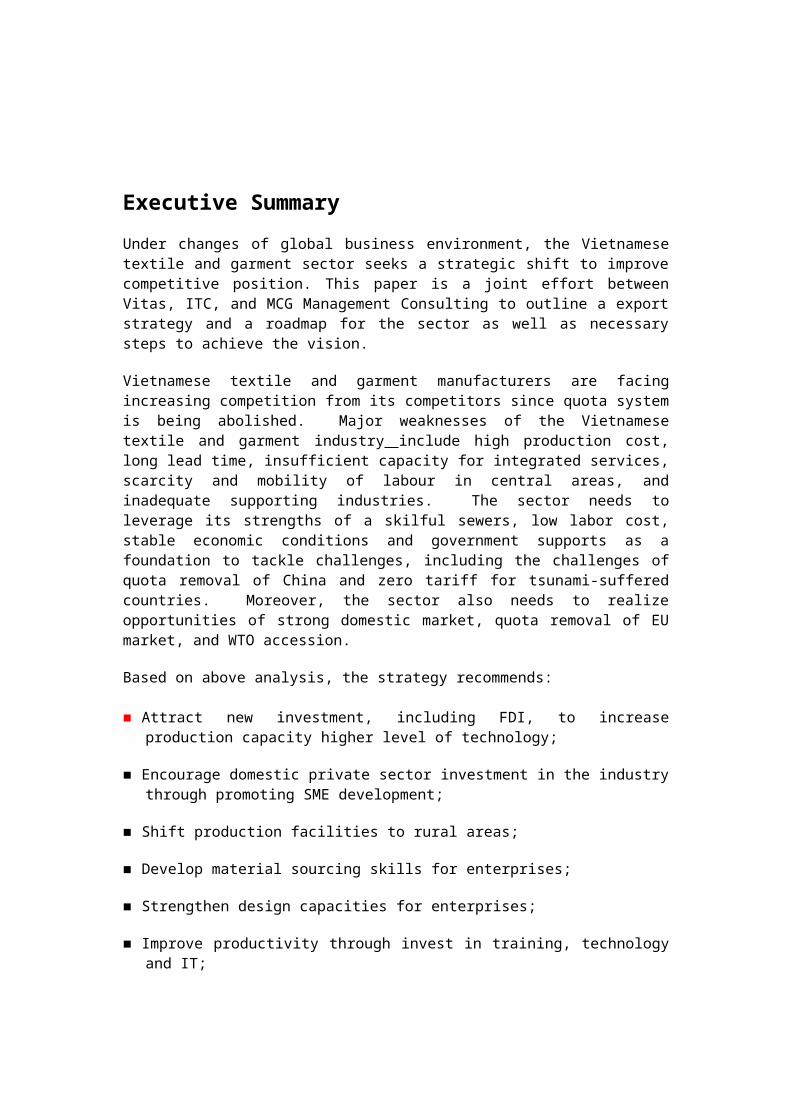

Executive SummaryUnder changes of global business environment, the Vietnamesetextile and garment sector seeks a strategic shift to improvecompetitive position. This paper is a joint effort betweenVitas, ITC, and MCG Management Consulting to outline a exportstrategy and a roadmap for the sector as well as necessarysteps to achieve the vision.

Vietnamese textile and garment manufacturers are facingincreasing competition from its competitors since quota systemis being abolished. Major weaknesses of the Vietnamesetextile and garment industry include high production cost,long lead time, insufficient capacity for integrated services,scarcity and mobility of labour in central areas, andinadequate supporting industries. The sector needs toleverage its strengths of a skilful sewers, low labor cost,stable economic conditions and government supports as afoundation to tackle challenges, including the challenges ofquota removal of China and zero tariff for tsunami-sufferedcountries. Moreover, the sector also needs to realizeopportunities of strong domestic market, quota removal of EUmarket, and WTO accession.

Based on above analysis, the strategy recommends:

Attract new investment, including FDI, to increaseproduction capacity higher level of technology;

Encourage domestic private sector investment in the industrythrough promoting SME development;

Shift production facilities to rural areas;

Develop material sourcing skills for enterprises;

Strengthen design capacities for enterprises;

Improve productivity through invest in training, technologyand IT;

Establish material sourcing centres;

Strengthen Vitas’ capacity to provide better services forits members;

Accelerate the process of SOE restructuring in the textileand garment sector;

Speed up the solutions of e-customs declaration, conductpost clearance audit and improve port capacities;

Improve tax policy to for the development of the materialindustry;

Establish the industrial information centre;

Promote E-commerce application in the industry;

Improve the effectiveness of trade fair participation andpublic relations;

Speed up the accession to WTO;

Increase labour practices.

1 Part I - Introduction

1.1 Rationale

Textile and garment sector is the second largest export earnerfor Vietnam, after oil and gas, with export value of USD 4.4billion in 2004 and estimated to be USD 4.8 billion in 2005.The garment and textile sector employs over two millionworkers, accounting for 18% of total industrial employment.

In the wake of removal of quota since 1 January 2005 for WTOcountries, Vietnam’s garment export has been facing increasingcompetitions from giant garment exporters such as: China,India, Pakistan and Indonesia. The unability of Vietnam’sgarment sector to meet 2005 export target of USD 5.2 billionreveals some weaknesses that the sector needs to address tobecome more competitive. A national strategy to addressweaknesses and promote the export of Vietnam’s garment sectoris urgently needed to meet the target of USD 8-9 billion in2010 set by the Prime Minister1.

This Strategy is a part of Project Vie/61/94 jointly funded bythe Government of Switzerland and Sweden and implemented byInternational Trade Centre (ITC) and Vietnam Trade PromotionAgency (Vietrade-Ministry of Trade).

1.2 Principles of Analysis

The analysis in this strategy follows three principles:

1.2.1 Scope of Strategy

Competitiveness of a sector in Vietnam comes from fourelements: (i) the competitiveness of enterprises, relating tocapacity development and competency (ii) the businessenvironment in which enterprise are operating, (iii) thepolicies of the Government and of other countries related to1 Decision 55/2001/QD/TTg of the Prime Minister on Approval for Strategy to promote Vietnam Textile and Garment Industry from 2001 to 2010.

the sector, including market access and trade promotion, and(iv) the contribution of the sector to the economic and socialdevelopment of the country. These elements interact with eachother; any problem in each element would adversely affectother elements and the competitiveness of the whole sector.Therefore, the scope of the export strategy of the garmentindustry shall address all of these four elements to be ableto improve export performance.

1.2.2 Framework for Strategy Design and Management

The strategy firstly analyses the status quo of Vietnam’sgarment sector with respect to its internationalcompetitiveness and performance. Then it states a vision forthe sector until 2010 and finally recommends which strategicmoves must be taken to achieve the vision.

Given the limited resources among public and private sectorsfor implementing the strategy, priorities of actions fromperspective of each stakeholder of the strategy are taken. Anaction plan is included in which it specifies whichorganization responsible for each activity with a timeframespecified.

1.2.3 Value Chain Analysis

Sector’s value chain is used as a main analysis tool in thisstrategy. Value chain analysis would give a picture of whereVietnam’s garment sector is standing in comparison to those ofother countries. The strengths and weaknesses in each link inthe value chain also give a strategic view of what should bedone in order to add value in each link and to move up to morevalue-added activities. It is important to address thecurrent value chain, but the strategy also looks at how theglobal value chain, and Vietnam’s role within it, will evolveover the coming years.

2 Part II – Status Quo Analysis

2.1 New Challenges after the Phase-out of theQuota System

The quota system had somehow created market distortion. Anumber of inefficient garment exporting countries in the 90stook advantage of the quota accesses to garment importingcountries. In a quota-free period, these countries would finddifficult to compete with more efficient exporting countries.

The phase-out of quota system since 1 January 2005 hasdemonstrated that. In the first half of 2005, garmentexporters such as Mexico, Philippines and Nepal saw theirnegative export growth rates of -3.62%, -4.56%, and -14.34%;other exporters such as China, India, Bangladesh, Indonesiaand Thailand increased their export growth rates of 50.49%,36.59%, 16.51%, 9.09% and 8.71% respectively. During the sameperiod, garment export of Vietnam grew only 3.37%2.

Without quota constraint, garment importers are now free tosource from countries and factories in the world that bringmost value to them. A number of sourcing practices, which hadappeared before the phase-out of quota system, have beenstrengthened with the phase-out and have to be addressed bygarment exporters to survive:

Importers have been sourcing from less countries and lessfactories, but with larger order, in selected countries toreduce overheads related to the sourcing. During 2002-2005,importers has reduced sourced countries from 53 to 26 andthis trend has been strengthened after 1 January 2005.

Retail prices, and therefore sourcing prices, of garmentare reducing because of (i) the appearance and growingimportance of discount mega-stores such as Wal Mart, (ii)the over-production of garment from developing countries.

2 http://www.emergingtextiles.com

That situation led to the reduction of export price of 10-20% in the last 3-5 years3.

Buyers have increasingly demanded shorter delivery time,smaller quantity per order because they have been trying tocut inventory, reduce sale-off to increase profit. Thistrend is also partly driven by the effectiveness ofcompanies such as Zara and Gap, which have placed mostemphasis on lean inventory and short lead time.

Product life cycle has shortened and style has changedfaster

International buyers have increasingly sourced directlyfrom garment manufacturers and circumvented buying agents.However, only garment manufacturers that are able toprovide services formerly offered by buying agents such asmaterial sourcing, shipping , designing and full-packageservice manufacturers benefit from this trend.

2.2 Vietnam’s Garment Export Performance

Vietnam’s garment export is estimated to be USD 4.8 billion in2005, an increase of 9.5% compared to the export value lastyear. This growth rate is the lowest level since 2002. Thereason is the phase-out of WTO Agreement on Textile andClothing (ATC) leading to a stronger competition from giantgarment exporters such as: China especially in earlier 2005when the country was not re-imposed quota, and India,Bangladesh, Sri Lanka and Pakistan etc... Moreover, Vietnam’sgarment export to US market is still subjected to quota.

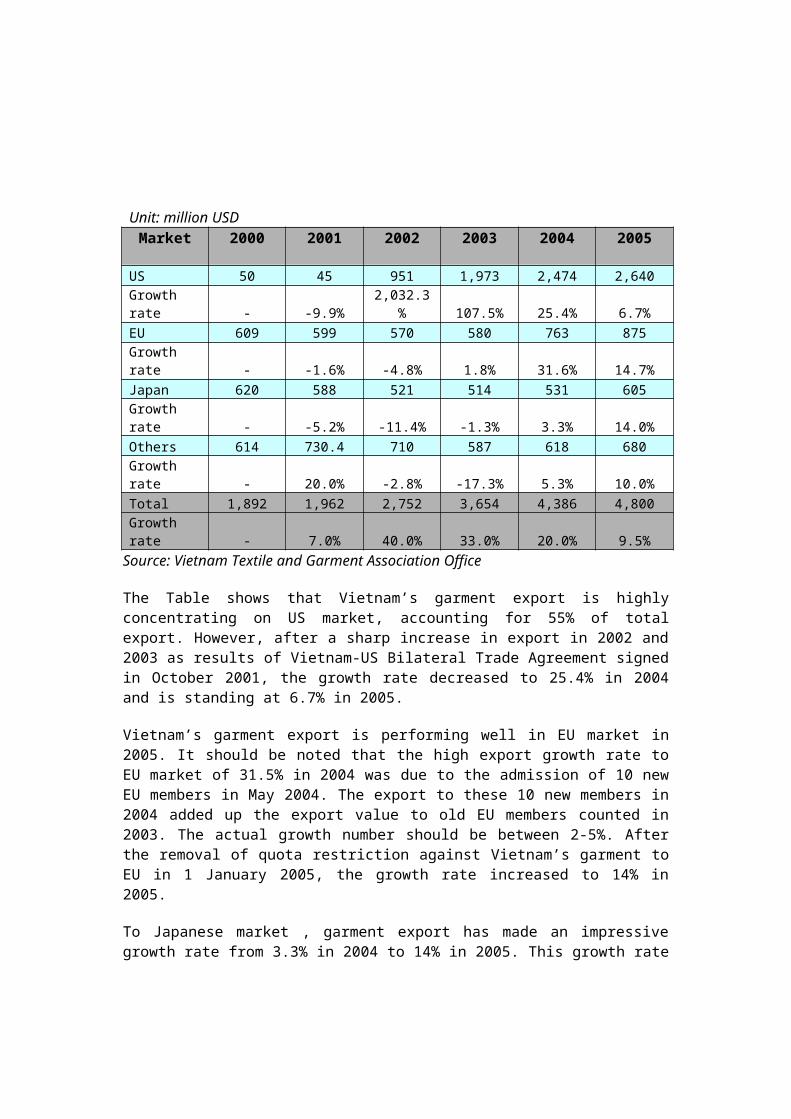

The three biggest garment importers from Vietnam are US, EUand Japan, which account for 55%, 20% and 13% of the totalgarment export value respectively. Vietnam’s exportperformance in these markets is presented in Table 1.

Table 1: Vietnam’s garment export performance from 2000 to 2005

3 Turning the Garment Industry Inside Out-Oxfam Hong Kong 2004

Unit: million USDMarket 2000 2001 2002 2003 2004 2005

US 50 45 951 1,973 2,474 2,640Growth rate - -9.9%

2,032.3% 107.5% 25.4% 6.7%

EU 609 599 570 580 763 875Growth rate - -1.6% -4.8% 1.8% 31.6% 14.7%Japan 620 588 521 514 531 605Growth rate - -5.2% -11.4% -1.3% 3.3% 14.0%Others 614 730.4 710 587 618 680Growth rate - 20.0% -2.8% -17.3% 5.3% 10.0%Total 1,892 1,962 2,752 3,654 4,386 4,800Growth rate - 7.0% 40.0% 33.0% 20.0% 9.5%

Source: Vietnam Textile and Garment Association Office

The Table shows that Vietnam’s garment export is highlyconcentrating on US market, accounting for 55% of totalexport. However, after a sharp increase in export in 2002 and2003 as results of Vietnam-US Bilateral Trade Agreement signedin October 2001, the growth rate decreased to 25.4% in 2004and is standing at 6.7% in 2005.

Vietnam’s garment export is performing well in EU market in2005. It should be noted that the high export growth rate toEU market of 31.5% in 2004 was due to the admission of 10 newEU members in May 2004. The export to these 10 new members in2004 added up the export value to old EU members counted in2003. The actual growth number should be between 2-5%. Afterthe removal of quota restriction against Vietnam’s garment toEU in 1 January 2005, the growth rate increased to 14% in2005.

To Japanese market , garment export has made an impressivegrowth rate from 3.3% in 2004 to 14% in 2005. This growth rate

resulted from stronger garment demand of Japanese market, thegeneral foreign trade growth between Japan and Vietnam and thefurther understanding of Japanese market by Vietnam’s garmentmanufacturers. In all, Vietnam’s proximity to Japanese marketand the consistant and high quality of Vietnam’s garment arethe two most important competitive advantages of Vietnam inthis market.

2.3 Vietnam’s Current Textile and Garment ExportValue Chain

Garment is a buyer-driven chain, meaning that internationalbuyers (retailers or brand name marketers) normally have adominant position in the value chain. This stems fromfollowing reasons:

Over-production of garment.Buyers can choose to buyapparel from several thousands of garment factories in manyof developing as well as developed countries. It isestimated that the world’s current garment supply capacityis twice higher than the demand;

Apparel retailers or brand name companies dictate fashiontrends in each fashion season by discussing and agreeingtogether on the colors and models in advance/ beforehand .

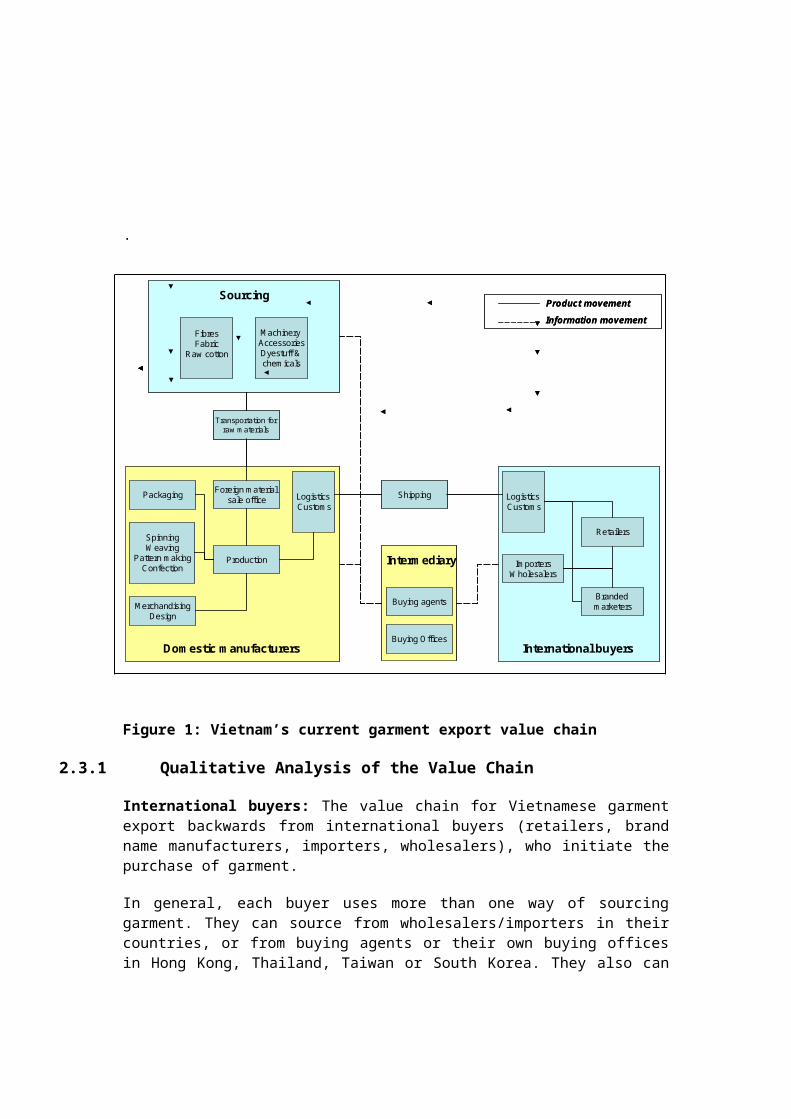

The garment value chain in Figure 1 below is typical forcurrent Vietnam garment export, which accounts approximately70% of export is in the form of CMT (Cut-Make-Trim). The valuechain includes four main components: international buyers,domestic manufacturers, sourcing and intermediary components.

.

Figure 1: Vietnam’s current garment export value chain

2.3.1 Qualitative Analysis of the Value Chain

International buyers: The value chain for Vietnamese garmentexport backwards from international buyers (retailers, brandname manufacturers, importers, wholesalers), who initiate thepurchase of garment.

In general, each buyer uses more than one way of sourcinggarment. They can source from wholesalers/importers in theircountries, or from buying agents or their own buying officesin Hong Kong, Thailand, Taiwan or South Korea. They also can

Production

SpinningW eaving

Pattern m akingConfection

M erchandisingDesign

M achinery AccessoriesDyestuff & chem icals

FibresFabric

Raw cotton

Packaging

Transportation for raw m aterials

Logistics Custom s

Branded m arketers

Retailers

Im portersW holesalers

Foreign m aterial sale office Shipping Logistics

Custom s

Buying agents

Buying Offices

Product movementInformation movement

Sourcing

Interm ediary

International buyersDom estic m anufacturers

Production

SpinningW eaving

Pattern m akingConfection

M erchandisingDesign

M achinery AccessoriesDyestuff & chem icals

FibresFabric

Raw cotton

Packaging

Transportation for raw m aterials

Logistics Custom s

Branded m arketers

Retailers

Im portersW holesalers

Foreign m aterial sale office Shipping Logistics

Custom s

Buying agents

Buying Offices

Product movementInformation movement

Sourcing

Interm ediary

International buyersDom estic m anufacturers

source directly from garment manufacturers when the garmentmanufacturers can provide full-package service4.

For Vietnam, international buyers normally source throughbuying agents and their own buying offices5.

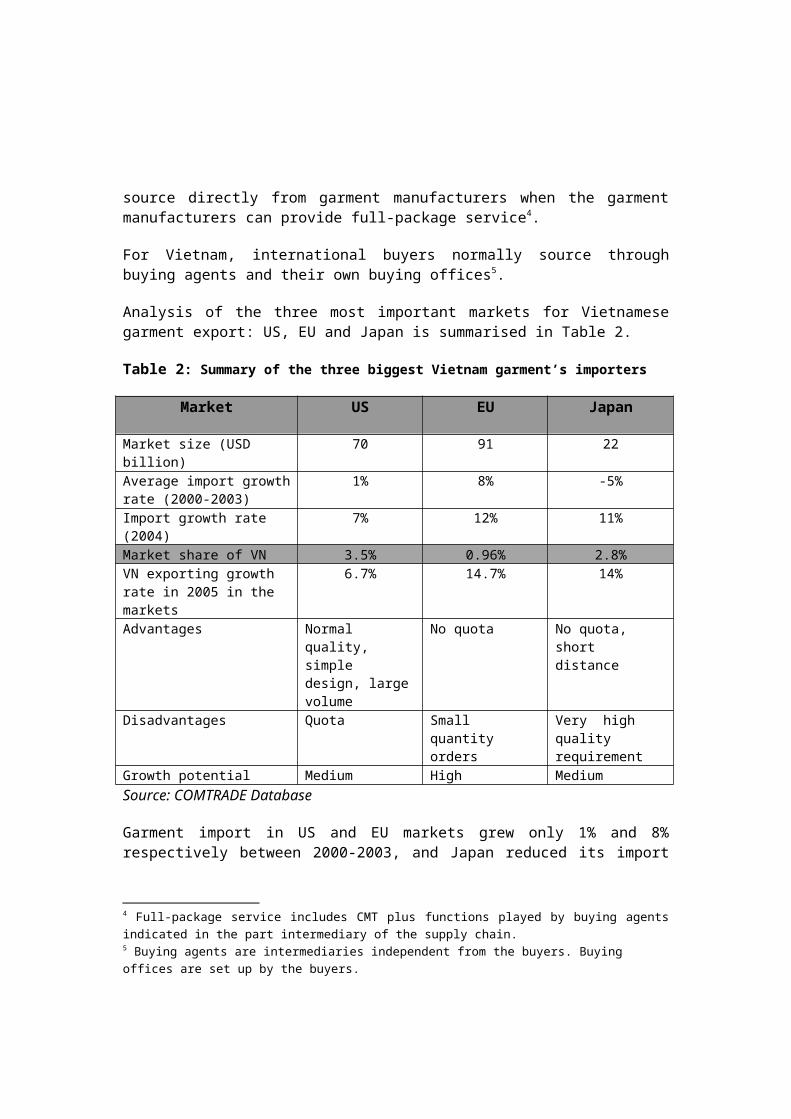

Analysis of the three most important markets for Vietnamesegarment export: US, EU and Japan is summarised in Table 2.

Table 2: Summary of the three biggest Vietnam garment’s importers

Market US EU Japan

Market size (USD billion)

70 91 22

Average import growthrate (2000-2003)

1% 8% -5%

Import growth rate (2004)

7% 12% 11%

Market share of VN 3.5% 0.96% 2.8%VN exporting growth rate in 2005 in the markets

6.7% 14.7% 14%

Advantages Normal quality, simple design, largevolume

No quota No quota, short distance

Disadvantages Quota Small quantity orders

Very high quality requirement

Growth potential Medium High MediumSource: COMTRADE Database

Garment import in US and EU markets grew only 1% and 8%respectively between 2000-2003, and Japan reduced its import

4 Full-package service includes CMT plus functions played by buying agentsindicated in the part intermediary of the supply chain.5 Buying agents are intermediaries independent from the buyers. Buying offices are set up by the buyers.

of garment during the same period. However, the trend waschanged as the growth rates of garment import increased to 7%in US market, 12% in EU market and 11% in Japanese market in2004.

Exporting of garment from Vietnam gains quite good marketshares in US and Japanese markets of 3.5% and 2.8%respectively. The market share of Vietnam in EU market is muchlower than in US and Japanese markets, accounting for 0.96% oftotal import.

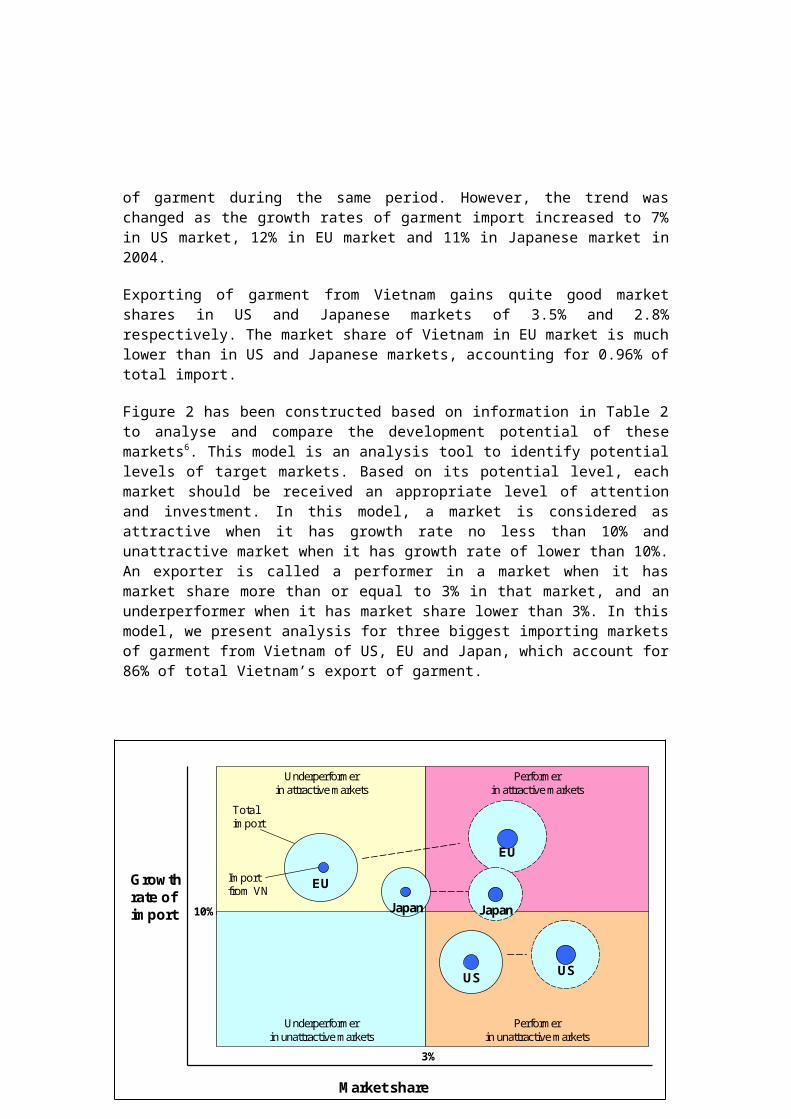

Figure 2 has been constructed based on information in Table 2to analyse and compare the development potential of thesemarkets6. This model is an analysis tool to identify potentiallevels of target markets. Based on its potential level, eachmarket should be received an appropriate level of attentionand investment. In this model, a market is considered asattractive when it has growth rate no less than 10% andunattractive market when it has growth rate of lower than 10%.An exporter is called a performer in a market when it hasmarket share more than or equal to 3% in that market, and anunderperformer when it has market share lower than 3%. In thismodel, we present analysis for three biggest importing marketsof garment from Vietnam of US, EU and Japan, which account for86% of total Vietnam’s export of garment.

6 This model is devised based on the Boston Consulting Group’s Growth Share Matrix and the General Electric’s Market Attractiveness Portfolio Strategies.

Underperformerin attractive markets

Performerin attractive markets

Underperformerin unattractive markets

Performerin unattractive markets

JapanEU

US

EU

Japan

M arket share

Grow th rate of im port

Total im port

Im port from VN

US

10%

3%

Figure 2: Development trajectories in the three biggest importers

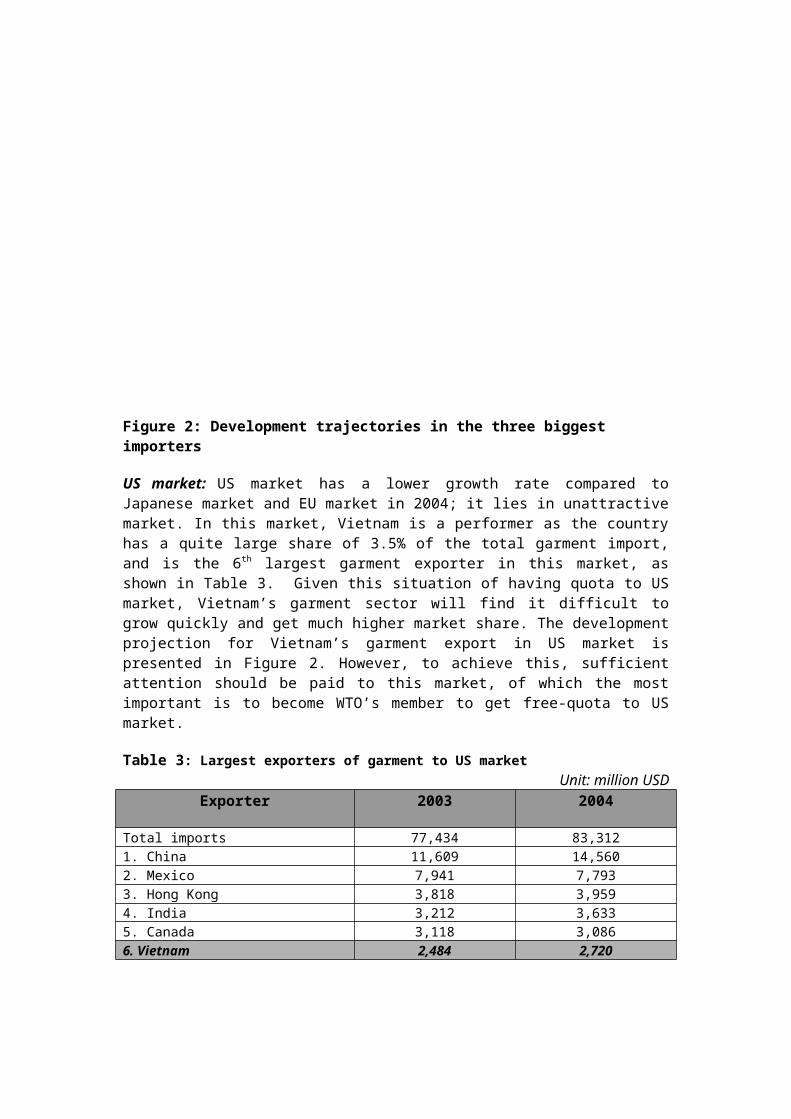

US market: US market has a lower growth rate compared toJapanese market and EU market in 2004; it lies in unattractivemarket. In this market, Vietnam is a performer as the countryhas a quite large share of 3.5% of the total garment import,and is the 6th largest garment exporter in this market, asshown in Table 3. Given this situation of having quota to USmarket, Vietnam’s garment sector will find it difficult togrow quickly and get much higher market share. The developmentprojection for Vietnam’s garment export in US market ispresented in Figure 2. However, to achieve this, sufficientattention should be paid to this market, of which the mostimportant is to become WTO’s member to get free-quota to USmarket.

Table 3: Largest exporters of garment to US marketUnit: million USD

Exporter 2003 2004

Total imports 77,434 83,3121. China 11,609 14,5602. Mexico 7,941 7,7933. Hong Kong 3,818 3,9594. India 3,212 3,6335. Canada 3,118 3,0866. Vietnam 2,484 2,720

7. Honduras 2,507 2,6788. Indonesia 2,376 2,6209. Pakistan 2,215 2,54610. Thailand 2,072 2,198Source: “Major Shippers Report”, US Department of Commerce, 2005

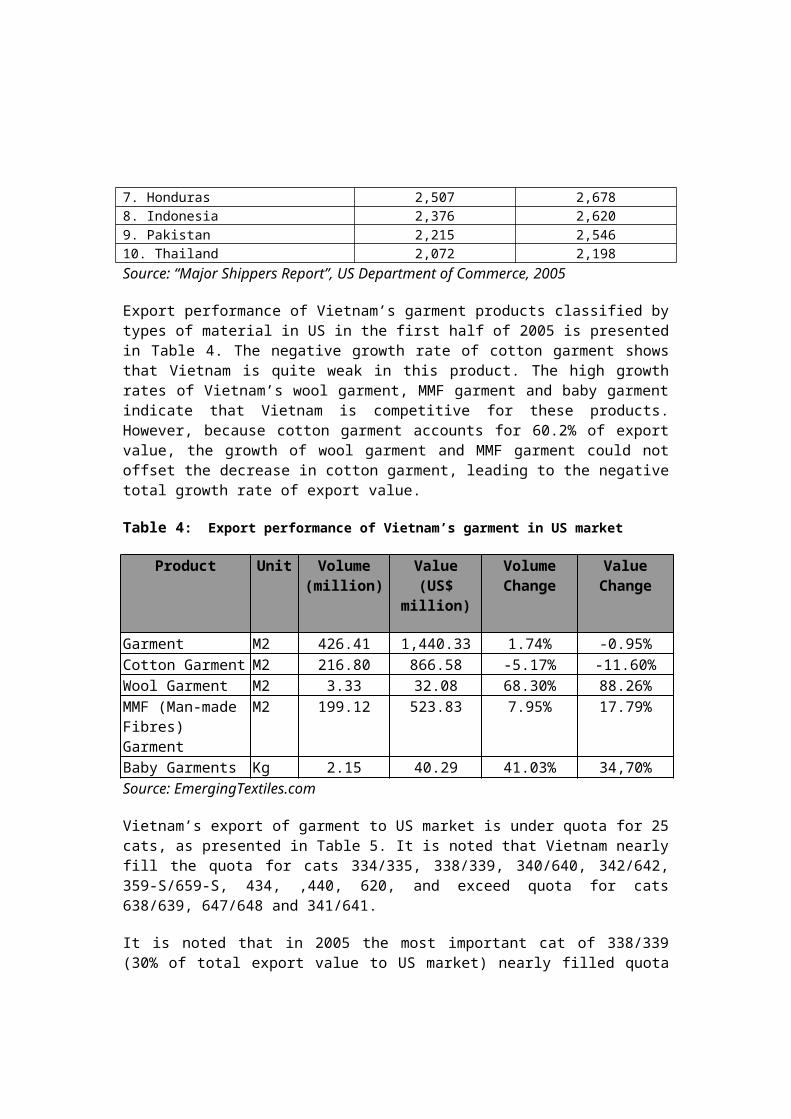

Export performance of Vietnam’s garment products classified bytypes of material in US in the first half of 2005 is presentedin Table 4. The negative growth rate of cotton garment showsthat Vietnam is quite weak in this product. The high growthrates of Vietnam’s wool garment, MMF garment and baby garmentindicate that Vietnam is competitive for these products.However, because cotton garment accounts for 60.2% of exportvalue, the growth of wool garment and MMF garment could notoffset the decrease in cotton garment, leading to the negativetotal growth rate of export value.

Table 4: Export performance of Vietnam’s garment in US market

Product Unit Volume(million)

Value(US$

million)

VolumeChange

ValueChange

Garment M2 426.41 1,440.33 1.74% -0.95%Cotton Garment M2 216.80 866.58 -5.17% -11.60%Wool Garment M2 3.33 32.08 68.30% 88.26%MMF (Man-made Fibres) Garment

M2 199.12 523.83 7.95% 17.79%

Baby Garments Kg 2.15 40.29 41.03% 34,70%Source: EmergingTextiles.com

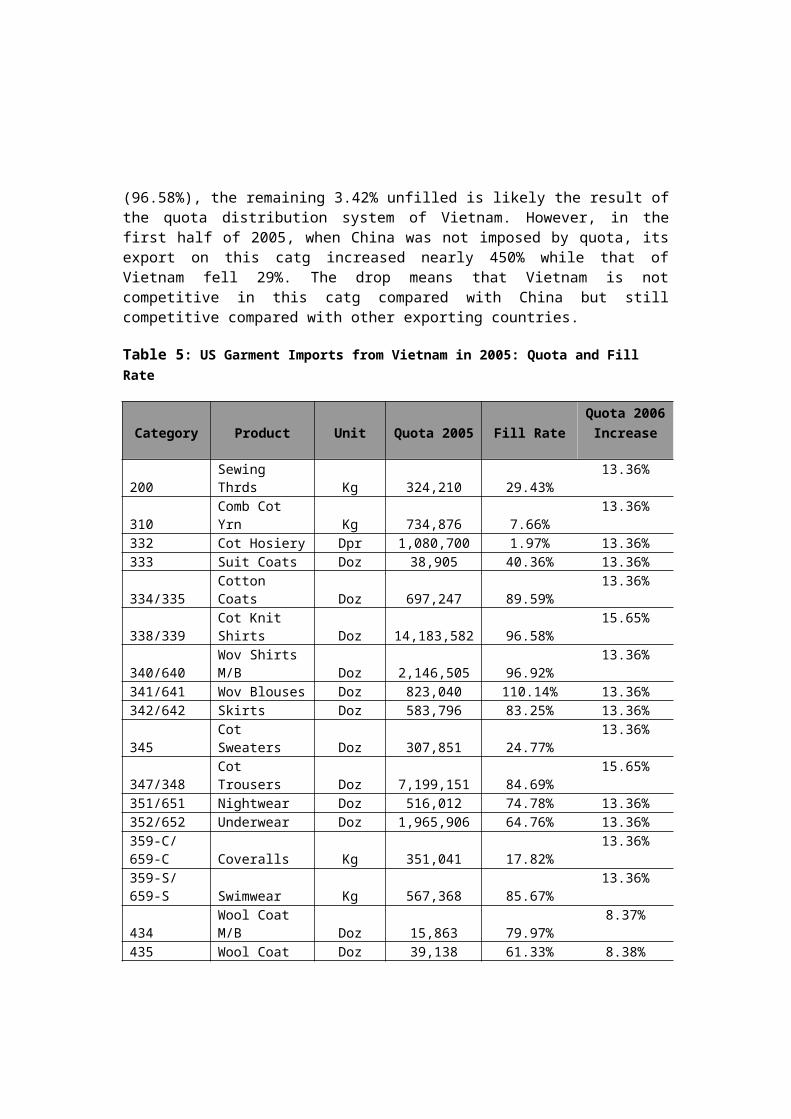

Vietnam’s export of garment to US market is under quota for 25cats, as presented in Table 5. It is noted that Vietnam nearlyfill the quota for cats 334/335, 338/339, 340/640, 342/642,359-S/659-S, 434, ,440, 620, and exceed quota for cats638/639, 647/648 and 341/641.

It is noted that in 2005 the most important cat of 338/339(30% of total export value to US market) nearly filled quota

(96.58%), the remaining 3.42% unfilled is likely the result ofthe quota distribution system of Vietnam. However, in thefirst half of 2005, when China was not imposed by quota, itsexport on this catg increased nearly 450% while that ofVietnam fell 29%. The drop means that Vietnam is notcompetitive in this catg compared with China but stillcompetitive compared with other exporting countries.

Table 5: US Garment Imports from Vietnam in 2005: Quota and Fill Rate

Category Product Unit Quota 2005 Fill RateQuota 2006Increase

200Sewing Thrds Kg 324,210 29.43%

13.36%

310Comb Cot Yrn Kg 734,876 7.66%

13.36%

332 Cot Hosiery Dpr 1,080,700 1.97% 13.36%333 Suit Coats Doz 38,905 40.36% 13.36%

334/335Cotton Coats Doz 697,247 89.59%

13.36%

338/339Cot Knit Shirts Doz 14,183,582 96.58%

15.65%

340/640Wov Shirts M/B Doz 2,146,505 96.92%

13.36%

341/641 Wov Blouses Doz 823,040 110.14% 13.36%342/642 Skirts Doz 583,796 83.25% 13.36%

345Cot Sweaters Doz 307,851 24.77%

13.36%

347/348Cot Trousers Doz 7,199,151 84.69%

15.65%

351/651 Nightwear Doz 516,012 74.78% 13.36%352/652 Underwear Doz 1,965,906 64.76% 13.36%359-C/659-C Coveralls Kg 351,041 17.82%

13.36%

359-S/659-S Swimwear Kg 567,368 85.67%

13.36%

434Wool Coat M/B Doz 15,863 79.97%

8.37%

435 Wool Coat Doz 39,138 61.33% 8.38%

W/G

440Wov Wool Shirts Doz 2,448 98.41%

8.37%

447Wool Trsrs M/B Doz 50,919 54.83%

8.37%

448Wool Trsr W/G Doz 31,335 34.68%

8.37%

620 MMF Wov Fab M2 6,877,575 77.08% 13.36%632 MMF Hosiery Dpr 540,350 4.90% 13.36%

638/639MMF Knit Shirt Doz 1,289,975 104.11%

13.36%

645/646MMF Sweaters Doz 208,578 48.17%

13.36%

647/648MMF Trousers Doz 2,097,655 101.18%

13.36%

Source: United States International Trade Commission

In 2005, all of the hot cats of 338/339, 340/640, 347/348,620, 638/639 and 647/648 nearly fully filled the quotas. Thegaps between the quotas and the actual exports of these catsare the results of the efficiencies of the quota allocationsystem7

This fact demonstrates that quota to US market poses a bigproblem to the sector. Moreover, there are some other problemsof the quota. Experiences in recent years have proved thatquota has a negative impact on both US importers andVietnamese exporters, especially before an annual agreement onquota is reached. The fact is that US importers are hesitatedto source from a country with uncertain quota pool. Moreover,exporters do not know how much quota Vietnam would receivefrom US and how much quota their manufacturing partnersreceive from Vietnamese government. Currently, the automaticquota allocation system (until 70% of the quota is filled)applied by Vietnamese Government in 2006 can only provide acertainty of some extent, thus, solve a small part of the

7 The government has applied automatic quota distribution system up to 70% of the quota in 2006, In the first 3 months of 2006, 5 hottest cats, including cat 338/339 and cat 347/348, have filled 70% of the quota, the government has stopped the automatic quota distribution for these cats.

problem. In this context, the accession into WTO is of greatimportance for Vietnam’s garment sector to promote its exportto US market.

Japan is the third biggest market for Vietnam’s garmentexport. The import growth rate of Japan was as low as -5% peryear on average between 2000-2003, but increases to 11% in2004. In 2005, Vietnam’s garment export to Japan increased to14% with export value equivalence ofUSD 605 million,accounting for 2.8% of Japan’s total garment import. Vietnamis the second largest garment exporter in Japanese marketafter China that occupies an import share of 90%. Vietnam’sgarment export is considered as an underperformer in theattractive market of Japan. However, as shown in Figure 2,the position of Japan is in the corner of the quadrangular“underperformer in attractive market”, it is still quitedifficult for Vietnam to increase its export quickly in thismarket and gain higher market share. Similar to US market, thedevelopment trajectory is only achieved when appropriateexport promotion programs are implemented.

EU is the most potential market for Vietnam’s garment export.On one hand, EU’s import growth rate is higher than those ofUS and Japanese markets, 12% compared to 7% of US market and11% of Japanese market in 2004. On the other hand, EU is thelargest garment importer in the world, accounting for 43% oftotal global garment import while garment import from Vietnamonly accounts for 0.96% of EU’s total import. Vietnam’sgarment export only ranks 22nd in EU market, as shown in Table4. Currently, Vietnam’s garment export is enjoying GSP(Generalised System of Preferences) in EU market and freequota system.

Table 6: Largest exporters of garment to EU market

Exporter 2002 2003 2005

Total imports 68,313 80,359 875,000

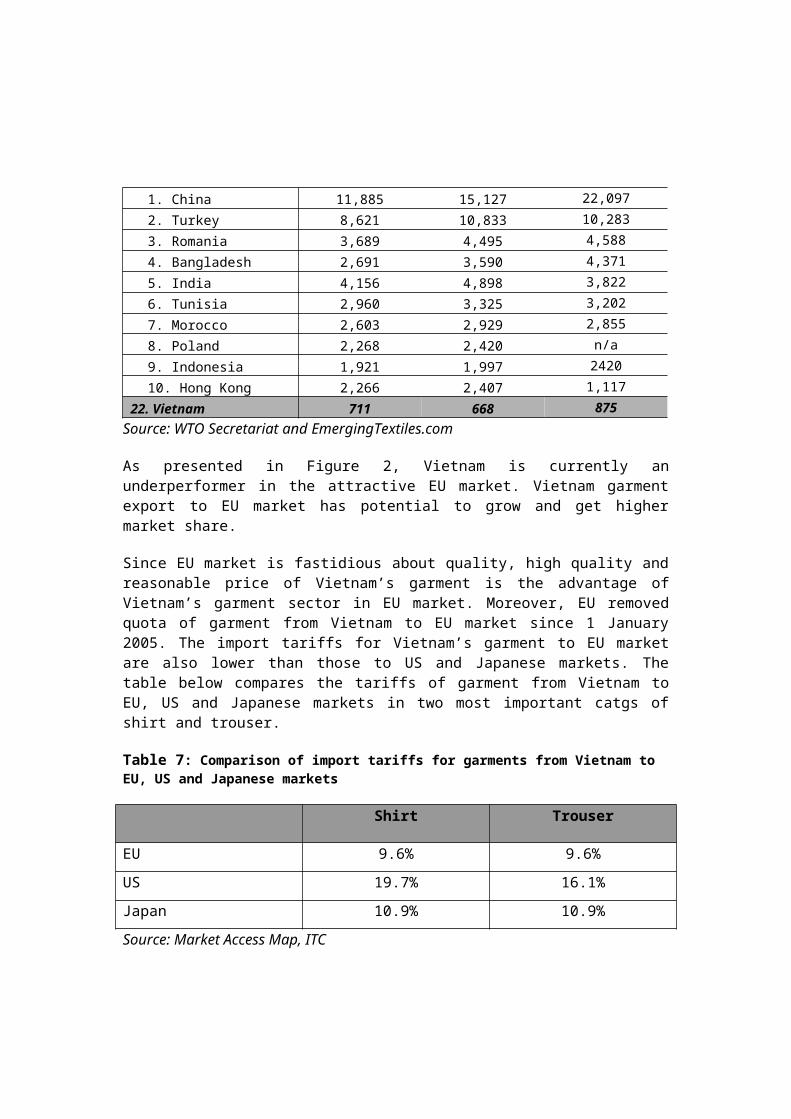

1. China 11,885 15,127 22,097 2. Turkey 8,621 10,833 10,283 3. Romania 3,689 4,495 4,588 4. Bangladesh 2,691 3,590 4,371 5. India 4,156 4,898 3,822 6. Tunisia 2,960 3,325 3,202 7. Morocco 2,603 2,929 2,855 8. Poland 2,268 2,420 n/a 9. Indonesia 1,921 1,997 2420 10. Hong Kong 2,266 2,407 1,117 22. Vietnam 711 668 875Source: WTO Secretariat and EmergingTextiles.com

As presented in Figure 2, Vietnam is currently anunderperformer in the attractive EU market. Vietnam garmentexport to EU market has potential to grow and get highermarket share.

Since EU market is fastidious about quality, high quality andreasonable price of Vietnam’s garment is the advantage ofVietnam’s garment sector in EU market. Moreover, EU removedquota of garment from Vietnam to EU market since 1 January2005. The import tariffs for Vietnam’s garment to EU marketare also lower than those to US and Japanese markets. Thetable below compares the tariffs of garment from Vietnam toEU, US and Japanese markets in two most important catgs ofshirt and trouser.

Table 7: Comparison of import tariffs for garments from Vietnam to EU, US and Japanese markets

Shirt Trouser

EU 9.6% 9.6%US 19.7% 16.1%Japan 10.9% 10.9%Source: Market Access Map, ITC

However, it is necessary to analyse EU buyers, to understandwhat have hindered export of Vietnam’s garment sector to EUmarket, and how to address the problems so as to improve theexport performance.

EU buyers are more concerned about quality than US buyers.They pay higher price and normally at lower quantity per orderthan US buyers. Also differently from US buyers, who providematerials to manufacturers, more than half of EU buyersrequire manufacturers to source materials and send materialsamples to them for approval. Finally, unlike US buyers, EUbuyers tend to stick to familiar garment providers.

After the VN-US Bilaterial Trade Agreement in 2001, Vietnam’sgarment enterprises did not pay due attention to the EU marketand shifted their focus to US market because although USbuyers pay lower price for garment, they require basic garmentat large volume and also provide materials for Vietnam’smanufacturers, which was convenient and suitable for largegarment manufacturers, especially the State-owned enterprises.At that time, Vietnam was also constrained by quota and theability to produce small order of garment for EU market.

With the phase-out of quota for Vietnam’s garment to EU marketsince early 2005 and increasing capacity of Vietnam’s garmentmanufacturers to meet smaller volume orders of EU buyers moreefficiently,8and Vietnam is aiming to move up to medium andhigh value garment market, EU is a suitable target market.

However, the sector needs to address a number of problemshindering its export to EU market, including the ability tosource materials effectively and efficiently in short andmedium term and the development of domestic materials sectorin long term. The sector also needs to get back the attentionof EU buyers.

8 The increasingly importance of foreign-invested garment enterprises (27% in 1998, 30% in 1999 and 35% in 2005 in terms of export value) and the development of medium-sized domestic enterprises give the sector higher flexibility in terms of order volume.

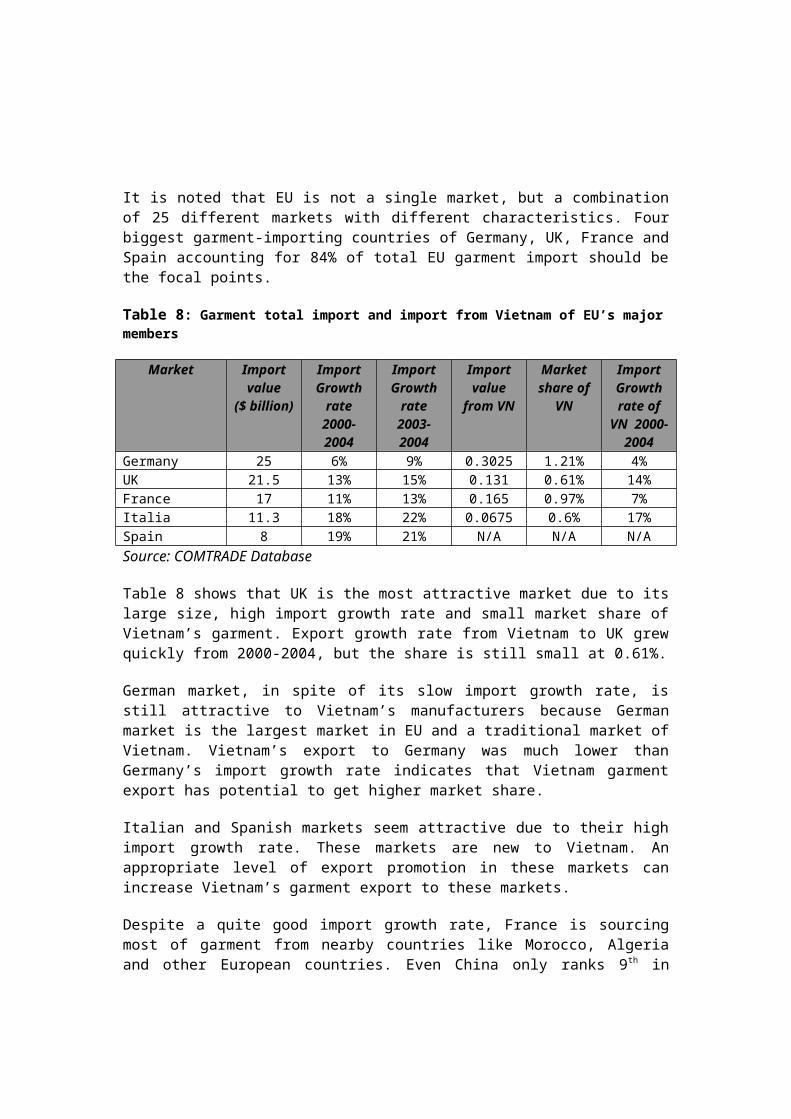

It is noted that EU is not a single market, but a combinationof 25 different markets with different characteristics. Fourbiggest garment-importing countries of Germany, UK, France andSpain accounting for 84% of total EU garment import should bethe focal points.

Table 8: Garment total import and import from Vietnam of EU’s majormembers

Market Importvalue

($ billion)

ImportGrowth

rate2000-2004

ImportGrowth

rate2003-2004

Importvalue

from VN

Marketshare of

VN

ImportGrowthrate of

VN 2000-2004

Germany 25 6% 9% 0.3025 1.21% 4%UK 21.5 13% 15% 0.131 0.61% 14%France 17 11% 13% 0.165 0.97% 7%Italia 11.3 18% 22% 0.0675 0.6% 17%Spain 8 19% 21% N/A N/A N/ASource: COMTRADE Database

Table 8 shows that UK is the most attractive market due to itslarge size, high import growth rate and small market share ofVietnam’s garment. Export growth rate from Vietnam to UK grewquickly from 2000-2004, but the share is still small at 0.61%.

German market, in spite of its slow import growth rate, isstill attractive to Vietnam’s manufacturers because Germanmarket is the largest market in EU and a traditional market ofVietnam. Vietnam’s export to Germany was much lower thanGermany’s import growth rate indicates that Vietnam garmentexport has potential to get higher market share.

Italian and Spanish markets seem attractive due to their highimport growth rate. These markets are new to Vietnam. Anappropriate level of export promotion in these markets canincrease Vietnam’s garment export to these markets.

Despite a quite good import growth rate, France is sourcingmost of garment from nearby countries like Morocco, Algeriaand other European countries. Even China only ranks 9th in

French market. Moreover, trade relationship between Vietnamand France is quite inactive.

EU buyers rarely source garment directly from Vietnam; theynormally order garment with buying agents or buying offices inthird countries like Hong Kong, Thailand, Taiwan, or SouthKorea. However, there are two-way communications between EUbuyers and buying offices, buying agents regarding garmentquality, delivery time of supplying countries. Therefore,garment export promotion to EU market needs to employ a two-pronged approach: promotion in EU market and promotion tobuying offices, buying agents. A number of considerations canbe used to promote export to EU market:

Collect, analyse and disseminate market information of EUmarket;

Promote sector corporation programs between Vitas andassociations in EU;

Strengthen direct contacts and sales to EU buyers;

Organize Vietnamese fashion week in EU with theparticipation of Vietnamese designers, and garmentmanufacturers; and

Invite EU industrial journalists to Vietnam to conductstudy and write articles about the industry to Europeanindustrial magazines.

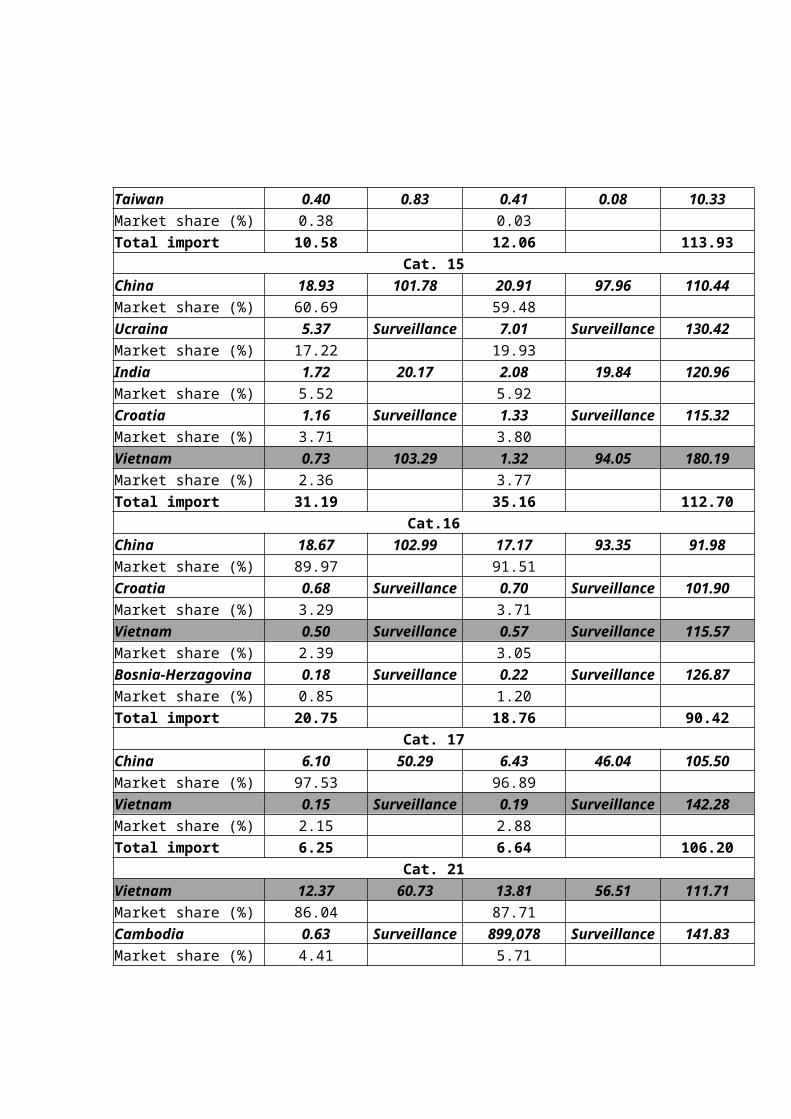

The table below shows products that Vietnam has competitive advantages in EU market.

Table 9: Competitive garment products of Vietnam in EU market

Exporters

2003 2004 % Exp

2004/2003Export (US$

million)% quotafill

Export (US$

million)% quotafill

Cat. 7

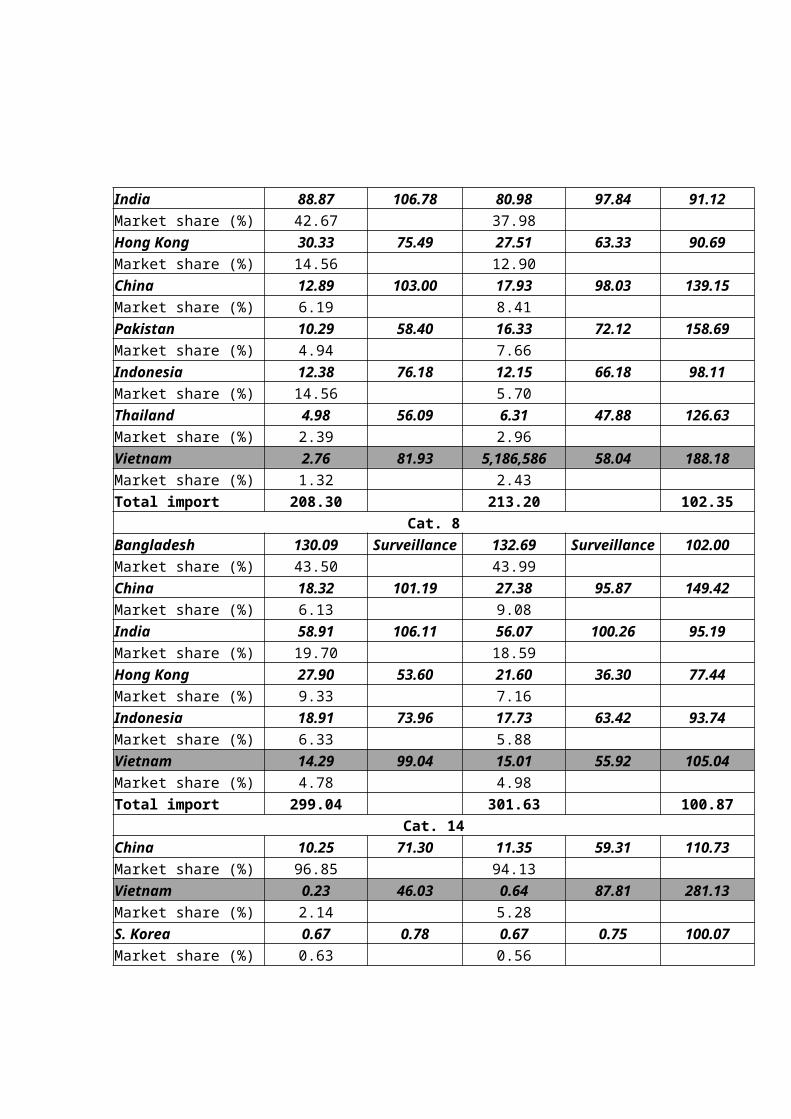

India 88.87 106.78 80.98 97.84 91.12Market share (%) 42.67 37.98Hong Kong 30.33 75.49 27.51 63.33 90.69Market share (%) 14.56 12.90China 12.89 103.00 17.93 98.03 139.15Market share (%) 6.19 8.41Pakistan 10.29 58.40 16.33 72.12 158.69Market share (%) 4.94 7.66Indonesia 12.38 76.18 12.15 66.18 98.11Market share (%) 14.56 5.70Thailand 4.98 56.09 6.31 47.88 126.63Market share (%) 2.39 2.96Vietnam 2.76 81.93 5,186,586 58.04 188.18Market share (%) 1.32 2.43Total import 208.30 213.20 102.35

Cat. 8Bangladesh 130.09 Surveillance 132.69 Surveillance 102.00Market share (%) 43.50 43.99China 18.32 101.19 27.38 95.87 149.42Market share (%) 6.13 9.08India 58.91 106.11 56.07 100.26 95.19Market share (%) 19.70 18.59Hong Kong 27.90 53.60 21.60 36.30 77.44Market share (%) 9.33 7.16Indonesia 18.91 73.96 17.73 63.42 93.74Market share (%) 6.33 5.88Vietnam 14.29 99.04 15.01 55.92 105.04Market share (%) 4.78 4.98Total import 299.04 301.63 100.87

Cat. 14China 10.25 71.30 11.35 59.31 110.73Market share (%) 96.85 94.13Vietnam 0.23 46.03 0.64 87.81 281.13Market share (%) 2.14 5.28S. Korea 0.67 0.78 0.67 0.75 100.07Market share (%) 0.63 0.56

Taiwan 0.40 0.83 0.41 0.08 10.33Market share (%) 0.38 0.03Total import 10.58 12.06 113.93

Cat. 15China 18.93 101.78 20.91 97.96 110.44Market share (%) 60.69 59.48Ucraina 5.37 Surveillance 7.01 Surveillance 130.42Market share (%) 17.22 19.93India 1.72 20.17 2.08 19.84 120.96Market share (%) 5.52 5.92Croatia 1.16 Surveillance 1.33 Surveillance 115.32Market share (%) 3.71 3.80Vietnam 0.73 103.29 1.32 94.05 180.19Market share (%) 2.36 3.77Total import 31.19 35.16 112.70

Cat.16China 18.67 102.99 17.17 93.35 91.98Market share (%) 89.97 91.51Croatia 0.68 Surveillance 0.70 Surveillance 101.90Market share (%) 3.29 3.71Vietnam 0.50 Surveillance 0.57 Surveillance 115.57Market share (%) 2.39 3.05Bosnia-Herzagovina 0.18 Surveillance 0.22 Surveillance 126.87Market share (%) 0.85 1.20Total import 20.75 18.76 90.42

Cat. 17China 6.10 50.29 6.43 46.04 105.50Market share (%) 97.53 96.89Vietnam 0.15 Surveillance 0.19 Surveillance 142.28Market share (%) 2.15 2.88Total import 6.25 6.64 106.20

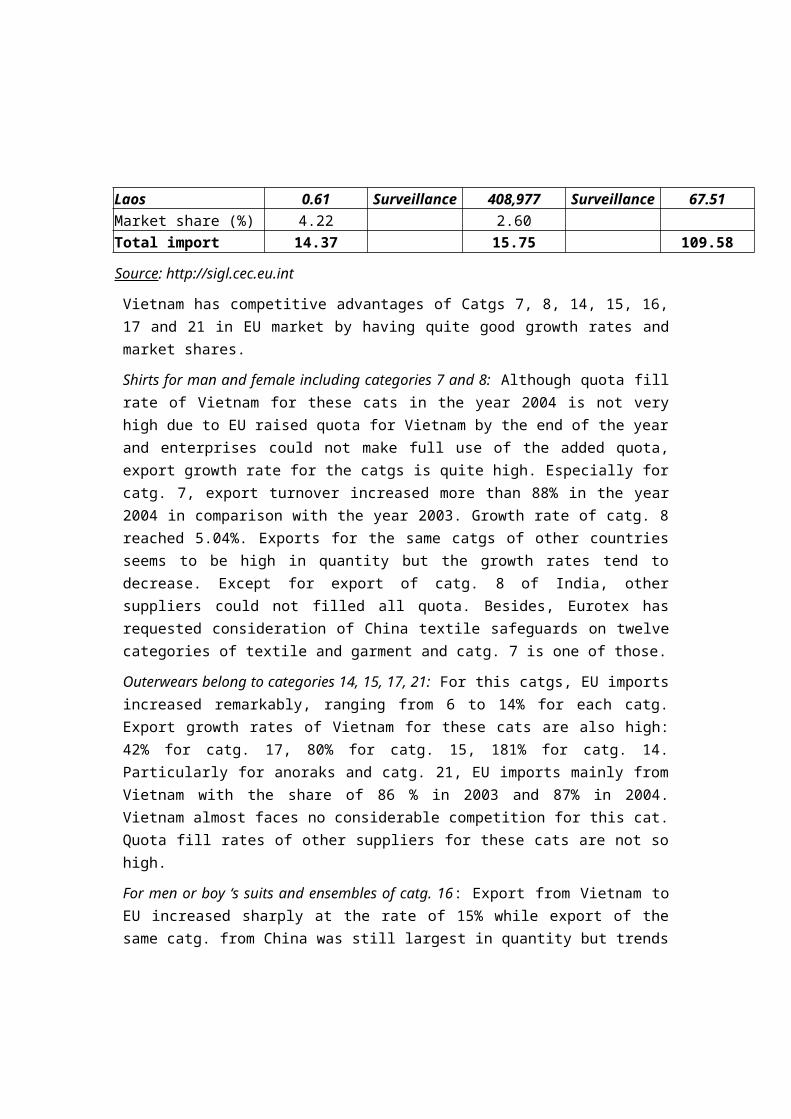

Cat. 21Vietnam 12.37 60.73 13.81 56.51 111.71Market share (%) 86.04 87.71Cambodia 0.63 Surveillance 899,078 Surveillance 141.83Market share (%) 4.41 5.71

Laos 0.61 Surveillance 408,977 Surveillance 67.51Market share (%) 4.22 2.60Total import 14.37 15.75 109.58

Source: http://sigl.cec.eu.int

Vietnam has competitive advantages of Catgs 7, 8, 14, 15, 16,17 and 21 in EU market by having quite good growth rates andmarket shares.

Shirts for man and female including categories 7 and 8: Although quota fillrate of Vietnam for these cats in the year 2004 is not veryhigh due to EU raised quota for Vietnam by the end of the yearand enterprises could not make full use of the added quota,export growth rate for the catgs is quite high. Especially forcatg. 7, export turnover increased more than 88% in the year2004 in comparison with the year 2003. Growth rate of catg. 8reached 5.04%. Exports for the same catgs of other countriesseems to be high in quantity but the growth rates tend todecrease. Except for export of catg. 8 of India, othersuppliers could not filled all quota. Besides, Eurotex hasrequested consideration of China textile safeguards on twelvecategories of textile and garment and catg. 7 is one of those.

Outerwears belong to categories 14, 15, 17, 21: For this catgs, EU importsincreased remarkably, ranging from 6 to 14% for each catg.Export growth rates of Vietnam for these cats are also high:42% for catg. 17, 80% for catg. 15, 181% for catg. 14.Particularly for anoraks and catg. 21, EU imports mainly fromVietnam with the share of 86 % in 2003 and 87% in 2004.Vietnam almost faces no considerable competition for this cat.Quota fill rates of other suppliers for these cats are not sohigh.

For men or boy ‘s suits and ensembles of catg. 16: Export from Vietnam toEU increased sharply at the rate of 15% while export of thesame catg. from China was still largest in quantity but trends

to fall (-8% in the year 2004 in comparison with the year2003).

Intermediary: Intermediary is an important link of garmentvalue chain of Vietnam’s garment export. Three main reasonscan be given to explain why international buyers sourcegarment from Vietnam mostly through intermediators. Firstly,few Vietnam’s garment manufacturers can provide services suchas material sourcing, designing, logistic arrangement andfull-package service for buyers, which are preconditions forbuyers to source directly from a country. Secondly, the longdistance between Vietnam and US or EU makes it ineffective interms of costs (quality control and travel expenses) andconvenience. Finally, many international buyers traditionallyrely on their agents instead of developing sourcing capacityin house.

In most cases, a buying office is responsible for a wholeregion, such as ASEAN region. For big garment exporters likeChina and India, a large international buyer usuallyestablishes an office in each country.

Buying agents normally conduct the following functions:

Quota holder seeking. This function was important underATC, but becomes less important after the removal of ATC on30 December 2004;

Identify most suitable suppliers for certain products interms of price, quality, timely delivery, and quotaavailability ;

Quality control for production;

Identify and contract with material providers;

Shipping arrangement for materials into manufacturer’scountry and for finished garment out of the country.

One of the most important functions of buying agents is tofind out which countries have available quota for eachcategories and coordinate sourcing activities so that they candeliver the garment customers demand. The phase-out of quotasystem since 1 January 2005 means that buying agents lose thisfunction and make the tasks of intermediators a little biteasier. Very few international buyers and buying agents haveestablished representative offices in Vietnam. Most of buyingagents and buying offices are based in Hong Kong, Thailand orTaiwan. To source garment from Vietnam, a representative frombuying agents and buying offices would fly to Vietnam toapprove factories, organize material purchase, quality controland shipment arrangement.

Vietnamese garment manufacturers: Currently, there areapproximately 1,500 garment manufacturers in Vietnam withproduction capacity of 2.25 billion converted men’s shirts peryear. Of these 1,500 manufacturers, 10% are state-owned, 65%are private and 25% are foreign-invested enterprises.

A large part Vietnam’s garment manufacturers are doing CMT forbuying agents and buying offices. The proportions of CMT andFOB are 70% and 30% respectively. The term "FOB" implies aform of garment production/distribution, and has practicallyno relationship with the one defined under Incoterm. The term“FOB” varies significantly in the forms of the actualcontractual relationships with foreign buyers, and they can beclassified into the following three types.

FOB Type I is where Vietnamese firms purchase input materialsfrom suppliers that are designated by foreign buyers. Thistype of export requires garment enterprises to take additionalresponsibilities of buying material from the designatedmaterial providers.

FOB Type II is where Vietnamese firms receive garment samplesfrom foreign buyers. In this type of production, Vietnamesefirms are provided with design and responsible for materialssourcing, production and transportation arrangement ofmaterials and completed products to buyer ports.

FOB Type III, or full-package service, is where the Vietnamesefirms initiate production of garments based on their owndesign, with no prior commitment of any kind from foreignbuyers. To be successful with this type of production,Vietnamese garment enterprises must be capable of materialsourcing, designing, marketing and logistics arrangement.

The classification shows that FOB Type I is not much differentfrom CMT except for paying for the materials designated bybuyers and transporting the materials to factories. The mostimportant requirement for moving up to FOB Type II is materialsourcing skill, while FOB Type III requires garment exportersto be responsible for everything before selling garment tobuyers. In fact, what differentiate CMT, FOB Type I, FOB TypeII and FOB Type III are the levels of services provided bysellers to buyers.

The reasons for the high proportion of CMT include:

Shortage of materials required inside the country, makingit difficult for manufacturers to find the requiredmaterials;

Weak material sourcing skills, including understanding allkinds of fabrics and yarns, including their characteristicsand uses, mill location and negotiation.

Sourcing materials require manufacturers to have enoughfinancial resources and be able to face risks related toun-usage of purchased materials resulting from possiblebroken-down contracts.;

Shortage of designing and marketing capacities required forFOB; and

Material sourcing is a profitable activity for buyingagents and buying offices.

In addition, Vietnamese garment manufacturers are mostly doingCMT for middle and low-end garment. In US market, CIF price

for garment imported from Vietnam is at the lowest level9.Reasons can be from designing skills to long lead time ofsourcing from Vietnam. Only basic, non-fashionable andnonsensitive garment is sourced from Vietnam at a lowprocessing price.

Not many enterprises in Vietnam can meet customer demandsregarding material sourcing, volume, quality, design, leadtime and price. This situation leads to two main options forexpanding the production capacities: (i) attracting moreinvestment, including FDI, into textile and garmentproduction, and (ii) strengthening the capacities of currentmanufacturers through improving soft skills such as materialsourcing, marketing, designing, etc.

Attracting new investment, especially FDI, into textile and garmentproduction:

Foreign-invested textile and garment enterprises have playedan important role in the development of Vietnam’s textile andgarment sector. At the end of 2004, there were 472 foreign-invested textile and garment enterprises, accounting for 25%of total number of enterprises. Foreign-invested manufacturersaccount for 35% of the total export value. Attracting FDI intotextile and garment sector is necessary to increase thesector’s production capacity, its competitiveness and exportvalue. FDI in textile and garment sector can increases theproduction capacity and be able to meet customer’s demandbecause:

FDI is a large source of capital to the sector, especiallyto the textile sub-sector which requires larger capitalinvestment;

Foreign-invested enterprises are equipped with more moderntechnology, better management skills and better technical

9 Cambodia’s garment industry: meeting the challenges of the post-quota environments, ADB, 2004

skills that enable them to achieve higher productivity andbetter quality; and

Foreign-invested enterprises normally already haverelationships with buyers, what takes newly-establisheddomestic enterprises time to develop.

However, the current shortage of labor in the textile andgarment sector must be solved to attract investment. Themajority of Vietnam’s textile and garment factories arelocated in urban areas or in the suburbs, particularly in HoChi Minh City and Hanoi. These factories currently have tocompete with other industries in the same areas for labor withrelatively low wages and hard working conditions. At the sametime, several rural areas in Vietnam with abundant low costlabor has not been exploited.

Strengthening the capacities of current manufacturers: This will bediscussed in detail in Section 2.4.

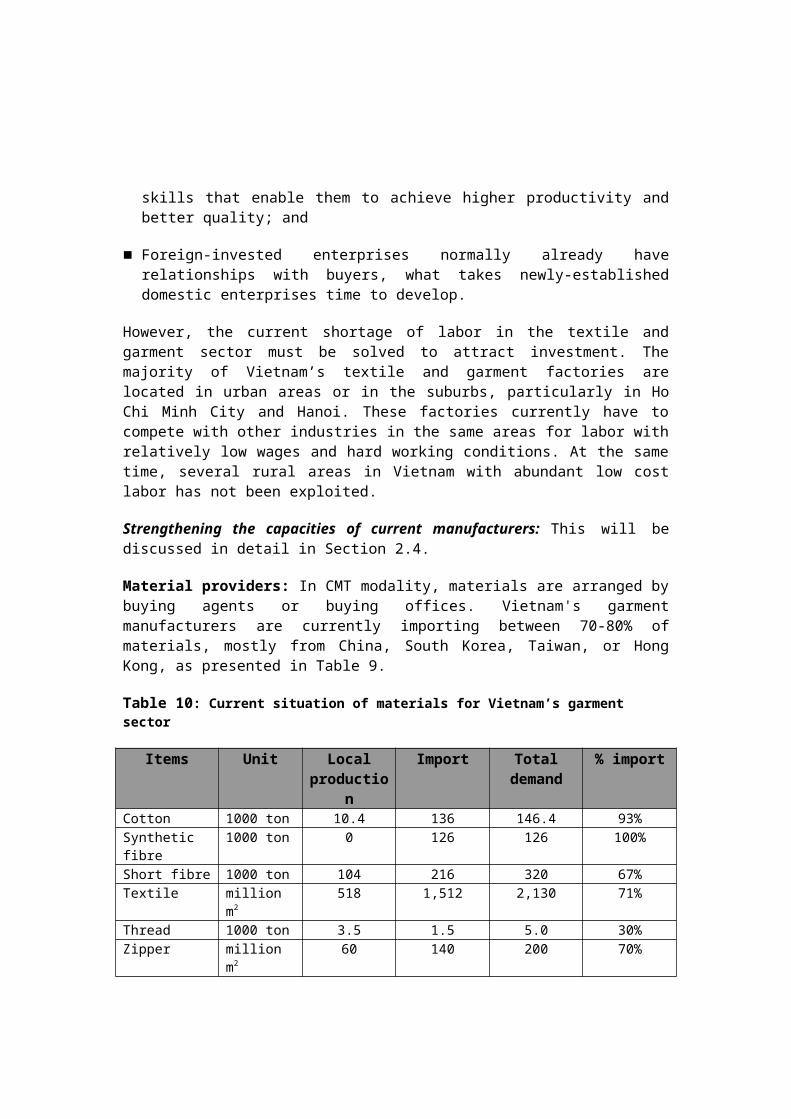

Material providers: In CMT modality, materials are arranged bybuying agents or buying offices. Vietnam's garmentmanufacturers are currently importing between 70-80% ofmaterials, mostly from China, South Korea, Taiwan, or HongKong, as presented in Table 9.

Table 10: Current situation of materials for Vietnam’s garment sector

Items Unit Localproductio

n

Import Totaldemand

% import

Cotton 1000 ton 10.4 136 146.4 93%Synthetic fibre

1000 ton 0 126 126 100%

Short fibre 1000 ton 104 216 320 67%Textile million

m2518 1,512 2,130 71%

Thread 1000 ton 3.5 1.5 5.0 30%Zipper million

m260 140 200 70%

Mex million m2

25 40 65 61%

Source: Assessment of Vietnam’s garment and textile sector after TCA, Vitas, 2005

Regarding domestic textile manufacturers, most of thesefactories are producing poor quality and simple kinds oftextile, focusing on cotton and cotton-PE textile; fewfactories produce wool and man-made fabric. These textiles arenot suitable for producing garment for export.

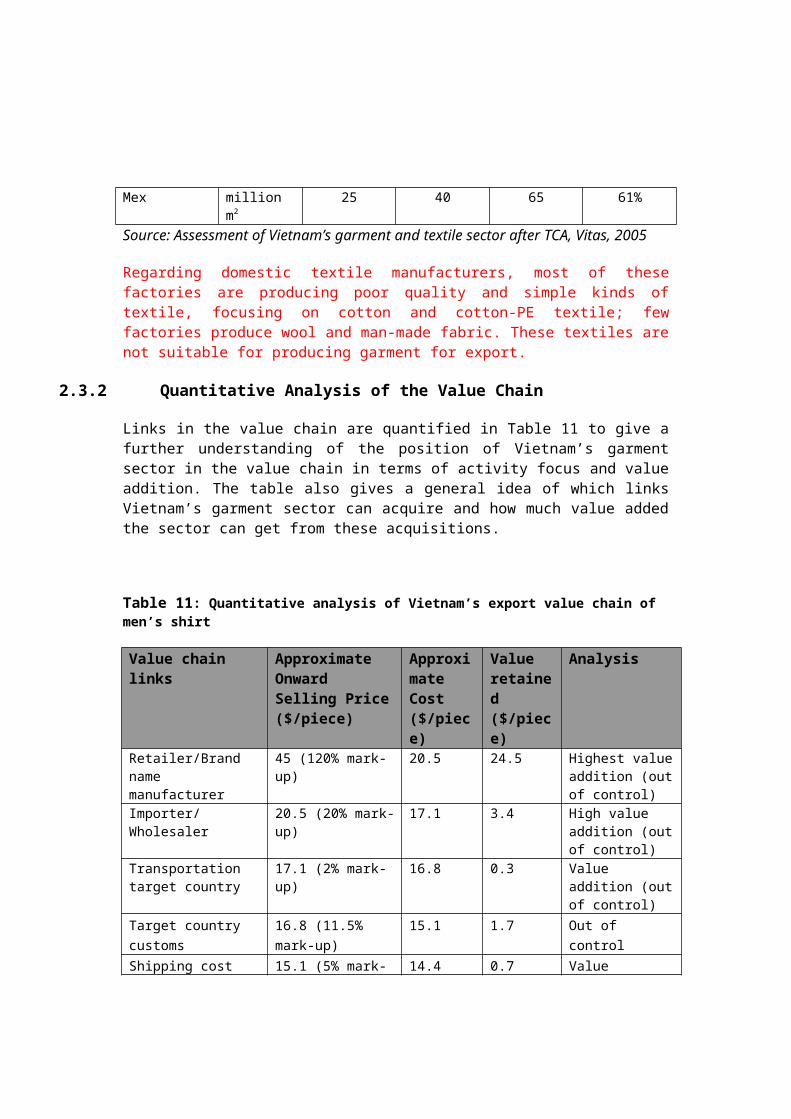

2.3.2 Quantitative Analysis of the Value Chain

Links in the value chain are quantified in Table 11 to give afurther understanding of the position of Vietnam’s garmentsector in the value chain in terms of activity focus and valueaddition. The table also gives a general idea of which linksVietnam’s garment sector can acquire and how much value addedthe sector can get from these acquisitions.

Table 11: Quantitative analysis of Vietnam’s export value chain of men’s shirt

Value chain links

Approximate Onward Selling Price($/piece)

Approximate Cost ($/piece)

Value retained ($/piece)

Analysis

Retailer/Brand name manufacturer

45 (120% mark-up)

20.5 24.5 Highest valueaddition (outof control)

Importer/Wholesaler

20.5 (20% mark-up)

17.1 3.4 High value addition (outof control)

Transportation target country

17.1 (2% mark-up)

16.8 0.3 Value addition (outof control)

Target country customs

16.8 (11.5% mark-up)

15.1 1.7 Out of control

Shipping cost 15.1 (5% mark- 14.4 0.7 Value

up) additionLocal transportation

14.4 (1% mark-up)

14.3 0.1 Value addition

Local customs (duty)

14.3 (0.5% mark-up)

14.2 0.1 Out of control

Buying Agent 14.2 (10-15% mark-up, incl. QC)

12.3 1.9 High value addition (Leakage)

Production Process (CMT)

12.3 (8% mark-up) 11.4 0.9 Low value addition of CMT

Material sourcing (Foreign Material sales office)

11.4 (20% mark-up)

9.5 1.9 High value addition (Leakage)

Transportation for raw materials

9.5 (2.5% mark-up)

9.3 0.2 Value addition

Material manufacturing

9.3 (10%) 8.5 0.8 High value addition (Leakage)

Fabric Accessories Fibres Cotton Machinery Spinning Weaving Confection Pattern making

Although the numbers in the table are only roughly precise,they reveal that Vietnam’s garment sector is focusing on oneof the lowest value-added activities of CMT with low mark-upof 8%. A number of more profitable activities of buying agent,material sourcing and material manufacturing are indicated as“Leakage” in the table because they are currently beingcarried out by foreign companies, while they are possibly doneby domestic companies.

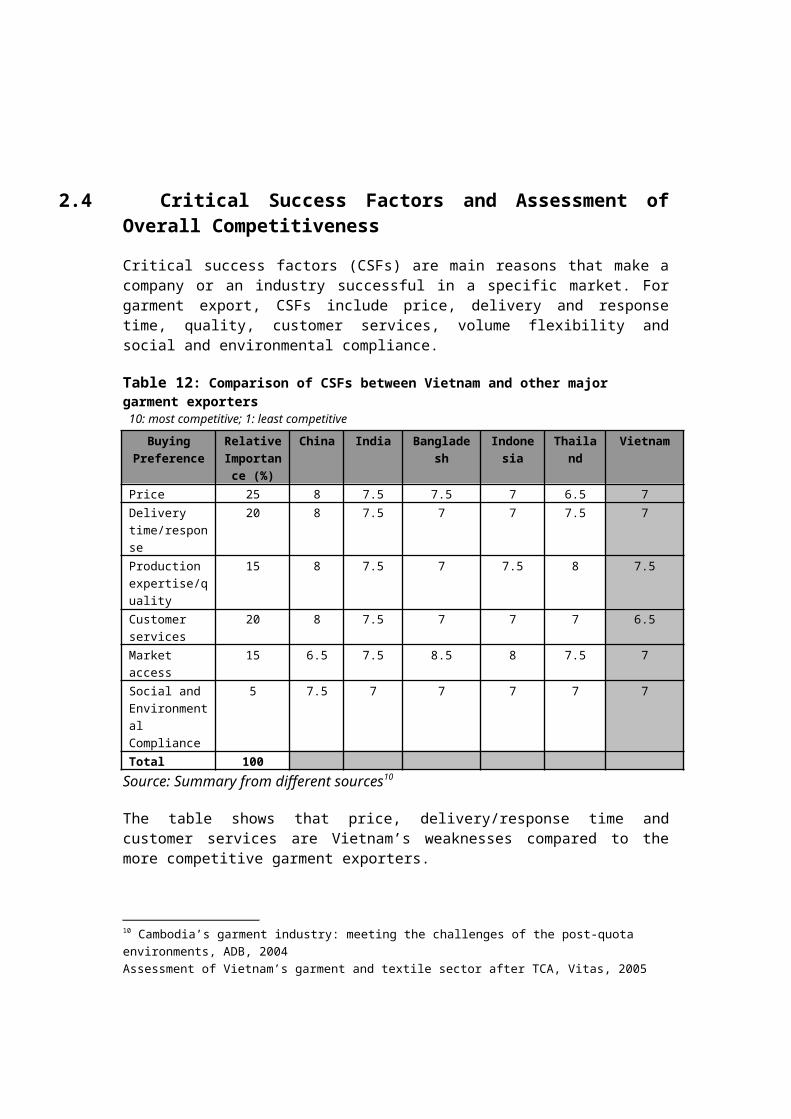

2.4 Critical Success Factors and Assessment ofOverall Competitiveness

Critical success factors (CSFs) are main reasons that make acompany or an industry successful in a specific market. Forgarment export, CSFs include price, delivery and responsetime, quality, customer services, volume flexibility andsocial and environmental compliance.

Table 12: Comparison of CSFs between Vietnam and other major garment exporters10: most competitive; 1: least competitive

BuyingPreference

RelativeImportance (%)

China India Bangladesh

Indonesia

Thailand

Vietnam

Price 25 8 7.5 7.5 7 6.5 7Delivery time/response

20 8 7.5 7 7 7.5 7

Production expertise/quality

15 8 7.5 7 7.5 8 7.5

Customer services

20 8 7.5 7 7 7 6.5

Market access

15 6.5 7.5 8.5 8 7.5 7

Social and Environmental Compliance

5 7.5 7 7 7 7 7

Total 100Source: Summary from different sources10

The table shows that price, delivery/response time andcustomer services are Vietnam’s weaknesses compared to themore competitive garment exporters.

10 Cambodia’s garment industry: meeting the challenges of the post-quota environments, ADB, 2004Assessment of Vietnam’s garment and textile sector after TCA, Vitas, 2005

China, India, and Indonesia all enjoy the advantage of adomestically developed textile industry and they are netexporters of textile. This advantage enables these countriesto have lower material costs, shorter delivery time and bettercustomer services than countries that need to import materialslike Vietnam, Bangladesh and Thailand.

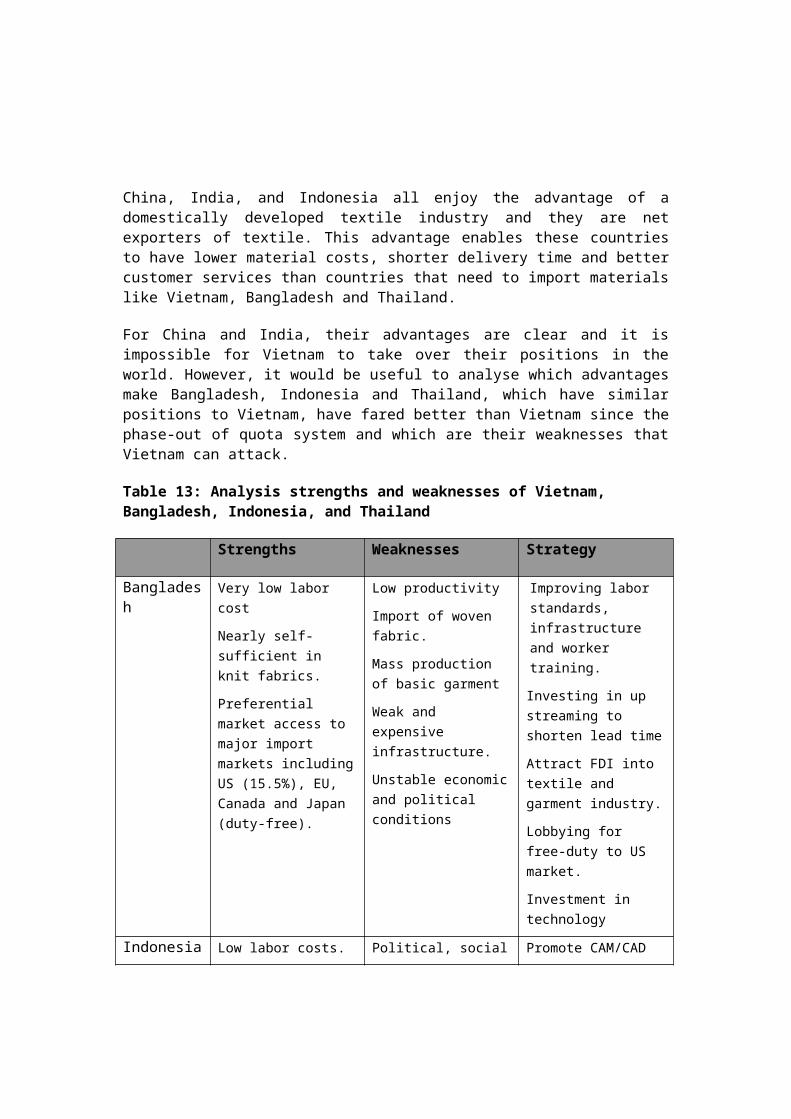

For China and India, their advantages are clear and it isimpossible for Vietnam to take over their positions in theworld. However, it would be useful to analyse which advantagesmake Bangladesh, Indonesia and Thailand, which have similarpositions to Vietnam, have fared better than Vietnam since thephase-out of quota system and which are their weaknesses thatVietnam can attack.

Table 13: Analysis strengths and weaknesses of Vietnam, Bangladesh, Indonesia, and Thailand

Strengths Weaknesses Strategy

Bangladesh

Very low labor cost

Nearly self-sufficient in knit fabrics.

Preferential market access to major import markets includingUS (15.5%), EU, Canada and Japan (duty-free).

Low productivity

Import of woven fabric.

Mass production of basic garment

Weak and expensive infrastructure.

Unstable economicand political conditions

Improving labor standards, infrastructure and worker training.

Investing in up streaming to shorten lead time

Attract FDI into textile and garment industry.

Lobbying for free-duty to US market.

Investment in technology

Indonesia Low labor costs. Political, social Promote CAM/CAD

Huge manufacturing base for raw materials.

Free-duty to EU market.

and Economic unrests.

Out-dated technology in textile and garment industry

Modernize old machine.

Move toward high value-added, high-fashion products.

Investment in upstreaming, especially in synthetic fibres

Thailand Good quality garment

Quite high productivity

Good designing skills

High labor costs

Shortage of labor

Still reliance onimported high-quality materials

Investment in fashion

Focus on high-endgarment

Investment in upstreaming, especially synthetic fibres.

Vietnam Reputation for good quality garment

Low – cost but skilful and hard-working labor

Potential domestic market

Stable and high economic growth

Quite large number of good designers outsidegarment enterprises

Shortage of laborin urban areas and suburbs.

Shortage of domestic materials

Focus on CMT, fewadditional services offered.

No direct shipment to majormarkets.

Quota to US market

Investment in upstreaming

Upgrading from CMT to FOB

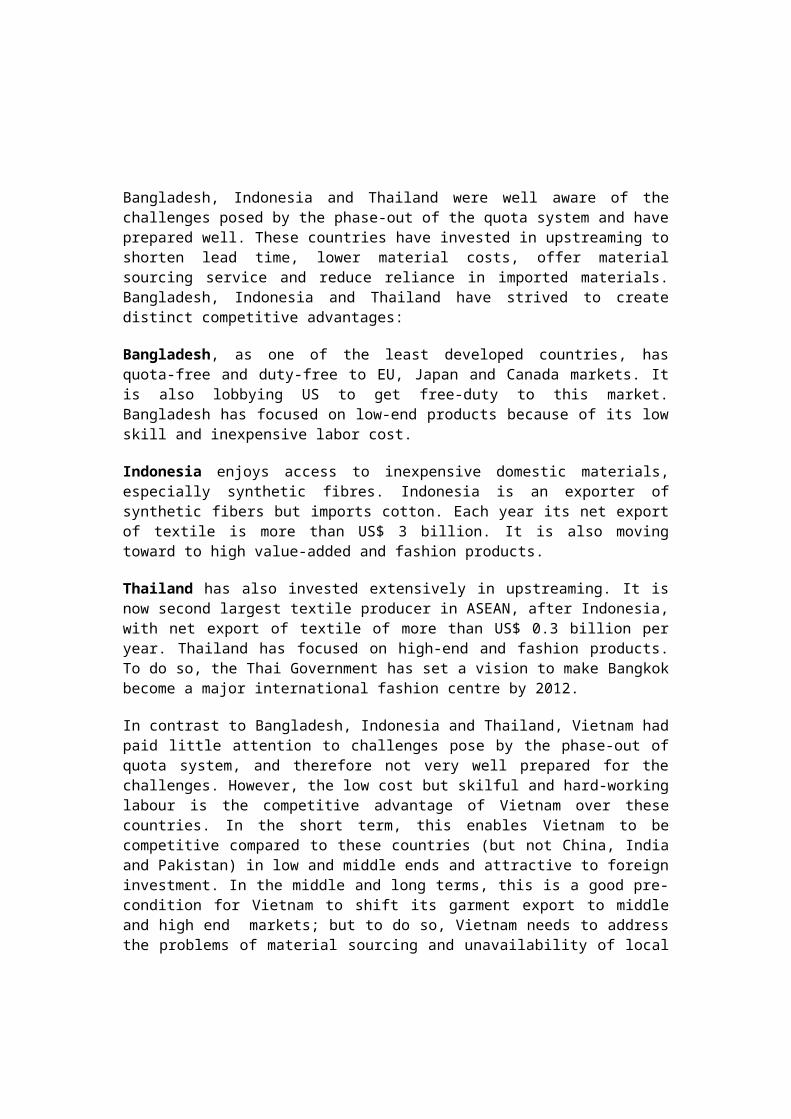

Bangladesh, Indonesia and Thailand were well aware of thechallenges posed by the phase-out of the quota system and haveprepared well. These countries have invested in upstreaming toshorten lead time, lower material costs, offer materialsourcing service and reduce reliance in imported materials.Bangladesh, Indonesia and Thailand have strived to createdistinct competitive advantages:

Bangladesh, as one of the least developed countries, hasquota-free and duty-free to EU, Japan and Canada markets. Itis also lobbying US to get free-duty to this market.Bangladesh has focused on low-end products because of its lowskill and inexpensive labor cost.

Indonesia enjoys access to inexpensive domestic materials,especially synthetic fibres. Indonesia is an exporter ofsynthetic fibers but imports cotton. Each year its net exportof textile is more than US$ 3 billion. It is also movingtoward to high value-added and fashion products.

Thailand has also invested extensively in upstreaming. It isnow second largest textile producer in ASEAN, after Indonesia,with net export of textile of more than US$ 0.3 billion peryear. Thailand has focused on high-end and fashion products.To do so, the Thai Government has set a vision to make Bangkokbecome a major international fashion centre by 2012.

In contrast to Bangladesh, Indonesia and Thailand, Vietnam hadpaid little attention to challenges pose by the phase-out ofquota system, and therefore not very well prepared for thechallenges. However, the low cost but skilful and hard-workinglabour is the competitive advantage of Vietnam over thesecountries. In the short term, this enables Vietnam to becompetitive compared to these countries (but not China, Indiaand Pakistan) in low and middle ends and attractive to foreigninvestment. In the middle and long terms, this is a good pre-condition for Vietnam to shift its garment export to middleand high end markets; but to do so, Vietnam needs to addressthe problems of material sourcing and unavailability of local

materials, lack of cooperation between designers and garmententerprises, and marketing skills.

2.4.1 Price

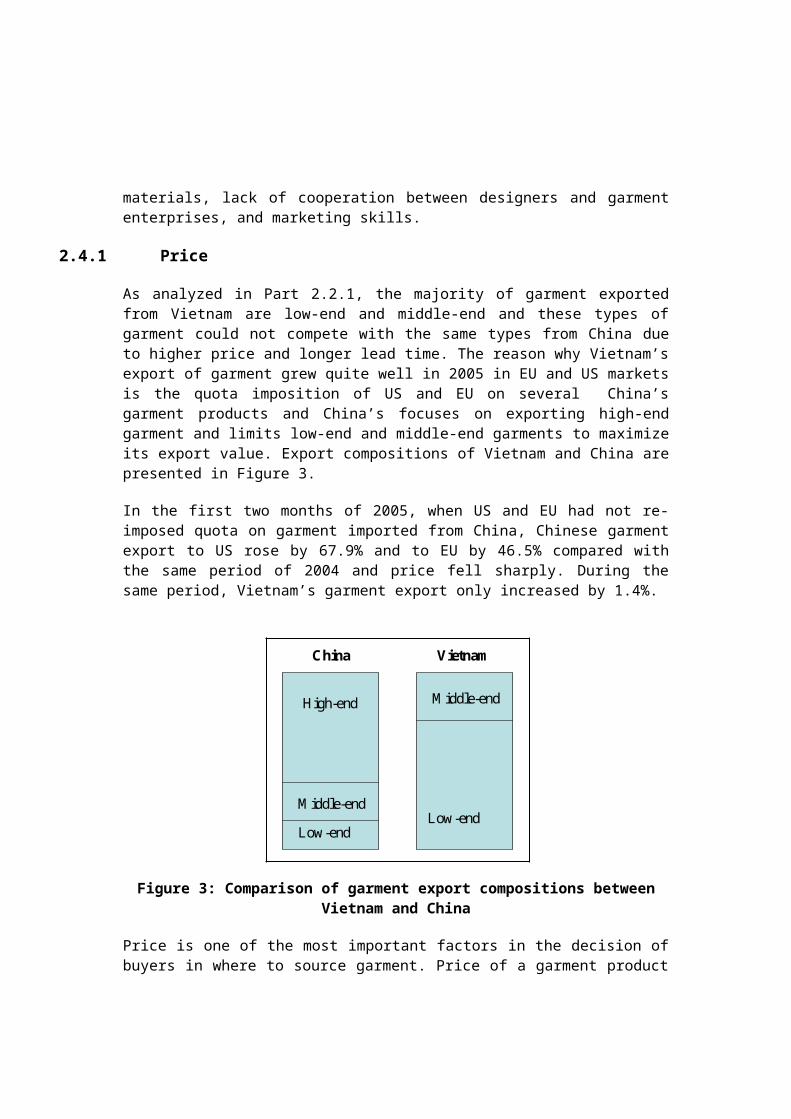

As analyzed in Part 2.2.1, the majority of garment exportedfrom Vietnam are low-end and middle-end and these types ofgarment could not compete with the same types from China dueto higher price and longer lead time. The reason why Vietnam’sexport of garment grew quite well in 2005 in EU and US marketsis the quota imposition of US and EU on several China’sgarment products and China’s focuses on exporting high-endgarment and limits low-end and middle-end garments to maximizeits export value. Export compositions of Vietnam and China arepresented in Figure 3.

In the first two months of 2005, when US and EU had not re-imposed quota on garment imported from China, Chinese garmentexport to US rose by 67.9% and to EU by 46.5% compared withthe same period of 2004 and price fell sharply. During thesame period, Vietnam’s garment export only increased by 1.4%.

Figure 3: Comparison of garment export compositions betweenVietnam and China

Price is one of the most important factors in the decision ofbuyers in where to source garment. Price of a garment product

High-end

M iddle-endLow-end

M iddle-end

Low-end

China Vietnam

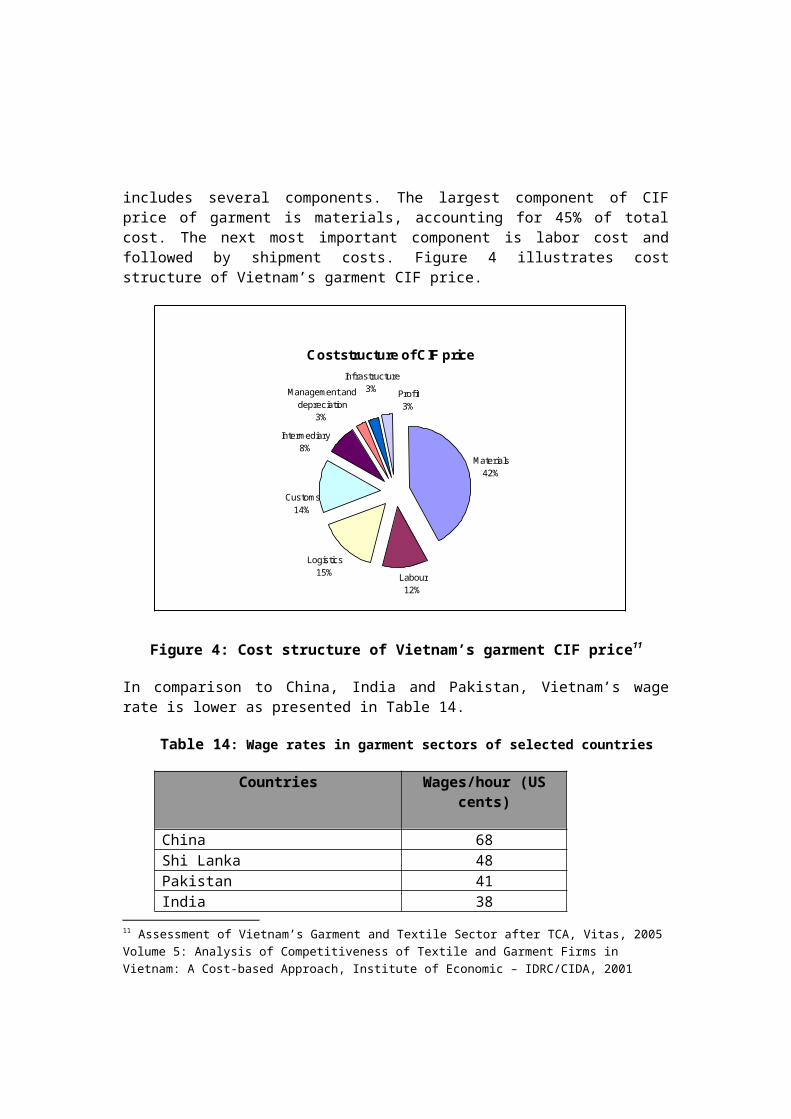

includes several components. The largest component of CIFprice of garment is materials, accounting for 45% of totalcost. The next most important component is labor cost andfollowed by shipment costs. Figure 4 illustrates coststructure of Vietnam’s garment CIF price.

Figure 4: Cost structure of Vietnam’s garment CIF price11

In comparison to China, India and Pakistan, Vietnam’s wagerate is lower as presented in Table 14.

Table 14: Wage rates in garment sectors of selected countries

Countries Wages/hour (UScents)

China 68Shi Lanka 48Pakistan 41India 38

11 Assessment of Vietnam’s Garment and Textile Sector after TCA, Vitas, 2005Volume 5: Analysis of Competitiveness of Textile and Garment Firms in Vietnam: A Cost-based Approach, Institute of Economic – IDRC/CIDA, 2001

Cost structure of CIF price

Materials42%

Labour12%

Logistics15%

Intermediary8%

Customs14%

Management and depreciation

3%

Profit3%

Infrastructure3%

Indonesia 27Vietnam 26Bangladesh 18-25Cambodia 23Laos 12.5Source: Stuart-Smith, Dayal, Brimble and Holl, 2004

However, Vietnam’s production cost is higher than those ofChina and India due to the following reasons:

Imported materials: Transportation, customs, capital andtransaction costs related to importing materials intoVietnam make material costs in Vietnam higher than those inChina and India. Cost for material inputs in Vietnam isapproximately 25-35% higher than in China. As materialcosts account for a large proportion of 45% in total cost,this is a big disadvantage for Vietnamese garment sector.

Labor productivity: In general, the labor productivity isbetween 50 - 60% that of China but slightly higher thanIndia’s and Bangladesh’s. The reasons could include poorproduction management, less specialization, lowworkemanship skill (high turnover due to low income),older sewing machine and lack of IT application.

2.4.2 Long lead time

Lead time has become increasingly important to the decision ofinternational buyers. On the one hand, retailers and brandname marketers are releasing more varieties of clothingproducts at lower volume each season. On the other hand, theyare growing adopting “lean retailing”, meaning that retailersand brand manufacturers are trying to cut inventory and reducesale-off to increase profit. These trends demand garmentsuppliers to ship garment at a shorter time.

Table 15: Lead time in clothing industry for Vietnam and selected competitors

Circular knit garments

Wovengarments

50-60 days 60-70 days 70-80 days 90-120 days

40-60 days China50-70 days India60-90 days Malaysia

ThailandIndonesiaVietnam

90-120 days Bangladesh CambodiaSource: Export Potential Assessment in Vietnam-WTC, 2005

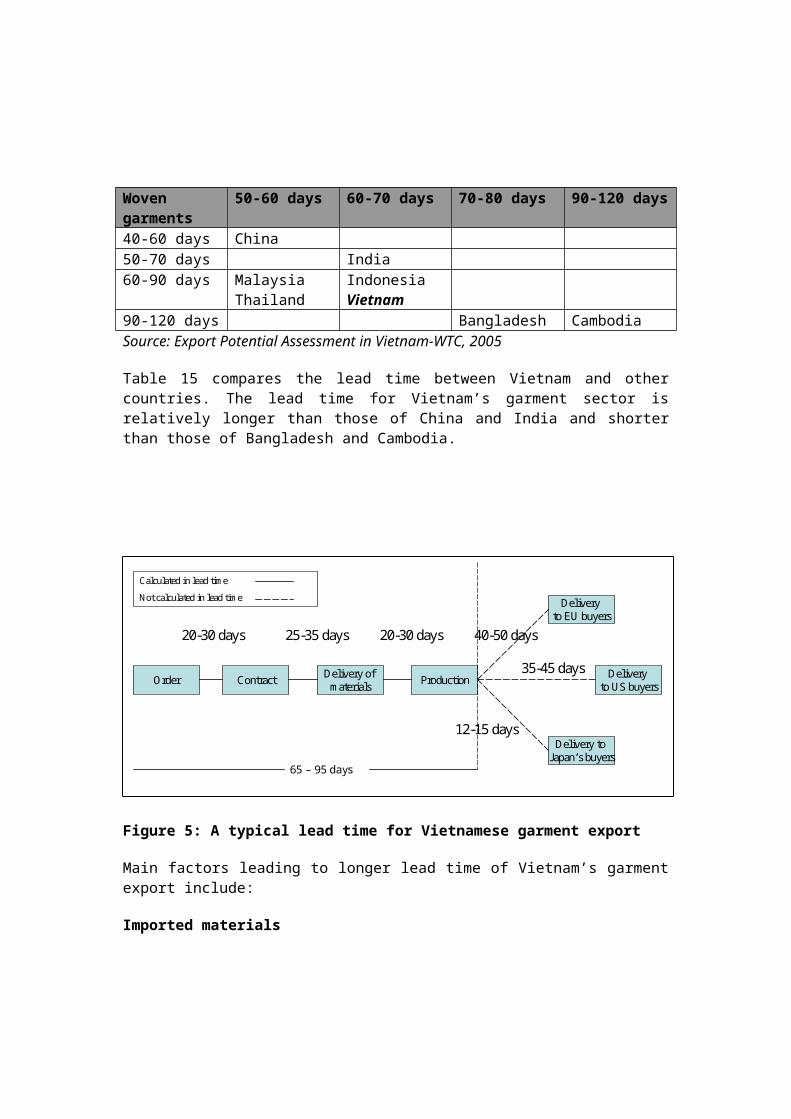

Table 15 compares the lead time between Vietnam and othercountries. The lead time for Vietnam’s garment sector isrelatively longer than those of China and India and shorterthan those of Bangladesh and Cambodia.

Figure 5: A typical lead time for Vietnamese garment export

Main factors leading to longer lead time of Vietnam’s garmentexport include:

Imported materials

Order Contract Delivery of materials Production

Delivery to Japan’s buyers

20-30 days 25-35 days 20-30 days

Delivery to EU buyers

Delivery to US buyers

35-45 days

40-50 days

12-15 days

Calculated in lead tim eNot calculated in lead tim e

65 – 95 days

Figure 5 above shows that the longest link in the lead time isthe time required for importing materials from othercountries, between 25-35 days. This link can be subdividedinto three period including (i) transportation from othercountries to Vietnam taking between 15-25 days, (ii) customsclearance taking between 3-7 days, and (iii) transportationfrom port to factory taking between 2-3 days.

Much shorter lead time could be achieved if garmentmanufacturers can purchase materials domestically. The timefrom Order to Contract can reduce to 15-25 days becausemanufacturers can quote price send counter-sampler faster. Thetime from Contract to Delivery of materials also can decreaseto 15-25 days.

Customs clearance

Customs clearance for each imported goods to and exportedgoods from Vietnam takes 3-7 days while it takes only 10minutes in Singapore, 60 minutes in New Zealand and sevenhours in Thailand12. The total time needed for importingmaterials and exporting finished garment is 6-14 days causingsignificant disadvantage for Vietnam’s garment export in termsof delivery time. In contrast, a large part of sea ports inChina adopts customs clearance for both export from and importto China takes between 1-1.5 days.

Geographic remote and shipment problem

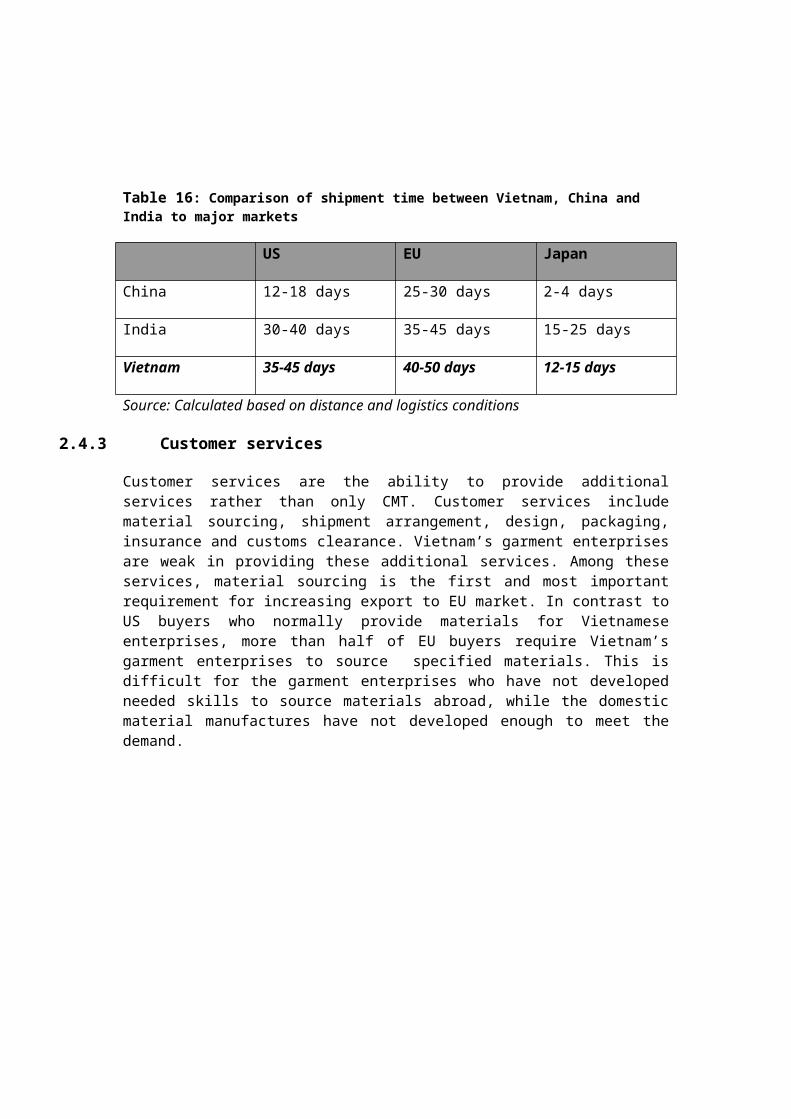

The long distances between Vietnam to US, EU and Japan and thecapacities of Vietnamese ports makes Vietnam less competitivethan main competitors in these markets, especially China andIndia. The shipping time for garment from Vietnam to US is 35-45 days, compared to 12-18 days from China to US as shown inTable 15. Shipment of garment from Vietnam to these marketsmust be transited in Hong Kong or Singapore. In these ports,Vietnamese garment containers are transferred to bigger shipsfor shipping to final ports.

12 http://www.vietnamtextile.org.vn/ePortalHHDM/

Table 16: Comparison of shipment time between Vietnam, China and India to major markets

US EU Japan

China 12-18 days 25-30 days 2-4 days

India 30-40 days 35-45 days 15-25 days

Vietnam 35-45 days 40-50 days 12-15 days

Source: Calculated based on distance and logistics conditions

2.4.3 Customer services

Customer services are the ability to provide additionalservices rather than only CMT. Customer services includematerial sourcing, shipment arrangement, design, packaging,insurance and customs clearance. Vietnam’s garment enterprisesare weak in providing these additional services. Among theseservices, material sourcing is the first and most importantrequirement for increasing export to EU market. In contrast toUS buyers who normally provide materials for Vietnameseenterprises, more than half of EU buyers require Vietnam’sgarment enterprises to source specified materials. This isdifficult for the garment enterprises who have not developedneeded skills to source materials abroad, while the domesticmaterial manufactures have not developed enough to meet thedemand.

2.5 SWOT Analysis

2.5.1 Strengths

Skilful sewers: Vietnamese sewers are considered to beskilful and able to learn new skills quickly. On one hand,this has enabled Vietnam’s garment manufacturers to recruitand train workers quickly and at low training cost. On theother hand, skilful and quick-learning workers has earnedVietnam’s garment sector an image of good and stablequality garment supplier.

Low labor cost: This is one of the most importantadvantages of Vietnam’s garment sector and it has been adecisive factor that enables Vietnam’s garment export toincrease quickly in recent years. Vietnam’s wage rates ingarment sector are one of the lowest levels in the world,approximately two third of Indian wage rate and about halfof China’s.

Support from the Government: The garment and textile sectorhas long received supports from the Government. TheGovernment has spent more than VND 8,000 billion in up-streaming investments in the last five years. Taxincentives, credit support and market access facilitationhave been implemented to support the development of thesector and increase export value. The most important policyin support of the sector is Decision 55-QD/TTg, which willbe analysed in more detail in Part 2.5 below.

Stable economic and political conditions: Vietnam has apositive image in the world as having a stable economic andpolitical condition. This factor plays an important role inthe decision of foreign investors in textile and garmentsector.

2.5.2 Weaknesses

High production cost: In spite of low wage cost, Vietnam’sproduction cost is relatively high compared to China, India

and Pakistan due to low productivity, high infrastructurecosts (electronic, internet, telephone, and transportation)and imported inputs. This reason makes Vietnamuncompetitive in low-end garment in comparison with China,India and Pakistan.

Long lead time: Long distances between Vietnam and mainmarkets of US and EU, import of inputs, long customsclearance are the main reasons for long lead time ofVietnam’s garment export. When international buyers haveincreasingly required garment suppliers to deliver garmentin shorter time, this problem has significantly reduced thecompetitiveness of Vietnam’s garment sector.

Lack of capacity to provide full-package services: In thecontext of severely growing competition in internationaltextile trade, buyers have increasingly preferred to skipbuying agents and sourced garment directly frommanufacturers that can provide full-package service. Veryfew Vietnam’s garment enterprises that have ability toprovide full-package service because they lack designing,material sourcing and logistics arrangement capacities.

Labor scarcity, especially in urban areas: Garmententerprises in urban and industrial areas find difficult torecruit enough garment sewers. Worse still, garmentmanufacturers have a high level of labor mobility,especially after New Year Holiday.

Inadequate human resources development: Vietnam’s garmentsector is in shortage of high-skilled labors such astechnicians, marketing staffs, middle managers anddesigners. For long, most of Vietnam’s garmentmanufacturers have focused on doing CMT and been passive inapproaching clients; therefore, marketing, management anddesigning skills were not of great importance in the past.

Inadequate supporting industries: Domestic textile andaccessories industries have not met the requirements ofgarment manufacturers in terms of quantity and quality.

Vietnam’s garment sector is importing 70-80% materials,increasing production cost, lead time and risks associatedwith transportation, customs and delay. Design and trainingare also under-developed as analysed in Part 2.6 below.

2.5.3 Opportunities

Potential domestic market: Domestic buyers are spendingUSD1.5 billion on garment in 2005 and estimated to spendUSD3.5 billion in 2010. Therefore, Vietnam’s garmententerprises are paying more attention to domestic market,creating more competition in the market among domestic andforeign garment brands. The competition has forced domesticgarment enterprises to develop designing and marketingskills. These skills help the garment enterprises becomemore competitive in export markets.

Removal of quota to EU market: The removal of garment quotato EU market for Vietnam in 1 January 2005 opens a newopportunity for Vietnam’s garment sector to significantlyincrease export value. As analysed in Part 2.2.1, EU marketis more attractive than US market in terms of size andgrowth rate.

Quotas on China: Early 2005, to limit the over-expansion ofChinese garment export to their markets, EU and US imposedquota on garment imported from China in the form of notallowing garment import growth rates from these countrieshigher than 10% per annum. The quota has greatly decreasedthe competition from China’s garment export and opened moreopportunities to Vietnam up to 2008.

WTO accession: It is expected that Vietnam will become WTOmember within two years. The accession means the removal ofall quotas that are currently imposed on Vietnamese garmentexport, most importantly the quota to US market. This wouldincrease Vietnamese share in US garment import becausequota is one of the biggest barriers for Vietnam in thismarket.

ASEAN Free Trade Agreement (AFTA): The free-dutyarrangement among ASEAN member give Vietnam a number ofopportunities: (i) Indonesia and Thailand can be sourcingdestination for fabrics, (ii) establish factories in otherASEAN countries such as Cambodia could partly solve thequota problem of Vietnam to US market, and most importantly(iii) Vietnam and other ASEAN countries, as a trade bloc,could promote negotiation with Japan, EU and US markets togive ASEAN favored tariff for garment imported from ASEANand/or accept cumulative rules of origin for garment andtextile products.

Potential to enhance the competitiveness: Vietnam’s garmentsector possesses a great potential to improve its overallcompetitiveness. Increasing supply of local materials wouldhelp Vietnamese garment manufacturers to lower productioncost and decrease lead time. Customs initiatives such as e-customs clearance, priority customs clearance card (givepriority of clearance for enterprises that have not evadedcustoms law) have been implemented and selective customschecking is expected to implemented with new customs law tobe passed in early 2006, which will shorten lead time forVietnam’s garment export, as a result of shorter time forimporting materials and for exporting garment.

Although it is difficult to expand garment productionfacilities in urban areas due to shortage of labor, highland costs, ect., there are still opportunities for garmententerprises to invest and build garment factories in ruralareas, especially in industrial zones in the areas, to takeadvantage of abundant and low cost labor, and favoredinvestment policies from local governments.

2.5.4 Threats

Removal of quota for China in 2008: The current quotas onChinese garment exports to US and EU are valid until theend of 2008. When the quota are removed, Vietnam’s garmentsector would face much harder competition from China’sgarment exports. Therefore, Vietnam only has nearly 3 years

to come to increase its competitiveness to prepare itselffor this.

Zero tariff for tsunami-suffered countries, including SriLanka, Thailand, and Indonesia: EU have given zero tarifffor garment imported from Sri Lanka, Thailand andIndonesia, the countries suffered from Tsunami in 2004.This increase the competitiveness of garment exports fromthese countries to EU market, while these countries rankhigher than Vietnam in exporting to EU market.

2.6 Government Policy and Strategy in Support ofthe Sector

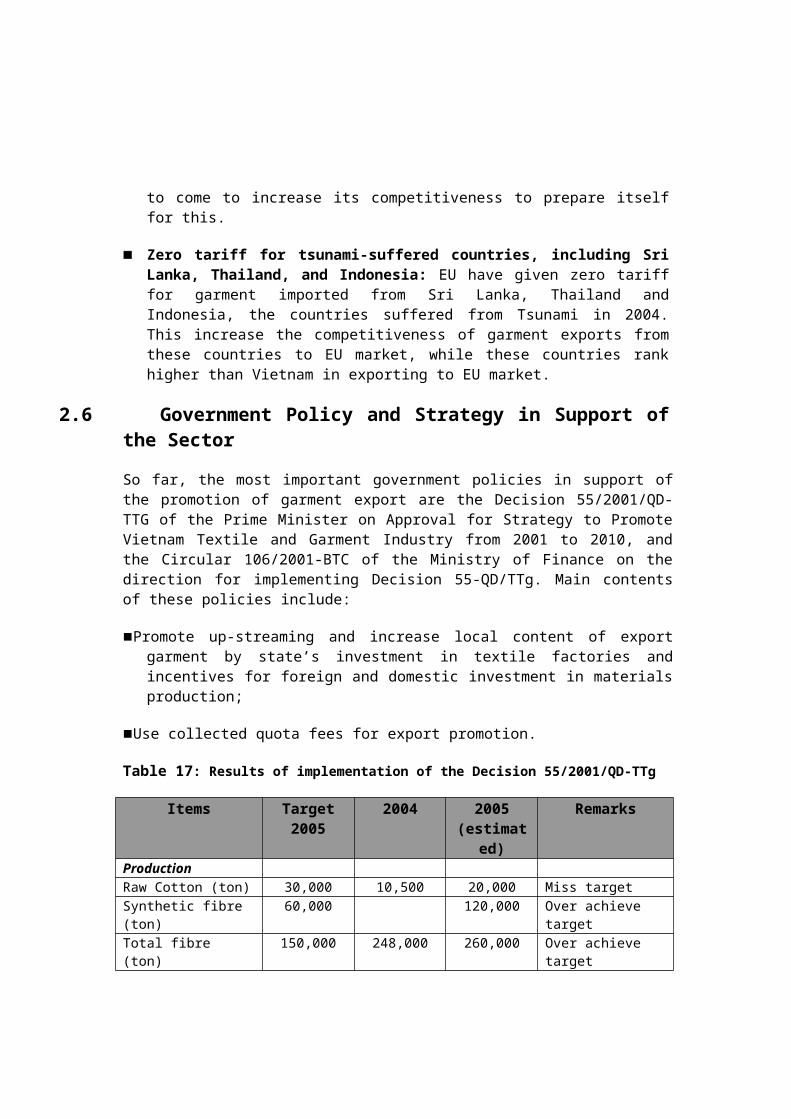

So far, the most important government policies in support ofthe promotion of garment export are the Decision 55/2001/QD-TTG of the Prime Minister on Approval for Strategy to PromoteVietnam Textile and Garment Industry from 2001 to 2010, andthe Circular 106/2001-BTC of the Ministry of Finance on thedirection for implementing Decision 55-QD/TTg. Main contentsof these policies include:

Promote up-streaming and increase local content of exportgarment by state’s investment in textile factories andincentives for foreign and domestic investment in materialsproduction;

Use collected quota fees for export promotion.

Table 17: Results of implementation of the Decision 55/2001/QD-TTg

Items Target2005

2004 2005(estimat

ed)

Remarks

ProductionRaw Cotton (ton) 30,000 10,500 20,000 Miss targetSynthetic fibre (ton)

60,000 120,000 Over achieve target

Total fibre (ton)

150,000 248,000 260,000 Over achieve target

Textile (millionm2)

800 518.2 750 Miss target

Garment (millionproduct)

780 926.3 1,000 Over achieve target

Export value (billion USD)

4-5 4.38 4.8 Achieve target

Labor employment 2.5-3million

2 million 2-2.1million

Miss target

Local content 50% 35% 38-42% Miss targetSource: Assessment of Vietnam’s garment and textile sector after TCA, Vitas, 2005

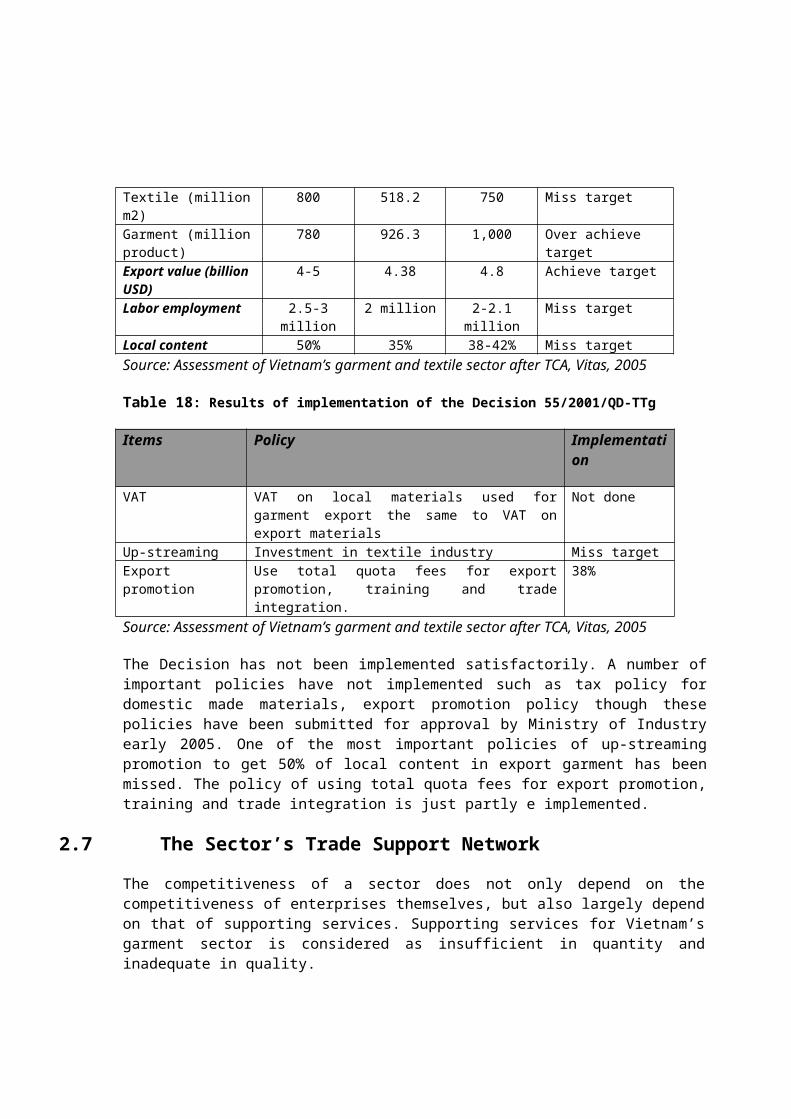

Table 18: Results of implementation of the Decision 55/2001/QD-TTg

Items Policy Implementation

VAT VAT on local materials used forgarment export the same to VAT onexport materials

Not done

Up-streaming Investment in textile industry Miss targetExportpromotion

Use total quota fees for exportpromotion, training and tradeintegration.

38%

Source: Assessment of Vietnam’s garment and textile sector after TCA, Vitas, 2005

The Decision has not been implemented satisfactorily. A number ofimportant policies have not implemented such as tax policy fordomestic made materials, export promotion policy though thesepolicies have been submitted for approval by Ministry of Industryearly 2005. One of the most important policies of up-streamingpromotion to get 50% of local content in export garment has beenmissed. The policy of using total quota fees for export promotion,training and trade integration is just partly e implemented.

2.7 The Sector’s Trade Support Network

The competitiveness of a sector does not only depend on thecompetitiveness of enterprises themselves, but also largely dependon that of supporting services. Supporting services for Vietnam’sgarment sector is considered as insufficient in quantity andinadequate in quality.

Any strong and developed sector is based on strong supportingservice and industries. Also importantly is the close connectionand collaboration between research, training and technologytransfer. Table 18 is compiled to have an overall view of thecurrent situation of supporting services for Vietnam’s garment andtextile sector.

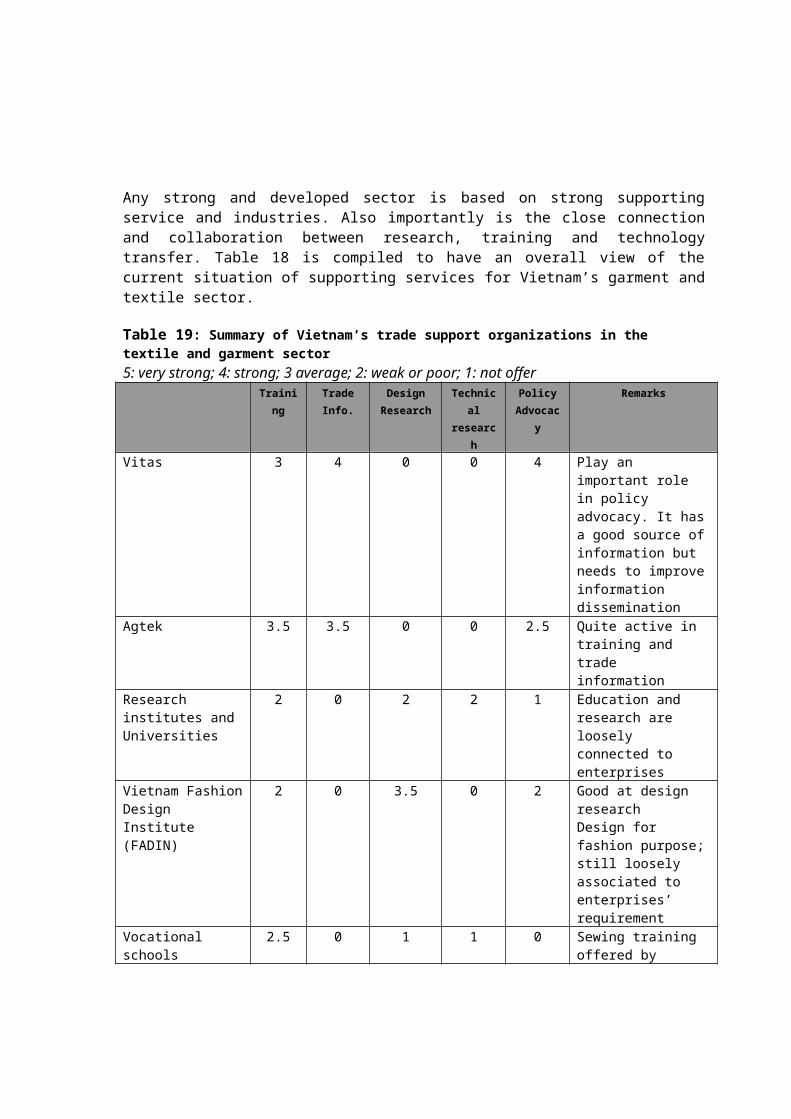

Table 19: Summary of Vietnam’s trade support organizations in the textile and garment sector5: very strong; 4: strong; 3 average; 2: weak or poor; 1: not offer

Training

TradeInfo.

DesignResearch

Technical

research

PolicyAdvocac

y

Remarks

Vitas 3 4 0 0 4 Play an important role in policy advocacy. It hasa good source ofinformation but needs to improveinformation dissemination

Agtek 3.5 3.5 0 0 2.5 Quite active in training and trade information

Research institutes and Universities

2 0 2 2 1 Education and research are loosely connected to enterprises

Vietnam FashionDesign Institute (FADIN)

2 0 3.5 0 2 Good at design researchDesign for fashion purpose;still loosely associated to enterprises’ requirement

Vocationalschools

2.5 0 1 1 0 Sewing training offered by

vocational schools are quite basic withbackward facilities

The table shows that these services are weak in Vietnam. Thisalso reflects the dominant production process of CMT byVietnam’s garment manufacturers. Garment design is mostly doneto serve domestic market.

2.8 Summary of ConclusionTrend of moving towards free-quota enforces buyers to changeportfolio by shifting to source countries with lower cost,faster response, higher quality, and better services. As aresult, the global value chain is reorganized with morepowerful role of mass retailer, less intermediaries and fewersuppliers. This transitional period creates an opportunityfor Vietnam to reposition and upgrade its role in the globalgarment chain.

Vietnamese garment exporters have a long history of processingCMT with low risk, small margin, dependence on intermediaries,and increasingly fierce competition on price. These factorsurge strategic changes in Vietnam value chain toward higherefficiency of supply chain and production to pursuit costcompetitive, or more value added activities to move to FOBmode or upgrading the chain to implement both. Strategic moveshould pay attention to following implications of theanalysis: