Embed Size (px)

Citation preview

Project onBanks Emerging as Financial Supermarket: A

Study of Retail Banking Practices of Central Banks in India

Presented by Natasha Chhabra

MBA 3rd sem

Flow of presentation

Company profile

Research Objectives

Scope of the study

Research Methodology

Data Interpretation

Key Findings

Suggestions

Implications of the study

Recommendation for future research

Central Bank of India (Marathi: सेटरल बकँ ऑफ इिंडिया), a government-owned bank, is one of the oldest and largest commercial banks in India. It is based in Mumbai. The

bank has 4600 branches and 4 extension counters across 27 Indian states and

three Union Territories. At present, Central Bank of India has overseas office at

Nairobi, Hong Kong and a joint venture with Bank of India, Bank of Baroda, and the

Zambian government. The Zambian government holds 40 per cent stake and each

of the banks has 20 per cent. Recently it has also opened a representative office at

Nairobi, Kenya.

Central bank of India is one of 18 Public Sector banks in India to

get recapitalisation finance from the government over the next 24 months.

Central Bank of India has approached the Reserve Bank of India (RBI) for

permission to open representative offices in five more locations - Singapore, Dubai,

Doha and London [

COMPANY PROFILE

HISTORY OF THE COMPANY

It was established on 21 December 1911 by Sir Sorabji Pochkhanawala with Sir

Pherozeshah Mehta as Chairman, and claims to have been the first commercial

Indian bank completely owned and managed by Indians.

By 1918 it had established a branch in Hyderabad. A branch in

nearby Secunderabad followed in 1925.

In 1923, it acquired the Tata Industrial Bank in the wake of the failure of

the Alliance Bank of Simla. The Tata bank, established in 1917, had opened a

branch in Madras in 1920 that became the Central Bank of India, Madras.

Central Bank of India was instrumental in the creation of the first Indian exchange

bank, the Central Exchange Bank of India, which opened in London in 1936.

However, Barclays Bank acquired Central Exchange Bank of India in 1938.

What is Retail Banking - It is the new mantra in the banking sector. It refers to the dealings of a bank with its individual customers

Banks journey since 1 7 8 6 brought a revolutionary change in banking in India. Banks have come a long way from depository institute to a complete financial supermarket.

Banks Financial Supermarket

Retail Banking is the cluster of products and services that banks provide to consumers and small businesses through branches, the Internet, and other channels. As this definition implies, banks organize their retail activities along three complementary dimensions: customers served, products and services offered, and the delivery channels linking customers to products and services.

Almeida, 2003

Objectives of Retail Banking:

•Provide target customers a full range of financial products and banking services.

•Give the customers a one stop window for all their banking requirements.

SCOPE FOR RETAIL BANKING IN INDIA:•All round increase in economic activity.

•Increase in the purchasing power. The rural areas have the large purchasing power at their disposal and

this is an opportunity to market Retail Banking.

•India has 200 million households and 400 million middleclass population more than 90% of the savings come from

the house hold sector. Falling interest rates have resulted in a shift. “Now People Want To Save Less And Spend

More.”

•Nuclear family concept is gaining much importance which may lead to large savings, large number of banking

services to be provided are day-by-day increasing.

•Tax benefits are available for example in case of housing loans the borrower can avail tax benefits for the loan

repayment and the interest charged for the loan.

Cha

nnel

Pro

duct

s &

S

ervi

ces

BANK

Reliability

DemandAgency

Customer

BranchAccounts

Accounts

Plastic

MoneyPlastic

Money

Demat/ Share A/c

Demat/ Share A/c

Investment Banking

Investment Banking

InsuranceInsuranceHome

loneHome

lone

Mortgage

FinancingMortgage

Financing

ATM

Bankassurance

Call Center

Phone/ Internet Banking

Mutual FundsMutual Funds

Retail Finance Umbrella

Research Objectives

To contemplate the emerging trends in Retail Banking in India

To assess the level of Bank customers’ Satisfaction in terms of

Techno-savvy Retail services offered by the banks

To examine the Opportunities and challenges for Banks

becoming the Financial Supermarket

To study the Retail Marketing Strategies in selected 12 Retail

Banks

To suggest the futuristic vision for Retail banking in India

Scope of the study• Study includes Public, Private and Foreign banks operating in

India

• Bank branches within the city limits and situated in major towns

• Emphasis on studying the retail practices of these banks

• Profile of technologically aware customers and knowing their preferences for selecting banks and their services

• Degree of acceptance of technology for better services

• Customer satisfaction generated from advanced products and techno savvy banking services

Research MethodologyResearch design

A research design is the arrangement of conditions for collection and analysis of data in a manner that aims to

combine relevance to the research purpose with economy in procedure. It is the conceptual structure within which

research is conducted. It constitutes the blueprint for the collection, measurement and analysis of data. My

research design is descriptive in nature as it involves studying the perceptions and expectations of customers in

order to measure the service quality provided by the service provider. The study thus finds out the major areas of

improvement so that company services to the customers can be improved.

.

Method of Data Collection

The primary data was collected with the help of a structured, non disguised questionnaire. Secondary data was

collected from journals, magazines, newspapers, books & internet with a view to supplement the primary data.

The study of secondary sources made the with a view to supplement the primary data. The study of secondary sources

made the structuring of questionnaire easy.

Sample Sizes The sample size undertaken in this research study is 80.

Types of Data

Primary Data:The sources of primary data were structure questionnaires used in the research project.

Secondary data: The sources of secondary data were internet, books, banks, articles newspapers, journals, magazines etc.

Data Collection ApproachesQualitative Approach

• In depth study & review of literature• Review of work on Retail Banking practices • Understanding various factors contributing in

customer satisfaction and bank service preferencesStep - 1

Step - 2

• Personal interview with Bank managers and executives

Result• Draft Questionnaire developed• Multi Dimensional Scale developed• Direction for quantitative research

Data Collection ApproachesQuantitative Approach

• Distribution of draft instrument to sample of population

• Survey refined & tested for reliability and validity of constructs

Cronbach Coefficient Alpha > 0.7 - Reliable

Step - 1

Step - 2 • Instrument pre – testing

• Final Instrument Development

S.No.

Product and services

Percentage (%)

1 Saving A/C 100

2 Current A/C 100

3 Demat A/C 50

4 Forex sevice 40

5 Net banking 90

6 Home loan 100

7 Electronic transfer

100

8 Mutual fund 60

9 ATM 100

10

Personal loan 60

DATA ANALYSIS AND INTERPRETATION

Q1. What products and services does your bank offer to you?

Interpretation:The sample size out of 80 respondents 100% peoples are said that their banks provides all financial services.

S.No. Details Percentage (%)

1 Yes 85

2 No 15

Q3. Does your bank inform you timely about the new products and services?

Interpretation:The sample size out of 80 respondents, 85% says that Yes bank inform them timely about the new products and services and

15% says No.

S.No. Details Percentage (%)

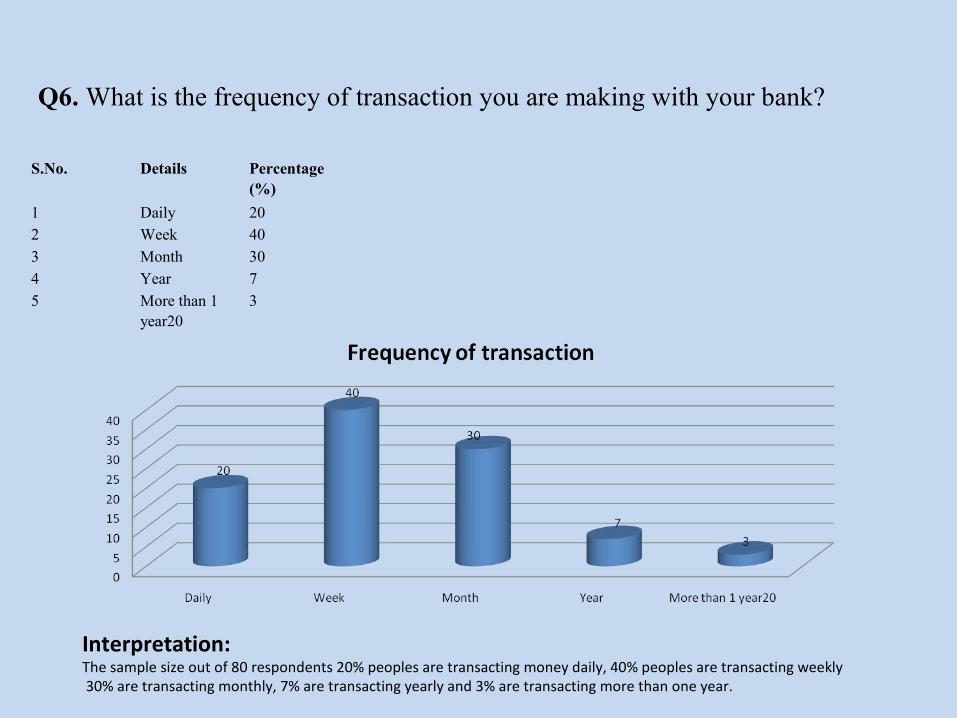

1 Daily 202 Week 403 Month 304 Year 75 More than 1

year203

Q6. What is the frequency of transaction you are making with your bank?

Interpretation:The sample size out of 80 respondents 20% peoples are transacting money daily, 40% peoples are transacting weekly 30% are transacting monthly, 7% are transacting yearly and 3% are transacting more than one year.

S.No. Details Percentage (%)

1 Yes 60

2 no 40

Q7. According to you, does your bank provide core banking facility for the customers?

Interpretation:

sample size out of 80 respondents 60% peoples said yes, 40% peoples said no.

Presentation & Analysis of Data Coding of data and preparation of Master Data Sheet

Tabulation, classification and graphical representation.

Mean and Standard deviation of the variables used in questionnaire

To measure customer satisfaction in terms of techno savvy Retail

banking services Factor Analysis was performed

Prior to factor analysis correlation matrix used to identify the

applicability of Factor analysis.

Discriminant analysis to find the highest contributing factors in

showing differences in satisfaction among three banking sectors.

Key FindingsRetail Product Satisfaction

Product features and availability of a wider product range under one roof

Product innovation is significant factor for foreign bank customers

Retail Channel Satisfaction

Availability, accessibility and functionality

Ease of banking and convenience is favored by the customer

Loss of customer relationships and deposits to banks with extensive online services,

virtual banks, and non-banks

Retail Service Satisfaction

Reliability, responsiveness, convenience, frontline employee satisfaction, and

competence of the Bank are found most important contributors in Customer

satisfaction.

Ease of use, accuracy and security are prime factors define the satisfaction of online

customers

Key FindingsFindings on Demographic characteristics-

Women enlightenment towards banking services

Old is Gold- Customer with longer years of a/c holding

Education plays an important role

Business brings more business

High income created more needs and less satisfaction

New private sector banks are becoming new destination of bank customers

Saving is at higher side in customer’s mind

3 S behind choosing a Bank - Security, Strength and Speed

Key FindingsTechno readiness

Increased awareness and uses of ATM and Net banking

Among non users it is mainly due to fear and insecurity

Online banking preferred as the fastest means of any transaction

Excitement towards retail bank technology is high

Gaining high-tech knowledge

Human touch experience still beats the speed and convenience of online banking

to some extent.

Customer prefer remote channel for obtaining information and routine

transaction, but still believe in branch banking for purchase action.

Suggestions Create the culture and organizational model needed to promote greater

commitment, accountability and competency

need to provide easily accessible mechanisms, appropriate financial advice and

customizing services

Create a better, consistent customer experience across channels

Improve the Branch - the ultimate destination for purchase action

Improve the online experience – ease of use and accuracy

Make better use of customer information- need to develop products and services

that their clients need before the clients even know they need them

shift from customer volume based strategies to customer value based strategies.

Inbound Customer Marketing- Focus on specific customers and situations , respond

properly and Integrate transversal customer information throughout channels

Implications of the study

It presents an overall picture of present and emerging Retail Banking trends.

This study helps banks to develop the strategies to improve bank service

quality and enhance customer satisfaction.

It gives the blue print for area of improvements and also suggest customers

attitude towards Retail banking practices.

It suggest product innovation and market expansion strategies for banks

Helps in understanding of global market for Indian banks

Gives an understanding to the banks about what factors contribute to overall

customer satisfaction

The findings presented in this study can be used by both academician and

practitioners

Recommendations for future Research

Replicating the present study with other financial services or in other cultural

environment

More specific research could address each of the services provided in the

banking industry

More direct items on the behavioral aspects of customer satisfaction can be

closely examination by future researchers

Need to recognize varying levels of profitability between market segments, a

key criterion of which is the preferred mode of service delivery

Impact of service managed customer learning in changing attitudes and thus

profitability

Thank you….!