Embed Size (px)

Citation preview

Nuts & Bolts of Lost Profit Cases

COMPLEX FINANCIAL LITIGATION FOR THE NON-EXPERT Premiere Date: February 23, 2017

This webinar is sponsored by: EisnerAmper 1

2

3

4

5

MODERATOR Erin Hollis Marshall & Stevens, Chicago

PANELISTS Don May DMA Economics, NY John Levitske Huron Consulting Group, Chicago Leland Chait Sugar Felsenthal Grais & Hammer, NY

MEET THE FACULTY

6

SERIES SPONSOR

7

ABOUT THIS WEBINAR

Expectations, we all have them. Maybe a business partner, supplier or vendor didn’t live up to their end of the bargain and the business suffers. What is the remedy? What are the damages and how do you seek repayment of the loss profits?

Lost profits are an economic measure of damages a business suffers as a result of a wrongful act, and can only be claimed over the loss period. In this webinar we discuss types of wrongful acts that can lead to such damages, what makes an effective claim to recover lost profits, proactive solutions to prevent or reduce claims, and what the difference is between a reduction in business value and lost profits.

Further complicating the understanding of damages are other remedies that are often confused with lost profits, which are also covered.

8

ABOUT THIS SERIES Many people do not understand the specialization that the legal industry has undergone in the past several decades. Just as one would not go to a dermatologist for lung cancer, one would not ask a tax attorney to defend a DUI.

But the specialization goes even deeper: litigation over commercial disputes should be handled by someone with deep experience with such disputes; the best criminal defense attorney or divorce litigator is simply not the likely best choice because, among other reasons, issues tend to repeat themselves. This is not to say that once an attorney has done one “xyz case” she is an expert at all “xyz cases,” but the truth is that the expression “the practice of law” exists for good reason.

This webinar series explores four common litigation scenarios involving complex financial issues. Each episode is delivered in Plain English understandable to business owners and executives without much background in these areas. Yet, each episode is proven to be valuable to seasoned professionals. As with all Financial Poise Webinars, each episode in the series brings you into engaging, sometimes humorous, conversations designed to entertain as it teaches. And, as with all Financial Poise Webinars, each episode in the series is designed to be viewed independently of the other episodes, so that participants will enhance their knowledge of this area whether they attend one, some, or all of the episodes.

9

EPISODES IN THIS SERIES

EPISODE #1 Common Issues and Strategies in Business Breakups 1/19/2017 EPISODE #2 Nuts & Bolts of Lost Profit Cases 2/23/2017 EPISODE #3 Resolving Shareholder Disputes 4/20/2017 EPISODE #4 Defending Against “Avoidance Actions” 5/11/2017

Dates shown are premiere dates; all webinars will be available on demand after premiere date

10

WHAT ARE LOST PROFITS?

• Revenues that would have been earned but for the wrongful act (‘but for’ revenues)

LESS

• Incremental costs necessary to derive these revenues

EQUALS

• Lost Profits

11

WHAT ARE LOST PROFITS (CONT’D)?

The factual or “but for” causation showing needed for recovery of lost profits damages -- as with all damages -- requires a plaintiff to prove by a preponderance of the evidence that there is ‘some reasonable connection between the act or omission of the defendant and the damage which the plaintiff has suffered.’

12

WHAT ARE LOST PROFITS (CONT’D)?

• Profits must be shown to have been factually and legally caused by -- and a reasonably foreseeable result of -- the defendant’s wrongful conduct.

• Further, a plaintiff must prove his or her estimate of lost profits to a “reasonable certainty,” establishing such damages through an adequate evidentiary foundation.

13

WHAT IS THE DIFFERENCE BETWEEN LOST PROFITS AND LOST VALUE?

• Lost Profits = Incremental profits the company would had have earned but for the wrongful act

• Lost Value = The present value of lost profits over the life of the company discounted at the appropriate risk adjusted rate of return

• How do you decide which analysis to utilize? ! When lost profits extend over the life of the company

14

STANDARD FOR PROVING LOST PROFITS • Tort or Contract must have:

! Causation - Some reasonable connection between the act or omission of the defendant and the damage which the plaintiff has suffered.

! Reasonable foreseeability – Lost profits must be shown to have been factually and legally caused by the defendant’s wrongful conduct.

! Reasonable certainty - Establishing such damages through an adequate evidentiary foundation; applies only to the fact of damages, not to the amount of damages

15

ESTABLISHED BUSINESSES

• Provides evidence of a successful past track record of business, along with evidence establishing anticipated future net profits, offer the greatest likelihood of recovering lost profits

• Use expert testimony based upon a solid evidentiary foundation addressing the underlying economic data quantifying gross revenue and variable expenses

• May use outside or inside expert testimony

16

WHAT ABOUT RECENTLY ESTABLISHED OR NEW BUSINESSES?

• May use alternative forms of proof to establish lost profits, such as industry averages, governmental standards

• Must still meet the “reasonable certainty” standard

• Damages for lost profits are confined to the period in which it would be reasonable to replace the profits

17

WHAT ABOUT RECENTLY ESTABLISHED OR NEW BUSINESSES (CONT’D)?

• Alternative Tools ! The Wrongdoer Rule ! Lost Opportunity

" Loss of Chance Doctrine " Loss of Earnings Opportunity " Loss of Business Opportunity

18

GENERAL FLOW OF CALCULATING LOST PROFITS

• Understand which lost profits damages model is appropriate • Use evidentiary standards • Calculate lost profits • Develop the causal economic link between defendant’s action

(event) and the loss • Select the period to examine • Estimate the relevant lost revenues and associated costs • Utilize assumptions that have reasonable certainty

19

LOST PROFIT METHODS

• Before-and-After Approach • Yardstick Approach • Sales Projection Approach • Market Share Approach • Alternative methodologies

20

HISTORICAL DAMAGES

21

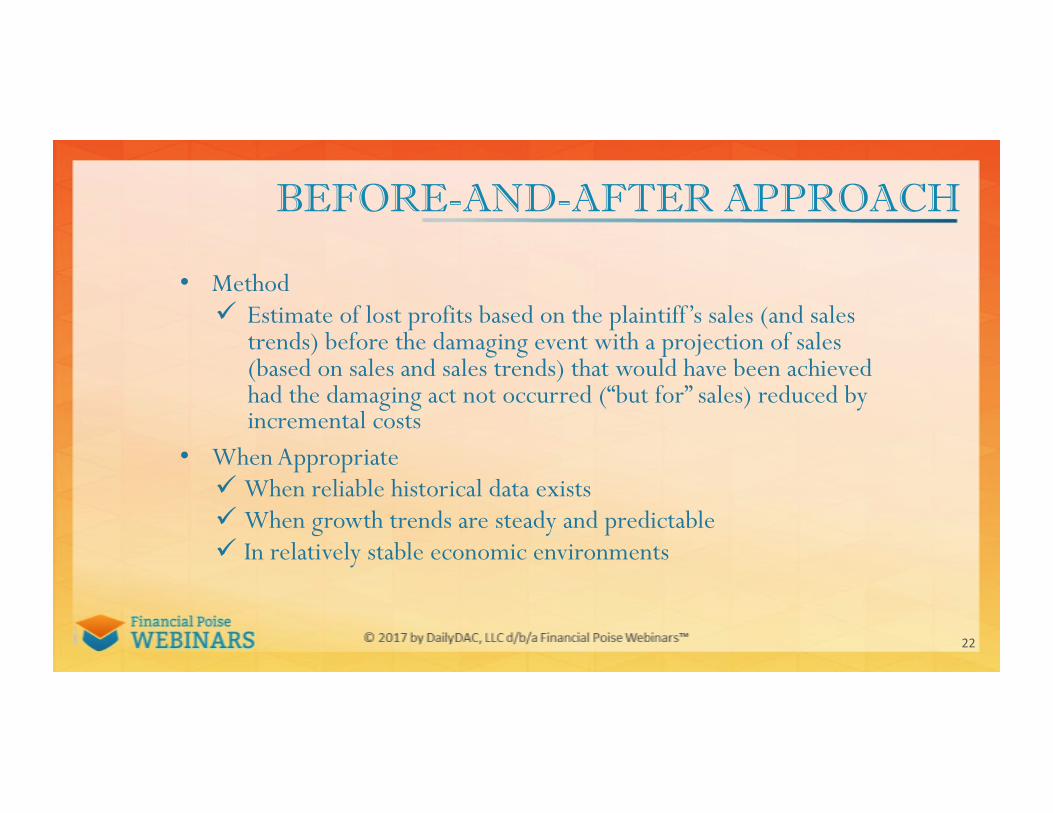

BEFORE-AND-AFTER APPROACH

• Method ! Estimate of lost profits based on the plaintiff’s sales (and sales

trends) before the damaging event with a projection of sales (based on sales and sales trends) that would have been achieved had the damaging act not occurred (“but for” sales) reduced by incremental costs

• When Appropriate ! When reliable historical data exists ! When growth trends are steady and predictable ! In relatively stable economic environments

22

HISTORICAL DAMAGES & FUTURE DAMAGES

23

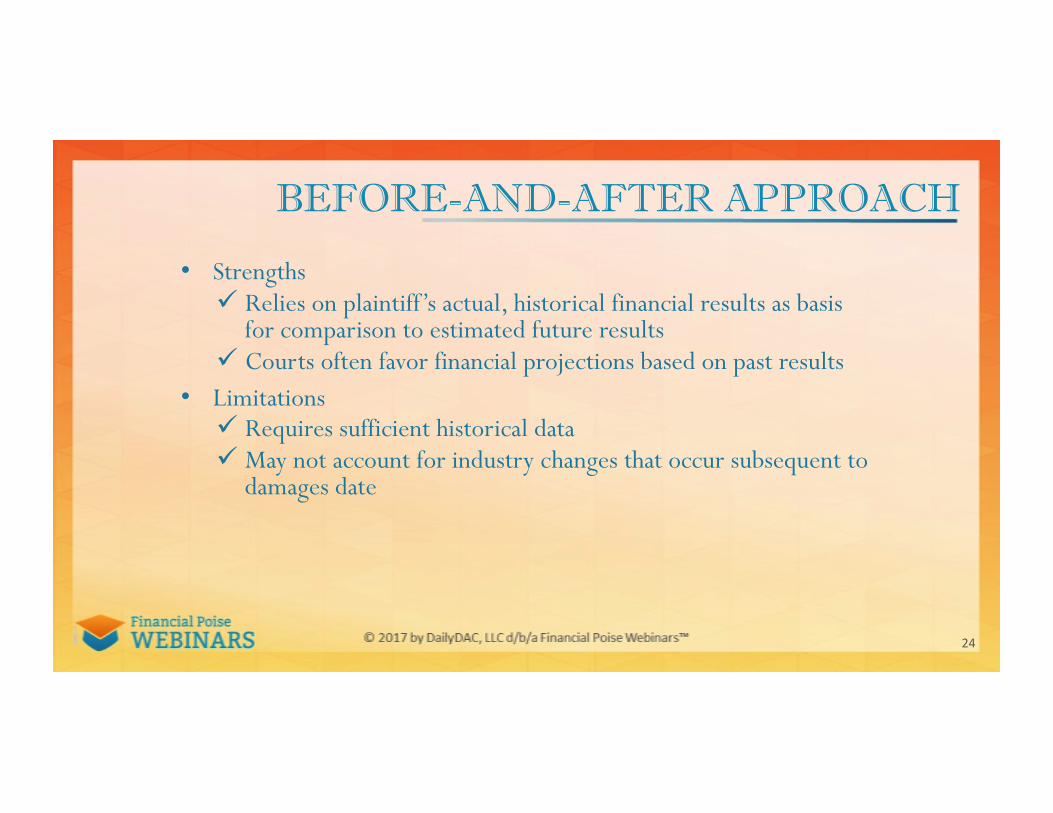

BEFORE-AND-AFTER APPROACH

• Strengths ! Relies on plaintiff’s actual, historical financial results as basis

for comparison to estimated future results ! Courts often favor financial projections based on past results

• Limitations ! Requires sufficient historical data ! May not account for industry changes that occur subsequent to

damages date

24

BEFORE-AND-AFTER APPROACH (CONT’D)

25

Plaintiff Company - Sales

1998 1999 2000 2001

EVEN

T

2002 2003 2004

Actual Sales $180,000 $219,000 $262,000 $317,000 $298,000 $295,000 $302,000

Growth Rate 21.7% 19.6% 21.0% -6.0% -1.0% 2.4%

Projected Sales - - - - 383,570 464,120 561,585

Growth Rate 21.0% 21.0% 21.0%

Lost Sales - - - - ($85,570) ($169,120) ($259,585)

Total Lost Sales ($514,275)

YARDSTICK APPROACH

• Method ! Estimate of the plaintiff’s profits based on a yardstick – e.g., a

comparable company, division or industry benchmark - that is not affected by the damaging act

• When Appropriate ! When a reliable yardstick exists ! With newly established firms ! Accounts for differences in time periods ! When market conditions may have changed subsequent to the

damages event date

26

YARDSTICK COMPARISON

27

YARDSTICK APPROACH

• Strengths • Can provide objective, reliable benchmark for estimating • Yardstick is independent of effects from damaging act • Accounts for changes in the industry or market that may have

occurred subsequent to the damages event date • Limitations

• Lack of comparability between plaintiff and yardstick (e.g., size, sales channels)

• Yardstick data may not be available

28

MARKET SHARE APPROACH

• Method ! Calculates lost profits based on the difference between the

plaintiff’s “but-for” market share and its market share after the damaging act.

• When Appropriate ! When reliable market share data exists ! When plaintiff company products/services fit within “market”

29

MARKET SHARE APPROACH (CONT’D)

• Strengths ! Can provide objective, reliable basis for estimating ! Other companies in “market” are independent of damaging act ! Accounts for changes in the industry during relevant period

• Limitations ! Difficult to determine market share – lack of data,

comparability ! May be difficult to assess due to dynamic markets

30

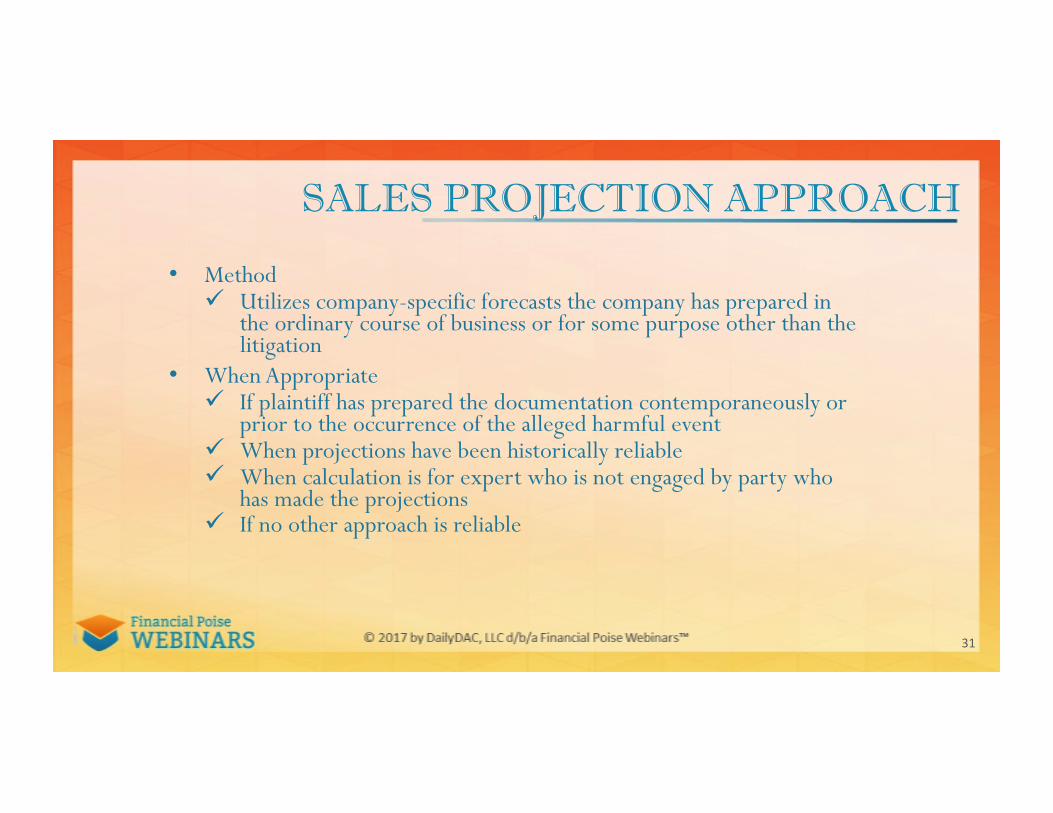

SALES PROJECTION APPROACH

• Method ! Utilizes company-specific forecasts the company has prepared in

the ordinary course of business or for some purpose other than the litigation

• When Appropriate ! If plaintiff has prepared the documentation contemporaneously or

prior to the occurrence of the alleged harmful event ! When projections have been historically reliable ! When calculation is for expert who is not engaged by party who

has made the projections ! If no other approach is reliable

31

EXPECTED IMPAIRMENT OF FCFs

32

SALES PROJECTION APPROACH

• Strengths ! May allow the expert to incorporate more easily the effects of

other factors (beyond the harmful act) that might increase or decrease the estimated economic damages

! Can be very effective if used by expert for party opposing the party who made the projection

• Limitations ! Does not control for market events that may have occurred

subsequent to the damages event ! Difficult to independently support the underlying foundation for

the projections ! Speculative or nothing more than a “wish list”

33

ESTIMATING INCREMENTAL COSTS • Costs should only be those costs related to the the lost

incremental revenues (“Avoidable or incremental Costs”)

• Examples of costs that may be included (Incremental) ! Direct costs (materials, commissions) ! Other variable or semi-variable costs

" Salaries " Infrastructure

• Examples of costs that should not be included ! Corporate overhead ! Other fixed costs (depreciation, amortization)

34

EVIDENTIARY SUPPORT

• Informed opinion - Lost profits may be established by evidence of past experience or expert testimony sufficient to quantify the extent of loss, either of which must be properly supported by admissible evidence.

• Judgmental approximation - Plaintiff's owner provided evidence of the company's past experience and lost profits; owner has substantial experience.

• Credible evidence – Industry averages, governmental information, official statistics, etc.

35

WHAT EVIDENCE IS NECESSARY?

• “The Company’s profits would have been $XXX,XXX, based on…” ! Examine financial statements for history ! Demand for product ! Consistent pricing trends over time ! Industry trends over time ! Competitive risk is low ! Technology risk is low ! Customer retention is constant/high

36

WHAT EVIDENCE IS NECESSARY? (CONT’D)

• “The risk the Company would NOT achieve $XXX,XXX in profits is very low, based on …”

! Customer and product demand ! Low risk of product/service obsolescence ! Industry trends that support achievability ! Backlog orders

37

WHAT EVIDENCE IS NECESSARY? (CONT’D)

• “The Company’s profits are now only $X,XXX, due to …”

! Customer cancellations of orders or contracts ! Lost customer or documented market share ! Lost productivity

38

WHAT EVIDENCE IS NECESSARY? (CONT’D)

• “The Defendant’s actions are directly responsible for the loss in profits, based on …”

! Customers lost as a direct result of the defendant’s actions " Cancellation documentation/letters

! Inability to gain new customers " Documentation of futile efforts

39

WHAT EVIDENCE IS NECESSARY? (CONT’D)

• “No other factors contributed the Company’s ability to earn $XXX,XXX in profits, as proved by …”

! Industry stability ! Economic stability ! No new competitive entrants into market place ! No new governmental or regulatory issues

40

QUALIFIED EXPERT

• Must be a qualified expert, experienced in field (highly recommend credentialed individual) ! Accounting Professional (CPA) ! Valuation expert (ASA, ABV, CFA) ! Economist

• Must use proper methodology • Must be objective • Must have sufficient evidentiary support

41

DEFENDING AGAINST AN ACTION

• What defenses exist to a lost profit action?

• What can a party do to challenge the lost profits findings of an expert?

42

CONCLUDING THOUGHTS

• Applicable standards • Burden of proof • Evidentiary challenges • Remedies • Methodologies • Qualified expert • Other remedies

43

ABOUT THE FACULTY

44

ERIN HOLLIS ehollis@marshall-‐stevens.com

Ms. Hollis is a Financial ValuaAon and ConsulAng Director of Marshall & Stevens Incorporated. Her valuaAon experience includes sale/purchase, insurance, financing, and estate planning and corporate planning. She also has special purpose appraisal experience with specific types of feasibility. Her other professional acAviAes include authoring numerous arAcles on valuaAon in several publicaAons, speeches, and being a member of the American Society of Appraisers, where she parAcipates as a Business ValuaAon CommiTee member. She is also a past (2012-‐-‐2013) President and current member of the American Society of Appraisers Chicago Chapter.

Ms. Hollis entered the appraisal profession in 2000. Prior to becoming a Director of Marshall & Stevens, she held the Director posiAon of Tax & ValuaAon Services with ValuaAon Advisory Services and simultaneously with Strategic Tax Advisors for 13 years. In her posiAon, Ms. Hollis oversaw all aspects of business development, producAon, administraAon, financial planning, quality control, revenue and client development. Ms. Hollis is a graduate of Michigan State University, a qualified expert witness, and an Accredited Senior Appraiser (ASA) in Business ValuaAon of the American Society of Appraisers. She is also CerAfied in Distress Business ValuaAon (CDBV) with the AssociaAon of Insolvency & Restructuring Advisors

ABOUT THE FACULTY

45

JOHN LEVITSKE [email protected]

John Levitske is a Senior Director in the Commercial Dispute Advisory pracAce of Huron ConsulAng Group in Chicago. He has three decades of experience in business valuaAon and forensic accounAng. He focuses on complex business valuaAon, economic damages, and forensic accounAng maTers, and the resoluAon of valuaAon and accounAng (e.g. working capital, earnouts and representaAons) disputes arising from M&A transacAons, commercial and shareholder liAgaAon, business divorce and private company controversies.

John holds an MBA, cum laude, from the University of Notre Dame, and both a JD and BS in Business AdministraAon from Duquesne University. He also is a CerAfied Public Accountant licensed in Illinois and Pennsylvania, Accredited in Business ValuaAon by the American InsAtute of CerAfied Public Accountants, Accredited Senior Appraiser in Business ValuaAon by the American Society of Appraisers, Chartered Financial Analyst charterholder with the CFA InsAtute, CerAfied in Financial Forensics with the AICPA, CerAfied Forensic LiAgaAon Consultant with the Forensic Expert Witness AssociaAon, CerAfied Insolvency & Restructuring Advisor with the AssociaAon of Insolvency & Restructuring Advisors, and Chartered Global Management Accountant with the AICPA.

ABOUT THE FACULTY

46

DON MAY [email protected]

Don May is Managing Partner at DMA Economics LLC and possesses over 30 years’ experience in consulAng, valuaAon and liAgaAon support as well as researching, publishing and teaching at the university level. His experience includes implemenAng a broad range of damage analyses and valuaAons for businesses of various sizes and in numerous industries. Prior to founding DMA Economics LLC, Dr. May was Managing Director at Berkley Research Group and the Principal in charge of valuaAon and liAgaAon support services for a regional accounAng firm, a Managing Director for PricewaterhouseCoopers and a professor at the MassachuseTs InsAtute of Technology -‐ Sloan School of Management.

Dr. May has prepared expert reports and tesAfied in federal and state courts as well as AAA, JAMS, and FINRA arbitraAon hearings and has effecAvely communicated as an expert witness tesAfier and consultant in several mulA-‐million dollar cases.

ABOUT THE FACULTY

47

LELAND CHAIT [email protected]

Leland Chait is a partner with Sugar Felsenthal Grais & Hammer who heads the Firm’s Complex LiAgaAon PracAce whose pracAce includes Bankruptcy, ReorganizaAon and Creditors’ Rights.

As a problem solver, Lee successfully tries business disputes in state and federal courts throughout the United States, focusing on maTers in the healthcare and insurance fields, and in resolving business divorces. He advises individuals and businesses with complex commercial disputes, including cases brought on a class acAon basis, in the employment, insurance, anAtrust, regulatory compliance and healthcare fields.

Visit www.eisneramper.com EisnerAmper. Let's Get Down to Business®

EisnerAmper LLP is a leading full-‐service advisory and accounFng firm, and is among the largest in the United States. We provide audit, accounFng, and tax services, as well as corporate finance, internal audit and risk management, liFgaFon services, consulFng, private business services, employee benefit plan audits, forensic accounFng, and other professional advisory services to a broad range of clients across many industries. We work with high net worth individuals, family offices, closely held businesses, start-‐ups, middle market and Fortune 500 companies. EisnerAmper is PCAOB-‐registered and provides services to more than 200 public companies and to thousands of enFFes spanning the hedge, private equity, brokerage and insurance

space in the financial services marketplace. As companies grow we help them reach their goals every step of the way. With offices in New York (NY), New Jersey (NJ), Pennsylvania (PA), California (CA), and the Cayman Islands, and as an independent member of Allinial

Global, EisnerAmper serves clients worldwide.

48

49

50