Embed Size (px)

Citation preview

GOODS AND SERVICES TAX (GST) IN INDIA

Submitted to: khushabu ma’am BBA v

A presentation byRAHISH KHAN

INDIAN ECONOMY-AN OVERVIEW The Indian economy, the third largest

economy in the world in terms of PURCHASING POWER, is going to touch new height in coming years. according to global investment bank by 2035 India would be 3RD largest economy of the world just after US and CHINA. It will grow to 60% of size of the US economy.

India’s economy is the 11th largest economy in the world.

G-20 major economy and a member of BRICS.

WHAT IS GST?‘G’ – Goods‘S’ – Services‘T’ – Tax

“Goods and Service Tax (GST) is a comprehensive tax levy on manufacture, sale and consumption of goods and service at a national level.GST is a tax on goods and services with value addition at each stage having comprehensive and continuous chain of set-of benefits from the producer’s/ service provider’s point up to the retailer’s level where only the final consumer should bear the tax.”

HISTORY OF GST In 2000, the vajpayee government started

discussion on GST by setting up an empowered committee. An announcement was made by p. chidambaram ,

the union finance minister , during the centrel budget of 2007-2008that it would be introduced form april 1,2010 .

This proposal is given by vijay kelkar The government came out with a first discussion

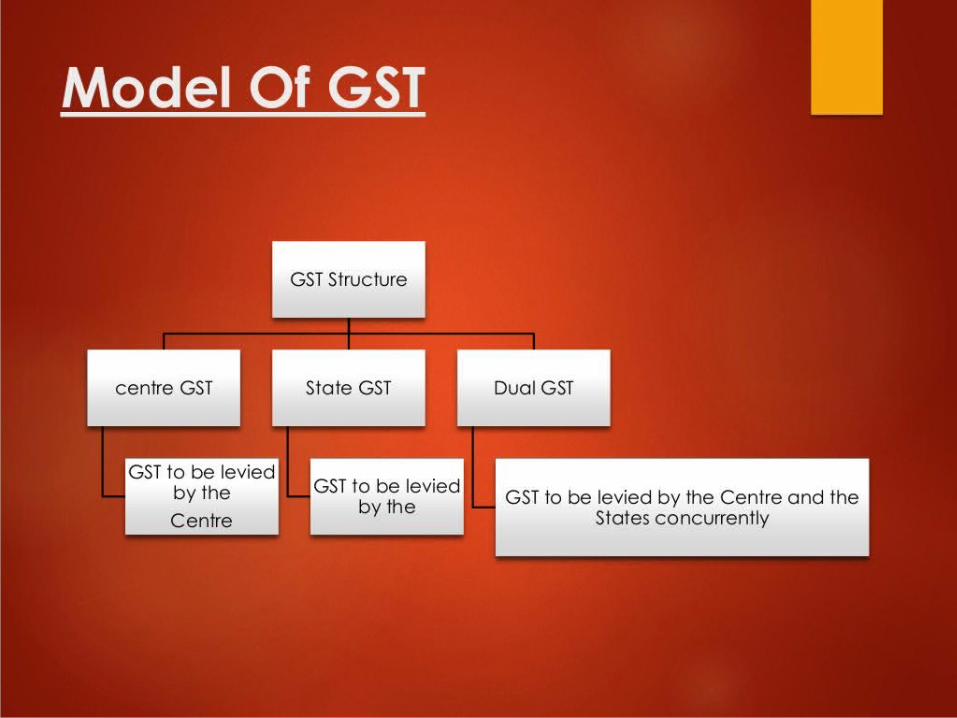

paper on GST in nov, 2009. Only Canada has dual GST model(Just like India is

going to implement Dual GST Model).

WHY GST 1. Estimate is that GST can boost India’s GDP by 1-2

per cent. 2. GST will convert the country into unified market,

replacing most indirect taxes with one tax. 3. GST will to provide the benefits of simplification of

tax regime, broadening of tax base, elimination of tax cascades, enhancing export competitiveness, ensuring greater regional equity, and improvement in transparency.

4. GST is a Value added tax, i.e., the final consumer will bear only the GST charged by the last dealer in the supply chain, with set-off benefits at all the previous stages.

5. GST has become a preferred global standard. All OECD countries, except the US, follow this taxation structure.

NEED FOR GSTIntroduction of a GST to replace the existing multiple tax structures of Centre and State taxes is not only desirable but imperative in the emerging economic environment. Increasingly, services are used or consumed in production and distribution of goods and vice versa. Separate taxation of goods and services often requires splitting of transaction values into value of goods and services for taxation, which leads to greater complexities, administration and compliances costs. Integration of various taxes into a GST system would make it possible to give full credit for inputs taxes collected. GST, being a destination-based consumption tax based on VAT principle, would also greatly help in removing economic distortions and will help in development of a common national market.

WHO IS BUILDING A SOFTWARE OF GST “Infosys has been awarded the contract of Rs.1,380 crore to

build and maintain the GST system. After the system is operational, Infosys will operate the system for a period of five years,” said Navin Kumar, chairman of GSTN.

According to existing government guidelines, open-source technology will be used by Infosys. Tata Consultancy Services Ltd, Wipro Ltd, Tech Mahindra Ltd and Microsoft Corp. were the other companies in the fray, Kumar confirmed.

GST-HOW IT WORKS The dealers registered under GST(manufacturers,

wholesalers and retailers and service providers)will charge GST on the price of goods and services from their customers.

They will claim credits for the GST included in the price of their own purchases of goods and service used by them.

The sellers or service provider collect the tax from their customer , who may or may not be the ultimate customer, and before depositing the same to the exchequer, they have already paid.

GST - SALIENT FEATURES It would be applicable to all transactions of goods and service. It to be paid to the accounts of the Centre and the States

separately. The rules for taking and utilization of credit for the Central

GST and the State GST would be aligned. Cross utilization of ITC between the Central

GST and the State GST would not be allowed except in the case of inter-State supply of goods.

The Centre and the States would have concurrent jurisdiction for the entire value chain and for all taxpayers on the basis of thresholds for goods and services prescribed for the States and the Centre.

The taxpayer would need to submit common format for periodical returns, to both the Central and to the concerned State GST authorities.

Each taxpayer would be allotted a PAN-linked taxpayer identification number with a total of 13/15 digits.

WHET ARE EFFECTS OF GST ON INDIAN ECONOMY

Positive Changes Once GST Is Passed. Due to various Centre and State taxes, a consumer today pays 25-27%

more for a product, compared to what it actually coasted to be manufactured. Although there is no mention of a cap, but as per experts, GST can be limited at 18-20% once approved in the Lok Sabha. Thus, the prices of goods can come down.

Prices of small cars and two-wheelers can drastically come down once GST Bill is approved. As of now, small cars which have length of less than 4 meters and engine capacity less than 1500 cc are taxed at 30.4%, which will come down to 18-20% with GST. A price drop of10% is expected by the industry. However, prices of luxury cars won’t be affected.

Prices of movie tickets is also expected to drop Prices of Made in India mobile phones and electronic gadgets can

come down, as various Inter-state taxes would be removed and a uniform tax structure would be implemented. However, doubts persists among handset makers and they have requested the Govt. for more clarification

– Govt. is pretty optimistic that ‘One Nation One Tax’policy can stop corruption as well

NEGATIVE CHANGES ONCE GST IS PASSED Effective service tax is presently 15%, which would increase to

18-20% once GST is passed. Hence, although prices of goods and products can come down, service industry will bear the brunt of higher taxes.

Air travel, hotels would become more expensive. Currently, economy class tickets are taxed 6% and non-economy class tickets are charged 9%. Once GST is implemented, it would increase to 18%, thereby leading to direct increase of 9-12% tax on the tickets. Unless the airlines absorb this increase, the additional tax has to be paid by the consumer

Insurance premiums, investments would be more expensive Cigarettes, branded clothes, branded jewellery, and even mobile

phone calls would be more expensive post GST A lot will change once GST Bill is approved, as there exists

several clauses and conditions pertaining to inter-state movements, power of States to levy tax and/or remove tax and the issue of 93% workers in India who are working in unorganized sector.

We will keep you updated as more details come in.

WHICH STATES ACCEPT GST Assam - 12 August,2016. Bihar 17 August,2016 Jharkhand 17 August, Himachal Pradesh 22 August Chhattisgarh 22 August, Gujarat 23 August, Madhya Pradesh 24 August, Delhi 24 August, Nagaland 26 August, Maharashtra 29 August, Haryana 29 August, Sikkim 30 August, Telangana 30 August, Mizoram 30 August, GOA 31 August, Odhisha 1 September, Rajasthan 2 September, Andhra Pradesh 9 September

WHAT WILL BE OUT OF GST? Levies on petroleum products Levies on alcoholic products Taxes on lottery and betting Basic customs duty and safeguard duties on

import of goods into India Entry taxes levied by municipalities or

panchayats Entertainment and Luxury taxes Electricity duties/ taxes Stamp duties on immovable properties Taxes on vehicles

EXEMPTION OF GOODS AND SERVICES Concept of providing threshold exemption of

GST Scope of composition and compounding

scheme under GST Items of GS to be exempt Treatment for goods exempt under one state

and taxable under the other

CONCLUSION The taxation of goods and services in India has, hitherto,

been characterized as a cascading and distortionary tax on production resulting in mis-allocation of resources and lower productivity and economic growth. It also inhibits voluntary compliance. It is well recognized that this problem can be effectively addressed by shifting the tax burden from production and trade to final consumption. A well designed destination-based value added tax on all goods and services is the most elegant method of eliminating distortions and taxing consumption. Under this structure, all different stages of production and distribution can be interpreted as a mere tax pass-through, and the tax essentially ‘sticks’ on final consumption within the taxing jurisdiction.

A ‘flawless’ GST in the context of the federal structure which would optimize efficiency, equity and effectiveness. The ‘flawless’ GST is designed as a consumption type destination VAT based on invoice-credit method.

![1261084 82 GS-30, GS-32, GS-46, GS-47 Slab Scissor [CE] · Operator's Manual CE GS™-1530/32 GS™-1930/32 GS™-2032 GS™-2632 GS™-3232 with Maintenance Information GS™-2046](https://img.dokumen.tips/doc/110x75/5f723aded681a6518a11728a/1261084-82-gs-30-gs-32-gs-46-gs-47-slab-scissor-ce-operators-manual-ce-gsa-153032.jpg)