Embed Size (px)

Citation preview

Team Members :

Peeyush Sahu

Abhishek Anand

Himanshu Varshney

Ravi Ranjan

PGPSM 2014-15

A Status Report

on

Highlights:

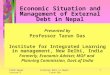

(i) At end-December 2013, India’s external debt stock stood at US$ 426.0 billion, recording

an increase of US$ 21.1 billion (5.2 per cent) over the level of US$ 404.9 billion at end-

March 2013. India’s external debt to GDP ratio stood at 23.3 per cent at end-December

2013 vis-à-vis 21.8 per cent at end-March 2013.

(ii) The rise in external debt during the period was due to long-term debt particularly NRI

deposits. A sharp increase in NRI deposits reflected the impact of fresh FCNR(B) deposits

mobilized under the swap scheme during September-November 2013.

(iii) At end-December 2013, long-term external debt was US$ 333.3 billion, showing an

increase of 8.1 per cent over the end-March 2013 level of US$ 308.2 billion. Long-term

external debt accounted for 78.2 per cent of total external debt at end-December 2013 vis-

à-vis 76.1 per cent at end-March 2013.

(iv) Short-term external debt was US$ 92.7 billion at end-December 2013, showing a

decline of 4.1 per cent over US$ 96.7 billion at the end-March 2013. Short-term debt

accounted for 21.8 per cent of total external debt at end-December 2013 (23.9 per cent at

end-March 2013).

(v) Valuation gain (appreciation of US dollar against the Indian rupee and other major

currencies) was US$ 11.9 billion and as such accounted for the decline in the debt stock at

end-December 2013 of equivalent amount. This implies that the increase in debt would

have been US$ 33.0 billion at end-December 2013 had there been no valuation gain.

(vi) The shares of Government (Sovereign) and non-Government debt in the total external

debt were 17.9 per cent and 82.1 per cent respectively, at end-December 2013.

(vii) The share of US dollar denominated debt was the highest in the external debt stock

and stood at 63.6 per cent at end-December 2013, followed by debt denominated in Indian

rupee (19.4 per cent), SDR (7.1 per cent), Japanese yen (5.0 per cent) and Euro (3.1 per

cent).

(viii) The ratio of short-term external debt (original maturity) to foreign exchange reserves

stood at 31.5 per cent at end-December 2013 (33.1 per cent at end-March 2013).

(ix) The ratio of concessional debt to total external debt declined to 10.6 per cent

at end-December 2013 from 11.2 per cent at end-March 2013.

0

50000

100000

150000

200000

250000

300000

350000

400000

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

De

bt

in (

)US

$ M

n

Years

India's External Debt - US $ Million

Introduction:

External debt (or foreign debt) is that part of the total debt in a country that

is owed to creditors outside the country. The debtors can be the government, corporations

or citizens of that country. The debt includes money owed to private commercial banks,

other governments, or international financial institutions such as the International Monetary

Fund (IMF) and World Bank.

"Gross external debt, at any given time, is the outstanding amount of those

actual current, and not contingent, liabilities that require payment(s) of principal and/or

interest by the debtor at some point(s) in the future and that are owed to nonresidents by

residents of an economy“

Outstanding and Actual Current Liabilities:

For this purpose, the decisive consideration is whether a creditor owns a

claim on the debtor. Here debt liabilities include arrears of both principal and interest.

Principal and Interest:

When this cost is paid periodically, as commonly occurs, it is known as an

interest payment. All other payments of economic value by the debtor to the creditor that

reduce the principal amount outstanding are known as principal payments. However, the

definition of external debt does not distinguish between whether the payments that are

required are principal or interest, or both. Also, the definition does not specify that the

timing of the future payments of principal and/or interest need be known for a liability to

be classified as debt.

Residence:

To qualify as external debt, the debt liabilities must be owed by a resident to

a nonresident. Residence is determined by where the debtor and creditor have their centers

of economic interest—typically, where they are ordinarily located—and not by their

nationality.

Current and Not Contingent:

Contingent liabilities are not included in the definition of external debt. These

are defined as arrangements under which one or more conditions must be fulfilled before a

financial transaction takes place. However, there is analytical interest in the potential

impact of contingent liabilities on an economy and on particular institutional sectors, such

as government.

Generally external debt is classified into four heads:

(1) public and publicly guaranteed debt

(2) private non-guaranteed credits;

(3) central bank deposits; and

(4) loans due to the IMF.

However the exact treatment varies from country to country. For example,

while Egypt maintains this four head classification, in India it is classified in seven heads:

(a) Multilateral

(b) Bilateral

(c) IMF loans

(d) Trade Credit

(e) Commercial Borrowings

(f) NRI Deposits

(g) Rupee Debt

(h) NPR Debt

Indicators of external debt sustainability:

There are various indicators for determining a sustainable level of external

debt. While each has its own advantage and peculiarity to deal with particular situations,

there is no unanimous opinion amongst economists as to one sole indicator. These

indicators are primarily in the nature of ratios i.e. comparison between two heads and the

relation thereon and thus facilitate the policy makers in their external debt management

exercise. These indicators can be thought of as measures of the country’s “solvency” in that

they consider the stock of debt at certain time in relation to the country’s ability to generate

resources to repay the outstanding balance.

Examples of debt burden indicators include the

(a) Debt to GDP ratio

(b) Foreign debt to exports ratio

(c) Government debt to current fiscal revenue ratio etc.

This set of indicators also covers the structure of the outstanding debt including the

(a) Share of foreign debt

(b) Short-term debt and

(c) Concessional debt in the total debt stock.

A second set of indicators focuses on the short-term liquidity requirements of

the country with respect to its debt service obligations. These indicators are not only useful

early-warning signs of debt service problems, but also highlight the impact of the inter-

temporal trade-offs arising from past borrowing decisions. Examples of liquidity monitoring

indicators include the:

(a) Debt service to GDP ratio

(b) Foreign debt service to exports ratio

(c) Government debt service to current fiscal revenue ratio etc.

The final indicators are more forward looking as they point out how the debt

burden will evolve over time, given the current stock of data and average interest rate. The

dynamic ratios show how the debt burden ratios would change in the absence of

repayments or new disbursements, indicating the stability of the debt burden. An example

of a dynamic ratio is the ratio of the average interest rate on outstanding debt to the

growth rate of nominal GDP.

External Debt Stock:

At end-December 2013, India’s total external debt stock was US$ 426.0

billion, showing an increase of US$ 21.1 billion (5.2 per cent) over the level of US$ 404.9

billion at end-March 2013 (Table 1). After declining for 2 quarters in a row, the stock of

external debt rose in the quarter ended December 2013 reflecting mainly the higher

mobilization under FCNR(B) deposits special swap window in September-November 2013.

Thus, long-term debt increased by US$ 25.1 billion (8.1 per cent) to US$ 333.3 billion. As a

proportion of total debt, long-term debt was 78.2 per cent.

Short-term debt on the other hand recorded a decline of 4.1 per cent to

reach US$ 92.7 billion and constituted 21.8 per cent of the total external debt at end-

December 2013. Short-term debt witnessed decline during the period due to Foreign

Institutional Investor (FII) outflows from the debt segment and fall in trade related credit.

Quarter-wise change in external debt position since March 2012 is given in

Table 2 below. External debt at end-December 2013 increased by 5.9 per cent over the

previous quarter (end September 2013) and 8.1 per cent over the corresponding

quarter of previous year (end-December 2012).

External Debt Indicators:

The share of short-term debt in total external debt decreased to 21.8 per

cent at end-December 2013 from 23.9 per cent at end-March 2013. India’s foreign

exchange reserves provided a cover of 69.0 per cent to the external debt stock at end-

December 2013 (72.1 per cent at end-March 2013). The ratio of short-term external debt

to foreign exchange reserves was 31.5 per cent at end-December 2013, as compared to

33.1 per cent at end-March 2013. The ratio of concessional debt to total external debt

declined to 10.6 per cent at end-December 2013 from 11.2 per cent at end-March 2013,

reflecting the increasing share of non-Government debt. The key external debt indicators

are presented in Table 3.

Table 3: India’s Key External Debt Indicators

Key Components Causing Rise in India’s External Debt:

India’s external debt has witnessed substantial rise in recent period led by

both long-term as well as short-term debt components. Between end-March 2012 and end-

March 2013, long-term debt showed an increase of US$ 26.0 billion (9.7 per cent), while

the rise in short-term debt was US$ 18.5 billion (23.7 per cent). The sharp increase in

short-term debt was mainly on account of higher trade related credit. Of the total rise

(US$ 44.5 billion) of external debt at end-March 2013 over end March 2012, the

long-term debt accounted for 58.4 per cent of the total rise, while the rest (41.6 percent)

was on account of short-term debt.

The rise in long-term external debt was primarily due to higher

commercial borrowings and NRI deposits. The two components under long-term external

debt viz., commercial borrowings and NRI deposits have been major drivers of rise in

India’s external debt (Figure 2.5). The increase in commercial borrowings gives rise to

some concerns given that the depreciation of the rupee results in higher debt service

burden (in rupee terms) that may affect profitability and the balance sheets of corporate

that have large exposures to such borrowings.

Summary:

India's external debt (21.2 per cent of GDP) continues to be dominated by

borrowings of longer maturity. At end-March 2013, long-term debt accounted for 75.2 per

cent while the rest (24.8 percent) was short-term debt. The changing composition of

long term debt, as is evident from the decreasing shares of multilateral and bilateral

credit (and corresponding decline in the share of sovereign and concessional debt)

signifies a maturing market economy that is increasingly integrated into the world

economy. Though the rising shares of components viz. ECB are in line with the

broad policy orientation of the Indian economy (that has emphasized attracting foreign

savings into the economy over the past few decades), these developments signal

heightened exposure of the domestic corporate sector to external shocks including adverse

exchange rate movements.

Debt Service Payments:

India’s total external debt service payments at US$ 31.3 billion during 2012-

13, showed marginal improvement over the previous year. Debt service payments at this

level remain manageable as indicated by the debt service ratio of 5.9 per cent in

2012-13 viz’a’viz 6.0 per cent in 2011-12. Debt service on external commercial

borrowings, with share of 74.2 per cent, dominated the India’s total debt service payments,

followed by external assistance, NRI deposits and rupee debt. The dominance of

external commercial borrowings is an indication of growing recourse to the use of

ECBs by the companies to meet their financing requirements.

International Comparison:

International comparison based on World Bank's 'International Debt

Statistics 2013‘ indicates that India continues to be among the less vulnerable countries

and India’s key debt indicators compare well with other indebted developing countries.

India’s key debt indicators, especially debt to GNI ratio, debt service ratio, short-term to

total external debt and the cover of external debt provided by foreign exchange reserves

continues to be comfortable.

Sovereign External Debt:

Multilateral sources continue to dominate India’s sovereign external debt

and Japan remains the single largest bilateral creditor. A substantial portion of

sovereign external debt is denominated in SDRs mainly on account of borrowings from

IDA, as well as inclusion of ‘IMF Credits 'in the country’s external debt liabilities since

2004-05. Rupee denominated sovereign debt witnessed increase in recent period,

reflecting the liberalization of FII investment in Government Treasury/securities.

Government guaranteed external debt has continued to remain low.

External Debt Management:

India’s external debt has remained within manageable limits due to

prudent external debt management policy of the Government of India. The policy

continues to focus on monitoring long and short-term debt, raising sovereign loans on

concessional terms with longer maturities, regulating external commercial borrowings

through end-use, all-in-cost and maturity restrictions; and rationalizing interest rates on

Non-Resident Indian deposits.

ooooooo