Embed Size (px)

Citation preview

2-1

Basic Cost Accounting Concepts

2-2

What is Cost Accounting?

The branch of accounting that deals with calculation of cost per unit, management of cost per unit and control of cost per unit is called cost accounting

2-3

Objectives of Cost Accounting1-To calculate accurate profit2-To calculate correct value of ending inventories 3-To calculate correct value of C.G.S4- To calculate accurate price of Goods

2-4

Learning Objective 1

Identify and give examples of each of the

three basic manufacturing cost

categories.

2-5

The ProductThe Product

DirectMaterials

DirectMaterials

DirectLaborDirectLabor

ManufacturingOverhead or FOH

ManufacturingOverhead or FOH

Classifications of Manufacturing Costs

2-6

Direct Materials

Raw materials that become an integral part of the product and that can be

easily traceable

Example: Tyres in an automobileExample: Tyres in an automobile

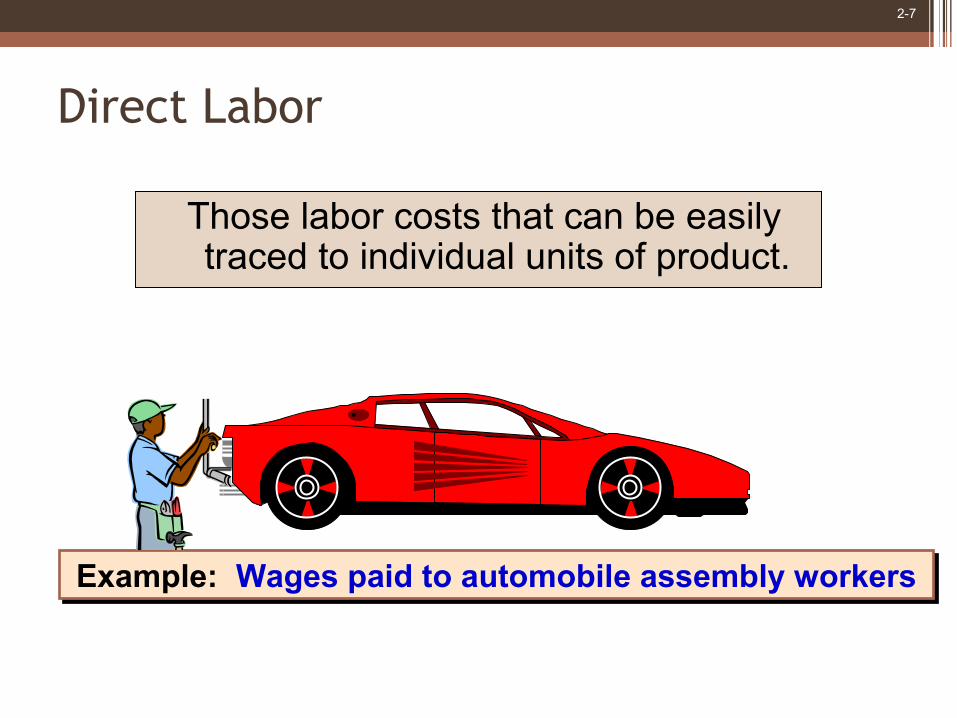

2-7

Direct Labor

Those labor costs that can be easily traced to individual units of product.

Example: Wages paid to automobile assembly workersExample: Wages paid to automobile assembly workers

2-8

Manufacturing OverheadManufacturing costs that cannot be easily traced directly to specific units produced.

Examples: Indirect materials and indirect laborExamples: Indirect materials and indirect labor

2-9

Nonmanufacturing Costs

Administrative Costs

All executive, organizational, and

clerical costs.

2-10

Learning Objective 2

What is difference between product costs

and period costs and give examples of each.

2-11

Product Costs Versus Period Costs

Product costs include direct materials, direct

labor, and manufacturing

overhead.

Period costs include all selling costs and

administrative costs.

Inventory Cost of Good Sold

BalanceSheet

IncomeStatement

Sale

Expense

IncomeStatement

2-12

Quick Check

Which of the following costs would be considered a period rather than a product cost in a manufacturing company?A. Manufacturing equipment depreciation.B. Property taxes on corporate headquarters.C. Direct materials costs.D. Electrical costs to light the production facility.E. Sales commissions.

2-13

Quick Check

Which of the following costs would be considered a period rather than a product cost in a manufacturing company?A. Manufacturing equipment depreciation.B. Property taxes on corporate headquarters.C. Direct materials costs.D. Electrical costs to light the production facility.E. Sales commissions.

2-14

Classifications of Costs

Manufacturing costs are oftenclassified as follows:

DirectMaterialDirect

MaterialDirectLaborDirectLabor

ManufacturingOverhead

ManufacturingOverhead

PrimeCost

ConversionCost

2-15

Learning Objective 3

Understand cost behavior patterns

including variable costs, fixed costs, and mixed

costs.

2-16

Cost Classifications for Predicting Cost Behavior

Cost behavior refers to how a cost will react to changes in the level of

activity. The most common

classifications are:

▫ Variable costs.

▫ Fixed costs

▫ Mixed costs.

2-17

Variable Cost

Your total texting bill is based on how many texts you send.

Number of Texts Sent

To

tal T

ext

ing

Bill

2-18

Variable Cost Per Unit

The cost per text sent is constant at Rs. 2 per text message.

Number of Texts Sent

Co

st P

er T

ext

Sen

t

2-19

Fixed Cost Your monthly contract fee for your cell phone is

fixed for the number of monthly minutes in your contract. The monthly contract fee does not change based on the number of calls you make.

Number of Minutes UsedWithin Monthly Plan

Mo

nth

ly C

ell

Ph

on

e C

on

tra

ct F

ee

2-20

Fixed Cost Per Unit

Within the monthly contract allotment, the average fixed cost per cell phone call made decreases as

more calls are made.

Number of Minutes UsedWithin Monthly Plan

Mo

nth

ly C

ell

Ph

on

e

Co

ntr

act

Fe

e

2-21

Fixed Costs and the Relevant Range

Fixed costs would increase Fixed costs would increase at a rate of $30,000 for each at a rate of $30,000 for each additional 1,000 square feet. additional 1,000 square feet.

For example, assume office space is available at For example, assume office space is available at a rental rate of $30,000 per year in increments of a rental rate of $30,000 per year in increments of

1,000 square feet. 1,000 square feet.

2-22

Ren

t C

ost

in T

hous

ands

of

Do

llars

0 1,000 2,000 3,000 Rented Area (Square Feet)

0

30

60

Fixed Costs and the Relevant Range

90

Relevant

Range

2-23

Cost Classifications for Predicting Cost Behavior

Behavior of Cost (within the relevant range)

Cost In Total Per Unit

Variable Total variable cost Increase Variable cost per unitand decrease in proportion remains constant.

to changes in the activity level.

Fixed Total fixed cost is not affected Fixed cost per unit decreasesby changes in the activity as the activity level increase and

level within the relevant range. increases as the activity level falls.

2-24

Quick Check

Which of the following costs would be variable with respect to the number of cones sold at a Baskins & Robbins shop? (There may be more than one correct answer.)A. The cost of lighting the store.B. The wages of the store manager.C. The cost of ice cream.

2-25

Quick Check

Which of the following costs would be variable with respect to the number of cones sold at a Baskins & Robbins shop? (There may be more than one correct answer.)A. The cost of lighting the store.B. The wages of the store manager.C. The cost of ice cream.

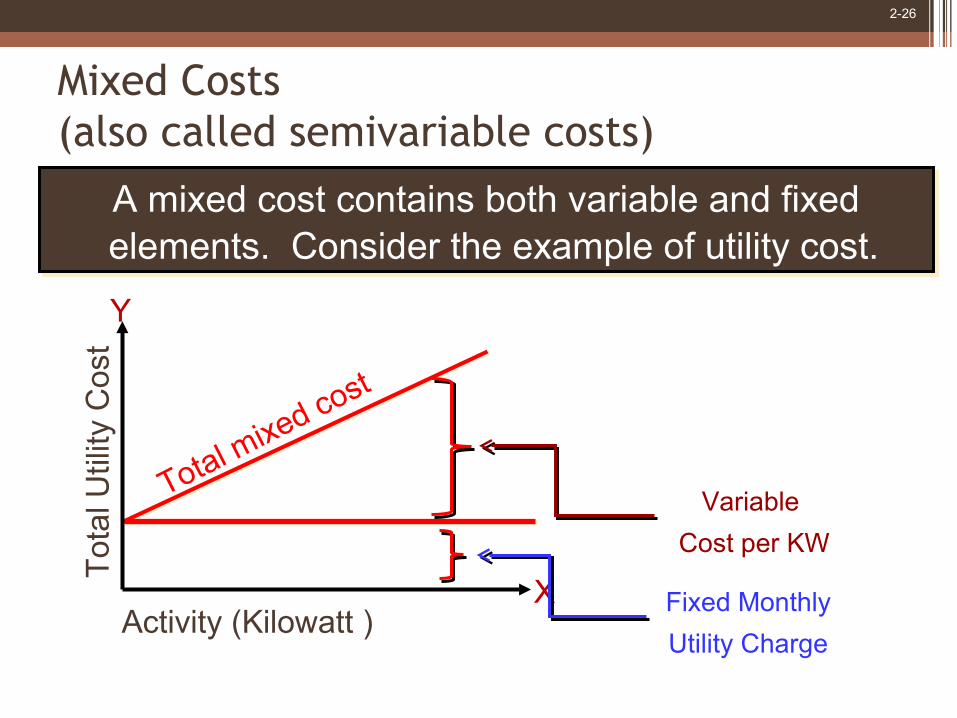

2-26

Fixed Monthly

Utility Charge

Variable

Cost per KW

Activity (Kilowatt )

Tot

al U

tility

Cos

t

X

Y

A mixed cost contains both variable and fixed elements. Consider the example of utility cost. A mixed cost contains both variable and fixed elements. Consider the example of utility cost.

Mixed Costs(also called semivariable costs)

Total mixed cost

2-27

Mixed Costs

Fixed Monthly

Utility Charge

Variable

Cost per KW

Activity (Kilowatt Hours)

To

tal U

tility

Co

st

X

Y

Total mixed cost

2-28

Mixed Costs – An Example

If your fixed monthly utility charge is $40, your If your fixed monthly utility charge is $40, your variable cost is $0.03 per kilowatt and your monthly variable cost is $0.03 per kilowatt and your monthly activity level is 2,000 kilowatt , what is the amount of activity level is 2,000 kilowatt , what is the amount of

your utility bill?your utility bill?

If your fixed monthly utility charge is $40, your If your fixed monthly utility charge is $40, your variable cost is $0.03 per kilowatt and your monthly variable cost is $0.03 per kilowatt and your monthly activity level is 2,000 kilowatt , what is the amount of activity level is 2,000 kilowatt , what is the amount of

your utility bill?your utility bill?

2-29

Learning Objective 4

Analyze a mixed cost using a scattergraph plot

and the high-low method.

2-30

Scattergraph Plots – An ExampleAssume the following hours of maintenance work

and the total maintenance costs for six months.

2-31

Plot the data points on a graph (Total Cost Y vs. Activity X).

Plot the data points on a graph (Total Cost Y vs. Activity X).

The Scattergraph Method

X

Y

Hours of Maintenance

Tota

l M

aint

enan

ce C

ost

2-32

The High-Low Method – An Example

The The variable cost variable cost per hourper hour of of

maintenance is maintenance is equal to the change equal to the change

in cost divided by in cost divided by the change in hours.the change in hours.

The The variable cost variable cost per hourper hour of of

maintenance is maintenance is equal to the change equal to the change

in cost divided by in cost divided by the change in hours.the change in hours.

= $6.00/hour$6.00/hour$2,400

400

2-33

The High-Low Method – An Example

Total Fixed Cost = Total Cost – Total Variable CostTotal Fixed Cost = Total Cost – Total Variable Cost

Total Fixed Cost = $9,800 – ($6/hour Total Fixed Cost = $9,800 – ($6/hour × 850 hours)× 850 hours)

Total Fixed Cost = $9,800 – $5,100Total Fixed Cost = $9,800 – $5,100

Total Fixed Cost = Total Fixed Cost = $4,700$4,700

2-34

The High-Low Method – An Example

YY = $4,700 + $6.00 = $4,700 + $6.00XXThe Cost Equation for Maintenance

2-35

Quick Check

Sales salaries and commissions are $10,000 when 80,000 units are sold, and $14,000 when 120,000 units are sold. Using the high-low method, what is the variable portion of sales salaries and commission?a. $0.08 per unitb. $0.10 per unit c. $0.12 per unitd. $0.125 per unit

2-36

Sales salaries and commissions are $10,000 when 80,000 units are sold, and $14,000 when 120,000 units are sold. Using the high-low method, what is the variable portion of sales salaries and commission?a. $0.08 per unitb. $0.10 per unit c. $0.12 per unitd. $0.125 per unit

Quick Check

2-37

Quick Check

Sales salaries and commissions are $10,000 when 80,000 units are sold, and $14,000 when 120,000 units are sold. Using the high-low method, what is the fixed portion of sales salaries and commissions?a. $ 2,000b. $ 4,000 c. $10,000d. $12,000

Sales salaries and commissions are $10,000 when 80,000 units are sold, and $14,000 when 120,000 units are sold. Using the high-low method, what is the fixed portion of sales salaries and commissions?a. $ 2,000b. $ 4,000 c. $10,000d. $12,000

2-38

Sales salaries and commissions are $10,000 when 80,000 units are sold, and $14,000 when 120,000 units are sold. Using the high-low method, what is the fixed portion of sales salaries and commissions?a. $ 2,000b. $ 4,000 c. $10,000d. $12,000

Sales salaries and commissions are $10,000 when 80,000 units are sold, and $14,000 when 120,000 units are sold. Using the high-low method, what is the fixed portion of sales salaries and commissions?a. $ 2,000b. $ 4,000 c. $10,000d. $12,000

Quick Check

2-39

Learning Objective 5

Prepare income statements for a

merchandising company using the traditional and

contribution formats.

2-40

The Traditional and Contribution Formats

Comparison of the Contribution Income Statement with the Traditional Income Statement

Traditional Format Contribution Format

Sales 100,000$ Sales 100,000$ Cost of goods sold 70,000 Variable expenses 60,000 Gross margin 30,000$ Contribution margin 40,000$ Selling & admin. expenses 20,000 Fixed expenses 30,000 Net operating income 10,000$ Net operating income 10,000$

2-41

Learning Objective 6

Understand the differences between direct and indirect

costs.

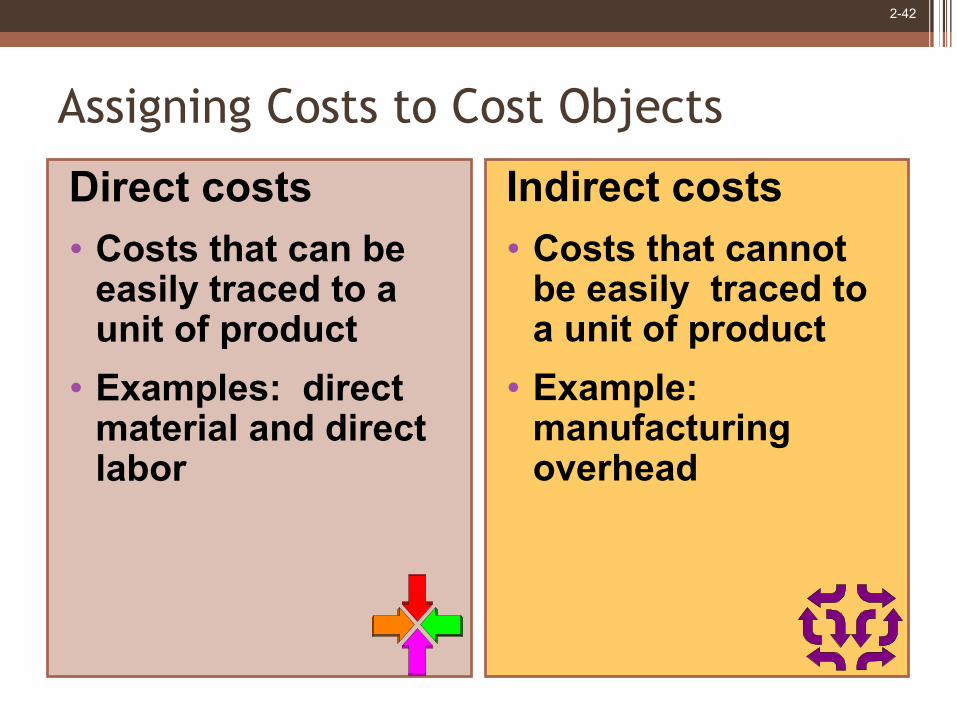

2-42

Assigning Costs to Cost Objects

Direct costs• Costs that can be

easily traced to a unit of product

• Examples: direct material and direct labor

Indirect costs• Costs that cannot

be easily traced to a unit of product

• Example: manufacturing overhead

2-43

Learning Objective 7

Understand cost classifications used in

making decisions: differential costs,

opportunity costs, and sunk costs.

2-44

Differential Cost and Revenue

Costs and revenues that differ among alternatives.

Example: You have a job paying $1,500 per month in your hometown. You have a job offer in a neighboring city that pays $2,000 per month. The travelling cost to the city is $300 per month.

Example: You have a job paying $1,500 per month in your hometown. You have a job offer in a neighboring city that pays $2,000 per month. The travelling cost to the city is $300 per month.

Differential revenue is: $2,000 – $1,500 = $500

Differential cost is: $300

2-45

Opportunity Cost

The potential benefit that is given up when one alternative

is selected over another.Example: If you werenot attending cost accounting class,you could be earning$25,00 per semester. Your opportunity costof attending accounting class for one semester is $25,00.

2-46

Sunk Costs

Sunk costs have already been incurred and cannot be changed now or in the

future. These costs should be ignored when making decisions.

2-47

Quick Check

Suppose you are trying to decide whether to drive or take the train to Portland to attend a concert. You have enough cash to do either, but you don’t want to waste money needlessly. Is the cost of the train ticket relevant in this decision? In other words, should the cost of the train ticket affect the decision of whether you drive or take the train to Portland?A. Yes, the cost of the train ticket is relevant.B. No, the cost of the train ticket is not relevant.

2-48

Quick Check

Suppose you are trying to decide whether to drive or take the train to Portland to attend a concert. You have ample cash to do either, but you don’t want to waste money needlessly. Is the cost of the train ticket relevant in this decision? In other words, should the cost of the train ticket affect the decision of whether you drive or take the train to Portland?A. Yes, the cost of the train ticket is relevant.B. No, the cost of the train ticket is not relevant.

2-49

Quick Check

Suppose you are trying to decide whether to drive or take the train to Portland to attend a concert. You have ample cash to do either, but you don’t want to waste money needlessly. Is the annual cost of licensing your car relevant in this decision?A. Yes, the licensing cost is relevant.B. No, the licensing cost is not relevant.

2-50

Quick Check

Suppose you are trying to decide whether to drive or take the train to Portland to attend a concert. You have ample cash to do either, but you don’t want to waste money needlessly. Is the annual cost of licensing your car relevant in this decision?A. Yes, the licensing cost is relevant.B. No, the licensing cost is not relevant.

2-51

Quick Check

Suppose that your car could be sold now for $5,000. Is this a sunk cost?A. Yes, it is a sunk cost.B. No, it is not a sunk cost.

2-52

Quick Check

Suppose that your car could be sold now for $5,000. Is this a sunk cost?A. Yes, it is a sunk cost.B. No, it is not a sunk cost.

2-53

Thank You