Embed Size (px)

Citation preview

What can the risk neutral moments tell us about futurereturns?

Juan ImbetNuria Mata

Barcelona GSE

[email protected]@barcelonagse.eu

June 29, 2015

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 1 / 27

Agenda

1 Objectives

2 Motivation

3 Literature Review

4 Methodolody

5 Results

6 Conclusions and future work

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 2 / 27

Objectives

Objectives

Estimate periodically the risk neutral distribution for several timehorizons

Test the predictability power of the statistical moments of thedistribution with respect to future returns

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 3 / 27

Motivation

Motivation

Return predictability has an important implication both forpractitioners and for financial models of risk and return.

We want to determine if investors’ expectations reflected in the riskneutral distribution contain information about future prices.

Investors in the options’ market seem to be more sophisticated thaninvestors in the stock market. Black (1975)

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 4 / 27

Literature Review

Return Predictability

Kendall (1953): Prices move in a random fashion

Use aggregate economic variables to predict future returnsFama and Schwert (1977), Keim and Stambaugh (1986), Fama andFrench (1989) and Kothari and Shanken (1997)

Use financial ratios to predict future returnsFama and French (1988), Campbell and Shiller (1988) and Cochrane(1991):

Do options’market lead the stock market, or vice versa?Diltz and Kim (1996), Finucane (1999), Manaster and Rendleman(1982)

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 5 / 27

Literature Review

Return Predictability (cont.)

Common regressors from the options’ market are the implied volatility(VIX) and the trading volume.

We test the predictability power of the moments of the risk neutraldistribution.

The common methodology consists of regressing returns on past lagsof the regressors

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 6 / 27

Literature Review

Return Predictability (cont.)

Inference is problematic because predictors are highly persistent

Standard inference analysis leads to overestimation of thepredictability power

Stambaugh (1999) and Lewellen (2004) propose a methodology tocorrect these issues.

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 7 / 27

Literature Review

Estimation of the risk neutral distribution

We will focus on the branch of non parametric estimations of the riskneutral distribution considering the following papers:

Ait-Sahalia and Lo (1998): Seminar paper on the estimation of theunconditional risk neutral distribution using the same variables as theBlack Scholes model.

Ait-Sahalia and Duarte (2003): Propose a methodology to estimatethe conditional distribution using information at the end of eachtrading day

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 8 / 27

Methodology

Methodology

Under no arbitrage conditions, the fundamental theorem of asset pricingmust hold:

pt = e−r(T−t)∫ ∞−∞

XT f (XT )dXT (1)

It is well known that we can recover the risk neutral distribution from calloption prices: Breeden and Litzenberger (1978)

f (x) = er(T−t)∂2C ()

∂K 2|K=x (2)

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 9 / 27

Methodology

Methodology (cont.)

At the end of each trading day what differs between call options is theirtime-to-maturity and the strike price.

It is coherent to estimate the call option function C () as a function ofthe strike price and time-to-maturities.

Instead of estimating the function itself, we will estimate all of itsderivatives jointly.

We can achieve this goal by a non parametric local polynomial fitting.

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 10 / 27

Methodology

Methodology (cont.)

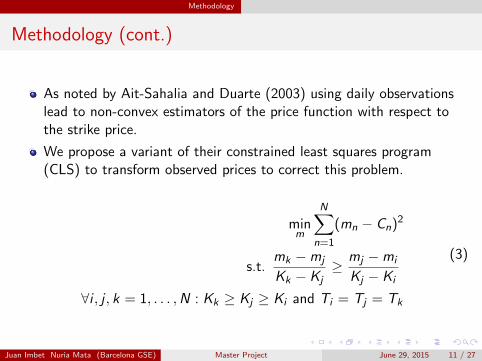

As noted by Ait-Sahalia and Duarte (2003) using daily observationslead to non-convex estimators of the price function with respect tothe strike price.

We propose a variant of their constrained least squares program(CLS) to transform observed prices to correct this problem.

minm

N∑n=1

(mn − Cn)2

s.t.mk −mj

Kk − Kj≥

mj −mi

Kj − Ki

∀i , j , k = 1, . . . ,N : Kk ≥ Kj ≥ Ki and Ti = Tj = Tk

(3)

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 11 / 27

Methodology

Methodology (cont.)

Assuming that the function C () is smooth enough, we approximate itaround a point (K0,T0) using a two dimensional Taylor expansion:

C (K0,T0) ≈2∑

k=0

(∑

i+j=k

βij(K − K0)i (T − T0)j) (4)

Where:

(i !)(j!)βij =∂ i+j

∂K i∂T jC (K0,T0) (5)

The risk neutral distribution can be estimated directly from β20

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 12 / 27

Methodology

Methodology (cont.)

We use a non parametric Generalized Least Squares (GLS) to estimate thederivatives of the function:

minβij

N∑n=1

[(mn −2∑

k=0

(∑

i+j=k

βij(Kn − K0)i (Tn − T0)j))κ(Ki−K0

hK)κ(Ti−T0

hT)

hKhT]

(6)

The weighted least squares estimator is therefore:

β = (X′ΩX)−1X′Ωm

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 13 / 27

Methodology

Methodology (cont.)

Where:

Ω =

ω1 0 . . . 00 ω2 . . . 0...

.... . .

...0 0 . . . ωN

, β =[(βij)i+j=k∀k=0,...3

](7)

ωn =κ(

Kn−K0hK

)κ(Tn−T0

hT)

hKhT

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 14 / 27

Methodology

Methodology (cont.)

And

, X =

1 (K1 − K0) (T1 − T0) (K1 − T0)(K1 − T0) (K1 − K0)

2 (T1 − T0)2

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

1 (KN − K0) (TN − T0) (KN − K0)(TN − T0) (KN − K0)2 (TN − T0)

2

(8)

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 15 / 27

Methodology

Methodology (cont.)

For each time-to-maturity we estimate the risk neutral distributionfrom the estimations of β20 around each strike price

We scale the distribution to have an integral of one

The four moments are estimated numerically using Riemann sums

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 16 / 27

Methodology

Methodology (cont.)

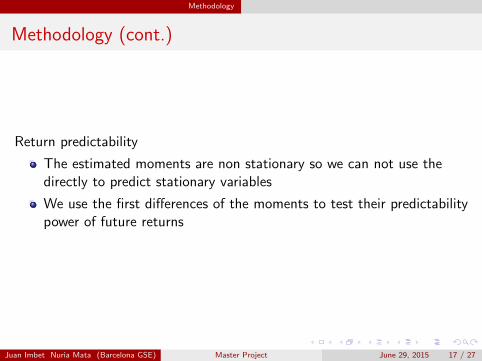

Return predictability

The estimated moments are non stationary so we can not use thedirectly to predict stationary variables

We use the first differences of the moments to test their predictabilitypower of future returns

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 17 / 27

Methodology

Methodology (cont.)

We follow the methodology from Lewellen (2004)

rt = α0 + αM∆Mt−1 + αV ∆Vt−1 + αS∆St−1 + αK∆Kt−1 + εt (9)

∆Mt = γ0M + γM∆Mt−1 + εMt (10)

∆Vt = γ0V + γV ∆Vt−1 + εVt (11)

∆St = γ0S + γS∆St−1 + εSt (12)

∆Kt = γ0K + γK∆Kt−1 + εKt (13)

Where M,V ,S ,K are the mean, volatility, skewness and kurtosis of thedistribution. ∆Xt = Xt − Xt−1 We assume that each one of theseregressors follows an AR(1) process.

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 18 / 27

Methodology

Methodology (cont.)

To test the significance of αM , αV , αs , αK we use the following adjustedstandard error estimator:

αi = αOLSi − θi (γi − γi ) i ∈ M,V , S ,K (14)

Where θi is estimated from the following regression:

εt = θiεit + υit (15)

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 19 / 27

Methodology

Methodology (cont.)

Assuming γi ≈ 1 the distribution of αi is:

αi ∼ N (αi , σ2υi

(X ′X )−1ii ) (16)

Where X is the matrix of regressors and σ2υi the variance of υi .

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 20 / 27

Results

Results

Data Description

We use S & P 500 options from January 4th 1996 to April 14th 2014as our study sample

We cleaned the data using the same conditions as in Ait-Sahalia andLo (1998)

Since in-the-money options are less liquid than out-of-the-money weuse put call parity to complete the spectrum of strike prices.

We use bandwidths proportional to the standard deviation of eachvariable

We use the standard Gaussian kernel

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 21 / 27

Results

Results (cont.)

The risk neutral distribution is estimated daily, weekly and monthly with atime horizon of 1, 8, and 30 days. Figure 1 shows as an example the dailyrisk neutral distribution with an horizon of 30 days during 2008:

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 22 / 27

Results

Predicting Returns

Figure: Testing the predictability power of the risk neutral moments

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 23 / 27

Results

Predicting Results (cont.)

There is no statistical evidence to conclude that the sample momentsof the risk neutral distribution predict future returns at any timehorizon considered.

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 24 / 27

Conclusions and future work

Conclusions

We made two main contributions: Methodologically, we extend theframework of Ait-Sahalia and Duarte (2003) to consider bothtime-to-maturities and strike prices as variables of the call optionprice function.

The empirical contribution consists of considering the first fourmoments of the risk neutral distribution as regressors to predictreturns.

Our results suggest that these statistical moments do not predictfuture returns

As far as we can tell this is the paper with the largest amount of riskneutral distributions estimated

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 25 / 27

Conclusions and future work

Suggestions for future research

Automatic data driven bandwidth selection algorithms

Use the risk neutral distribution to estimate the likelihood of eventsand use them to anticipate changes in the stock market.

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 26 / 27

Conclusions and future work

THANK YOU!Questions?

[email protected]@barcelonagse.eu

Juan Imbet Nuria Mata (Barcelona GSE) Master Project June 29, 2015 27 / 27