Embed Size (px)

Citation preview

US economy accelerating

but not yet in top gear

25th November 2014

Catherine L. Mann OECD Chief Economist

OECD Economic Outlook US and Global Briefing

GLOBAL OUTLOOK

2

The global economy is stuck in low gear

3

World GDP growth

Per cent, seasonally adjusted annualised rate

Source: November 2014 Economic Outlook database.

-8

-6

-4

-2

0

2

4

6

8

-8

-6

-4

-2

0

2

4

6

8

Average (1995-2007)

Trade growth has been weak

4

Trade intensity1

Index, 1990=100

1. Index of sum of exports and imports as a ratio of GDP. Source: November 2014 Economic Outlook database.

50

100

150

200

250

300

350

United States Trend (1990-2007)

50

100

150

200

250

300

350

Japan

50100150200250300350

European Union

50100150200250300350

BRIICS

5

Demand patterns are diverging

.

Non-residential investment per capita

Index, 2005 = 100

Private consumption per capita

Index, 2005 = 100

80

90

100

110

120

80

90

100

110

120 United States Euro area Japan

85

90

95

100

105

110

115

85

90

95

100

105

110

115United States Euro area Japan

Source: OECD National Accounts database; November 2014 Economic Outlook database; and OECD calculations.

6

Trends are also diverging among emerging economies

.

GDP per capita Volume, 2005=100

Source: OECD National Accounts database; November 2014 Economic Outlook database; IMF WEO database; Central Statistical Organisation, India; and OECD calculations.

80

100

120

140

160

180

200

220

240

80

100

120

140

160

180

200

220

240

China

India

Brazil

Russia

Growth projections for 2015-16

GDP Volume, percentage change

7

Source: November 2014 Economic Outlook database.

Column1 2013 2014 2015 2016World 3.1 3.3 3.7 3.9

United States 2.2 2.2 3.1 3.0Euro area -0.4 0.8 1.1 1.7

Japan 1.5 0.4 0.8 1.0China 7.7 7.3 7.1 6.9India 4.7 5.4 6.4 6.6Brazil 2.5 0.3 1.5 2.0Russia 1.3 0.3 0.0 1.6

Global risks are on the downside

There is a growing risk of euro area stagnation

Diverging monetary policies could lead to more volatility for emerging economy

Advanced economy debt levels are high and credit growth in some emerging economies has been rapid

Potential growth rates could fall further

8

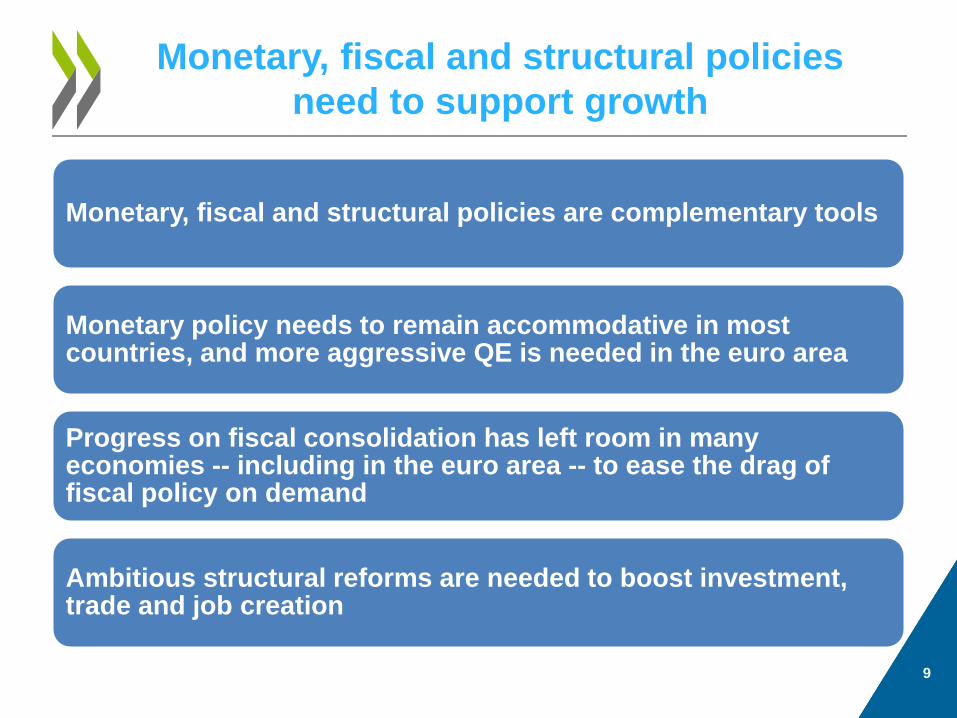

Monetary, fiscal and structural policies need to support growth

Monetary, fiscal and structural policies are complementary tools

Monetary policy needs to remain accommodative in most countries, and more aggressive QE is needed in the euro area

Progress on fiscal consolidation has left room in many economies -- including in the euro area -- to ease the drag of fiscal policy on demand

Ambitious structural reforms are needed to boost investment, trade and job creation

9

US OUTLOOK

10

11

Output is expected to accelerate relative to its trend over the past few quarters

GDP

Volume, 2009=100 Real GDP growth

Per cent, annual rate

12

Consumption accelerates modestly but all pistons are not firing

13

Household wealth has rebounded and deleveraging has largely run its course

14

Business investment looks mediocre

15

Residential investment accelerates but remains well below cruising speed

16

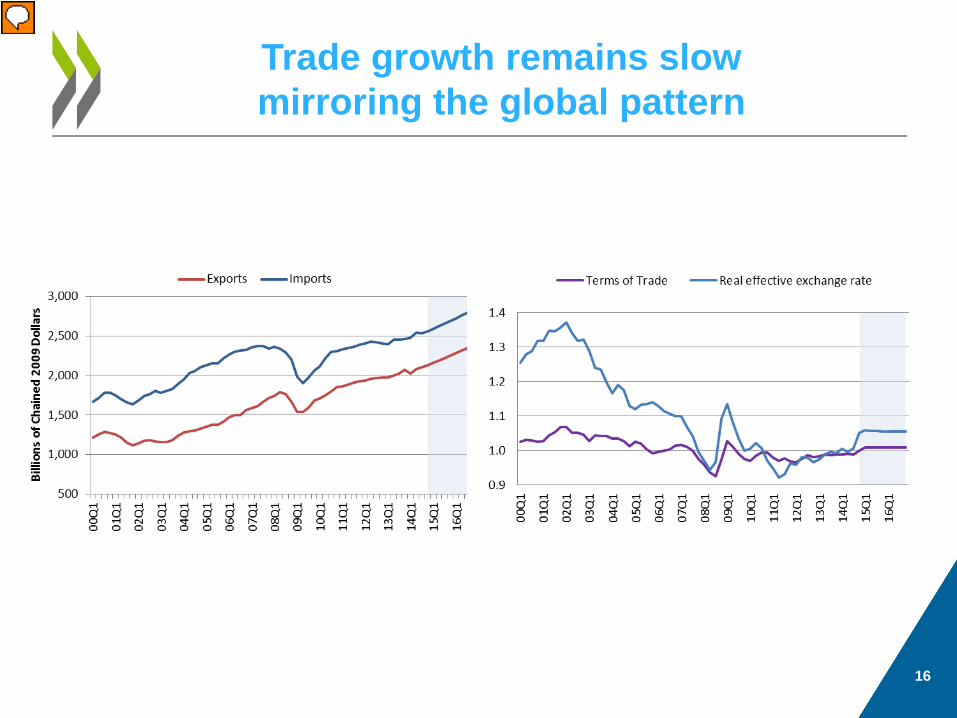

Trade growth remains slow mirroring the global pattern

17

The drag from fiscal consolidation is waning

Government spending Contribution to GDP growth 4 quarter moving average

Government fixed assets Annual growth rate

real net fixed assets (excluding defense)

18

The budget deficit has narrowed but debt remains high

19

Declines in unemployment running ahead of the recovery

20

Signs that labour market slack remains elevated

21

Labour market tightening should put upward pressure on wages and demand

22

Inflation rises but not achieve target

Risks

Acceleration of aggregate demand may not materialise

Normalisation of monetary policy could create financial market tensions

Upside and downside risks from the process of monetary policy normalisation

Household consumption and business investment may pick up more quickly than expected

23

Monetary and fiscal policy

Fiscal policy should focus on addressing longer-term pressures associated with healthcare spending and old age pensions

Assuming the recovery remains on track, policy rates should be gradually raised as labour-market slack is eliminated and wage growth becomes more apparent

Monetary policy rates should remain at their current low level through mid-2015

The authorities should facilitate infrastructure spending

24

25

More information…

data visualization tool

OECD Economic Outlook, November 2014

• Website with additional information

• Read this publication online

• Compare your country with OECD data

www.oecd.org/eco/economicoutlook.htm

OECD OECD Economics

Disclaimers: The statistical data for Israel are supplied by and under the responsibility of the relevant Israeli authorities. The use of such data by the OECD is without prejudice to the status of the Golan Heights, East Jerusalem and Israeli settlements in the West Bank under the terms of international law. This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.