Embed Size (px)

Citation preview

AIR

BEWARE!

CA AMEET PATEL

14th

November, 2016

Sometimes, air can harm

you

• Ask the residents of Delhi

• They will tell you what happens when AIR

is neglected

In Tax parlance also,

AIR

is equally important

What is AIR?

To keep a watch on high value transactions undertaken by

the taxpayer, the Income-tax law has framed the concept of

statement of financial transaction or reportable

account (previously called as ‘Annual Information

Return (AIR)’.

With the help of this statement, the tax authorities will

collect information on certain prescribed high value

transactions undertaken by a person during the year.

So,

technically, its no longer

AIR

but

FTRA

Who has to file an FTRA?

Statement of financial transaction or reportable

account is to be filed

• by certain prescribed entities

• and in such statement they are required to

furnish the details of specified financial

transactions or any reportable account

registered/recorded/maintained by them

during the year.

Who has to file an FTRA?

• the REGISTRAR or SUB-REGISTRAR appointed under section 6 of the

Registration Act, 1908;

• the registering authority empowered to register MOTOR VEHICLES under

Chapter IV of the Motor Vehicles Act, 1988;

• the POST MASTER GENERAL as referred to in clause (j) of section 2 of

the Indian Post Office Act, 1898;

• the COLLECTOR referred to in clause (g) of section 3 of the Right to Fair

Compensation and Transparency in Land Acquisition, Rehabilitation and

Resettlement Act, 2013;

• the recognised STOCK EXCHANGE referred to in clause (f) of section 2 of

the Securities Contracts (Regulation) Act, 1956;

Who has to file an FTRA?

• an officer of the RESERVE BANK OF INDIA, constituted under section 3 of

the Reserve Bank of India Act, 1934;

• a DEPOSITORY referred to in clause (e) of sub-section (1) of section 2 of

the Depositories Act, 1996; or

• a prescribed reporting financial institutions

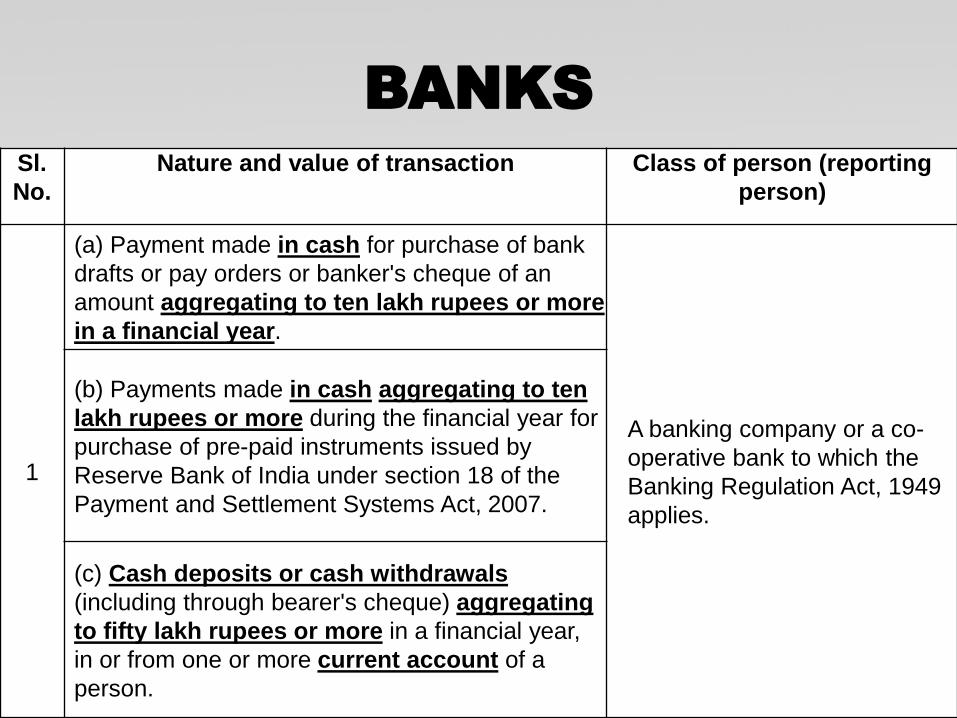

BANKS

Sl.

No.

Nature and value of transaction Class of person (reporting

person)

1

(a) Payment made in cash for purchase of bank

drafts or pay orders or banker's cheque of an

amount aggregating to ten lakh rupees or more

in a financial year.

A banking company or a co-

operative bank to which the

Banking Regulation Act, 1949

applies.

(b) Payments made in cash aggregating to ten

lakh rupees or more during the financial year for

purchase of pre-paid instruments issued by

Reserve Bank of India under section 18 of the

Payment and Settlement Systems Act, 2007.

(c) Cash deposits or cash withdrawals

(including through bearer's cheque) aggregating

to fifty lakh rupees or more in a financial year,

in or from one or more current account of a

person.

BANKS / POST OFFICES

Sl. No. Nature and value of transaction Class of person (reporting person)

2

Cash deposits aggregating to

ten lakh rupees or more in a

financial year, in one or more

accounts (other than a current

account and time deposit) of a

person.

(i) A banking company or a co-operative

bank to which the Banking Regulation Act,

1949 applies (including any bank or banking

institution referred to in section 51 of that

Act);

(ii) Post Master General10 as referred to in

clause (j) of section 2 of the Indian Post

Office Act, 1898.

BANKS / POST OFFICES /

NBFC / NIDHI

Sl. No. Nature and value of

transaction

Class of person (reporting person)

3

One or more time

deposits (other than a

time deposit made

through renewal of

another time deposit) of

a person aggregating to

ten lakh rupees or

more in a financial year

of a person.

(i) A banking company or a co-operative bank to which

the Banking Regulation Act, 1949 applies (including

any bank or banking institution referred to in section 51

of that Act);

(ii) Post Master General as referred to in clause (j) of

section 2 of the Indian Post Office Act, 1898;

(iii) Nidhi referred to in section 406 of the Companies

Act, 2013;

(iv) Non-banking financial company which holds a

certificate of registration under section 45-IA of the

Reserve Bank of India Act, 1934 (6 of 1934), to hold or

accept deposit from public.

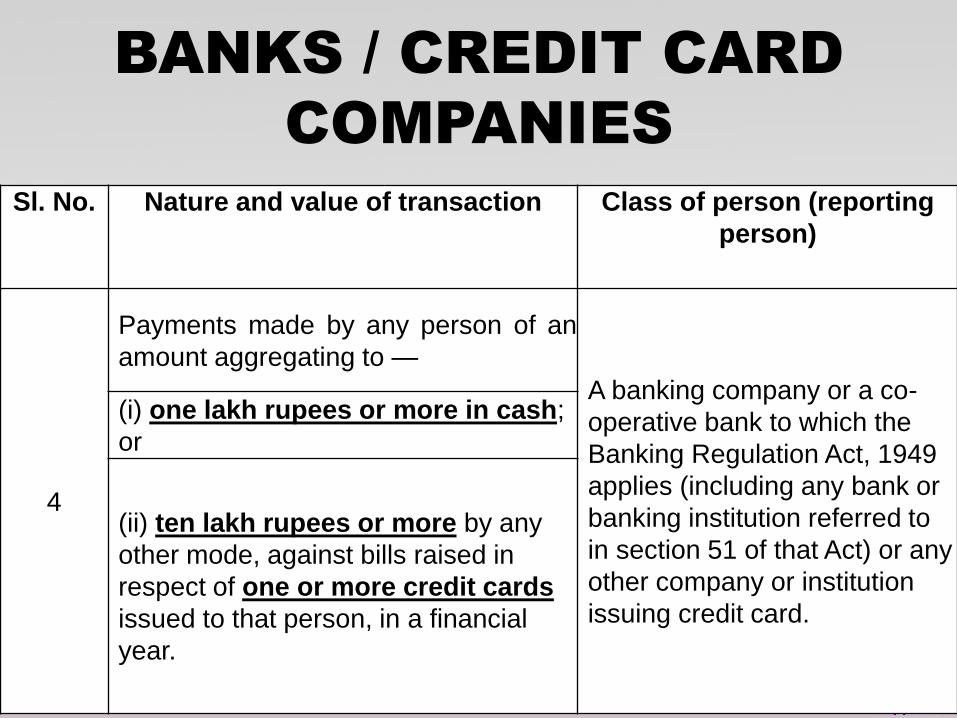

BANKS / CREDIT CARD

COMPANIES

Sl. No. Nature and value of transaction Class of person (reporting

person)

4

Payments made by any person of an

amount aggregating to —

A banking company or a co-

operative bank to which the

Banking Regulation Act, 1949

applies (including any bank or

banking institution referred to

in section 51 of that Act) or any

other company or institution

issuing credit card.

(i) one lakh rupees or more in cash;

or

(ii) ten lakh rupees or more by any

other mode, against bills raised in

respect of one or more credit cards

issued to that person, in a financial

year.

BOND ISSUERS

Sl. No. Nature and value of

transaction

Class of person

(reporting person)

5

Receipt from any person of an

amount aggregating to ten

lakh rupees or more in a

financial year for acquiring

bonds or debentures issued

by the company or institution

(other than the amount

received on account of

renewal of the bond or

debenture issued by that

company).

A company or institution

issuing bonds or

debentures.

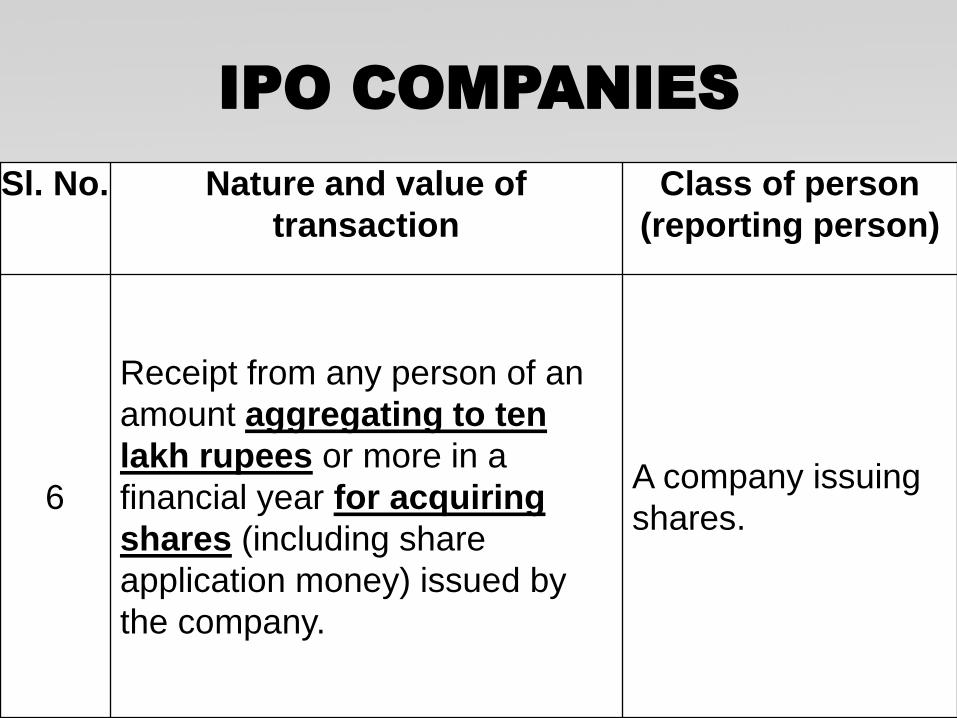

IPO COMPANIES

Sl. No. Nature and value of

transaction

Class of person

(reporting person)

6

Receipt from any person of an

amount aggregating to ten

lakh rupees or more in a

financial year for acquiring

shares (including share

application money) issued by

the company.

A company issuing

shares.

COMPANIES

Sl.

No.

Nature and value of

transaction

Class of person

(reporting person)

7

Buy back of shares

from any person (other

than the shares bought

in the open market) for

an amount or value

aggregating to ten lakh

rupees or more in a

financial year.

A company listed on a

recognised stock

exchange purchasing its

own securities under

section 68 of the

Companies Act, 2013.

MUTUAL FUNDS

Sl.

No.

Nature and value of

transaction

Class of person

(reporting person)

8

Receipt from any person of an

amount aggregating to ten

lakh rupees or more in a

financial year for acquiring

units of one or more

schemes of a Mutual Fund

(other than the amount

received on account of

transfer from one scheme to

another scheme of that

Mutual Fund).

A trustee of a Mutual

Fund or such other

person managing the

affairs of the Mutual

Fund as may be duly

authorised by the

trustee in this behalf.

FOREX DEALERS

Sl.

No.

Nature and value of transaction Class of person

(reporting person)

9

Receipt from any person for sale

of foreign currency including

any credit of such currency to

foreign exchange card or

expense in such currency through

a debit or credit card or through

issue of travellers cheque or draft

or any other instrument of an

amount aggregating to ten lakh

rupees or more during a financial

year.

Authorised

person as referred to

in clause (c) of

section 2 of the

Foreign Exchange

Management Act,

1999.

SUB REGISTRAR

Sl.

No.

Nature and value of

transaction

Class of person

(reporting person)

10

Purchase or sale by

any person of

immovable property

for an amount of thirty

lakh rupees or more

or valued by the stamp

valuation authority

referred to in section

50C of the Act at thirty

lakh rupees or more.

Inspector-General

appointed under

section 3 of the

Registration Act, 1908

or Registrar or Sub-

Registrar appointed

under section 6 of that

Act.

TAX AUDITEES

Sl.

No.

Nature and value of

transaction

Class of person

(reporting person)

11

Receipt of cash payment

exceeding two lakh

rupees for sale, by any

person, of goods or

services of any nature

(other than those specified

at Sl. Nos. 1 to 10)

Any person who is

liable for audit under

section 44AB of the

Act.

But its not only the AIR or

FTRA that you need to

worry about

You also need to know

CIB

CIB

In 1975, the Income Tax Department formed

the Central Information Branch (CIB) for

strengthening tax data-base. Initially, CIB

operated under the supervision of DGsIT

(Investigation). This was later brought under

the Directorate of Income Tax (Intelligence)

in June 2007.

CIB

The key function areas of DCI are

(i) widening of tax base through identification of stop filers

and non-filers

(ii) Deepening of tax base by providing information for proper

selection of cases for scrutiny assessments

(iii) through collection, collation of information from internal

as well as external sources and its dissemination to

Assessing officers (AOs) and other users in I.T. Dept.

It also collects information relating to financial transactions like

investment, expenses, payment of taxes, etc and details of

persons who are involved in some specified activities. The

mandate also provides for identification and investigation of cases

of tax evasion arising out of criminal matters, having any financial

implication punishable as an offence under any Direct Tax Law.

So, the ITO has two

tools with which he can

confront a tax payer

with massive dose of

information

AIR/FTRA & CIB

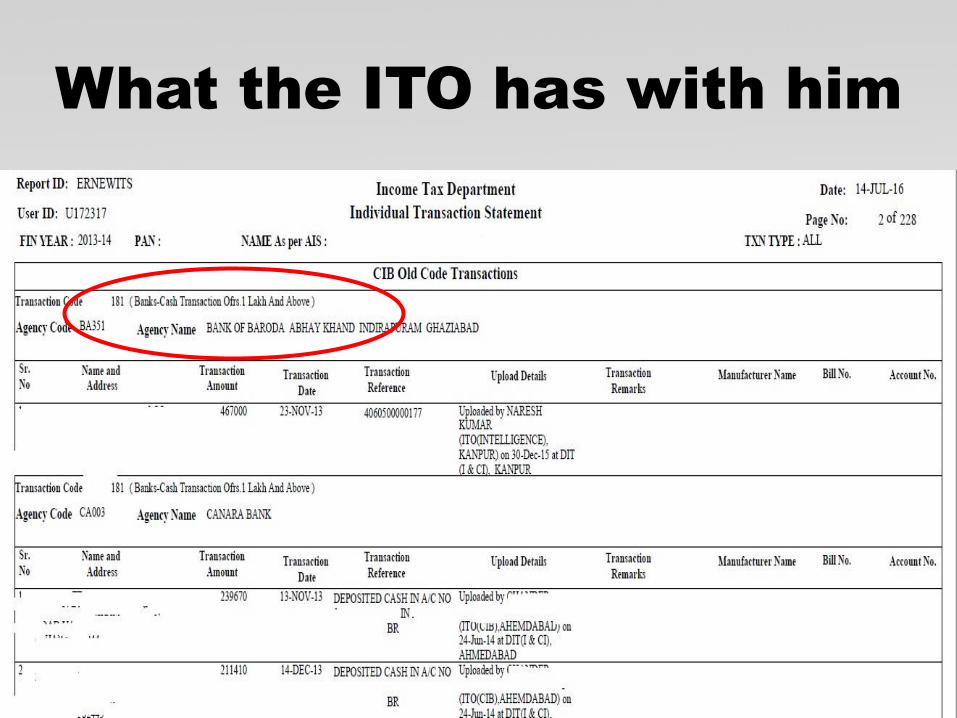

What the ITO has with him

What the ITO has with him

What the ITO has with him

What the ITO has with him

What the ITO has with him

How does this affect you?

• If return of income is not filed

• If return of income is filed

If return of income is not

filed

• Based on the transactions reported against

your PAN, you may get a notice for non

filing

• You will need to explain why you have not

filed the return

• Mostly the replies are to be given online

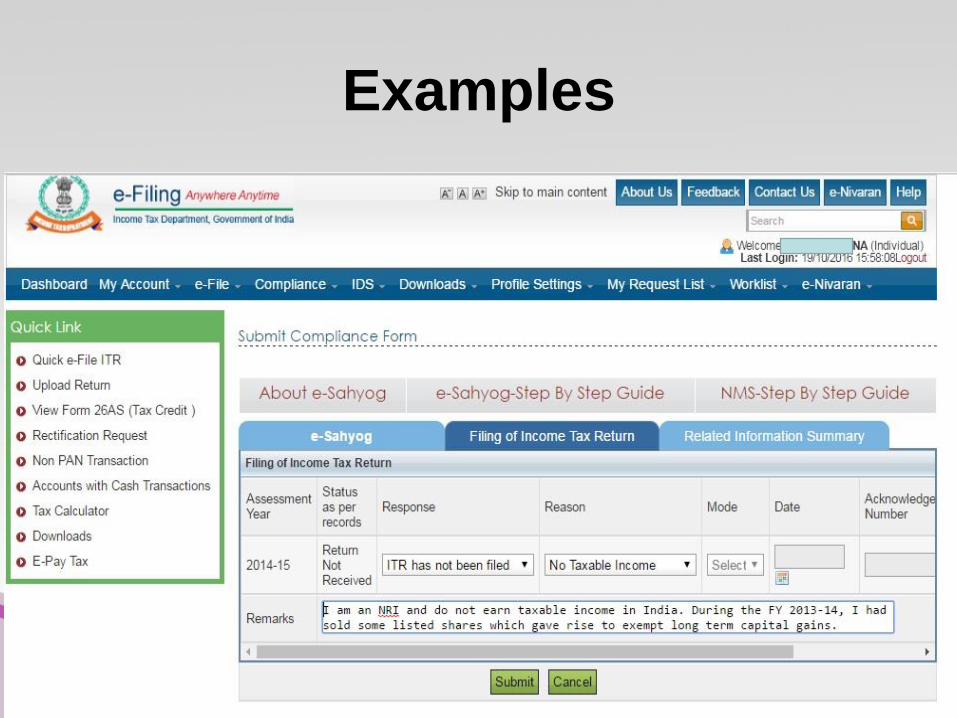

Examples

Examples

If return of income is not

filed

• Even if you have not given your PAN, you

will get a notice

• Non filers have got notices stating that PAN

is not mentioned in the document

• Do not under estimate the power and extent

of the analysis by the Income-tax

department of the data that they get through

AIR/FTRA & CIB

If return of income is filed

• Based on the transactions reported against

your PAN, you may get a notice for scrutiny

• You will need to match the reported

transactions / information with your return /

books of account

Demonetisation of

High

Denomination

Currency Notes

8/11

• The PM dropped a bombshell through his

address on TV

• Rs. 500 & Rs. 1000 notes are no longer

legal now

• How does this affect you?

• Most households in the country

would have a few of the high

denomination notes which are

now no longer legal tender

• What to do with these notes?

There are 2 aspects involved:

1. Depositing the money into

the bank or exchanging it for

new notes

2. Income-tax implications

Based on public

statements by the

Revenue

Secretary:

Scenario 1 –

House wife / Retired Person

• Deposit of cash upto Rs. 2,50,000 in

each account will not attract suspicion

and inquiry

• It will not be reported also

Scenario 2 –

Any other person

• Deposit of cash upto Rs. 2,50,000 in

each account will not attract suspicion

and inquiry

• It will not be reported also

Scenario 3 –

Businessman

a) Deposit of cash upto Rs. 10,00,000

b) Deposit of cash in excess of Rs.

10,00,000

Scenario 3(a) –

Businessman

Deposit of cash upto Rs. 10,00,000

i) Need to ensure that it can be explained

ii) Questions could be asked

iii) Scrutiny may be attracted

Scenario 3(b) –

BusinessmanDeposit of cash in excess of Rs.

10,00,000

i) Need to ensure that it can be explained

ii) Questions could be asked

iii) Scrutiny may be attracted

iv) If the amount does not match with the

returned income, it will be added to the

taxable income

Scenario 3(b) –

BusinessmanIf that amount is added to your income

then:

i) It will be considered as “tax evasion”

ii) You then pay tax + interest

iii) You also pay PENALTY

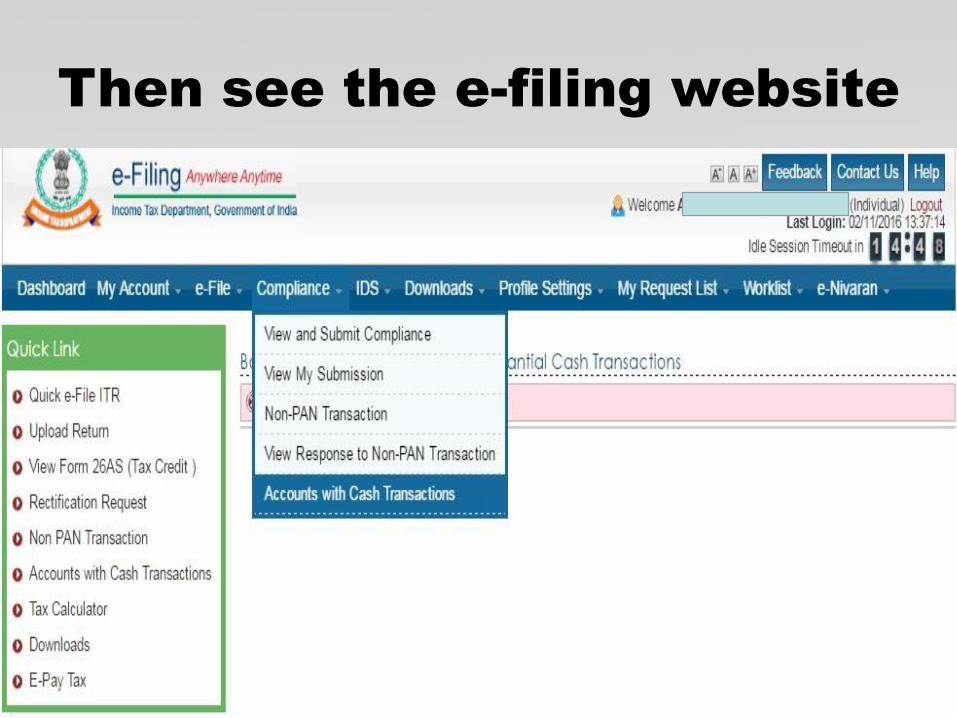

Need proof that

the government is

serious about

this?

Then see the e-filing website

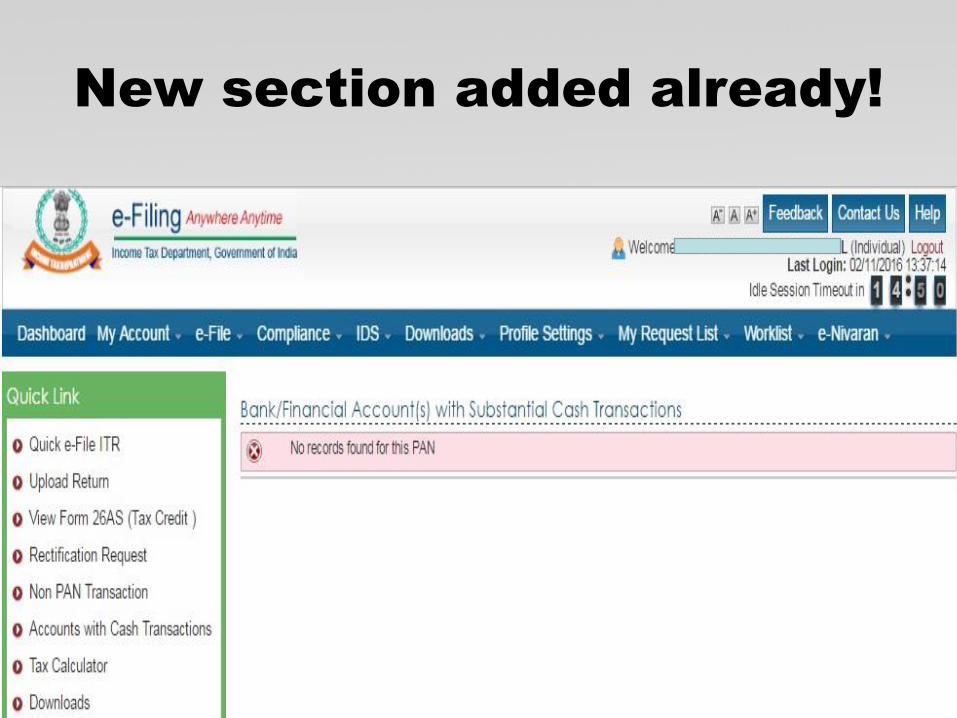

New section added already!

Can you show the cash as

current year’s income?

• Several messages on Whatsapp & Email

saying that tax + interest + PENALTY @

200% will be payable

• Is this correct?

PENALTY @ 200%

• Section 270A is being referred to

• This section talks of “unreported income”

• When you offer income to tax, can it be

said to be “unreported income”?

• Too many complications involved here

Penalty @ 200%

• Will they or will they not?

• Every case is different

• Facts of each case will be

looked at

• Scrutinies will be widespread

and many

Matching of cash deposited

• With current year’s books / income

• With earlier years’ income

• With other factors (debtors’ aging;

seasonal sales pattern, TCS returns (for

scrap sales) etc

• IS IT REALLY CURRENT YEAR’S

INCOME? This question is supremely

important

So, what to do?

• Don’t panic

• Don’t act in haste

• Think 100 times before depositing cash

into the bank

• Consult an honest tax consultant before

taking action

• DO NOT RELY ON WHATSAPP

MESSAGES / EMAIL / MEDIA REPORTS