Embed Size (px)

Citation preview

Click to edit Master title styleClick to edit Master title style

Beyond e-Invoicing

A pragmatic approach to

optimize your financial processes

FROM INSIGHT

TO REALIZATION

optimize your financial processes

Click to edit Master title styleClick to edit Master title style1. Introduction

Team

• Walter Deprins

• Jos Feyaerts

• Christophe Van Olmen

• Benjamin Coumont

Timing

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION2

Beyond e-invoicing

Timing• 16h30 – 18h30: seminar

• 18h30 – 20h00: drink & bite

Slides

Q&A

Click to edit Master title styleClick to edit Master title style

1. Introduction

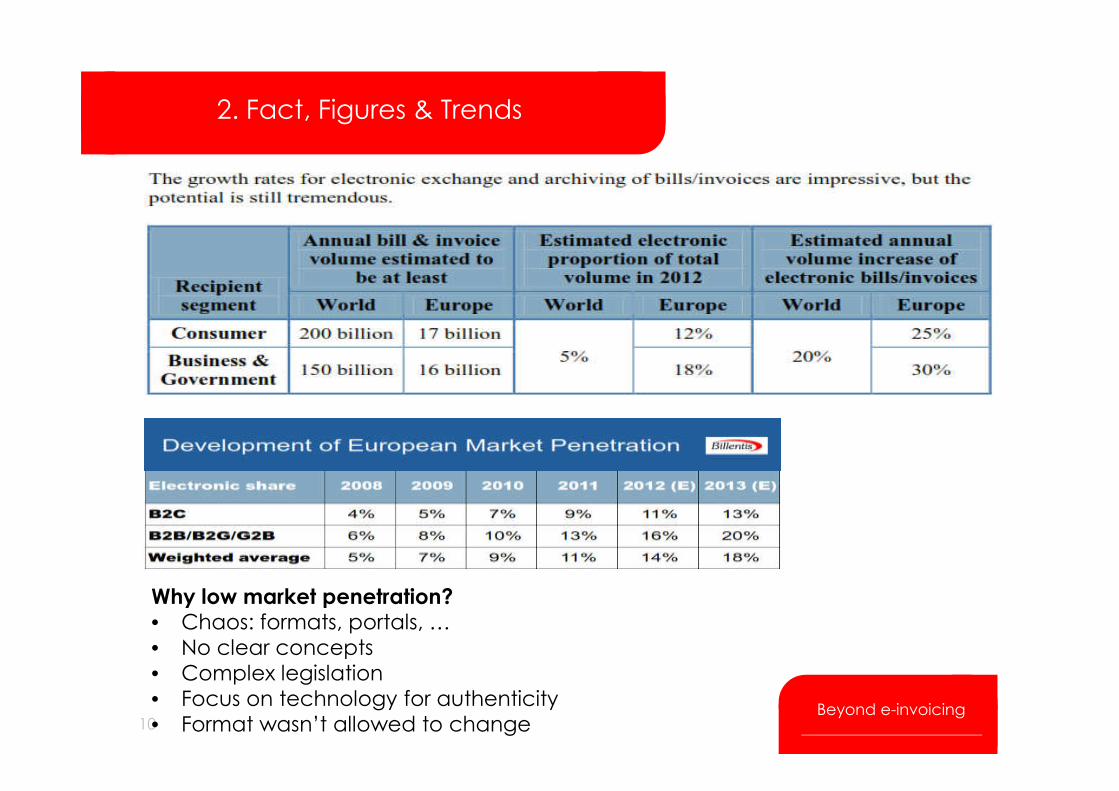

2. Facts, figures & trends

3. The new legal framework

4. Opportunities

Content

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

4. Opportunities

5. Building blocks

6. Our approach

7. Conclusion

3Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style1. Introduction

By using our e-invoicing:

no envelopes or looking after your cup of coffee between piles of invoices.

With our e-invoicing you will save time and eliminate input errorsYou can simply download invoice data as a PDF or structured file

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION4

You can simply download invoice data as a PDF or structured file

Afterwards you can load it into your ERP.

You can also view process related documents as orders and

transport documents on our portal. You can even download them.

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style1. Introduction

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION5

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

“IS THIS REALLY

AN IMPROVEMENT

1. Introduction

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

AN IMPROVEMENT

FOR THE RECEIVER?”

6Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style1. Introduction

Why still a traditional invoice process?

Digital isn't “special” anymore - it’s the new “normal”

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION7

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style1. Introduction

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION8

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style1. Introduction

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION9

Beyond e-invoicing

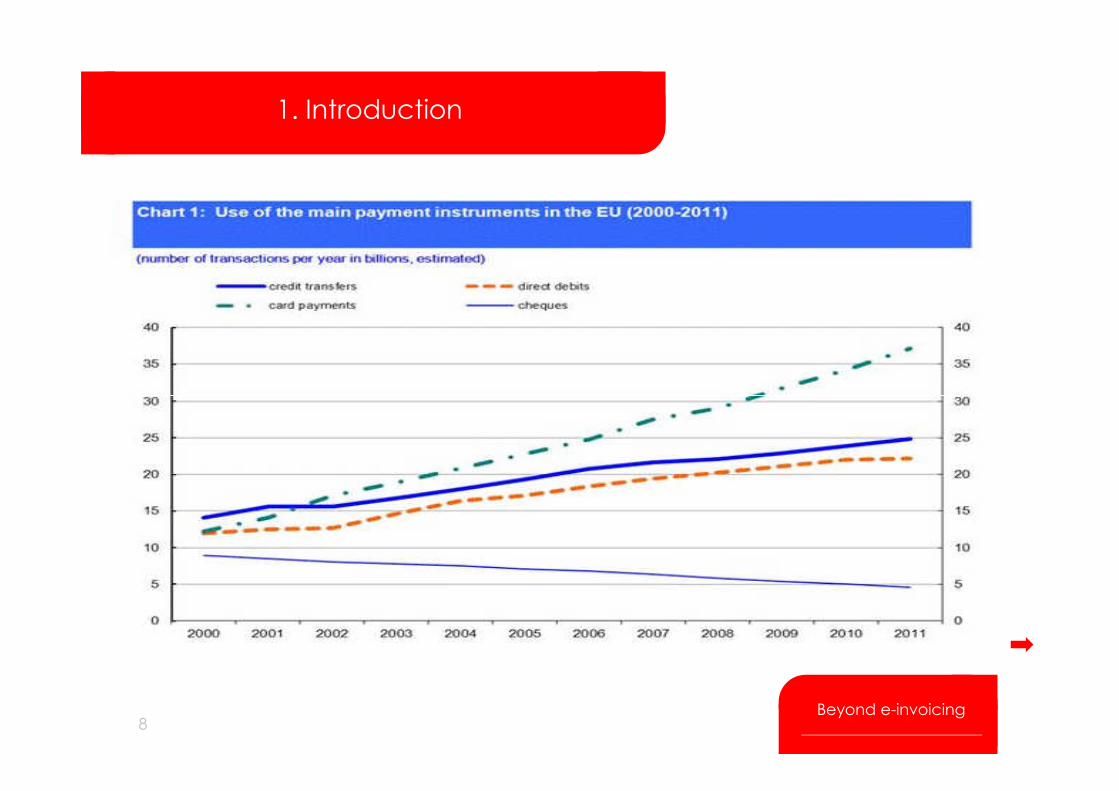

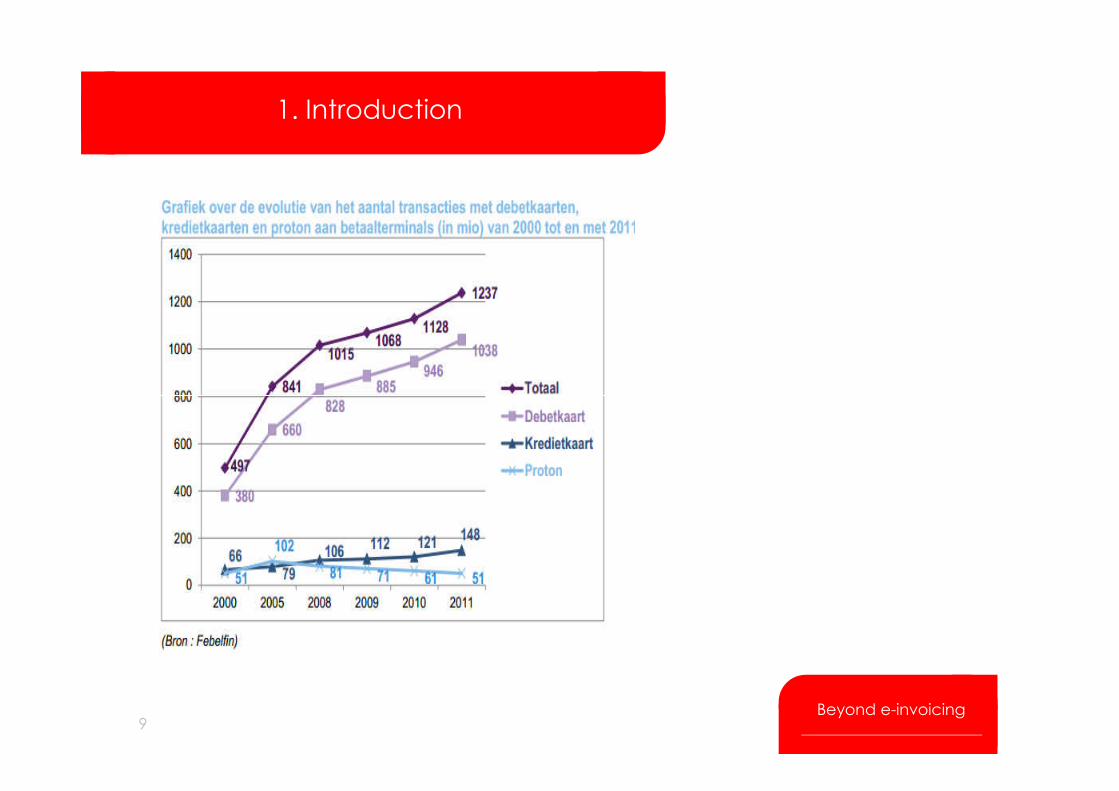

Click to edit Master title styleClick to edit Master title style2. Fact, Figures & Trends

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION10

Why low market penetration?• Chaos: formats, portals, …

• No clear concepts

• Complex legislation

• Focus on technology for authenticity

• Format wasn’t allowed to changeBeyond e-invoicing

Click to edit Master title styleClick to edit Master title style2. Fact, Figures & Trends

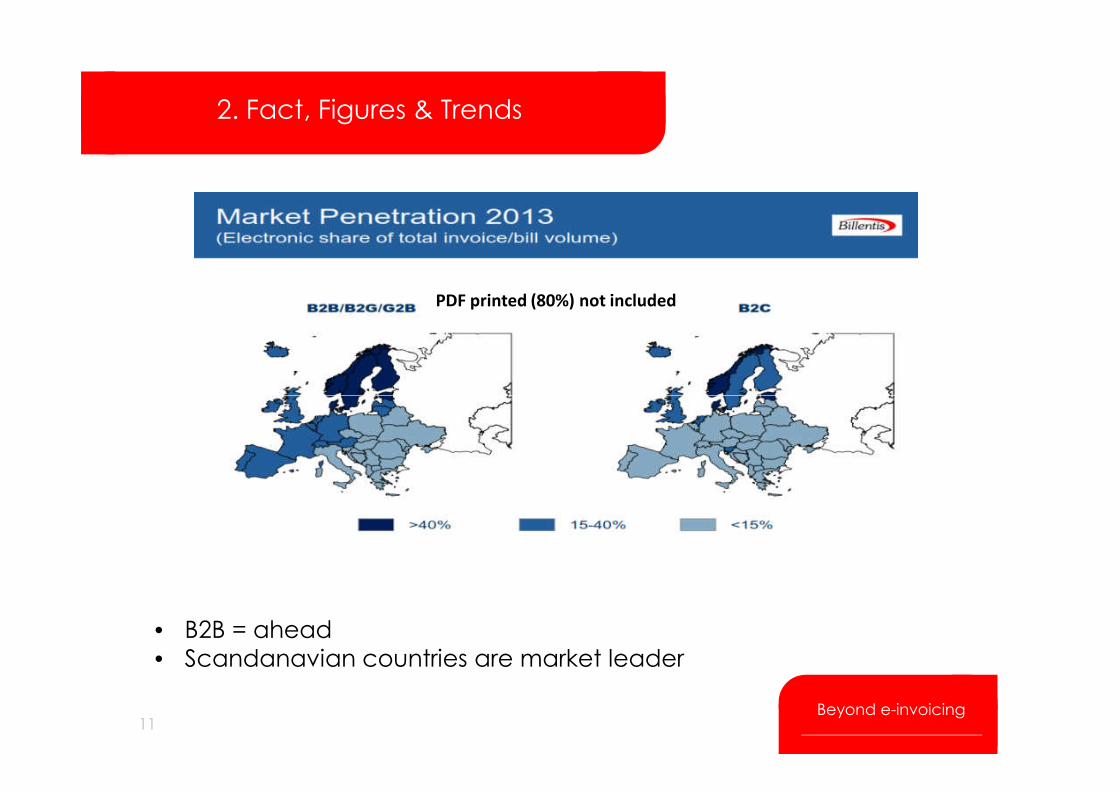

PDF printed (80%) not included

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION11

• B2B = ahead

• Scandanavian countries are market leader

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

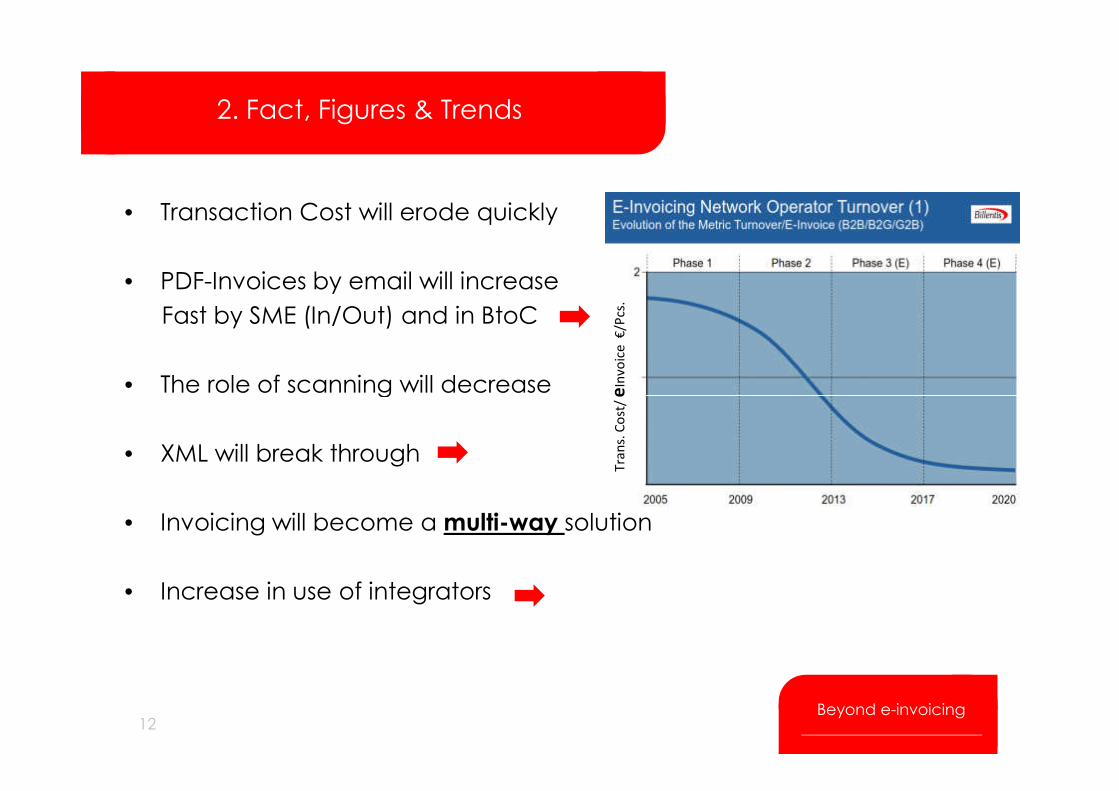

• Transaction Cost will erode quickly

• PDF-Invoices by email will increase

Fast by SME (In/Out) and in BtoC

• The role of scanning will decrease

2. Fact, Figures & Trends

eIn

vo

ice

€/P

cs.

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• The role of scanning will decrease

• XML will break through

• Invoicing will become a multi-way solution

• Increase in use of integrators

12

Tra

ns.

Co

st/ e

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style2. Fact, Figures & Trends

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION13

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style2. Fact, Figures & Trends

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION14

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

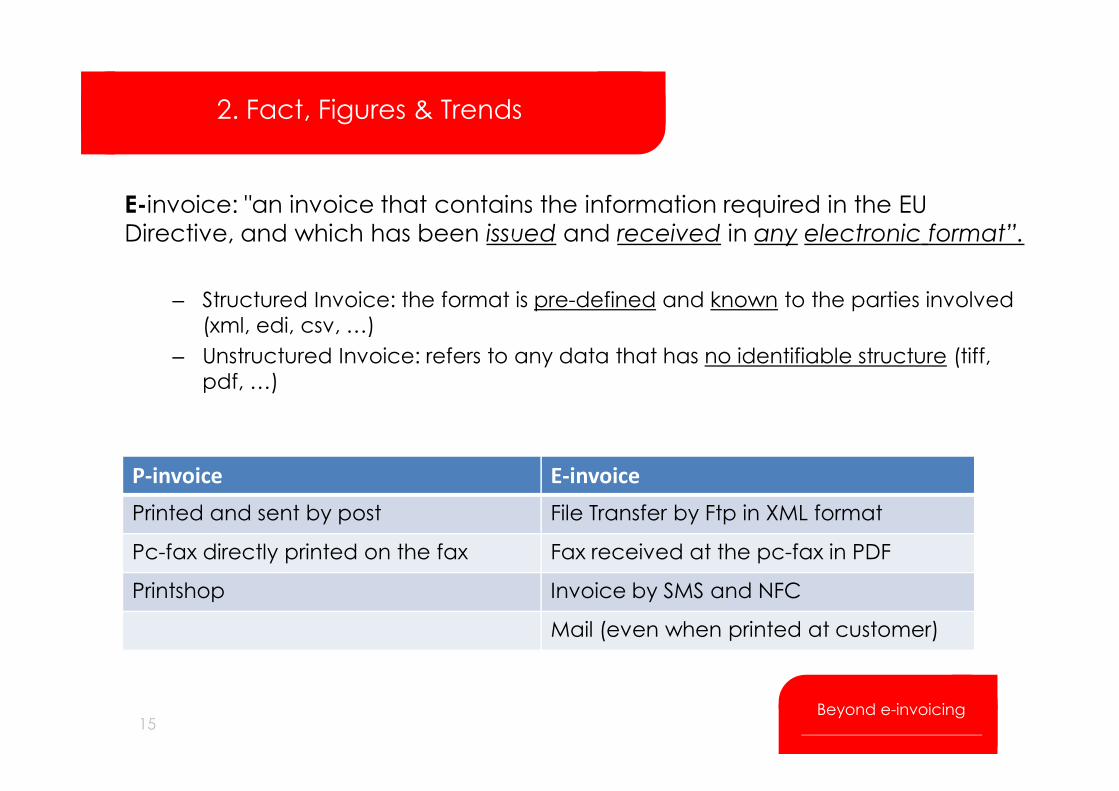

E-invoice: "an invoice that contains the information required in the EU

Directive, and which has been issued and received in any electronic format”.

– Structured Invoice: the format is pre-defined and known to the parties involved

(xml, edi, csv, …)

– Unstructured Invoice: refers to any data that has no identifiable structure (tiff,

pdf, …)

2. Fact, Figures & Trends

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

P-invoice E-invoice

Printed and sent by post File Transfer by Ftp in XML format

Pc-fax directly printed on the fax Fax received at the pc-fax in PDF

Printshop Invoice by SMS and NFC

Mail (even when printed at customer)

15Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

New Rules, new possibilities:

• Fundamentals of the EU directive: 2010/45/EU

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• VAT Highlights

• Self-Billing

• Related laws and upcoming initiatives

16Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

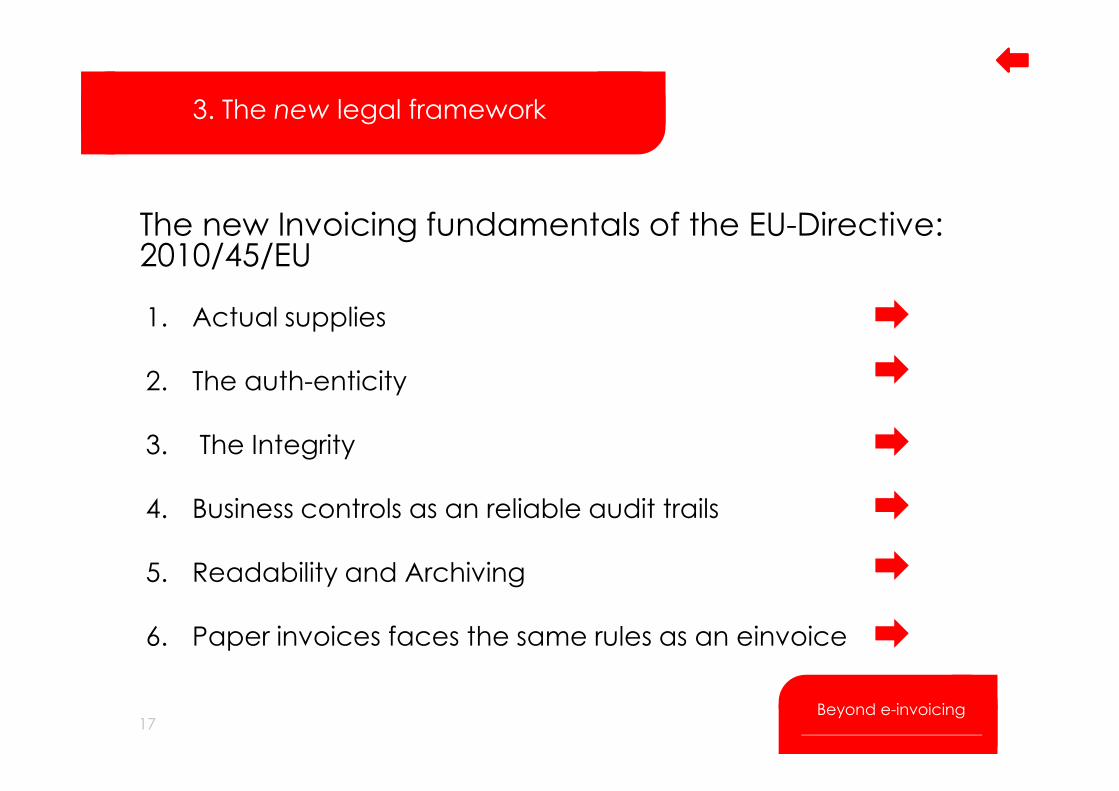

The new Invoicing fundamentals of the EU-Directive: 2010/45/EU

1. Actual supplies

2. The auth-enticity

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

2. The auth-enticity

3. The Integrity

4. Business controls as an reliable audit trails

5. Readability and Archiving

6. Paper invoices faces the same rules as an einvoice

17Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

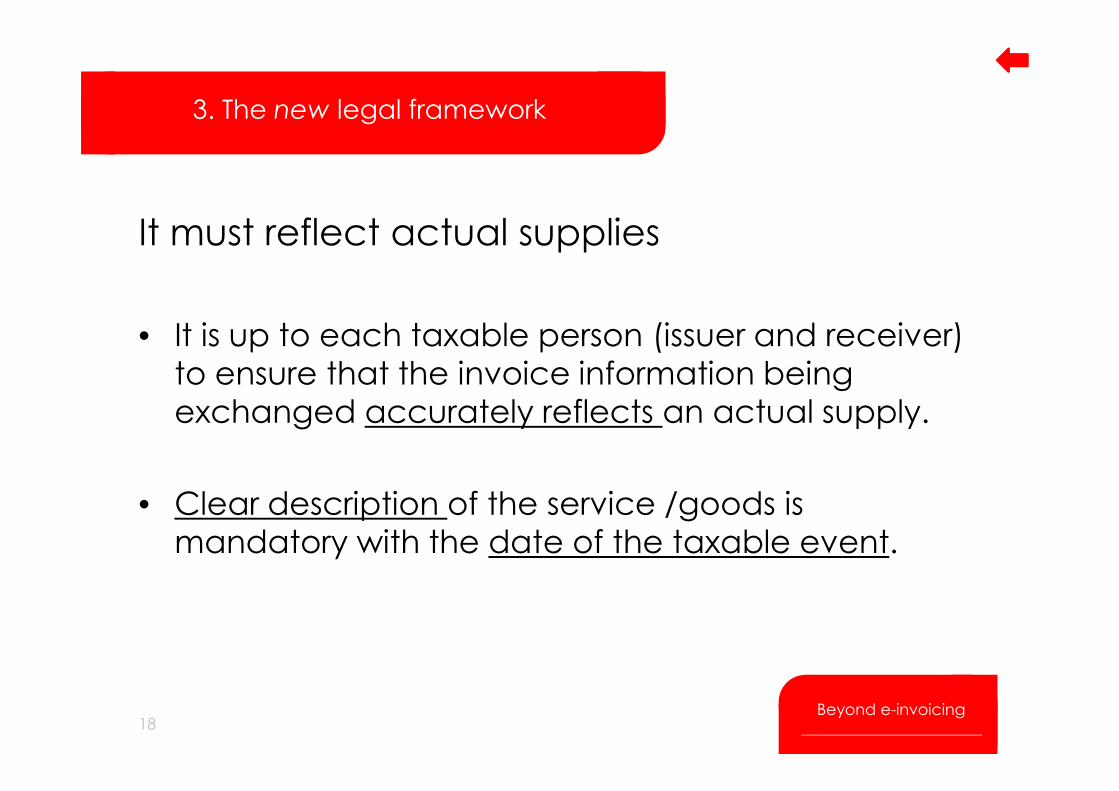

It must reflect actual supplies

• It is up to each taxable person (issuer and receiver)

to ensure that the invoice information being

exchanged accurately reflects an actual supply.

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

exchanged accurately reflects an actual supply.

• Clear description of the service /goods is

mandatory with the date of the taxable event.

18Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

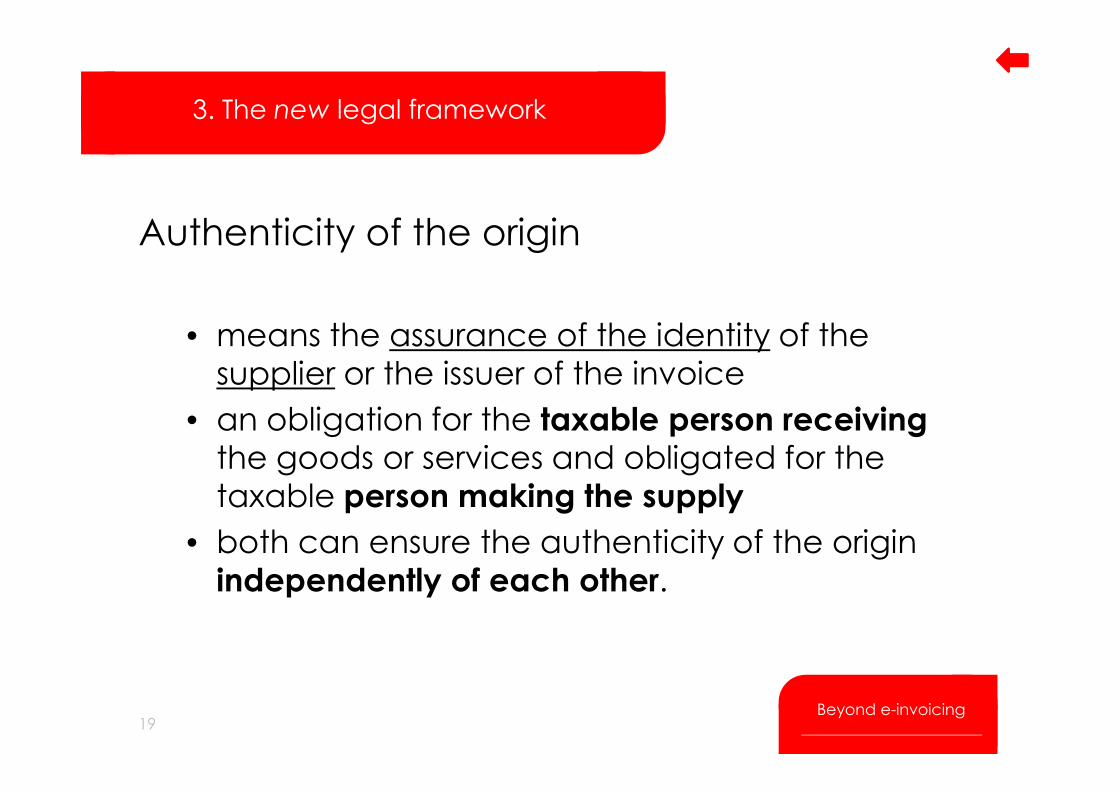

Authenticity of the origin

• means the assurance of the identity of the supplier or the issuer of the invoice

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• an obligation for the taxable person receiving

the goods or services and obligated for the

taxable person making the supply

• both can ensure the authenticity of the origin independently of each other.

19Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

Integrity

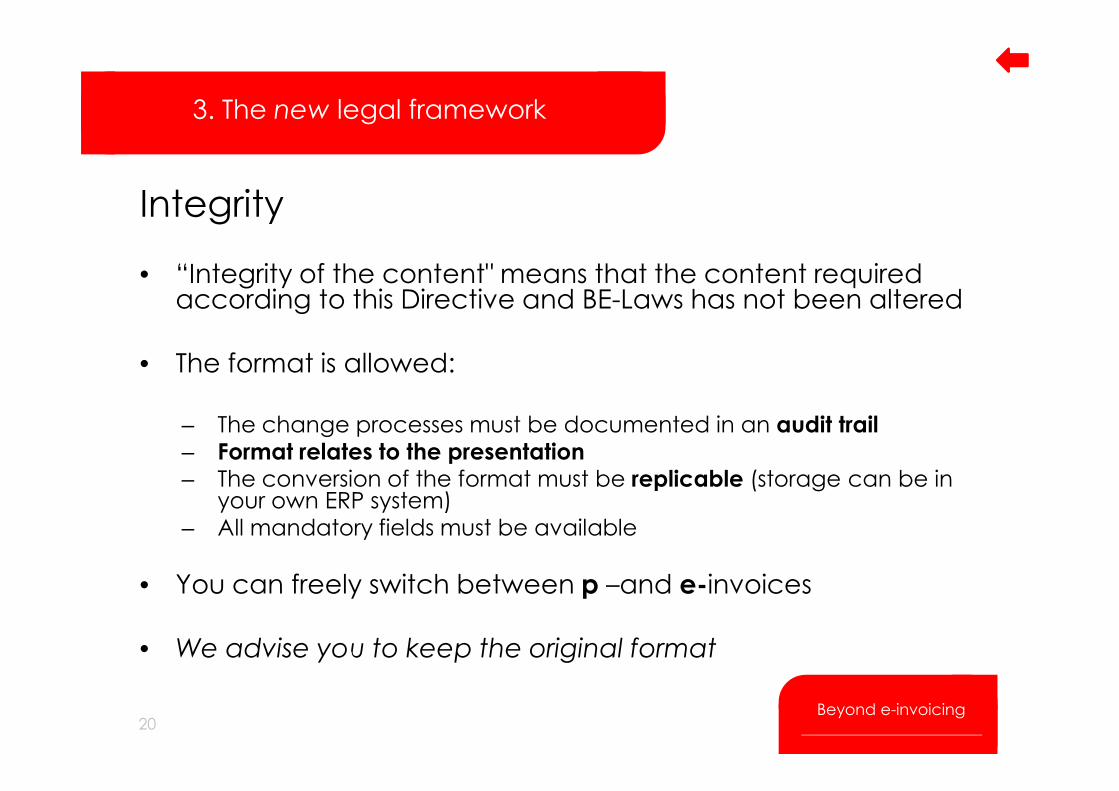

• “Integrity of the content" means that the content required according to this Directive and BE-Laws has not been altered

• The format is allowed:

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

– The change processes must be documented in an audit trail– Format relates to the presentation – The conversion of the format must be replicable (storage can be in

your own ERP system)– All mandatory fields must be available

• You can freely switch between p –and e-invoices

• We advise you to keep the original format

20Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

Business controls

can be used to establish reliable audit trails linking invoices and supplies

• thereby ensuring that any invoice complies with those requirements. (whether on paper or in electronic form)

• The authenticity and integrity of electronic invoices can also be

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• The authenticity and integrity of electronic invoices can also be ensured by using certain existing technologies

– such as Electronic Data Interchange (EDI) and advanced electronic signatures.

• taxable persons should not be required to use any particular electronic-invoicing technology. As there exist different technologies

• The depth of detail of documentation depends on the size of your company

• NB: p-invoice is subject to the same law

21Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

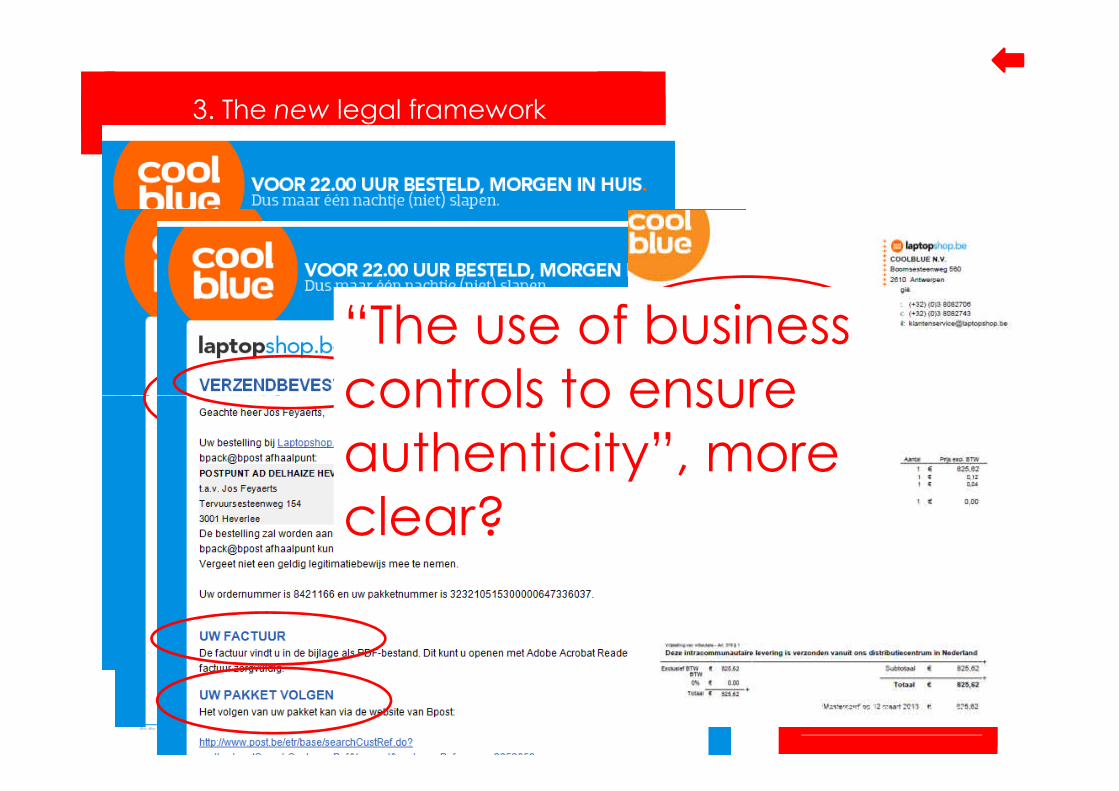

“The use of business

controls to ensure

authenticity”, what

does it mean?

3. The new legal framework

“The use of business

controls to ensure

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

does it mean?

22

controls to ensure

authenticity”, more

clear?

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

Readability and archiving

• The mandatory content of an invoice must be able to be reproduced at any time in a readable way.

• Period 7 years after revision period of VAT

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• Period 7 years after revision period of VAT

• The applicable national archiving rules depend in general on the place of delivery (localization rule)

• p-invoices need to be kept within Belgian borders

• e-invoices can be stored anywhere, must be accessible in Belgium at any time

23Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

Paper invoice: same rules as e-invoice

• EU Directive 2010/45/EU regarding the rules on invoicing aims to promote and further simplify invoicing rules by removing existing burdens and barriers.

• It establishes equal treatment between paper and electronic invoices (the same process for paper invoices can be applied for e-invoices) without

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

same process for paper invoices can be applied for e-invoices) without increasing the administrative burden on paper invoices and has the aim to promote the uptake of e-invoicing by creating the freedom of choice in ensuring the authenticity of origin, integrity of content and legibility

• The implicit agreement is the major remaining difference between p –and e-invoice

• We advise for explicit agreements integrated in contracts and general purchase and sales conditions clarifying: format, fields, connection data, Spam filter, confirmations, login’s etc.

24Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

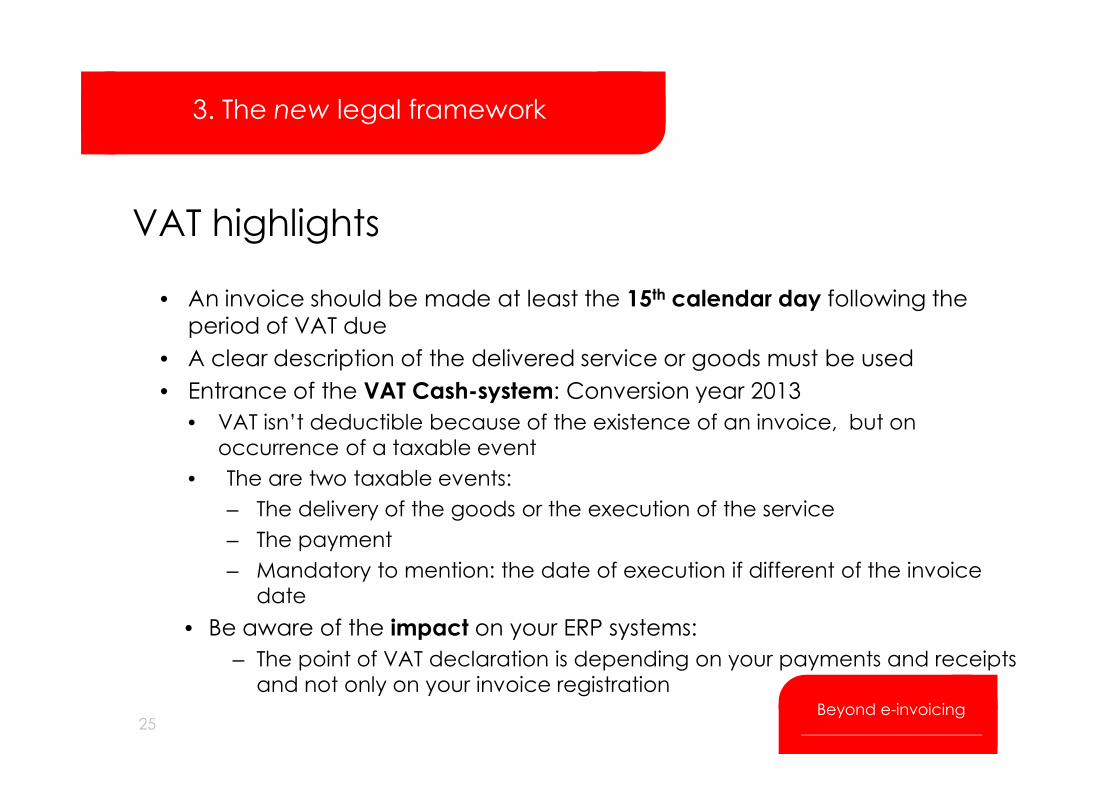

VAT highlights

• An invoice should be made at least the 15th calendar day following the period of VAT due

• A clear description of the delivered service or goods must be used

• Entrance of the VAT Cash-system: Conversion year 2013

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• Entrance of the VAT Cash-system: Conversion year 2013

• VAT isn’t deductible because of the existence of an invoice, but on

occurrence of a taxable event

• The are two taxable events:

– The delivery of the goods or the execution of the service

– The payment

– Mandatory to mention: the date of execution if different of the invoice

date

• Be aware of the impact on your ERP systems:

– The point of VAT declaration is depending on your payments and receipts

and not only on your invoice registration

25Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

VAT highlights

• Tax is only deductible at the client in the period that supplier has

declared it.

• Conversion year 2013

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• Conversion year 2013

– In general: 2013 is a conversion year

– Be aware that no conversion period is granted for intra-

community transactions

26Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

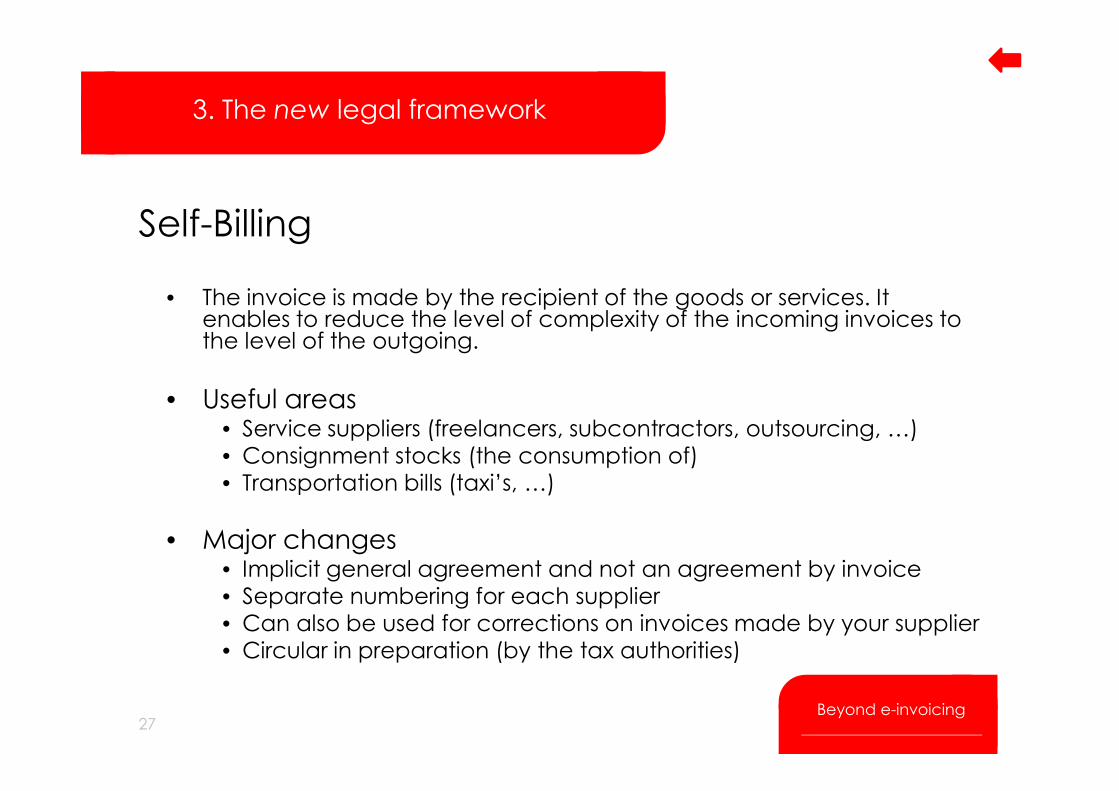

Self-Billing

• The invoice is made by the recipient of the goods or services. It enables to reduce the level of complexity of the incoming invoices to the level of the outgoing.

• Useful areas

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• Useful areas• Service suppliers (freelancers, subcontractors, outsourcing, …)• Consignment stocks (the consumption of)• Transportation bills (taxi’s, …)

• Major changes• Implicit general agreement and not an agreement by invoice• Separate numbering for each supplier• Can also be used for corrections on invoices made by your supplier• Circular in preparation (by the tax authorities)

27Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

Related laws end upcoming initiatives

• Directive 2011/07/EU: on combating late payment in commercial transactions should be converted in Belgian laws by 16/03/2013.Still under construction

30 day rules with max 60 days as exemption

3. The new legal framework

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• New Circulaire about self-billing to adopt the old (Circulaire nr. AOIF 48/2005 (E.T.110.313) dd. 08.12.2005) to the new VAT law

• The proposal of modernizing the law about security rights on movable assets :

– retention and reservation of ownership

– the installation of a register of all pledges

– Mortgage on the commercial fund must be converted into a pledge.

28Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

From Insight to Opportunity

1. Savings

4. The Opportunities

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

2. Efficiency Improvements

3. Financial Supply Chain process improvements

4. E-communication

29Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

Click to edit Master title style

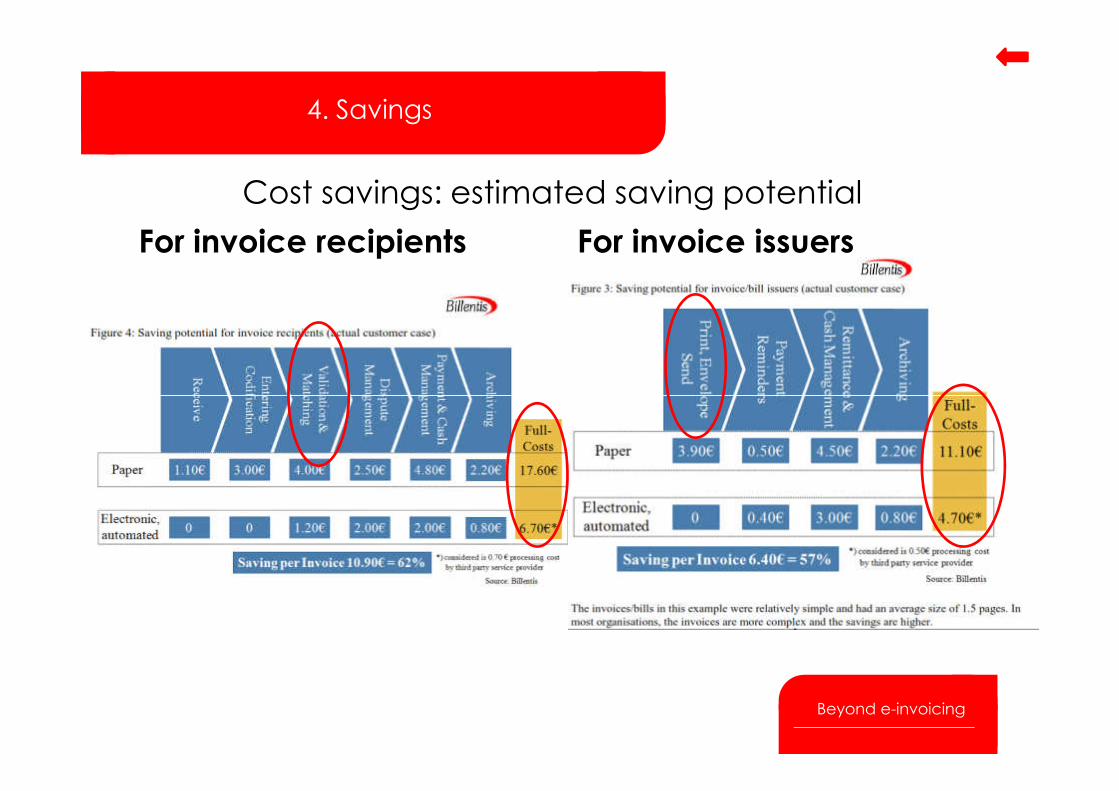

For invoice recipients For invoice issuers

Cost savings: estimated saving potential

4. Savings

FROM INSIGHT

TO REALIZATIONBeyond e-invoicing

Click to edit Master title styleClick to edit Master title style

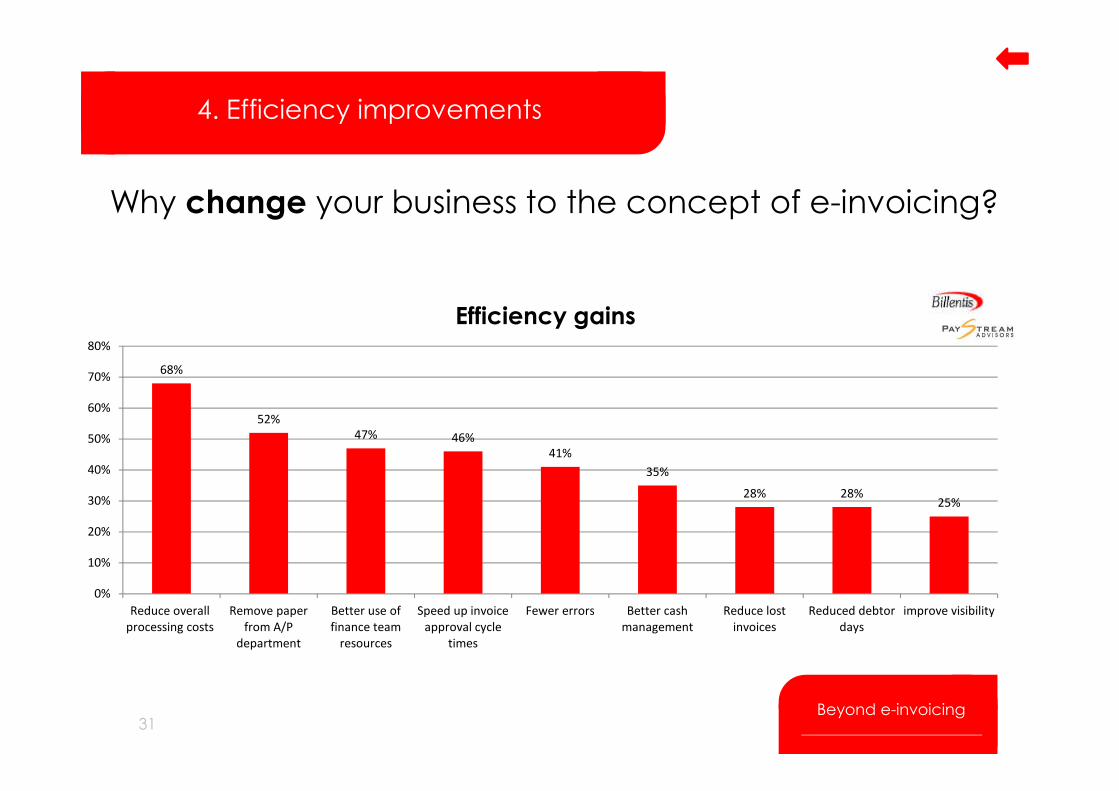

Why change your business to the concept of e-invoicing?

4. Efficiency improvements

68%70%

80%

Efficiency gains

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION31

52%

47% 46%

41%

35%

28% 28%25%

0%

10%

20%

30%

40%

50%

60%

Reduce overall

processing costs

Remove paper

from A/P

department

Better use of

finance team

resources

Speed up invoice

approval cycle

times

Fewer errors Better cash

management

Reduce lost

invoices

Reduced debtor

days

improve visibility

Beyond e-invoicing

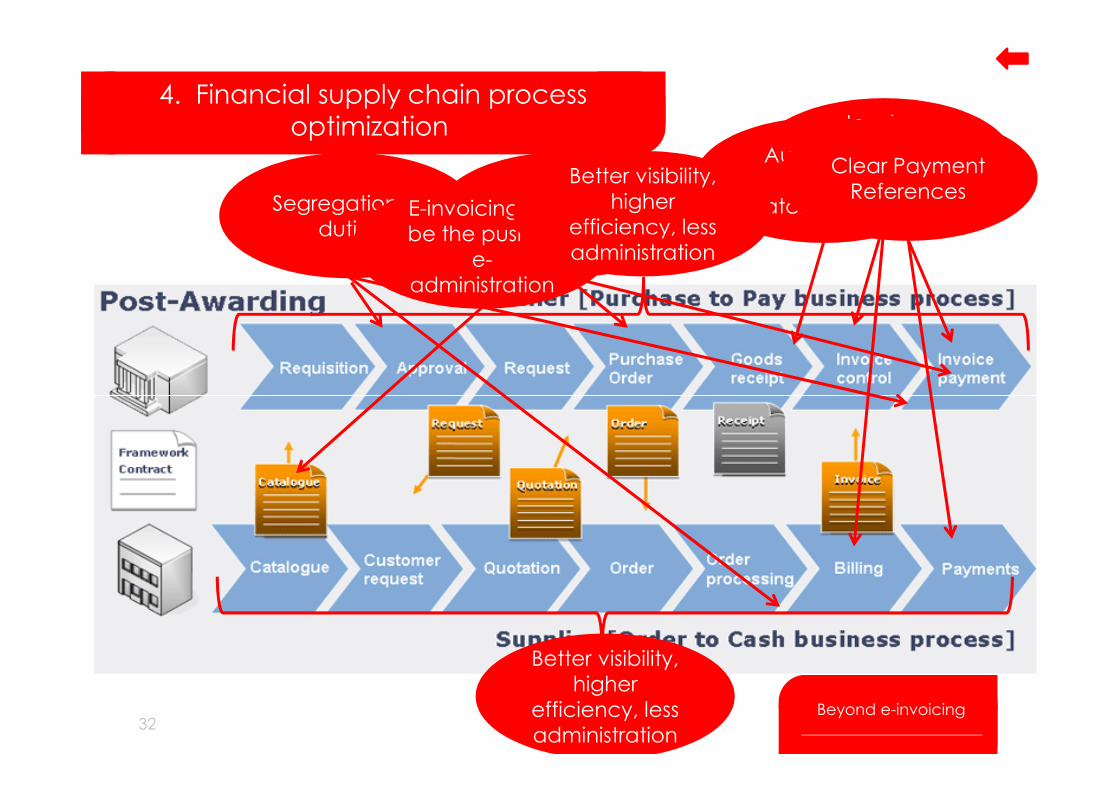

Click to edit Master title styleClick to edit Master title style4. Financial supply chain process

optimization Invoice

created once

� booked

twice

Automated

invoice

matching (O&I)

Clear Payment

ReferencesBetter use of

cash discountsSegregation of

dutiesE-invoicing will

be the push to

e-

administration

Better visibility,

higher

efficiency, less

administration

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION32

Better visibility,

higher

efficiency, less

administration

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

• Invoice Marketing – Invoices could be an essential part of your communication plan

– Use social media in your dunning process, e.g.: rewards offered on social media for early payment

4. E-communication

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

rewards offered on social media for early payment

– Invites / reminders by sms

• Is this the end of the p-invoice?– NO � important to segment your customer!

33Beyond e-invoicing

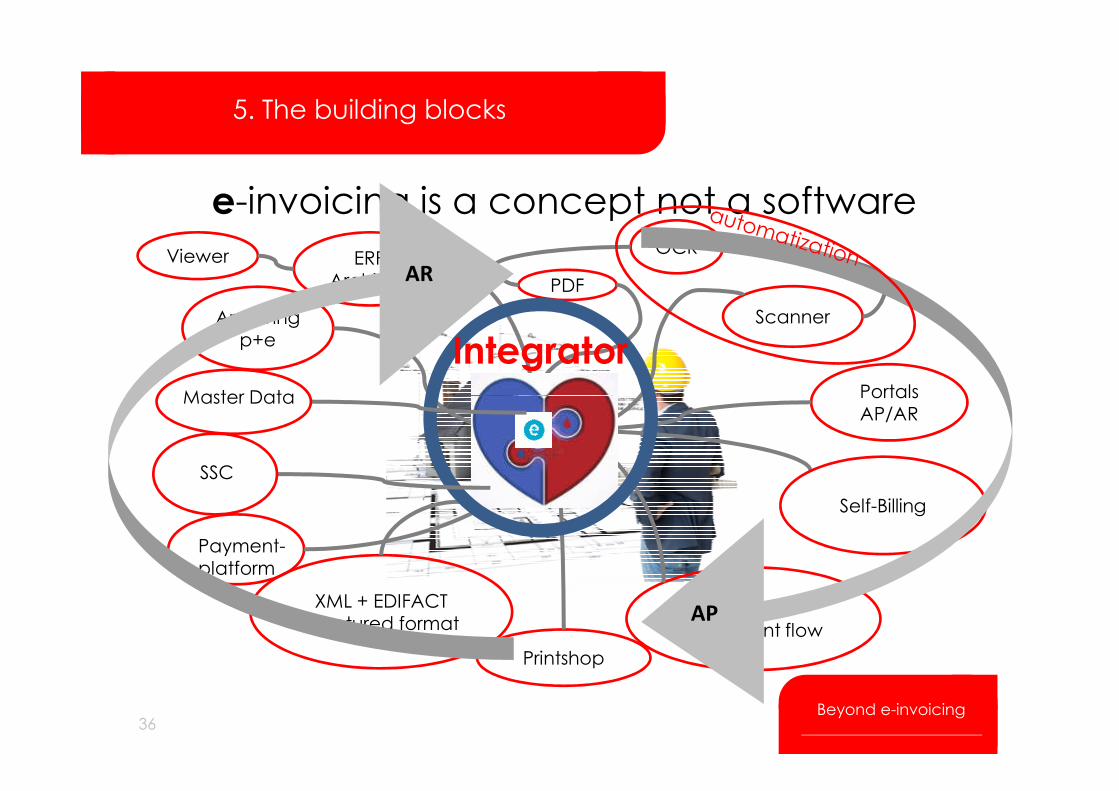

Click to edit Master title styleClick to edit Master title style5. The building blocks

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION34

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style5. The building blocks

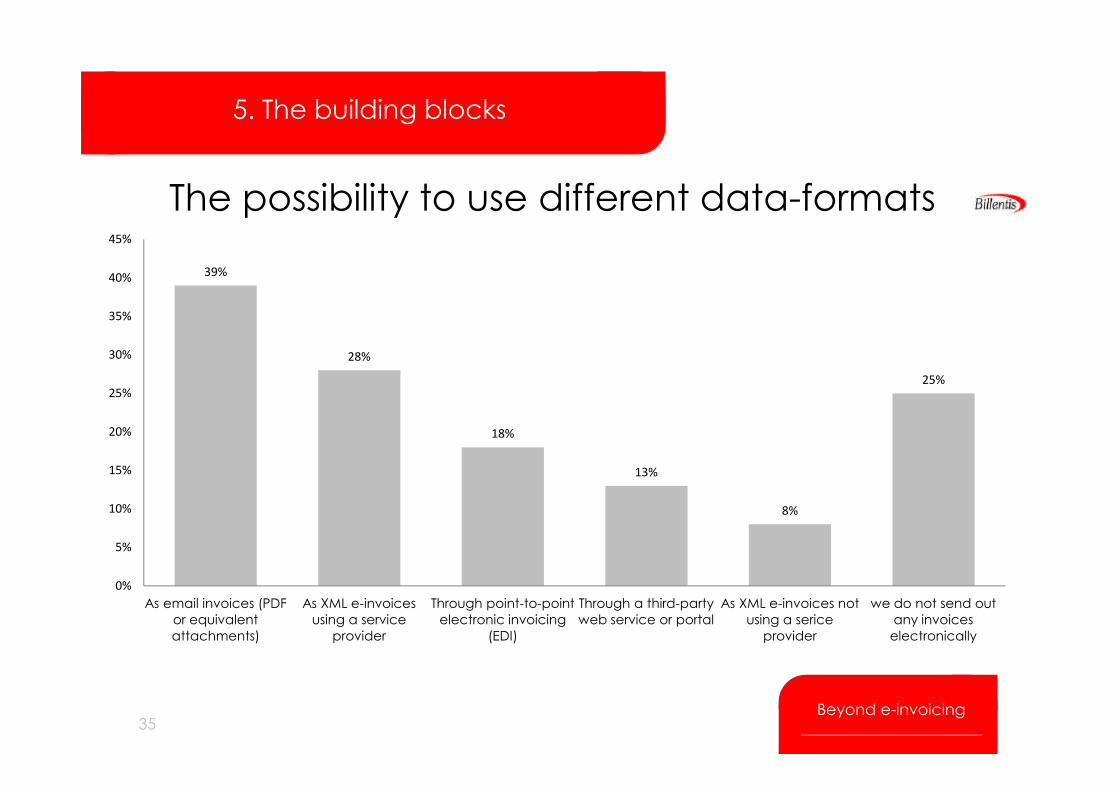

The possibility to use different data-formats

39%

28%

25%25%

30%

35%

40%

45%

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION35

18%

13%

8%

0%

5%

10%

15%

20%

25%

As email invoices (PDF

or equivalent

attachments)

As XML e-invoices

using a service

provider

Through point-to-point

electronic invoicing

(EDI)

Through a third-party

web service or portal

As XML e-invoices not

using a serice

provider

we do not send out

any invoices

electronically

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style5. The building blocks

Scanner

Archivingp+e

Portals

ERPArchieve

Viewer

e-invoicing is a concept not a softwareOCR

Integrator

AR

Master Data

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION36

Printshop

Work -Document flow

XML + EDIFACT structured format

Payment-platform

Portals AP/AR

Self-Billing

AP

SSC

Master Data

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

IPAAS is the ETL of data management

5. The building blocks: IPAAS

Extract data, Transform the formats, Load data in the target system

Major Challenge

Flexible management of

multi-flows and multi-

formats

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

SaaS: Software as a Service

IpaaS: Information Platform as a Service 37

formats

Format standardize

The different formats

attempt hasn’t been

really successful

Beyond e-invoicing

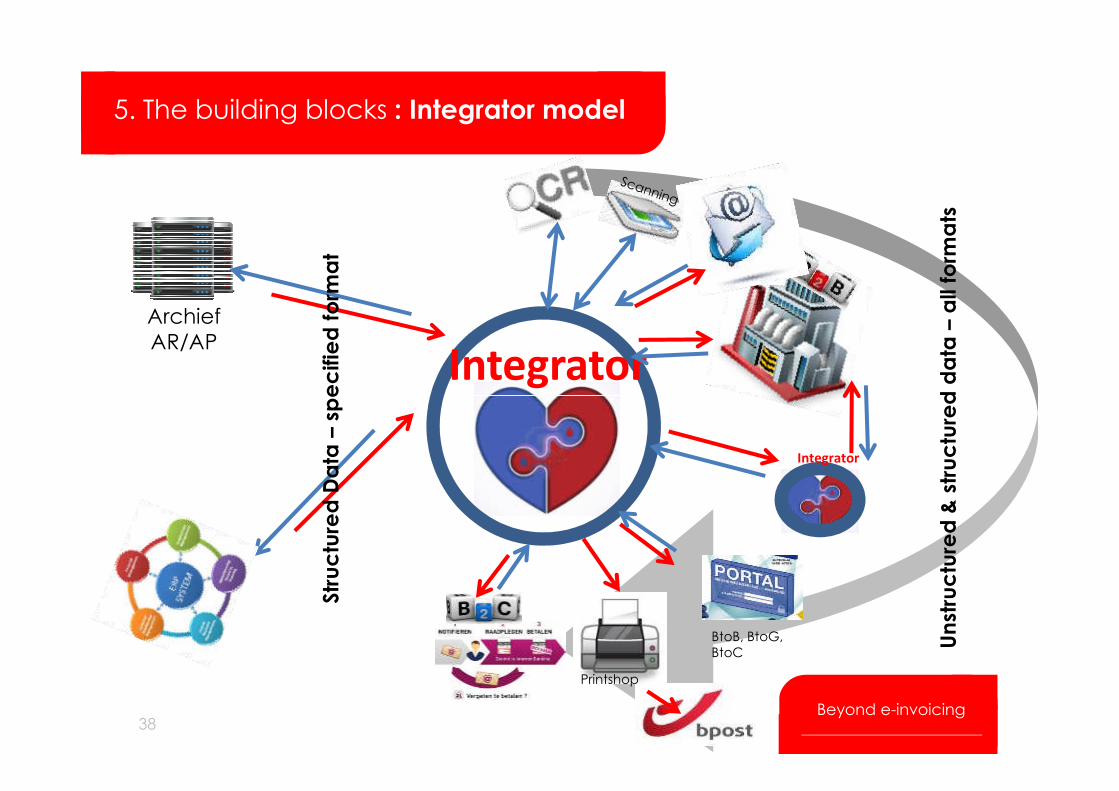

Click to edit Master title styleClick to edit Master title style

Integrator

Archief

AR/AP

5. The building blocks : Integrator model

spe

cifie

dfo

rma

t

stru

ctu

red

da

ta –

all

form

ats

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION38

BtoB, BtoG,

BtoC

Printshop

Str

uc

ture

dD

ata

–sp

ec

ifie

d

Un

stru

ctu

red

& s

tru

ctu

red

Integrator

Beyond e-invoicing

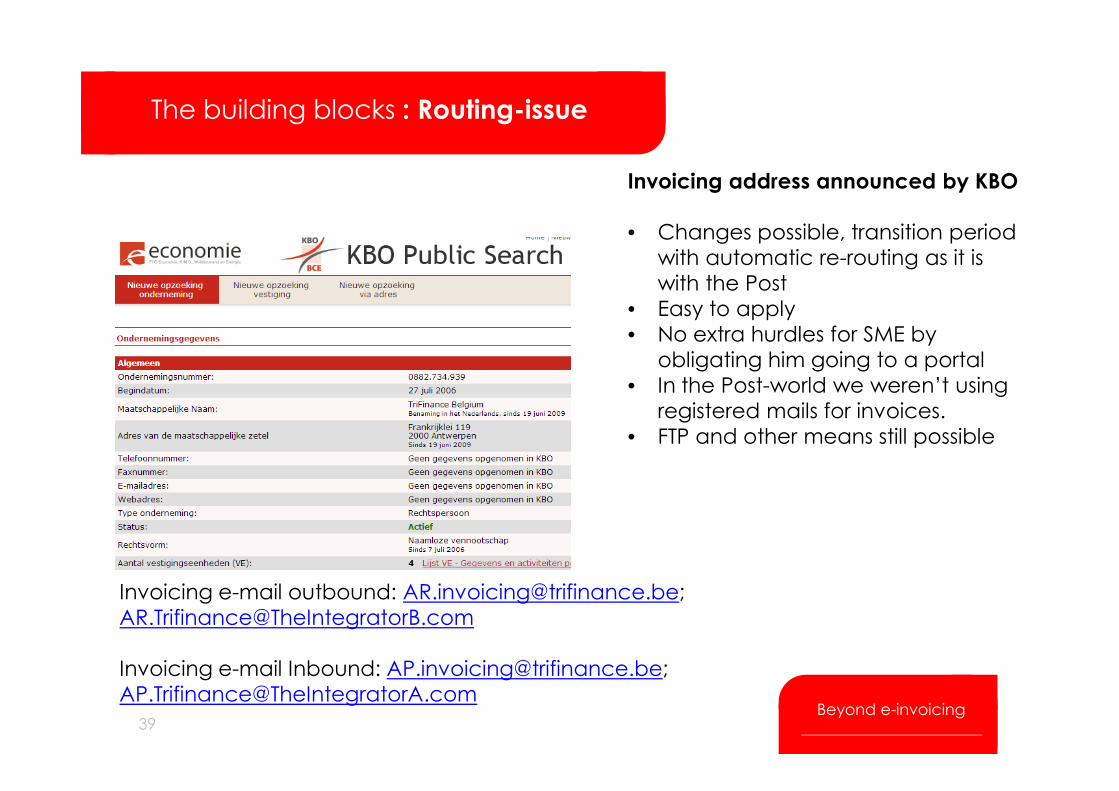

Click to edit Master title styleClick to edit Master title styleThe building blocks : Routing-issue

Invoicing address announced by KBO

• Changes possible, transition period

with automatic re-routing as it is

with the Post

• Easy to apply

• No extra hurdles for SME by

obligating him going to a portal

• In the Post-world we weren’t using

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION39

Invoicing e-mail outbound: [email protected];

Invoicing e-mail Inbound: [email protected];

• In the Post-world we weren’t using

registered mails for invoices.

• FTP and other means still possible

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

Conclusions

• Need for an integrated concept, covering multiple flows and formats

• Segment your debtors and creditors depending:

5. The building blocks

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• Segment your debtors and creditors depending: size, technological skills, payment habits, etc.

• Integrator tools will become important to give every partner a maximum flexibility

• Paper invoices will remain and have their relevance for specific segments and situations

40Beyond e-invoicing

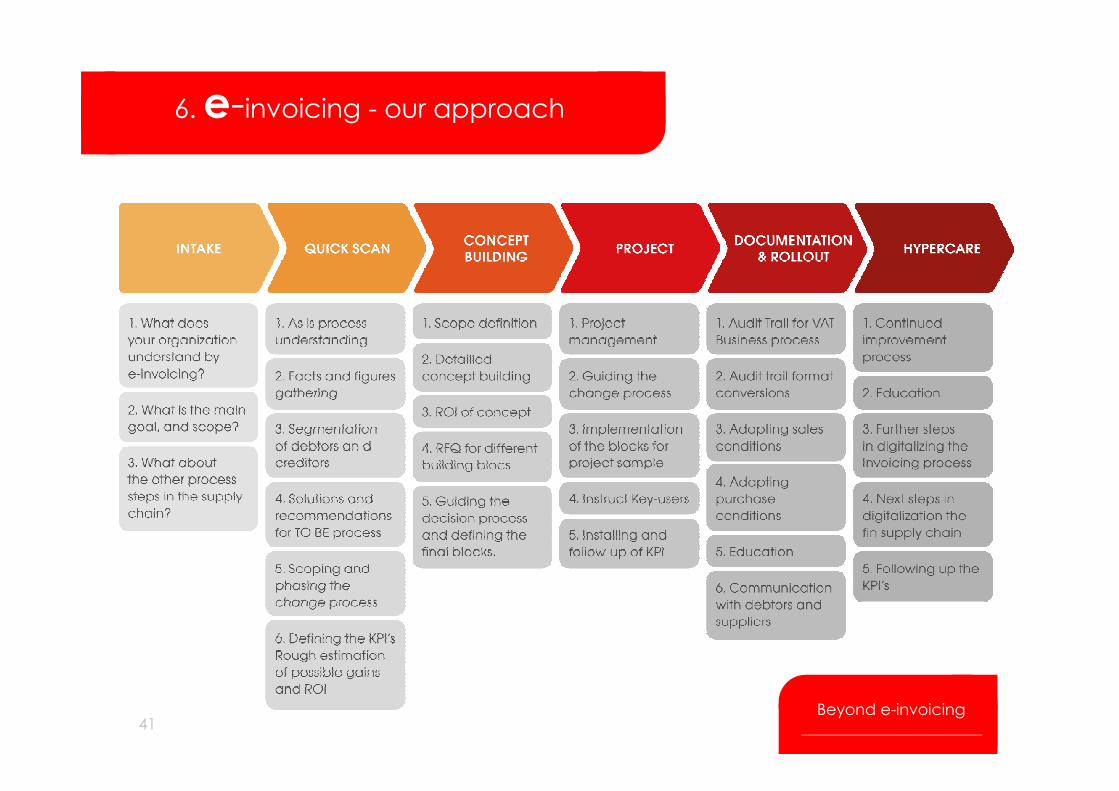

Click to edit Master title styleClick to edit Master title style6. e-invoicing - our approach

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION41

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

• Don’t deny the use of good enough technologies for lower segments (PDF-Text, XML, Excel-Templates, are allowed) – the digital supply chain will become the new normal…

• Pushed and supported by EU and government initiatives

Conclusions

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

• Have a holistic view of the whole fin. supply chain and marketing aspects. Take the opportunity to optimize youroperational processes

• Look at the fiscal differences between EU member states.

• There’s a lot of new legislation coming up in 2013 about the financial supply chain: take it as an opportunity

42Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

• For implementation

– Segment your suppliers and clients and keep the boarders low for

PME partners

– Master data is important for the automation in the invoice process

– Enforce the e-invoice from the beginning and support the change

process at your partners

– Communicate with your business partners

Conclusions

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

– Communicate with your business partners

– Do not go for a 100% solution but get started

– Use the 80/20 Pareto, the possibilities of multi ways and the allowed

format conversion

• Use flexible solutions – agility is important

43

“think big, start up small, scale up fast!”

Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

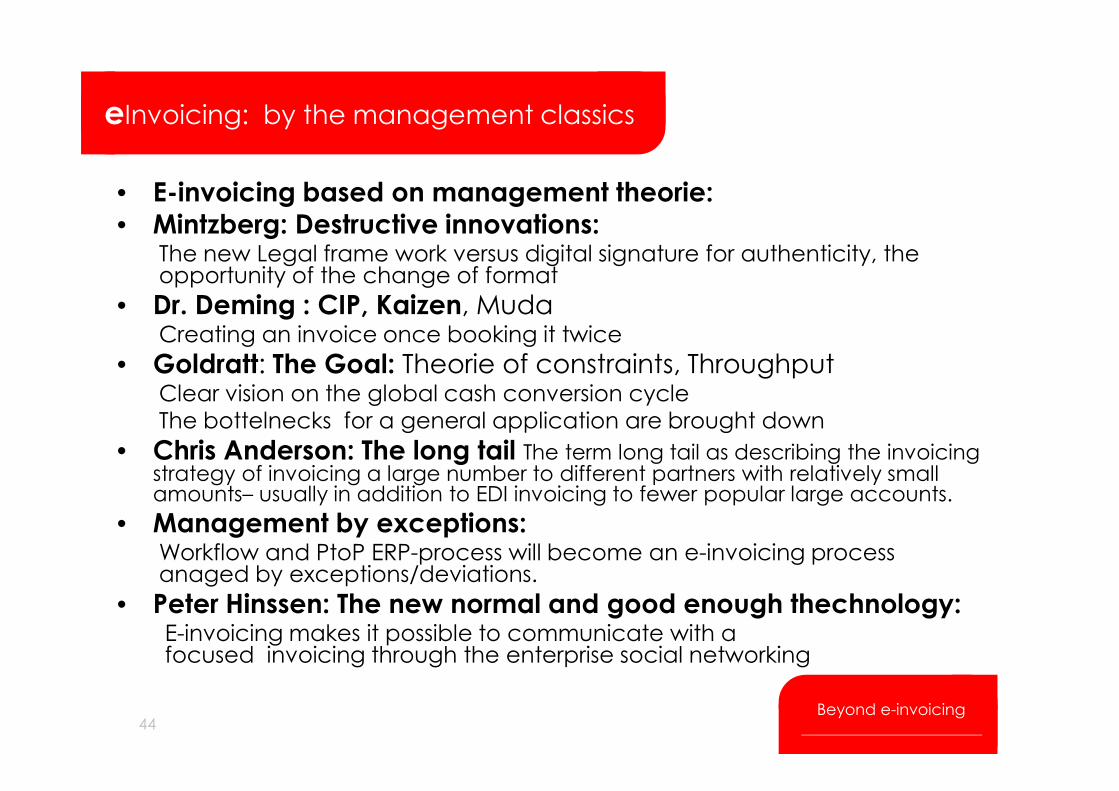

• E-invoicing based on management theorie:

• Mintzberg: Destructive innovations:The new Legal frame work versus digital signature for authenticity, the opportunity of the change of format

• Dr. Deming : CIP, Kaizen, MudaCreating an invoice once booking it twice

• Goldratt: The Goal: Theorie of constraints, ThroughputClear vision on the global cash conversion cycle

eInvoicing: by the management classics

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION

Clear vision on the global cash conversion cycleThe bottelnecks for a general application are brought down

• Chris Anderson: The long tail The term long tail as describing the invoicing strategy of invoicing a large number to different partners with relatively small amounts– usually in addition to EDI invoicing to fewer popular large accounts.

• Management by exceptions:Workflow and PtoP ERP-process will become an e-invoicing process anaged by exceptions/deviations.

• Peter Hinssen: The new normal and good enough thechnology:E-invoicing makes it possible to communicate with a focused invoicing through the enterprise social networking

44Beyond e-invoicing

Click to edit Master title styleClick to edit Master title style

“THANK YOU

FOR

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION45

Beyond e-invoicing

FOR

YOUR PRESENCE!”

Click to edit Master title styleClick to edit Master title styleTriFinance

FROM INSIGHT

TO REALIZATION

FROM INSIGHT

TO REALIZATION46

Beyond e-invoicing