Embed Size (px)

Citation preview

Sreejith S Fims 2008

Trading Profit and Loss Account

Sreejith S

Sreejith S Fims 2008

Income Statement

• Statement showing the revenues, expenses

• To know the Income generated in a period

• It depicts a business entity's financial performance due to operations as well as other activities

Sreejith S Fims 2008

Income Statement

• Trading Account

• Profit and Loss account

Sreejith S Fims 2008

Trading account

• First section of Income Statement

• Find out the Gross profit

Sreejith S Fims 2008

Gross Profit

• It is the profitability of the goods bought or manufactured, sold by the firm

• Sales – Cost of Goods sold

Sreejith S Fims 2008

Cost of Goods Sold

• Opening Stock +

Purchases -

Closing Stock

Sreejith S Fims 2008

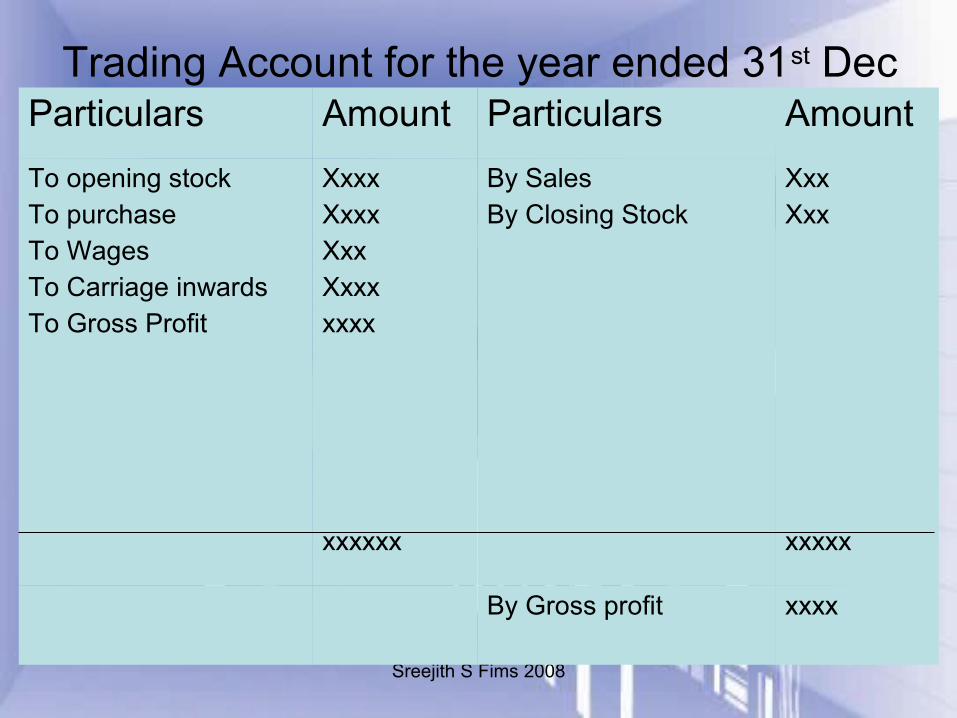

Trading Account for the year ended 31st DecParticulars Amount Particulars Amount

To opening stockTo purchaseTo WagesTo Carriage inwardsTo Gross Profit

XxxxXxxxXxxXxxxxxxx

xxxxxx

By SalesBy Closing Stock

XxxXxx

xxxxx

By Gross profit xxxx

Sreejith S Fims 2008

Opening Stock

• remained unsold stock at the end of previous year.

• brought into books with the help of opening entry

• in the first year of a business there will be no opening stock

Sreejith S Fims 2008

Purchases

• total purchases i.e. cash plus credit purchases

• Any return outwards (purchases return) should be deducted out of purchases

Sreejith S Fims 2008

Buying Expenses

• All expenses relating to purchase of goods are also debited in the trading account

• carriage inwards freight, duty, clearing charges, excise duty, import duty, etc

Sreejith S Fims 2008

Manufacturing Expenses

• Such expenses are incurred by businessmen to manufacture or to render the goods in saleable condition

• motive power, gas fuel, stores, royalties, factory expenses, foreman and supervisor's salary etc.

Sreejith S Fims 2008

Sales.

• Sales mean total sales i.e. cash plus credit sales. If there are any sales returns, these should be deducted from sales.

Sreejith S Fims 2008

Closing Stock

• It is the value of stock lying unsold in the godown or shop on the last date of accounting period.

Sreejith S Fims 2008

Prepare a Trading Account

• Opening Stock 100000• Purchases 672000• Carriage Inwards 30000• Wages 50000• Sales 1100000• Returns inwards 100000• Return outwards 72000• Closing Stock 200000

Sreejith S Fims 2008

Profit and Loss Account

• To find out the Net profit

• Difference between Operating expenses and income

Sreejith S Fims 2008

Particulars Amount Particulars Amount

To salariesTo carriage outwardsTo Interest on loanTo Bad debtsTo AdvertisingTo Export DutyTo PackagesTo RentTo Commission PaidTo Depreciation

To net profit transferred to capital account

XxxxXxxxXxxXxxxxxxxxxxxxxxxxxxxxxxxxx

By Gross profitBy Discount receivedBy Commission receivedBy Rent receivedBy Interest receivedBy Income from investmentsBy Dividend received

XxxXxxxxxxxxxxxxxxxxxxxxxxx

xxxx xxxxx

Profit and Loss account for the year ended 31st march 2008

Sreejith S Fims 2008

Indirect Expenses

• Selling and distribution expenses

• Administrative Expenses

• Financial Expenses

• Maintenance, depreciations and Provisions etc.

Sreejith S Fims 2008

Selling and Distribution Exp

• a) Salesmen's salary and commission• (b) Commission to agents• (c) Freight & carriage on sales• (d) Sales tax• (e) Bad debts• (f) Advertising• (g) Packing expenses• (h) Export duty.. etc

Sreejith S Fims 2008

Administrative Expenses.

• (a) Office salaries & wages• (b) Insurance• (c) Legal expenses• (d) Trade expenses• (e) Rates & taxes• (f) Audit fees• (g) Insurance• (h) Rent• (i) Printing and stationery• (j) Postage and telegrams• (k) Bank charges… etc

Sreejith S Fims 2008

Financial Expenses

• (a) Discount allowed

• (b) Interest on Capital

• (c) Interest on loan

• (d) Discount Charges on bill discounted

Sreejith S Fims 2008

Maintenance, depreciations and Provisions etc

• (a) Repairs

• (b) Depreciation on assets

• (c) Provision or reserve for doubtful debts

• (d) Reserve for discount on debtors.

Sreejith S Fims 2008

Prepare a Profit and Loss Account• Salaries 110000

• Legal Charges 25000

• Consultancy fee 32000

• Audit Fee 1000

• Discount Received 18000

• Electricity 17000

• Gross profit 420000

• Postage & Telegram 12000

• Stationary 27000

• Depreciation 65000

• Discount Allowed 19000

• Bad debts 17000

• Interest 70000

Sreejith S Fims 2008

Particulars Debit Credit

Capital Opening StockCash MachineryPurchasesWages DiscountOffice ExpSalesSundry DebtorsSundry CreditorsSalary

Closing Stock Rs 2700

20001440736018200100005006000

8500

10000

64000

10000

300

50000

3700

64000

Trial Balance on 31st March 2008

Sreejith S Fims 2008

Sreejith S Fims 2008

Particulars Debit Credit

Capital Purchase & SalesOpening StockDebtors and CreditorsBank LoanOverdraftSalariesAdvertisementOther ExpReturnsFurnitureBuildingCash

Closing Stock Rs 100000

6050007200090000

270000110000600004000045000089000050002592000

8700001210000

170000200000112000

2592000

Trial Balance on 31st March 2008