Embed Size (px)

Citation preview

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clustering

Volatility Clustering

Consider a risk driver Xt whose increment ∆Xt has close to zeroautocorrelation (2.10)

Xt displays volatility clustering if

Cr{|∆Xt|, |∆Xt−l|} 6= 0 (2.87)

• Goal: model volatility clustering (2.87)• Possible approaches:

• Generalized Autoregressive Conditional Heteroscedastic (GARCH)processes (Section 2.5.1)

• Generalizations of GARCH (Section 2.5.2)• Stochastic volatility processes (Section 2.5.3)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clustering

Volatility Clustering

Consider a risk driver Xt whose increment ∆Xt has close to zeroautocorrelation (2.10)

Xt displays volatility clustering if

Cr{|∆Xt|, |∆Xt−l|} 6= 0 (2.87)

• Goal: model volatility clustering (2.87)• Possible approaches:

• Generalized Autoregressive Conditional Heteroscedastic (GARCH)processes (Section 2.5.1)

• Generalizations of GARCH (Section 2.5.2)• Stochastic volatility processes (Section 2.5.3)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clustering

Volatility Clustering

Consider a risk driver Xt whose increment ∆Xt has close to zeroautocorrelation (2.10)

Xt displays volatility clustering if

Cr{|∆Xt|, |∆Xt−l|} 6= 0 (2.87)

• Goal: model volatility clustering (2.87)• Possible approaches:

• Generalized Autoregressive Conditional Heteroscedastic (GARCH)processes (Section 2.5.1)

• Generalizations of GARCH (Section 2.5.2)• Stochastic volatility processes (Section 2.5.3)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clustering

Invariance test for equity log-return: autocorrelation ellipsoid

• Risk driver: log-value of GE

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

GARCH

Generalized Autoregressive Conditional Heteroscedastic(GARCH(1, 1)) model

∆Xt = µ+ Σtεt (2.88)

Σ2t = c+ bΣ2

t−1 + a (∆Xt−1 − µ)2 (2.89)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

GARCH

Generalized Autoregressive Conditional Heteroscedastic(GARCH(1, 1)) model

∆Xt = µ+ Σtεt (2.88)

Σ2t = c+ bΣ2

t−1 + a (∆Xt−1 − µ)2 (2.89)

location standardized invariant

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

GARCH

Generalized Autoregressive Conditional Heteroscedastic(GARCH(1, 1)) model

∆Xt = µ+ Σtεt (2.88)

Σ2t = c+ bΣ2

t−1 + a (∆Xt−1 − µ)2 (2.89)

location standardized invariant

• a, b, c ≥ 0

• a+ b < 1 ⇒ ∆Xt is stationary• a = b = 0 ⇒ ∆Xt is a random walk (2.8)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

GARCH

Generalized Autoregressive Conditional Heteroscedastic(GARCH(1, 1)) model

∆Xt = µ+ Σtεt (2.88)

Σ2t = c+ bΣ2

t−1 + a (∆Xt−1 − µ)2 (2.89)

location standardized invariant

The next-step dispersion reads

Σ2t+1 =

c

1− b + a∞∑l=0

bl (∆Xt−l − µ)2 (2.90)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

GARCH

Generalized Autoregressive Conditional Heteroscedastic(GARCH(1, 1)) model

∆Xt = µ+ Σtεt (2.88)

Σ2t = c+ bΣ2

t−1 + a (∆Xt−1 − µ)2 (2.89)

location standardized invariant

The next-step dispersion reads

Σ2t+1 =

c

1− b + a∞∑l=0

bl (∆Xt−l − µ)2 (2.90)

⇓

The next-step dispersion given current information is not random

Σt+1|it = σt+1 (2.91)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

GARCH

Generalized Autoregressive Conditional Heteroscedastic(GARCH(1, 1)) model

∆Xt = µ+ Σtεt (2.88)

Σ2t = c+ bΣ2

t−1 + a (∆Xt−1 − µ)2 (2.89)

location standardized invariant

How to fit the GARCH model (2.88)-(2.89)?

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

GARCH

Generalized Autoregressive Conditional Heteroscedastic(GARCH(1, 1)) model

∆Xt = µ+ Σtεt (2.88)

Σ2t = c+ bΣ2

t−1 + a (∆Xt−1 − µ)2 (2.89)

location standardized invariant

How to fit the GARCH model (2.88)-(2.89)?

1 Assume εt ∼ N (0, 1) ⇒ Xt+1|it ∼ N (xt + µ, σt+1)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

GARCH

Generalized Autoregressive Conditional Heteroscedastic(GARCH(1, 1)) model

∆Xt = µ+ Σtεt (2.88)

Σ2t = c+ bΣ2

t−1 + a (∆Xt−1 − µ)2 (2.89)

location standardized invariant

How to fit the GARCH model (2.88)-(2.89)?

1 Assume εt ∼ N (0, 1) ⇒ Xt+1|it ∼ N (xt + µ, σt+1)

2 Estimate via maximum likelihood

(a, b, c, µ) ≡ argmaxa,b,c,µ

{−t∑t=1

pt lnσ2t −

t∑t=1

pt (∆xt − µ)2 /σ2t } (2.94)

= c+ bσ2t−1 + a (∆xt−1 − µ)2 (2.89)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

GARCH

Generalized Autoregressive Conditional Heteroscedastic(GARCH(1, 1)) model

∆Xt = µ+ Σtεt (2.88)

Σ2t = c+ bΣ2

t−1 + a (∆Xt−1 − µ)2 (2.89)

location standardized invariant

How to fit the GARCH model (2.88)-(2.89)?

1 Assume εt ∼ N (0, 1) ⇒ Xt+1|it ∼ N (xt + µ, σt+1)

2 Estimate via maximum likelihood

(a, b, c, µ) ≡ argmaxa,b,c,µ

{−t∑t=1

pt lnσ2t −

t∑t=1

pt (∆xt − µ)2 /σ2t } (2.94)

3 Extract the realized invariant (2.5)

εt =xt − xt−1 − µ

σt(2.95)

= c+ bσ2t−1 + a (∆xt−1 − µ)2 (2.89)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

Volatility clustering: autocorrelation ellipsoid of absolute

• Risk driver: log-value of S&P 500 stock

GARCH residual

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringGARCH

Volatility clustering: absolute P&L vs absolute GARCH

• Risk driver: P&L of equity momentum strategy

residual

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringExtensions of GARCH

Extensions of GARCH

How to extend GARCH processes?

Generalize dispersion (2.89)

g (Σt) = c+ bg (Σt−1) + ah (∆Xt−1) (2.96)

• GARCH(1, 1) (2.89): g (z) = h (z) = z2

• EGARCH: g (z) = ln z

• ACD model (2.97)-(2.98): g (z) = h (z) = z

ACD follows from applying the model to a positive process (arrivaltime gaps)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringExtensions of GARCH

Extensions of GARCH

How to extend GARCH processes?

Generalize dispersion (2.89)

g (Σt) = c+ bg (Σt−1) + ah (∆Xt−1) (2.96)

• GARCH(1, 1) (2.89): g (z) = h (z) = z2

• EGARCH: g (z) = ln z

• ACD model (2.97)-(2.98): g (z) = h (z) = z

ACD follows from applying the model to a positive process (arrivaltime gaps)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringExtensions of GARCH

Extensions of GARCH

How to extend GARCH processes?

Generalize dispersion (2.89)

g (Σt) = c+ bg (Σt−1) + ah (∆Xt−1) (2.96)

• GARCH(1, 1) (2.89): g (z) = h (z) = z2

• EGARCH: g (z) = ln z

• ACD model (2.97)-(2.98): g (z) = h (z) = z

ACD follows from applying the model to a positive process (arrivaltime gaps)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringExtensions of GARCH

Volatility clustering: autocorrelation ellipsoid of ACD

• Risk driver: time of trades

residual

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

Stochastic volatility

Stochastic volatility model

∆Xt = µ+ Σtε1,t (2.99)

Σ2t+1 = c+ bΣ2

t + ε2,t+1 (2.100)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

Stochastic volatility

Stochastic volatility model

∆Xt = µ+ Σtε1,t (2.99)

Σ2t+1 = c+ bΣ2

t + ε2,t+1 (2.100)

not independent

not deterministic given current information

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

Stochastic volatility

Stochastic volatility model

∆Xt = µ+ Σtε1,t (2.99)

Σ2t+1 = c+ bΣ2

t + ε2,t+1 (2.100)

not independent

not deterministic given current information

Stochastic volatility model (2.99)-(2.100) is a linear state space model(2.101)-(2.102) (suppose µ = 0)

observable equation (2.101) : Yt = Ht + εt

transition equation (2.102) : Ht+1 = c+ bHt + εt+1

(2.101)

(2.102)

Yt ≡ ln(∆X2t ) εt ≡ ln(ε21,t)

Yt ≡ ln(Σ2t ) εt ≡ ln(ε22,t)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

Stochastic volatility

Stochastic volatility model

∆Xt = µ+ Σtε1,t (2.99)

Σ2t+1 = c+ bΣ2

t + ε2,t+1 (2.100)

not independent

not deterministic given current information

Stochastic volatility model (2.99)-(2.100) is a linear state space model(2.101)-(2.102) (suppose µ = 0)

observable equation (2.101) : Yt = Ht + εt

transition equation (2.102) : Ht+1 = c+ bHt + εt+1

(2.101)

(2.102)

Yt ≡ ln(∆X2t ) εt ≡ ln(ε21,t)

Yt ≡ ln(Σ2t ) εt ≡ ln(ε22,t)

⇒ Σt hidden variableARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

Stochastic volatility

Stochastic volatility model

∆Xt = µ+ Σtε1,t (2.99)

Σ2t+1 = c+ bΣ2

t + ε2,t+1 (2.100)

not independent

not deterministic given current information

How to fit the Stochastic volatility model? (2.99)-(2.100)?

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

Stochastic volatility

Stochastic volatility model

∆Xt = µ+ Σtε1,t (2.99)

Σ2t+1 = c+ bΣ2

t + ε2,t+1 (2.100)

not independent

not deterministic given current information

How to fit the Stochastic volatility model? (2.99)-(2.100)?1 Estimate linear state space model (2.101)-(2.102) (Table 18b.5)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

Stochastic volatility

Stochastic volatility model

∆Xt = µ+ Σtε1,t (2.99)

Σ2t+1 = c+ bΣ2

t + ε2,t+1 (2.100)

not independent

not deterministic given current information

How to fit the Stochastic volatility model? (2.99)-(2.100)?1 Estimate linear state space model (2.101)-(2.102) (Table 18b.5)

2 Extract the realized invariants (2.5)

ε1,t+1 =xt+1 − xt − µ

σt+1, ε2,t+1 = σ2

t+1 − c− bσ2t (2.103)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

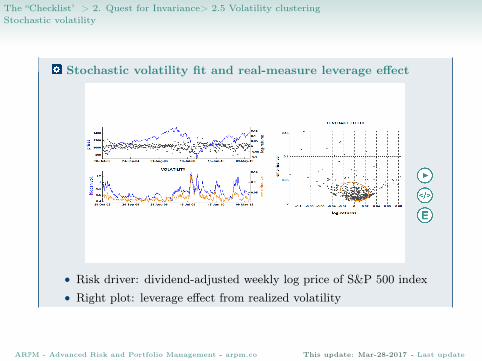

Stochastic volatility fit and real-measure leverage effect

• Risk driver: dividend-adjusted weekly log price of S&P 500 index• Right plot: leverage effect from realized volatility

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

Stochastic volatility fit and risk-neutral leverage effect

• Risk driver: dividend-adjusted weekly log price of S&P 500 index• Right plot: leverage effect from call options implied volatility

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

Stochastic Volatility

How to extend stochastic volatility (2.100)?

• Volatility component into the volatility invariant

Σ2t+1 = c+ bΣ2

t + |Σt|ε2,t+1 (2.104)

• Normalizing and Variance Stabilizing (NoVaS) processes

Σ2t+1 = c+ bΣ2

t + a∆X2t+1 (2.105)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 2. Quest for Invariance> 2.5 Volatility clusteringStochastic volatility

Stochastic Volatility

How to extend stochastic volatility (2.100)?

• Volatility component into the volatility invariant

Σ2t+1 = c+ bΣ2

t + |Σt|ε2,t+1 (2.104)

• Normalizing and Variance Stabilizing (NoVaS) processes

Σ2t+1 = c+ bΣ2

t + a∆X2t+1 (2.105)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

![NOTES ON SCALE-INVARIANCE AND BASE-INVARIANCE FOR … · arXiv:1307.3620v1 [math.PR] 13 Jul 2013 NOTES ON SCALE-INVARIANCE AND BASE-INVARIANCE FOR BENFORD’S LAW MICHAŁ RYSZARD](https://img.dokumen.tips/doc/110x75/5aee16367f8b9a45569086fd/notes-on-scale-invariance-and-base-invariance-for-13073620v1-mathpr-13-jul.jpg)