Embed Size (px)

Citation preview

Str

ictl

yPri

vate

and C

onfi

denti

al

www.evaluation.us

TAILORED VALUATION

[Company XYZ]

New York - London – Miami - Madrid

This document is an extract of the full report

January 2011

www.evaluation.us

Str

ictl

yPri

vate

and C

onfi

denti

al

www.evaluation.us

INDEX

Page

1. Aim of the report and Executive Summary 4

2. Financial Hypothesis 6

3. Valuation Methodology 12

4. Trading Valuation 19

5. Private Transactions Valuation 22

6. DCF Valuation 26

7. Conclusion: Valuation Range 30

Appendix

I. e-Valuation Company Presentation 32

II. WACC Calculation 33

III. Historical and Projected Financial Statements 34

IV. Difference Between Value and Price 37

V. Glossary 38

VI. e-Vauation’s References 39

VII. Contact Details 40

www.evaluation.us

Est

ricta

mente

Pri

vado y

Confi

dencia

l January 2011 COMPANY XYZ – TAILORED VALUATION

www.e-valuation.us3. Valuation Methodology

In order to carry out XYZ’s valuation, e-Valora has used contrasted, generally accepted valuation

methodologies: the Discounted Cash Flows methodology (DCF), the Multiples of Trading Comparable

Companies methodology and the Multiples of Private Transactions methodology. The application of each of

these methodologies, results in a specific valuation range for XYZ. In order to establish an estimated valuation

range for the company, e-Valora calculates a weighted average of the results of the different methodologies,

where the different weights are estimated using its own criteria and experience. We believe that the use of

all of these methodologies improves the reliability of the valuation obtained given that they are

complementary. Furthermore, it allows us to contrast the results of one and other (including the basic

assumptions made).

In the case of the DCF methodology, the assumptions that are considered are based on e-Valora’s estimates.

Such information allows a qualitative and quantitative analysis of the current and expected future situation of

XYZ.

If the strategy carried out by the Company in the future is different from the one that has been considered

according to the information provided by the Client, or if such information differs from reality, our view about

the value of XYZ would vary accordingly.

Each of the methodologies mentioned take into account the information of XYZ in a different way, providing a

complementary view of the company’s value.

Introduction

12

www.evaluation.us

Est

ricta

mente

Pri

vado y

Confi

dencia

l January 2011 COMPANY XYZ – TAILORED VALUATION

www.e-valuation.us

Valuation using Multiples of Trading Comparable Companies (continuation)

According to the multiples found and weighting each of them as indicated in the following table, the company’s valuation range would be of

between 169.172 and 186.980 Euros.

4. Trading Valuation

21

VALUATION USING MULTIPLES OF TRADING COMPARABLE COMPANIES

Companies PER3

Euros 2010 2011 2012 2010 2011 2012 2010 2011 2012 2010 2011 2012

Mean 0,35x 0,36x 0,30x 10,9x 7,4x 5,4x 16,9x 9,9x 7,0x 25,9x 15,6x 10,3x

Company XYZ's Magnitudes 4.421.756 4.386.531 4.474.261 14.549 17.414 19.490 14.372 17.062 18.958 10.779 12.796 14.219

Results: Value of the Company 1.564.738 1.559.332 1.322.394 159.030 129.028 105.893 242.783 168.805 132.625 170.328 91.225 145.949

Weights 5% 5% 5% 50% 50% 50% 25% 25% 25% 20% 20% 20%

2010 2011 2012

Value of the Company 388.776 275.907 298.172

Value of the Company reduced by 20% 311.021 220.726 238.538

Company Value Estimation USING MULTIPLES OF TRADING COMPARABLE COMPANIES 256.761 Euros

RANGE 5%

COMPANY'S VALUATION RANGE USING MULTIPLES OF TRADING COMPARABLE COMPANIES 243.923 269.599 Euros

- Net Debt (Negative) 108.765 108.765

VALUATION RANGE OF THE COMPANY'S EQUITY USING MULTIPLES OF TRADING COMPARABLE COMPANIES 352.688 378.365 Euros

Note 1 : EBITDA stands for Earnings before interest, taxes, depreciation and amortisation

Nota 2: EBIT stands for Earnings before interest and taxes

Nota 3: PER is equal to the company's market capitalization divided by the profit/loss (after taxation)

E.V./Turnover E.V./EBITDA1 E.V./EBIT2

www.evaluation.us

Est

ricta

mente

Pri

vado y

Confi

dencia

l January 2011 COMPANY XYZ – TAILORED VALUATION

www.e-valuation.us

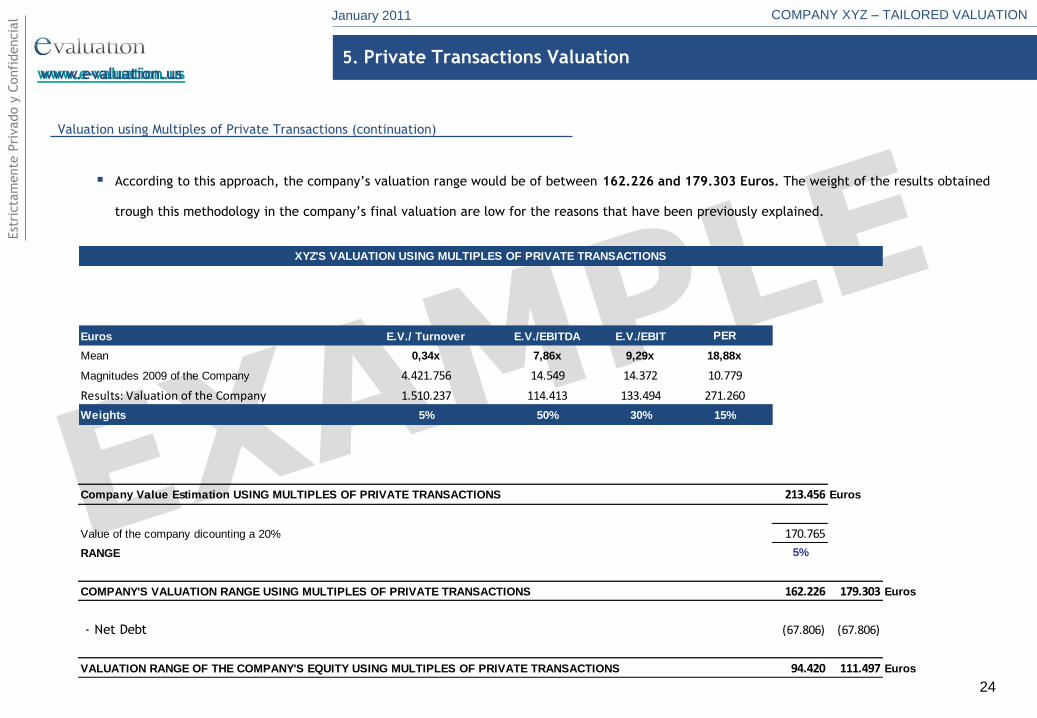

According to this approach, the company’s valuation range would be of between 162.226 and 179.303 Euros. The weight of the results obtained

trough this methodology in the company’s final valuation are low for the reasons that have been previously explained.

5. Private Transactions Valuation

24

Valuation using Multiples of Private Transactions (continuation)

Euros E.V./ Turnover E.V./EBITDA E.V./EBIT PER

Mean 0,34x 7,86x 9,29x 18,88x

Magnitudes 2009 of the Company 4.421.756 14.549 14.372 10.779

Results: Valuation of the Company 1.510.237 114.413 133.494 271.260

Weights 5% 50% 30% 15%

Company Value Estimation USING MULTIPLES OF PRIVATE TRANSACTIONS 213.456 Euros

Value of the company dicounting a 20% 170.765

RANGE 5%

COMPANY'S VALUATION RANGE USING MULTIPLES OF PRIVATE TRANSACTIONS 162.226 179.303 Euros

- Net Debt (67.806) (67.806)

VALUATION RANGE OF THE COMPANY'S EQUITY USING MULTIPLES OF PRIVATE TRANSACTIONS 94.420 111.497 Euros

XYZ'S VALUATION USING MULTIPLES OF PRIVATE TRANSACTIONS

www.evaluation.us

Est

ricta

mente

Pri

vado y

Confi

dencia

l January 2011 COMPANY XYZ – TAILORED VALUATION

www.e-valuation.us

Conclusion: Final Valuation Range

Taking into account the results obtained using the different methodologies described, and considering that our reference

methodology is the DCF (with a weight of 85%, compared to 10% for the multiples of Trading Comparable Companies

methodology and the 5% of the multiples of Private Transactions methodology), we obtain an average value, to which we

apply a reliability range of +/- 5%.

Taking into account such assumptions, we conclude that the final valuation range for XYZ is the following : between

247.163 and 273.180 Euros.

To calculate the market value of XYZ’s shares (Equity Value), the company’s net debt (it shows a company's overall debt

situation by netting the value of a company's liabilities and debts with its cash and other similar liquid assets) at the

moment of the valuation has to be subtracted from the enterprise value previously calculated.

Based on the historical data provided by the company, and considering the company’s net debt as of December of 2008

(1,669,850 Euros), the valuation range of the its Equity would be of between 179.357 y 205.374 Euros.

7. Conclusion: Valuation Range

256.971

162.226

169.172

247.163

284.021

179.303

186.980

273.180

50.000 100.000 150.000 200.000 250.000 300.000

DCF

Private Comparable Transactions

Trading Comparable Companies

Total

Equity’s Market Value

30

www.evaluation.us

Est

ricta

mente

Pri

vado y

Confi

dencia

l January 2011 COMPANY XYZ – TAILORED VALUATION

www.e-valuation.us

e-Valuation Financial Services Northern Europe One Canada Square, 29th Floor, Canary Wharf London E14 5DY United Kingdom

e-Valuation Financial Services Southern Europe c/ José Ortega y Gasset, 42 Madrid, Madrid 28006 Spain

e-Valora offers financial consulting services to the private as well as to the public sector, and is specialized in

company valuations. Among other services provided, we must highlight advisory services towards mergers and

acquisitions, the elaboration of economic and financial studies, business and viability plans, and financial and

business consulting services.

Since its foundation in November of 2000 by a team of experts coming from international investment banks, e-

Valora has carried out more than 1,000 valuations of Spanish and foreign companies, from companies with less than

1 million Euros of turnover to companies with more than 500 million Euros of turnover, from start-ups to companies

with more than 80 years of history, including services and industrial companies.

At the end of 2008, e-Valora increased its professional team with members that have a wide experience in

investment banking, coming from entities such as Bank of America or Rothschild, that have worked in projects

belonging to every economic sector.

e-Valora has got ISO 9001 Certification in Business Valuation Services, Corporate Finance Advisory Services and

Elaboration of Valuation Multiples.

Its offices locations and contact details are the following :

e-Valuation Financial Services North America14 Wall Street, 20th FloorNew York City, New York 10005 United States of America

e-Valuation Financial Services Central and South AmericaBrickell Avenue, 11th FloorMiami, 33131

United States of America

Appendix I. e-Valora Company Presentation

32

www.evaluation.us

Est

ricta

mente

Pri

vado y

Confi

dencia

l January 2011 COMPANY XYZ – TAILORED VALUATION

www.e-valuation.us

Nota 1: WACC: Weighted Average Cost of Capital

The cost of capital is equal to the weighted average of the cost of debt and equity

To calculate the DCF we need to estimate the company’s cost of capital:

When valuing XYZ, the WACC has been calculated as the mean of the WACC of other companies that operate in the same industry

In the following table we detail how such discount rate has been calculated:

The calculated and adjusted discount rate is of 15,0%. A 5% has been added to such rate to take into consideration the company’s risk premium given

that it is smaller than its comparables, its equity has no liquidity and its turnover is very concentrated.

Appendix II. WACC Calculation

Calculation of the Weighted Average Cost of Capital

33

Comparable Companies WACC

ADECCO 9,5%

RANDSTAD 9,7%

MANPOWER 10,9%

USG People 9,8%

Kelly services 9,8%

Kforce 10,0%

Administaff, Inc. 10,5%

Average 10,0%

+ 5 percentage points 5,0%

WACC 15,00%

Company A

Company B

Company C

Company D

Company E

Company F

Company G

www.evaluation.us

Est

ricta

mente

Pri

vado y

Confi

dencia

l January 2011 COMPANY XYZ – TAILORED VALUATION

www.e-valuation.usAppendix III. Historical and Projected Financial Statements

34

Balance Sheet (Euros)

ASSETS 2007 2008 2009 N 2010 2011 2012 2013 2014

FIXED ASSETS 242 242 0 707 1.232 1.596 1.802 1.846

Tangible assets 242 242 0 707 1.232 1.596 1.802 1.846

Machinery 2.019 2.019 2.019 2.150 2.280 2.412 2.549 2.689

Other Installations 10.504 10.504 10.504 11.184 11.860 12.548 13.258 13.989

Tangibles 1.123 1.123 1.123 1.196 1.268 1.341 1.417 1.495

Accumulated Depreciation (13.404) (13.404) (13.645) (13.822) (14.175) (14.706) (15.422) (16.327)

CURRENT ASSETS 387.336 486.015 1.283.384 826.409 832.153 861.447 900.304 944.446

Debtors 390.341 484.555 1.261.830 696.037 690.860 704.677 725.818 747.592

Clients' Average payment days from invoice 385 533 127 57 57 57 57 57

Accounts Receivable 80.939 69.235 1.261.830 696.037 690.860 704.677 725.818 747.592

Other Debtors 309.402 415.320 0 0 0 0 0 0

Cash and cash equivalents (3.005) 1.460 21.554 130.372 141.293 156.770 174.486 196.853

TOTAL ASSETS 387.578 486.257 1.283.384 827.117 833.385 863.043 902.106 946.291

LIABILITIES 2007 2008 2009 N 2010 2011 2012 2013 2014

EQUITY 14.385 16.166 24.719 35.498 48.294 62.513 77.594 97.314

Shareholder's Equity 14.385 16.166 24.719 35.498 48.294 62.513 77.594 97.314

Capital 3.005 3.005 3.005 3.005 3.005 3.005 3.005 3.005

Reserves 895 11.379 13.161 13.161 13.161 13.161 13.161 13.161

Retained Surpluses/(Accumulated losses) 572 0 0 8.553 19.331 32.128 46.346 61.428

Profit/loss 9.912 1.782 8.553 10.779 12.796 14.219 15.081 19.720

CURRENT LIABILITIES 373.193 470.090 1.258.665 791.619 785.091 800.531 824.512 848.977

Short term debts 0 0 40.000 0 0 0 0 0

Debts held with financial institutions 0 0 0 0 0 0 0 0

Other short term debts 0 0 40.000 0 0 0 0 0

Short term debts with associated companies 0 0 49.360 0 0 0 0 0

Accounts Payable 373.193 470.090 1.169.305 791.619 785.091 800.531 824.512 848.977

Suppliers (87) 0 0 0 0 0 0 0

Creditors 372.755 447.286 171.592 0 0 0 0 0

Company's payment days form invoice 800 1.982 365 0 0 0 0 0

Pending remunerations (432) 7.992 344.635 245.837 243.879 248.756 256.219 263.906

% over sales 0,1% 2,4% 8,7% 5,6% 5,6% 5,6% 5,6% 5,6%

Income tax payable (2.303) 10.946 496.344 350.240 347.449 354.398 365.030 375.981

% over sales 0,6% 3,3% 12,5% 7,9% 7,9% 7,9% 7,9% 7,9%

Social Security Institutions Payable 3.260 3.867 156.734 195.542 193.763 197.376 203.262 209.090

% over total staff costs 1,8% 1,6% 4,7% 4,7% 4,7% 4,7% 4,7% 4,7%

Public Treasury, Output VAT 0 0 (0) 0 0 0 0 0

TOTAL LIABILITIES 387.578 486.257 1.283.384 827.117 833.385 863.043 902.106 946.291

www.evaluation.us

Est

ricta

mente

Pri

vado y

Confi

dencia

l January 2011 COMPANY XYZ – TAILORED VALUATION

www.e-valuation.usAppendix V. Glossary

Intangible Assets or Intangible Fixed Asset: Non-physical assets such as franchises, trademarks, patents, copyrights, goodwill,

shares, securities and contracts (as distinguished from physical assets) that grant rights and privileges.

Tangible Assets or Tangible Fixed Asset: Physical assets (such as machinery, property, etc).

Amortization: Accounting procedure that gradually reduces the cost of value of an asset, tangible or intangible, (e.g.

investments in research & development), through periodic charges to the profit and loss account in order to fix the costs during

its estimated useful life.

Trading Comparable Companies: Those enterprises whose business value is obtained through methods that compare the

company to be valued to similar enterprises. It is calculated dividing the market value of the last ones by a financial magnitude

of the companies’ profit and loss account (such as net income, net sales, etc). When multiplying by the same enterprise’s

magnitude of the company to be valued, we will obtain its approximate value.

EBITDA: EBITDA refers to operating profit before amortizations.

EBIT: Earnings Before Interest and Taxes.

Balance Sheet: Statement of a company’s financial position at a given point in time. Lists the assets of a company and how

they have been financed. Total assets is equivalent to liabilities plus shareholders’ equity.

Cost of Supplies: Cost related to the production, supply, transport and storage of raw materials and the materials used in the

production process. In this section can also be included the cost of outsourcing services to provide the customer.

Profit and Loss Account: Financial statement that shows the expenses and revenues generated during a period of time.

Weighted Average Cost of Capital: Calculated as the cost of equity * (equity value / firm value) + cost of debt * (net debt /

firm value) * (1- corporate tax). It is a discount rate typically used to discount future free cash flows to the moment of

valuation.

Discounted Cash Flows (DCF): Company’s valuation method based on the idea that the value of a company is related to what it

is able to generate in the future. It is calculated as the future cash flows of a company, discounted back to present value using

an appropriate discount rate.

Net Debt: Total debt of the company minus any cash or liquid funds that the company has but does not require for its operating

activity.

38

www.evaluation.us

Est

ricta

mente

Pri

vado y

Confi

dencia

l January 2011 COMPANY XYZ – TAILORED VALUATION

www.e-valuation.usAppendix VI. e-Valuation’s References

2008 - 2009

Logistics

Media

Metallurgy

Quality Consulting

New Techonlogies

Other Building Specilialists

Outsourcing Services

Production and Distribution

Public Administration

Rail

Recreation

Advertising

Automotive

Aviation

Biotechnology

Brokerage and Financial Services

Building Materials Manufacturer

Business Services

Construction and Contracts

Construction and Materials

Construction Related Services

Consulting, Audit and Advisory

Ecological and Recycling

Editorial

Education and Training

Electronics

Engineering and Machinery

Entertainment and Leisure

Forestry

Healthcare

Insurance

Internet

Local TV

Renewable Energies

Restaurant

Retail

Software and Data Security

Sports

Steel

Technology

Telecommunicaciones

Textiles

Transportation and Logistics

Quemical Industry

NOTE: For confidentiality reasons our clients´ names are not revealed.39

www.evaluation.us

Est

ricta

mente

Pri

vado y

Confi

dencia

l January 2011 COMPANY XYZ – TAILORED VALUATION

www.e-valuation.usAppendix VII. Contact Details

www.evaluation.us

e-Valuation Financial Services North America e-Valuation Financial Services Northern Europe

14 Wall Street, 20th Floor One Canada Square, 29th Floor, Canary Wharf

New York City, New York, 10005 London, E14 5DY

Estados Unidos Reino Unido

e-Valuation Financial Services Central and South America e-Valuation Financial Services Southern Europe

111 Brickell Avenue, 11th Floor c/ José Ortega y Gasset, 42

Miami, 33131 Madrid, 28006

Estados Unidos España

40