Embed Size (px)

Citation preview

Sergey Syntulsky

Smart grid: technology and market

evidence

Smart grid ecosystem transition

Current state Target state

(Mostly) price and volume-

taking consumer

Prosumer with internal

optimization

Utility as unilateral service

provider

Utility as adaptive network

of prosumers

B2B utilities equipment

vendors

B2B + B2C vendors and

lessors

Regulation of power system

technical and economic

issues

Regulation of information

exchange (privacy,

interoperability) and pricing

of information/control

services

Current stateRole Current state

Consumers Demand response mostly for large consumers, PV

devices for household consumption, AMI, time-based

rates. But hard to engage in complicated cooperation,

need to be seamless.

Utilities Economic stimuli are not aligned enough. Later timing

option benefits (no exponential growth for early

adopters). It is easier to force new hardware installation,

but harder to encourage new business-processes.

Vendors Those who can work in emerging business model

achieve exponential growth, others have moderate

margins.

Governments Face transition problems: stranded assets, subsidies for

early adopters, problems with regulation for both old

and new ecosystem.

Open issues

Full equipment replacement :

Move to advanced metering and control devices

Move to distributed generators

Storage, consumer devices, electrical cars

Mechanism design, proper stimuli for each side:

New technical and economic regulation (information

exchange protocols, market model)

Good patterns for small (esp. household) consumers

involvement

Right risk/return for private funding

Plan

Technology changes

Bi-directional communications with consumer (AMI)

Intermittent (solar and wind) and cheap balancing

(gas and biofuel) power generation

Demand response/energy efficiency

Distribution automation

Moderate increase in reliability

Financial data perspective

Valuation of smart grid projects

Some cases in Russia

Technology trends

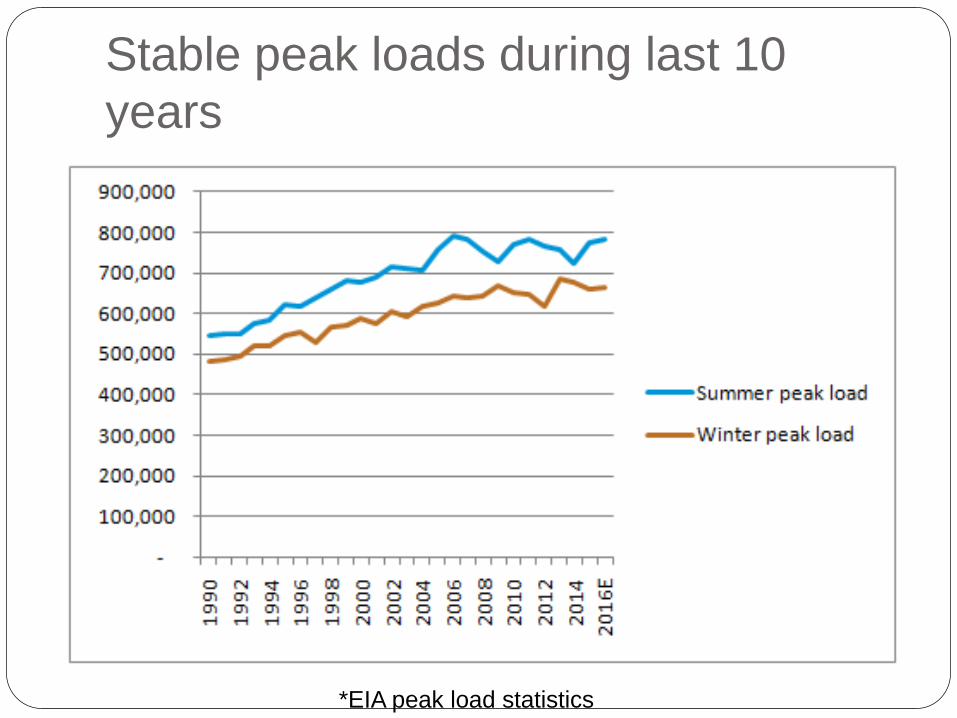

Stable peak loads during last 10

years

*EIA peak load statistics

Demand response ~700 000 customer-based devices under SGIG

prpgram (mostly direct load control devices and

controllable thermostats)

Customers enrolled in time-based pricing:

*chart from smartgrid.gov

Distribution automation

~8000 automated feeder switches installed (5%

of distribution circuits) in SGIG (smart grid

investment grant) program

=>50% shorter and 11%-49% less frequent

outages

Utilities data analytics market for utilities and

regulators is expected to grow 33% per year

Cybersecurity plan requirements for subsidized

projects

Reliability

*Charts from Larsen, LaCommare, Eto, Sweeney, Assessing Changes in reliability of the US Electric power

system, 2015

Plan

Technology changes

Financial data perspective

Changes in utilities cost structure

Historical growth of sales and earnings

Fundamental growth rate

Sales/asset ratio

ETF historical returns and PEG

Valuation of smart grid projects

Some cases in Russia

Utilities cost structure change

*EIA utilities expenses report

Historical growth High sales growth in

equipment sector

(>market)

Small growth in utilities

and power sectors

(<market)

Strong margin growth

relative to weak sales

growth in utilities and

power sectors

*data published by Aswath Damodaran:

http://people.stern.nyu.edu/adamodar/New_Home_Page/dataarchived.html

Fundamental growth rate = ROC *

reinvestment rate

Reinvestment rate (NetCapEx/EBIT)

NetCapEx = CapEx - Depreciation

Return on capital (EBIT/Assets)

Sales/assets ratio

Net investments / sales by industry

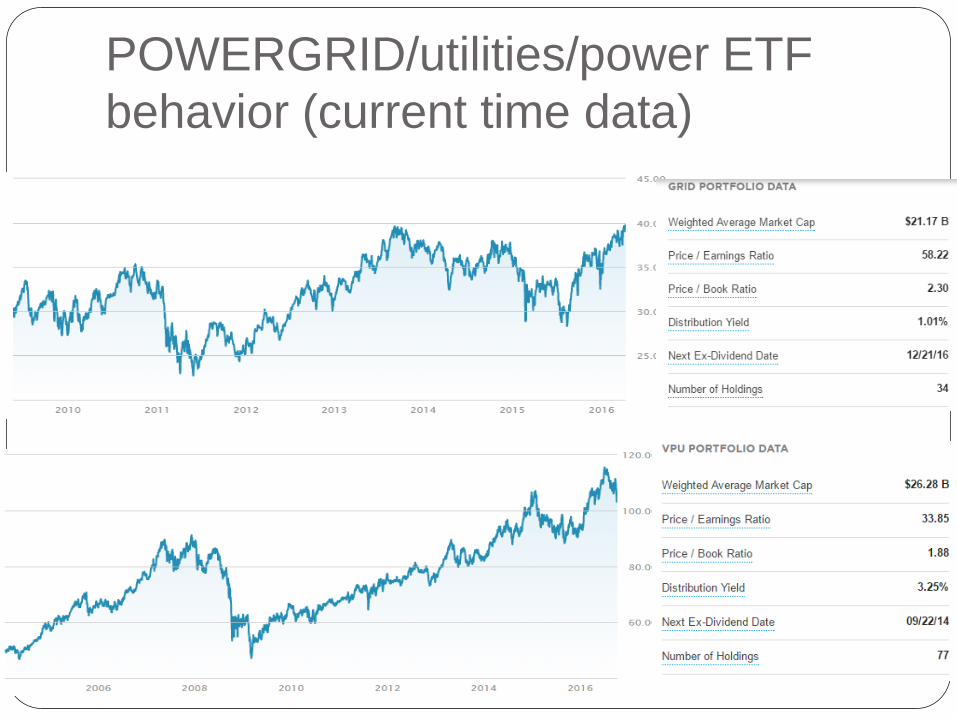

POWERGRID/utilities/power ETF

behavior (current time data)

Price/Earnings/Growth

*data published by Aswath Damodaran:

http://people.stern.nyu.edu/adamodar/New_Home_Page/dataarchived.html

Plan

Technology changes

Financial data perspective

Valuation of smart grid projects

Smart grid as real option

Generator valuation

Smart grid valuation

Some cases in Russia

Real option characteristics Some of smart grid value is delivered in straight-

forward way:

Reliability/QOS increase

Reduction in losses due to better dispatch

Decrease in capacity reserves needed

Other part of smart grid value is an option:

To build new generation (small scale and on consumer

side)

To establish new pricing and shared control schemes

While first part can be estimated under existing

regulatory framework, second is non-trivial

Example

Consider option:

to build small-scale gas-fired power plant on

consumer side

connect it to the grid,

sell excess energy to the grid for years.

Its value depends on gas and power market

prices

Gas power fired plant can be valued as spark

spread option

t – hour

Vt – consumption

C – generator capacity

K – efficiency coefficient

Gt – gas price

Xt – electricity price

f – price of electricity consumed from grid

g – price for selling electricity

Example: generator valuation

Example: smart grid valuation

Cost – cost function to build generator with capacity

C

Build 2D tree:

1st dimension – long-term gas price

2nd dimension – long-term electricity price

Plan

Technology changes

Financial data perspective

Valuation of smart grid projects

Some cases in Russia

Smart grids in Russia: pros and cons

UIAS FTS of Russia regulation approach

Utilities automation issues

Smart grids in Russia: cons

Some factors are against immediate smart grid

development:

Low demand for non-hydro renewables (cheap gas)

Low household tariffs (cross-subsidies)

Low median household income (will not invest in

smart appliances)

Access to cheap financing is limited for small

entities

Poor contracts enforcement (incumbent can

preserve market share)

Smart grids in Russia: pros Some new initiatives like virtual power plant and

smart grid in Crimea, not enough information

On opposite there are some markets with good economic potential: Wind and fossil-based microgrids for power supply of

isolated or remote sites (like mines and related housing) Insolated territories of Northern Caucasus with

extremely high transmission expenses Large energy-intensive consumers (including world

largest district heating systems, water supply and disposal)

Smart grid creation seems to be less relevant task than power grid automation and quantitative decision support

UAIS scheme

SCADA and

metering system

ERP and

accounting

Computer-aided

design systems

Balance management system

Investments planning

Abnormal situations (losses,

outages) root cause analysis

Regulatory accounting and

cost allocation

Regional

regulatory

bodies

Holding

Federal

regulatory body

Cross-

validation

between grids

Forecasting and planning next

year balance

Scheme of typical contracts between

power grids in single region

Issues with utilities grid automation Technological state of different power grid parts can

be very different, often managed on different platforms

Accounting, CAD and metering entities are often not mapped

No explicit topology information is combined with metering data, unable to localize losses

Data exchange between power grid (operates metering) and energy retail (billing function) is poorly formalized (no single protocol)

Most value can be gained after full data model consolidation, it is time-consuming and expensive

Hard to prove value of analytical work to regulator under weak institutions

High corruption level leads to:

high abnormal power losses (stealing of energy)

unnecessary investments,

Projects, that are dedicated to prevent such

things can face opposition

Issues with utilities grid automation

![[Smart Grid Market Research] Smart Grid Hiring Trends Study (Part 2 of 2)- Zpryme Smart Grid Insights](https://img.dokumen.tips/doc/110x75/5414021c8d7f7284698b47a9/smart-grid-market-research-smart-grid-hiring-trends-study-part-2-of-2-zpryme-smart-grid-insights.jpg)

![[Smart Grid Market Research] South Korea: Smart Grid Revolution, Zpryme Smart Grid Insights, July 2011](https://img.dokumen.tips/doc/110x75/5414026d8d7f727d698b47c7/smart-grid-market-research-south-korea-smart-grid-revolution-zpryme-smart-grid-insights-july-2011.jpg)

![[Smart Grid Market Research] Smart Grid Index: November 2012 - Zpryme Smart Grid Insights](https://img.dokumen.tips/doc/110x75/541402018d7f728a698b47a5/smart-grid-market-research-smart-grid-index-november-2012-zpryme-smart-grid-insights.jpg)