Embed Size (px)

Citation preview

UNEXPLORED MULTIBAGGER SMALL CAP STOCKS

EQUITY RESEARCH REPORT

CHEMFAB ALKALIS LTD.

BSE CODE: 506894 NSE CODE: CHEMFALKAL

Industry: Commodity Chemicals CMP: Rs. 94.40 (06/09/2015)

Market Cap: 86.66 (INR in Crore) Target Price: Rs. 170 Date: Sep 06, 2015 Time Period: 12 – 24 months

Saral Gyan Capital Services

An Independent Equity Research Firm www.saralgyan.in | www.saralgyan.com

HIDDEN GEMS – AUGUST 2015

- 2 - SARAL GYAN CAPITAL SERVICES

TABLE OF CONTENT

S.No Content Page No.

1. Company Background 03

2. Recent Developments 06

3. Financial Performance 07

4. Peer Group Comparison 09

5. Key Concerns / Risks 09

6. Saral Gyan Recommendation 10

7. Disclaimer 12

HIDDEN GEMS – AUGUST 2015

- 3 - SARAL GYAN CAPITAL SERVICES

1. Company Background A Chennai based company Chemfab Alkalis Ltd (CAL) was incorporated in 1983. The company was promoted by

M/s Titanium Equipment and Anode Manufacturing Company Limited. CAL manufactures chemicals for industrial applications. In June 2009, chlorates division has been closed permanently due to frequent power problems and labor unrest. Company established India’s first Membrane Cell Caustic Soda Plant and commenced production from July, 1985. CAL is the first Indian company to use the power saving ion exchange membrane cell technology to manufacture caustic soda. Chemfab Alkalis (CAL) also produces Sodium Hypochlorite and sodium Chlorate and the bye products of caustic soda like chlorine and hydrozen. Chemfab Chlorates, a group company was amalgamated with Chemfab Alkalies Ltd during the year 2001-02 on the approval from High court of Madras. The company has also takenover the management of Salt fields by the way of backward integration. The salt fields are situated at marakanam 25 kms from the factory of the company. Chemfab Alkalis was selected for the 1988 award of excellence in Environment Preservation and Pollution Control by the Federation of Indian Chambers of Commerce and Industry for its membrane cell technology which totally eliminated the use and disposal of mercury. Products

Caustic Soda Lye in two grades (33% & 48%).

Liquid Chlorine

Hydrogen Gas

Hydrochloric Acid

Sodium Hypochlorite / Bleach Liquor

Barium Sulphate The above products are completely free from mercury and are used in food processing industries as well. The first ever pollutant free caustic soda in the country was from CAL. The quality of the products matches the requirements of BIS and meets international specifications.

HIDDEN GEMS – AUGUST 2015

- 4 - SARAL GYAN CAPITAL SERVICES

CAL commenced the operation with the production capacity of 25 TPD and now operates at 100 TPD. The features of the plant recently revamped it’s with the latest-state-of-the-art BiTAC technology, and looking forward to double its production capacity to 200 TPD.

Chlor alkali market in India has witnessed healthy growth in recent years, largely driven by increasing demand from end user industries due to higher output from the chemicals sector. Chlor alkali market is broadly categorized into three segments, namely Caustic Soda, Chlorine and Soda Ash. Caustic Soda finds major application in diverse industries, such as soap & detergents, pulp & paper and textile processing among others. Chlorine is produced as a by-product during caustic soda production and is widely used during PVC manufacturing, drinking water disinfection and pharmaceutical production. Soda Ash is used mainly during glass, soap & detergent and silicate production. With strong growth anticipated in all these end use industries, the market for chlor alkali in India is forecast to grow considerably in the next five years. According to India Chlor Alkali Market Forecast & Opportunities, 2019, the market for chlor alkali in India is projected to exhibit a CAGR of around 7% during 2014-19. The market is expected to witness high penetration rate in the Western and Northern regions of the country. The market, though highly fragmented at present, is gradually moving towards consolidation, particularly with the entry of foreign players and expansion in distribution network of existing players. Among the three market segments, caustic soda held the highest revenue share, followed by chlorine and soda ash segments. Soap & detergent is the main end user industry in the chlor alkali market, followed by glass, pulp &paper, alumina and other industries.

HIDDEN GEMS – AUGUST 2015

- 5 - SARAL GYAN CAPITAL SERVICES

Research & Development The Company has an in-house Research Development Department, where the main areas of focus are Energy Conservation, Process Upgradation and Environmental Preservation. The Ministry of Science and Technology, Department of Scientific and Industrial Research, Government of India, has recognized the Company’s inhouse R & D facilities, which is valid upto 31st March, 2017. The Company has a sophisticated Quality Assurance (QA) Laboratory recognized by DuPont, USA for the analysis of Chlor- Alkali brine. The Brine from various Chlor- Alkali Industries in India is being analyzed at CAL-QA Laboratory. The Company continues to take all possible steps to conserve energy in every area of its operations recognized by DuPont, USA for the analysis of Chlor- Alkali brine. The Brine from various Chlor- Alkali Industries in India is being analyzed at CAL-QA Laboratory. The Company continues to take all possible steps to conserve energy in every area of its operations. The company continues to use hydrogen gas instead of conventional fuel reducing the carbon footprint. The company has also installed solar street lightings and also the Bio Gas plant for replacing conventional energy sources by making investment of Rs. 10 lakhs.

HIDDEN GEMS – AUGUST 2015

- 6 - SARAL GYAN CAPITAL SERVICES

2. Recent Development Replacement of old plant with Bipolar BiTAC Electrolysers Plant from CEC, Japan. In 2014, company introduced a new BiTAC® Electrolysers from CEC, Japan for the first time in the Country. The new Plant was commissioned during August 2014, and is operating well within the agreed operational parameters and will result in savings in energy consumption to the tune of 30% to 40%. Company has also replaced the old Caustic Concentration plant with a new Plant and this was commissioned in the month of March 2015. This will also result in improved operational efficiencies.

Ongoing Expansion Plans to drive Revenue Growth & Profitability Company awaits the statutory clearances for its expansion plans and a favourable decision on its appeal before the National Green Tribunal. Company has also made plans for venturing into newer areas for Chlorine utilisation. The Company is in the process of developing 632 acres of salt fields and the production of salt is expected to commence post completion of the development activities. The new Salt fields which were acquired are slated to commence production shortly. With all these measures, management is confident that company is poised for a great leap ahead and achieving good results in the forthcoming years.

HIDDEN GEMS – AUGUST 2015

- 7 - SARAL GYAN CAPITAL SERVICES

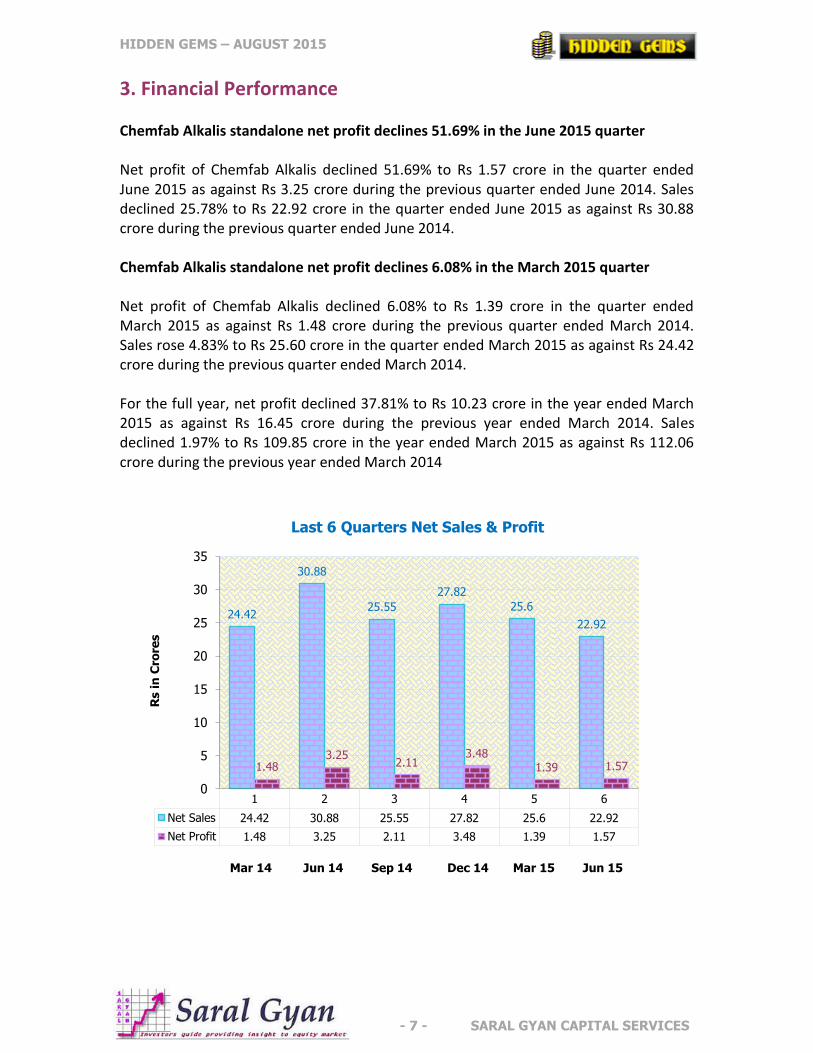

3. Financial Performance Chemfab Alkalis standalone net profit declines 51.69% in the June 2015 quarter Net profit of Chemfab Alkalis declined 51.69% to Rs 1.57 crore in the quarter ended June 2015 as against Rs 3.25 crore during the previous quarter ended June 2014. Sales declined 25.78% to Rs 22.92 crore in the quarter ended June 2015 as against Rs 30.88 crore during the previous quarter ended June 2014. Chemfab Alkalis standalone net profit declines 6.08% in the March 2015 quarter Net profit of Chemfab Alkalis declined 6.08% to Rs 1.39 crore in the quarter ended March 2015 as against Rs 1.48 crore during the previous quarter ended March 2014. Sales rose 4.83% to Rs 25.60 crore in the quarter ended March 2015 as against Rs 24.42 crore during the previous quarter ended March 2014. For the full year, net profit declined 37.81% to Rs 10.23 crore in the year ended March 2015 as against Rs 16.45 crore during the previous year ended March 2014. Sales declined 1.97% to Rs 109.85 crore in the year ended March 2015 as against Rs 112.06 crore during the previous year ended March 2014

1 2 3 4 5 6

Net Sales 24.42 30.88 25.55 27.82 25.6 22.92

Net Profit 1.48 3.25 2.11 3.48 1.39 1.57

24.42

30.88

25.55

27.82

25.6

22.92

1.48 3.25

2.11 3.48

1.39 1.57

0

5

10

15

20

25

30

35

Rs i

n C

rore

s

Mar 14 Jun 14 Sep 14 Dec 14 Mar 15 Jun 15

Last 6 Quarters Net Sales & Profit

HIDDEN GEMS – AUGUST 2015

- 8 - SARAL GYAN CAPITAL SERVICES

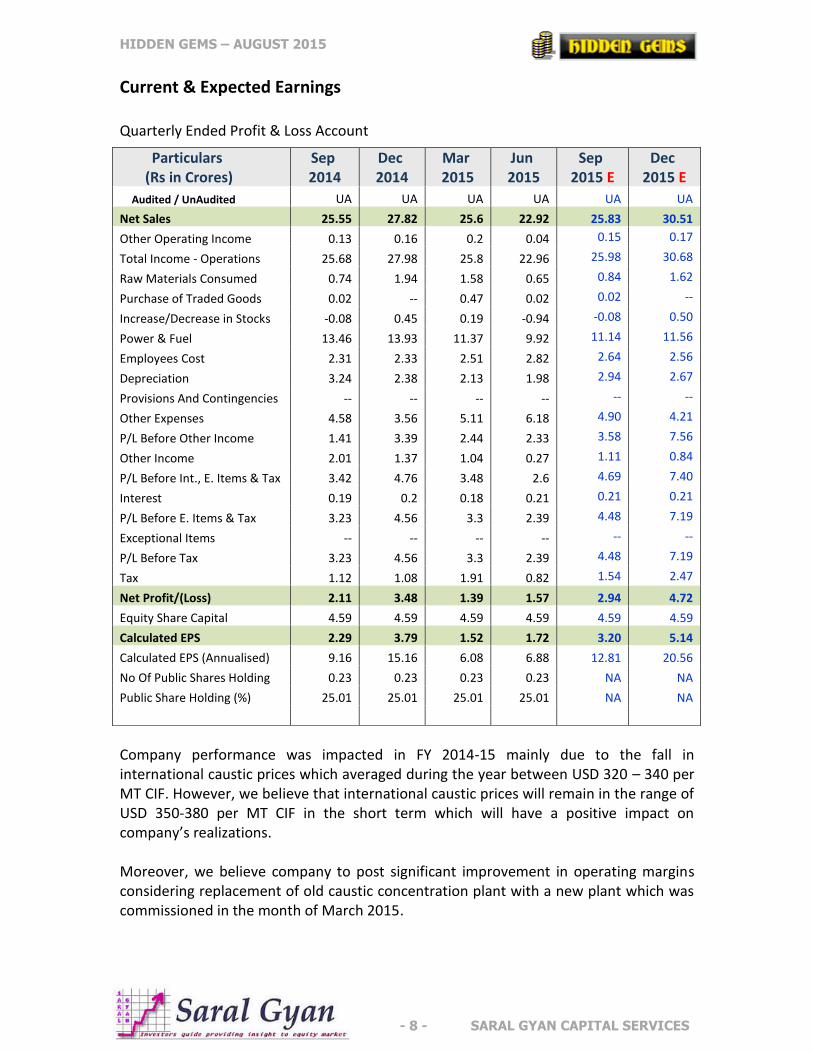

Current & Expected Earnings Quarterly Ended Profit & Loss Account

Company performance was impacted in FY 2014-15 mainly due to the fall in international caustic prices which averaged during the year between USD 320 – 340 per MT CIF. However, we believe that international caustic prices will remain in the range of USD 350-380 per MT CIF in the short term which will have a positive impact on company’s realizations. Moreover, we believe company to post significant improvement in operating margins considering replacement of old caustic concentration plant with a new plant which was commissioned in the month of March 2015.

Particulars (Rs in Crores)

Sep 2014

Dec 2014

Mar 2015

Jun 2015

Sep 2015 E

Dec 2015 E

Audited / UnAudited UA UA UA UA UA UA

Net Sales 25.55 27.82 25.6 22.92 25.83 30.51

Other Operating Income 0.13 0.16 0.2 0.04 0.15 0.17

Total Income - Operations 25.68 27.98 25.8 22.96 25.98 30.68

Raw Materials Consumed 0.74 1.94 1.58 0.65 0.84 1.62

Purchase of Traded Goods 0.02 -- 0.47 0.02 0.02 --

Increase/Decrease in Stocks -0.08 0.45 0.19 -0.94 -0.08 0.50

Power & Fuel 13.46 13.93 11.37 9.92 11.14 11.56

Employees Cost 2.31 2.33 2.51 2.82 2.64 2.56

Depreciation 3.24 2.38 2.13 1.98 2.94 2.67

Provisions And Contingencies -- -- -- -- -- --

Other Expenses 4.58 3.56 5.11 6.18 4.90 4.21

P/L Before Other Income 1.41 3.39 2.44 2.33 3.58 7.56

Other Income 2.01 1.37 1.04 0.27 1.11 0.84

P/L Before Int., E. Items & Tax 3.42 4.76 3.48 2.6 4.69 7.40

Interest 0.19 0.2 0.18 0.21 0.21 0.21

P/L Before E. Items & Tax 3.23 4.56 3.3 2.39 4.48 7.19

Exceptional Items -- -- -- -- -- --

P/L Before Tax 3.23 4.56 3.3 2.39 4.48 7.19

Tax 1.12 1.08 1.91 0.82 1.54 2.47

Net Profit/(Loss) 2.11 3.48 1.39 1.57 2.94 4.72

Equity Share Capital 4.59 4.59 4.59 4.59 4.59 4.59

Calculated EPS 2.29 3.79 1.52 1.72 3.20 5.14

Calculated EPS (Annualised) 9.16 15.16 6.08 6.88 12.81 20.56

No Of Public Shares Holding 0.23 0.23 0.23 0.23 NA NA

Public Share Holding (%) 25.01 25.01 25.01 25.01 NA NA

HIDDEN GEMS – AUGUST 2015

- 9 - SARAL GYAN CAPITAL SERVICES

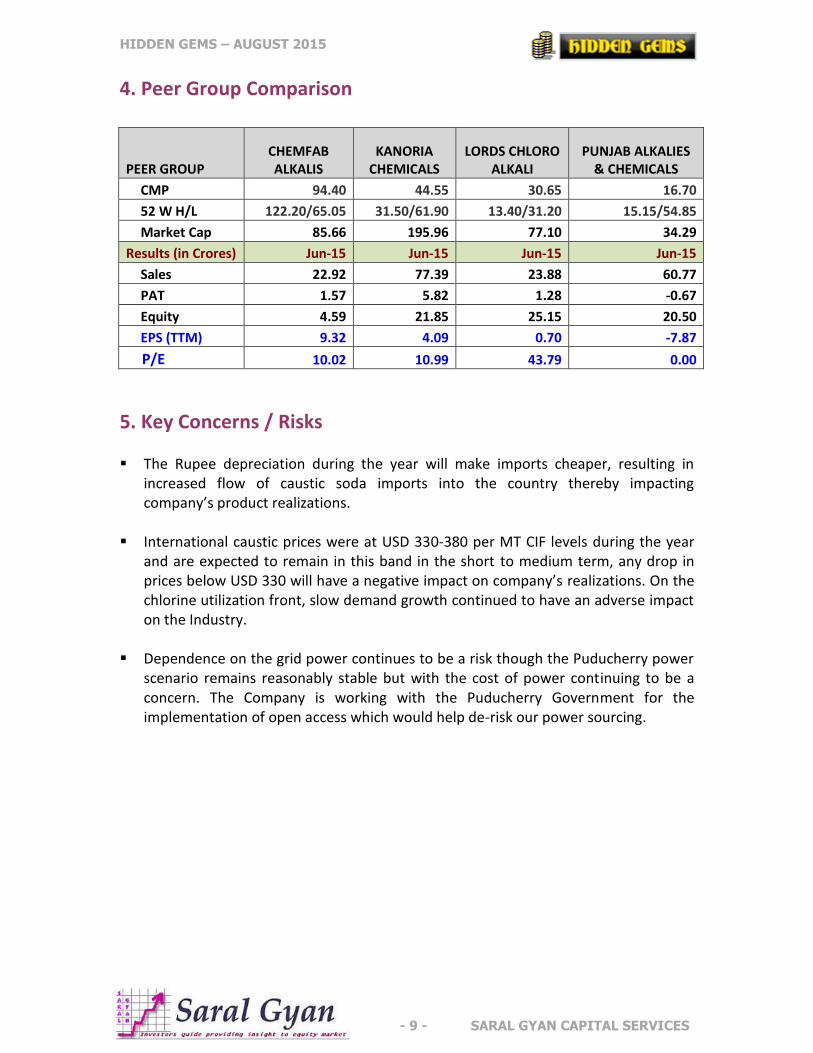

4. Peer Group Comparison

PEER GROUP CHEMFAB ALKALIS

KANORIA CHEMICALS

LORDS CHLORO ALKALI

PUNJAB ALKALIES & CHEMICALS

CMP 94.40 44.55 30.65 16.70

52 W H/L 122.20/65.05 31.50/61.90 13.40/31.20 15.15/54.85

Market Cap 85.66 195.96 77.10 34.29

Results (in Crores) Jun-15 Jun-15 Jun-15 Jun-15

Sales 22.92 77.39 23.88 60.77

PAT 1.57 5.82 1.28 -0.67

Equity 4.59 21.85 25.15 20.50

EPS (TTM) 9.32 4.09 0.70 -7.87

P/E 10.02 10.99 43.79 0.00

5. Key Concerns / Risks The Rupee depreciation during the year will make imports cheaper, resulting in

increased flow of caustic soda imports into the country thereby impacting company’s product realizations.

International caustic prices were at USD 330-380 per MT CIF levels during the year

and are expected to remain in this band in the short to medium term, any drop in prices below USD 330 will have a negative impact on company’s realizations. On the chlorine utilization front, slow demand growth continued to have an adverse impact on the Industry.

Dependence on the grid power continues to be a risk though the Puducherry power

scenario remains reasonably stable but with the cost of power continuing to be a concern. The Company is working with the Puducherry Government for the implementation of open access which would help de-risk our power sourcing.

HIDDEN GEMS – AUGUST 2015

- 10 - SARAL GYAN CAPITAL SERVICES

6. Saral Gyan Recommendation

Chlor-Alkali is the basic Heavy Chemical Industry, manufacturing Caustic Soda, with Chlorine, Hydrogen, Sodium Hypo Chlorate and Hydro Chloric Acid as by-products. Overall, the Financial Year 2014-15 was an average year for the Industry, primarily due to the fall in international caustic prices which averaged during the year between USD 320 – 340 per MT CIF. International caustic prices have now moved to USD 360-380 per MT CIF levels and are expected to remain in this band in the medium term which will have a positive impact on company’s realizations.

Caustic Soda finds major application in diverse industries, such as soap & detergents, pulp & paper and textile processing among others. Chlorine is produced as a by-product during caustic soda production and is widely used during PVC manufacturing, drinking water disinfection and pharmaceutical production. With the rebound in the country’s GDP, the demand for caustic is likely to grow strong which will help company to boost its revenue growth with higher capacity utilization. However, slower chlorine demand is expected to continue to impact the capacity utilisation of the company.

In 2014, company introduced new BiTAC® Electrolysers from CEC, Japan for the first time in the country. The new Plant was commissioned during August 2014, and is expected to result in savings in energy consumption to the tune of 30% to 40%. Company has also replaced its old caustic concentration plant with a new plant which was commissioned in Mar’15. These initiatives will help company to improve its profit margins significantly with increase in revenues going forward.

With the rebound in the country’s GDP, the demand for caustic is likely to grow

strong. However, slower chlorine demand is expected to continue to impact the capacity utilisation of the industry. The investments and efforts taken by the Company during last financial year are expected to result in significant savings in its manufacturing costs, especially power cost.

Company’s EBITDA and PAT margins are expected to improve significantly

considering investments and efforts taken by the Company during last financial year which will result in significant savings in its manufacturing costs, especially power cost.

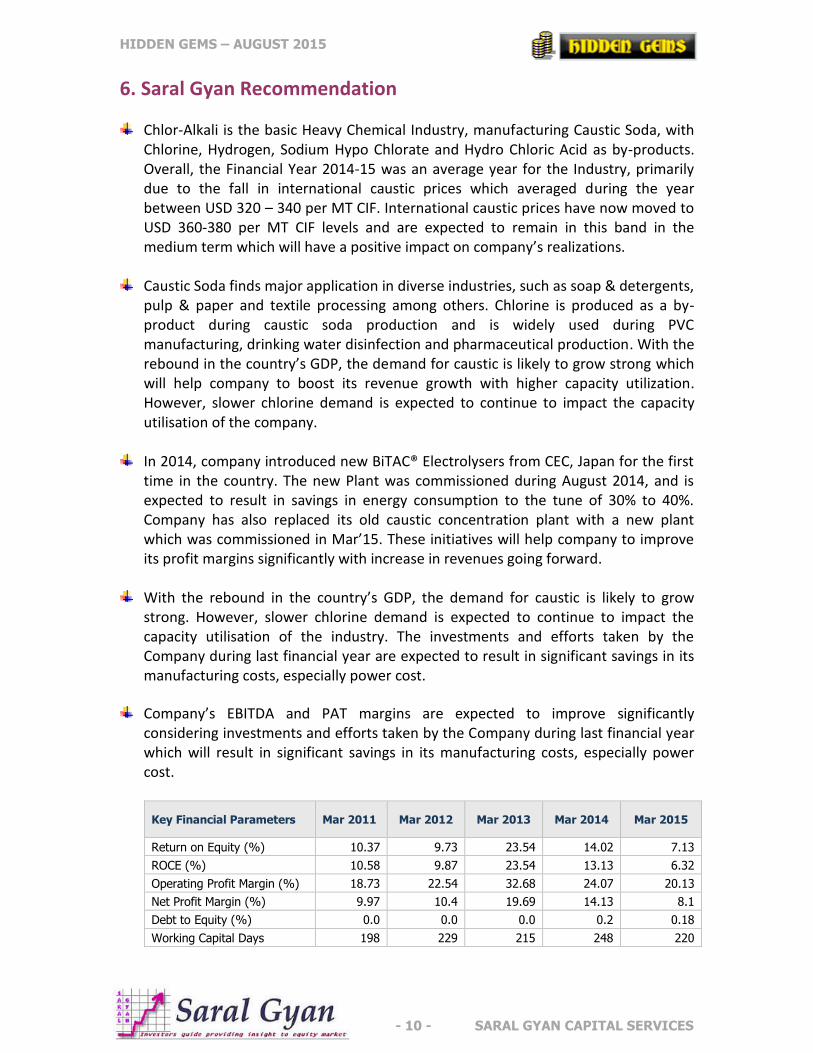

Key Financial Parameters Mar 2011 Mar 2012 Mar 2013 Mar 2014 Mar 2015

Return on Equity (%) 10.37 9.73 23.54 14.02 7.13

ROCE (%) 10.58 9.87 23.54 13.13 6.32

Operating Profit Margin (%) 18.73 22.54 32.68 24.07 20.13

Net Profit Margin (%) 9.97 10.4 19.69 14.13 8.1

Debt to Equity (%) 0.0 0.0 0.0 0.2 0.18

Working Capital Days 198 229 215 248 220

HIDDEN GEMS – AUGUST 2015

- 11 - SARAL GYAN CAPITAL SERVICES

Chemfab Alkalis is virtually debt free with reserves of Rs. 125 crores in its books which is much more than the company’s current market capital of Rs. 87 crores. Promoter’s shareholding is at 75% without pledging any shares and rest is held by non-institutional investors. FII and DII shareholding is nil in the company.

Company awaits the statutory clearances for its expansion plans and a favourable decision on its appeal before the National Green Tribunal. Company has also made plans for venturing into newer areas for Chlorine utilisation. The new Salt fields which were acquired are slated to commence production shortly. With all these measures, management is confident that company is poised for a great leap ahead and achieving good results in the forthcoming years.

Management has rewarded shareholders by paying regular dividend in the past. For FY 14-15, company has declared dividend of Rs. 1.25 per share.

YEAR Mar'11 Mar'12 Mar'13 Mar'14 Mar'15

EPS 10.55 8.15 25.60 17.93 11.15

Dividend / Share (In Rs) 2.50 0.00 5.00 1.25 1.25

As per our estimates, Chemfab Alkalis Ltd can deliver bottom line of 13.5 crores for full financial year 2016, annualized EPS of Rs. 14.7 with forward P/E ratio of 6.4X for FY16. Valuation looks attractive for a debt free company with expected expansion in its profit margins.

On equity of Rs. 4.59 crore, the estimated annualized EPS for FY 15-16 works out to Rs. 14.7 and the Book Value per share is Rs. 142.86. At current market price of Rs. 94.40, stock price to book value is 0.66.

Considering recent initiatives taken by the management in terms of improving operational efficiencies and company’s expansion plans to drive business growth, Saral Gyan team recommends “Buy” on Chemfab Alkalis Ltd at current market price of Rs. 94.40 for target of Rs. 170 over a period of 12 to 24 months. Buying Strategy:

70% at current market price of 94.40 30% at price range of 80-85 (in case of correction in stock price in near term)

Portfolio Allocation: 3% of your equity portfolio.

HIDDEN GEMS – AUGUST 2015

- 12 - SARAL GYAN CAPITAL SERVICES

7. Disclaimer Important Notice: Saral Gyan Capital Services is an Independent Equity Research Company.

© SARAL GYAN CAPITAL SERVICES

DISCLOSURE WITH REGARDS TO OWNERSHIP AND MATERIAL CONFLICTS OF INTEREST:

a. 'subject company' is a company on which a buy/sell/hold view or target price is given/changed in this Research Report

b. Neither Saral Gyan, it's Associates, Research Analyst or his/her relative have any financial interest in the subject company.

c. Neither Saral Gyan, it's Associates, Research Analyst or his/her relative have actual/beneficial ownership of one percent or more securities of the subject company

d. Neither Saral Gyan, it's Associates, Research Analyst or his/her relative have any other material conflict of interest at the time of publication of the research report.

DISCLOSURE WITH REGARDS TO RECEIPT OF COMPENSATION:

a. Neither Saral Gyan nor it's Associates have received any compensation from the subject company in the past twelve months.

b. Neither Saral Gyan nor it's Associates have managed or co-managed public offering of securities for the subject company in the past twelve months.

c. Neither Saral Gyan nor it's Associates have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months.

d. Neither Saral Gyan nor it's Associates have received any compensation for products or services from the subject company.

e. Neither Saral Gyan nor it's Associates have received any compensation or other benefits from the subject company or third party in connection with the research report.

GENERAL DISCLOSURES:

a. The Research Analyst has not served as an officer, director or employee of the subject company. b. Saral Gyan or the Research Analyst has not been engaged in market making activity for the subject company.

Definitions of Terms Used:

a. Buy recommendation: This means that the investor could consider buying the concerned stock at current market price keeping in mind the tenure and objective of the recommendation service.

b. Hold recommendation: This means that the investor could consider holding on to the shares of the company until further update and not buy more of the stock at current market price.

c. Buy at lower price: This means that the investor should wait for some correction in the market price so that the stock can be bought at more attractive valuations keeping in mind the tenure and the objective of the service.

d. Sell recommendation: This means that the investor could consider selling the stock at current market price keeping in mind the objective of the recommendation service.

LEGAL DISCLAIMER: Nothing published herein or on www.saralgyan.in / www.saralgyan.com should be considered as personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investment advice. This document prepared by our research analysts does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. It should be noted that the information contained herein is from publicly available data or other sources believed to be reliable. Neither Saral Gyan, nor any person connected with it accepts any liability arising from the use of this document. This document is prepared for assistance only and is not intended to be and must not be taken as the basis for any investment decision. The investment discussed or views expressed may not be suitable for all investors. The user assumes the entire risk of any use made of this information. The recipients of Saral Gyan material should rely on their own investigations and take their own professional advice. Each recipient of Saral Gyan should make such investigations as it deems necessary to arrive at an independent evaluation of an investment referred to in this document (including the merits and risks involved), and should consult its own advisers to determine the merits and risks of such an investment. Price and value of the investments referred to in this material may go up or down.