Embed Size (px)

DESCRIPTION

Dissertation Presented in partial fullfulment of the requirements of The Manchester MBA.

Citation preview

0

The University of Manchester

Manchester Business School

Risk Management in Islamic Financial Institutions

Mohamed Abdulla Ebrahim

Student registration number: 7396184

This dissertation is submitted in partial fulfilment

of the requirements for the degree of

Master of Business Administration.

1

A. DECLARATION

This work has not previously been accepted in substance for any degree

and is not being concurrently submitted in candidature for any degree.

Signed……………………………………………….

Mohamed Abdulla Ebrahim

Student number: 7396184

Date 4th April 2011

STATEMENT 1

The dissertation being submitted in partial fulfilment of the requirements

for the degree of MBA

Signed……………………………………………….

Mohamed Abdulla Ebrahim

Student number: 7396184

Date 4th April 2011

STATEMENT 2

This dissertation is the result of my own independent work/investigation,

except where otherwise stated. Other sources are acknowledged by

footnotes giving explicit references. A bibliography is appended.

Signed……………………………………………….

Mohamed Abdulla Ebrahim

Student number: 7396184

Date 4th April 2011

STATEMENT 3

I hereby give my consent for my dissertation, if accepted, to be available for photocopying,

interlibrary loans and for electronic access, and for the title and

summary to be made available to outside organizations.

Signed……………………………………………….

Mohamed Abdulla Ebrahim

Student number: 7396184

Date 4th April 2011

2

B. ACKNOWLEDGEMENTS

I would like to dedicate this work to Caliph/Imam Hassan Ibne Ali (A.S) fifth (5th)

and last of

the Rightly Guided (Rashidun) Caliphs, the essence of whose life‟s work was to preserve the

unity of the Ummah of his grandfather the Prophet Mohamed (PBUH), the cost of which

included his abdicating from the role of Caliph to preserve this unity. One of his sayings which

inspires me and which I would like to share is “Teach others your knowledge and learn the

knowledge of other, so you will bring your knowledge to perfection and learn something you

did not know.”

I would like acknowledge the support and contributions of my family and friends who

influenced, encouraged and supported me to do this excellent MBA. I would like to mention the

contribution of my mother Late Mrs. Shirin Ebrahim, who pushed me to pursue excellence,

loved me unconditionally and inspired me to follow the path to actualise my talents and dreams.

I am thankful to two of my former employers during whose employ I started and completed the

process of attaining the Manchester MBA, namely Ernst & Young, Mombasa, Kenya, and

Credo Investments FZE, Dubai, UAE under whose employ I completed most of the academic

coursework and allowing leave me to attend the workshops as and when required.

I would like to record my appreciation to Dr. Antony Merna for his supervision of the project

and the support he provided during the course of completing this dissertation.

I am responsible for anything controversial in the dissertation, which is not meant to undermine

any school of thought/individual, as its objective is to increase knowledge.

Mohamed Abdulla Ebrahim

April 2011

3

C. ABSTRACT

Islamic finance (Capital Markets, Banking and Insurance) has emerged from a niche financial

market to the mainstream of finance. The geographic market, clientele served, products base and

volume of funds have grown significantly. Furthermore, the players have increased and now

include not only pure Islamic institutions but also hybrid players (conventional bank with

Islamic Finance windows). Therefore, not understanding the unique risks of the Islamic Finance

model (risk sharing and risk pooling) can cause a failure of the model igniting a financial crises

with a ripple effect on the Islamic faith. Hence, managing these unique risks is extremely

important.

Purpose / Perceived Value

To increase the academic knowledge base on Risk Management in Islamic Financial Institutions

and hope some useful insights would be obtained which in turn would lead to improvement in

risk management practices in Islamic Financial Institutions. This would explore the subject of

corporate risk management in the context of Islamic Financial Institutions, which are run on the

Islamic legal and economic system, which prohibits Riba (interest), avoids Gharar (uncertainty),

avoids Maysir (gambling or excessive speculation).

Methodology

Review material on risk management, Islamic finance and risk management in Islamic financial

institutions and their basis in academic and professional knowledge already written on. Analyse

disclosures in annual financial statements of three Islamic Financial Institutions and apply these

against a Risk Management framework. Carry out a Linkedin based pilot research survey on

Risk Management practices in Islamic Financial Institutions.

4

TABLE OF CONTENTS

S/No Title/Chapter From

Page

To

Page

Cover page 0 0

A Acknowledgements 1 1

B Declaration 2 2

C Abstract 3 3

1 Introduction 5 10

2 Risk Management 11 17

3 Islamic Finance 18 26

4 Importance of Risk Management in Islamic Financial Institutions 27 38

5 Analysis of Risk Management disclosures in Financial Statements 39 51

6 Analysis of responses from Linkedin pilot survey questioner 52 58

7 Conclusions and Recommendations for Further Work 59 62

8 Bibliography 63 63

5

Chapter 1: Introduction

1.1 Background

Risk Management is gaining momentum as a subject and a professional discipline in its own

right as distinct from Corporate Governance, Internal Audit/control, Financial Reporting and

Regulatory compliance to which it is closely aligned with. This has become pertinent as the

recent global financial crises (late 2007 to 2009) which has caused the deepest recession since

the Great depression which started in 1929 and continued to throughout the 1930‟s, has been

seen widely as a failure of financial institutions to manage the risks they undertook while

transacting business.

Islamic Finance has been one of the fastest growing segments of the financial sector. At one

time a common fallacy was Islamic Finance was less riskier than conventional finance, due to

the maxims of “al-kharaj bil dhaman and al-ghunm bil ghurm”, which basically propagate the

principle of „no risk no gain‟, very much underline the recognition of risk elements in Islamic

finance. (Zaid Ibrahim & Company)1. This dissertation shall endeavour to reflect the view that

Islamic Finance is simply different with its own unique set of risks which are neither more or

less riskier than other forms of finance.

A study undertaken by the International Monetary Fund (Cihak and Hesse, 2008)2 provides

empirical evidences which verify that Islamic finance is not necessarily more or less risky than

conventional finance. The study points out, that by having profit-loss sharing financing, this

shifts the direct credit risk from banks to their investment depositors. However, it also increases

the overall degree of risk of the asset side of banks‟ balance sheets, because it makes Islamic

banks vulnerable to risks normally borne by equity investors rather than holders of debt.

It was also pointed out that, because of their compliance with the Shariah, Islamic banks can use

fewer risk hedging techniques and instruments (such as derivatives and swaps) than

conventional banks. However, it is interesting to note that because of this prohibition against the

use of derivative products and short-selling activities in the form used by its conventional

counterparts, Islamic finance were largely shielded from exposure to „toxic assets‟ such as those

arising from collateralised debt obligations (CDO) and credit default swaps (CDS). But all is

was not well when the dust settled as Islamic Finance institutions like the Kuwait based Global

Investment House was technically in solvent.

1 Demystifying Islamic Finance – Correcting misconception, advancing value propositions Zaid Ibrahim & Co.

2 Islamic Banks and Financial Stability: An Empirical Analysis Martin Čihák and Heiko Hesse (2008) IMF working paper 0816

6

1.2 Aim and Objectives

The aim of this dissertation is to explore the theory and practice of risk management in the

context of Islamic Financial institutions, which is a fast growing segment of the financial sector.

Islamic Finance is no longer a niche confined to Muslim countries in the Middle East, it is part

of mainstream finance, with London vying with Dubai and Kuala Lumpur to be the Capital of

Islamic Finance. It is believed that a lot of written material is available on both Islamic Finance

and Risk management but much less on Risk Management practices in Islamic Financial

institutions. Its aim is to show that Islamic Finance is neither more riskier nor less riskier than

conventional finance, it is simply different.

The Islamic Finance model is based on social justice as articulated in the Holy Quran and the

traditions, acts and sayings of Prophet Muhammad (PBUH). This system prohibits Interest-

Riba, excessive risk taking “Gharar” (Uncertainty, Risk or Speculation) is also prohibited and

dealing only in activities considered Halal. In essence it is based on universal ethics flavored by

a religious outlook.

Objectives

To look at Islamic Finance and the unique risks it poses due to its principles and nature.

To understand how these risks differ from risks in conventional finance,

To review how these risks are currently being addressed

How these practices can be improved.

1.3 Literature Review

The literature review would include among others the following sources

a) Published research on both Risk Management and Islamic Finance by international

organisations and professional firms like IMF, Ernst & Young etc.

b) Published books on Corporate Risk Management and Islamic Finance

c) Publication of articles on Islamic finance, Risk Management on the internet/websites.

d) Published articles related to Risk Management in Islamic Finance in Magazines.

7

1.4 Research Methodology

To achieve the stated aims and objectives, the research methodology to be as follows:-

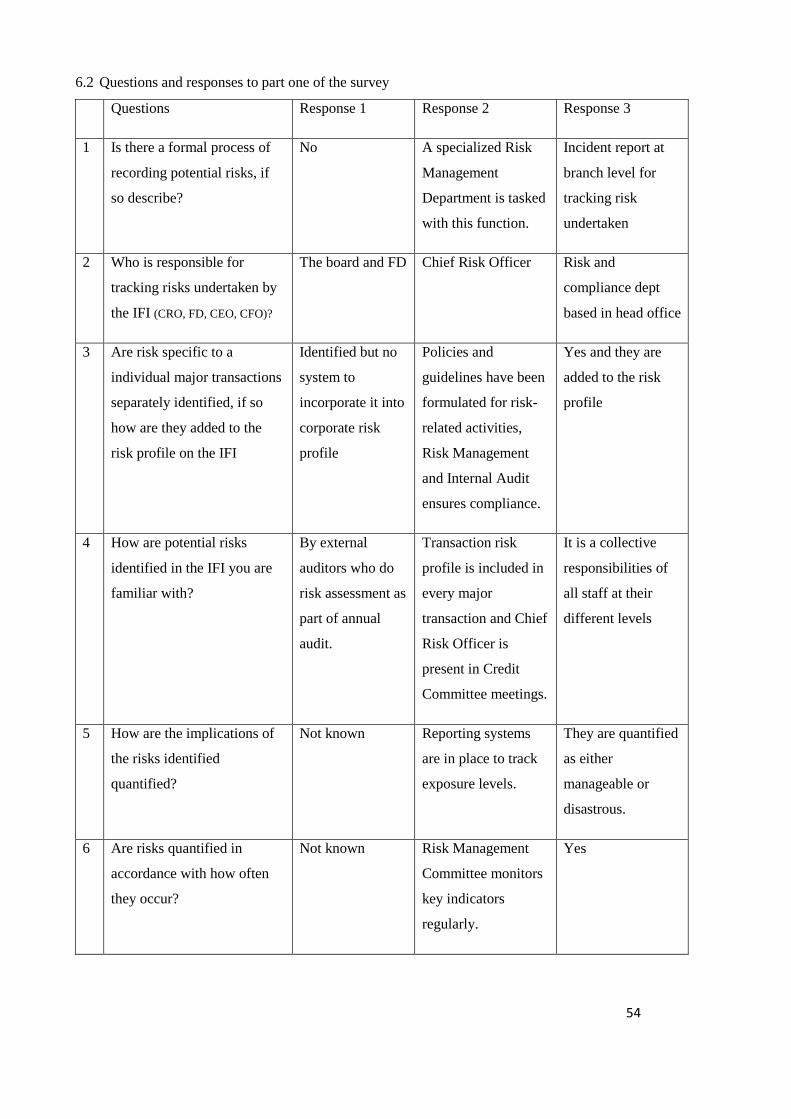

a) Questioner on Linkedin to Professionals and advisors working in Islamic finance on risk

management practices in Islamic Financial Institutions. The questions would be based on a

risk management model i.e. how risk identification takes place, and how these risks are dealt

with or should be dealt with in their opinion. This questioner will give an insight in current

practices in Risk Management and elicit opinion on the way forward. The following

questions will be put forward to be answered by the respondents.

Part 1 based on the Risk management cycle3 (Smith, 1995) comprises of the following

questions related to each component in accordance with your knowledge and experience

related to risk management practices in Islamic Financial institutions (IFI):-

1 Identification of Risks/Uncertainties

How are potential risks identified in the IFI you are familiar with?

Is there a formal process of recording potential risks?

Who is responsible for tracking risks undertaken by the IFI (CRO, FD, CEO, CFO)?

Are risk specific to a individual major transactions separately identified?

2 Analysis of Implications

How are the implications quantified?

Are risks quantified in accordance with how often they occur?

Are risks quantified as to severity i.e. potential of loss or impact on IFI?

To whom are these reported i.e. to the Board of directors or executive management?

3 Response to minimize risk

The following are the typical responses to minimize risk for an entity, please indicate in

your opinion the percentage of occurrences the particular response is chosen? Total 100%

Risk Avoidance (declining transaction)

Risk reduction (maybe by syndication)

Risk transfer (hedging or insurance)

Risk retention (accept the risk)

4 Allocation of appropriate contingencies

How is the desirable/acceptable level of risk determined?

How are resources allocated to ensure the overall risk level is acceptable?

Are contingency plans put place should the risk materialize?

If yes, how are these communicated to the members of the organization?

3 Corporate Risk Management – Tony Merna and Faisal F Al Thani 2nd edition 2010

8

Part 2 Objective is to elicit opinion on way forward on improving the practice of risk

management in Islamic Financial Institutions.

In your opinion is the state of risk management practice adequate for the needs of the IFI,

you are familiar with?

In your view what are the three key improvements that should be made to make the risk

management process better?

The following are the Global Top 10 risks as Identified in The Ernst & Young Business Risk

Report 2010 4(2009 rank in brackets), please rank the risks in your opinion as they apply to

Islamic Financial Institutions:

1. Regulation and compliance (2)

2. Access to credit/funding (1)

3 Slow recovery or double-dip recession (No change)

4. Managing talent (7)

5. Emerging markets (12)

6. Cost cutting (No change)

7. Non-traditional entrants (5)

8. Radical greening (4)

9. Social acceptance risk and corporate social responsibility (New)

10. Executing alliances and transactions (8)

b) Analytical synthesis of publicly available information regarding risk management in Annual

Reports of the following three Islamic Financial Institutions Meezan Bank (Pakistan), Al

Baraka Banking group (Bahrain but operating through out the Middle East and North

African region) and Khaleej Takaful - Insurance (Dubai) .

1.5 Limitations of the Research

The research is limited to the responses of members of Linkedin groups with interest in

Islamic Finance and to the publicly disclosed information in Annual Financial Statements of

the three selected Islamic Financial Institutions. Hence it will not be having information on

detailed risk management practices in the selected Institutions and in other Islamic Financial

Institutions. The opinion on the way forward will be limited to the views of the respondents

of the questioner.

4 The Ernst & Young Business Risk Report 2010

9

1.6 Scope of Dissertation

The scope of the dissertation will be to explore the risk management practices in Islamic

Financial Institutions, by reviewing the currently published literature and responses on Risk

Management practices and propose a way forward to improve these practices. This will be

structured in chapters as described below:-

Chapter 2 - Risk Management

This will Introduce Risk Management, exploring what risk management can achieve to enhance

value to a business. Then I will introduce the concept of risk and uncertainty. Thereafter the risk

management process/cycle. Finally the available tools and techniques used to mitigate, share or

transfer risk.

Chapter3 – Islamic Finance

This chapter will introduce the reader to the background and general principles governing

Islamic Finance. Then each section will look at the different general products of Islamic Finance

which includes Islamic Banking, Islamic Insurance – Takaful and Islamic Capital markets.

Chapter 4: Importance of Risk Management in Islamic Finance

This chapter will attempt to identify risks unique to the Islamic economic model, the threats

posed by risks peculiar to Islamic Finance, how to deal with these risks identified,

Islamic financial instruments which may be considered both to aggravate risk and to

mitigate risk depending on the context.

Chapter 5: Analysis of Risk Management disclosures in Financial Statements

This chapter will present the analysis of the risk management disclosures in the financial

statements of Meezan Bank based in Pakistan, Khaleej Takaful an Islamic insurance company

based in Dubai, United Arab Emirates and Al Baraka banking group headquartered in Manama,

Bahrain but having a pan Arab base operating through various subsidiaries in Middle East and

North Africa region.

10

Chapter 6: Analysis of responses from Linkedin questioner

This chapter will analyse the responses from the Questioner for members of Groups on Islamic

Finance on Linkedin and CIMA Islamic Finance forum on their perception of Risk Management

in Islamic Finance Institutions and the Questioner for people working in Islamic Financial

institutions and are members of groups in Linkedin and CIMA Islamic Finance Forum. I shall

then endeavour to synthesis the findings of the analysis and suggest on the way forward to

improve practice of risk management in Islamic Financial Institutions.

Chapter 7: Conclusions and Recommendations for Further Work

This chapter will present a summary of the dissertation, its findings and draw conclusions. It

will also attempt to suggest the way forward to improve risk management practises in Islamic

Financial Institutions. Lastly it will make recommendation for further work in this area

especially the interplay between corporate governance and risk management in Islamic

Financial Institutions.

11

Chapter 2: Risk Management

2.1 Introduction

This chapter will give a background to risk management and its development as a discipline.

Thereafter it will look at the relationship between risk and uncertainty, from which the

dissertation will discuss the risk management process, finally it will discuss the tools and

techniques used. Risk Management has numerous definitions usually based on the context in

which it is being discussed among these are:

“Risk management is formal process that enables the identification, assessment, planning and

management of risk.” 5(Merna and Al Thani 2010)

COSO ERM defines enterprise risk management as a process designed to identify potential

events that may effect the entity, and manage risk to be within its risk appetite, to provide

reasonable assurance regarding the achievement of entity objectives. The process is effected by

an entity‟s board of directors, management and other personnel, applied in strategy setting and

across the enterprise. 6

ASNZ 4360 states that risk management is an integral part of good business practice and quality

management. The standard further specifies that risk management means inter alia identifying

and taking opportunities to improve performance as well as taking action to avoid or reduce the

chances of something going wrong.7

The Institute of Risk Management in its risk management standard says Risk can be defined as

the combination of the probability of an event and its consequences (ISO/IEC Guide 73). In all

types of undertaking, there is potential for events and consequences that constitute opportunities

for benefit (upside) or threats to success (downside). Risk Management is increasingly

recognised as being concerned with both positive and negative aspects of risk. Therefore this

standard considers risk from both perspectives.8

The common theme arising from the various definitions are that risk management is a

management process to deal with uncertainties faced by any entity, threats to its resources and

its consequences, as it chooses the opportunities presented by its operating environment, to

increase the value of the entity.

5 Corporate Risk Management 2

nd edition Tony Merna and Faisal F Al Thani

6 COSO ERM

7 ASNZ 4360

8 A Risk Management Standard - http://www.theirm.org/publications/documents/ARMS_2002_IRM.pdf

(Assessed 26 February 2011)

12

2.2 Risks faced by an Islamic Financial institution

Common risks faced by an Islamic Financial Institution are shown in Figure 2.1 (author‟s own)

below:

Price risk is the context of an Islamic Financial Institution is that the value of the underlying

commodity or asset which forms the basis of the contract between the Islamic financial

institution and the financed party will vary from the original price. The exchange rate risk arises

when the rate of exchange fluctuates for its funding and also financing transaction.

Credit risk is the uncertainty of the financed party being unable to meet its obligations to the

Islamic Financial Institution as and when they fall due. This is a speculative risk undertaken

with an objective of a gain, with the possibility of a loss.

Profit rate risk is the risk that the profit generated from partnership contracts will not be as

envisaged or the profit rate indicated to the institutions investment account holders will not be

sufficient or balanced. Furthermore, some investment account holders benchmark this profit rate

with interest rates offer by conventional banks, and can move their funds to conventional

financial institutions.

Liquidity risk arises due to two main reasons, firstly the inherent mismatch been the term of the

source of funds (deposits which are mainly short-term) and the destination of the funds (project

funding which are mainly long-term) and secondly the risk that the funds raised by the Islamic

Financial Institution from the Capital markets in form of Sukuk‟s and expected to be repaid and

at that point in time there is no appetite from buyers to purchase the new issue.

Pure risks are risks for which there is potential for only a downside and is best exemplified by

damage to owned assets or property and legal liability due to being sued by third parties like

customers and employees among others.

Risks faced by IFI’s

Price Risk Credit Risk Pure Risks

Liquidity Risk

Commodity or

Asset Price Risk

Exchange

Rate Risk Damage to assets Legal Liability

Profit Rate Risk

13

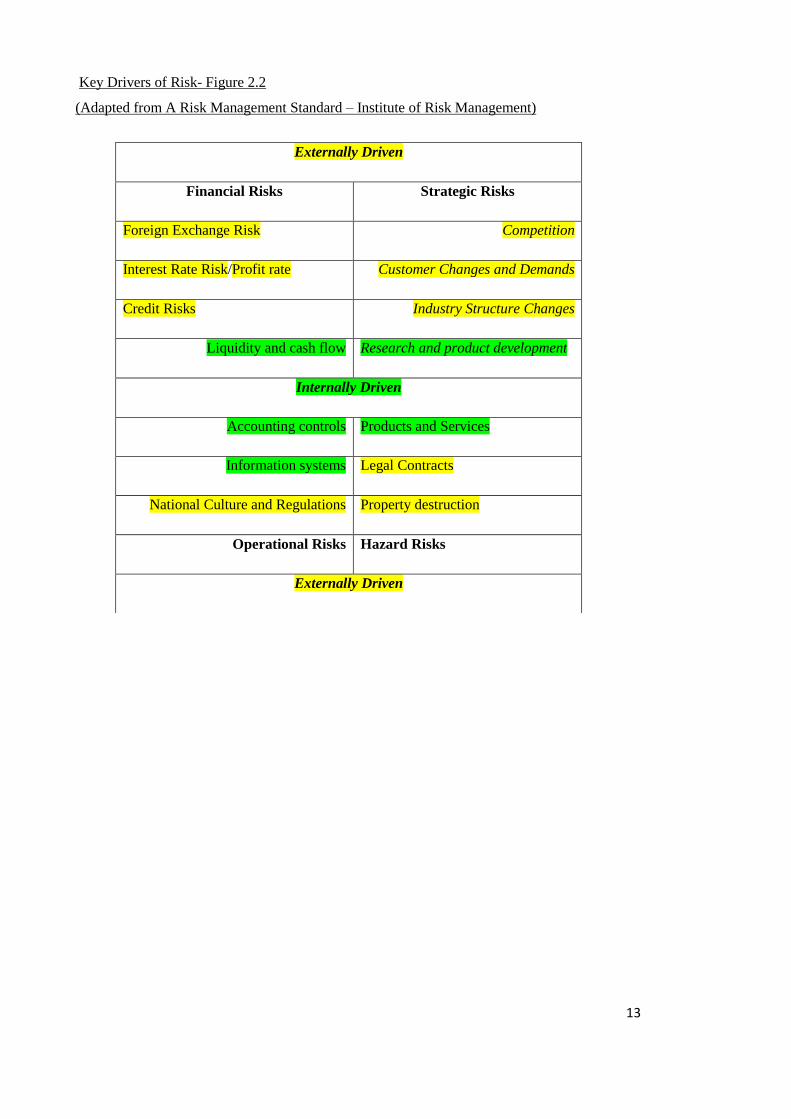

Key Drivers of Risk- Figure 2.2

(Adapted from A Risk Management Standard – Institute of Risk Management)

Externally Driven

Financial Risks Strategic Risks

Foreign Exchange Risk Competition

Interest Rate Risk/Profit rate Customer Changes and Demands

Credit Risks Industry Structure Changes

Liquidity and cash flow Research and product development

Internally Driven

Accounting controls Products and Services

Information systems Legal Contracts

National Culture and Regulations Property destruction

Operational Risks Hazard Risks

Externally Driven

Internally Driven

Externally Driven

14

2.3 The Concept of Risk and Uncertainty

Risk is simply defined as a probability of a loss or gain. One situation is riskier than another if it

has a greater expected loss or a greater uncertainty (defined as the variability around the

expected loss).9 Therefore risk is linked to the quantum of loss or profit (risk reward ratio) i.e.

the probability of an event occurring causing either a gain or loss and how much the gain/loss

varies from the expected outcome which is an average.

Business inevitable has to undertake risk in its daily activities as perfect information is a myth.

Risk is usually thought of in respect of a negative event happening, the probability of it

happening and the quantum of the loss when it occurs. Uncertainty is said to exist in a business

transaction whereby the decision-makers lack complete knowledge, information or

understanding of the proposed transaction and its possible consequences.

In his seminal work Risk, Uncertainty, and Profit, Frank Knight (1921) established the

distinction between risk and uncertainty.10

“Uncertainty must be taken in a sense radically

distinct from the familiar notion of Risk, from which it has never been properly separated. The

term "risk," as loosely used in everyday speech and in economic discussion, really covers two

things which, functionally at least, in their causal relations to the phenomena of economic

organization, are categorically different. The essential fact is that "risk" means in some cases a

quantity susceptible of measurement, while at other times it is something distinctly not of this

character; and there are far-reaching and crucial differences in the bearings of the phenomenon

depending on which of the two is really present and operating. ... It will appear that a

measurable uncertainty, or "risk" proper, as we shall use the term, is so far different from an

unmeasurable one that it is not in effect an uncertainty at all. We accordingly restrict the term

"uncertainty" to cases of the non-quantitive type.

9 Risk Management & Insurance 2

nd edition Harrington and Niehaus

10 http://en.wikipedia.org/wiki/Risk accessed on 26 February 2011

15

2.4 The Risk Management Process

Risk Management deals both with insurable as well as uninsurable risks and is an approach

which involves a formal orderly process for systematically identifying, analysing and

responding to risk events.1 (Merna & Al Thani 2010).

A diagrammatic representation of the Risk Management Process Figure 2.3 adapted from A

Risk Management Standard by the Institute of Risk Management4

Definitions

Risk Assessment: Is the overall process of risk analysis and risk evaluation.

Risk Reporting: Threats & Opportunities to Board of Director & affected Business Managers

Risk Treatment: Is the process of selecting and implementing measures to modify the risk.

Residual Risk Reporting: to its stakeholders on a regular basis setting out its risk management

policies and the effectiveness in achieving its objectives

Monitoring: This process provides assurance that there are appropriate controls in place for the

organisation‟s activities and that the procedures are understood and followed.

Organisation’s Strategic Objectives

Risk Assessment

Risk Analysis - Risk Identification - Risk Description - Risk Estimation

Risk Evaluation Risk Reporting: Threats and Opportunities

Th

Risk Treatment

Residual Risk Reporting

Monitoring

Modifications Formal Audit

16

There are two major dimensions of a loss exposure are the loss frequency and loss severity.

Loss frequency is measured by probability of the occurrence of an event based on past

experience. Loss severity is measured by maximum possible loss and expected loss. Hence

classification of risk in accordance with these two dimensions is the starting point in managing

risk. In the view of business it is sensible to focus on exposures to risks rather than the potential

upside. The key exposures to risk in any organisation are physical asset exposures, legal liability

exposures, human resource exposure and financial asset exposures.

2.5 Risk Management Tools and Techniques

There are two major categories of risk management tools and techniques used by risk

professionals to analyse risk namely Quantitative techniques and Qualitative techniques, which

are applied to the dimensions of loss exposures. Qualitative techniques seek to compare the

relative significance of risk faced by an enterprise in terms of the consequences to it.

Quantitative techniques and tools attempt to determine absolute value ranges, using statistical

tools like probability distributions to quantify probable outcome.

Qualitative Techniques for risk management include Brainstorming, Assumption Analysis,

Delphi, Interviews, Hazard and Operability Studies (HAZOP), Failure Modes and Effect

Criticality Analysis (FMECA), Checklist, Prompt list, Risk Registers, Risk Mapping,

Probability Impact Tables, Risk Matrix Chart, Project Risk Management Road Mapping.

Quantitative techniques for risk management include Decision Trees, Controlled Interval and

Memory Technique, Monte Carlo Simulation, Sensitivity Analysis and Probability-Impact Grid

Analysis.

Other techniques include Soft Systems Methodology, Utility Theory, Risk attitude and Utility

Theory, Nominal Group Technique, Stress Testing and Deterministic Analysis, Tornado

Diagram, Country Risk Analysis and Political Risk Analysis.

Risk Control techniques include Risk Avoidance by not undertaking the activity which can lead

to a loss, Loss Control which include Loss prevention (reducing the frequency of losses) and

Loss reduction (reducing the severity of losses), Risk Separation this reduces the probability

that several losses will at the same time , Risk Combination/pooling increases the predictability

of losses through the law of large numbers and Risk Transfer which can include transferring the

cause of the risk, transferring the risk itself, transferring the cause of the risk and transferring the

consequence of the risk through insurance.

17

Contracts can be used to mitigate or transfer risk like insurance contracts for hazard (pure risks

like theft, fire etc), derivative contracts (options, forwards, futures and swaps) to mitigate

against financial risks like commodity prices, foreign exchange risks, interest rate risks and

contracts where risk is transferred to the counterparty through legal clauses.

The choice of the technique whether to assess the risk or alter the risk depends on the context of

the situation, availability and the resources including time and money to the organisation.

Hence, there is no one set of techniques to ensure universal applicability.

2.6 Summary

Risk management should be embedded within the organisation through the strategy and budget

processes. It should be highlighted in induction and all other training and development as well

as within operational processes e.g. product/service development projects. The Board has the

overall responsibility for determining the strategic direction of the organisation and for creating

the environment and the structures for risk management to operate effectively. There should be

a risk champion on the board to ensure the board is aware of the risks under taken by the entity

and decide whether these are acceptable. Business unit managers s have primary responsibility

for managing risk on a day to-day basis, hence risk management should be a regular

management-meeting item to allow consideration of exposures and to reprioritise work in the

light of effective risk analysis. The same awareness of risk issues is also required for those

involved in the audit and review of internal controls and facilitating the risk management

process and includes both the internal audit function and external auditors.

18

Chapter 3: Islamic Finance

3.1 Introduction

Islamic finance constitutes the fastest growing segment of the financial system in the world.

Modern Islamic banking started about three decades ago, the number and reach of Islamic

financial institutions worldwide has risen from one institution in one country in 1975 to over

300 institutions operating in more than 75 countries (El Qorchi, 2005)11

. In Sudan and Iran, the

entire banking system is currently based on Islamic finance principles. However the roots of the

Islamic Banking system goes back back through time to the profit and loss sharing principles in

the Code of Hammurabi in the 18th century BCE. Over the centuries, philosophers and

theologians alike have debated the issues surrounding justness of exchange and the charging of

interest. Charging of interest is long seen as damaging to individuals as well as the economy by

the majority of theologians and philosophers. Even the Christian Holy Bible and Jewish Holy

Torah forbid Usury. This chapter will explore the general principle of Islamic Finance, briefly

going into the sources of Islamic Law without going into the details of the various schools of

thought which are contentious issues even among Islamic scholars depending on whether they

are Sunni or Shia, region from which they come from (scholars from some regions are more

liberal than others). There are Islamic Scholars who have approved derivative s contracts

(forward, swaps and options), while other scholars consider these as unlawful. An example

would be HH Prince Karim Aga Khan IV Imam to Nizari Ismaili Shia Muslims, direct lineal

male descendant of the Prophet Mohamed (PBUH) and widely respected in the Muslim

community worldwide has a different opinion on the interest which is not usury therefore not

“Riba” which is prohibited in the Quran, hence he has significant interests in conventional

banking institutions both in the developed and developing world, which is significantly altering

the economic lives of people living in those countries. In the other end of the Shia spectrum lies

the Mustali Ismaili Shia Muslims, in whose view even instalment sale contracts where the

current cash price and instalment sale price differ is considered unlawful and profit loss sharing

without the investor being actively involved in the business is prohibited, This based on the

principle, all earnings have to be from the individuals sweat, law of one price and avoidance of

excessive profit. Then it will give a bird‟s eye view of Islamic Banking, which is a banking

system that is based on the principles of Islamic law and guided by Islamic economics. Two

basic principles behind Islamic banking are the sharing of profit and loss and, significantly, the

prohibition of the collection and payment of interest. Collecting interest is not permitted under

Islamic law.

11 IMF Working Paper WP/08/16 Islamic Banks and Financial Stability: An Empirical Analysis

Prepared by Martin Čihák and Heiko Hesse

19

Thereafter, we shall take a peek into the world of Islamic insurance – Takaful, which is based

on risk pooling and sharing rather than risk transfer. Takaful is where members contribute

money into a pooling system in order to guarantee each other against loss or damage. Takaful is

based on Islamic religious law, and is based on the responsibility of individuals to cooperate and

protect each other. Lastly, it will explore Islamic Capital Markets products the most well know

is the Islamic bond called a Sukuk. Since interest is prohibited Sukuks must be able to link

the returns and cash flows of the financing to the assets purchased, or the returns generated from

an asset purchased. This is because trading in debt is prohibited under Sharia. As

such, financing must only be raised for identifiable assets. It can be compared to a sale,

lease/rent and buy back transaction in conventional finance.

3.2 Islamic Finance general principles

The guiding principles of Islamic Finance are based on Islamic Law (Sharia) as documented in

the Holy Quran and promulgated in the Sunnah (Hadith - sayings and living habits/acts of

Prophet Mohamed (PBUH), which are universally accepted by all Muslims. Different schools

of jurisprudence both Sunni and Shia place different level of emphasis on secondary sources

like Ijma (consensus of Scholars), Ijtihad (independent legal reasoning), Qiyas (analogical

deduction), Aql (use intellect to find general principles applicable in the situation from the Holy

Quran and Sunnah ), saying and acts of Shia Imams who are descendents of Prophet Mohamed

–PBUH according to Shia beliefs they are responsible for guiding the Muslims ummah and

interpreting the Holy Quran according to the changing time and space, Urf (common practices

of a given society not addressed in the Holy Quran and Sunnah) and Al-Maslaha Al-Mursalah

(Maliki Sunni) "underlying meaning of the revealed text in the light of public interest". 12

Islamic Finance is based on the prohibition of interest ("Riba"), excessive uncertainty

("Gharar") and gambling ("Maysir" or "Qimar"). Being Sharia compliant also means that the

funding should not be for the purposes of haram (prohibited activities) like pornography,

building a brewery or casino or a pork farm etc. Judaism and Christianity also prohibit usury

(interest) in their religious texts the Torah and Bible respectively. Holy Quran commands honest

fulfilment of all contracts (al-Maidah: 1); prohibits the betrayal of any trust (al-anfal: 27);

forbids the earning of income from cheating, price manipulation, dishonesty or fraud (an-nisa‟a:

29); shuns the use of bribery to derive undue advantage (al-baqarah: 188); and promotes clarity

in contracts to minimise manipulation from dubious ambiguity (al-baqarah: 282)

12

http://en.wikipedia.org/wiki/Sources_of_Islamic_law (accessed 14th March 2011)

20

3.3 Islamic Banking

The roots of Islamic banking goes to the time of the establishment of the Islamic Arab empire -

the Caliphate which conquered vast areas in Middle Central Asia, North Africa and parts of

Europe in the 7th Century, where systems of payments and finance were required which

included Qardan Hasannah (interest free loan), Hawallah (promissory notes/ bills of exchange),

a currency (Dinar), Waqf (trusts), to facilitate trade and mercantilism and pay the employees of

the Islamic state. However, this dissertation shall focus on modern Islamic banking, which is

based on the following concepts - Definitions adapted from FAS 1 issued by AAOIFI13

:-

Mudarabha - A partnership in profit between capital and labour. It may be conducted

between investment account holders as providers of funds and the Islamic bank as a

mudarib. The Islamic bank announces its willingness to accept the funds of investment

amount holders, the sharing of profits being as agreed between the two parties, and the

losses being borne by the provider of funds except if they were due to misconduct,

negligence or violation of the conditions agreed upon by the Islamic bank. In the latter

cases, such losses would be borne by the Islamic bank. A Mudarabha contract may also

be concluded between the Islamic bank, as a provider of funds, on behalf of itself or on

behalf of investment account holders, and business owners and craftsmen.

Salam : - Purchase of a commodity for deferred delivery in exchange for immediate payment

according to specified conditions or sale of a commodity for deferred delivery in exchange for

immediate payment.

Murabaha : - Sale of goods with an agreed upon profit mark up on the cost. Murabaha sale is

of two types. In the first type, the Islamic bank purchases the goods and makes it available for

sale without any prior promise from a customer to purchase it. In the second type, the Islamic

bank purchases the goods ordered by a customer from a third party and then sells these goods to

the same customer. In the latter case, the Islamic bank purchases the goods only after a customer

has made a promise to purchase them from the bank.

Musharaka : - A form of partnership between the Islamic bank and its clients whereby each

party contributes to the capital of partnership in equal or varying degrees to establish a new

project or share in an existing one, and whereby each of the parties becomes an owner of the

capital on a permanent or declining basis and shall have his due share of profits. However,

13 Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI)

http://www.aaoifi.com/aaoifi/Definitions/tabid/209/language/en-US/Default.aspx (accessed 14 March 2011)

21

losses are shared in proportion to the contributed capital. It is not permissible to stipulate

otherwise.

Istisna’a : - A contract whereby the purchaser asks the seller to manufacture a specifically

defined product using the seller‟s raw materials at a given price. The contractual agreement of

Istisna‟ has characteristic similar to that of Salam in that it provides for the sale of a product not

available at the time of sale. It also has a characteristic similar to the ordinary sale in that the

price may be paid on credit; however, unlike Salam, the price in the Istisna‟ contract is not paid

when the deal is concluded.

Ijarah and Ijarah Wa Iktana:- A lease agreement (similar to a hire purchase agreement)

whereby instead of lending money and earning interest, the Islamic bank purchases the asset and

rents it to the party requiring the asset and earns rental income. In ijarah wa iktana the renter

agrees to buy the asset at a nominal price at the end of the contract, in ijarah there is no such

agreement to purchase the asset.

3.4 Islamic Insurance – Takaful

Takaful is an Arabic word meaning guaranteeing each other. An Islamic insurance

(Takaful) industry observing the rules and regulations of Islamic Sharia law has

developed in recent years, which in common with Islamic banking avoids interest,

excessive uncertainty and gambling. However this concept has been practiced in various

forms for over 1400 years based on shared responsibility in the system of aquila as

practiced between Muslims of Mecca and Medina, which laid the foundation of mutual

assistance insurance – Takaful based on risk pooling and sharing today. Although some

Muslim scholars consider any form of insurance to be against the concept that Muslims

believe in God, who is the provider and sustainer of all and is based on the following

verse from the Holy Quran “Who, when a misfortune overtakes them, say: 'Surely we

belong to Allah and to Him shall we return'.". (Sura Al-Baqara, Verse 156)

Takaful is based on the concept of social solidarity, cooperation and mutual

indemnification of losses of members. It is a pact among a group of persons who agree

to jointly indemnify the loss or damage that may inflict upon any of them, out of the

fund they donate collectively. The Takaful contract so agreed usually involves the

concepts of Mudarabah (partnership in profit), Tabarru´ (to donate for benefit of others)

and Ta-Awun (mutual assistance or sharing of losses) with the overall objective of

22

eliminating the element of uncertainty. Even though all Muslims believe in the will of

Allah who is the owner of everything and we are merely his stewards, the steward had a

duty to protect the assets given to him in trust by the owner, hence justification for a

Sharia compliant Islamic alternative Takaful to conventional insurance. This view point

for Takaful is justified based on the following Islamic jurisprudence sources14

.

Basis of Co-operation Help one another in al-Birr and in al-Taqwa (virtue, righteousness and

piety): but do not help one another in sin and transgression. (Holy Quran Surah Al-Maidah,

Verse 2) and Allah will always help His servant for as long as he helps others. (Hadith Narrated

by Imam Ahmad bin Hanbal and Imam Abu Daud)

Basis of Responsibility The place of relationships and feelings of people with faith, between

each other, is just like the body; when one of its parts is afflicted with pain, then the rest of the

body will be affected. (Narrated by Imam al-Bukhari and Imam Muslim)

One true Muslim (Mu‟min) and another true Muslim (Mu‟min) is just like a building whereby

every part in it strengthens the other part. (Narrated by Imam al-Bukhari and Imam Muslim)

Basis of Mutual Protection: - By my life, which is in Allah‟s Power, nobody will enter Paradise

if he does not protect his neighbor who is in distress. (Narrated by Imam Ahmad bin Hanbal)

Key Elements of Takaful

Mutual Guarantee: Loss covered by donations of members in fund which pays out losses.

Ownership of Fund: Contributors are owners of fund, hence entitled to the profit.

Elimination of uncertainty: Donations are voluntary and no pre-determined benefits.

Management of Takaful Fund: Operator uses either Mudaraba (Partnership) or Wakala

(Principal Agent relationship ) contract to manage funds, which are Sharia compliant.

Investments Conditions: Avoids interest and haram (prohibited) activities for investment.

14

http://en.wikipedia.org/wiki/Takaful (accessed on 14 March 2011)

23

3.5 Islamic capital markets

There are two major components of Islamic capital markets namely Sukuk‟s (Sharia compliant

bonds) and Islamic investment funds. Using the double entry sheet terminology the Sukuk sits

on the credit side of the balance sheet hence is a liability, while Islamic investment funds sit on

the debit side of the balance sheet hence an asset. Both the capital market instruments are

market traded on organised stock exchanges, with some restrictions on the tradability of debt

instruments.

Sukuk is the Arabic word for financial certificate, commonly analogous to a bond (promise to

pay) in conventional finance. It is asset based rather than asset backed to comply with sharia

requirements. The beauty of the Sukuk lies in asset securitisation, whereby future cash flows

emanating from an asset are converted into present cash flow. A sukuk can be created on an

existing asset and also on a future asset which is being created. The sukuk can be structured as

Sukuk Murabaha which constitutes partial ownership in a debt, Sukuk Al Ijara which is asset

backed, Sukuk Al Istisna which is project backed, Sukuk Al Musharaka which is business

backed or Sukuk Al Istithmar which is an investment. From a strict sharia perspective debt

certificates are not tradable at a price other than at par or face value, as any money generated

from holding money is considered interest which is prohibited, hence most sukuk instruments

are held to maturity. Therefore the secondary market although in exists but has limited trades.

An Islamic investment fund is a Sharia compliant fund which invests in halal activites, avoids

excessive uncertainty, avoid interest and is not overly speculative (gamble). These can be

structured as a mutual fund, a hedge fund or electronic traded fund (ETF).

The common types of investments funds are commodity funds, equity funds, murabaha

funds and Ijara funds.

Commodities funds generate profits by buying and reselling commodities. Due to the

restrictions on the use of derivatives, commodities fund make use of two types of contracts:

1. Istina‟a- It‟s a contract where the buyer of an item funds upfront the production of the

item. A detailed specification of the item as to be agreed before production starts and

the cost of production has to be paid in full when the contract is agreed.

2. Bay al-salam which is similar to a forward contract where the buyer pays in advance for

the delivery of raw materials or tangible goods at a later date.

Equity funds invest in equity shares of companies engaged in halal business activities. These are

similar to ethical investing funds.

24

Murabaha funds are similar to development funds, and use the „cost-plus‟ financing model,

where a fund will buy goods and sell them to a third party at a given price. The price is made of

the cost of goods plus a profit margin.

Ijara Funds acquire and keep ownership of an asset (real estate, machinery, vehicles or

equipment) and then makes profits by leasing it out in return of a rental payment. The fund is

responsible for the management of the assets and will earns a management fee. This is similar to

Real Estate Investments Trusts (REITs) and Energy Royalty Trusts (common in Canada).

3.6 Differences between Islamic Finance and Conventional Finance instruments

Sukuk and Bonds

Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI) defines a

sukuk as being: “Certificates of equal value representing after closing subscription, receipt of

the value of the certificates and putting it to use as planned, common title to shares and rights in

tangible assets, usufructs and services, or equity of a given project or equity of a special

investment activity”. Hence, it is a mezzanine financial instrument that is neither debt nor

equity, created by a process of securitization of cash flow and ownership of an asset or project.

The sukuk holder shares in the cash flow generated by the asset and the disposition proceed of

the assets. A bond on the other hand is a contractually obligation to pay to bondholders, on

certain specified dates, interest and principal.

Takaful and Insurance

Takaful is based on the principles on mutual assistance and voluntary contribution in a pool of

funds to be shared among those in the group afflicted by perils or calamities, without guarantees

that the fund will be adequate of expectation that the operator will earn a profit. In conventional

insurance the insurer collects premium from the insured to cover expected payout and profit,

this is akin to speculation (Maysir) which is forbidden in Islamic Finance. The insurer pays

premiums to be covered for risks that may or may not materialize, this is uncertainty (Gharar),

which is also forbidden in Islamic Finance. Lastly, the premiums collected are invested to earn

interest (usury) which is forbidden in Islamic Finance.

3.7 Summary

The basic principles underlying the Islamic Finance concept are very similar to ethical

investing, co-operative arrangements, and mutual principles, very closely aligned to

conventional financial products but avoiding interest, excessive uncertainty and speculation.

25

Chapter 4: Importance of Risk Management in Islamic Finance

4.1 Introduction

Product complexity in Islamic Finance has increased as there is a trend to develop an Islamic

variant for most products in non-Islamic finance, but the pace in risk management practices has

not developed at the same rate. This has been attributed (Ahsan Ali, December 2009)15

to the

following:-

Lack of Standardised product descriptions and attributes within Islamic Finance.

Lack of understanding of Islamic structures and therefore, weak regulatory frameworks

within countries to manage Islamic Financial Institutions (IFIs).

Limited data on Islamic transaction and low technological adaptability for technology-based

risk management models.

Concentration of Islamic Finance institutions in emerging markets, where the risk

management techniques for both conventional and Islamic modes of financing lag the

developed markets.

Due to the above reasons it is (Ahsan Ali, 2009)15

postulated that Islamic Financial Institutions

are inherently riskier propositions than their conventional counterparts.

The above arguments can be countered by the following:-

Standardisation of product descriptions, Islamic Finance Structures and accounting

attributes are taking places through the efforts of Accounting and Auditing Organization for

Islamic Financial Institutions (AAOIFI) and Islamic Financial Services Board (IFSB).

However, having two bodies with similar objectives and membership of which is voluntary

by Islamic Financial Institutions creates confusion in the perception of the general public.

Furthermore, there is weak enforcement capability as these organizations do not have

credible sanctions mechanisms, to enforce application of standards set.

Islamic Finance is no longer confined to the developing world as London and New York are

becoming major centers for Islamic Capital Market products, hence risk management

techniques are improving and technological developments will catch up.

The data availability is increasing especially in Malaysia and Gulf markets, with

publications like Business Islamica, Gulf news quarterly and Global Islamic Finance.

15

Risk Management Integral to the Future of Islamic Finance – Article in Business Islamica December

2009

26

Risk management in Islamic Finance is driven by the principles of Islamic economics which are

derived from the Holy Quran and Sunnah of Prophet Mohamed (PBUH). Hence it is prone to

the usual risks faced by all financial institutions plus risks which affect primarily Islamic

Financial Institutions. The importance of the concept of risk management in Islamic Finance is

emphasised by the following verse in the Holy Quran and Saying of Prophet Mohamed (PBUH)

Further he said: "O my sons! Do not enter the capital of Egypt by one gate: but go into it by

different gates. However know it well that I cannot ward off you Allah‟s will for none other

than He has nay authority whatsoever. On Him do I put my trust and all who want to rely upon

anyone should put their trust on Him alone." (Surah Yusuf: Verse 67)

Prophet Muhammad noticed a Bedouin leaving his camel without tying it and he asked the

Bedouin “Why didn‟t you tie down your camel?” The Bedouin answered, “I put my trust in

God.” Muhammad replied, “Tie your camel and put your trust in God.”

In this chapter the author shall identify risks faced by Islamic Financial Institutions, look at risk

affected due to its economic model or how normal business risks uniquely affect them. Then the

author shall look at threats posed by these risks and consequently how those risks can be dealt

with. Finally it shall discuss Islamic Financial Instruments which are used in Islamic Finance

which mitigate certain risks but create a different type of risk for an IFI.

4.2 Identification of risks in the Islamic Finance economic model

Credit Risk

This is the risk whereby the borrower defaults on the loan. In the Islamic Financial Institution‟s

(IFI‟s) context this means the counter party defaults on its contractual obligation and the IFI has

to foreclose on the underlying asset, this becomes particularly challenging in the instance of

residential real estate instalment sale transaction, which would conflict with its responsibility to

society. It is important to note that IFI‟s generally have greater exposure to real estate than

conventional banks, where the bank becomes owner of the asset which according to IFRS this

needs to be incorporated on its balance sheet, which creates additional volatility in its reported

earnings. Furthermore greater focus on asset financing through Ijara (leasing) and Murabaha

(sale with profit mark-up), may cause a tendency to overlook credit worthiness and ability to

repay of the counterparty.

Market Risk

Hedging using conventional derivatives is restricted, as some scholars consider it to be Maysir

(gambling) which is prohibited, hence the possibility of a higher than normal margin risk

27

especially in fixed margin Murabaha (sale with profit mark up) i.e. mismatch between what is

earned on the assets and what is paid out on its investment accounts. These restriction leads to

artificial inflation of values of investment opportunities as too much capital is chasing too few

assets. Furthermore, IFI‟s run a higher foreign exchange risk on their balance sheets particularly

translation risk for banks with operation in multiple countries, which have to be consolidated as

per IFRS requirements, due to limited opportunities to hedge.

Operational Risk

IFI‟s have to ensure correct processing and sequential documentation for most of its

transactions, as any error invalidates the entire transactions and profit has to be donated.

Liquidity Risk

This is higher in IFI‟s as the secondary market for Islamic Capital market instruments is

underdeveloped, due to prohibition in sale of debt at a price other than at par. Thus most Islamic

Capital market instruments are held to maturity, which restricts the ability to realise cash when

required repay investment account holders, hence a minor run on an IFI can have a major effect

on its solvency, as it cannot access its central bank as lender of last resort.

Reputational Risk

This is higher in IFI‟s due to the risk of Sharia compliance requirements, while Sharia decrees

and decisions are not standardised or follow the principles of judicial precedence as in English

common law. Sharia boards are made up of scholars, who sometimes disagree on products lines

like Tawaruk (Shariah-compliant of finance through which loan finance is raised by buying

installments in local commodities that are owned by the bank) which is acceptable to certain

scholars and prohibited by others. The Sharia board of an IFI can be changed to get scholars

who are compliant to the wishes of the IFI‟s owners, hence they could be accused of “scholar

shopping or fatwa shopping” which has the potential to damage its reputation in the eyes of

Investment Account holders. This happened in Dubai during the recent global financial crises

when some real estate developers wished to change the underlying assets of instruments in a

process of consolidation of projects, which were considered unacceptable to certain scholars.

Furthermore, fatwa‟s issued by prominent scholars not on the IFI‟s Sharia board also tend to

influence behaviour of market participants.

28

Classical Islamic Law 16

classified risk in into three categories as follows:-

1. Essential risk and al-kharāj bi-dhaman, which can be roughly translated as „the profit belongs to

him who bears responsibility‟. This maxim encapsulates the concept of risk for return (al ghunm

bil ghurm). Parties who enter into an agreement are entitled to its benefit as long as there is

some form of associated risk. Without the risk, the transaction would not be shari‟a compliant.

Any condition to the contrary would make the transaction void, such as anything contrary to the

rule on a total or partial loss or decrease in value of an asset is on account of its owner). If one

requires a return of some form, then one should be able to take on the associated level of risk. In

an Islamic sales contract, the seller bears all the risks of loss of the asset until title is transferred

to the buyer who then in turn takes on the full risks, including risks of defect, damage or

depreciation arising thereafter. In an Islamic leasing arrangement, the lessor assumes all risks of

loss (not caused by the lessee) and the risks of maintenance and payments of taxes. Whereas the

lessee assumes the risks of rental payment, of any loss of profit and of under-utilisation

associated with the rental of the asset. In a mudaraba arrangement, the risk of loss, damage or

decrease in value of the mudaraba assets and capital is borne by the investor (rab al mal) as long

as there is no default, misconduct or breach by the investment manager (mudarib).

2. Gharar Katheer, which can be roughly translated as „excessive/gross uncertainty or speculation‟.

Muslims are strictly prohibited from entering into this second category of risks as such risks

make a transaction or a contract void from a shari‟a perspective. Whereas in conventional

finance, this is a form of tradable risk which can be separated and sold on, or, which can be

mitigated against. This form of risk is also known as gharar jaseem and it can be further

classified into the following sub-types of prohibited risks:

a. Risk in Existence (i.e., the sale of an non-existent item, such as crops, on a future basis);

b. Risk in taking Possession (i.e., the sale of a run-away camel or commodity / property that

has to be repossessed);

c. Risk in Quantity (i.e., sale price or rent being unknown in a sale or lease contract);

d. Risk in Quality (i.e., type, quantity or specifications of the subject matter of contract being

unknown); and

e. Risk in Time of Payment (i.e., a deferred sale without fixing the exact period).

16 Islamic Finance project Harvard Law School, Islamic Legal Studies Program, Harvard-LSE Workshop London

School of Economics 26 February 2009 Workshop on Risk Management: Islamic Economic and Islamic EthicoLegal

Perspectives on the Current Financial Crisis – A short Report Prepared by Husam El-Khatib Introduction by Zohaib

Patel.

29

Involvement of any of the above types of risks make contracts of consideration or exchange

(aqood al muawadat) void with the unanimous opinion of the jurists. In contracts of gifts or

donations (aqood al tabarro‟at), the majority of jurists are of the opinion that these risks make

such forms of contracts void, with the exception of Maliki jurists who view risks in contracts of

gifts are permissible. From this Maliki opinion, contemporary jurists have derived that takaful is

permitted despite containing Risks in Existence, Possession, Quantity and Period.

These risks are deemed excessive and gross in nature as they fall into the categories of gambling

and speculation, being some of the causes for the current global financial crisis. Short sales for

instance are prohibited on the basis they fall foul of the rule on Risk of Possession; they involve

the sale of something (i.e., shares) which are not owned by the seller at the time of the initial

sale. Also, the sale and trading of debt falls foul of the above prohibited categories of risks as

such activities carry with them additional („gross‟) levels of risks, such as the possibility of non-

payment of the debt by the actual debtor.

An important corollary to the prohibition on excessive risk is that shari‟a does not permit a party

to intentionally take on such forms of excessive risks and then to hedge against those same risks

with the help of some form of hedging or risk management tool, irrespective of whether the

actual hedging/risk management tool is shari‟a compliant in itself or not.

3. The third category can be described as a level in between the former two. This can include a

variety of forms of risk, including market risk and operational risk. This is not a risk that is

part of a financing tool‟s inherent structure per se. Therefore, this type of risk can be

mitigated against or avoided.

4.3 Threats posed by risks peculiar to Islamic finance

Insolvency

The threat of insolvency is higher than average due by lack of liquidity in Islamic asset

instruments and securities due to an under developed secondary markets and lack of access to

central bank as lender of last resort in case of a run by investment account holders on the

Islamic Financial Institution. This happens because of the mismatch of maturity term between

Investment account deposits and the longer term financing arrangements. Also most

instruments are held to maturity due to prohibition on sale of debt other than at par, so when

there is a short-term liquidity crunch its effects are more severe unless its owners have funds

elsewhere to provide liquidity, which the usual response is to withdraw from other markets

causing a domino effect.

30

Reputational Damage to the Islamic Finance Brand/Segment

Due to the fragmented nature of Sharia decisions and decrees, which are developed

independently by scholars in different markets, without having judicial precedence

requirements, with some scholars from different schools of thought being more liberal than

other, widespread acceptance is difficult, especially for controversial issues. This prevents an

orderly development of standards of product development and financial reporting. A point to

note is that IFI‟s are required to confirm to the financial reporting framework of its country of

operation. A general fatwa by prominent scholar not on a particular IFI‟s Sharia board can

cause loss of credibility and confidence by the consumers if he makes a compelling argument in

public about a particular transaction or product developed and IFI and approved by its Sharia

board. This is a controversial issue for Islamic Credit card issuers (fixed fee based) and process

on changing underlying security for a sukuk or project funding transaction in the event of real

estate project consolidation on the crash in real estate market. This is compounded by lack of a

universally accepted body for determining mandatory product standards and financial reporting,

plus membership of AAOIF and IFSB is voluntary. In short the risk borne by an IFI is product

is approved by its Sharia board, but vocally disapproved by a leading scholar, causing a

reputational disaster in the perception of the public, aggravated if the scholar was a dissenting

former member of the Sharia advisory board.

Greater potential for volatility of reported earnings

IFI‟s financial statements if prepared and compliant with International Financial Reporting

Standards (IFRS) have to report financial instruments and assets using “mark to market”

principles, due to the requirement of ownership of assets which have to be reported on the

balance sheet and movement in value passing through the income statement, caused profits to

fluctuate more than conventional financial institutions. This aggravates during economic

downturn, as not only are the financial instruments subject to downward valuation, also losses

on assets which will eventually be sold to counterparties.

Operational Risk - Contracts

Islamic Finance transactions are subject to multiple contracts to make them compliant with

Sharia rules, the threat of misclassification of a transaction can lead to a requirement for

different type of contract which if missed would negate the entire transaction i.e. making it non-

Sharia compliant. This is further compounded by lack suitable trained finance personnel in

Sharia Law and Sharia scholars suitably trained in finance to structure Islamic Financial

transactions appropriately.

31

4.4 How to deal with the risks identified

Insolvency

Insolvency caused by lack of liquidity in Islamic Financial Instruments and Sharia non-

compliance of short-term funding from lender of last resort (Central Bank) could be solved by

forming a supra-national body to bailout Islamic Financial Institution‟s funded by a voluntary

donation each year say 0.2% of the member institution‟s operating profits. This fund could also

be used to buy illiquid instruments from IFI‟s to finance short-term liquidity constraints, give

Qardan Hasanah (interest free good loan) to IFI‟s for their short –term liquidity needs, and

operated on a mutual assistance basis. It could also act as manager of last resort to protect

investment account holder‟s funds in case of eminent collapse of a member IFI. This measure

would have a positive impact on the credibility of the Islamic Finance market and improve its

reputation. Qardan Hassanah mentioned in The Holy Quran 'If you lend unto Allah Qardan

Hasanah , He will multiply it for you and He will forgive you, for Allah is the Most

Appreciative , Most Forbearing' (Verse 64-17)

Reputational Damage to the Islamic Finance Brand/Segment

A supra-national co-ordinating body (possibly formed by the merger of AAOIFI and IFSB with

unification of standards) which operates a global database of Islamic Financial products

approved by validly constituted Sharia advisory boards, irrespective of national, sectarian or

doctrinal bias, preferable based in a neutral International Financial Centre like London. This

body could also have a depository of experts on Islamic Law and Finance which could review

products developed which have been challenged by other scholars and considered acceptable by

others by giving an independent opinion (a form of judicial review). Financial reporting for

IFI‟s could benefit if the industry would petition the International Accounting Standards Board

(IASB) to consider issuing an International Financial Reporting Standard (IFRS) for IFI‟s.

Operational Risk – Contracts

This risk can be dealt with by having well reputed scholars on Sharia boards with persons with

knowledge of both Islamic Law and Financial knowledge and belonging to multiple schools of

thought or Islamic jurisprudence, to enable a diversified meaningful debate, when considering

Islamic Products. Furthermore more personnel working within IFI should be encouraged to be

certified by globally reputed Institutions like the Chartered Institute of Management

Accountant‟s17

Certificate in Islamic Finance qualification.

17

http://www.cimaglobal.com/Study-with-us/Certificate-in-Islamic-Finance/

32

4.5 Islamic Financial Instruments/Transactions – Risk Mitigation and Risk Creation

Sukuk (Sharia compliant bond equivalents) and Ijara (lease or buy and rent contracts)

Islamic Financial Institutions that either issue or purchase Sukuk or enter into Ijara contracts are

investing in real assets. The return on these assets takes the form of rent, and is uniformly

spread over the rental period. The underlying asset provides additional security for the investor

and the productivity of the asset is the basis of the return on investment. The claim embodied in

Sukuk is not simply a claim to cash flow but an ownership claim. Hence, interest risk is

avoided and so is the risk of the fluctuation of the value of the borrowing (as selling of debt at a

price other than at par is forbidden), which mitigates the financial risk of the entity. However

the ownership claim has to be reflected in the balance sheet of the IFI which results in volatility

of earnings and balance sheet values due to mark to market rules required for most financial

reporting frameworks. Furthermore, the prohibition of the sale of debt other than at par,

prevents the development of the secondary market in these securities, creating liquidity

constraints as these are not easily convertible to cash.

Musharaka and Mudaraba

Under these transactions the Islamic Financial Institution participates in the profit or loss of the

transaction, instead of receiving interest. These transactions even though compliant with Sharia

create above average credit risk, as a known amount of cash flow in form of interest is replaced

by an uncertain amount of profit or loss.

Derivatives Instruments in Islamic Finance

This is one area which has the most controversy in Islamic Finance, as some of the hadith‟s

used to justify derivative contracts like futures, options and forwards are challenged by many

scholars, plus the lack of understanding of the workings of these instruments among Sharia

scholars and the larger public. However, this dissertation would like to take the view that it is

only a matter of time and financial education of Sharia scholars in the working of derivatives to

hedge against market risks faced by IFI‟s like currency risk and commodity risk, that Sharia

compliant products will gain widespread use. The main argument against derivatives are that it

has excessive uncertainity (Gharar) and is gambling (Maysir). A comment in support of

development of Islamic derivative products by a scholar is stated - "we should realize that even

in the modern degenerated form of futures trading, some of the underlying basics concepts as

well as some of the conditions for such trading are exactly the same as were laid down by the

Prophet Mohamed (PBUH) for forward trading. For example, there are clear sayings of the

Prophet Mohamed (PBUH) that he who makes a Salaf (forward trade) should do that for a

33

specific quantity, specific weight and for a specified period of time. This is something that

contemporary futures trading pays particular attention to." (Fahim Khan, 1996) 18

A recent development in Iran is to allow trading Islamic Derivative products.

The Securities and Exchange Organization of Iran has put on agenda to add new Islamic

instruments such as Derivative Securities, Istisna & Murabaha in Capital Market as of the next

Iranian calendar year (March 21, 2011).19

(Ali Salehabadi, Iran Daily 8th

March 2011)

4.6 Summary

It is well understood that Risk Management is Integral for Islamic Financial institutions, which

is supported by both statements in the Holy Quran and traditions of the Prophet Mohamed

(PBUH). It has been seen that Islamic financial transactions are interest (Riba) free, abhors

uncertainty (Gharar), and eschews gambling (Maysir), however these are not risk free. Islamic

Financial Instruments mitigate against certain risks, while creating others for Islamic Financial

Institutions.

The effect of the recent global financial crises on Islamic Financial Institutions has been

minimal, some commentators have tried to portray this as the superiority of the Islamic

economic system which eschews uncertainty, interest and gambling. This is because one of the

key causes was complex derivative products like credit default swap (CDS) and collateralised

debt obligations (CDO) which very few people understood how they operate and the risks

inbuilt in these instruments. While it is agreed that Islamic Financial Institutions would have

avoided these instruments, however some Islamic Financial Institutions For example, a number

of renowned players in the management of Islamic funds, such as The Investment Dar (TID)

and Global Investment House (GIH), both based in Kuwait, have suffered major losses during

the crisis and have become technically insolvent. Plus the debt crises of Dubai and its

consequent real estate market crash revealed excessive speculation. Hence, a majority of Islamic

Financial Institutions while relatively immune because they were not in the centres where the

financial markets were sophisticated. Furthermore, the experience of Kuwait Finance House

during the Souk Al Manakh20

, is a signal for Islamic Financial Institutions to be vigilant about

risk management, as being Islamic will not protect them from excessive speculation.

18

Fahim Khan (Islamic Futures and their Markets, Research Paper No.32, Islamic Research and Training Institute,

Islamic Development Bank, Jeddah, Saudi Arabia, 1996, p.12)

19 http://www.sukuk.me/news/articles/28/Irans-Bourse-to-Add-New-Islamic-Financial-Instrum.html (21 March 2011

20

http://en.wikipedia.org/wiki/Souk_Al-Manakh_stock_market_crash (accessed 25 March 2011)

34

Chapter 5: Analysis of Risk Management disclosures in Financial Statements

5.1 Introduction

This chapter will look at disclosed information on Risk Management in the published financial

statements of three Islamic Financial institutions namely:-

Meezan Bank (Pakistan)

Khaleej Takaful (UAE)

Al Baraka Banking group (Kingdom of Bahrain)

Disclosures on risk management made in the financial statements will be analysed in reference

to figure 2.2 Key Drivers of Risk in Chapter 2.

5.2 Meezan Bank (Pakistan) - based on the Annual Report 2009

Meezan bank is a Pakistan based bank offering retail, corporate and investment banking

services i.e. savings products, Investment products, credit cards, trade finance, capital raising

(Sukuk) for corporate clients and the Government of Pakistan. The products are similar to those

offered by conventional banks.

Risk Management Framework (Annual Report 2009 - Operations review & Note 40)

“Risk management is an integral part of the business activities of the Bank. The Bank manages

the risks through a framework of risk management policies and procedures, organizational

structure and risk measurement and monitoring mechanism that are closely aligned with the

overall operations of the Bank. Risk management activities broadly take place at different

hierarchy levels. The Board of Directors provides overall risk management supervision while

the management of the Bank actively ensures that the risks are adequately identified, measured

and managed. An independent and dedicated Risk Management department guided by a prudent

and a robust framework of risk management policies and guidelines is in place.

The Board has constituted the following committees for effective management of risks

comprising of the Board members: 1. Risk Management Committee

2. Audit Committee

The Risk Management Committee is responsible for reviewing and guiding risk policies and

procedures and control over risk management. The Audit Committee - comprised of three non-