Embed Size (px)

Citation preview

Monthly Webinar Series

presents

Public Solicitation of Private Offerings: Implications of the SEC’s Repeal of the Marketing Ban for Reg D Deals

July 25, 2013

Panelists John Hogoboom, Partner, Lowenstein Sandler LLP

Mark Wood, Partner and Co-‐Chair, Securities Practice Group, Katten Muchin Rosenman LLP William Hicks, Member, Mintz, Levin, Cohn, Ferris, Glovsky and Popeo, P.C.

Moderator Brett Goetschius, Editor and Publisher, Growth Capital Investor

Thank you for participating in “Public Solicitation of Private Offerings: Implications of the SEC’s Repeal of the Marketing Ban for Reg D Deals.” This manual contains information you will need for this webinar.

CONFERENCE MANUAL

This manual contains:

•Dial-‐in/log-‐on instructions.

Speaker bio and contact information. •Tips for submitting questions. •Pertinent information from the pages of Growth Capital Investor.

CONFERENCE DETAILS

The webinar is scheduled for Thursday, July 25, 2013 at 2:00 p.m. EDT, 1:00 p.m. CDT, 12:00 p.m. MDT, and 11:00 a.m. PDT. It will last 90 minutes.

HOW TO JOIN THE WEBINAR

Online With Streaming Audio •Go to http://web.beaconlive.com •On the “Join a Meeting” side of the login page, enter meeting room: mnm2

•Enter your unique PIN (sent in your email confirmation).

•Click on “Join Meeting” to access the presentation.

•Make sure your computer speakers are turned on and at the correct volume. You can adjust the volume by using the up and down arrows above the presenter’s box.

Optional Telephone Access If you have trouble streaming the sound through your computer, please follow these instructions to listen by phone:

•Dial 1-‐877-‐533-‐4964 about 5-‐10 minutes before the start of the conference.

•Enter your unique PIN (sent in your e-‐mail confirmation).

•You will hear music on hold until the conference has started or be connected directly if it has already begun.

•If you have trouble with your PIN stay on the line and an operator will assist you.

•If you are using a speakerphone, put the phone on MUTE for best sound quality.

•If you are disconnected at any point, just repeat the processes above.

PLEASE NOTE: Only one dial in and one log on per PIN are allowed.

If you have problems accessing the webinar, please call 877-‐297-‐2901. HOW TO SUBMIT QUESTIONS

Questions may be submitted at any time during the call using the chat function on the web interface in the lower left corner of your screen. Just type in your question and send it to “Q&A session” in the drop-‐down menu.

Conference Manual Page 1

General Solicitation in Private Placements

MarketNexus Media – July 25, 2013

Conference Manual Page 2

2

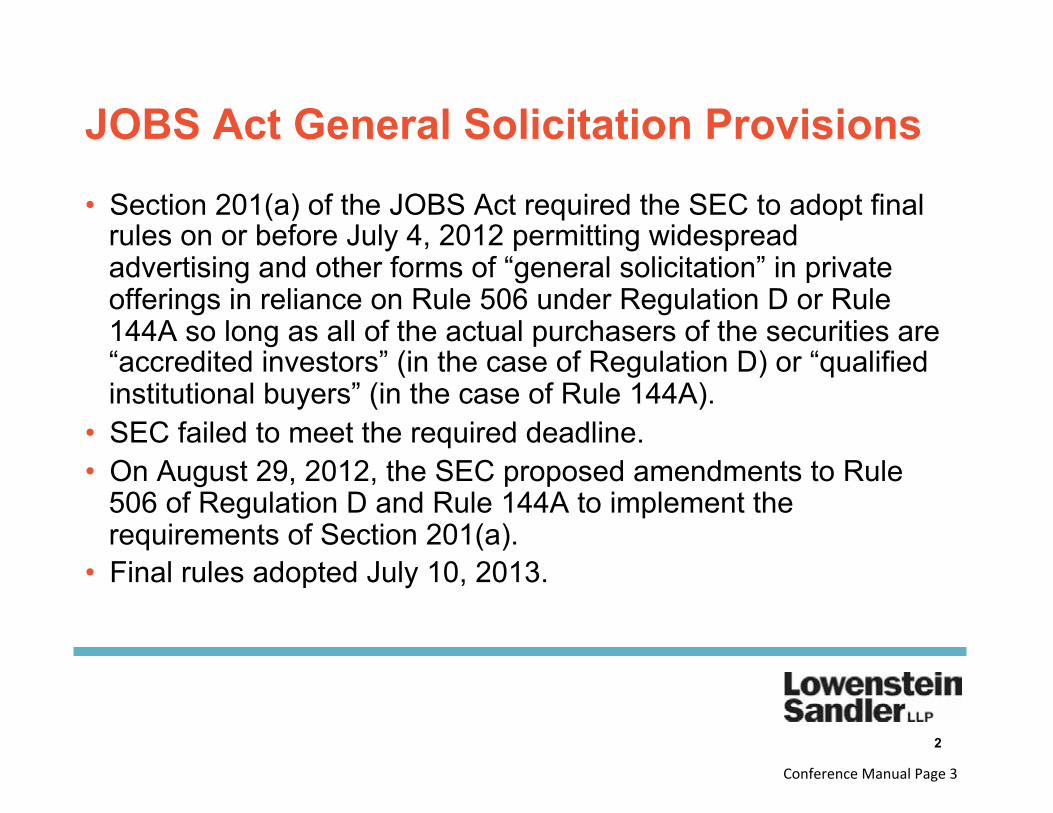

JOBS Act General Solicitation Provisions

Section 201(a) of the JOBS Act required the SEC to adopt final rules on or before July 4, 2012 permitting widespread advertising and other forms of “general solicitation” in private offerings in reliance on Rule 506 under Regulation D or Rule 144A so long as all of the actual purchasers of the securities are “accredited investors” (in the case of Regulation D) or “qualified institutional buyers” (in the case of Rule 144A). SEC failed to meet the required deadline. On August 29, 2012, the SEC proposed amendments to Rule 506 of Regulation D and Rule 144A to implement the requirements of Section 201(a). Final rules adopted July 10, 2013.

Conference Manual Page 3

New General Solicitation Rules

New Rule 506(c) provides a new and separate exemption under the Rule that permit issuers to use general solicitation and general advertising to offer securities, provided that the issuer takes reasonable steps to verify that all purchasers of the securities are accredited investors. Whether the steps taken by the issuer to verify the accredited investor status of the purchasers are “reasonable” is an objective determination, based on the particular facts and circumstances of each offering and investor. SEC has declined to mandate specific methods of verification; however, the final rule sets forth several non-exclusive, non-mandatory methods that may be used to verify the status of individual accredited investors.

3

Conference Manual Page 4

Verification Procedures

Whether the verification steps taken are “reasonable” will be an objective determination by the issuer (or those acting on its behalf), considering the particular facts and circumstances of each purchaser and transaction, including, among other things: – The nature of the purchaser and the type of accredited investor that

the purchaser claims to be. – The amount and type of information that the issuer has about the

purchaser. – The nature of the offering, such as the manner in which the

purchaser was solicited to participate in the offering, and the terms of the offering, such as a minimum investment amount.

4

Conference Manual Page 5

Nature of the Person

SEC acknowledges that reasonable steps to verify the accredited investor status of natural persons poses greater practical difficulties as compared to other categories of accredited investors. Natural persons may be accredited investors based on either a “net worth test” or an “income test.” SEC recognizes that it may be more difficult for an issuer to obtain information about a person’s assets and liabilities than about a person’s income. Potential privacy concerns.

5

Conference Manual Page 6

Purchaser Information

The more information an issuer has indicating that a prospective purchaser is an accredited investor, the fewer steps it would have to take to verify the purchaser’s status, and vice versa. If actual knowledge that purchaser is an accredited investor, no additional steps required. Verification examples: – Publicly available information in filings with a federal, state or local

regulatory body. – Third-party verification of a person’s status as an accredited

investor, provided that the issuer has a reasonable basis to rely on such third-party verification.

6

Conference Manual Page 7

Natural Person Verification

Under the “income test,” an issuer may rely on any IRS form that reports income of the purchaser for the two most recent years, along with a written representation from the purchaser that he or she has a reasonable expectation of reaching the necessary income level during the current year. Under the “net worth test,” an issuer may rely on certain documentation disclosing the assets and liabilities of the purchaser, dated within the prior three months: – Assets -- bank statements, brokerage statements, certificates of deposit,

tax assessments and appraisal reports issued by independent third parties;

– Liabilities -- a credit report from at least one of the nationwide consumer reporting agencies, provided that purchaser represents in writing that all liabilities necessary to make a determination of net worth have been disclosed.

7

Conference Manual Page 8

Natural Person Verification

Under either test, issuers may rely on written confirmations from broker-dealers, registered investment advisers, licensed attorneys and/or CPAs that such entity or person has taken reasonable steps to verify the purchaser’s accredited investor status within the prior three months. – Statements by others may also be acceptable if the party takes

reasonable steps to verify the purchaser’s accredited investor status and the issuer has a reasonable basis to rely on that verification.

Issuers can verify existing investors who are natural persons by having the person certify at the time of sale that he or she qualifies as an accredited investor.

8

Conference Manual Page 9

Nature and Terms of the Offering

Issuers soliciting new investors from the general public (e.g., through a public website or a widely disseminated email) must take additional steps to verify accredited investor status. – Not sufficient for the issuer only to require that a person check a box in

a questionnaire or sign a form, absent other information about the purchaser indicating accredited investor status

– Can’t rely solely on investor representations in subscription documents, absent other information.

Issuers soliciting new investors from a database of pre-screened accredited investors created and maintained by a reasonably reliable third party may rely on the database as long as they have a reasonable basis for doing so.

9

Conference Manual Page 10

Nature and Terms of the Offering

Minimum investment amount. – If required minimum is sufficiently high that only accredited investors

could reasonably be expected to meet it, it may be reasonable for the issuer to take no steps other than to confirm that the purchaser’s investment is not being financed by the issuer or any other third party.

– No specific SEC guidance as to what minimum investment level is high enough.

Issuers may be able to check the accredited investor status of potential investors with third-party services where the services, rather than the issuers themselves, obtain appropriate documentation or take other steps to verify such status.

10

Conference Manual Page 11

Issuer Burden

Rule 506(c) continues to apply the “reasonable belief” standard to the condition that all purchasers are accredited investors. Issuer has the burden of demonstrating that its offering is entitled to an exemption. – Issuers need to create and retain adequate records that document

the steps taken throughout the verification process. – SEC intends to monitor the development of verification practices,

and will review the impact of compliance with the verification requirement on investor protection and capital formation.

Verification process only one part of perfecting the Rule 506 exemption.

11

Conference Manual Page 12

Other New Changes Rule 144A also amended to permit general solicitation so long as issuer reasonably

believes all purchasers are QIBs. Consistent with the historical treatment of concurrent Regulation S and Rule 144A/

Rule 506 offerings, concurrent offshore offerings that are conducted in compliance with Regulation S will not be integrated with domestic unregistered offerings that are conducted in compliance with Rule 506 or Rule 144A.

Privately offered funds can make a general solicitation under amended Rule 506 without losing the ability to rely on Sections 3(c)(1) and 3(c)(7) of the Investment Company Act, which provide commonly used exclusions from the definition of “investment company”. – However, due to concerns about investor protection, the SEC intends to monitor and study the

development of private fund advertising and review whether any further action is necessary. SEC confirmed that securities issued in new Rule 506(c) offerings will be “covered

securities” for purposes of Section 18(b)(4)(E) of the Securities Act. As a result, state blue sky registration requirements will not apply to securities offered and sold in Rule 506(c) offerings.

12

Conference Manual Page 13

Bad Actor Disqualification New Rule 506(d) precludes reliance on Rule 506 (subject to a reasonable care

exception) when a “covered person” has been the subject of a specified triggering event.

“Covered Persons” – the issuer and any predecessor or affiliated issuer; – any director, executive officer, other officer participating in the offering, general partner or

managing member of the issuer; – any beneficial owner of 20% or more of the issuer’s outstanding voting equity securities,

calculated on the basis of voting power; – any investment manager of an issuer that is a pooled investment fund and any director, executive

officer, other officer participating in the offering, general partner or managing member of the investment manager, as well as any director, executive officer or participating officer of any such general partner or managing member;

– any promoter connected with the issuer in any capacity at the time of the sale; – any person that has been or will be paid (directly or indirectly) remuneration for solicitation of

purchasers in connection with sales of securities in the offering (a “compensated solicitor”); and – any director, executive officer, other officer participating in the offering, general partner, or

managing member of any compensated solicitor.

13

Conference Manual Page 14

Bad Actor Disqualification

New Rule 506(d) will apply if a covered person is subject to certain disqualifying events, including: – a criminal conviction within ten years before the proposed sale of securities (or

five years, in the case of issuers) in connection with the purchase or sale of any securities, involving the making of any false filing with the SEC or arising out of the conduct of the business of certain financial intermediaries;

– a court injunction or restraining order, entered within five years before the sale, in connection with the purchase or sale of a security, the making of a false filing with the SEC, or arising out of the conduct of certain types of financial intermediaries;

– an SEC stop order or order suspending use of the Regulation A exemption issued within five years before the sale;

– certain SEC cease and desist and disciplinary orders; – a suspension or expulsion from membership in a self-regulatory organization

(“SRO”) or from association with an SRO member; and – certain regulatory orders barring a covered person from certain associations or

that are based on fraudulent, manipulative or deceptive conduct and was issued within 10 years of the proposed sale of securities.

14

Conference Manual Page 15

Bad Actor Disqualification

SEC waiver possible if: – SEC determines that the issuer has shown good cause “that it is not

necessary under the circumstances that an exemption be denied.” – Several factors noted that could be relevant in deciding whether to grant

a waiver, such as a change of control or a change of supervisory personnel.

506(d) only relates to events occurring after the effective date of the new rule. – Issuer must provide investors written disclosure of prior events that

would have triggered disqualification. – Applies to all offerings under Rule 506, regardless of whether the

purchasers are accredited investors. – Must provide disclosure “a reasonable time prior to sale.” – Failure to comply with this disclosure requirement could result in loss of

the exemption.

15

Conference Manual Page 16

New Rule Proposals

In addition to amending Rule 506 to add new paragraphs (c) and (d), the SEC proposed a number of additional changes to Regulation D, Form D and Rule 156. Proposed changes intended to address concerns regarding general solicitation and to permit the SEC to monitor activity under Regulation D, Proposed rules are subject to comment. Unlikely to be effective before the effective date of new Rules 506(c) and (d).

16

Conference Manual Page 17

Advance Filing and Updating of Form D

Rule 503 would be amended to require an issuer intending to engage in general solicitation for a Rule 506(c) offering to file an initial Form D at least 15 calendar days in advance of commencing any general solicitation and to disclose certain information required by revised Form D. The initial Form D would be required to be updated within 15 calendar

days after the date of first sale of securities in the offering, to update the initial Form D and to provide additional information. A final amendment would be required within 30 calendar days after the

termination of any offering conducted in reliance on Rule 506(b) or (c). Until the termination amendment is filed, the offering would be deemed to

be ongoing, and the issuer would be subject to the current Rule 503 requirements to file amendments to Form D at least annually and otherwise as needed to reflect changes in previously filed information. SEC seeks comment on inadvertent general solicitation issue.

17

Conference Manual Page 18

Additional Form D Information

The proposal would amend Form D to require issuers to provide additional information to enable the SEC to better analyze the impact of general solicitation on the market for Rule 506 offerings. Also would increase information available to the SEC regarding the overall use of the Rule 506 exemption.

18

Conference Manual Page 19

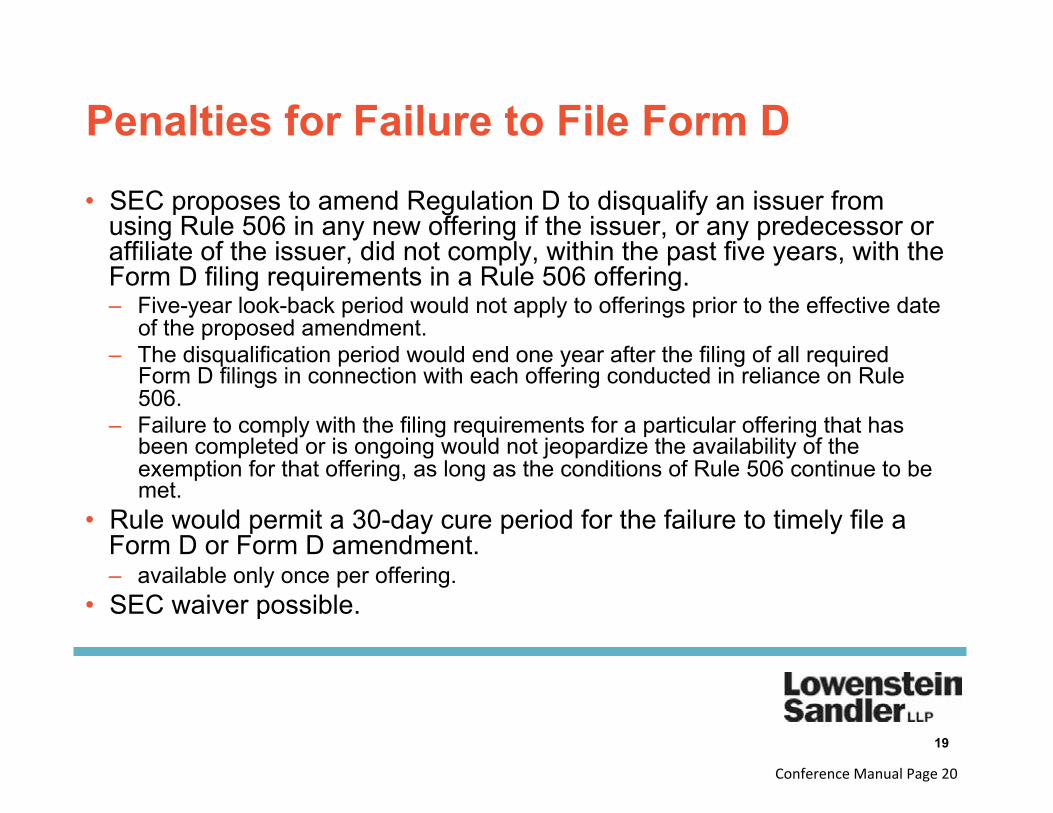

Penalties for Failure to File Form D

SEC proposes to amend Regulation D to disqualify an issuer from using Rule 506 in any new offering if the issuer, or any predecessor or affiliate of the issuer, did not comply, within the past five years, with the Form D filing requirements in a Rule 506 offering. – Five-year look-back period would not apply to offerings prior to the effective date

of the proposed amendment. – The disqualification period would end one year after the filing of all required

Form D filings in connection with each offering conducted in reliance on Rule 506.

– Failure to comply with the filing requirements for a particular offering that has been completed or is ongoing would not jeopardize the availability of the exemption for that offering, as long as the conditions of Rule 506 continue to be met.

Rule would permit a 30-day cure period for the failure to timely file a Form D or Form D amendment. – available only once per offering. SEC waiver possible.

19

Conference Manual Page 20

General Solicitation Materials

New Rule 509 would require an issuer to include specified legends in all written general solicitation materials used in a Rule 506(c) offering. Compliance with the proposed legend requirements wouldn’t affect issuer requirement to take reasonable steps to verify that purchasers in a Rule 506(c) offering are accredited investors. The legend and other disclosure requirements of proposed Rule 509 would not be conditions to the Rule 506(c) exemption. Proposal would disqualify an issuer from relying on Rule 506 in subsequent offerings if the issuer, or any of its predecessors or affiliates, has been subject to any court order enjoining non-compliance with proposed Rule 509.

20

Conference Manual Page 21

Submission of General Solicitation Materials

New Rule 510T would require an issuer conducting a Rule 506(c) offering to submit to the SEC any written general solicitation materials prepared by or on behalf of the issuer and used in connection with the offering. – Materials would have to be submitted to the SEC no later than the date of first use. – Materials submitted would not be treated as “filed” or “furnished” for purposes of the

Securities Act or the Exchange Act, including the liability provisions thereof – Submitted materials would not be made publicly available. SEC does not intend that submitted materials would be subject to the staff

review and comment process. SEC expects that the temporary rule would expire two years after its

effective date. Submission requirement would not be a condition to the Rule 506(c)

exemption. – issuer would be disqualified from relying on Rule 506 in subsequent offerings if it or

any of its predecessors or affiliates has been subject to any court order enjoining non-compliance with proposed Rule 510T.

21

Conference Manual Page 22

Private Funds Private funds making an offering under Rule 506(c) would be required to include

additional disclosures in their written general solicitation materials. – Any performance data provided would have to be given as of the most recent practicable date. – If performance data do not reflect the deduction of fees and expenses, the disclosure would have

to state that fees and expenses have not been deducted and that performance may have been lower than presented had such fees and expenses been deducted.

SEC proposes to extend Rule 156 (which provides guidance on manipulative practices) to apply to all sales literature used by private funds, whether in offerings under Rule 506(c) or otherwise. – Sales literature would include any communication used by any person to offer to sell or induce the

sale of securities of any investment company or private fund. SEC has asked for comment on whether additional restrictions on private fund

offerings are necessary in connection with Rule 506(c) offerings by private funds – Use of performance data – Should the SEC impose standardized calculation methodologies.

22

Conference Manual Page 23

Legal Disclaimer

Although this presentation may provide information concerning potential legal issues, it is not a substitute for legal advice from qualified counsel. The presentation is not created or designed to address the unique facts of circumstances that may arise in any specific instance, and you should not and are not authorized to rely on the contents of this presentation as a source of legal advice and this presentation material does not create any attorney-client relationship between you and Lowenstein Sandler LLP.

23

Conference Manual Page 24

Legal Disclaimer

Although this presentation may provide information concerning potential legal issues, it is not a substitute for legal advice from qualified counsel. The presentation is not created or designed to address the unique facts of circumstances that may arise in any specific instance, and you should not and are not authorized to rely on the contents of this presentation as a source of legal advice and this presentation material does not create any attorney-client relationship between you and Lowenstein Sandler LLP.

23

Conference Manual Page 25

SPEAKER BIOS AND CONTACT INFORMATION

John D. Hogoboom is a founding member of the Lowenstein Sandler Specialty Finance Group and is co-‐chair of the Life Sciences Group. He specializes in representing clients in the life sciences and other industries in mergers and acquisitions, public and private securities offerings, private equity investments and general corporate and securities law. Mr. Hogoboom is listed inThe Best Lawyers in America in the 2007-‐2012 editions of the publication, in both the corporate law and securities law categories.

CONTACT John D. Hogoboom Founding Member, Specialty Finance Group Lowestein Sandler LLP 646-‐414-‐6846 [email protected]

Conference Manual Page 26

Mark D. Wood is head of Katten Muchin Rosenman's securities practice and concentrates in corporate and securities law. He represents public companies, issuers and investment banks in initial public offerings (IPOs) and other public offerings, private investment in public equity (PIPE) transactions, debt securities and other securities matters. Mr. Wood is a leading practitioner in representing investors, public companies and placement agencies in PIPE transactions.

CONTACT Mark D. Wood Head, Securities Practice Katten Muchin Rosenman 312-‐902-‐5493 [email protected]

Conference Manual Page 27

William Hicks is a Member with Mintz Levin Cohn Ferris Glovsky and Popeo. He has extensive experience representing placement agents and underwriters in structuring and executing initial public offerings, alternative public offerings, including reverse mergers, Form 10/Resale S-‐1 club deals and confidentially marketed IPOs, Confidentially Marketed Public Offerings (CMPOs), registered directs, PIPEs and private placements. Mr. Hicks represents venture capital firms and private equity firms in customized investments in public companies, including structured PIPEs and registered directs.

CONTACT William Hicks Member Mintz Levin Cohn Ferris Glovsky and Popeo 617-‐348-‐1799 [email protected]

Conference Manual Page 28

Vol. II Issue 13 The Journal of Emerging Growth Company Finance July 15, 2013

Repeal of General Solicitation Ban Brings New Era for Private Offerings

by Brett Goetschius

Last week’s long-anticipated repeal of the ban on public advertising of private securities offerings either ushers in a new era of transparent, in-formation-rich, digitally-greased, and crowd-vetted capital markets, or

it is a leap into the abyss that will pervert the most trusted capital markets in the world into a carnival midway of investment hustlers, crowd madness pan-derers and common thieves. That seems to be the consensus, or lack thereof, of regulators and growth capital professionals surveyed in the wake of the SEC’s action to implement the mandate set by Congress a year ago when it passed the JOBS Act.

On July 10, the Securities and Exchange Commission held an open meet-ing regarding its nine-month old proposal to repeal the ban on the advertis-ing and general solicitation of Regulation D securities offerings. Although the amendment, known as Rule 506(c), was ultimately adopted, concerns regard-ing investor protection were raised by two commissioners, Elisse Walter and Luis Aguilar.

Walter’s concerns about the risks of fraud and the promotion of invest-ments inappropriate to less sophisticated investors came short of persuading her to vote against the repeal. Aguilar was blunter in his criticism, decry-ing the Commission’s move to repeal the ban before approving additional

Energy Exploration, Medical Device Growth EPP Issuers Buck

Post-Deal Price Drops in Q2by Joe Gose

The stock market’s bull run in the first half of 2013 that pushed the Dow Jones Industrial Average and Standard & Poor’s 500 indexes to all time highs failed to influence initial investor reaction to growth

equity private placements (EPPs). Looking at stock price performance on an industry-by-industry basis, in-

vestors largely sold on the news of a private deal, and sentiment three days after announcement was frequently more pessimistic than the response over the first half of 2013, according to analysis by Growth Capital Investor.

Additionally, transaction activity slowed from a year earlier while the

IN THIS ISSUE Sponsored Deals Recovering

from Slow Q1After a slow 2013 first quarter, sponsored growth equity private placements – deals taken by long-only fundamental investors – generated more deals and more dollars in the second quarter....2

Rollup King Returns to SPAC MarketJonathan Ledecky is making a big bet investing in mobile advertising. ............................................. 3

Judge Limits Yuhe Investor Suit Against UnderwritersUnderwriters of a $40 million secondary offering from chicken breeder Yuhe International fight-ing investor suit in alleged $12 million diversion scheme. .............................................................. 4

ALSO INSIDEFormer Deephaven Manager Launches New Fund; FINRA Readies Crowdfunding Portal Rules for Comment; Oramed Pharm Raises $4.6M via Aegis; Oak Ridge Micro-Energy Raises $2.5M from Precept Fund, Insiders; other stories and deals of note .... 5

EPP, PIPE & APO MARKET DATAAggregate Year-to-Date Market Activity .............. 9Deal Performance – Growth Capital EPPs ......... 11Growth Capital EPP Candidates ....................... 15 See Repeal on page 13

See Q2 on page 16

Growth Capital Investor

Growth Equity Private Placement Activity

Source: PlacementTracker, a service of Sagient Research. April data thru 7/15/13.

Investment ($B) Deals

0

$0.5

$1.0

$1.5

$2.0 billion

Feb. Mar. Apr. May June July*2013

31

48

40

5053

12

Conference Manual Page 29

mitigating rules aimed at keeping “bad actors” out of the market and strengthening disclosure requirements for pri-vate offerings.

“It is a false proposition to suggest that the Commission’s hands are tied — and that the JOBS Act prevents the Com-mission from protecting investors and safeguarding the integ-rity of the securities markets at the same time that it makes the changes required to Rule 506,” Aguilar said in remarks before casting the lone dissenting vote.

“The Commission is going ahead with the adoption of Rule 506(c), but only proposing the changes that would help to mitigate the harm to investors. The measures discussed in the accompanying proposal should have been considered as part of the amendments to allow general solicitation…. It is reckless to create a known risk today, with just the hope of a speculative remedy tomorrow.”

Seeking to deflect the criticism that removing the gener-al solicitation ban would “open the floodgates of fraud,” the commission staff proposed additional amendments to Rule 506 that would formalize the verification process for accredit-ed investors. The commission also voted to publish for public comment a proposal to impose several additional reporting requirements on Form D to:

• require issuers and investors to provide additional in-formation on Form D

• veliminate the ability of an issuer to use Rule 506 ex-emptions if it failed to file a required Form D duringthe prior five-year period (with certain cure provisions)

• require issuers to file a Form D at least 15 days priorto engaging in any general solicitation and to file a fi-nal amendment to that Form D not later than 30 daysfrom the end of the offering

• for an initial two-year period, require issuers engagingin general solicitations under Rule 506(c) to submittheir solicitation materials to the SEC on a confidentialbasis

• impose legending requirements on any general solicita-tion materials

• extend the advertising guidance in Rule 156 applicableto public funds to private funds.

Both Commissioners Paredes and Gallagher opposed the Form D rule changes. Paredes said that the additional disclosure requirements would “undermine the intent of the JOBS Act,” and hurt the ability of small companies in par-ticular to raise capital. According to the SEC, Reg D offer-ings completed from 2009-2012 raised an average of $30M. However, the median Reg D offering amount was $2M, il-lustrating the large volume of smaller deals that occur in the market.

In addition, the commission approved the long-proposed

“bad actor” provisions of the Dodd-Frank financial regulatory reform act. The rules seek to exclude persons and corporate entities which have been convicted of a felony or have been involved in other disciplinary cases with the SEC from partic-ipating in restricted securities offerings. This rule would nar-row coverage to executive officers, beneficial owners of 20% of an issuer, and investment managers involved in offerings. Additionally, events triggering the “bad actor” designation must occur after the adoption of the ruling, thus excluding past events.

The final language, which narrowed the scope of the rule dramatically from that originally proposed in early 2011, drew a sharp rebuke by Aguilar, who criticized chang-es from the original proposal which excluded any actions prior to adoption of the proposal from triggering bad actor status (the original proposal had included activities dating back five years.) Aguilar also criticized the expansion of the beneficial owner threshold from 10% to 20%, and the nar-rowing of covered persons from any officer of the issuer or any officer of a person paid to solicit investors, to only ex-ecutive officers of such entities and officers who participate in the offering.

The General Solicitation repeal was approved by a 4-1 vote. Despite concerns raised by Aguilar, the Bad Actor Rule passed unanimously, and the Form D proposal was approved for release for comment by a 3-2 vote, with dissent from Gal-lagher and Paredes. The new rules will be effective 60 days after their publication in the Federal Register.

Market Reaction SplitEquity crowdfunding advocates who had waited more

than a year for the advertising ban, seen as the key obstacle to accredited investor-based crowdfunding, to be repealed, uni-formly hailed the action. However, the reaction among tradi-tional Reg D market professionals was more mixed.

Cromwell Coulson, president of OTC Markets, the primary quotation market for securities of unlisted public companies, hailed the repeal as a blow for market transpar-ency.

“I think it’s awesome that they lifted the ban on trans-parency,” Coulson said. Until now, private companies have been forced to raise capital in an information vacuum, he ex-plained, in which the dissemination of information about the company was severely proscribed.

“The general solicitation ban was really a ban on trans-parency. That’s terrible for market efficiency and investor education,” he added. Coulson believes the repeal of the solicitation ban “will totally change the path that a compa-ny will take toward becoming an exchange-listed company,” by creating gradations of ever-greater public reporting and

Repeal continued from front page

July 15, 2013 Copyright © 2013 MarketNexus Media, Inc. 13

Growth Capital Investor

Conference Manual Page 30

trading levels, much like the three designations now accord-ed OTC stocks – the Pink, QB, and QX levels – at OTC Markets.

Coulson believes the ability to solicit investment will keep a lot of companies private that might otherwise have gone public too early in their corporate and financial devel-opment to truly benefit from fully public status. “There will be lots of small companies that can exist as private companies, because transparency is now allowed. Public versus private distinctions should go away. ‘Sales restricted’ should be the new description,” for private securities, he said.

OTC Markets is moving quickly to adapt to the new re-gime. The firm plans to begin quoting 144A securities, and introduce a service to announce and post Reg D offering pro-spectuses.

Bill Hicks of Mintz Levin is similarly expansive on the potential of letting slip the dogs of advertising upon the pri-vate capital markets. Calling the change nothing less than “transformative” for corporate capital formation, Hicks sug-gested solicited 506(c) offerings could help fuel varieties of alternative public offerings (APOs).

“This really opens the door,” said Hicks. The repeal of the solicitation ban is “the real crowdfunding bill. It will allow small companies to go out and market an offering broadly,” helping to create a retail shareholder base that is critical to maintaining liquidity in their shares.

“This will allow the kind of crowdfunding that is actually useful,” said Hicks, adding that solicited offerings could be used in conjunction with an institutional-investor led financ-ing of a reverse merger, commonly called an “APO” or alter-native public offering.

“When you add a Form 10 self-filing with a reverse merg-er and a 506(c) filing, you have a very interesting possible format,” he said. Adding in a publicly marketed offering to the traditional APO process could broaden a newly public company’s shareholder base, providing better liquidity to initial APO investors, and offering institutions the trading volume, share price support and public float they demand before making significant long-term investments in emerging growth companies.

Hicks said he believes that solicited offerings could make the Form 10 APO a favored path for larger private emerging growth companies seeking to go public without an IPO but for which establishing a large retail investor base quickly is critical. This path could be especially attractive to companies that can tap sizable retail customer or affinity group bases.

He added that the repeal will be highly disruptive to the angel and venture capital markets, and that he sees the 506(c) offerings market developing more in parallel than

in conjunction with those markets in the near term. Tra-ditional angel and venture fund models are clearly the in-cumbents that will be disrupted by the new offerings, and are reacting with the typical hostility toward innovation that old-guard players express when their market hegemo-ny is challenged.

Mindful of that hostility, Hicks believes those companies seeking to raise capital will face a difficult choice between traditional venture-style capital raising and 506(c) offer-ings. Given the current lack of institutional venture investors which are willing to consider investment in companies with a dispersed shareholder base, “It will be more the exception than the rule,” says Hicks, that a 506(c) or Title III crowd-funded company will be able to attract institutional venture capital later on.

Coulson agreed that the solicitation ban repeal and 50b(c) will be a “game changer” for the venture capital market, which in the past, “wanted all of their portfolio companies’ informa-tion, but wanted to keep it to themselves,” he said. This gave VC firms huge advantages in pricing and allocating capital that other potential capital providers lacked. Now, companies will be able to release financial information and projections to any potential funding source, leveling the playing field and expanding the potential investor pool.

Mark Wood of Katten Muchin Rosenman believes that repeal of the solicitation ban will impact the traditional PIPE market as well as private equity. Proposed requirements to submit Form D filings 15 days prior to commencing 506(c) offerings, and to require offering marketing documents to be filed with the SEC ahead of offering marketing periods will be “tricky” to navigate for issuers and PIPE agents, even when no truly public solicitation is intended.

“SEC is taking the position that you are planning to do a public solicitation anyway, why should you have a prob-lem with telling the world about your plans ahead of time,” said Wood. “But that assumes everyone is going to do it in a truly public way, taking full advantage of the rule. I think companies might seek to use [the 506(c) exemption] on the margins, to get around concerns that when you broaden a private placement beyond the investor group that you are really comfortable with but say, are conducting an offering pursuant to confidentiality agreements so that the offering re-mains confidential, you couldn’t do that if these proposals go through,” he said.

“The SEC seems to be saying you can either do it com-pletely private in the old fashioned way, or fully public. The Commission is not allowing for any middle ground. There is all this arcane guidance on public solicitation that is difficult to interpret and confusing for issuers. When you are doing a private placement, you’re worried you are going to cross some

July 15, 2013 Copyright © 2013 MarketNexus Media, Inc. 14

Growth Capital Investor

Conference Manual Page 31

line. We had hoped these rules would allow companies that still really intended to follow the old model of private placement offerings to not worry so much about whether they’d uninten-tionally crossed the line [into public solicitation.] That if they found they had crossed the line, they could just declare it a publicly solicited offering. But it’s not going to work like that,” Wood said. “You are going to have to follow a different regime from the outset to qualify for the exemption.”

Wood also thinks there will be a “great reluctance” among issuers to submit their offering marketing materials to the SEC, even in a confidential manner. “That’s more scrutiny than most issuers want.”

Jack Hogoboom of Lowenstein Sandler was the most pessimistic of those contacted about the repeal of the solici-tation ban. Calling the repeal “completely misguided from a policy perspective,” Hogoboom said he agreed with many of Commissioner Aguilar’s criticisms, but wasn’t surprised giv-en the pressure on Chairman Mary Jo White to adopt the year-old Congressional mandate that the SEC took a princi-ples-based rule making approach to implementing the repeal while augmenting its monitoring and information gathering capabilities.

Hogoboom, highly skeptical that public promotion of

private offerings will prove beneficial to the markets overall, is particularly dismayed that the Commission moved in the same breath to weaken proposals that would have helped pre-vent fraud perpetrators from entering the market. He cited the elimination of any grandfathering of trigger events in the Bad Actor Rule as a prime example of the Commission’s poor judgment and naiveté.

“I would really like to know why they didn’t include a look-back on prior bad actors,” Hogoboom said. “That’s a loophole that people are going to be able to exploit.” He was also surprised that the threshold for applying the bad actor test to investors was raised from the proposed 10% or larger beneficial ownership in an issuer, the long-established thresh-old for affiliate and insider status in a public company, to 20% beneficial ownership.

Yet like Wood, Hogoboom took issue with several of the Form D filing requirements, calling the requirement to file 15 days prior to a 506(c) offering too restrictive, and the one-year penalty prohibition from using 506(c) for issuers who have failed to file a Form D in the past five years, too punitive. Overall, he says he is taking a “wait and see” stance on the Form D proposals, expecting additional revisions before any final rules are adopted, which will come at the earliest in late September.

Jack HogoboomLowenstein Sandler

Mark WoodKatten Muchin Rosenman

Public Solicitation of Private Offerings: Implications of the SEC’s Repeal of the Marketing Ban for Reg D Deals

July 25, 2013 2:00 – 3:30 pm EDT

The SEC’s recent repeal of the ban on general solicitation and advertising of Reg D private placement offerings will transform the private and public equity capital markets. Join our discussion of the immediate impacts on private Reg D offerings, alternative public offerings (APOs), and the private placement of public equity (PIPE) market, featuring a panel of top Reg D securities offering experts.

This is a 90-minute live interactive webcast with online and post-program Q&A hosted by Brett Goetschius, Editor & Publisher of Growth Capital Investor.

Free for subscribers to Growth Capital Investor. $199 for non-subscribers.

This program will be submitted for CLE credit eligibility in NY and CA.

For more information or to register: http://growthcapitalist.com/events

Growth Capital Investor Monthly Webinar Series

Bill HicksMintz Levin

Panelists:

July 15, 2013 Copyright © 2013 MarketNexus Media, Inc. 15

Growth Capital Investor

Conference Manual Page 31