Embed Size (px)

Citation preview

ON THE EFFECTIVENESS OF

EXCHANGE RATE INTERVENTIONS

IN EMERGING MARKETS

Christian DaudeOECD Economics Department

Eduardo Levy YeyatiUniversidad Torcuato Di Tella

Arne NagengastDeutsche Bundesbank

Encuentro Anual de la Sociedad de Economistas del Uruguay

Montevideo, 22/12/2014

Outline

• Motivation

• Empirical approach

• Main results and robustness

• Potential extensions

Floating Exchange Rates and FX-market

Intervention

• Different motives for intervention

– Exchange rate moving away from a RER target: implies an explicit or implicit ER rigidity

– Leaning against the wind (exchange rate moving away from equilibrium): “corrective” intervention to smooth out deviations or volatility

• This paper focuses on the second type of interventions

– Literature tends to focus on precautionary/prudential interventions (Aizenman and Lee, 2007; Obstfeld et al, 2010)

– Evidence that interventions correlate negatively with exchange rate pressure and are frequently complemented with capital controls (make intervention for precautionary motives more expensive)

– Other parts of the academic literature focus on:• Fear of floating/postponing devaluations (Calvo and Reinhart, 2002; Hausmann et al,

2000)

• Preserving a depreciated exchange rate to foster growth ((Rodrik, 2008; Hausmann et al, 2005; Johnson et al, 2010; Gluzmann et al, 2012)

• Preventing Dutch-disease (Rajan and Subramanian, 2011; Cardenas et al, 2011)

Survey data on FX intervention motives

Empirical approach

• Panel of 18 emerging economies with floating exchange

rates

• Two-step approach:

– First step: estimate the equilibrium real exchange rate based on

fundamentals (commodity terms of trade, government consumption,

productivity, trade openness, net foreign asset position)

– Second step: error correction model augmented by short-term

financial drivers (VIX, interest rate differentials)

– The effectiveness of interventions is tested within the second step

Endogeneity problem and intervention

variable-.

15

-.1

-.05

0

.05

.1

e(

dlre

r | X

)

-.15 -.1 -.05 0 .05e( dltr | X )

coef = .62596092, se = .08292779, t = 7.55

Korea

-.15

-.1

-.05

0

.05

.1

e(

dlre

r | X

)

-.2 -.1 0 .1e( dltr | X )

coef = .15479632, se = .07001543, t = 2.21

Brazil

-.1

-.05

0

.05

e(

dlre

r | X

)

-.2 -.1 0 .1e( dltr | X )

coef = .03259619, se = .04897594, t = .67

Chile

-.1

-.05

0

.05

.1

e(

dlre

r | X

)

-.1 -.05 0 .05 .1e( dltr | X )

coef = .25088801, se = .11631723, t = 2.16

Colombia

Changes in reserves (logs) and the RER

Endogeneity problem and intervention

variable (cont.)

Changes in Reserves-M2 ratio and RER

-.15

-.1

-.05

0

.05

.1

e(

dlre

r | X

)

-.05 0 .05e( int1 | X )

coef = -.57982027, se = .15096658, t = -3.84

Brazil

-.1

-.05

0

.05

e(

dlre

r | X

)

-.04 -.02 0 .02 .04e( int1 | X )

coef = -.43349667, se = .14243481, t = -3.04

Chile

-.1

-.05

0

.05

.1

e(

dlre

r | X

)

-.04 -.02 0 .02 .04e( int1 | X )

coef = -.89636597, se = .2000494, t = -4.48

Colombia

-.15

-.1

-.05

0

.05

.1

e(

dlre

r | X

)

-.03 -.02 -.01 0 .01 .02e( int1 | X )

coef = -.95277839, se = .34829487, t = -2.74

Korea

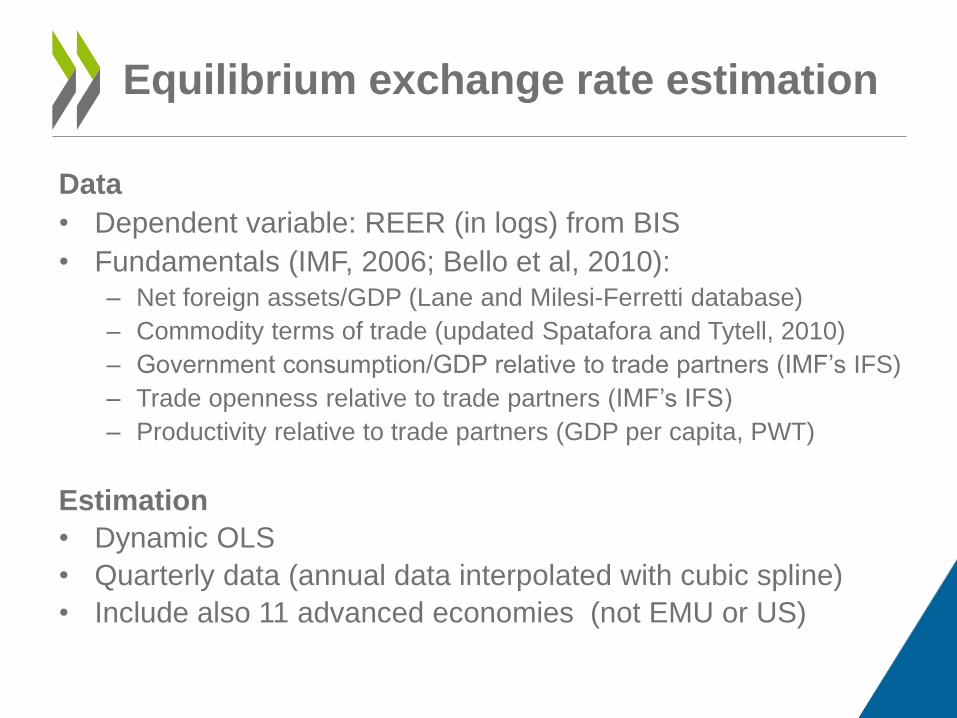

Data

• Dependent variable: REER (in logs) from BIS

• Fundamentals (IMF, 2006; Bello et al, 2010):

– Net foreign assets/GDP (Lane and Milesi-Ferretti database)

– Commodity terms of trade (updated Spatafora and Tytell, 2010)

– Government consumption/GDP relative to trade partners (IMF’s IFS)

– Trade openness relative to trade partners (IMF’s IFS)

– Productivity relative to trade partners (GDP per capita, PWT)

Estimation

• Dynamic OLS

• Quarterly data (annual data interpolated with cubic spline)

• Include also 11 advanced economies (not EMU or US)

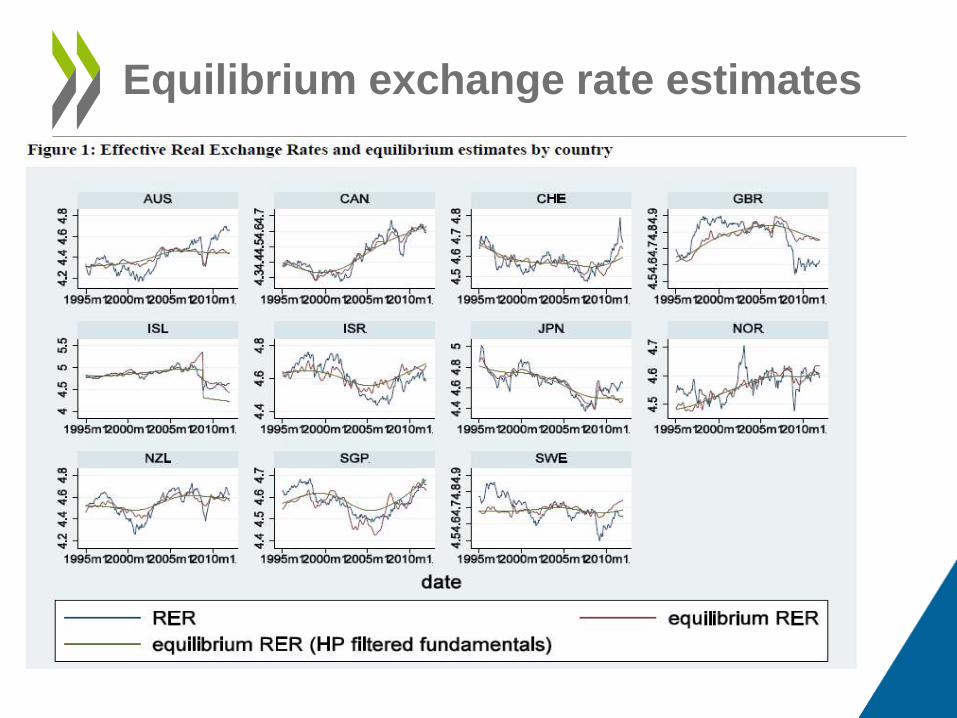

Equilibrium exchange rate estimation

Equilibrium exchange rate estimates

Equilibrium exchange rate estimates

Equilibrium exchange rate estimates

ERER at trend versus current

fundamentals

• Monthly data

• INT: strict proxy for intervention (Levy Yeyati et al, 2013)

• Precautionary motives make reserves and M2 move together to avoid bank and currency runs (Obstfeld et al, 2010): INT mitigates some potential biases (e.g. an appreciation that induce the Central Bank to build reserves for precautionary motives, as a stronger currency deteriorates the R/M2 ratio due to valuation effects).

• Bias is generally a attenuation bias, but we also instrument INT by the first difference in M2.

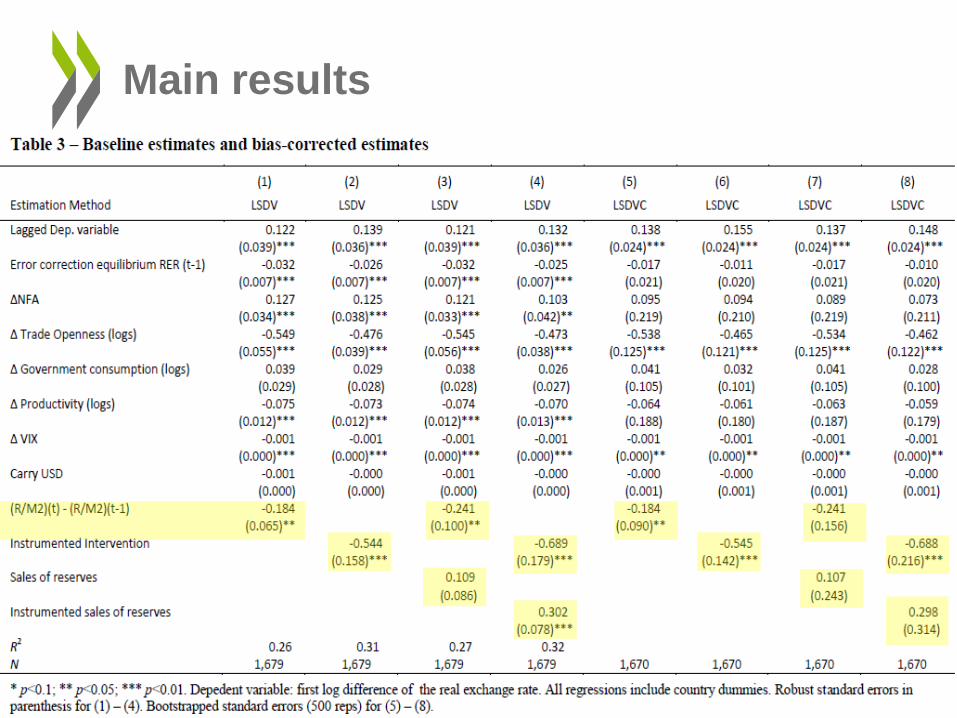

Second step error correction model

Main results

Robustness

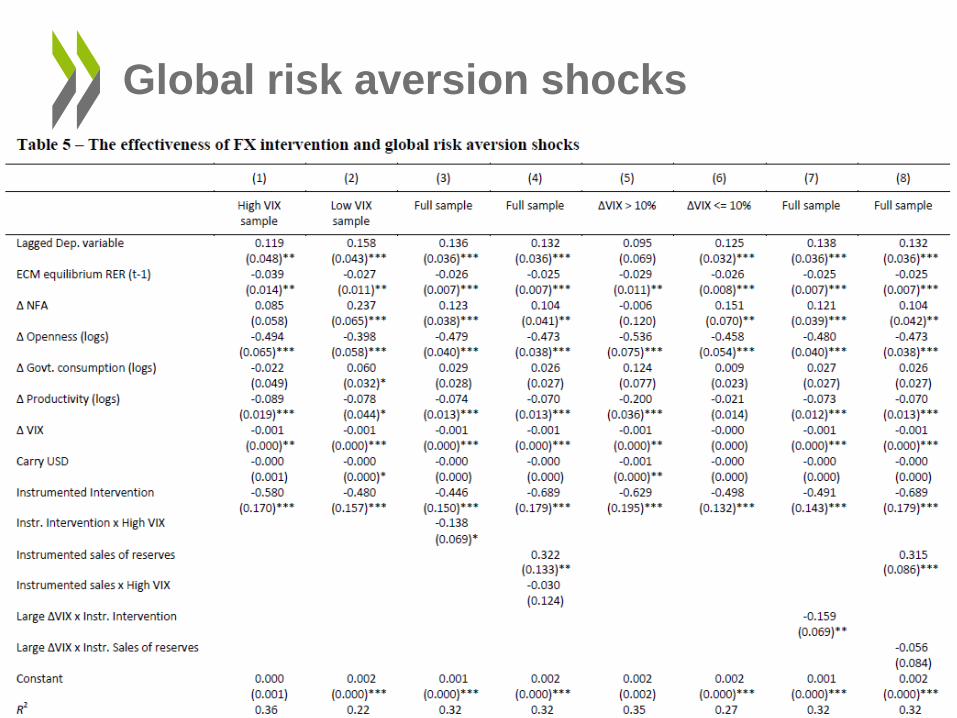

Global risk aversion shocks

Global USD shocks

Exploring the channels

• “Leaning against the wind” is on average effective.

• Little evidence of important asymmetries in terms of the

direction of interventions or directions of shocks

• No significant difference between what triggers deviation

(VIX versus global USD shocks)

• Interventions are more effective for large deviations

• Interventions are less effective in dollarized economies

(in line with the existence of a portfolio channel) and

under high inflation (in line with a signalling channel).

Conclusions