Embed Size (px)

Citation preview

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 1

NewBase 14 April 2014 Khaled Al Awadi

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Shell, BP said to sign LPG supply deals with Kuwait By Reuters

Royal Dutch Shell and BP have signed deals to supply Kuwait with liquefied natural gas (LNG) over the next few years, a Kuwait Petroleum Corp (KPC) official was quoted as saying on Sunday. Kuwait began importing LNG in 2009 and signed deals for Shell and Swiss-based trader Vitol to supply it during the peak power demand period from April to October over the last four summers.

Jamal Al-Loughani, deputy director of marketing at KPC, told the Kuwaiti Al-Seyassah newspaper that Shell andBP have been contracted to supply the OPEC member country over the next 5-6 summers. He said the total volume of super-cooled gas to be delivered between the two companies would be around 2.5 million tonnes a year.

Kuwait will sign another contract to buy LNG from a third company later this week, he said, without elaborating.Surging air conditioning demand in the hot Middle Eastern summer and a lack of domestic supply means Kuwaitneeds to import more gas each year to feed its power plants.

Location: Mina Al-Ahmadi, Kuwait ,

Date: Commissioned August 2009

Owner: Kuwait National Petroleum Company

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 2

Background

Kuwait, as one of the world’s highest per-capita consumers of electricity, was unable to produce enough gas to generate the power it needed. Instead, the nation was relying on higher-cost crude oil to generate power. This was detrimental to both their economy and the environment. Working with Kuwait National Petroleum Company (KNPC), Excelerate Energy designed and constructed the Mina Al-Ahmadi GasPort (MAAGP). Located approximately 20 miles south of Kuwait City, MAAGP was Kuwait’s first LNG import terminal. The facility was intended to be an interim solution to bridge the gap between Kuwait’s existing natural gas needs and the future development of domestic gas reserves.

Solution

Using Excelerate Energy’s GasPort technology, an Energy Bridge FSRU is stationed at the existing Mina Al-Ahmadi South Jetty facility and delivers regasified LNG at a baseload rate of up to 500 million cubic feet per day (MMcf/d) through our high-pressure gas arm. In addition, the MAAGP incorporates an innovative shuttle tanker berth that provides for ship-to-ship LNG transfer and boil-off gas management capabilities between a conventional LNG carrier and the FSRU. This allows Excelerate Energy to keep the FSRU on station while receiving cargo deliveries of LNG from conventional carriers dockside, resulting in a flexible terminal that can provide seasonal baseload service to Kuwait.

Results

The many compelling features of the MAAGP include the short time span between inception and in-service and low capital investment. MAAGP was developed from concept to commercial operations in just 18 months. The capital cost for the project, even with extensive refurbishments and enhancements made to the existing jetty facilities, was significantly less than that of a land-based facility of similar capacity. With the added benefit of seasonal flexibility and the resultant cost savings, our company’s partnership with KNPC on this project was a natural fit.

Key Facts

• Kuwait’s first LNG receiving facility • GasPort dockside configuration • Baseload throughput capacity 500 MMcf/d with peak capacity of 600 MMcf/d • Seasonal facility planned for operations April through October • Direct access to processing facilities and other industrial consumers • Direct access to the Kuwait gas grid

The Future LNG plan for Kuwait is in the pipeline

Kuwait National Petroleum Co. (KNPC) has let a prefrontend engineering design and frontend engineering design contract for an LNG import and regasification terminal in Kuwait to unit of Foster Wheeler AG’s global engineering and construction group.

The terminal will have design sendout capacity of about 1.5 bcfd with four 180,000-cu-m, full-containment LNG storage tanks. The design also will allow for future expansions of as much as 3 bcfd and installation of four more equally sized LNG storage tanks.

The terminal is scheduled for completion in October with commercial operations starting in 2020.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 3

Kuwait signs $12 bn oil contracts, tenders others Source : AFP

The Kuwait National Petroleum Company on Sunday signed contracts worth $12 billion (nine billion euros) with three international consortia to upgrade two refineries and invited bids to build a new multi-billion-dollar refinery.State-owned KNPC's chief Mohammed al-Mutairi signed the contracts with the three consortia led by Britain's Petrofac (Frankfurt: A0HF9Y - news) , US Fluor and Japan's JGC

Corporation (Other OTC: JGCCF - news) . Most of the other companies in the consortia are South Korean.

Mutairi said the project is due to be completed in early 2018. The cost of the venture -- called the Clean Fuel Project -- is more than $13 billion if smaller preparatory contracts are added, lower than the previous estimated cost of $16.4 billion, project manager Abdullah al-Ajmi told AFP.

The contracts, the first mega project in the OPEC member's vital oil sector for 25 years, will upgrade two of the three

existing refineries by installing 37 advanced processing units that will reduce sulphur and carbon pollutants, Mutairi told reporters.

The current production capacity of the two refineries of Mina Al-Ahmadi and Mina Abdullah is around 730,000 barrels per day, while the capacity of Kuwait's third refinery at Shuaiba is 200,000 bpd. At the end of the project, the capacity of the two refineries will increase to 800,000 bpd, while Kuwait plans to shut the third refinery.

KNPC on Sunday began inviting bids for two of the five-package project to build a state-of-the-art refinery with a capacity of 615,000 bpd, project manager Khaled al-Awadhi told reporters. The two tenders are for marine works and storage tanks.

Next (Dusseldorf: NXG.DU - news) month, the company will tender the three main packages for building the body of the refinery, said Awadhi, adding that KNPC hopes to award all the five contracts in the first quarter of next year. The refinery, estimated to cost around $15 billion, is slated to come onstream in between the end of 2018 and the first quarter of 2019, Awadhi said.

Kuwait's refining capacity will reach over 1.4 million bpd from the current level of 930,000 bpd, when the projects are completed. Most of the production will be for export to Asian and European markets, he said.

The two projects have been repeatedly delayed because of political disputes between parliament and the government. The project to build a new refinery was scrapped by the government around five years ago, after five Japanese and South Korean companies were awarded contracts.

Lawmakers had opposed the plan complaining of a lack of transparency in the tendering process, but they have not raised objections to the new contracts.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 4

UN report adds urgency to UAE clean energy efforts April Yee , The National

The world must triple its use of clean energy and trim fossil fuels consumption to a third of current levels to avoid the worst effects of global warming, said a UN report released yesterday. The 2050 prescription from the UN Intergovernmental Panel for Climate Change places extra urgency on Abu Dhabi’s efforts to build the Arab world’s first civilian nuclear power plant and bring to life experimental technologies such as carbon burial. But it also casts a shadow on the income that has enabled those investments – the oil and gas sector that contributes 40 per cent of the nation’s GDP.

Delaying efforts to cut emissions could result in long-term costs in the economy and in temperature increases, said the report, which will help to guide representatives from 194 nations, including the UAE, when they meet next year to draft a plan to curb carbon emissions.

“2050 is 35 years away, which I view as long enough time to cut fossil fuels by a third and to triple renewables,” said Bob Bryniak, the chief executive of Golden Sands, a regional utilities consultancy. “The opportunity cost for not cutting the use of fossil fuels is very high. It is also

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 5

important that the above efforts start sooner rather than later, as a typical power plant lasts 25 to 35 years.”

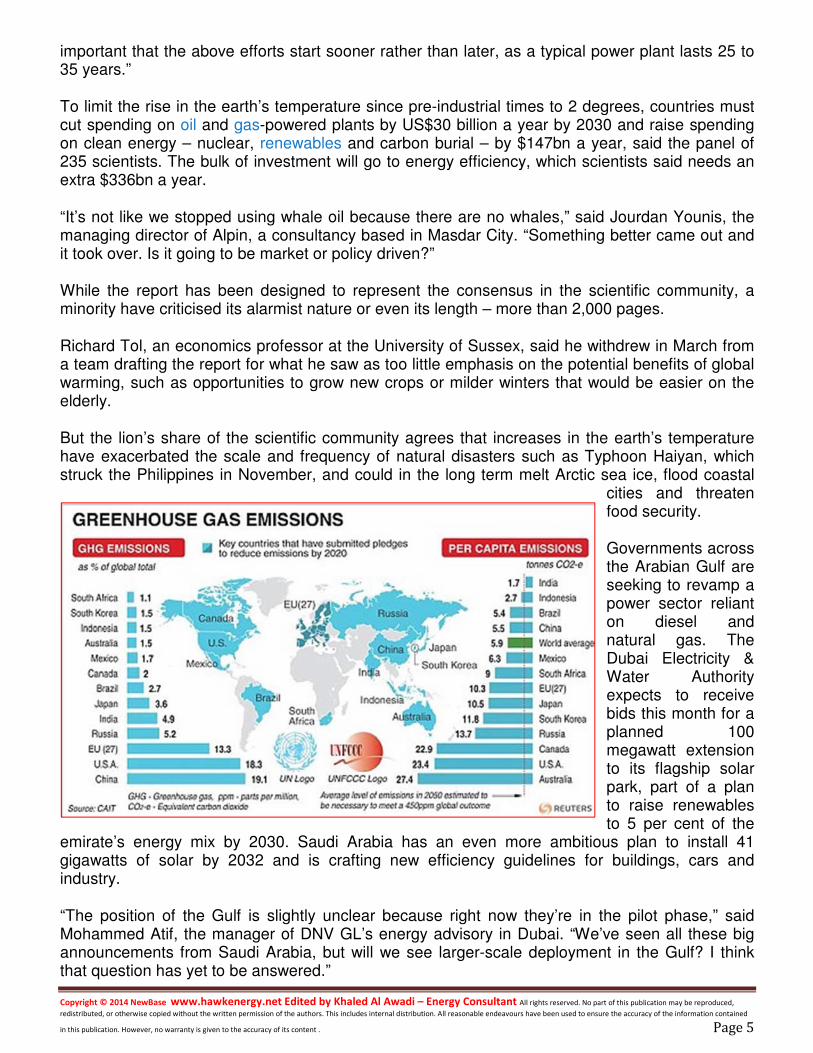

To limit the rise in the earth’s temperature since pre-industrial times to 2 degrees, countries must cut spending on oil and gas-powered plants by US$30 billion a year by 2030 and raise spending on clean energy – nuclear, renewables and carbon burial – by $147bn a year, said the panel of 235 scientists. The bulk of investment will go to energy efficiency, which scientists said needs an extra $336bn a year.

“It’s not like we stopped using whale oil because there are no whales,” said Jourdan Younis, the managing director of Alpin, a consultancy based in Masdar City. “Something better came out and it took over. Is it going to be market or policy driven?”

While the report has been designed to represent the consensus in the scientific community, a minority have criticised its alarmist nature or even its length – more than 2,000 pages.

Richard Tol, an economics professor at the University of Sussex, said he withdrew in March from a team drafting the report for what he saw as too little emphasis on the potential benefits of global warming, such as opportunities to grow new crops or milder winters that would be easier on the elderly.

But the lion’s share of the scientific community agrees that increases in the earth’s temperature have exacerbated the scale and frequency of natural disasters such as Typhoon Haiyan, which struck the Philippines in November, and could in the long term melt Arctic sea ice, flood coastal

cities and threaten food security.

Governments across the Arabian Gulf are seeking to revamp a power sector reliant on diesel and natural gas. The Dubai Electricity & Water Authority expects to receive bids this month for a planned 100 megawatt extension to its flagship solar park, part of a plan to raise renewables to 5 per cent of the

emirate’s energy mix by 2030. Saudi Arabia has an even more ambitious plan to install 41 gigawatts of solar by 2032 and is crafting new efficiency guidelines for buildings, cars and industry.

“The position of the Gulf is slightly unclear because right now they’re in the pilot phase,” said Mohammed Atif, the manager of DNV GL’s energy advisory in Dubai. “We’ve seen all these big announcements from Saudi Arabia, but will we see larger-scale deployment in the Gulf? I think that question has yet to be answered.”

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 6

Aramco unveils self-capture CO2 emission car http://www.saudigazette.com.sa

The UN Climate Change Conference, COP18 Doha 2012, is all about finding solutions for a sustainable future and Saudi Aramco, one of the participants in Saudi delegation, is presenting one of the most innovative ideas: a car that captures its own CO2 emissions.

The project was initiated in 2003, when engineers from Saudi Aramco started working on theoretical hypotheses to reduce the carbon impact of cars. After years of research and development, Saudi Aramco’s R&D team defined a promising and feasible concept to capture CO2 emissions from conventional car engines. That car, which is still a prototype at this moment, captures its own CO2 emission and stocks it onboard. The system enabling this performance

consists of 3 components: a carbon capture unit utilizing absorbent materials that can capture CO2 from the exhaust stream, a compression and storage system, and finally a unit recycling the heat produced by the vehicle to operate the whole carbon capture system onboard, without any additional or external energy supply. At this stage, the prototype captures 10 percent of its emissions, but the target is to reach 60 percent in the near future with a more compact configuration. The concept would not be complete without a solution to dispose of the CO2 stocked onboard, and the engineers have already determined some ways to dispose of the collected carbon dioxide. Drivers will upload the CO2 when they refuel their tank at petrol stations. Those stocks of carbon will then be used for EOR (enhanced oil recovery), sequestration and industrial uses or they will be converted on-site into alternative energy such as fuel or fuel additives. An expert from Aramco said “it is a challenging project and we are optimistic about implementing it and our aim is for the technology to be mass produced. This concept will have a bright future, if we come up with effective ways to use and convert the CO2 into useful purposes.”

NewBase Comments :-

We do not understand why everyone is going around with expanding the problem of CO2 emissions from cars , when it is so simple , just use EV that operate on rechargeable batteries or fuel cell ( Hydrogen fuel ) . With governmental degrees to enforce that 10% of card manufactured must be of EV type every year, in a very short time will displace all oil or gas cars from the world.

NGV or LPG or Bio diesel or LNG cars are only waste of resources that can be used to speed up the advancement in the EV technologies. In the above case Aramco, could have been wiser if it had introduced a green EV car rather than complication the CO2 emission issue .

A car prototype that captures its own CO2 emission.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 7

UK/Norway: Spike Exploration announces oil and gas

discovered in four wells , Source: Spike Exploration – Press release

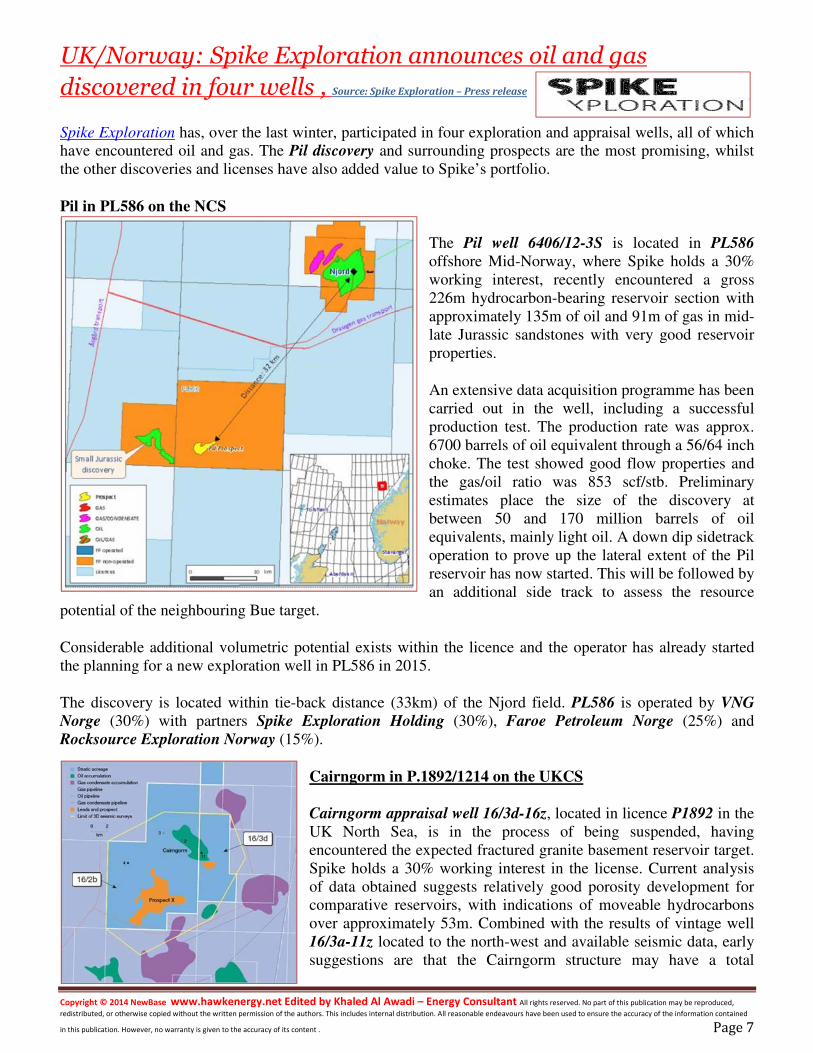

Spike Exploration has, over the last winter, participated in four exploration and appraisal wells, all of which have encountered oil and gas. The Pil discovery and surrounding prospects are the most promising, whilst the other discoveries and licenses have also added value to Spike’s portfolio.

Pil in PL586 on the NCS

The Pil well 6406/12-3S is located in PL586 offshore Mid-Norway, where Spike holds a 30% working interest, recently encountered a gross 226m hydrocarbon-bearing reservoir section with approximately 135m of oil and 91m of gas in mid-late Jurassic sandstones with very good reservoir properties.

An extensive data acquisition programme has been carried out in the well, including a successful production test. The production rate was approx. 6700 barrels of oil equivalent through a 56/64 inch choke. The test showed good flow properties and the gas/oil ratio was 853 scf/stb. Preliminary estimates place the size of the discovery at between 50 and 170 million barrels of oil equivalents, mainly light oil. A down dip sidetrack operation to prove up the lateral extent of the Pil reservoir has now started. This will be followed by an additional side track to assess the resource

potential of the neighbouring Bue target.

Considerable additional volumetric potential exists within the licence and the operator has already started the planning for a new exploration well in PL586 in 2015.

The discovery is located within tie-back distance (33km) of the Njord field. PL586 is operated by VNG

Norge (30%) with partners Spike Exploration Holding (30%), Faroe Petroleum Norge (25%) and Rocksource Exploration Norway (15%).

Cairngorm in P.1892/1214 on the UKCS

Cairngorm appraisal well 16/3d-16z, located in licence P1892 in the UK North Sea, is in the process of being suspended, having encountered the expected fractured granite basement reservoir target. Spike holds a 30% working interest in the license. Current analysis of data obtained suggests relatively good porosity development for comparative reservoirs, with indications of moveable hydrocarbons over approximately 53m. Combined with the results of vintage well 16/3a-11z located to the north-west and available seismic data, early suggestions are that the Cairngorm structure may have a total

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 8

hydrocarbon column of approx. 243m.

Well 16/3d-16z will be suspended with the intention for the group to return to the location at a subsequent date, with an appropriate rig and equipment to carry out a production test. The further assessment of well results will continue in the intervening period.

The Cairngorm discovery is located 5km to the north west of the East Brae field in the Viking Graben. The well was operated by Enquest Heather (45%) with partners Spike Exploration UK (30%) and Kufpec UK (25%).

Solberg in PL475 on the NCS

In PL475 offshore Mid-Norway, where Spike holds a 10% working interest, the Solberg well 6407/1-7 plus a sidetrack 6407/1-7A have been completed. The wells were drilled about 8km northeast of the Tyrihans field and 5km northeast of the 6407/1-6S gas/condensate discovery. In the main well bore gas/condensate was proven in two sandstone intervals with a total net vertical thickness of 12m in the Lange formation, and with a gross reservoir thickness of 16m. In the side track gas/condensate was proven in two sandstone intervals with a total net vertical thickness of 7m, and with a gross reservoir section of 13m.

The preliminary resource estimate for the Solberg

discovery within PL475 is in the range 6 to 25 million barrels of oil equivalents, whereof 1 to 5 million barrels is condensate. In addition, the revised preliminary resource estimate for the Rodriguez discovery within PL475 is in the range 6 to 38 million barrels of oil equivalents. The gas condensate ratio is expected to be similar in both Rodriguez and Solberg. Thus is the combined current resource estimate in PL475 between 12 and 63 million barrels of oil equivalents, mainly gas.

The Rodriguez and Solberg gas and condensate discoveries have been made in channel systems which are likely to extend across several licences and northwards into the PL590 in which Spike also holds a 10% interest.

PL475 is operated by Wintershall Norge (35%) with partners Spike Exploration Holding (10%), Faroe

Petroleum Norge (20%), Centrica Resources (Norge) (20%) and Moeco Oil & Gas Norge (15%).

Novus in PL645 on the NCS

The Novus-well 6507/10-2S in PL645, also offshore Mid-Norway, has been completed. Spike holds a 15% interest in the license. A 12.5m oil column and a 12m gas column were encountered in the Middle Jurassic Garn formation, with thicker reservoir rocks and better reservoir quality than expected.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 9

Preliminary estimation of the size of the discovery is between 6 and 16 million barrels of recoverable oil equivalent. The well result will be used to refine the geological model and de-risk additional prospects and leads in the licence for potential future drilling. The discovery is located some 9km to the south of the Heidrun oil field.

PL645 is operated by Faroe Petroleum

Norge (30%) with partners Spike

Exploration Holding (15%), Centrica

Resources (Norge) (40%), Concedo (10%) and Skagen44 (5%).

CEO of Spike Exploration, Bjørn

Inge Tønnessen commented: 'We in Spike are very pleased to see that our exploration efforts are showing positive results – the team has worked hard and dedicated to achieve this. The Pil-discovery is excellent with an exciting upside – we are very much looking forward to exploring the full potential of that license. Further, Spike has built a significant licence portfolio on the Norwegian Continental Shelf. In

addition to the significant resources discovered in the last four wells, two more firm wells within substantial potential are due to spud within the next 4 months. Spike’s dedicated search for oil and gas on the Norwegian Continental Shelf will continue in the years to come'.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 10

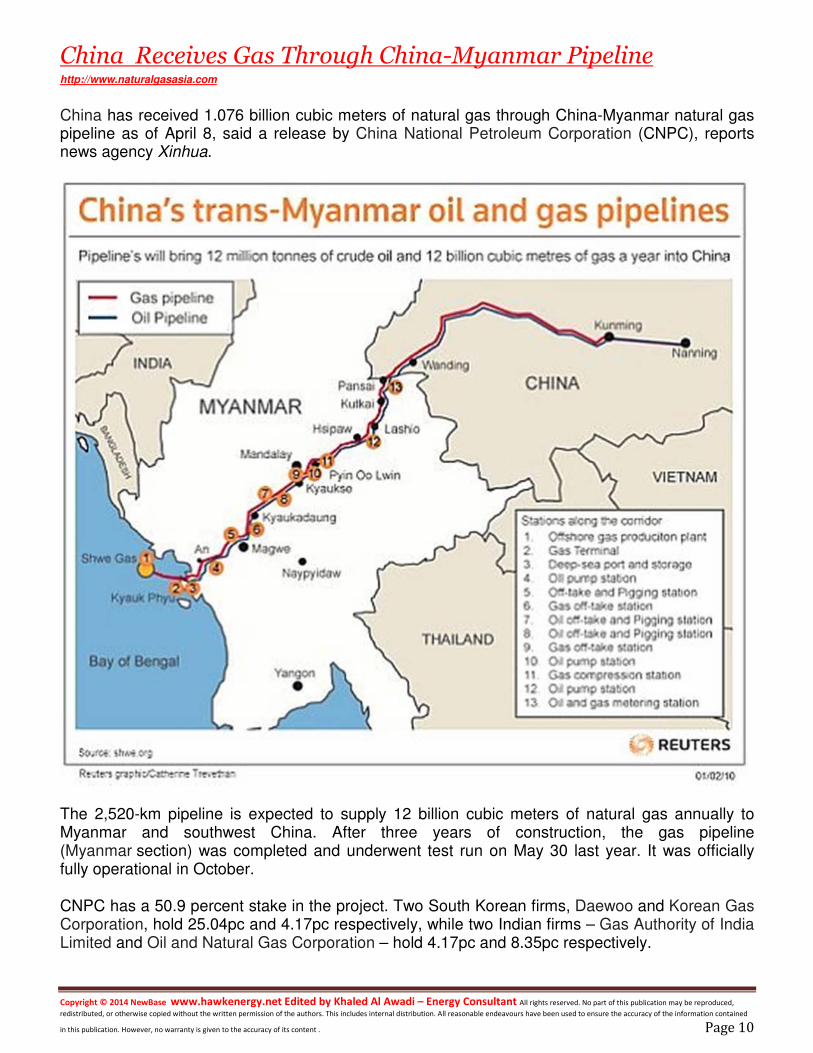

China Receives Gas Through China-Myanmar Pipeline http://www.naturalgasasia.com

China has received 1.076 billion cubic meters of natural gas through China-Myanmar natural gas pipeline as of April 8, said a release by China National Petroleum Corporation (CNPC), reports news agency Xinhua.

The 2,520-km pipeline is expected to supply 12 billion cubic meters of natural gas annually to Myanmar and southwest China. After three years of construction, the gas pipeline (Myanmar section) was completed and underwent test run on May 30 last year. It was officially fully operational in October.

CNPC has a 50.9 percent stake in the project. Two South Korean firms, Daewoo and Korean Gas Corporation, hold 25.04pc and 4.17pc respectively, while two Indian firms – Gas Authority of India Limited and Oil and Natural Gas Corporation – hold 4.17pc and 8.35pc respectively.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 11

NewBase Special Report :- THE GOLDEN AGE OF US NATURAL GAS - HOW WILL

PRODUCERS SUPPLY EXPANDING DEMAND? Rick Smead, RBN Energy

The golden years of natural gas abundance are off and running, with export projects, new industrial proposals, new power generation use, and expanded transportation use - all building on a perception of long-term abundant supply at reasonable prices. Does it all work out in the end? Do supply and demand balance at stable, affordable prices, even with a lot more demand? Today we examine the likelihood that gas producers can provide adequate supplies without causing significant upward pressure on prices.

This is analyzing the concerns voiced by some as to whether the natural gas renaissance is real and sustainable, with plenty of natural gas at reasonable prices. In Part I “Golden Years: The

Golden Age of U.S. Natural Gas,” we tackled the history of industry regulation before the shale era. In Golden Years: The Golden Age of U.S. Natural Gas Part II—How Much Gas Do We Need?, we developed a reasonable demand scenario out to 2025. [Why does our scenario go out to 2025? See the box insert for an explanation.] Our total US demand estimate of 92.5 Bcf/d represented an upward adjustment of 15.5 Bcf/d over EIA’s 2013 estimate (77 Bcf/d) . We knew EIA’s demand estimate was balanced with supply at reasonable, stable prices (real, constant-dollar prices staying below $6.00 until the mid-2030s, and even nominal prices staying below $6.00 into the mid-2020s). Our initial goal in this episode was to determine whether our higher total demand estimate could be met without gas prices jumping higher.

Well, what a difference a couple of weeks can make. Subsequent to that last blog installment, EIA issued the “early release” version of its next Annual Energy Outlook, AEO2014(ER). This new forecast starts to recognize much more demand than earlier versions, getting closer to a reasonable supply-demand target than we have seen EIA do in the past. Basically, by 2025 EIA

Source: EIA and RBN Energy

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 12

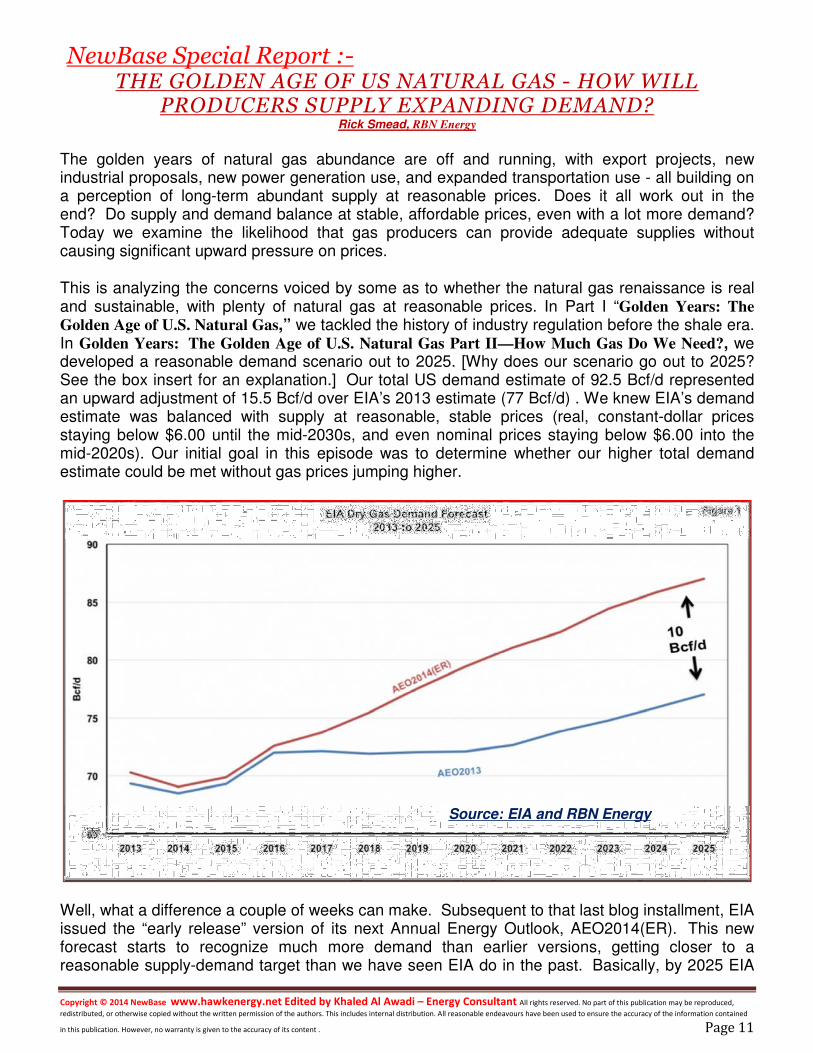

has added about 10 Bcf per day of demand, reflecting big increases in industrial use, power generation and LNG exports over last year’s forecast. Figure 1 compares the forecast total demand from 2013 to 2025.

As of 2025, EIA’s outlook last year, AEO2013 - blue line on the chart - had demand at 77.0 Bcf per day. The new release, AEO2014(ER) – red line on the chart - shows total demand of 87.0 Bcf per day – a lot closer to the estimate from our previous blog of 92.5 Bcf/d.

In the new EIA outlook, industrial load by 2025 goes from 21.4 to 23.0 Bcf per day. Power generation goes from 23.2 to 26.0 Bcf per day. Pipeline exports go from 1.4 to 2.3 Bcf per day, and LNG exports go from 2.9 to 7.0 Bcf per day. The residual demand for all other sources is pretty flat at 28.7 Bcf per day.

EIA shows its supply forecast meeting the total load just fine with domestic production. And, even in the way-out years beyond the 2025 reference, EIA shows supply meeting greatly expanded demand with nominal prices not reaching double-digits until the mid-2030s.

However, there are two wrinkles in that supply-demand balance: First, as we indicated, a reasonable 2025 demand scenario is still somewhat higher than EIA’s new forecast, by about 5.5 Bcf per day. Second, in moving from its AEO2013 supply-demand forecast to this more robust AEO2014(ER) forecast, EIA shows some upward pressure on prices, about 30 cents or 5% in 2025.

This brings us to supply. Is EIA fully recognizing what the industry can do without a lot of upward price pressure? Can the industry meet an additional 5.5 Bcf per day in 2025 without adding to EIA’s upward pressure? No, EIA is not fully recognizing industry performance, and yes, the industry can do a lot more. EIA has always been, and continues to be, conservative in catching up with what the industry can actually do. This is not necessarily a criticism, given EIA’s mandated mission, but it does say that we should look very carefully at EIA forecasts before relying upon them in making decisions.

Source: EIA and RBN Energy

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 13

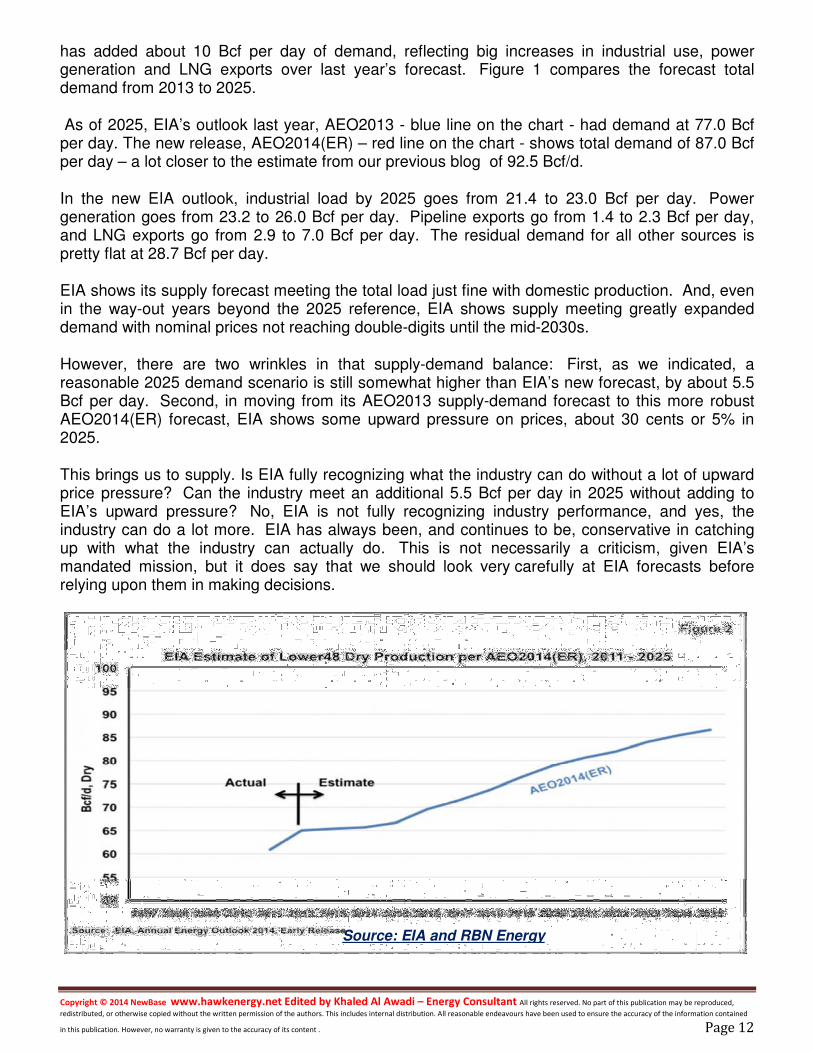

Let’s start with the production forecast used to balance with demand in AEO2014(ER). Figure 2 sets this out, starting at about 60 Bcf per day in 2011 and reaching 87 Bcf per day in 2025. That looks reasonable enough, right? The two years of actual history at the beginning of the study are succeeded by slight flattening of growth, but then by steady growth to meet demand.

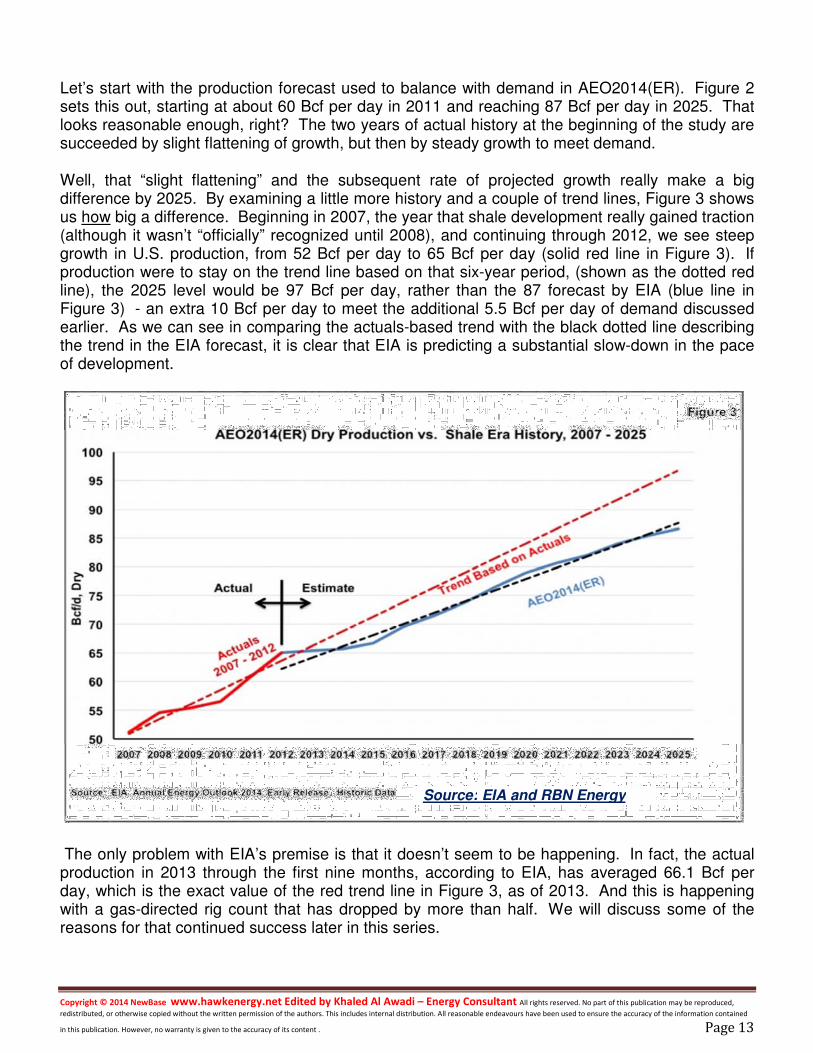

Well, that “slight flattening” and the subsequent rate of projected growth really make a big difference by 2025. By examining a little more history and a couple of trend lines, Figure 3 shows us how big a difference. Beginning in 2007, the year that shale development really gained traction (although it wasn’t “officially” recognized until 2008), and continuing through 2012, we see steep growth in U.S. production, from 52 Bcf per day to 65 Bcf per day (solid red line in Figure 3). If production were to stay on the trend line based on that six-year period, (shown as the dotted red line), the 2025 level would be 97 Bcf per day, rather than the 87 forecast by EIA (blue line in Figure 3) - an extra 10 Bcf per day to meet the additional 5.5 Bcf per day of demand discussed earlier. As we can see in comparing the actuals-based trend with the black dotted line describing the trend in the EIA forecast, it is clear that EIA is predicting a substantial slow-down in the pace of development.

The only problem with EIA’s premise is that it doesn’t seem to be happening. In fact, the actual production in 2013 through the first nine months, according to EIA, has averaged 66.1 Bcf per day, which is the exact value of the red trend line in Figure 3, as of 2013. And this is happening with a gas-directed rig count that has dropped by more than half. We will discuss some of the reasons for that continued success later in this series.

Source: EIA and RBN Energy

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 14

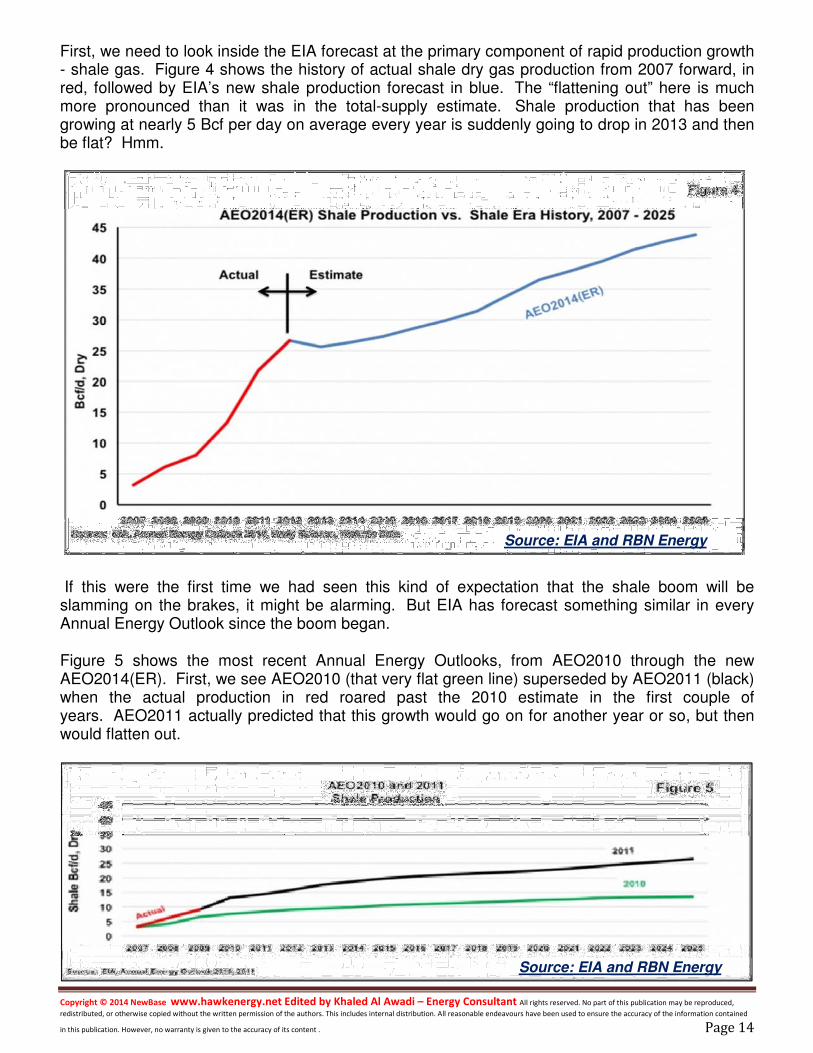

First, we need to look inside the EIA forecast at the primary component of rapid production growth - shale gas. Figure 4 shows the history of actual shale dry gas production from 2007 forward, in red, followed by EIA’s new shale production forecast in blue. The “flattening out” here is much more pronounced than it was in the total-supply estimate. Shale production that has been growing at nearly 5 Bcf per day on average every year is suddenly going to drop in 2013 and then be flat? Hmm.

If this were the first time we had seen this kind of expectation that the shale boom will be slamming on the brakes, it might be alarming. But EIA has forecast something similar in every Annual Energy Outlook since the boom began.

Figure 5 shows the most recent Annual Energy Outlooks, from AEO2010 through the new AEO2014(ER). First, we see AEO2010 (that very flat green line) superseded by AEO2011 (black) when the actual production in red roared past the 2010 estimate in the first couple of years. AEO2011 actually predicted that this growth would go on for another year or so, but then would flatten out.

Source: EIA and RBN Energy

Source: EIA and RBN Energy

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 15

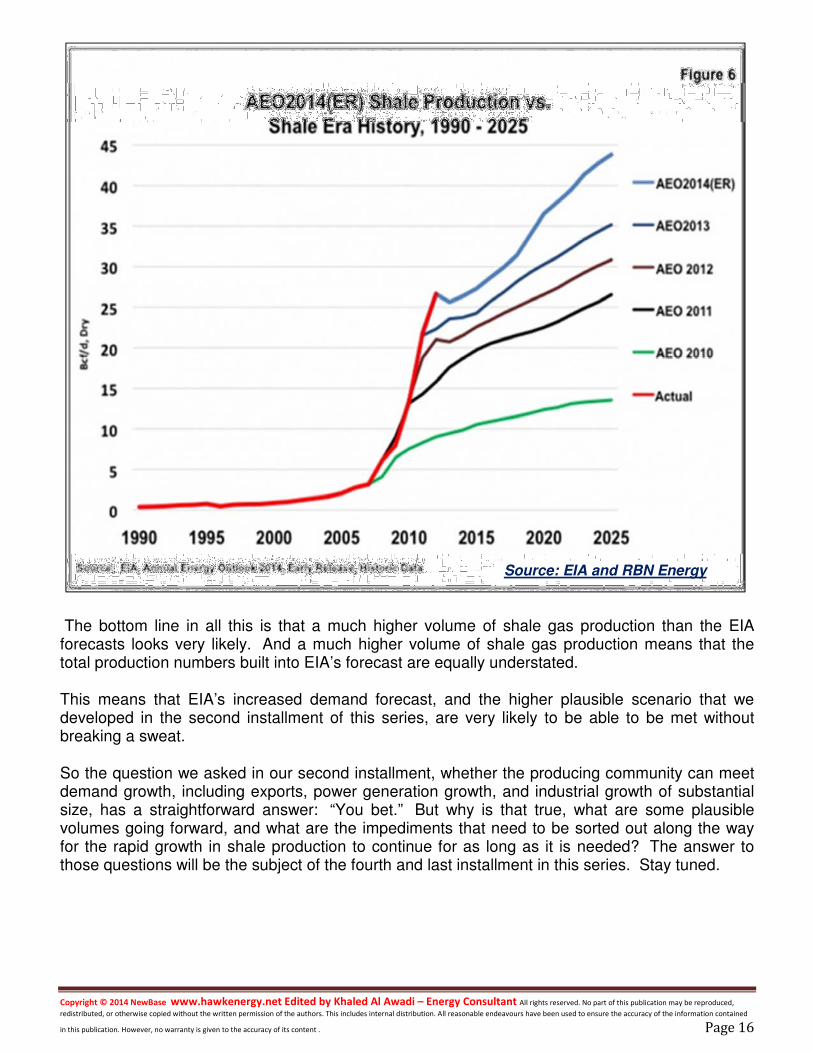

But actual production just wouldn’t cooperate with these pessimistic forecasts. By the time AEO2012 and 2013 rolled around, in the second block of Figure 5, the red “actual” curve had gone well past AEO2011, then had also jumped past AEO2012’s (brown) pessimistic view of continued progress,.

AEO2013 (dark blue) appeared to say “great work, now you’re ready to rest.” Wrong again. In the third block of Figure 5, we once again see the red actual-production curve leaping past the 2013 estimate.

And now we have the 2014 estimate, saying, one more time,that the brakes will be stomped upon, suddenly dropping some and then moving forward in stately fashion to respectable, but comparatively modest results. And even to achieve that stately growth, EIA predicts some upward price movement from its AEO2013 forecast, suggesting that the production involved will be dipping into the more expensive parts of the cost curve. Should we believe this? Do you believe it?

Rounding out this retrospective of EIA’s conservative and tentative recognition of shale abundance is the summation in Figure 6, showing the exponential growth in shale production from 1990 forward, with all these sequential “flattening” forecasts sticking out the side. This looks less like a forecast and more like a giant squid.

Source: EIA and RBN Energy

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 16

The bottom line in all this is that a much higher volume of shale gas production than the EIA forecasts looks very likely. And a much higher volume of shale gas production means that the total production numbers built into EIA’s forecast are equally understated.

This means that EIA’s increased demand forecast, and the higher plausible scenario that we developed in the second installment of this series, are very likely to be able to be met without breaking a sweat.

So the question we asked in our second installment, whether the producing community can meet demand growth, including exports, power generation growth, and industrial growth of substantial size, has a straightforward answer: “You bet.” But why is that true, what are some plausible volumes going forward, and what are the impediments that need to be sorted out along the way for the rapid growth in shale production to continue for as long as it is needed? The answer to those questions will be the subject of the fourth and last installment in this series. Stay tuned.

Source: EIA and RBN Energy

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 17

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Your partner in Energy Services

Khaled Malallah Al Awadi, MSc. & BSc. Mechanical Engineering (HON), USA ASME member since 1995 Emarat member since 1990

Energy Services & Consultants Mobile : +97150-4822502

Khaled Al Awadi is a UAE National with a total of Khaled Al Awadi is a UAE National with a total of Khaled Al Awadi is a UAE National with a total of Khaled Al Awadi is a UAE National with a total of 24 years24 years24 years24 years of experience in theof experience in theof experience in theof experience in the Oil & Gas sector. Currently working as Oil & Gas sector. Currently working as Oil & Gas sector. Currently working as Oil & Gas sector. Currently working as

Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for

the GCC area via Hawk Energy Service as a UAE operations the GCC area via Hawk Energy Service as a UAE operations the GCC area via Hawk Energy Service as a UAE operations the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations base , Most of the experience were spent as the Gas Operations base , Most of the experience were spent as the Gas Operations base , Most of the experience were spent as the Gas Operations

Manager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years , heManager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years , heManager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years , heManager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years , he has developed has developed has developed has developed

great experiences in the designing & constructinggreat experiences in the designing & constructinggreat experiences in the designing & constructinggreat experiences in the designing & constructing of gas pipelines, gas metering & regulating stations and in the engineering of supply of gas pipelines, gas metering & regulating stations and in the engineering of supply of gas pipelines, gas metering & regulating stations and in the engineering of supply of gas pipelines, gas metering & regulating stations and in the engineering of supply

routes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements along with many Mroutes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements along with many Mroutes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements along with many Mroutes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements along with many MOUs for OUs for OUs for OUs for

the local authorities. He has becomethe local authorities. He has becomethe local authorities. He has becomethe local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE anda reference for many of the Oil & Gas Conferences held in the UAE anda reference for many of the Oil & Gas Conferences held in the UAE anda reference for many of the Oil & Gas Conferences held in the UAE and Energy program broadcasted Energy program broadcasted Energy program broadcasted Energy program broadcasted

internationally , via GCC leading satelliteinternationally , via GCC leading satelliteinternationally , via GCC leading satelliteinternationally , via GCC leading satellite ChannelsChannelsChannelsChannels . . . .

NewBase : For discussion or further details on the news above you may contact us on +971504822502 , Dubai , UAE

NewBase 14 April 2014 K. Al Awadi