Embed Size (px)

Citation preview

Overview Equity Market Overview 1Valuations 2

Publicly Traded Companies 4

C-Store Trends Margins 6Government and Regulatory 8

Recent M&A Activity 10

Segment Focus: Grocery Stores 12

Fuel Pricing & Supply Charts 14

About Mercer Capital 17

Q1: Motor Fuels

Q2: Grocery Stores

Q3: Alternative Fuels & Transportation

Q4: Foodservices

2016

www.mercercapital.com

VALUE FOCUSConvenience Stores

SEGMENT FOCUS Grocery Stores

© 2016 Mercer Capital // www.mercercapital.com 1

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

During the three months ending March 2016, equity market pricing for the convenience store index remained essentially

flat, outperforming the Russell 2000 which fell 2.2% during the quarter. Performance among individual index participants

was mixed. TA continued to endure a steep price decline (-27.7%) as it failed to meet fourth quarter revenue and earnings

expectations. CASY and CST posted relatively smaller declines of 5.2% and 1.9%, respectively. In comparison, CASY’s

stock posted a 17.3% increase during the fourth quarter of 2015. The contrasting first quarter decline is attributable to

declining same-store sales during the first part of 2016. The grocery store index posted a 6.7% decrease during the

quarter. This decline was largely led by Kroger (KR) which posted an 8.7% decrease, spurred by lowering its same-

store sales expectations. KR has the largest market capitalization in our grocery index. The fast food index posted a

quarterly increase of 7.0%. With the exceptions of CMG and JACK, performance was up across the board.

70

80

90

100

110

120

Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16

MCM C-Store Index MCM Grocery Index MCM Food Franchise Index Russell 2000 3/31/15= 100

C-Store, Grocery Store, & QSR Stock Indices

OverviewEquity Market Overview

Data Source: S&P Global Market Intelligence / Bloomberg

© 2016 Mercer Capital // www.mercercapital.com 2

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

4

5

6

7

8

9

10

11

12

Q1 2011

Q2 Q3 Q4 Q1 2012

Q2 Q3 Q4 Q1 2013

Q2 Q3 Q4 Q1 2014

Q2 Q3 Q4 Q1 2015

Q2 Q3 Q4 Q1

Mid-Point

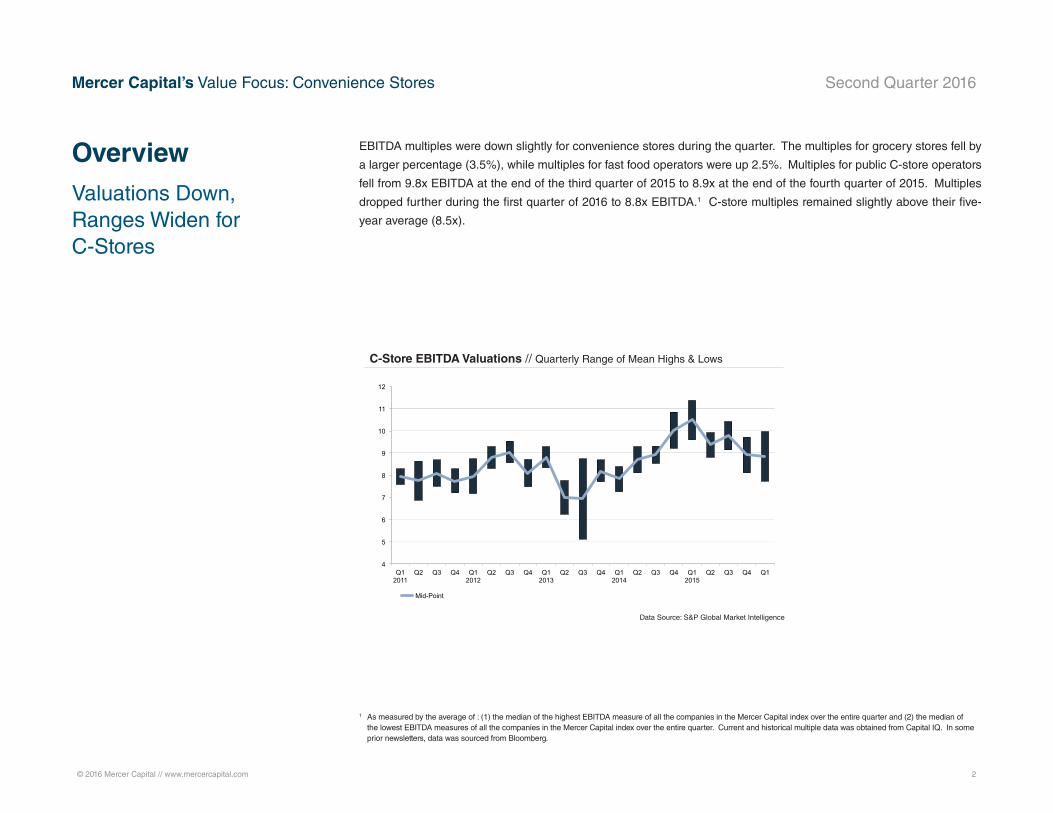

C-Store EBITDA Valuations // Quarterly Range of Mean Highs & Lows

Data Source: S&P Global Market Intelligence

EBITDA multiples were down slightly for convenience stores during the quarter. The multiples for grocery stores fell by

a larger percentage (3.5%), while multiples for fast food operators were up 2.5%. Multiples for public C-store operators

fell from 9.8x EBITDA at the end of the third quarter of 2015 to 8.9x at the end of the fourth quarter of 2015. Multiples

dropped further during the first quarter of 2016 to 8.8x EBITDA.1 C-store multiples remained slightly above their five-

year average (8.5x).

1 As measured by the average of : (1) the median of the highest EBITDA measure of all the companies in the Mercer Capital index over the entire quarter and (2) the median of the lowest EBITDA measures of all the companies in the Mercer Capital index over the entire quarter. Current and historical multiple data was obtained from Capital IQ. In some prior newsletters, data was sourced from Bloomberg.

OverviewValuations Down, Ranges Widen for C-Stores

© 2016 Mercer Capital // www.mercercapital.com 3

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

Fast Food (QSR) EBITDA Valuations // Quarterly Range of Mean Highs & Lows

9

10

11

12

13

14

15

16

17

Q1 2011

Q2 Q3 Q4 Q1 2012

Q2 Q3 Q4 Q1 2013

Q2 Q3 Q4 Q1 2014

Q2 Q3 Q4 Q1 2015

Q2 Q3 Q4 Q1 2016

Mid-Point

Data Source: S&P Global Market Intelligence

3

4

5

6

7

8

9

Q1 2011

Q2 Q3 Q4 Q1 2012

Q2 Q3 Q4 Q1 2013

Q2 Q3 Q4 Q1 2014

Q2 Q3 Q4 Q1 2015

Q2 Q3 Q4 Q1 2016

Mid-Point

Grocery Store EBITDA Valuations // Quarterly Range of Mean Highs & Lows

Data Source: S&P Global Market Intelligence

© 2016 Mercer Capital // www.mercercapital.com 4

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

Ticker

Stock Price at 3/31/16

LTM Price Range Equity Market

CapEnterprise

Value

Revenue EBITDA EBITDA Margins

High Low LTM 2016 Est.

2017 Est. LTM

2016 Est.

2017 Est. LTM

2016 Est.

2017 Est.

Convenience Stores

Alimentation Couche Tard Inc ANCUF $43.97 $47.22 $37.00 $24,885 $27,087 $33,810 $34,734 $35,180 $2,004 $1,909 $2,290 5.9% 5.5% 6.5%

Casey's General Stores Inc CASY $120.22 $129.29 $80.44 $4,689 $5,535 $7,299 $7,754 $7,140 $549 $470 $558 7.5% 6.1% 7.8%

TravelCenters of America LLC TA $9.40 $18.10 $6.41 $365 $1,117 $5,851 $6,137 $6,132 $151 $155 $129 2.6% 2.5% 2.1%

CST Brands Inc CST $39.08 $44.58 $29.68 $2,955 $4,411 $11,444 $9,776 $10,152 $476 $416 $402 4.2% 4.3% 4.0%

Murphy USA Inc MUSA $60.74 $73.64 $47.73 $2,532 $3,022 $12,790 $13,172 $12,765 $342 $369 $406 2.7% 2.8% 3.2%

Average C-Stores $7,085 $8,235 $14,239 $14,315 $14,274 $704 $664 $757 4.6% 4.2% 4.7%

Median C-Stores $2,955 $4,411 $11,444 $9,776 $10,152 $476 $416 $406 4.2% 4.3% 4.0%

Grocery Stores

Fresh Market Inc/The TFM $23.42 $41.70 $17.81 $1,099 $1,131 $1,818 $1,755 $1,857 $169 $188 $193 9.3% 10.7% 10.4%

Village Super Market Inc VLGEA $26.08 $33.30 $23.05 $369 $415 $1,594 na na $67 na na 4.2% na nm

SpartanNash Co SPTN $21.53 $33.34 $17.57 $809 $1,357 $7,847 $7,680 $7,699 $197 $225 $231 2.5% 2.9% 3.0%

Weis Markets Inc WMK $43.95 $49.16 $37.14 $1,182 $1,182 $2,877 na na $161 na na 5.6% na nm

Ingles Markets Inc IMKTA $43.89 $57.43 $31.77 $889 $1,814 $3,765 $3,810 $3,761 $237 $241 $239 6.3% 6.3% 6.4%

Whole Foods Market Inc WFM $33.36 $51.70 $28.07 $11,639 $11,704 $15,388 $15,420 $15,963 $1,300 $1,405 $1,349 8.4% 9.1% 8.4%

SUPERVALU Inc SVU $6.78 $12.00 $3.94 $1,797 $4,511 $17,947 $17,826 $17,601 $769 $774 $779 4.3% 4.3% 4.4%

Kroger Co/The KR $41.71 $42.63 $27.17 $40,292 $51,551 $108,872 $108,541 $109,914 $5,608 $5,096 $5,686 5.2% 4.7% 5.2%

Average Grocery Stores $7,260 $9,208 $20,013 $25,839 $26,132 $1,064 $1,322 $1,413 5.7% 6.4% 6.3%

Median Grocery Stores $1,141 $1,586 $5,806 $11,550 $11,831 $217 $508 $509 5.4% 5.5% 5.8%

Source: Bloomberg

Publicly Traded Companies

© 2016 Mercer Capital // www.mercercapital.com 5

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

Ticker

Stock Price at 3/31/16

LTM Price Range Equity Market

CapEnterprise

Value

Revenue EBITDA EBITDA Margins

High Low LTM 2016 Est.

2017 Est. LTM

2016 Est.

2017 Est. LTM

2016 Est.

2017 Est.

Fast Foods (QSR)

McDonald's Corp MCD $117.25 $126.96 $85.41 $106,324 $130,446 $25,413 $25,331 $24,153 $8,701 $8,781 $9,201 34.2% 34.7% 38.1%

Wendy's Co/The WEN $10.70 $11.50 $8.33 $2,925 $5,328 $1,908 $1,871 $1,320 $383 $396 $386 20.1% 21.2% 29.2%

Yum! Brands Inc YUM $72.57 $94.22 $64.58 $30,478 $34,455 $13,105 $13,195 $13,464 $2,668 $2,744 $2,977 20.4% 20.8% 22.1%

Dunkin' Brands Group Inc DNKN $42.32 $55.77 $36.21 $3,921 $6,374 $811 $810 $851 $365 $416 $448 45.0% 51.3% 52.7%

Krispy Kreme Doughnuts Inc KKD $15.07 $20.45 $12.90 $950 $962 $514 $494 $520 $66 $67 $73 12.9% 13.5% 14.0%

Panera Bread Co PNRA $194.78 $220.44 $162.07 $4,817 $5,223 $2,682 $2,686 $2,809 $377 $392 $404 14.1% 14.6% 14.4%

Chipotle Mexican Grill Inc CMG $479.85 $758.61 $399.14 $14,676 $14,676 $4,501 $4,513 $4,367 $894 $884 $415 19.9% 19.6% 9.5%

Jack in the Box Inc JACK $76.38 $97.10 $61.78 $2,733 $3,448 $1,540 $1,543 $1,607 $287 $291 $321 18.6% 18.9% 19.9%

Restaurant Brands International Inc QSR $37.21 $44.12 $29.16 $8,398 $20,417 $4,050 $4,031 $4,104 $1,368 $1,627 $1,713 33.8% 40.4% 41.7%

Sonic Corp SONC $32.18 $35.27 $22.54 $1,586 $2,092 $612 $605 $630 $165 $164 $178 27.0% 27.0% 28.2%

Average Fast Foods $17,681 $22,342 $5,514 $5,508 $5,382 $1,527 $1,576 $1,612 24.6% 26.2% 27.0%

Median Fast Foods $4,369 $5,851 $2,295 $2,279 $2,208 $380 $406 $410 20.2% 21.0% 25.2%

Source: Bloomberg

Publicly Traded Companies (continued)

© 2016 Mercer Capital // www.mercercapital.com 6

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

According to OPIS, nationwide retail gasoline margins ended the first quarter of 2016 at 12.8 cents per gallon, down from

24.8 cents per gallon 12 weeks earlier, and below the historical five-year average of 19.7 cents.2 Between the end of

the first quarter and the time of this publication, retail fuel margins have rebounded to approximately 25 cents per gallon,

as shown in the chart below. Fuel retailers are facing a difficult environment in which retail price increases cannot keep

pace with wholesale price increases. Fuel prices increased approximately a penny per day during March, but remain

at their lowest levels since 2009. Diesel margins ended the fourth quarter at 26.9 cents per gallon, down from a 54.2

cent margin twelve weeks earlier. The chart below presents the relationship between retail gasoline prices and margin.

C-Store TrendsMargins

2 National Association of Convenience Stores 2016 Retail Fuels Report.

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

1999 2001 2003 2005 2007 2009 2011 2013 2015 May '15

July '15

Sept '15

Nov '15

Jan '16

Mar '16

May '16

July '16

Gasoline Margin Retail Price Sources: NACS, OPIS & EIA

12 Months Ended March 31, 2016

Following the End of Q1

1999 - 2015

Gasoline Price and Spread Per Gallon

© 2016 Mercer Capital // www.mercercapital.com 7

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

C-Store TrendsMargins

Generally, over 70% of a C-store’s sales are motor fuels; however, fuel typically contributes only one-third of total

convenience store gross margin dollars. Despite periodic fluctuations, fuel margins have been relatively consistent on

an annual basis, averaging 19.7 cents per gallon for 2011 through 2015. There is a relatively modest delay between

the time crude prices increase and the time that pump prices rise. Similarly, retail price reductions typically lag when

wholesale prices drop. Retailers tend to reduce their markups when costs are escalating. Conversely, when costs are

declining, retailers tend to leave their pump prices elevated – leading to increased fuel margins – until competition forces

pump pricing downward. The time lag between cost changes and retail price adjustments, as well as the duration of

cost trends, are significant influencers of operator margin. On average, it costs retailers approximately 12 to 16 cents

to dispense a gallon of fuel. Given that the average five-year markup on gasoline was 19.7 cents, this translates to a

typical three to seven cents per gallon of bottom line profit.

© 2016 Mercer Capital // www.mercercapital.com 8

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

Swipe Fees

Walmart, Kroger, and Home Depot have recently filed lawsuits against Visa regarding the rules surrounding chip

debit cards. The retail giants argue that chip and PIN technology is a more secure payment method, and stores should

be able to require a PIN entry. As it stands, the stores are required to accept only a customer signature as validation.

Walmart also argues that the electronic signature verification is more expensive with Visa than the alternative PIN-

based method. Walmart Canada is no longer accepting Visa cards. Home Depot has also filed suit against MasterCard.

The Second Court of Appeals overturned the class-action settlement from 2012 related to Visa/MasterCard lawsuits

regarding the reasonableness of swipe fees. The court ruled that the settlement was inadequate.

H.R. 5465, which would repeal the 2010 Durbin Amendment, was recently introduced. A majority of retailers

(including NACS) are opposed to the repeal as it would likely lead to substantially higher fees being borne by retailers

and ultimately consumers. As it stands, the Durbin Amendment requires that banks impose fees that are reasonable and

proportionate to the cost of processing the transaction. According to the National Retail Federation, 89% of consumers

do not support a repeal of the Durbin Amendment. With the current laws in place, U.S. retailers still pay the highest

swipe fees in the world.

Wages

The DOL finalized its new overtime rules in May. The new rules are slated to go into effect in December 2016. The

current exemption (the dollar compensation level above which overtime rules would not apply) would nearly double

under the new statutes. The NACS and other retail consortiums are opposed to the new rules, and continue to actively

lobby for the rules to be withdrawn.

The Seattle minimum wage is set to increase to $15 per hour. Businesses with more than 500 employees have until

2017 to comply, but companies below this threshold will be given an additional three to four years. The International

Franchise Association argues that the relevant employee count for a franchisee’s business should be the local

franchisee’s employee count, but both the U.S. District Court and the Ninth Circuit Court of appeals determined that

the employee count of the franchisor will be considered the applicable amount. Opponents say that the lower court’s

decision inappropriately burdens franchisees which often operate more like small businesses. SCOTUS elected not

to hear an appeal regarding Seattle’s higher minimum wage law’s applicability to franchises. This effectively ends the

matter, but a similar suit has been filed in New York.

C-Store TrendsGovernment and Regulatory

© 2016 Mercer Capital // www.mercercapital.com 9

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

Tobacco

The FDA issued its new regulations in May. The new regulations put cigars, chewing tobacco, and most, if not

all, e-cigarette and vaping products under the purview of the FDA. Under the terms of the regulations, any product

introduced to the market after February 15, 2007 must file an application for permission to market and sell the product.

A slew of industry associations and individual retailers have filed suit in response alleging government overreach, and

there is some controversy regarding what actually constitutes a “tobacco product”. Some manufacturers utilize nicotine-

like substances obtained from non-tobacco plants to create the vaping liquid, so those manufacturers argue that they

should be exempt from the regulations. There is a movement in Congress to make the February 2007 date more current

in order to exclude additional products.

C-Store TrendsGovernment and Regulatory (continued)

© 2016 Mercer Capital // www.mercercapital.com 10

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

Recent M&A Activity

The following table summarizes M&A activity since the publication of our last newsletter. In addition to the major

transactions listed, there were several transactions involving 50 or fewer units since our last publication. 2014 and 2015

were busy in terms of M&A activity, but overall activity seems to be slowing.

Acquirer Target # of Stores Locations Comments

7-Eleven CST Brands, Inc. 79 c-stores California, WyomingTransaction completed; $408 million closing price

Island Energy Services

Chevron USA58 c-stores and certain other assets

HawaiiExpected to close during the second half of 2016; stations to be rebranded as Texaco stores

7-Eleven Imperial Oil 148 c-stores CanadaThe Esso-branded stations are expected to be converted to 7-Eleven's brand

Croton Holding Co. Par Mar Oil Co.

52 c-stores, several car washes, 16 quick-service restaurants

Ohio, Kentucky, West Virginia

NA

Sun Capital Partners affiliate

Admiral Petroleum 139 c-stores Michigan, Indiana NA

Dollar General Walmart Express 41 c-stores across 11 statesRepresents Dollar General's first foray into the fuel market

Travel Centers of America

Quaker Steak & Lube

10 operated sites; 40 franchisee or licensee sites

North America NA

Western RefiningNorthern Tier Energy

260+ c-storesMost in Minnesota and Wisconsin

Western Refining already owns a majority stake in Northern Tier Energy

Source: Convenience Store Decisions

© 2016 Mercer Capital // www.mercercapital.com 11

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

Acquirer Target # of Stores Locations Comments

Alimentation Couche-Tard

A/S Dansk Shell

286 company-operated stores; 197 dealer owned or operated stores; 211 automated sites

Denmark6th largest acquisition in Couche-Tard's history

NATravel Centers of America

NA NATA rejected a buyout offer from a private equity firm; deal value approximately $540 million

The Guess Corp. is planning to acquire c-stations

1,000+ c-stores North AmericaActual purchaser would be a Guess Corp. subsidiary; purchases will be over the course of the next year

CST Brands, Inc. accepting offers for a potential sale

3,000+ c-stores North AmericaBidders include 7-Eleven, Couche-Tard, several private equity firms

Pilot Flying J and Speedway LLC formed a joint venture - SFJ Southeast

121 travel centers Mostly Southeast41 locations contributed by Speedway; 79 locations contributed by Pilot Flying J

Loblaw Cos. Ltd. looking for buyers of its retail sites

212 retail fuel sites located adjacent to grocery stores

Canada NA

Global Partners, LP looking to sell assets 86 sites Northeastern market NA

Source: Convenience Store Decisions

Recent M&A Activity (continued)

© 2016 Mercer Capital // www.mercercapital.com 12

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

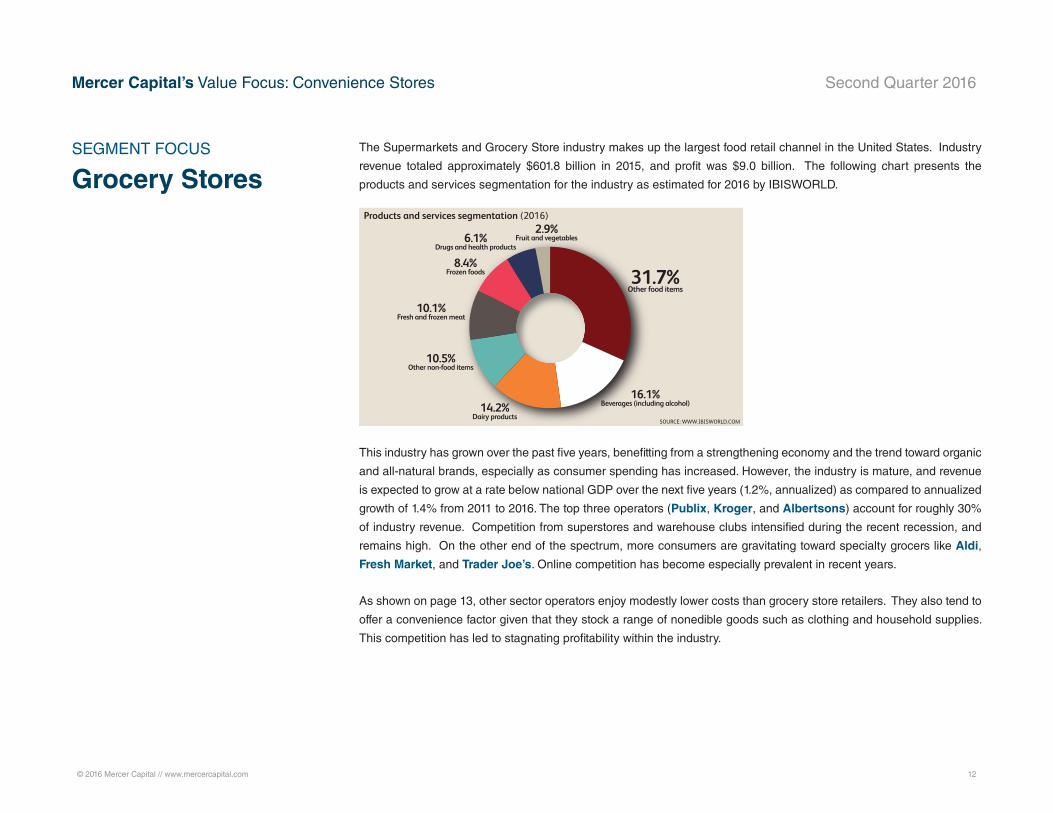

Grocery StoresSEGMENT FOCUS The Supermarkets and Grocery Store industry makes up the largest food retail channel in the United States. Industry

revenue totaled approximately $601.8 billion in 2015, and profit was $9.0 billion. The following chart presents the

products and services segmentation for the industry as estimated for 2016 by IBISWORLD.

This industry has grown over the past five years, benefitting from a strengthening economy and the trend toward organic

and all-natural brands, especially as consumer spending has increased. However, the industry is mature, and revenue

is expected to grow at a rate below national GDP over the next five years (1.2%, annualized) as compared to annualized

growth of 1.4% from 2011 to 2016. The top three operators (Publix, Kroger, and Albertsons) account for roughly 30%

of industry revenue. Competition from superstores and warehouse clubs intensified during the recent recession, and

remains high. On the other end of the spectrum, more consumers are gravitating toward specialty grocers like Aldi,

Fresh Market, and Trader Joe’s. Online competition has become especially prevalent in recent years.

As shown on page 13, other sector operators enjoy modestly lower costs than grocery store retailers. They also tend to

offer a convenience factor given that they stock a range of nonedible goods such as clothing and household supplies.

This competition has led to stagnating profitability within the industry.

WWW.IBISWORLD.COM Supermarkets & Grocery Stores in the US May 2016 4

% c

hang

e

4

-4

-2

0

2

2109 11 13 15 17 19Year

Per capita disposable income

SOURCE: WWW.IBISWORLD.COM

% c

hang

e

4

-2

-1

0

1

2

3

2208 10 12 14 16 18 20Year

Revenue Employment

Revenue vs. employment growth

Products and services segmentation (2016)

31.7%Other food items

8.4%Frozen foods

16.1%Beverages (including alcohol)

6.1%Drugs and health products

2.9%Fruit and vegetables

14.2%Dairy products

10.5%Other non-food items

10.1%Fresh and frozen meat

SOURCE: WWW.IBISWORLD.COM

Key Statistics Snapshot

Industry at a GlanceSupermarkets & Grocery Stores in 2016

Industry Structure Life Cycle Stage Mature

Revenue Volatility Low

Capital Intensity Low

Industry Assistance Low

Concentration Level Low

Regulation Level Medium

Technology Change Medium

Barriers to Entry Medium

Industry Globalization Low

Competition Level High

Revenue

$601.8bnProfit

$9.0bnWages

$59.7bnBusinesses

42,539

Annual Growth 16-21

1.2%Annual Growth 11-16

1.4%

Key External DriversPer capita disposable incomeAgricultural price indexUrban populationHealthy eating index

Market ShareThe Kroger Co. 16.1%

Albertsons LLC 9.7%

Publix Super Markets Inc. 5.6%

p. 25

p. 5

FOR ADDITIONAL STATISTICS AND TIME SERIES SEE THE APPENDIX ON PAGE 35

SOURCE: WWW.IBISWORLD.COM

© 2016 Mercer Capital // www.mercercapital.com 13

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

The industry is mature and continues to consolidate. Merger and acquisition activity among the larger players has been

high in the past few years. The Kroger Company merged with Harris Teeter in 2014 to expand within the Southeast and

Mid-Atlantic market areas and create a network of over 2,600 stores. Kroger also acquired Roundy’s in 2015 adding

151 stores to its network. Safeway and Albertsons merged in early 2015 to create a nationwide network of over 2,200

stores. This is an industry in which economies of scale are crucial; larger size helps enterprises better compete with

mass merchandisers by lowering per-unit costs. The grocery store industry has been facing increasing competition

from superstores and discount warehouse clubs, such as Wal-Mart. According to Wal-Mart’s 10-K for the fiscal year

ended January 31, 2016, grocery store segment revenues were 56% of total company revenues. Supermarkets are also

increasingly facing competition from convenience stores, food service providers, and dollar stores.

Grocery Stores (continued)

WWW.IBISWORLD.COM Supermarkets & Grocery Stores in the US May 2016 22

Competitive Landscape

Basis of Competition Internal competitionSupermarket and grocery store operators fiercely compete for the consumer’s dollar in an increasingly competitive food retailing sector. Due to the homogeneous nature of the goods sold at supermarkets, industry participants compete on price by offering discounts and promotions in addition to customer loyalty awards. Supermarkets rely on a large volume of sales with low markups and offer generic- or store-branded food items that are less expensive than branded products to drive sales. Most stores offer weekly savings on popular products to entice new consumers.

Other than lower prices, grocery stores must attract customers with the range and quality of products they offer. Industry players who offer an extended range of goods cater to a larger consumer

base from both low- and high-income households. However, if grocery stores price their high-quality products too high, they risk losing sales, even from high-income households. In the years following the recession, private label products have maintained their popularity among consumers. In particular, higher-end generic goods, such as Whole Foods’ 365 organic line of products, have enjoyed increasing sales as consumers seek affordability and value. Consequently, retailers that offer a range of private label products have benefited from improved sales and margins.

Supermarkets offer a variety of products and services, aside from traditional grocery and nonedible products. For instance, through its partnership with Starbucks, Safeway

Sector vs. Industry Costs

n Profi tn Wagesn Purchasesn Depreciationn Marketingn Rent & Utilitiesn Other

Average Costs of all Industries in sector (2016)

Industry Costs (2016)

0

20

40

60

Perc

enta

ge o

f rev

enue

80

100

SOURCE: WWW.IBISWORLD.COM

3.2 1.5

9.63.8 1.00.9

73.3

9.9

10.04.3 1.51.1

70.7

9.1

Level & Trend Competition in this industry is High and the trend is Increasing

Cost Structure Benchmarks continued

WWW.IBISWORLD.COM Supermarkets & Grocery Stores in the US May 2016 25

Player Performance The Kroger Company was founded in 1883 and is the largest grocery store chain in the United States. Headquartered in Cincinnati, the retailer employs 431,000 people throughout the United States. The company operates one retail segment, which includes its retail food and drug stores, multidepartment stores, jewelry stores and convenience stores. Along with its retail business, Kroger operates 38 manufacturing facilities where it produces a variety of private label goods, primarily baked goods and dairy products, which are sold at its retail outlets.

Kroger participates in the Supermarkets and Grocery Stores industry through its food and drug stores segment and multidepartment stores. The company operates more than 2,770 supermarkets and grocery stores across the United States. Kroger trades under 24

brand names across 35 states. Also, the company uses private labels as a way to differentiate its products and compete against other industry players. The company sells about 13,000 private-label items in three tiers: Private Selection is the premium-quality private label, offering food and beverages that cater to consumers’ specific gourmet tastes; the midrange Banner brand makes up the majority of private-label sales; and Kroger Value maintains an emphasis on price.

Over the past five years, Kroger has focused on driving sales productivity in markets that it already operates in, as well as expanding through strategic acquisitions. Since Kroger is the largest grocery retailer, it aims to acquire companies in locations where it can expand its market share. For instance, in 2011, the company acquired eight stores

Major CompaniesThe Kroger Co. | Albertsons LLC Publix Super Markets Inc. | Other Companies

68.6%Other

The Kroger Co. 16.1%

Albertsons LLC 9.7%

Publix Super Markets Inc. 5.6%

SOURCE: WWW.IBISWORLD.COM

Major players(Market share)

The Kroger Co. (industry-specifi c, excluding fuel centers) - fi nancial performance

Year*Revenue

($ million) (% change)Operating Income

($ million) (% change)

2011-12 72,742.4 N/C 2,146.8 N/C

2012-13 77,748.8 6.9 2,224.2 3.6

2013-14 76,666.0 -1.4 2,123.7 -4.5

2014-15 86,281.0 12.5 2,495.4 17.5

2015-16 91,310.0 5.8 2,973.0 19.1

2016-17** 96,628.4 5.8 3,285.4 10.5

*Year-end January; **Estimates SOURCE: ANNUAL REPORT

The Kroger Co. Market share: 16.1% Industry Brand Names Dillons Food 4 Less Kroger Owen’s Pay Less Super Markets Smith’s Ralph’s Harris Teeter

© 2016 Mercer Capital // www.mercercapital.com 14

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

Wholesale and Retail Prices

Motor Fuel and Brent Crude Price Fluctuation

$0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 $4.00 $4.50 $5.00

$20

$40

$60

$80

$100

$120

$140

Mar-11

Jun-1

1

Sep-11

Dec-11

Mar-12

Jun-1

2

Sep-12

Dec-12

Mar-13

Jun-1

3

Sep-13

Dec-13

Mar-14

Jun-1

4

Sep-14

Dec-14

Mar-15

Jun-1

5

Sep-15

Dec-15

Mar-16

Price/Gallon Price/Barrel

WTI Brent Gasoline Diesel

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

0.2

Mar-11

Jun-1

1

Sep-11

Dec-11

Mar-12

Jun-1

2

Sep-12

Dec-12

Mar-13

Jun-1

3

Sep-13

Dec-13

Mar-14

Jun-1

4

Sep-14

Dec-14

Mar-15

Jun-1

5

Sep-15

Dec-15

Mar-16

Price Volatility

Gasoline Brent Diesel

Data Source: Calculated by Mercer Capital from raw data obtained from the US Energy Information Administration (EIA.gov)

Data Source: Calculated by Mercer Capital from raw data obtained from the US Energy Information Administration (EIA.gov)

Fuel Pricing & Supply Charts

© 2016 Mercer Capital // www.mercercapital.com 15

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

U.S. Ending Stocks of Crude Oil

Thousand Barrels

Prime Supplier Sales Volumes

1,000,000

1,050,000

1,100,000

1,150,000

1,200,000

1,250,000

Jan-1

1

Apr-11

Jul-1

1

Oct-11

Jan-1

2

Apr-12

Jul-1

2

Oct-12

Jan-1

3

Apr-13

Jul-1

3

Oct-13

Jan-1

4

Apr-14

Jul-1

4

Oct-14

Jan-1

5

Apr-15

Jul-1

5

Oct-15

Jan-1

6

Apr-16

U.S. Ending Stocks of Crude Oil (Thousand Barrels)

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

Gas

Diesel

2010 2011 2012 2013 2014 2015 Oct '14

Nov '14

Dec '14

Jan '15

Feb '15

Mar '15

Apr '15

May '15

June '15

July '15

Aug '15

Sept '15

Oct '15

Nov '15

Dec '15

Jan '16

Feb '16

Mar '16

Apr '16

000'

s G

allo

ns/D

ay

Regular Mid-Grade Premium Diesel

Data Source: US Energy Information Administration (EIA.gov)

Data Source: US Energy Information Administration (EIA.gov)

Fuel Pricing & Supply Charts (continued)

© 2016 Mercer Capital // www.mercercapital.com 16

Mercer Capital’s Value Focus: Convenience Stores Second Quarter 2016

Non-Motor Fuel Prices

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

Mar-10

Jun-1

0

Sep-10

Dec-10

Mar-11

Jun-1

1

Sep-11

Dec-11

Mar-12

Jun-1

2

Sep-12

Dec-12

Mar-13

Jun-1

3

Sep-13

Dec-13

Mar-14

Jun-1

4

Sep-14

Dec-14

Mar-15

Jun-1

5

Sep-15

Dec-15

Mar-16

Price/Gallon

No. 2 Heating Oil Propane

Data Source: US Energy Information Administration (EIA.gov)

Fuel Pricing & Supply Charts (continued)

Percentage Change in Non-Motor Fuel Spread by Month

-12% -10% -8% -6% -4% -2% 0% 2% 4% 6% 8%

10%

1/4/20

16

1/11/2

016

1/18/2

016

1/25/2

016

2/1/20

16

2/8/20

16

2/15/2

016

2/22/2

016

2/29/2

016

3/7/20

16

3/14/2

016

3/21/2

016

3/28/2

016

% +/- in Heating Oil Spread % +/- Inc/Dec in Propane Spread

Data Source: US Energy Information Administration (EIA.gov)

Mercer CapitalConvenience Store Industry Services

Contact Us

Copyright © 2016 Mercer Capital Management, Inc. All rights reserved. It is illegal under Federal law to reproduce this publication or any portion of its contents without the publisher’s permission. Media quotations with source attribution are encouraged.

Reporters requesting additional information or editorial comment should contact Barbara Walters Price at 901.685.2120. Mercer Capital’s Industry Focus is published quarterly and does not constitute legal or financial consulting advice. It is offered as an

information service to our clients and friends. Those interested in specific guidance for legal or accounting matters should seek competent professional advice. Inquiries to discuss specific valuation matters are welcomed. To add your name to our mailing list

to receive this complimentary publication, visit our web site at www.mercercapital.com.

Mercer Capital provides the multi-unit retailing and QSR industries with corporate valuation, financial reporting, transaction advisory, and related services.

Industry Segments

Mercer Capital serves the following industry segments:

• Motor Fuels

• Grocery Stores

• Alternative Fuels & Consumer Transportation

• Foodservices

Mercer Capital Experience

• Family and management succession planning

• Buy-side and sell-side transaction advisory assistance

• Conflict resolution and litigation support

• Trust and estate planning

• Buy-sell agreement valuation, design, and funding advisory

Contact a Mercer Capital professional to discuss your needs in confidence.

Eden G. Stanton, CFA

901.270.7250

Timothy R. Lee, ASA

901.322.9740

MERCER CAPITAL

Memphis

5100 Poplar Avenue, Suite 2600

Memphis, Tennessee 38137

901.685.2120

Dallas

12201 Merit Drive, Suite 480

Dallas, Texas 75251

214.468.8400

Nashville

102 Woodmont Blvd., Suite 231

Nashville, Tennessee 37205

615.345.0350

www.mercercapital.com

BUSINESS VALUATION & FINANCIAL ADVISORY SERVICES