Embed Size (px)

Citation preview

Analysis of 2015 venture investment activity in Swedish private tech companies

Industrifonden Swedish Tech Funding Report 2015

2

Industrifonden is a Swedish venture capital fund, investing in early-stage tech and

life science growth companies. Founded in 1979, Industrifonden is a reinvesting

evergreen fund with SEK 4 billion (~$480M) in assets.

About Industrifonden.

industrifonden.com

@industrifonden

/company/industrifonden

Copyright Industrifonden

3

With 2015 in the books, we look back on a year where the Swedish

startup scene truly consolidated its position as a force to be reckoned

with. 2015 saw countless publications naming Sweden the new startup

center and records were broken over and over again.

As always, building a global company requires deep pockets and 2015

saw a massive influx of venture capital to Swedish tech companies

looking to do just that. In the wake of negative interest rates combined

with a number of high profile tech startups reaching unicorn status,

asset managers from all sectors and geographies turned to tech

companies in search of returns. Adding to this, a number of large

venture funds aiming to cover the Nordic tech scene launched during

the year, resulting in more capital invested and more deals per capita

than the rest of Europe’s top performing countries.

The last quarter of the year did show a cool-down in terms of larger

funding rounds, while the high levels of smaller rounds seen in Q2 and

Q3 remained and even increased further. Companies in the seed

stage had a range of investors to choose from – it was rather the later-

stage companies that could experience difficulties in raising their next

round. Whether this was just a small hiccup or a response to soaring

valuations in the tech sector combined with general apprehension in

capital markets following increased volatility will be determined in the

first half of 2016.

The year ended with a total of $1.1 billion invested across 175

disclosed funding rounds. More than 250 investors participated in

funding Swedish tech startups. The majority of the deals were made

by local angel investors and VC firms.

Summary.

Copyright Industrifonden

Note: This report only covers investment activity, not exits. Therefore, the terms ‘deal’ and ‘funding round’ are used interchangeably throughout the report.

4

Q4 Highlights

Copyright Industrifonden

5

Q4 brought a record number of disclosed investments, but also a notable

shift towards smaller rounds. Q4 saw 30 percent more funding rounds

compared to Q3 and the quarter accounted for 35 percent of all

disclosed deals in 2015.

However, the investment sizes plunged with an average Q4 funding

round size of $1.9M. This is a significant decrease, indicating a 65

percent drop compared to the average Q3 funding round. Noteworthy is

that it was not just the increase in smaller funding rounds that pushed

down Q4 averages. Looking at the top five largest deals for each

quarter, Q4 is at the very bottom in terms of deal sizes. Q4 is also at the

bottom in terms of median deal sizes, with a median round of $0.7M –

half the size of the Q2 median of $1.4M but closer to the Q3 median

round of $0.8M.

As total deal count shows, it is clear that interest in the Swedish tech

scene remains at record-high levels. The clear decrease of larger deals

in Q4 is noteworthy however, as it could be a first indication of a gap in

expectations between founders and institutional investors following

soaring valuations throughout the year.

Q4: More deals, less cash

0

10

20

30

40

50

60

70

Q1 Q2 Q3 Q4

Increasing number of deals…Deal count

0%

10%

20%

30%

40%

50%

60%

70%

Q1 Q2 Q3 Q4

…but less capital raised compared to Q2-Q3% of total

Copyright Industrifonden

6

2015: The juggernaut year

Copyright Industrifonden

7

$1.1B(SEK 9.4B) raised during 2015

175Funding rounds

$1MMedian deal size

2011Median year a company that received

investment during 2015 was founded

57%Increase in mentions of ’startup’ or ’start-up’

in Swedish media compared to 2014

Source: Industrifonden database, Dow Jones EMEA Venture Capital Report, Dealroom.co, Retriever

1.7xCapital invested per capita in Swedish tech

startups 2015 compared to the UK

Copyright Industrifonden

8

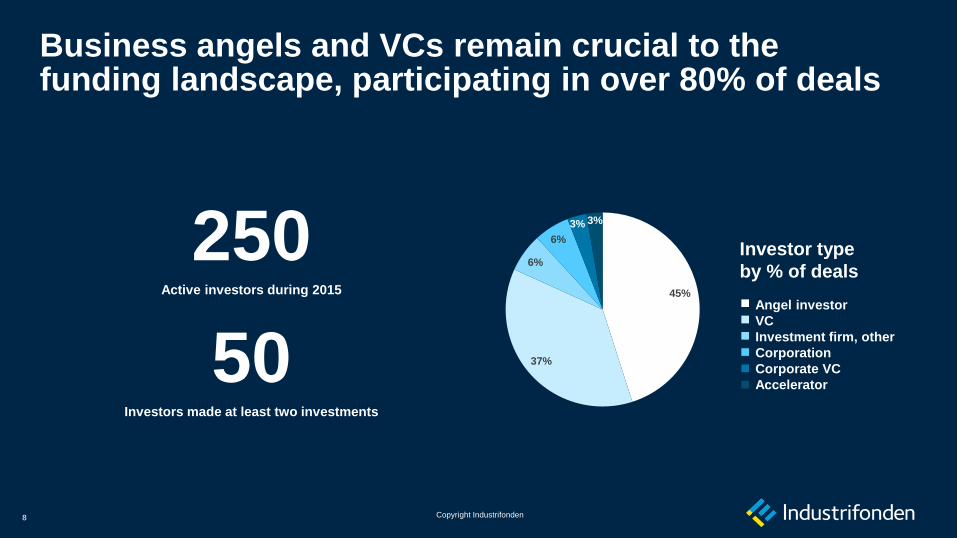

250Active investors during 2015

50Investors made at least two investments

Investor type

by % of deals

Angel investor

VC

Investment firm, other

Corporation

Corporate VC

Accelerator

45%

37%

6%

6%

3% 3%

Business angels and VCs remain crucial to the funding landscape, participating in over 80% of deals

Copyright Industrifonden

9

60%

Top 20 most active investors involved in 60% of all deals

Top 20 funding rounds make up 80% of total disclosed deal value

80%

Top 20 funding rounds as % of total deal value Top 20 most active investors’ deal count as % of total deal count

Copyright Industrifonden 2015Copyright Industrifonden

10

Quarterly breakdown: Increasing total deal count quarter-over-quarter, but fewer large funding rounds

Note: The inflated average (mean) deal size in Q2 2015 is mainly due to Spotify’s >$500m Series G financing

Deal count$M Deal count

0

10

20

30

40

50

60

70

0

2

4

6

8

10

12

14

16

Q1 2015 Q2 2015 Q3 2015 Q4 2015

Average deal size Median deal size Deal count

0

5

10

15

20

25

30

35

Q1 2015 Q2 2015 Q3 2015 Q4 2015

≤$1M $1.1 - 5M $5.1-25M >$25M

Copyright Industrifonden

11

Finance, Media, and SaaS most popular verticals by number of funding rounds

Top 3 verticals by deal count

12% 11% 11%

Note: Deal count as percentage of total

Software-as-a-Service (SaaS)MediaTechFinTech

Copyright Industrifonden

12

The international context

Copyright Industrifonden

13

Foreign investors active in later stages – founders rely on local investors for launch and early growth

Average share of

funding rounds

with foreign

participation 2015

Foreign

investors

by country

USA

UK

Rest of World

Germany

Denmark

Finland

32%

33%

25%

19%

10%

7%

6%

0

10

20

30

40

50

60

70

80

90

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

≤$1M $1.1 - 5M $5.1 - 25M >$25M

Funding rounds with foreign participation

Foreign participation % Total deal count

Deal count

Deal size

Copyright Industrifonden

14

Sweden ranks #1 in invested capital and deals per capita compared to peers

0

20

40

60

80

100

120

Sweden UK Germany France

$ raised per capita Q1-Q4 2015

0,000000

0,000002

0,000004

0,000006

0,000008

0,000010

0,000012

0,000014

Sweden UK France Germany

Deals per capita Q1-Q3 2015

Source: Industrifonden database, Dow Jones EMEA Venture Capital Reports 1Q-3Q 2015, Dealroom.co. Note: UK, France and Germany ranked top three in Europe on deal count and

capital raised. Data for amount raised for UK, Germany and France calculated as average of Dow Jones’ and Dealroom’s data for Q1-Q3 and Dealroom’s for Q4. Data for number of deals

for UK, France and Germany: Dow Jones. Differences in data collection methods and level of completeness may impact the comparison

Copyright Industrifonden

15

What’s included• This report covers disclosed venture investments in Swedish

private tech companies

• Analysis primarily based on proprietary database with 175

funding rounds from 2015, sorted on date of disclosure

• 10+ parameters including deal size, stage, investors and

vertical

• Both first-time and follow-on investments

• Deals are tracked in SEK. If originally reported in other

currencies, conversion is based upon exchange rate per date

of disclosure. Aggregate figures are subject to change due to

currency fluctuation

What’s not included• Investments in life science, med tech, bio tech, retail, and consulting

• Secondary investments and M&A deals

• Investments in public companies of any kind

• Grants, bank loans and other types of funding that is not intended to

result in ownership

For more information, contact:Björn Bergström, [email protected]

The information contained in this report has not been independently verified as to its accuracy. No representation or

warranty, express or implied, is given by Industrifonden or any of its directors, partners, officers, affiliates, employees,

advisers or agents as to the accuracy or completeness of the contents of this report or any other document or

information supplied or any opinions or projections expressed herein or therein, nor is any such party under any

obligation to update the report or correct any inaccuracies or omissions in it which may exist or become apparent.

Methodology

Copyright Industrifonden

Stay in touch.industrifonden.com

@industrifonden

/company/industrifonden