Embed Size (px)

Citation preview

EXPERIENCES WITH CROP INSURANCE IN INDIA

Risks and Agricultural Insurance

Evolution Insurance in India Performance of Yield and Weather Index Based InsuranceGap Between Supply and Demand for InsuranceConcluding Remarks and Way Forward

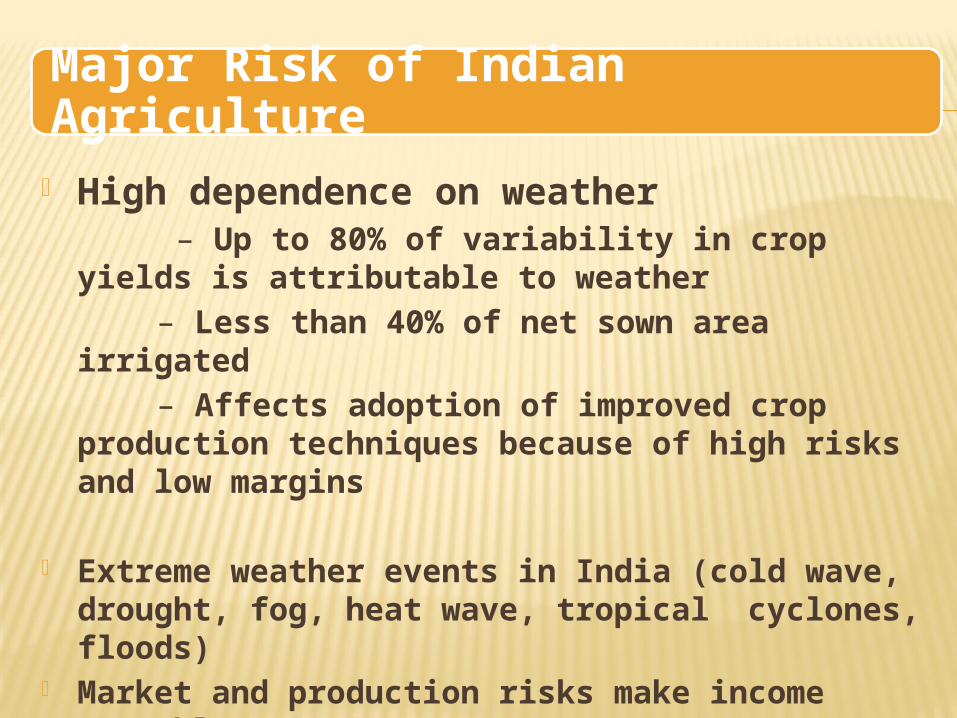

Major Risk of Indian Agriculture High dependence on weather – Up to 80% of variability in crop yields is

attributable to weather – Less than 40% of net sown area irrigated – Affects adoption of improved crop

production techniques because of high risks and low margins

Extreme weather events in India (cold wave,

drought, fog, heat wave, tropical cyclones, floods)

Market and production risks make income unstable

Access to formal financial services is limited

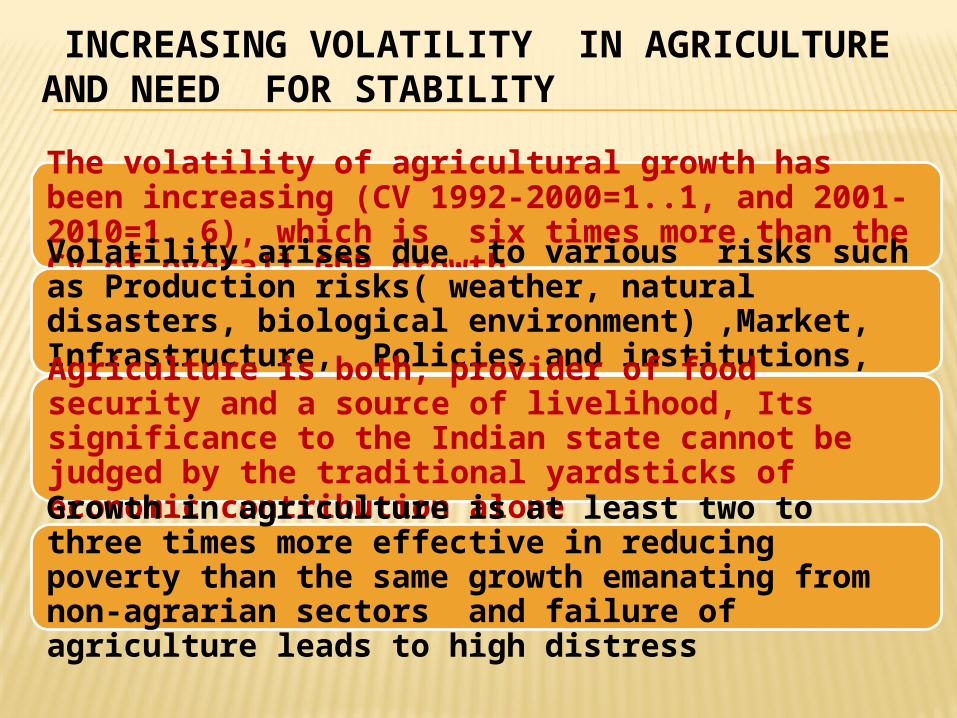

INCREASING VOLATILITY IN AGRICULTURE AND NEED FOR STABILITYThe volatility of agricultural growth has been increasing (CV 1992-2000=1..1, and 2001-2010=1..6), which is six times more than the CV of overall GDP growth .Volatility arises due to various risks such as Production risks( weather, natural disasters, biological environment) ,Market, Infrastructure, Policies and institutions, Politics etc. Agriculture is both, provider of food security and a source of livelihood, Its significance to the Indian state cannot be judged by the traditional yardsticks of economic contribution aloneGrowth in agriculture is at least two to three times more effective in reducing poverty than the same growth emanating from non-agrarian sectors and failure of agriculture leads to high distress

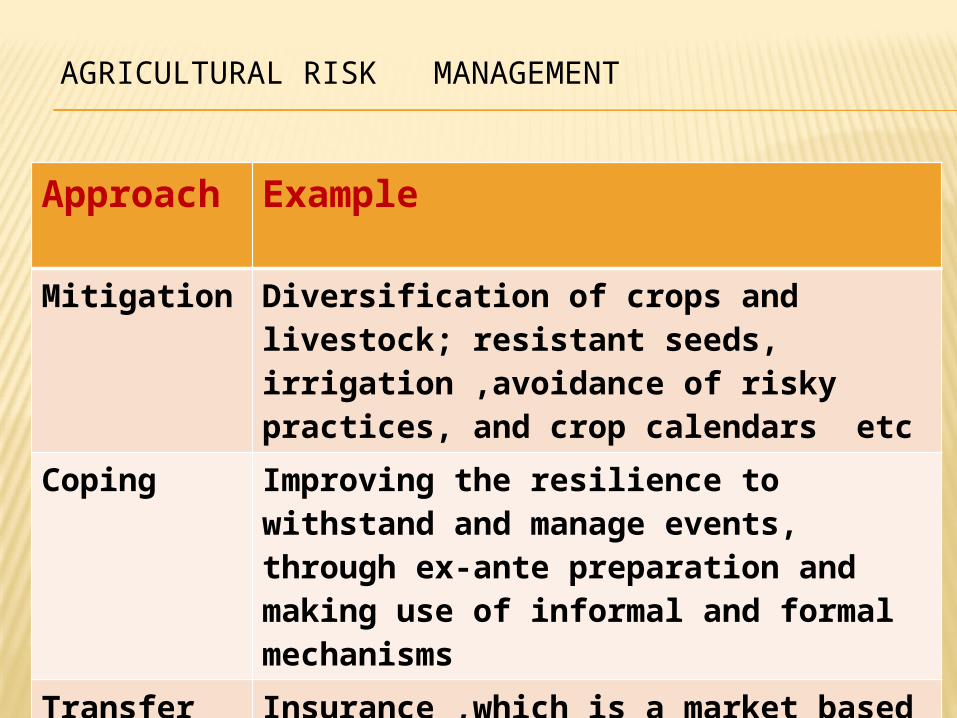

AGRICULTURAL RISK MANAGEMENT

Approach Example

Mitigation Diversification of crops and livestock; resistant seeds, irrigation ,avoidance of risky practices, and crop calendars etc

Coping Improving the resilience to withstand and manage events, through ex-ante preparation and making use of informal and formal mechanisms

Transfer Insurance ,which is a market based mechanism works best ,if mitigation is at optimum level

WHY INSURANCE FOR RISK MANAGEMENT Traditional coping mechanisms and adaptation strategies like drought proofing are not always effective against aggregate climatic risk.Sub-optimal risk management strategies fail to protect the households in the eventuality of covariate adverse shocks and catastrophic idiosyncratic shocks.The vulnerability of resource poor farmers and landless agricultural labourers is aggravated by the multitude of uninsured risks in such conditions. It is imperative to design risk management systems to stabilize crop incomes by attenuating seasonal and inter-annual variabilityProduction risk is most critical. Crop losses arising from production shortfalls/ crop output failure wipe out farm profits/price rise, and trigger a condition of distress.

EVOLUTION OF CROP INSURANCE SCHEMES IN INDIA

Insurance Scheme YearRain insurance scheme (Concept) 1920Crop Insurance Bill and a Model Scheme

1965

Comprehensive Crop Insurance Scheme (CCIS)

1985

National Agriculture Insurance Scheme (NAIS)

1999-2000

Modified National Agriculture Insurance Scheme (MNAIS)

2010-11

Weather Based Crop Insurance Scheme (WIBCIS)

2007-8

Pilot Coconut Palm Insurance Scheme (CPIS)

2013-14

National Crop Insurance Programme (NCIP)-consisting of MNAIS, WBCIS and CPIS

2013

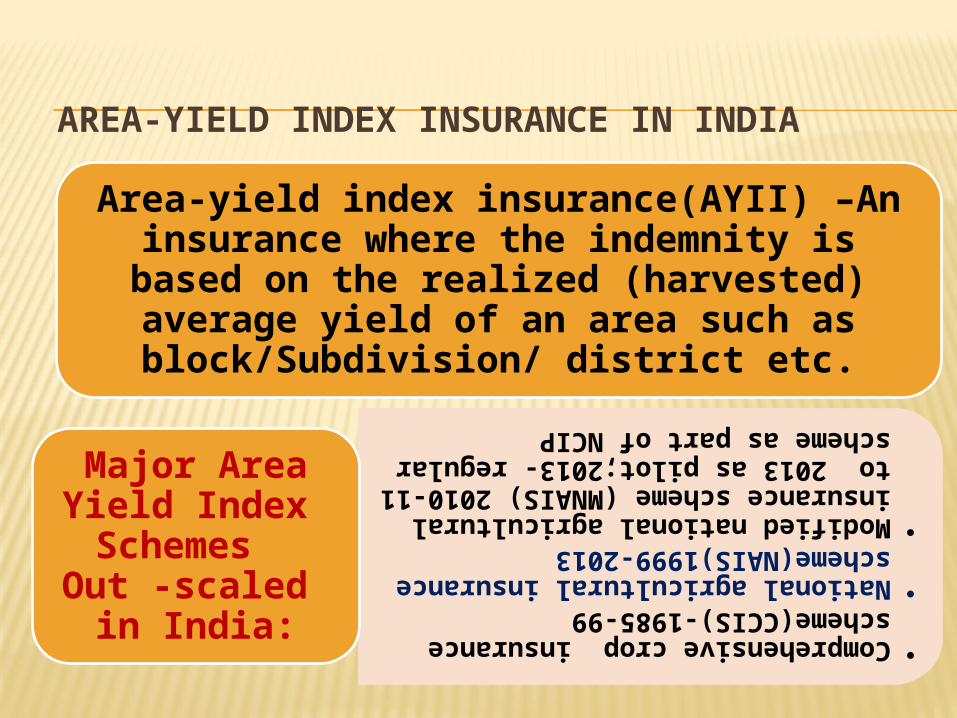

AREA-YIELD INDEX INSURANCE IN INDIA

Area-yield index insurance(AYII) –An insurance where the indemnity is based on the realized (harvested) average yield of an area such as block/Subdivision/ district etc.

•Comprehensive crop insurance scheme(CCIS)-1985-99

•National agricultural insurance scheme(NAIS)1999-2013

•Modified national agricultural insurance scheme (MNAIS) 2010-11 to 2013 as pilot;2013- regular scheme as part of NCIP

Major Area Yield Index Schemes

Out -scaled in India:

PERFORMANCE OF CCIS, NAIS AND MNAIS (GOI,2014)

Sum Insured (SI) (B Rs)

Premium(P)(BRs)

Claims (C)(B Rs)

Claims Ratio (C/ P)

Loss Cost (C /SI)( % )

CCIS (28 seasons) 457046 7304.5 45167.1 5.75 9.29 NAIS (26 Seasons)2837.2 84.6 279.6 3.3 9.85 MNAIS(6 Seasons) 110.2 10.88 8.64 0.79 7.84

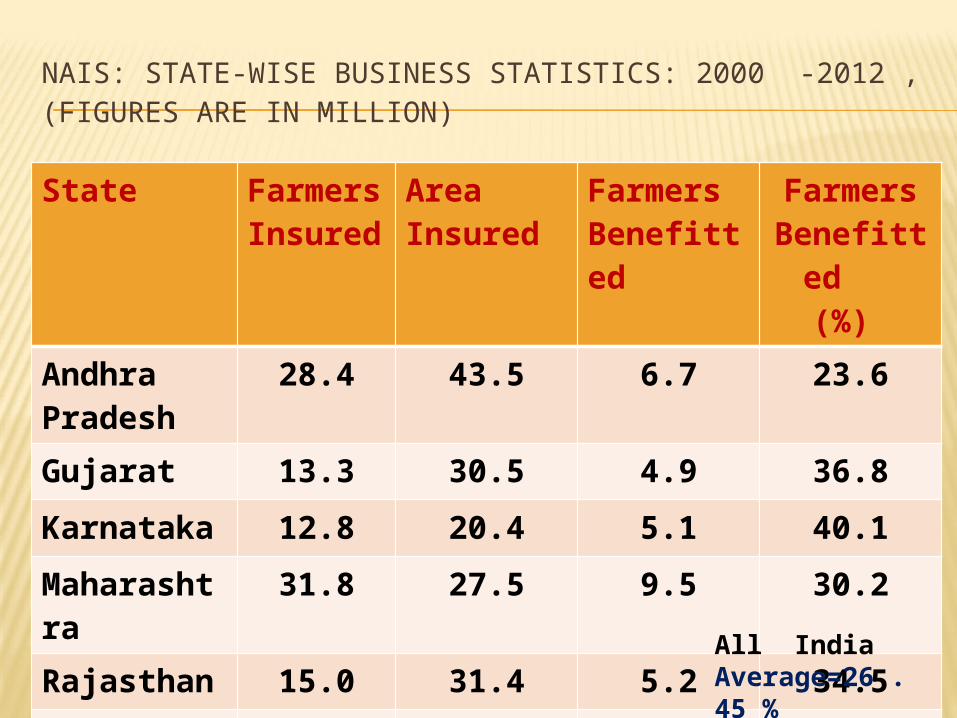

NAIS: STATE-WISE BUSINESS STATISTICS: 2000 -2012 ,(FIGURES ARE IN MILLION)

State Farmers Insured

Area Insured

Farmers Benefitted

Farmers Benefitted (%)

Andhra Pradesh

28.4 43.5 6.7 23.6

Gujarat 13.3 30.5 4.9 36.8Karnataka 12.8 20.4 5.1 40.1Maharashtra

31.8 27.5 9.5 30.2

Rajasthan 15.0 31.4 5.2 34.5Bihar 6.0 7.4 2.4 40.4All India

Average=26 .45 %

PROBLEMS ENCOUNTERED IN OPERATION OF YIELD BASED INSURANCE SCHEMES

Crop cutting experiment issues: High number in MNAIS, and areal spread CCEs difficult to manage/administer; ensuring data reliability problematic. -Probability of loss based rationalization of CCEs number; Use of GPRS-enabled and camera-fitted hand-held devices and smart phones/mobile phones—to record CCEsPremium related issues: High premium under MNAIS; Bundling of risks for fixing premium. No-claim bonus is absent-Better to identify the most critical risk and other risks may be covered as additional benefits! Consideration to no-claim bonus be givenAdverse selection :Though reduced ,but still exists.- Introduce multi year/season insurance contracts of 2-3 years at some discount in premium.

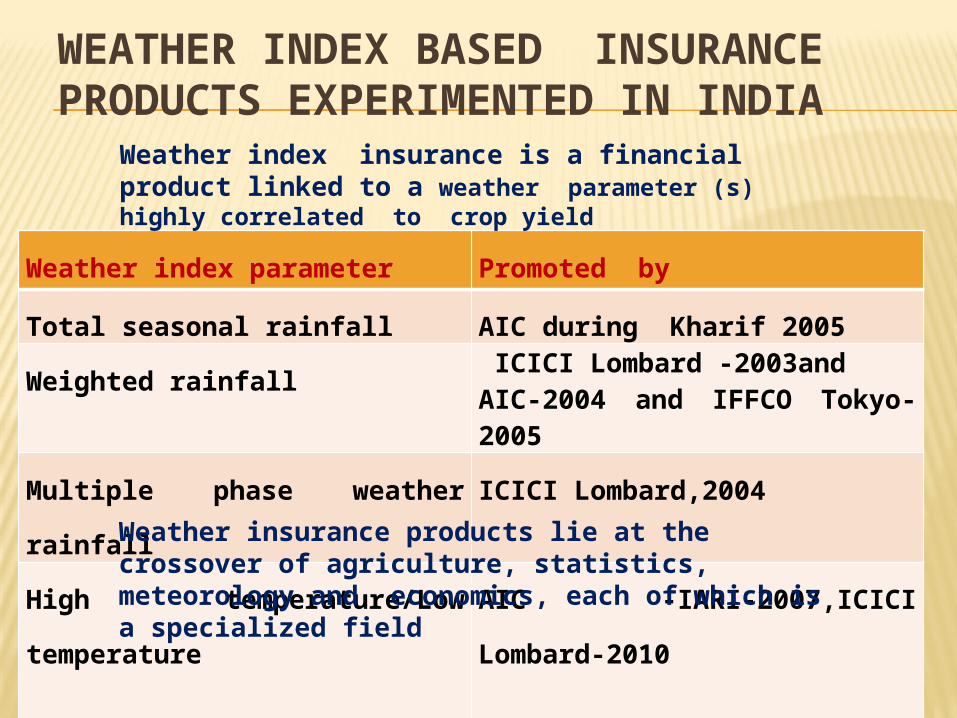

WEATHER INDEX BASED INSURANCE PRODUCTS EXPERIMENTED IN INDIA

Weather index parameter Promoted by

Total seasonal rainfall AIC during Kharif 2005Weighted rainfall ICICI Lombard -2003and

AIC-2004 and IFFCO Tokyo- 2005

Multiple phase weather rainfall

ICICI Lombard,2004

High temperature/Low temperature

AIC -IARI-2007,ICICI Lombard-2010

Weather index insurance is a financial product linked to a weather parameter (s) highly correlated to crop yield

Weather insurance products lie at the crossover of agriculture, statistics, meteorology and economics, each of which is a specialized field

PERFORMANCE OF WIBCIS FROM 2007-8 TO 2012-13 (GOI,2014)

Sum Insured (SI) (B Rs)

Premium(P)(BRs)

Claims (C)(B Rs)

Claims Ratio (C/ P)

Loss Cost (C /SI)( % )

Kharif season465.8 46.6 27.1 0.58 7.88 Rabi Season 343.7 28.6 25.8 0.90 7.5

WBCIS: STATE-WISE BUSINESS STATISTICS: 2007 -2013 (FIGURES ARE IN MILLION)

States Farmers

Insured

Area Insured

Farmers Benefitte

d

Farmers benefitte

d, (%)Andhra Pradesh

2.84 4.50 2.2 76

Bihar 8.9 9.4 6.9 77Gujarat 0.49 0.41 0.17 34

Karnataka 0.81 1.03 0.58 72Maharashtra

0.59 0.68 0.44 75

Rajasthan 30.28 42.05 16.69 55All India=62 %

ISSUES AND MEASURES FOR UP- AND OUT- SCALING WIBCIS Confidence in weather data- Low density of weather station(77% farmers remained unsatisfied), low reliability and accuracy of weather data, from private, third party source. High basis risk. A system of accreditation, certification and quality monitoring of AWSs is required Improvement in product design- Incomplete agronomic data, which distorted pricing . Products need to be based on sound agronomic and statistical theory to achieve robust actuarial design and pricing Ex-ante investment behaviour- Shift to riskier, higher-yield production techniques- higher expected profits was expected ,but no clear indication so far.Community based WIBCIS: More effective in case of small and marginal farmers, but out-scaling requires large number of dedicated organizations

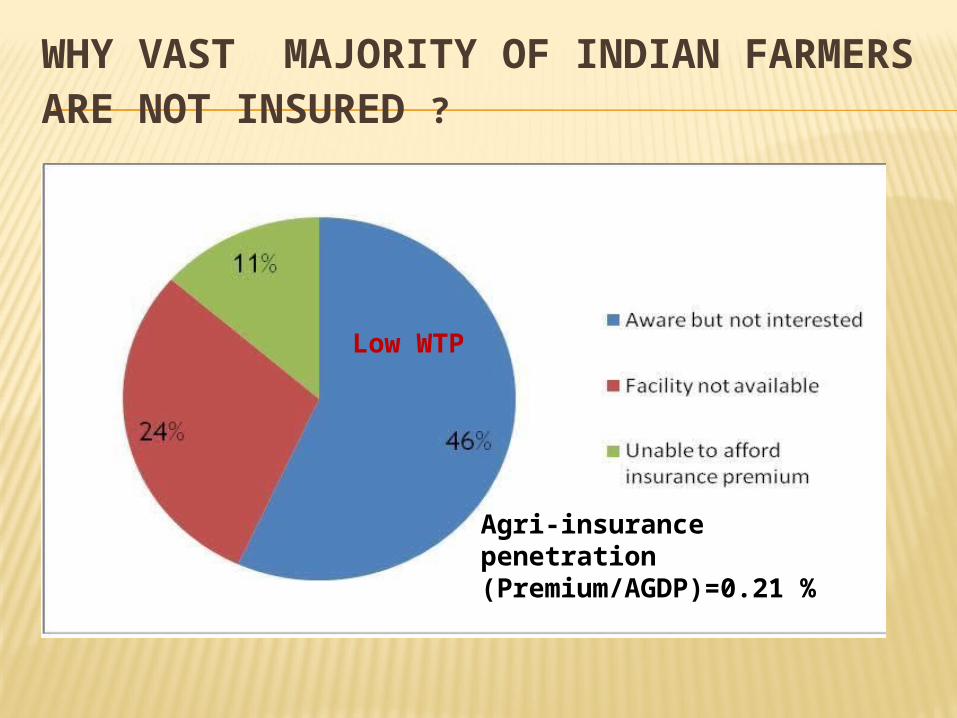

WHY VAST MAJORITY OF INDIAN FARMERS ARE NOT INSURED ?

Agri-insurance penetration (Premium/AGDP)=0.21 %

Low WTP

A CASE FOR COMPRESSIVE REVENUE ASSURANCE (RA) / INCOME PROTECTION (IP) PLAN

More effective at stabilizing income

A revenue-based program may also offer a simple way of assisting a wider variety of farms To match costs of risk protection with benefits and to base coverage on the market value of the item insured. Enhance possibilities to increase productivity and offset negative terms of trade trends.At country level high production sufficiency ,but at household income sufficiency to improve access!

RESEARCH ISSUES NEEDING ATTENTIONWhether insurance has improved household economy and livelihood opportunities to avoid distress?Has crop insurance promoted adoption of high risk- high income technologies?What is the price-value relationship of different schemes for lonee and nonlonee farmers?Why there is large gap between demand and supply of insurance products in spite of huge subsidies? Is it due to incomplete understanding of insurance purpose/ lack of suitable products/plethora of welfare programmes ? Do farmers need something beyond production insurance ?

LESSONS LEARNED IN AGRI-INSURANCE

Technically demanding and requires in-country expertiseData requirement are exhaustive – Long term data is a mustSubstantial investment in data base /infrastructureThere is no universal insurance product-Has to be modified as per needBundling/packaging help reduce transaction cost-Win win situation for the insurer and the insuredPublic-private partnerships are highly desirable-Best use of technical expertise and financial resourcesCompetition through multiple service providers- Results in lower premiumLong –term government commitment is a must- Crop insurance is partly government’s responsibility

CONCLUDING REMARKS AND WAY FORWARD(I)Insurance alone cannot provide a sustainable solution to risk faced by smallholder s. Integrated approach including risk mitigation, risk transfer and risk coping is required.In developing countries insurance must be combined with credit.Success of agricultural insurance depends on spreading risks, which requires deep and extensive market penetration .If financial sustainability is the desired goal, then a balance has to be maintained between premium, subsidy and cap on SI. Otherwise insurance can lead to maladaptation. The knowledge gaps that lead to basis risk require continuous research efforts

Helping to avoid poverty trap and protection of bank credit is not enough. Real payoffs from insurance requires unlocking access to high-value markets, modern technologies and inputs, information, and credit . Community based insurance can help in deeper penetration . For small farm holdings, community based insurance –through microinsurance provides better safety net and access to credit at low transaction cost. It has the potential to transform small farmers from subsistence to small scale commercial farming (eg contract farming). It will pay to build capacity at different levels within the country for large scale up- and out -scaling.

CONCLUDING REMARKS ANS WAY FORWARD(II)

AN INSURANCE CONTRACT IS MORE DIGNIFIED AND RELIABLE THAN DEPENDENCE ON THE AD HOC GENEROSITY OF DONORS (PROVENTION CONSORTIUM / IIASA) Policies,

technologies and institutions need attention for a win-win

solutionThank you

TYPICAL RISK LAYERS: RETENTION, COMMERCIAL, AND CATASTROPHIC (CARTEL ET AL, 2014 )