Embed Size (px)

Citation preview

Master Your Finances in 30 Days

Get the course at a 76% discount at:

https://www.udemy.com/finance-for-freedom/?couponCode=individualrising

Unit of Account

Medium of Exchange

Portable

Divisible

Fungible

Durable

Intrinsic Value

Gold and Silver coins and bullion

Paper currencies backed by precious metals

Created by mining precious metals and minting them into coins and bars

Intrinsic value remains stable over time because money supply growth is severely constrained

Contains all properties of money – portable, divisible, fungible, durable, intrinsic value

National currencies – dollars, euros, yen, yuan, etc.

Issued by government “fiat” (let it be done)

Legal tender for all debts, public and private

Backed by the “full faith and credit” of issuing government

Created through the central banking system

Portable, divisible, and fungible

Not durable, intrinsic value diminishes over time because money supply growth is unrestrained

1792 – Defined by the U.S. Coinage Act as 371.25 grains of pure silver

U.S. Mint coined gold and silver dollars per this measurement

Private Bank Notes backed by gold and silver

1900 - Gold Standard Act defined the dollar as 25.8 grains of gold nine/tenths fine

1913 - Federal Reserve Act created Federal Reserve Notes backed by gold

All holders of dollars free to convert paper dollars into physical gold at any time

1933 – President Roosevelt issues executive orders suspending domestic gold convertibility and criminalizing private gold ownership

Americans required to deliver all gold coins, gold bullion, and gold certificates to the Federal Reserve in exchange for $20.67 paper dollars/oz – violators subject to fines and imprisonment

U.S. dollar no longer redeemable in gold domestically 1944 - Bretton Woods Agreement establishes U.S. dollar as the

international reserve currency convertible at $35 per ounce 1968 – President Johnson signs the Gold Reserve Requirements

Elimination Act 1971 – President Nixon issues an executive order unilaterally

ending the direct convertibility of the dollar for gold at any price U.S. dollar no longer backed by anything but the “full faith and

credit” of the U.S. government

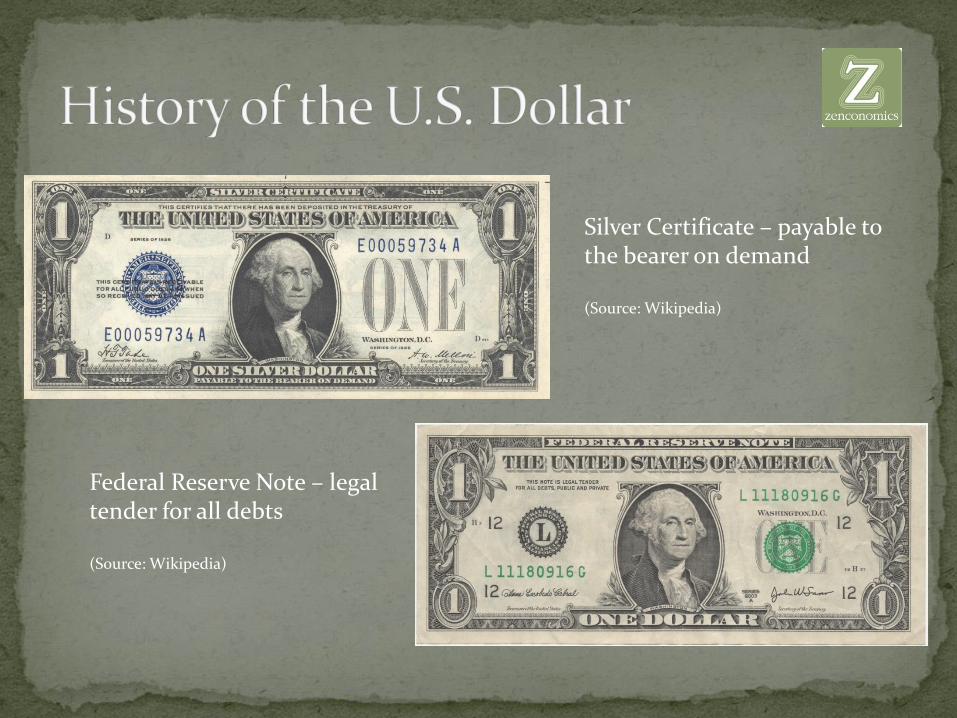

Silver Certificate – payable to the bearer on demand

(Source: Wikipedia)

Federal Reserve Note – legal tender for all debts

(Source: Wikipedia)

Purchasing power has declined by 98% since 1913

Purchasing power has declined by 21% since 2002

$1.00 purchased 50 times more in 1913

(Source: Wikipedia)

Commodity money for most of modern history up until the World Wars

Post-war period: all national currencies were linked to gold through the U.S. dollar under the Bretton Woods System

Bretton Woods unilaterally dismantled in 1971 which cut all currency ties to gold

100% fiat international monetary system

All national governments have been inflating the money supply

Currencies float in exchange value with one another, but lose purchasing power in terms of goods and services over time

Fiat money is an illusion – it is not wealth

True wealth is time and freedom

Fiat money must be converted into assets to build wealth

Only a small percentage of the population understands money and monetary history thus the conventional wisdom is often wrong

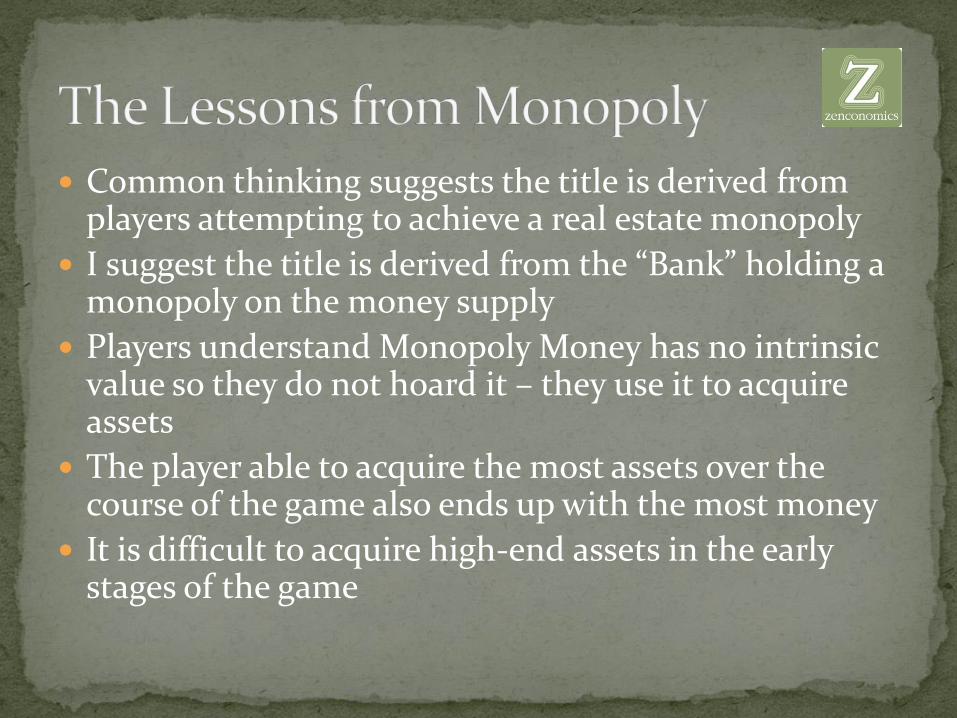

The Lesson from Monopoly

Common thinking suggests the title is derived from players attempting to achieve a real estate monopoly

I suggest the title is derived from the “Bank” holding a monopoly on the money supply

Players understand Monopoly Money has no intrinsic value so they do not hoard it – they use it to acquire assets

The player able to acquire the most assets over the course of the game also ends up with the most money

It is difficult to acquire high-end assets in the early stages of the game

Nearly everything you do has a financial impact

Decisions come with opportunity costs

Financial Freedom can only be attained by those who are able to forego instant gratification and think long-term

Frugal; not cheap

You have an Income Statement and Balance Sheet

Create spreadsheets to monitor your financial statements

Be cognitive of how your decisions affect your financial statements

Income

Job……………………..$3,000

Side business……..$ 500

Total…………………..$3,500

Net Income………..$1,390

Expenses

Mortgage…………….$1,200

Electric……………….$ 150

TV/Internet………..$ 115

Cell Phone………….$ 85

Student Loans…….$ 175

Fuel…………………….$ 90

Groceries…………….$ 120

Misc…………………….$ 175

Total…………………….$2,110

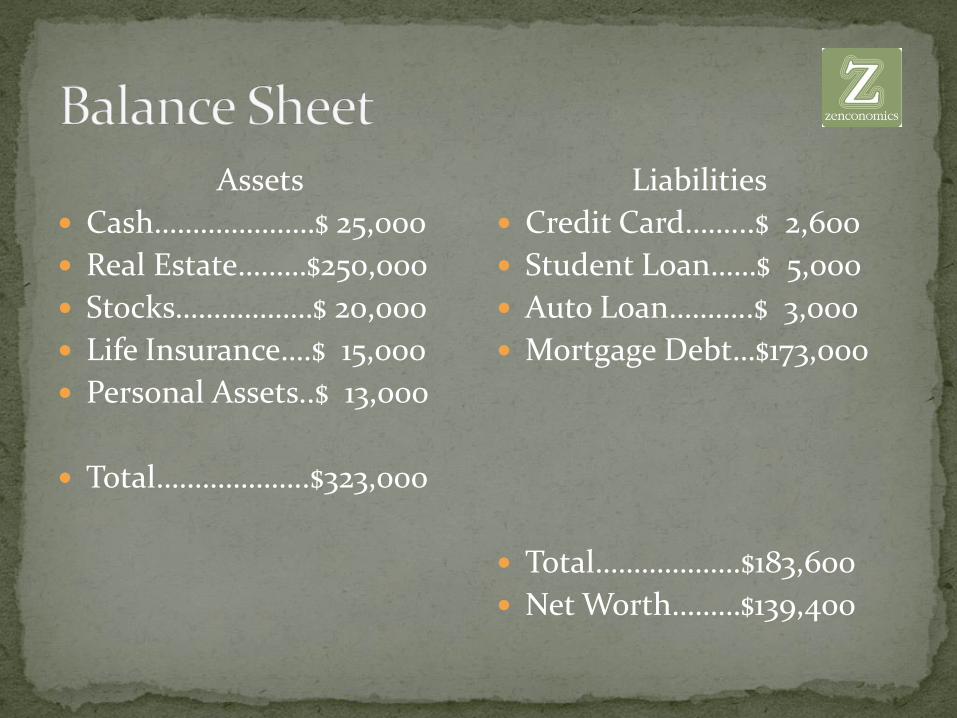

Assets

Cash…………………$ 25,000

Real Estate………$250,000

Stocks………………$ 20,000

Life Insurance….$ 15,000

Personal Assets..$ 13,000

Total………………..$323,000

Liabilities

Credit Card……...$ 2,600

Student Loan……$ 5,000

Auto Loan………..$ 3,000

Mortgage Debt…$173,000

Total……………….$183,600

Net Worth………$139,400

Create a spreadsheet to track expenses (every single cent!)

Analyze expenses for one or two months and determine where cuts can be made

Pour free cash flow from spending cuts into paying off consumer debt (high interest debt first)

Make these debt payments AS SOON as your paycheck is received

Remember, if you want what most don’t have you must be willing to sacrifice when others are not

Not many options if renting

Probably best to rent if you don’t expect to stay put for a long period of time

Assess mortgage if homeowner – how much of payment goes to interest and PMI?

PMI is private mortgage insurance paid by the homeowner to protect the lender from default

PMI waived at 80% LTV

Does it make sense to pay down or refinance?

Long-term goal: no fixed housing costs

Six to Twelve months minimum

Emergency Fund

Needs to be liquid

Standard checking account

Physical cash at home

Building the base takes time

Become money-conscious

Thinking long-term

Analyze and cut spending

Eliminate consumer debt completely

Assess housing

Build a cash reserve

This process both reduces your need for income and frees up income for capital formation

Invest AFTER your financial house is in order

Most of modern personal finance is either irrelevant, wrong, or dangerous

The monetary system works against those who do not understand it

Fiat money constantly loses purchasing power – remember the lessons from Monopoly!

The public school system ignores finance altogether

The universities teach an academic model that does not match up with real-world experience

Wall Street does not exist to make you rich; it exists to enrich itself by extracting money from the gullible masses

Do not follow the masses!

The economy is changing

Globalization

Technology – P2P/Cryptocurrency/3d Printing/Robotics

Falling Gatekeepers –media/publishing/education/finance

Reduced traditional employment

Increased entrepreneurial opportunity

Welcome to the Information Age!

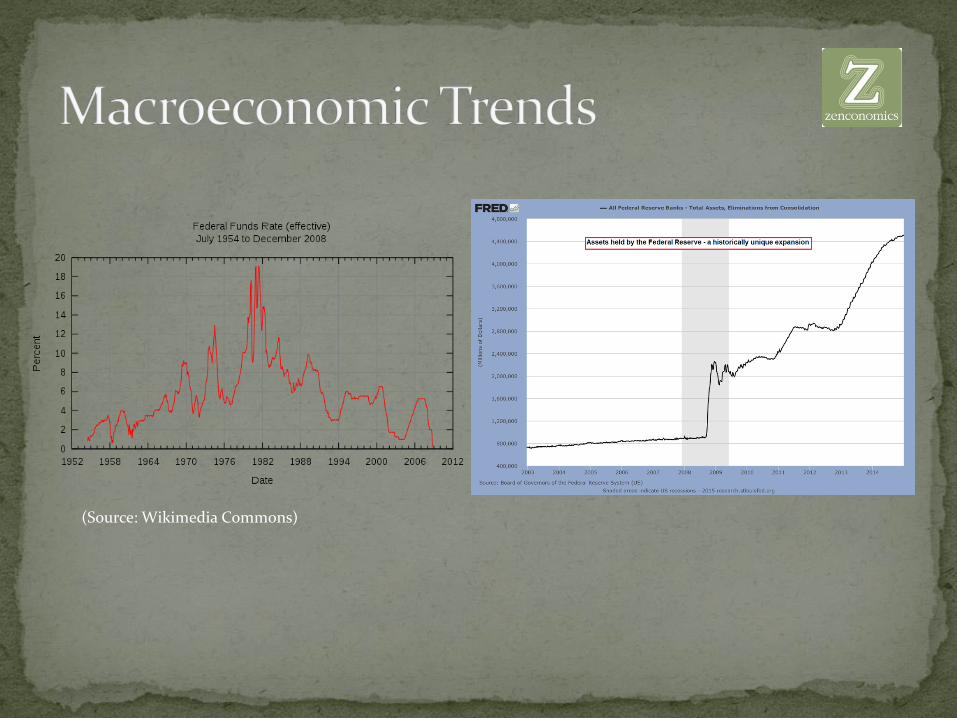

It took more than 200 years for the U.S. government to accumulate $1 trillion in debt; It took less than 30 years to accumulate another $17 trillion

2005-Present: $9 trillion in debt $200 trillion estimated unfunded liabilities Interest rates have been declining since the 1980’s Despite record-low rates, U.S. government paid $420 billion

in interest payments in 2013 Every developed nation is in a similar situation – high debt

and unfunded liabilities The Fed expanded it’s balance sheet by nearly $4 trillion to

bail out the financial system – no market for these bad assets

(Source: Wikimedia Commons)

The three-legged stool will soon be the one-legged stool (unicycle?)

10,000 Baby Boomers turning 65 every single day for the next 10 years

Social Security: $50 billion annual deficit - $134 trillion unfunded liabilities

Medicare: $30 billion annual deficit - $38 trillion unfunded liabilities

The Retirement Myth – carrot on a stick

Change seeds opportunity

What to do with your money

No one-size-fits-all plan

Fundamentals build resiliency

Asset Allocation builds antifragility

Remember, the goal is sustainable financial freedom

Create a model to allot a percentage of capital across several asset classes

Asset allocation guarantees that you cannot be wiped out by any wild market swings or Black Swans

Asset allocation ensures you will always have cash on hand to take advantage of opportunities as they arise

Perfectly suited for the ‘barbell’ strategy

Not necessary to diversify your stocks when you diversify your assets

Antifragile asset allocation model consists of:

Cash: 10-30%

Precious Metals: 10-30%

Real Estate: 30-60%

Stocks: 10-30%

Bonds: 0-10%

Bitcoin: 0-5%

Bank Account

Brokerage Account

Physical currency at home

IBC Life Insurance Policy (cash value)

Cash is your emergency reserve and your “dry powder” to purchase assets at a discount when the opportunity arises

Physical gold and silver coins/bullion stored at home

Physical gold and silver coins/bullion stored in an audited, allocated vault outside of your political jurisdiction (ex: Hard Assets Alliance)

Never store in a bank vault!! (See: FDR)

Precious metals anchor your capital

Precious metals are the ultimate insurance policy – they have maintained value over centuries

Hedge against fiat money, debt, inflation, currency crisis

The only asset not also someone else’s liability

Personal residence

Family farm/vacation home

Residential rental properties

Apartment buildings

Commercial rental properties

The largest piece of your model because the value of each unit is very high

Must acquire properly! (sound financing, don’t chase bubbles)

Advantaged within a fiat monetary system because the debt burden devalues with the currency

Can raise rents to combat inflation and rising property taxes

Online brokerage or full service broker

Private local stock

Must have an investment strategy – random stock picking is disastrous

Follow proper position sizing – only place 5-10% of stock portfolio into each position

Only purchase with limit orders

Consider manual stop-losses

Consider independent investment analysis

Market goes up slowly, market goes down rapidly

Do not invest in anything you see advertised

Be very skeptical of managed mutual funds (high fees/high turnover)

Track a list of blue chip capital efficient companies and wait patiently for them to go on sale

Do not diversify or be ultra-conservative (asset allocation)

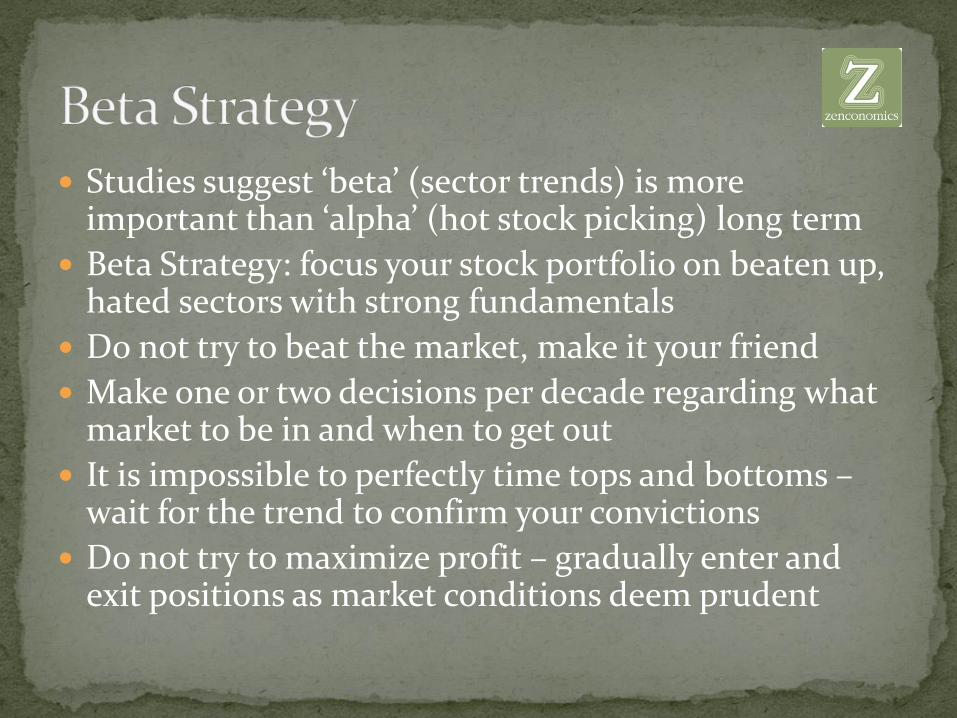

Seeking hot stocks (alpha) is simplistic and inconsistent

Studies suggest ‘beta’ (sector trends) is more important than ‘alpha’ (hot stock picking) long term

Beta Strategy: focus your stock portfolio on beaten up, hated sectors with strong fundamentals

Do not try to beat the market, make it your friend

Make one or two decisions per decade regarding what market to be in and when to get out

It is impossible to perfectly time tops and bottoms –wait for the trend to confirm your convictions

Do not try to maximize profit – gradually enter and exit positions as market conditions deem prudent

1971 – “Nixon Shock” cuts dollar’s link to gold: Gradually focus your portfolio on the gold sector

1979 – Fed Chairman Paul Volcker vows to raise interest rates to crush inflation: Casually exit your gold positions and move to cash

1982 – Price inflation waning and prime rate steadily falling: Gradually focus your portfolio on Dow blue-chips

2000 – The Dow has risen to $11,000 from $1,500 in 1985 which has attracted throngs of new investors: Casually exit your Dow positions and move to cash

2001 – Fed Chairman Alan Greenspan begins cutting interest rates and easing credit in response to the bursting of the tech bubble and 9/11: Gradually focus your portfolio on the gold sector once again

2009 – The Federal Reserve and the feds have bailed out Wall Street, drastically cut interest rates, and are pumping huge quantities of currency into the economy; the Dow has been cut in half: Casually exit your gold positions and move into Dow blue-chips

2015 – The Dow has nearly tripled since its 2009 low, but the economic recovery has been fundamentally weak; many commodity and gold stocks are 80%-90% off of their high: Gradually exit your Dow positions and move into commodity and gold stocks…

Seven decisions in four and a half decades

Focused stock investments produce antifragility

Impossible to predict the future or time markets, wait for the trend to verify your conviction

Asset allocation and stop-losses mitigate your risk of being wrong with beta picks

Not the ultra-conservative asset as presented under current conditions

Preferred legal treatment to stocks

Return = principal + interest payments

Must call broker with specific CUSIP

Best to purchase at steep discounts after a major bust in the credit cycle (corporate bonds)

Credit cycle tends to last 7-8 years

Watch ‘HYG’ ticker to gauge bond market

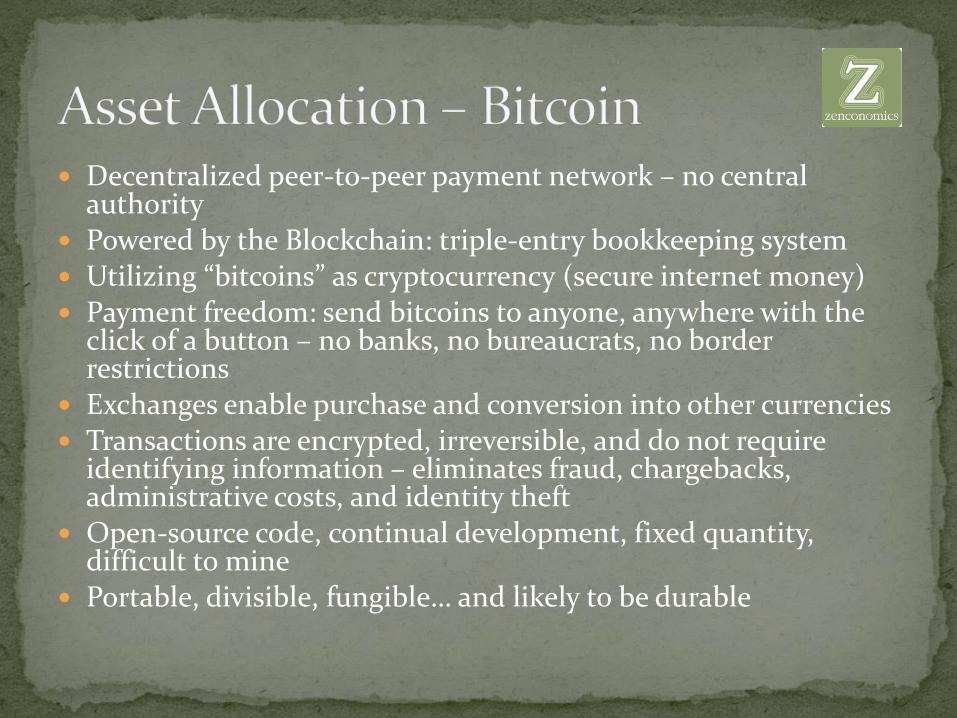

Decentralized peer-to-peer payment network – no central authority

Powered by the Blockchain: triple-entry bookkeeping system Utilizing “bitcoins” as cryptocurrency (secure internet money) Payment freedom: send bitcoins to anyone, anywhere with the

click of a button – no banks, no bureaucrats, no border restrictions

Exchanges enable purchase and conversion into other currencies Transactions are encrypted, irreversible, and do not require

identifying information – eliminates fraud, chargebacks, administrative costs, and identity theft

Open-source code, continual development, fixed quantity, difficult to mine

Portable, divisible, fungible… and likely to be durable

Cash – 24% Bank Accounts: $10,000 Brokerage Accounts: $15,000 Life Insurance Cash Value: $47,000

Precious Metals - 10% Gold: $20,000 Silver: $10,000

Real Estate – 45% Primary Residence: $135,000

Stocks – 20% Brokerage A: 45,000 Brokerage B: 15,000

Bitcoin – 1% Wallet A: 2,000 Wallet B: $1,000

Home Resiliency Six months stored food

Water storage

Alternative energy

Essential Provisions

Wine cellar

Family Garden

Livestock

Art Work

Collections/Hobbies

Understand money and its properties

Be aware of prominent macroeconomic trends!

Maximize Capital; Minimize Crap drastically reduces your need for income

Asset Allocation strategically deploys your income

Alternative Investments insulate you from financial catastrophe

Next step: Financial Escape Velocity

Develop scalable income streams outside of traditional employment and let investments compound for decades

Ideal: Stop trading time for money; get both on same side Scale the family business Start a family business Freelancing/Consulting Online Sales Launch information products (books, e-books, newsletters,

DVDs, guides, how-to manuals, online courses, etc.) Build or acquire microbusinesses (automated websites,

affiliate marketing, dropshipping, etc.) Rental Real Estate

Choose your own level of involvement

Work as much or as little as you want

Earn as much as you want

Live where you want

Network and interact with people of your choice

Become a sovereign individual

Live a meaningful and fulfilling life no matter what happens to the sociopolitical economy

Deliver value, educate, inspire, and bless the world

Master Your Finances in 30 Days

Get the course at a 76% discount at:

https://www.udemy.com/finance-for-freedom/?couponCode=individualrising