Embed Size (px)

Citation preview

Funding Options for CT Companies

2013

Presented to

Crossroads Venture Group

Boardroom Series

Liddy Karter, Managing DirectorHitesh Shah, Vice President

Confidential

Background

1

● Enhanced Capital Partners, Inc. (“ECP”) is a diversified, national asset management firmproviding financing to small-business in U.S. markets that have been underserved bytraditional sources of capital

● Founded in 1999 by former Welsh Carson Managing Partner Andrew Paul, ECP has gainedexperience in targeted investing through years of participation in numerous state andfederal public-private partnerships

● Working with small businesses for over 12 years has allowed ECP to develop an investmentapproach that combines innovative structures and conservative investment principles toprovide a dual bottom line return for our collective partners

● Our collaboration with marquee investment partners like Berkshire Hathaway and VulcanCapital provides our portfolio companies with a variety of funding options

● Office Locations in 10 States and Washington DC (Alabama, Colorado, Connecticut, Florida,Louisiana, Mississippi, New York, Oregon, Tennessee, Texas, Wyoming)

Confidential

ECP’s Platform

ECP

Office locations in

10 States and DC*

Berkshire Hathaway /

Vulcan Capital

19 State Focused

Funds

National Middle Market

SBIC Fund

Federal & State New Market Tax

Credits

Enhanced Equity Fund

& Sopris Capital

2

Confidential

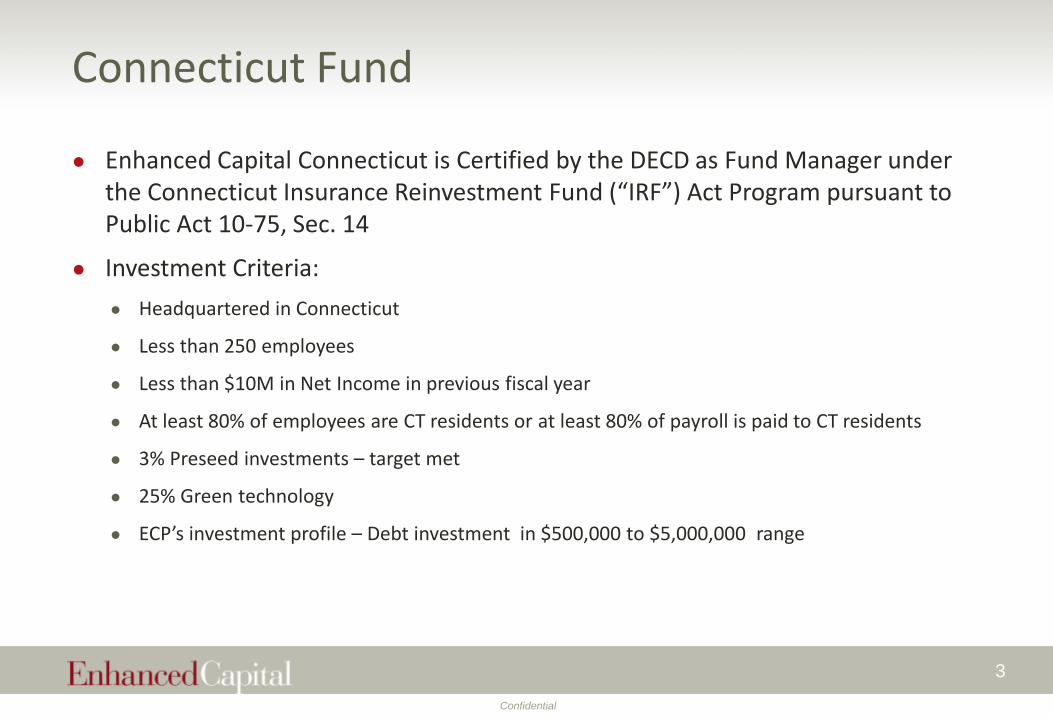

Connecticut Fund

● Enhanced Capital Connecticut is Certified by the DECD as Fund Manager under the Connecticut Insurance Reinvestment Fund (“IRF”) Act Program pursuant to Public Act 10-75, Sec. 14

● Investment Criteria:

● Headquartered in Connecticut

● Less than 250 employees

● Less than $10M in Net Income in previous fiscal year

● At least 80% of employees are CT residents or at least 80% of payroll is paid to CT residents

● 3% Preseed investments – target met

● 25% Green technology

● ECP’s investment profile – Debt investment in $500,000 to $5,000,000 range

3

Confidential

Connecticut Team

Elizabeth (“Liddy”) Karter - Managing Director, Connecticut

● Liddy serves as a Managing Director of Enhanced Capital and is responsible for overseeing investment activity in Connecticut. She brings experience in clean tech venture capital, corporate finance, and early stage company management.

● Prior to joining Enhanced Capital, she was a Managing Partner at IRON Ventures, a venture fund investing in sustainable business ventures enabling symbiotic reuse of energy, industrial material and water.

● Prior to IRON Ventures, Liddy was CEO of Resource Recovery Systems, Inc., a nationwide recycling company and CFO of Netkey, Inc., an ecommerce software company. Prior to that, she was Vice President of the Financial Services Group at Morgan Stanley.

● Liddy is active in angel investing and serves on the Board of the Angel Capital Association. She is Executive Director of the Connecticut Venture Group, a statewide trade association for venture funds in Connecticut and serves as a Mentor at the Yale Entrepreneurial Institute.

● Liddy received an MBA from Yale University and a BA in from Columbia University.

4

Confidential

Connecticut Team

Hitesh Shah – Vice President, Connecticut

● Hitesh serves as a Vice President at Enhanced Capital and focuses on investment activities in Connecticut.

● Prior to Enhanced Capital, he was an Analyst at Connecticut Center for Advanced Technology’s (CCAT) Entrepreneur Center, a physical and virtual incubator for technology led small businesses.

● Prior to CCAT, he was an Analyst at Connecticut Technology Council’s (CTC) statewide virtual incubation program for small businesses. Prior to CTC, he was a Financial Analyst at a small ceramics manufacturing company in India.

● Hitesh graduated with an MBA from University of Hartford and a BS in Accounting from University of Pune.

5

Confidential

Representative CT Portfolio

6

Confidential

Representative CT Portfolio

7

Confidential

Equity- Early Stage

● Focus on Angels and Funds

● Angel Investor Forum

● Centripetal Capital

● Boston and NY groups

● Family Offices

● Funds

● Launch

● Vital

● Elm street

8

9

Equity – Early Stage

•Overview

•Know your Investors

•Define the company

•Growth strategy

•Capital plan

•Connections

10

Common/

Founders

Stock

Common,

Preferred

or Bridge

Preferred

Convertible

Preferred,

Mezzanine,

Debt

Listed

Equity

Seed-

product

development

Early Stage-

Begin

sales

Series

A or B-

Ramp up

sales

Series

C or D-

Product

extension

IPO/M&A

Founders

3Fs,

SBIR,

University

Angels,

VC

Boutique

VCPrivate Eq

Inv. Banker

Investment

managers,

Hedge

funds

Company

Players

Collateral

First, we will clarify the

investment cycle….Match Investors to Company

11

Angels are not VC’s

What they have in common How they are different

Play in a similar space on the investment

continuum

VCs have fiduciary responsibility to

their Limited Partners

Look for similar things in a business plan Angels risk their own capital – no

need to invest

Only invest if outlook is for

> 10X return minimum

VC’s invest larger $ ~10x more than

angels.

Expect to invest in multiple rounds VCs may require control. Define

control

Portfolio approach: 2+ 7+ 1 Fund cycle affects VC investing

Time horizon is 5+ years Angels 50k deals/yr - VC 4k deals/yr:

Both ~$20B+

Confidential

Pick the Right Business

● Industry Sector- Fast and Hot● Innovative/Established,

● IT/Green Tech/Manufacturing, Medical Device

● Model- Capital light● Product/Service,

● Direct/Indirect

● Market – Addressable● B-B/B-C, Size

12

Confidential

Key Features

● Huge Market Need/Value Proposition

● Barriers to Entry

● Patents/Trade Secrets/Capital Advantage

● Team

● Experienced/friends?

● Collateral

● Building/Standard equipment/PG

13

Confidential

PreRev, PreMoney Value ~$1.8M.

●Negotiation

●Capitalization table

●What’s the right number?

●Methods

●Meeting the investors needs

14

Confidential

Sources of Value

15

• Numbers: projections, comps, 18m• Product – High margin, Necessary• Clients – Recurring? $1B market?• Intellectual Property • Management: track record,, team• Competition: ability to raise money• VC: life cycle of fund• Industry: hot or not, economy

16

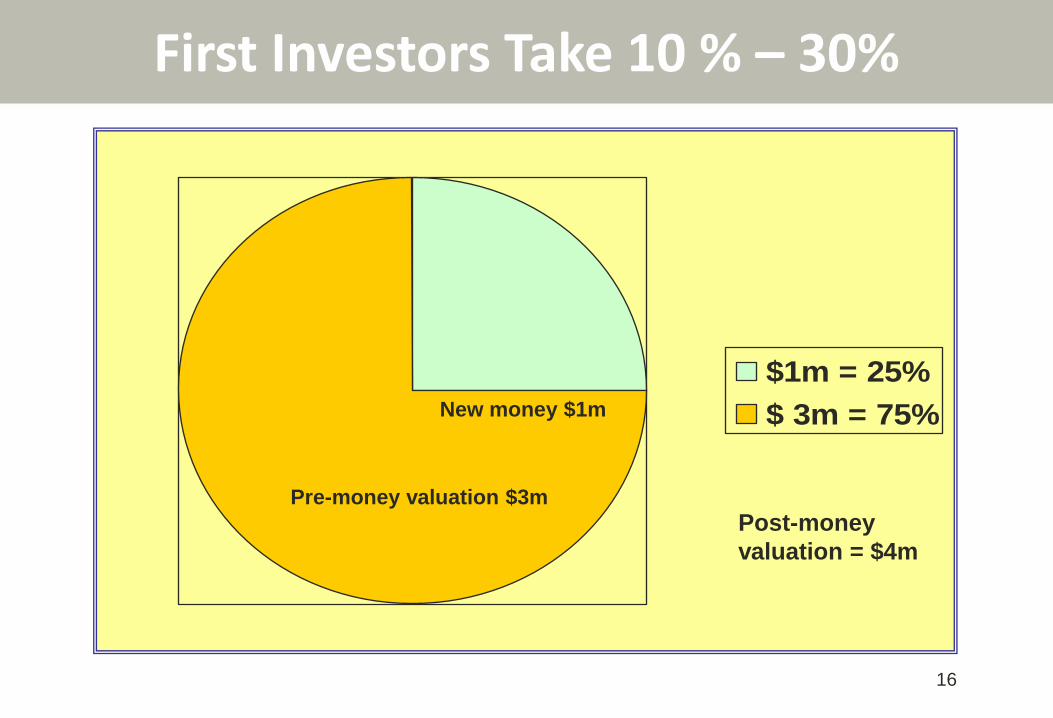

$1m = 25%

$ 3m = 75%

Pre-money valuation $3m

New money $1m

First Investors Take 10 % – 30%

Post-money

valuation = $4m

17

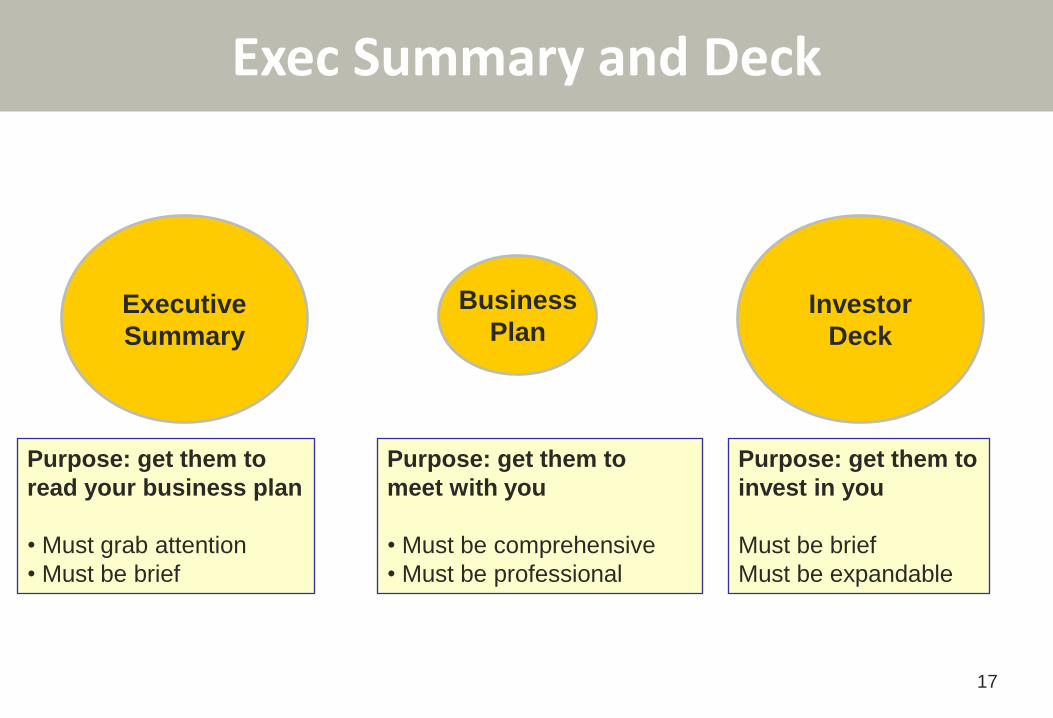

Executive

Summary

Business

PlanInvestor

Deck

Purpose: get them to

read your business plan

• Must grab attention

• Must be brief

Purpose: get them to

meet with you

• Must be comprehensive

• Must be professional

Purpose: get them to

invest in you

Must be brief

Must be expandable

Exec Summary and Deck

18

•Financial Model - Details

•Cash Flow - Don’t be shy

•Potential vs. Risk

•Expect to be wrong

• Know why

•Use Comparables

Know Your Numbers

19

• 2011: $200,000 invested by founders @$500k pre

• 2012: $100,000 friends and family with a post-

money valuation of $1.5M

• Currently looking to raise $500,000 with a pre-

money valuation of $2M

•Revenues $800k

• Expect to do a $10M VC round early 2014 @$10M

pre.

•TTM EBITDA - $1M

Funding Strategy- Simple

20

Sales & marketing Big salaries for

management

Distribution partners Paying off debt

Some product

development

Too much product

development

Use of proceeds

[email protected] Equity Financing in CT21

•CEO’s Main Job

•Constant Process

•Networking

•Build LT Relationships

•Create confidence

Funding Timing

[email protected] Equity Financing in CT22

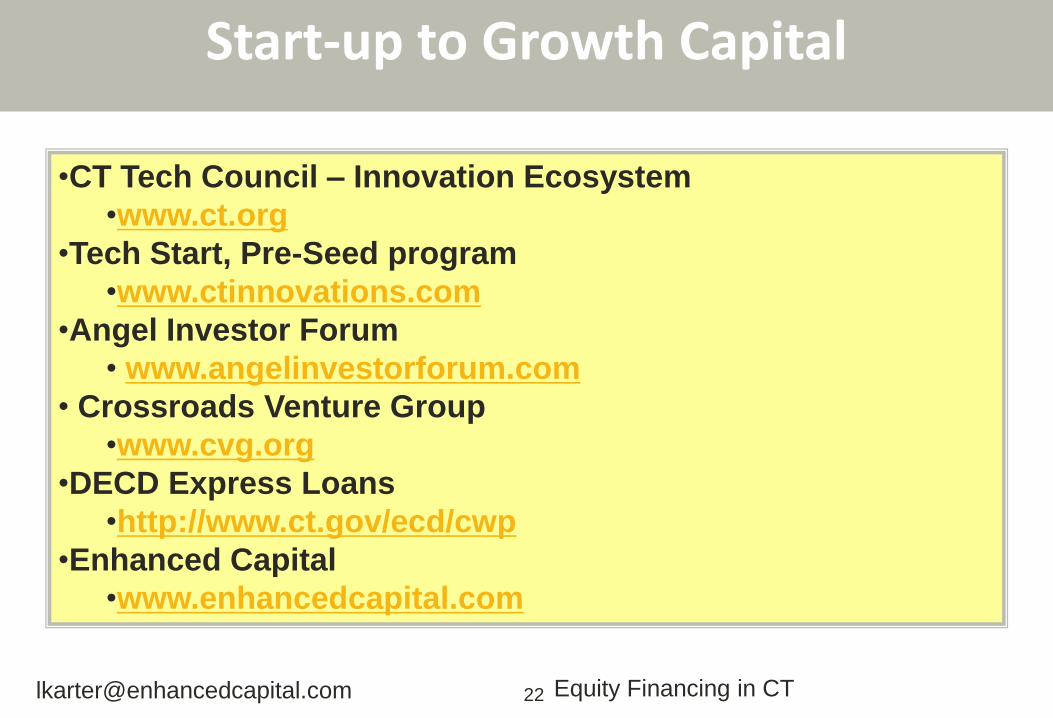

•CT Tech Council – Innovation Ecosystem

•www.ct.org

•Tech Start, Pre-Seed program

•www.ctinnovations.com

•Angel Investor Forum

• www.angelinvestorforum.com

• Crossroads Venture Group

•www.cvg.org

•DECD Express Loans

•http://www.ct.gov/ecd/cwp

•Enhanced Capital

•www.enhancedcapital.com

Start-up to Growth Capital

Confidential

Corporate VC 40% of Start up $

● The number of CVCs actively investing is steadily on the rise. In Q2’13, 66 different CVC investors participated in at least one investment which was up 40% versus the number of participating CVCs in Q3’11.

Confidential

CT Based Fortune 500 Companies

8 General Electric, Fairfield, $147 B 50 United Technologies, Hartford, $59.8 B 84 Aetna, Hartford, $36.6 B 103 Cigna, Bloomfield, $29.1 B 112 The Hartford Financial Services Group, Hartford, $26.4 B 131 Xerox, Norwalk, $22.4 B 241 Praxair, Danbury, $11.2 B 245 Stanley Black & Decker, New Britain, $11.1 B 340 Charter Communications, Stamford, $7.5 B 351 Terex, Westport, $7.3 B 399 EMCOR Group, Norwalk, $6.3 B 400 Starwood Hotels & Resorts, Stamford, $6.3 B 438 W.R. Berkley, Greenwich, $5.8 B 473 Priceline.com, Norwalk, $5.3 B 489 Pitney Bowes, Stamford, $5 B 492 Frontier Communications, $5 B

Confidential

CVC Growing

Confidential

CVC- $7B market

Confidential

CT Investment Highlights

27

CT 13 60,168,000 12 18,644,200 10 24,952,100 16 51,363,000 12 32,374,700 18 40,435,000

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013

STATE

Deals Amount Deals Amount Deals Amount Deals Amount Deals Amount Deals Amount

Rank 12 13 13 23 20 23 10 15 11 19 10 17

Confidential

VC $ Invested VC $/Capita 1 job/$25k VC

CA 12,864,904,100$ 338$ 514,596

MA 3,005,281,900$ 452$ 120,211

NY 2,088,210,300$ 107$ 83,528

CT 149,124,800$ 42$ 5,965

CT Investment Highlights

28

Confidential

CT is in the middle

●CAL

●MA

●NY

●>>>>CT

Confidential

Seed and Early for Corporate VC

40%

Confidential

Matchmaking- Corporate VC Sectors

● Internet

● Mobile

● Life Sciences

● Mostly just looking for a match

Confidential

Late Stage Equity

● Investment bankers and intermediaries

● Private Equity

32

Confidential

Debt

● Banks are back – 5%

● Private Debt a good option – see funds and I-bankers. 8%

● Mezzanine – 14%

● With State Support – 12% all in with equity kicker

33

Confidential

What is Mezzanine Debt?

● Mezzanine debt or mezzanine capital is a form of hybrid capital that has been around for 30 years and which can be structured as either preferred equity or unsecured debt. It is generally referred to the layer of debt that sits between senior debt and equity. Mezzanine debt lays claim to a corporation’s assets, yet also incorporates equity-based security options in its structure. It is senior only to common shares and is often a more expensive form of financing because of its positioning and inherently higher level of risk to the lender. And unlike Venture Capital, Mezzanine debt is used for adolescent and mature companies who are cash flow positive that need capital for a number of growth-related uses.

Confidential

Mezz. Debt benefits

● Mezzanine debt provides the following benefits:

● The company being funded gains capital while increasing their leverage

● The senior secured lender sees an injection of new opportunity equity and reduced leverage

● The mezzanine debt provider can put its capital to use at an attractive rate

● Shareholders avoid unnecessary dilution from new equity (which is also the most expensive form of capital)

● The company sees a lower cost of capital when compared to equity

● The company receives less rigid terms when compared to senior debt

● The company's weighted average cost of capital (WACC) can be reduced

● The company's return on equity (ROE) can be increased

Confidential

Contact Information

● Liddy Karter

● Email: [email protected]● Phone: (203) 376-7958

● Hitesh Shah

● Email: [email protected]● Phone: (203) 614-8771

Enhanced Capital Connecticut:1055 Washington Blvd, 8th FloorStamford, CT 06901Phone: (203) 614-8770Fax: (203) 614-8769Website: www.enhancedcapital.com

36