Embed Size (px)

Citation preview

Points to remember……….

• Long – Buy …(going long) [Bullish view]

• Short – Sell …(going short) [Bearish view]

• Squaring off (turn around trades) – opposite transaction to the previous one

• Buy low, sell high - gives a profit

• Sell high, buy low - also gives a profit

• Sell low, buy high – gives a loss

• Buy high, sell low – also gives a loss

Derivatives

• Derivatives are instruments whose value is derived from the value of underlying assets in a cantractual manner.

• The underlying could be stock, exchange rate, commodity etc.

Derivatives- Milestones

• In India derivatives trading started on exchange in June 2000 after SEBI granted final approval to this effect in May 2000

• First to be traded were futures contract on Index.• After this came, options on individual securities

and index• Futures contract on individual stocks were

launched in November,2001

Derivatives- Products

• The most common derivative products are

a) Forward

b) Futures

c) Options

Forward

• A forward contract is an agreement between two parties to buy or sell an asset on a specified date for specified price.

Features:• These are bilateral contract• These contracts are customised• There is a counter party risk

Derivatives – An example

• 10th Feb 2013– A Wheat Farmer will have crop ready by

March 2013– Worried about price fluctuations– A Bread maker needs wheat in March 2013– Worried about price fluctuations

• Both face a Price Risk

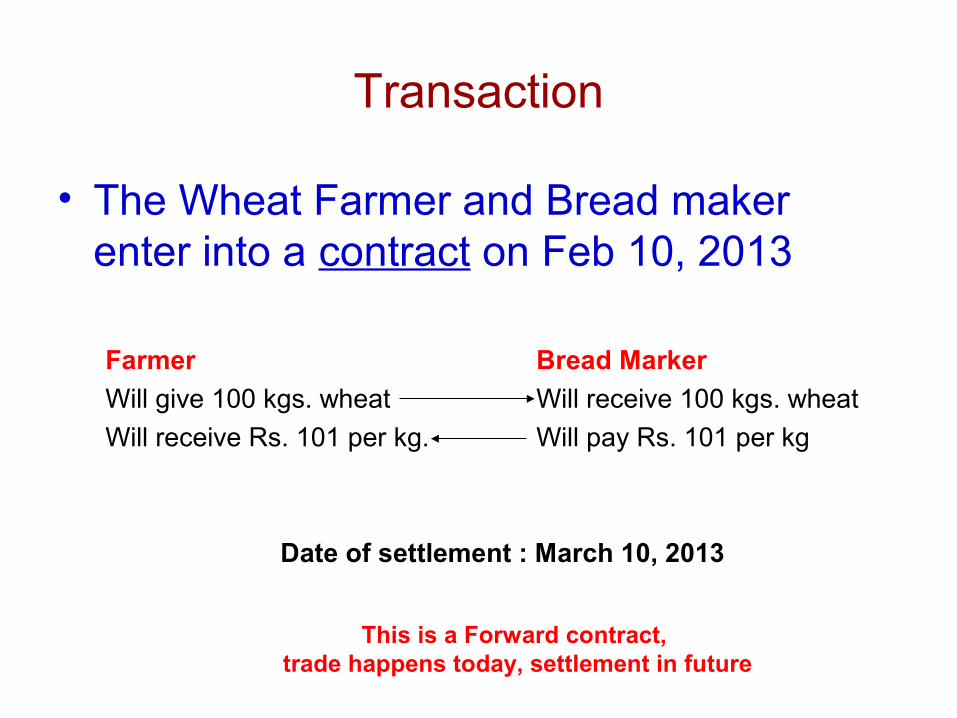

Transaction

• The Wheat Farmer and Bread maker enter into a contract on Feb 10, 2013

Farmer Bread Marker

Will give 100 kgs. wheat Will receive 100 kgs. wheat

Will receive Rs. 101 per kg. Will pay Rs. 101 per kg

Date of settlement : March 10, 2013

This is a Forward contract, trade happens today, settlement in future

Contract

Farmer Bread Marker

Will give 100 kgs. wheat Will receive 100 kgs. wheat

Will receive Rs. 101 per kg. Will pay Rs. 101 per kg

Date of settlement : March 10, 2013

Farmers OBLIGATION is to give wheat and the Bread Maker’s OBLIGATION is to pay

ContractTerms :

– Underlying : Wheat– Contract Date : Feb 10, 2013– Contract Price : Rs. 101 per kg– Quantity : 100 kg.– Settlement date : March 10, 2013

• By entering into the contract on Feb 10, 2013 what have the two parties done?Locked in a future price of Rs. 101/- per kg.

Settlement

• On March 10, 2013 :– Farmer gives 100 kg of wheat to the Bread

Maker– Farmer receives Rs. 101/- per kg of wheat

from the Bread maker– The contract entered on Feb 10, 2013 is

settled.– Price of wheat quoting in the spot market

(underlying price) is Rs. 75/- per kg.

Cash Settlement

• On March 10, 2013 :– Price of wheat quoting in the market is Rs. 75/-

per kg.– Who gains? By how much?– Farmer Rs. 26/- per kg.

• Settlement :– Loser pays to the Gainer the profit / loss – Farmer receives Rs. 26/- per kg. from the Bread

Maker

Derivatives

• Instruments whose value is derived from an underlying (Wheat,

Gold, Shares etc.)

• Derivatives cannot exist without the underlying

• Derivatives do not convey any ownership in the underlying

• Settlement : Cash settled or delivery of underlying

– Physical Delivery : Exchange money and goods on final

settlement

– Cash : Settle profit / loss on final settlement

Introduction to Futures

• Futures were designed to solve the problems that existed in the forward markets– Counter Party risk– Liquidity

• Futures contracts are standardized forward contracts that are traded on an exchange

• What are Futures?

• How do they trade on stock exchange?

Trade SettlementInitial margin

Daily Mark to Market Settlement

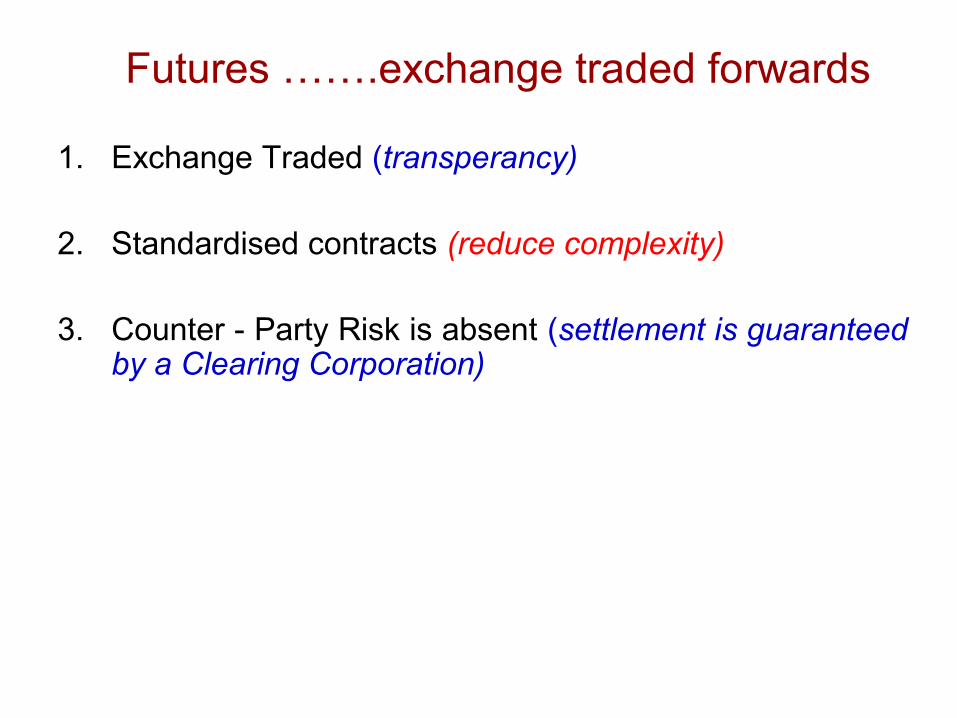

Futures …….exchange traded forwards

1. Exchange Traded (transperancy)

2. Standardised contracts (reduce complexity)

3. Counter - Party Risk is absent (settlement is guaranteed by a Clearing Corporation)

Daily Mark to Market Settlement – Futures contracts

Date

S ep1,2013 11:00 am

Spot Price ofABC Ltd. :

Rs. 490

Mr. Raju BuysABC Ltd. Futures @

Rs. 510

MTM Gain / Loss

Mr. Ajay SellsABC Ltd. Futures @

Rs. 510

MTM Gain / Loss

Remarks :Gainer receives MTM amount from the loser on a daily basis

S ep1,2013 3:30 pm

Rs. 500 Rs. 512 + Rs. 2 Rs. 512 - Rs. 2Ajay Pays Rs. 2 to Raju

S ep2,2013 3:30 pm

Rs. 510 Rs. 520 + Rs. 8 Rs. 520 - Rs. 8Ajay Pays Rs. 8 to Raju

S ep3,2013 3:30 pm

Rs. 495 Rs. 510 - Rs. 10 Rs. 510 + Rs. 10Raju Pays Rs. 10 to Ajay

S ep4,2013 3:30 pm Rs. 505 Rs. 515 + Rs. 5 Rs. 515 - Rs. 5

Ajay Pays Rs. 5 to Raju

S ep5,2013 3:30 pm

Rs. 515 Rs. 525 +Rs. 10 Rs. 525 - Rs. 10Ajay Pays Rs. 10 to Raju

Futures terminology

• Spot price : Price at which asset trades in the

spot market

• Futures : Price at which Futures contracts

trade in the futures market

• Contract cycle : The period over which a contract

trades

• Expiry Date : Last date of the contract

• Contract size : Amount or value of each contract

Futures terminology (cont.)

• Initial margin : Amount deposited initially to

trade futures (by both buyer & seller)

• Cost of Carry : Relationship between futures and spot

price is determined by cost of

carry. For financial assets it is

interest cost.

Contract Life Cycle - example

Futures contracts in NIFTY on Sep 2013: Any given time upto 3months duration contracts.

Contract Month Expiry/settlement date Sep 2013 258h Sep Oct 2013 25th Oct Nov 2013 29th Nov

*Expiry – last Thursday of the month

You are on Sep 22.You have a Near Month, Middle Month and Far Month contractsto choose from.

Initial Margin (IM)Stock (ABC Ltd.) Futures (ABC Ltd. Futures)

Rs. 500 Rs. 510

Buy 1000 shares Buy 1000 Futures

Value = Rs. 5,00,000 Value = Rs. 5,10,000

Pay Rs. 5,00,000 Pay IM = Rs. 51,000

After 10 days :

Rs. 600 Rs. 610

RETURN = 20% RETURN = 196%

Steps in trading Futures

• Pay Initial Margin

• Buy or Sell Futures

• Daily Mark to Market Settlement

Pricing of Futures

• Futures price = Spot Price + Cost of carry

• Cost of carry = interest rate*

• At expiry : Futures price = Spot price

*for financial futures

Pricing - Futures

Feb 10, you have Rs. 100.

How much will it become on March 10.

Depends on how much interest you can earn

If it is 12% p.a., then after 1 month Rs. 100 will become =

Rs. 101

F = S + Int.

Rs. 101 = Rs. 100 + Re. 1

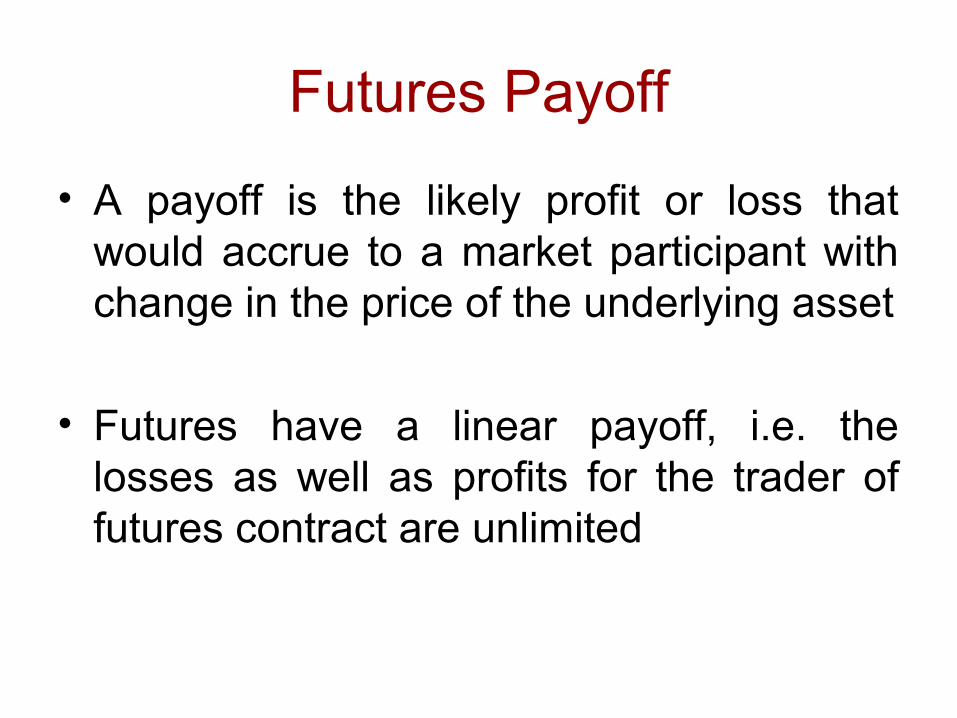

Futures Payoff

• A payoff is the likely profit or loss that would accrue to a market participant with change in the price of the underlying asset

• Futures have a linear payoff, i.e. the losses as well as profits for the trader of futures contract are unlimited

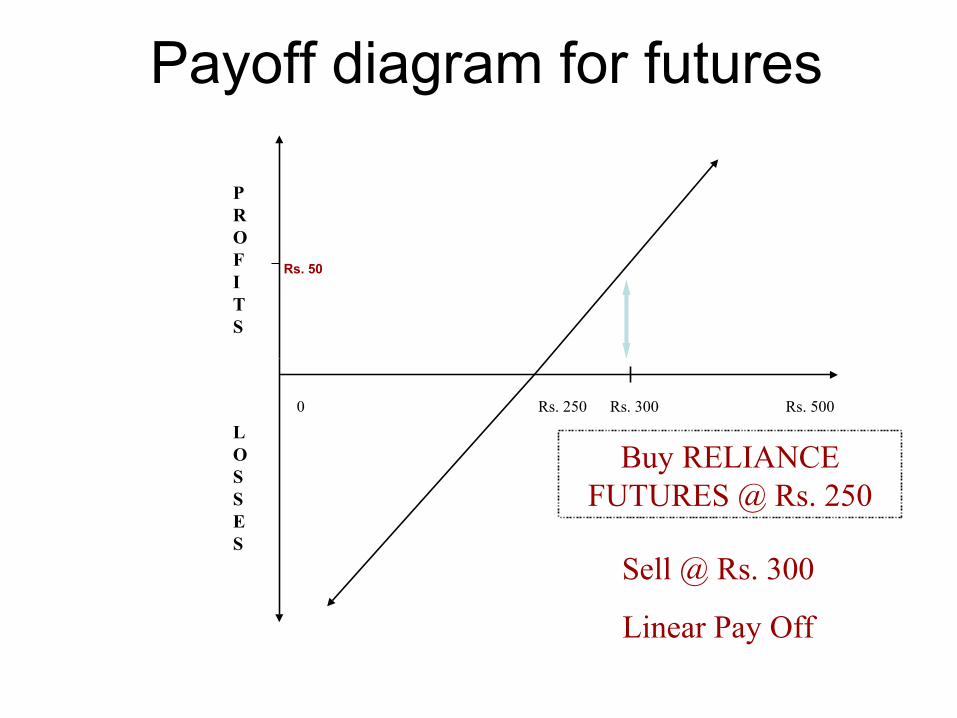

Payoff diagram for futures

PROFITS

LOSSES

Rs. 2500 Rs. 500

Buy RELIANCE FUTURES @ Rs. 250

Rs. 300

Sell @ Rs. 300

Linear Pay Off

Rs. 50

PROFITS

LOSSES

Payoff diagram for futures

Sell RELIANCE FUTURES @ Rs. 250

Buy @ Rs. 200

Linear Pay Off

Rs. 250Rs. 200

Final Settlement – convergence of Futures to Spot

Time

(a)

FuturesPrice

Spot Price

• On the final settlement day/ expiry day, the Futures contract is settled at the underlying closing price (spot price)

• Cash Settlement

Futures

Contract Descriptor:

• FUTSTK ACC 28 SEP2013

• FUTIDX NIFTY28 SEP2013

• Trading in Index Futures

Options

• Hyundai is launching a car - SONATA

• Price is Rs. 15 Lacs. [Purchase price]

• You can book the car by paying Rs. 50,000 [deposit]

Options

• By booking the car, what have you bought?» A RIGHT to buy the car

• When booking matures, can Hyundai force you to buy SONATA?

» Hyundai has only OBLIGATION

• Can you force Hyundai to sell SONATA?

Introduction to Options

An options contract gives the buyer the

right, but not the obligation to Buy or Sell a

specified underlying at a set price on or

before a specified date

: eg. Car Purchase, Insurance

Options

Options: Options are of two types - calls and puts. Calls give the buyer the right but not the obligation to buy. Puts give the buyer the right to sell but not the obligation to sell.

Options

• CALL OPTIONS : Gives the buyer of the Call Option the RIGHT to buy at the STRIKE PRICE

• CALL OPTIONS : The Seller of the Call Option has to meet his OBLIGATION of selling when the buyer EXERCISES his right

• The Buyer retains the RIGHT to Exercise or not Exercise

Options-Terminologies

• Strike Price

• Premium

• Time Value

• Intrinsic Value

• ITM,ATM,OTM

Call Option

• The Buyer of an Options needs to pay to the

Seller the PRICE of the Option.

• This is called as the PREMIUM.

• It is paid immediately on buying the Option.

• The Seller receives the Premium on T+1 day.

Call Option

Sep 15,Underlying Price Strike Price Premium

Rs. 100 Rs. 80 Rs. 30

Sep 28,Underlying Price can be above, at or below Strike Price

Rs. 112Rs. 81Rs. 75

At which underlying price Buyer will exercise the Option ?

Call Option

Sep 15, 2013

Underlying Price

Rs. 100

Strike price

Rs. 80

Premium

Rs. 30

Buyer’s Pay – Off (Dec. 24)

Underlying Pay off Net P/L

Rs. 200 Rs. 120 +Rs. 90

Rs. 160 Rs. 80 + Rs. 50

Rs. 120 Rs. 40 + Rs. 10

Rs. 110 Rs. 80 Rs. 0

Rs. 90 Rs. 10 - Rs. 20

Rs. 80 Nil - Rs. 30

Rs. 70 Nil - Rs. 30

Rs. 50 Nil - Rs. 30

Call Option• Buyer : Unlimited Profits, Limited Losses

• Seller : Unlimited Losses, Limited Profits

• Buyer : Losses Limited to the premium (max. loss)

• Seller : Profits Limited to the premium

(max. gain)

Call Option

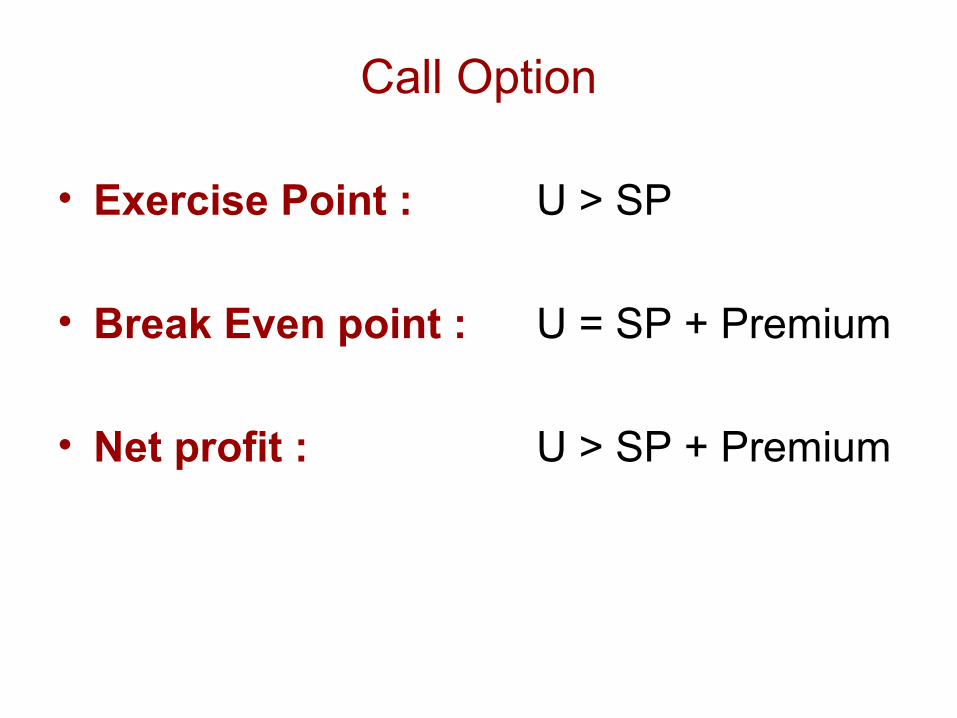

• Exercise Point : U > SP

• Break Even point : U = SP + Premium

• Net profit : U > SP + Premium

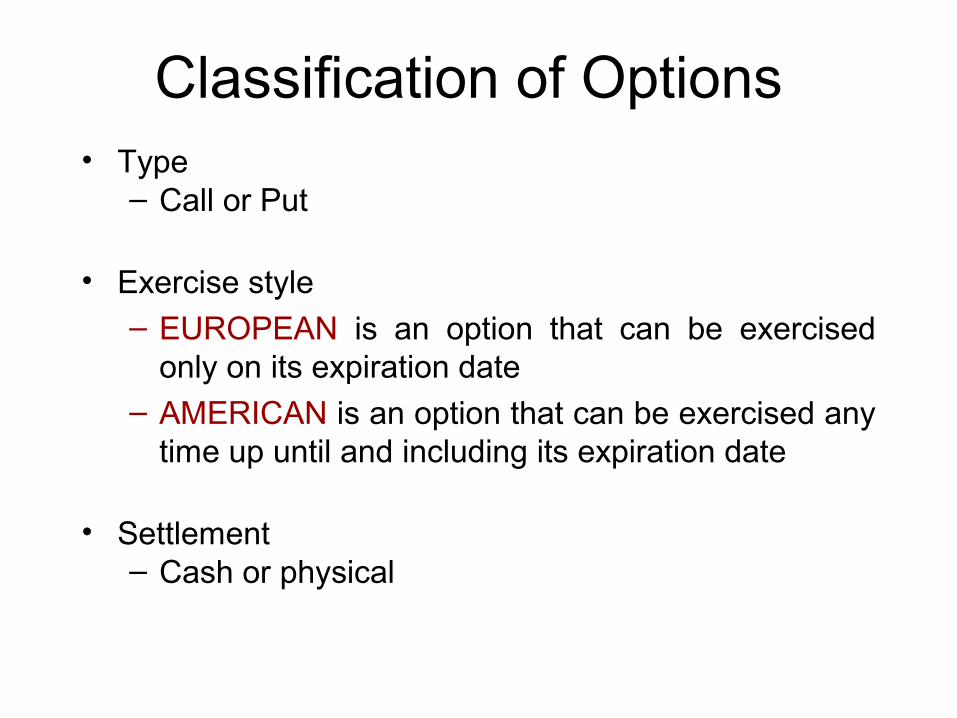

Classification of Options• Type

– Call or Put

• Exercise style

– EUROPEAN is an option that can be exercised only on its expiration date

– AMERICAN is an option that can be exercised any time up until and including its expiration date

• Settlement– Cash or physical

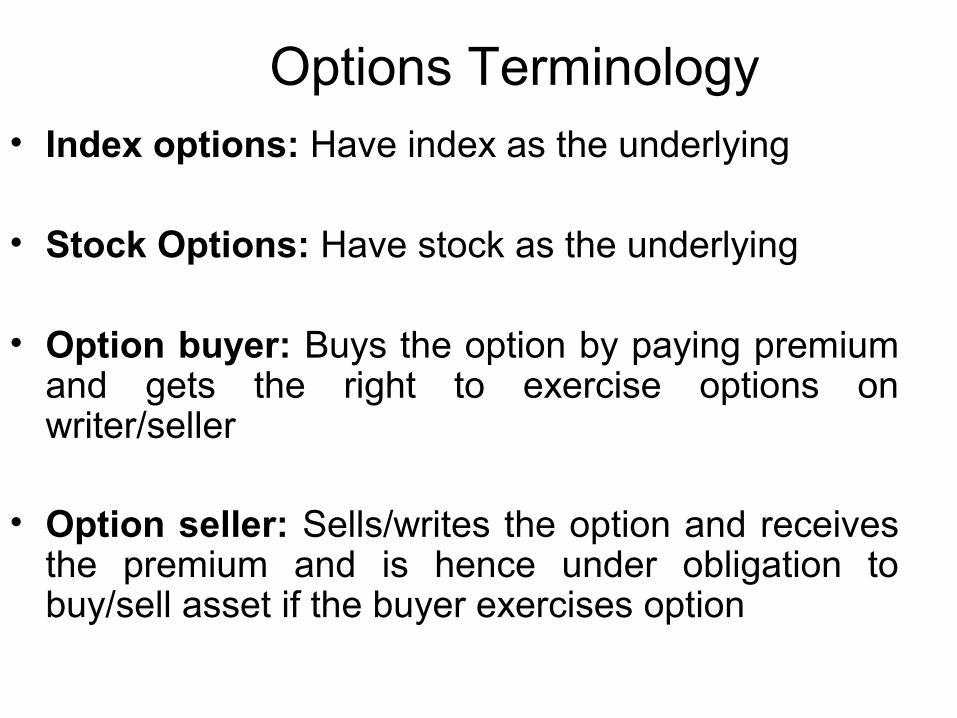

Options Terminology• Index options: Have index as the underlying

• Stock Options: Have stock as the underlying

• Option buyer: Buys the option by paying premium and gets the right to exercise options on writer/seller

• Option seller: Sells/writes the option and receives the premium and is hence under obligation to buy/sell asset if the buyer exercises option

• Option premium: Price paid by the buyer to seller to acquire the right. Comprises of Intrinsic Value and Time Value

• Strike / Exercise price: Price at which the underlying may be purchased or sold

• Expiry date: It’s last Thursday of the month for options to be exercised/ traded. Options cease to exist after expiry

Options Terminology

Options Payoff

• Optional characteristics of options results in a non linear payoff for options. Non linear payoffs provide flexibility to create combinations

• Losses of the buyer is limited to the premium paid and profits are unlimited

• For writers/sellers losses are unlimited and profits limited to the premium received

THE PAY OFF DIAG. - OPTIONS

• PROFITS AND LOSSES ON CALLS AND PUTS• Security – ACC

100

PROFITS

CALLS

LOSSES

100

LOSSES

PROFITS

PUTS

20 120

20

80

Exercises……….

Options

Contract Descriptor:

• OPTSTK ACC 420 28SEP2013 CE

• OPTIDX CNXIT 2200 24NOV2013 PE

• OPTIDX NIFTY 6000 24NOV2013 PE

RIGHTCALLS Buyer Buy at the strike price at expiry

OBLIGATIONSeller Sell at the strike price at expiry

RIGHTPUTS Buyer Sell at the strike price at expiry

OBLIGATIONSeller Buy at the strike price at expiry

CALLS & PUTS – RIGHTS AND OBLIGATION

BUYER OF AN OPTION

PAYS PREMIUM

PREMIUM IS THE MAXIMUM LOSS THE BUYER CAN SUFFER

SELLER OF AN OPTION

RECEIVES PREMIUM

PREMIUM IS THE MAXIMUM PROFIT THE SELLER CAN MAKE

APPLICABLE FOR BOTH CALLS AND PUTS

Understanding Premium

Premium is the price paid buy the Buyer to acquire an Option

Premium = Intrinsic Value of the Option + Time Value

Call Option Strike Price = Rs. 150 Underlying = Rs. 165

Calculate Premium?

Put Option Strike Price = Rs. 167 Underlying = Rs. 178

Calculate Premium

Spot value of NIFTY is 2240. An investor buys a oneMonth NIFTY 2227 put option for a premium of Rs.17.The option is________.

• Out of the money

• In the money

• At the money

• Above the money

NCFMNCFM

A call option that is out-of-the-money or at-the-money has ________.

only time value only intrinsic value

face value no value

NCFMNCFM

A put option is in-the-money if the price ofthe underlying asset is __________ thestrike price.

• Above• Below• Equal to• Between the premium and strike price

NCFMNCFM

Spot value of NIFTY is 2230. An investor buys a one

Month NIFTY 2245 call option for a premium of Rs.5.

After One month the spot value of NIFTY is 2250. The

Option is _________.

• In the money

• At the money

• Above the money• Out of the money

NCFMNCFM

An index put option at a strike of Rs. 2176 is selling at a premium of Rs. 28. At what index level will it break even for the buyer of the option?

•Rs. 2148•Rs. 2196•Rs. 2204•Rs. 2194

NCFMNCFM

www.nseindia.com

Certain Concepts - Options

• In the money- positive cash flow if

exercised

immediately

• At the money - zero cash flow if

exercised immediately

• Out of the money - negative cash flow if

exercised

immediately

Options

• New contracts are introduced at the ‘End of Day’ based on the underlying prices

• There would be minimum :

5 ITM

1 ATM &5 OTM contracts available

Options contracts (example)

Underlying - ACC Ltd. Rs. 100 Rs. 120 Rs. 125

Rs. 115 OTM contracts Rs. 110

Rs. 105ATM Rs. 100

Rs. 95 ITM contracts Rs. 90

Rs. 85 Rs. 80 Rs. 75

• Each month, Calls & Puts• Minimum number of strikes – 66(11 X 2 X 3)

Option - Strike Price Intervals• For Nifty Options - 10• For Options on Individual Securities:

Price of UnderlyingStrike Price Interval

Rs.

Less than or equal to Rs. 50 2.5

>50 ≤Rs.250 5

>250 ≤Rs.500 10

>500 ≤Rs.1000 20

>1000 ≤Rs.2500 30

>Rs.2500 50

Intrinsic value

Price of an option is called ‘Premium’

Premium = Intrinsic value + time value

Intrinsic value is the amount the contract is inthe money –e.g. Spot = 1000, Strike Price = 990 March CallPremium = Rs 15 (Intrinsic value = Rs. 10, timevalue = 5)

Exercises…………..

Options Pricing

• Intrinsic Value (IV )

Difference between spot and strike

ITM has IV, ATM and OTM have zero IV

• Time Value ( TV )

Difference between the premium and intrinsic value

ITM have both IV and TV, ATM and OTM have only TV

Longer the expiry more the TV, on expiry TV is 0

APPLICATIONS

Has a directional view on the market.

No position in the underlying.

Bullish : Buy Futures

Bearish : Sell Futures

Have a view on a security?•Believe market would go up

•What you can do today•Buy the security•Pay the entire money and take delivery

•What is the issue?•Costly to buy the security

•Opportunity cost of the investment

• What you could do •Buy Futures

Have a view on a Stock? Assumed figures

• 01 Sep 2013

• feels the market will rise– Buys 1 contract of Near month ABC Ltd. futures at Rs. 260 (market lot : 1000)

• 09 Sep 2013–ABC Ltd. futures has risen to Rs. 280– Sells off the position at Rs. 280

–Makes a profit of Rs.20000 (1000*20)

Have a view on the Market?• Believe market would go down

•What you can do today•Sell the security•Arrange for delivery by borrowing of security

• What is the issue?•Procedures of borrowing of securities•Cost of borrowing•Limited lenders and stringent conditions

• What you could do•Sell Futures

Have a view on a Stock? Assumed figures

• 1st Sep 2013• feels the market will fall•Sells 1 contract of March ABC Ltd. futures at Rs. 285 (1 contract is 1000 shares)

25th Sep 2013•ABC Ltd. Futures contract is trading at Rs. 265•Squares off his position at 265 •Makes a profit of Rs.20000 (1000*20)

Leverage

• Beginning of investment

– Shares of Reliance are trading at Rs.250– March futures are trading at Rs.260

• End of Investment– Shares of Reliance are trading at Rs.260

– March futures are trading at Rs.270

• Assume a margin of 15% for SSFs• Compare returns in securities with SSFs

Leverage

ABC Ltd. ABC Ltd. Futures

Initial price Rs.250 Rs.260

Initial Investment Rs.250 Rs.39 (IM)

Squaring up price Rs.260 Rs.270

Net gain Rs.10 Rs.10

Retn on investment 4.00% 25.64%

Hedging

• HEDGERS are traders who buy or sell to offset a risk exposure in the spot market

• Beta measures relationship between movement of the market (index) to the movement of the stock, e.g. HINDLEVER has a Beta of 1.30

• Index has beta of 1

• To hedge, sell Index Futures

• This is known as hedging

Hedging• When you Buy a Stock what do you get?

RISK

UNSYSTEMATIC SYSTEMATIC

•Company Specific Risk

•Diversifiable Risk

•Market Specific Risk

•Non-Diversifiable Risk

Nifty Futures

• It is a Futures contract on the Nifty index• Just like Reliance Futures is a futures contract

on Reliance Industries Ltd., Nifty Futures is a contract on the Nifty index

• If you feel Reliance share price will go up you buy Reliance Futures

• If you feel Nifty will go up, buy Nifty Futures• Cash settled

Have a view on the Market? Assumed figures

• 01 March 2007– feels the market will rise– Buys 1 contract of Near month Nifty futures at Rs. 2800 (market lot : 50)

• 09 March 2007–Nifty futures has risen to Rs. 2850– Sells off the position at Rs. 2850

–Makes a profit of Rs. 2500 (50*50)

Hedging – Managing market risk•14th March

• An investor buys HLL worth Rs. 900,000 @ Rs. 290 per share (3100 shares)•The expiry date of Nifty March futures is 27th Mar •Nifty index is at 4100 and Nifty futures is trading at Rs. 4110•The beta of Hindlever is 1.13•To hedge the investor needs to sell [Rs. 9,00,000*1.13] = Rs. 10,17,000 worth of index futures (= 250 Nifty Futures)

•19th March•Nifty futures is trading at Rs. 3915 and HLL is trading at Rs. 275 •Investors loss in HLL is Rs. 46,500•Nifty Futures position gains by Rs. 48,750•Investor gains Rs. 2250/-

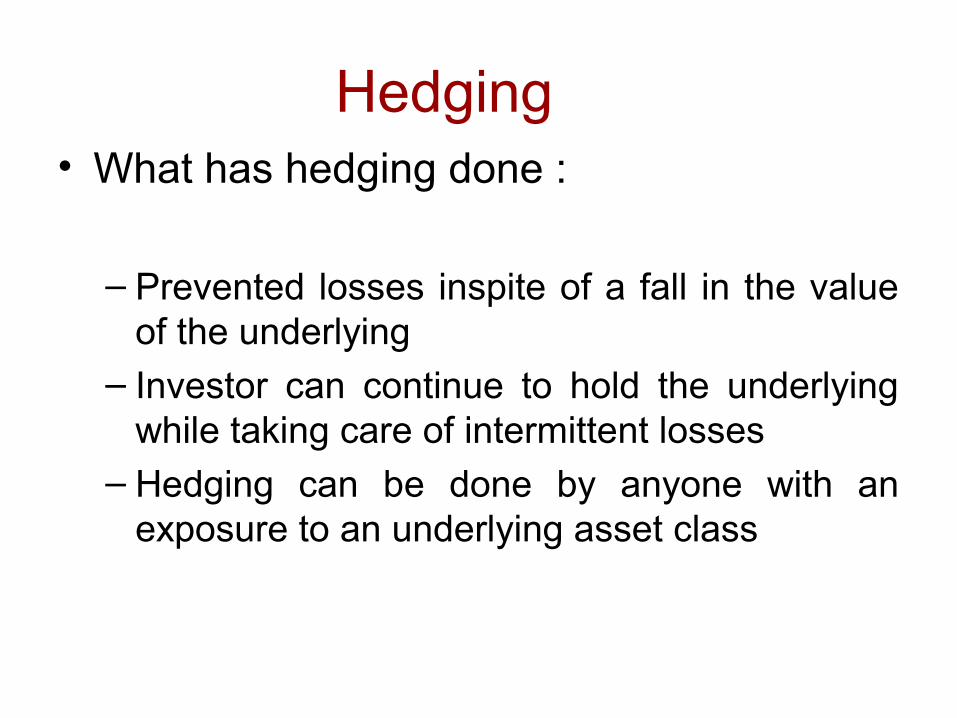

Hedging• What has hedging done :

– Prevented losses inspite of a fall in the value of the underlying

– Investor can continue to hold the underlying while taking care of intermittent losses

– Hedging can be done by anyone with an exposure to an underlying asset class

Hedging using Stock Futures

– Investor buys 2000 shares of Infosys @ Rs. 390

– Portfolio value is Rs. 7,80,000

– Infosys near month futures trades at Rs. 402

– To hedge, sell 2000 Infosys futures

– Underlying spot price falls to Rs. 300 on expiry

– Loss on Shares – Rs. 180,000

– Profit on Futures – Rs. 204,000

– Net gain = Rs. 24,000

www.nseindia.com

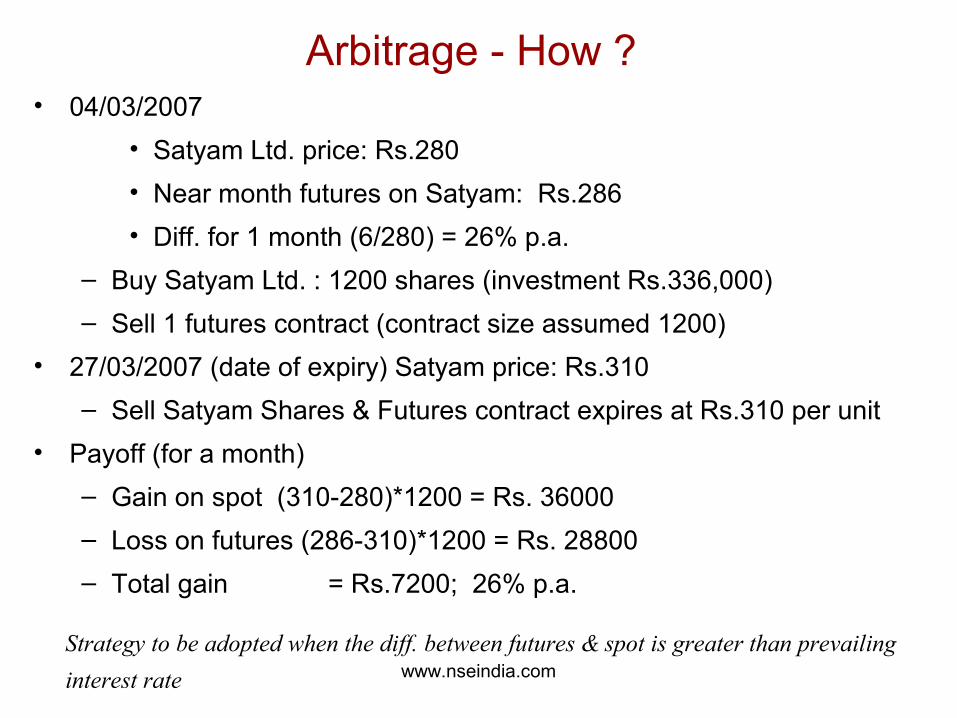

Arbitrage - How ?• 04/03/2007

• Satyam Ltd. price: Rs.280

• Near month futures on Satyam: Rs.286

• Diff. for 1 month (6/280) = 26% p.a.

– Buy Satyam Ltd. : 1200 shares (investment Rs.336,000)

– Sell 1 futures contract (contract size assumed 1200)

• 27/03/2007 (date of expiry) Satyam price: Rs.310

– Sell Satyam Shares & Futures contract expires at Rs.310 per unit

• Payoff (for a month)

– Gain on spot (310-280)*1200 = Rs. 36000

– Loss on futures (286-310)*1200 = Rs. 28800

– Total gain = Rs.7200; 26% p.a.

Strategy to be adopted when the diff. between futures & spot is greater than prevailing

interest rate

Options

Share Call Option

Initial price Rs.250 Rs.260

Initial Investment Rs.250 Rs. 2

Squaring up price Rs.300 Rs.300

Net gain Rs.50 Rs.38

Retn on investment 20.00% 1900.00%

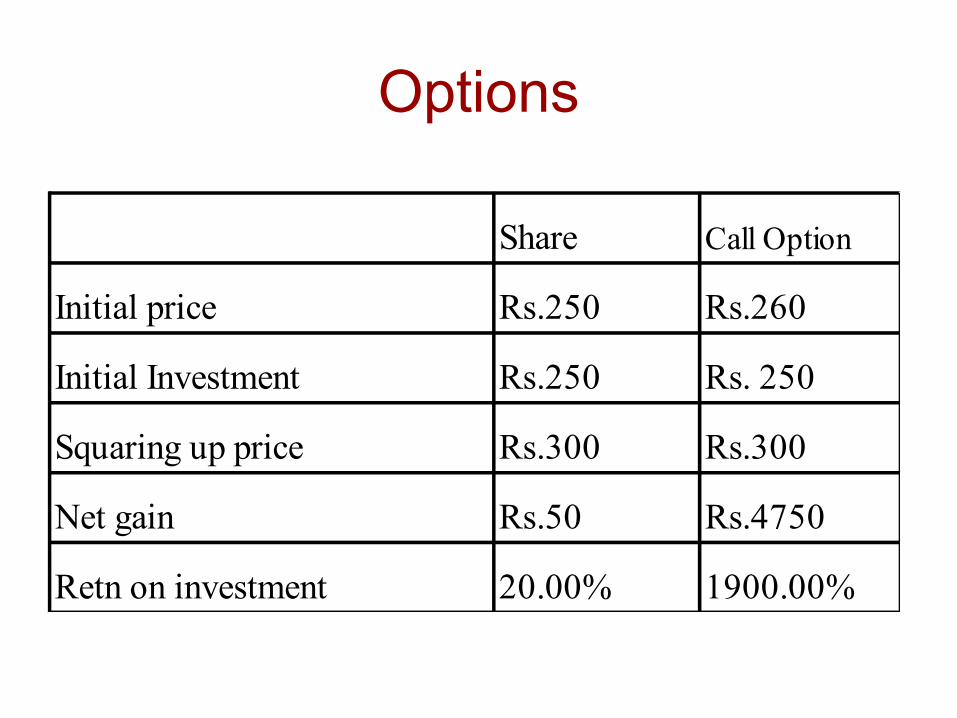

Options

Share Call Option

Initial price Rs.250 Rs.260

Initial Investment Rs.250 Rs. 250

Squaring up price Rs.300 Rs.300

Net gain Rs.50 Rs.4750

Retn on investment 20.00% 1900.00%

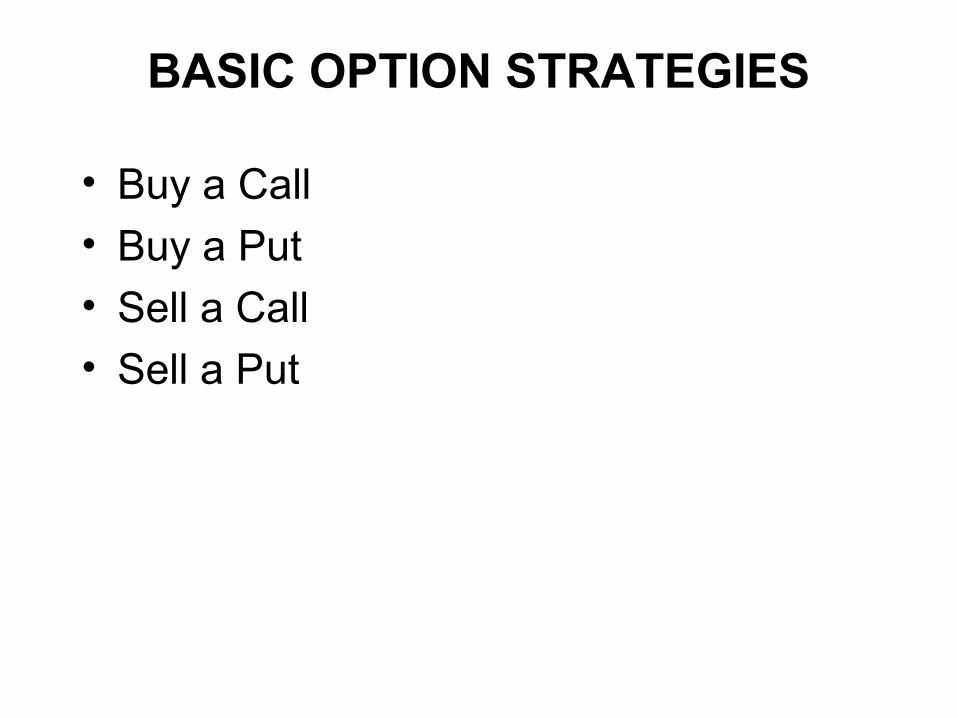

OPTION STRATEGIES

BASIC OPTION STRATEGIES

• Buy a Call

• Buy a Put

• Sell a Call

• Sell a Put

ADVANCE OPTION STRATEGIES

• Bullish Vertical Spreads Using Calls Using Puts

• Bearish Vertical Spreads Using Calls• Straddle Long Straddle Short Sraddle• Strangle Long Strangle Short Strangle• CoveredCall

• Butterfly Spread

Bullish Vertical SpreadsUsing Calls

• View- Underlying price will go up– But likes to reduce the cost – Buy a lower strike call and sell a higher strike call

– Example– Spot is 6000, Go long on 5800 strike Call by paying premium of Rs.

300 and sells a call of 6200 strike receiving a premium of Rs.145

– If price goes to 6200– Net position= 400-300+145=245 (max profit)– If price goes to 5500– Net Position=-300+145=155 (Max loss) – It is a limited profit and limited loss position– BEP is 5955

Bullish Vertical SpreadsUsing Puts

• View- Underlying price will go up– Net premium receipt strategy – Buy a lower strike put and sell a higher strike put

– Example– Spot is 6000, Go short on 6200 strike put by receiving premium of

Rs. 220 and buys a put of 6000 strike paying a premium of Rs.170

– If price goes to 5500– Net position= 220-700+500-170=-150 (max loss)– If price goes to 6500– Net Position=220-170=50 (Max profit) – It is a limited profit and limited loss position– BEP is 6150

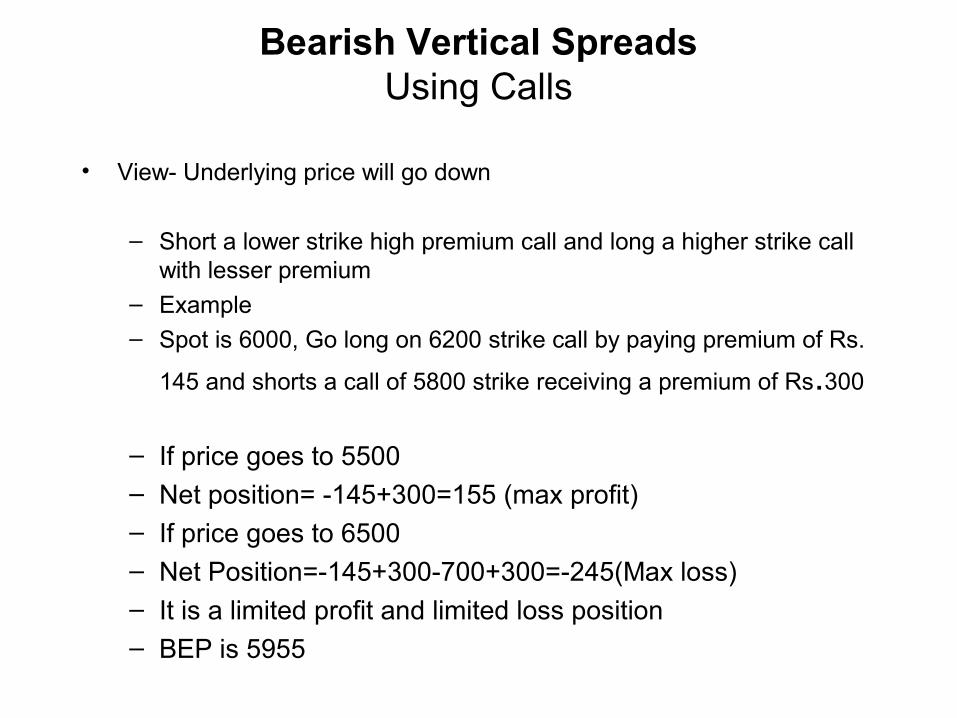

Bearish Vertical SpreadsUsing Calls

• View- Underlying price will go down

– Short a lower strike high premium call and long a higher strike call with lesser premium

– Example– Spot is 6000, Go long on 6200 strike call by paying premium of Rs.

145 and shorts a call of 5800 strike receiving a premium of Rs.300

– If price goes to 5500– Net position= -145+300=155 (max profit)– If price goes to 6500– Net Position=-145+300-700+300=-245(Max loss) – It is a limited profit and limited loss position– BEP is 5955

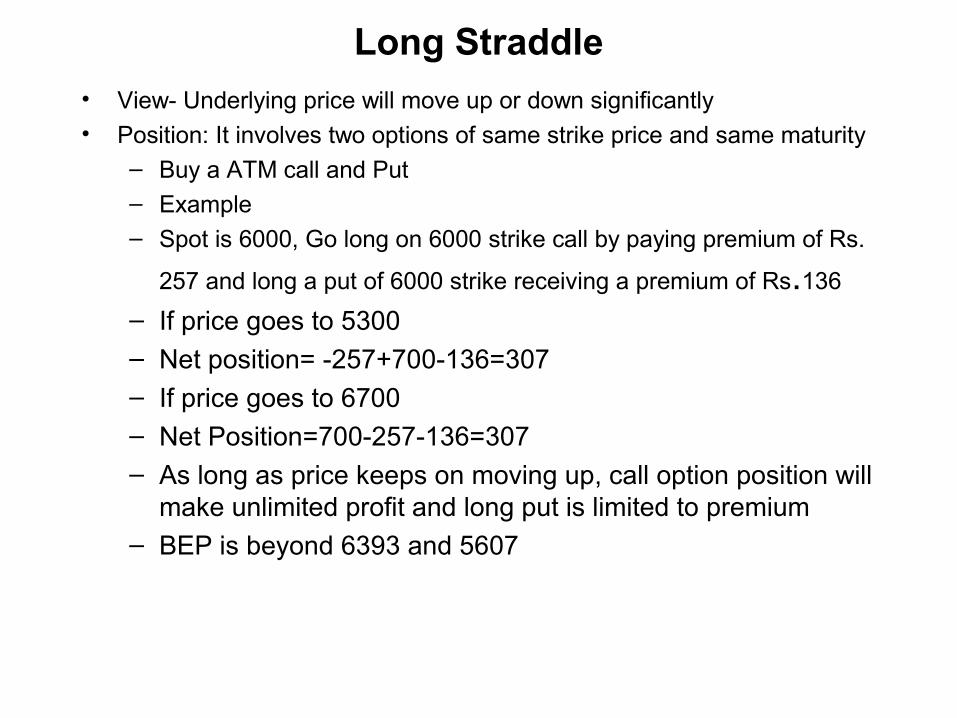

Long Straddle

• View- Underlying price will move up or down significantly• Position: It involves two options of same strike price and same maturity

– Buy a ATM call and Put– Example

– Spot is 6000, Go long on 6000 strike call by paying premium of Rs.

257 and long a put of 6000 strike receiving a premium of Rs.136

– If price goes to 5300– Net position= -257+700-136=307 – If price goes to 6700– Net Position=700-257-136=307– As long as price keeps on moving up, call option position will

make unlimited profit and long put is limited to premium– BEP is beyond 6393 and 5607

Short Straddle

• View- Underlying price would not move much or stable• Position: It involves two options of same strike price and same maturity

– Net receipt of premiums– Example

– Spot is 6000, Go short on 6000 strike call by receiving premium of Rs. 257 and short a put of 6000 strike receiving a premium of

Rs.136

– If price goes to 5800– Net position= 257-200+136=193 – If price goes to 6400– Net Position=257-400+136=-7– It is limited profit and unlimited strategy.– Will make profit if the price closes between 6393 and 5607