Embed Size (px)

DESCRIPTION

Citation preview

CREDIT MANUAL – POLICIES/SCREENSTWO WHEELER LOAN

Version 2.1

1STRICTLY CONFIDENTIALRISK MANAGEMENT

Contents

What we Fund

General Guidelines for credit policy

BAFL Business

Funding & Approval Parameter

Credit Guidelines

Documentation

Appendix

Annexure-Special Policy

2STRICTLY CONFIDENTIALRISK MANAGEMENT

What We Fund

New Asset Funding- LoanThis is the most common form of funding which BAFL offers to its customers .On this customer borrow fund from BAFL for purchase of new Two wheeler / Three wheeler .Usually customer invest a margin of 15% to 40% of the asset cost and borrows rest from BAFL .

Funding guidelines

Sourcing screen- Basic credit norms based on which cases would be sourced

Approval screens-Specific credit norms based on which cases would be approved

Deviation Matrix- Matrix for approval where specific credit norms are not met but having relevant mitigants for funding

3STRICTLY CONFIDENTIALRISK MANAGEMENT

General Guidelines for Credit Policy

Product wise policiesNormal PolicyNinja Policy

Customer profile wise policiesSalariedSelf EmployedAgri based

Program wise policiesIncome proof policySurrogate Income proof policyNo Income Proof

Demographic policiesState wise policiesStudent policiesNRI policies

Repayment mode –Repayment by Equated Monthly Installments (EMI)Post Dated Cheques (PDC)- only with MICR codeAuto Debit Mandate (ADM)Electronic Clearing System (ECS)Direct Cash Collection (DCC)

4STRICTLY CONFIDENTIALRISK MANAGEMENT

BAFL

3-Wheeler2-Wheeler

PassengerGoods Carrier

NinjaPlatinaDiscoverAvengerPulsar

Origination

Credit

Funding

Booking

Monitoring

Collection

Decentralized: At Dealer/ASC locations across India

Decentralized: At CSM locations pan India

Centralized: At SumaSoft- Pune

Centralized: At BAFL HO -Pune

Centralized: At HO Credit -Pune

Decentralized: At all locations

BAFL BUSINESS

5STRICTLY CONFIDENTIALRISK MANAGEMENT

Funding & Approval Parameters

6STRICTLY CONFIDENTIALRISK MANAGEMENT

FUNDING PARAMETERSSourcing screen

7

Parameter Salaried Self Employed Agri Based Funding

Minimum Age1*18 years (With co-applicant till

age of 21 years)***18 years (With co-applicant till

age of 21 years)***18 years (With co-applicant

till age of 21 years)***

Maximum Age at completion of tenure **

60 years 60 years 60 years

Minimum IncomeRs 4000 NTH pm

Rs 8000 NTH for cat ‘A’ towns****

Rs 60000/- p.aRs 100000/- pa for cat ‘A’

towns****Rs 48000/- p.a

Phone (No phone No loan)2*

WLL, Landline or Post paid/Prepaid mobile mandatory

WLL, Landline or Post paid/Prepaid mobile mandatory

WLL, Landline or Post paid/Prepaid mobile

mandatory

Dedupe Mandatory Bad status not fundable Bad status not fundable Bad status not fundable

Residence Stability3* 1 year 1 year 1 year

Business/ Office Stability4*

1 year 2 year2 year with ownership

proof of land

Tenure 36 Months 36 Months 36 Months

*Please refer notes on Slide no. 10

** Deviation of 5 years available at L4 level

***Applicants earning Family members should be taken as co applicant, for co-applicant refer credit norm

**** Cat A towns are , Delhi, Mumbai, Pune, Kolkata, Chennai, Bangalore, Hyderabad & Ahmedabad & Income is including family income

STRICTLY CONFIDENTIALRISK MANAGEMENT

8

APPROVAL PARAMETERS-SALARIED & S. EMPLOYED

STRICTLY CONFIDENTIAL

Particulars Parameters Salaried Self Employed Remarks

Funding Value Max Disb Amt 70,000 70,000

LTV % LTV on road price 85% 85%(Whichever is lower i.e. Funding or LTV)

CIBIL CIBIL report Compulsory Compulsory Refer Anexure-1 for locations

Dedupe Dedupe report Compulsory Compulsory Refer Annexure-2

Contact point verification

Residence Mandatory As per Annexure Refer Anexure-3 for Self employed

Office Compulsory in case of no landline at office As per Annexure Refer Anexure-3 for Self employed

TVR Compulsory at office landline Compulsory Reference TVR compulsory

Permanent AddressCompulsory in case rented less than a year &

no landline at permanent addressCompulsory in case rented less than a year

& no landline at permanent address

Phone Connection 2* Phone AvailabilityWLL, Landline or Post paid/Prepaid mobile

mandatoryWLL, Landline or Post paid/Prepaid mobile

mandatory₂Refer Notes to Approval Parameter

Residence 5* Ownership Owned/Parental/Rented/Leased Owned/Parental/Rented/Leased Refer Anexure-3 for Self employed

Income Proof Up to 85% LTV

Any income docs as per Annex-4 &Compulsory Income assessment form for

applicant < 12000/- salary in Cat A towns &Applicant< 8000/- salary in other towns p.m.

Any income docs as per Annex-4 &Compulsory Income assessment form for applicant < 12000/- earning in Cat “A”&

Applicant< 8000/- earning in other towns p.m

Refer Annexure-4 for complete document list

Surrogate Income Proof Up to 70% LTVCompulsory Income assessment form

to establish cash inflow of customerCompulsory Income assessment form

to establish cash inflow of customerRefer Annexure-5 for complete document list

No Income ProofUp to 75% with Own House

Compulsory Income assessment form Compulsory Income assessment form Refer Annexure 12

Cash flow to EMI Cash Flow1:03 1:03 Annexure-6 for Income assessment

form to derive cash flow

Bank Statement3 months bank statement

Compulsory to collect 3 month bank statement for Non DCC cases

Compulsory to collect 3 month bank statement for Non DCC cases

Refer point 10 in notes on slide no. 10

FI External AgencyIf CIBIL=>800 & current address & address on

CIBIL report should match then FI waiverIf CIBIL=>800 & current address & add. on CIBIL report should match then FI waiver

For CIBIL norms & locations, refer Annexure 1 & Appendix A resp.

Reference Minimum 2 As per Application Form & cross check in TVRAs per Application Form & cross check in

TVR

Maximum Tenor In Years 3 3

Approval Authority LTV and Model CSM/ASM/RM CSM/ASM/RMRefer Annexure 7 for Max LTV and approval authority

Schemes For exposure NIP,IP & SIP NIP,IP & SIP

Post Disbursement Doc RC Copy Regn copy with Hyp of BAFL Regn copy with Hyp of BAFL Refer Annexure 8 for trigger

Post Disb Asset Verification

PDAV report Optional Optional

Please refer notes on Slide No. 10

9

APPROVAL PARAMETERS- AGRI BASED FUNDING

Particulars Parameters Agri Based Funding

Funding Value Max Disbursement Amt 52000

LTV (Whichever is lower i.e Funding or LTV)

% LTV on road price 80%

CIBIL CIBIL report As per CIBIL location list

Dedupe Dedupe report Compulsory

Contact point verification

Residence Compulsory

Agri Land FI Optional

TVR Compulsory

Phone Connection 2* Phone Availability WLL, Landline or Post paid/Prepaid mobile compulsory

Residence 5* Ownership Owned

Income Proof Up to 80% LTV Refer Annexure 10

Surrogate Income Proof Up to 70% LTVLand Document of min 1 acre wet land with Agri survey

form- 6* ( more than 25 Kms)

No Income Proof Up to 75% LTV & Own landCompulsory Agri survey form -6*along with 1 acre wet

land docs, land to be within 25 Kms from house

Cash flow to EMI Cash flow to EMI 1:03

FI External Agency Compulsory

Reference Minimum 2 As per Application Form & cross check in TVR

Maximum Tenor In Years 3

Approval Authority LTV and Model Refer Annexure 7 for Max LTV and approval authority

Schemes Income NIP,IP & SIP

PDD RC Copy Regn copy with Hypothecation of BAFL- Refer Annex-8

Post Disb Asset Verification PDAV report Optional

STRICTLY CONFIDENTIALRISK MANAGEMENT

10

Notes to Approval Parameters

STRICTLY CONFIDENTIALRISK MANAGEMENT

S. No. Approval Parameter Definition

1 Co-applicant norm- Applicant blood relatives include Parents, Spouse,Son,Daughter,Brother, Sister staying in same city

2Pre paid connection to be accepted only in case of owned house in the name of applicant/parents/wife and valid rent/lease agreement

3Residence stability norm states the stability in current stay and if current stay is less than 1 year then immediate previousstay should be => 1 year in the same city . In case previous stability is not for the same city then refer Deviation Matrix

4Office stability norm states the stability in current job/business and if current stability is less than as per norm then immediate previous job/business should be as per norm in the same city . In case previous job/business is not for the same city then refer Deviation Matrix . In case of Agri profile it should be ownership of land for min 2 years

5In case of rented residence with bachelor accommodation ,permanent address to be obtained and captured in Application form.TVR to be conducted on permanent address on landline only . In case of absence of landline FI at permanent address to be conducted . If no phone at permanent address then no loan .

6

7/12 extract or similar docs of land to be collected and the same can be in the name of father/Grand father .There should be documentary evidence of relationship with applicant. For grandfather , documentary evidence can be Ration Card , Election card , Electricity bill , letter from sarpanche / Talathi office mentioning grandfather’s name as part of father’s name .In case of land in the name of father he should be co-applicant. The hologram should be checked carefully on document for authenticity. The Agri survey form should be filled and signed by customer and CSM. In case form filled by ASC then CSM to verify all details during TVR and confirm in writing in TVR

7 Ownership proof mandatory for residence(owned)/office (owned) mandatory in case of Self Employed

8Compulsory documents- Itemized bill for post paid connection of latest one latest month & can be treated as address proof in case address is same as current stay

9No funding to Negative profile as per Annexure -7 and limited funding with RM sign off to High Risk profile (HRP)-Annexure-8

10

Bank Statement for 3 months for Non DCC cases only.• First page of the bank Pass book is compulsory/Computerized statement with account opening date &

address/Welcome letter from bank for account opening along with latest ATM slip• No cheque return charges or minimum balance charges• Repayment Instruments to be collected from the same account

RISK MANAGEMENT STRICTLY CONFIDENTIAL 11

CIBIL Norms:-

1. It is compulsory to do CIBIL check for all the cases sourced in locations mention in Appendix A

2. CIBIL detect for 10 metros

• Delhi

• Mumbai

• Pune

• Kolkata

• Chennai

• Bangalore

• Hyderabad

• Ahmadabad

• Bhopal

• Jaipur

• Surat

3. Compulsory to insert print out of CIBIL report in the file /agreement (even if no match found or

Score is -1 or 0).

Annexure-1- CIBIL Norms

12

Annexure-2- Dedupe Status

STRICTLY CONFIDENTIALRISK MANAGEMENT

Dedupe Status Explanation Funding

Good Good existing track with BAFL Eligible for funding as per credit policy

Refer Not clear on track and subjective Not eligible for funding

W Existing customer < 6 months Not eligible for funding

Bad Existing customer with poor track record Not eligible for funding

New New case booked but no EMI deposited Not eligible for funding

*Note: •No match found in dedupe can be considered for finance subject to meeting other credit norms•Dedupe report is compulsory to be put in the file before approval•No report in the file will be treated as no dedupe done

Annexure-3- Self employed funding norms

13STRICTLY CONFIDENTIALRISK MANAGEMENT

Self Employed Norms

Up to 75% funding 75% to 85% funding Compulsory Documents

Owned House irrespective of office status

Yes Yes Ownership proof of house

FI pointOffice only with ownership proof of

residenceOffice only with ownership

proof of residence

Rented House and owned office

Yes with ownership proof of officeYes with ownership proof of

officeOwnership proof of office

FI point Office only Office and residence both

Rented House & office both

Yes , with registered rent agreement of office or resi and landline/WLL &

Post paid connection/Pre paid connection

Yes , with registered rent agreement of office or resi and

landline/WLL & Post paid connection/Pre paid connection

Registered rent/lease agreement & landline number

of office/resi

FI point Both at office and residence Both at office and residence

Residence cum office-owned

Yes with ownership proof of houseYes with ownership proof of

house Ownership proof

FI point Residence cum office Residence cum office

Residence cum office-rented

No Yes under Deviation MatrixITR/Sales Tax Return/Trade Certificate & Pan Card copy

FI point NA Resi cum office

14

Annexure-4- IP document list

STRICTLY CONFIDENTIALRISK MANAGEMENT

70 -85 % Income Proof- Any one proof to be submitted from the below list

Income proof- Salaried profile only

Latest salary slip with not more than 45 days old

Latest Form 16 with employee Id

Income Tax Return copy for current Assessment Year

Income proof- Self Employed profile only

Latest Income Tax return for current Assessment Year

Tax challans with ITS 2

Sales Tax Return

Audit certified reports

TDS certificate of the same Financial year

Bank Statement-Salaried & Self Employed

For previous six months with ABB=>1.5 times of EMI

No cheque bounce and minimum balance charge in last six months

Minimum 3 transaction per month with regular cash flow

PDC/ECS to be collected from the same account

15

Annexure-5- SIP document list

STRICTLY CONFIDENTIALRISK MANAGEMENT

up to 70% Surrogate Income Proof- Any one proof to be submitted from the below list

Bank Statement for 3 months

If the salary is credited in the bank than minimum 3 salary credit should get reflected in the statement

In case of self employed minimum 3 transaction per month should be available

Average bank balance should be >=EMI

No cheque return charges or minimum balance charges

PDC/ECS to be collected from the same account

Landline/Post paid connection

Connection should be minimum 3 months old

Average billing of Rs 750/- in mobile or Rs 250/- in landline(BSNL/MTNL) should be there per month

No prior unpaid dues to be reflected in the bills

Address mentioned on the bill should be of the place of current stay

Ownership of Car/Tractor -Collection of RC copy

Data of Applicant on the RC should be the same as per application form

Date of RC issuance should not be more than of 5 year

If the vehicle is not HP free then the track should be referred through bank statement/CIBIL/RTR

In case of Tractor ownership land documents to check for establishing level of harvesting and cash flow

PPF Account-collection of PPF statement

Account statement/Bank pass book should be in the name of applicant only

Statement should reflect the deposition of minimum Rs 12000/- in current financial year or previous year

There should be at least 3 deposition in last 6 months

Applicant detail should match with the details provided in Application Form

Mutual Fund SIP statement

MF statement should be in the name of applicant

Minimum of 12 months statement required with minimum of Rs 1000/- contribution

Applicant details should match with the details provided on Application form

Contd…

16

SIP list continues..

STRICTLY CONFIDENTIALRISK MANAGEMENT

up to 70% Surrogate Income Proof- Any one proof to be submitted from the below list

Life Insurance Policy

Policy should be =>12 months which belongs to LIC, HDFC standard , Max Newyork, Bajaj Allianz, SBI, ING, Tata AIG , Bharti Axa

Monthly subscription of Rs 600/- minimum towards the policy

If premiums are quarterly /annual than same needs to be calculated monthly to arrive at contribution

In case of quarterly or annual premium proof of last premium paid should be collected

In case of last premium paid is beyond 3 months than Policy continuity certificate to be obtained

Electricity bill

Electricity bill should be in the name of applicant or his/her parents

Latest bill to be collected and address should match with application form

Payment of minimum Rs 450/- per month with no outstanding in current bill, subsidy to consider while calculating this amount

Repayment Track record

Any track in the name of applicant of other financier except local financier for minimum 12 months

There should not be any arrear at the time of funding

Track should not be for more than 12 months old

Credit Card subscription

Only HSBC,Citi Bank, American Express, HDFC , SBI ,Axis, Kotak Mahindra Bank/Standard Chartered or Any Nationalized Bank card accepted

Statement of latest 3 months with no delay charges & penal charges

Regular payment trend in the statement every month

Photo copy of front side of card with minimum Rs 20000/- limit

Credit card should be minimum six months old

17

Annexure-6- Income Assessment Form- Compulsory

STRICTLY CONFIDENTIALRISK MANAGEMENT

18

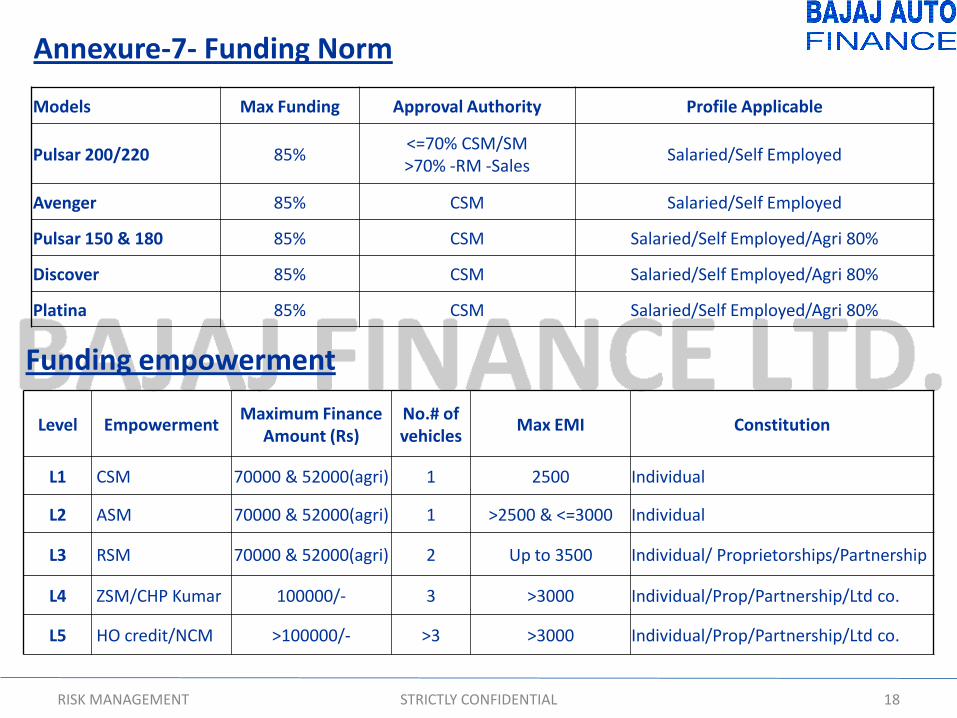

Annexure-7- Funding Norm

STRICTLY CONFIDENTIALRISK MANAGEMENT

Models Max Funding Approval Authority Profile Applicable

Pulsar 200/220 85%<=70% CSM/SM >70% -RM -Sales

Salaried/Self Employed

Avenger 85% CSM Salaried/Self Employed

Pulsar 150 & 180 85% CSM Salaried/Self Employed/Agri 80%

Discover 85% CSM Salaried/Self Employed/Agri 80%

Platina 85% CSM Salaried/Self Employed/Agri 80%

Funding empowerment

Level EmpowermentMaximum Finance

Amount (Rs)No.# of vehicles

Max EMI Constitution

L1 CSM 70000 & 52000(agri) 1 2500 Individual

L2 ASM 70000 & 52000(agri) 1 >2500 & <=3000 Individual

L3 RSM 70000 & 52000(agri) 2 Up to 3500 Individual/ Proprietorships/Partnership

L4 ZSM/CHP Kumar 100000/- 3 >3000 Individual/Prop/Partnership/Ltd co.

L5 HO credit/NCM >100000/- >3 >3000 Individual/Prop/Partnership/Ltd co.

19

Annexure-8 RC COPY

The onus of obtaining the RC photocopy and providing it to the operation team forupdation in Finnone lies with the sales team. In case the RC copy is not provided withintime line mentioned below the trigger would be implemented and the Dealer/Locationwould be in breach . All RC copy need to be stored as per process defined and attachedas annexure

STRICTLY CONFIDENTIALRISK MANAGEMENT

Days RC collection Trigger Remarks Suggested Action

X+ 60 days 75%75% of RC to be collected within 60 day's from the disbursement date

Communication to be sent to RM with trigger alarm giving 30 days notice to dealers to bring the pendency down

X+ 90 days 100%100% of RC to be collected within 90

day's from the disbursement date

Stop operations for dealers who fail to achieve this level & intimation to be

given from ZSM desk

"X represent the date of disbursement but trigger will only apply considering month end value

20

Annexure-9 Negative Profile

High Risk Profile

STRICTLY CONFIDENTIALRISK MANAGEMENT

1 Unregistered Security Agencies and their employees

2 Collection agency and their employees

3 Arms dealers

4 Politician

5 Two wheeler/Auto brokers only

6 Local Private Financiers

7 Bar and Liquor shop owner except Goa

8 Menial labour , servants, cooks, sweeper

9 RTO Agents

10 Cable TV Operator

11 Multi Level Marketing (MLM) members

*No funding to negative profile and there is no deviation

1 Police

2 Standalone STD/PCO/Xerox booth owners

3 Small time-Travel Agents/Tour operators

4 Registered Owners of Small time Private Security Agencies ( and their employees)

5 Small time Civil & Labour Contractors where there is Resi- Cum Office set up

6 Small Non branded courier agencies and their employees

7 Fresh Insurance Agents of Private Insurance Companies

8 Commission Agents

9 Employees of Distribution Channels(DSA/CPA/FI)

10 Advocates/Lawyers – except High court / supreme court

11 Media Journalists , reporters and editors

12 Home Guards

**Limited funding to HRP with RM sign off , refer deviation matrix for details

21

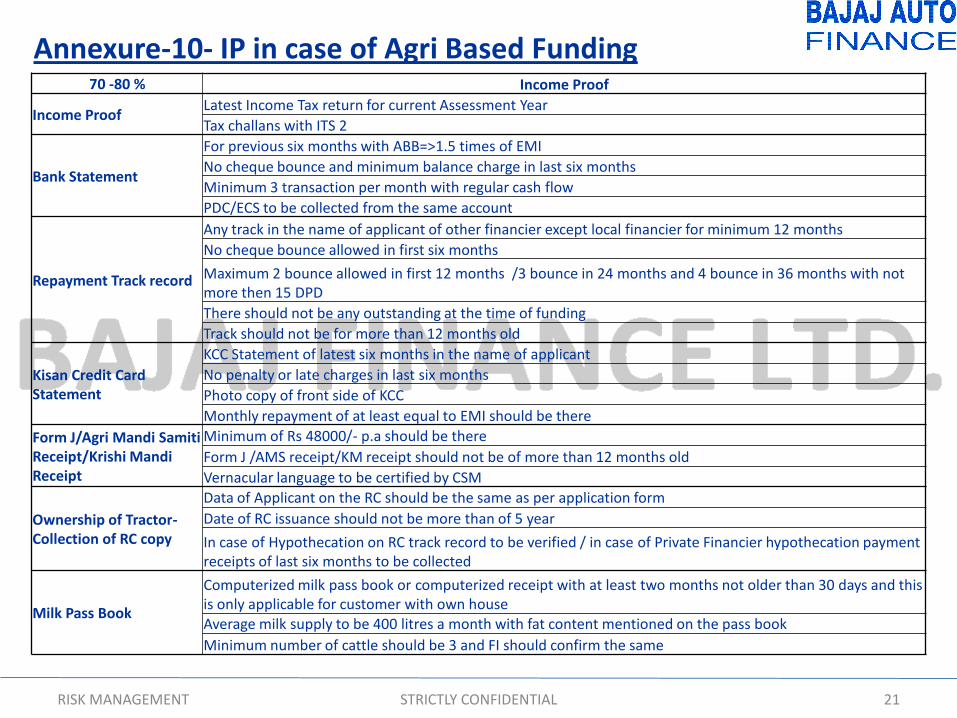

Annexure-10- IP in case of Agri Based Funding

STRICTLY CONFIDENTIALRISK MANAGEMENT

70 -80 % Income Proof

Income ProofLatest Income Tax return for current Assessment Year

Tax challans with ITS 2

Bank Statement

For previous six months with ABB=>1.5 times of EMI

No cheque bounce and minimum balance charge in last six months

Minimum 3 transaction per month with regular cash flow

PDC/ECS to be collected from the same account

Repayment Track record

Any track in the name of applicant of other financier except local financier for minimum 12 months

No cheque bounce allowed in first six months

Maximum 2 bounce allowed in first 12 months /3 bounce in 24 months and 4 bounce in 36 months with not more then 15 DPD

There should not be any outstanding at the time of funding

Track should not be for more than 12 months old

Kisan Credit Card Statement

KCC Statement of latest six months in the name of applicant

No penalty or late charges in last six months

Photo copy of front side of KCC

Monthly repayment of at least equal to EMI should be there

Form J/Agri Mandi Samiti Receipt/Krishi Mandi Receipt

Minimum of Rs 48000/- p.a should be there

Form J /AMS receipt/KM receipt should not be of more than 12 months old

Vernacular language to be certified by CSM

Ownership of Tractor-Collection of RC copy

Data of Applicant on the RC should be the same as per application form

Date of RC issuance should not be more than of 5 year

In case of Hypothecation on RC track record to be verified / in case of Private Financier hypothecation payment receipts of last six months to be collected

Milk Pass Book

Computerized milk pass book or computerized receipt with at least two months not older than 30 days and this is only applicable for customer with own houseAverage milk supply to be 400 litres a month with fat content mentioned on the pass book

Minimum number of cattle should be 3 and FI should confirm the same

22

Annexure 11

STRICTLY CONFIDENTIALRISK MANAGEMENT

Authority Region/Location Applicable

L1 Empowerment Dealership wise All CSM empowered by HO Credit

L2 Empowerment Dealership wise All ASM empowered by HO Credit

L3 Empowerment Region wise All RM sales empowered by HO Credit

L4 Deviation Empowerment

L4 Authority Region States

CHP Kumar Pan India All States

C V Aditya South AP, Karnataka, Kerala ,Tamilnadu

Parag Dixit North Delhi, Haryana,Punjab,HP, Rajasthan

Kamlesh Nankani West Maharashtra, Gujarat, MP, Chattisgarh, UP &UT

L5 (Policy Deviation Empowerment)

L5 Authority Region States

Ankoor S Kulkarni Pan India All States

V Karunakaran Pan India All States

Pratyush Chandramadhur Pan India All States

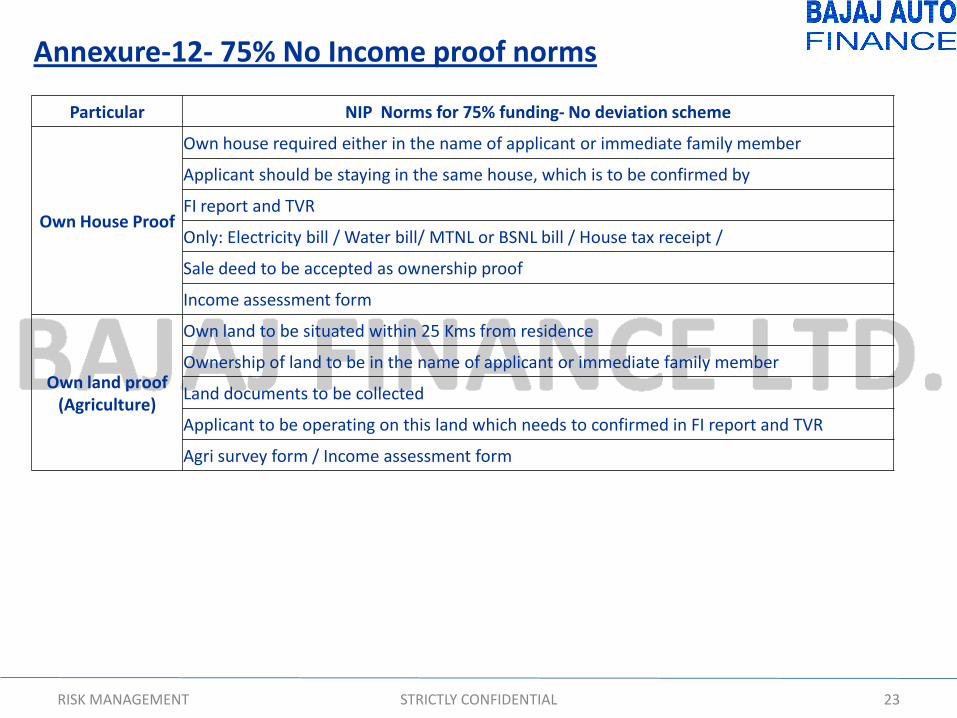

Annexure-12- 75% No Income proof norms

RISK MANAGEMENT STRICTLY CONFIDENTIAL 23

Particular NIP Norms for 75% funding- No deviation scheme

Own House Proof

Own house required either in the name of applicant or immediate family member

Applicant should be staying in the same house, which is to be confirmed by

FI report and TVR

Only: Electricity bill / Water bill/ MTNL or BSNL bill / House tax receipt /

Sale deed to be accepted as ownership proof

Income assessment form

Own land proof (Agriculture)

Own land to be situated within 25 Kms from residence

Ownership of land to be in the name of applicant or immediate family member

Land documents to be collected

Applicant to be operating on this land which needs to confirmed in FI report and TVR

Agri survey form / Income assessment form

24

Deviation Matrix

STRICTLY CONFIDENTIALRISK MANAGEMENT

Deviation Details Explanation L2 L3 L4**

Max Age Funding up to 65 years of applicant /co-applicant at the closure of tenure

Age Norm - - Yes

Residence StabilityIn case of current stay less than norm and immediate previous stay as per norm but for some other city

Residence Stability - Yes -

Office/Business StabilityIn case of current office/business less than norm and immediate previous office/business as per norm but for some other city and document proof available

Office Stability - Yes -

Stability

Residence stability met and having own house but business stability <2 year but > 1 year, can be funded with proof of resi ownership

Stability Norm Yes - -

Residence stability met but office stability <1 year >9 months can be funded

Stability Norm Yes - -

Office/Business stability met but residence stability <1 year but >9 months ,can be funded with itemized bill of post paid connection

Stability Norm Yes - -

Repayment from co-applicant

Any PDC/ECS issued by co-applicant needs deviation approval( repayment instrument can be taken either from applicant or co-applicant . Not acceptable from both applicant & co-applicant)

Repayment - Yes -

Any deviation to Income Proof dox

Any of criteria not meeting but have sufficient mitigant to support the case

Income Proof - - Yes

Rented House and Office bothIn case registered rent agreement available either for only Resi or Office

Self Employed Norm - Yes -

HRP fundingFunding allowed with RTR/1 year banking only as per WIP norm

HRP Funding - Yes -

Negative FI reportFor reasons-customer not met/house locked but with third party confirmation on stay and positive TVR

Negative FI Yes - -

*All deviation approval to be taken on mail and attach the copy in file

**For L4 Deviation Authority please refer Annexure 11

Credit Guidelines

25

Application Form :Application form to be filled completely with all information having applicantphotograph which should be signed across by applicant .No overwriting or cutting allowed inApplication form .

Field Investigation :FI to be conducted through external agencies in all the cases . In case ofsalaried profile verification to be conducted at residence and for self employed people FI to beconducted as per Annexure 3

Telephonic Verification: TVR to be conducted by CSM mandatorily in all the cases before approvalTVR should be done on the number which belongs to applicant .

Deviation Approval :All Deviation approval should be taken on mail and a copy of mail to beattached in the file .

Vernacular Language :In case of any pre approval document available in vernacular languageshould be signed and certified by CSM . CSM needs to mention the title of document .In casecustomer signs in vernacular language then signature verification becomes mandatory

Thumb impression :In case of any applicant or co-applicant putting thumb impression onagreement or PDC , a verification to be obtained from banker or the impression should be notarized.

STRICTLY CONFIDENTIALRISK MANAGEMENT

26

Credit Guidelines

Document Verification: In pre approval stage all KYC documents has to be signed by customer andsales representative of BAFL to verify the photocopy of KYC documents produced by the applicantwith the original & should certify the copy as original seen and verified (OSV). Need to mention thename of the verifier , date of certification & signature.

Existing customer :Any customer has already availed loan from BAFL & loan is active & wants toapply for another loan can be considered for repeat funding at ZSM or NCM level only. Total BAFLexposure and EMI liability to calculate and check the capacity of customer along with need ofsecond vehicle.

Loan Amount :Maximum Loan amount –Rs 70,000/-

Tenure: Minimum tenure - 12 months

•Maximum tenure - 36 months

Minimum EMI - Rs 1200/-

Repayment :

•Repayment has to be through PDC/ECS/ADM/DCC as per approval parameter

•All EMI should be rounded off to nearest rupee

STRICTLY CONFIDENTIALRISK MANAGEMENT

27

Credit Guidelines

PAN No. Verification –As a credit check we can verify the PAN card online from the following URL.& same should be marked verified in the photocopy of Pan card enclosed in the file.

URL: https://incometaxindiaefiling.gov.in/portal/knowpan.do (Put the cust. details on the screen & then click on submit query) Or https://onlineservices.tin.nsdl.com/etaxnew/tdsnontds.jsp (Go to ‘Challan No./ITNS 280’ for PAN No. check)

Repayment of loan with multiple bank account- Repayment from multiple bank accounts cannot be accepted . Need to accept the repayment only from one bank account.

Capturing Credit Scheme - It is mandatory to put credit scheme in every case ,Please find below the credit scheme against credit policies .The case would be put on hold in case the same is not available on DM sheet. . Credit schemes will be circulate with every new scheme that would be launched . Mandatory to mention the same in the DM sheet in spl credit approval

STRICTLY CONFIDENTIALRISK MANAGEMENT

Credit Policy Applicable Location Validity Credit Scheme

With Income Proof PAN INDIA 31st Mar’11 Select the ‘IP’ option in DM sheet

Surrogate Income Proof PAN INDIA 31st Mar’11 Select the ‘SIP’ option in DM sheet

No Income Proof PAN INDIA 30th Jun’11 Select the ‘NIP’ option in DM sheet

O

Due Date for PDC / ECS / ADM

For Salaried profile:-

For example: If the case is disbursed between 1st to 15thOct then the due date would be 8-Nov’10

OR If the case is disbursed between 16th to 31st Oct then the due date would be 8-Dec’10.

For Non Salaried profile:-

For example: If the case is disbursed between 1st to 15th Oct then the due date would be 12-Nov’10

OR If the case is disbursed between 16th to 31st Oct then the due date would be 12-Dec’10.

• Non salaried would include profiles like self employed, Agriculture, businessman & other profiles which are not salaried.

• All the existing PDCs cases will continue to be banked with due dates 5th /10th / 15th & thus no change.

• Where ever a Co Applicant is giving Repayment Modes, please consider his profile for the purpose of due date.

RISK MANAGEMENT STRICTLY CONFIDENTIAL 28

Disbursement Date PDC Date

1 to 15 8th of Next month

16 to 31 8th of next to next month

Disbursement Date PDC Date

1 to 15 12th of Next month

16 to 31 12th of next to next month

Credit Guidelines

RISK MANAGEMENT STRICTLY CONFIDENTIAL 29

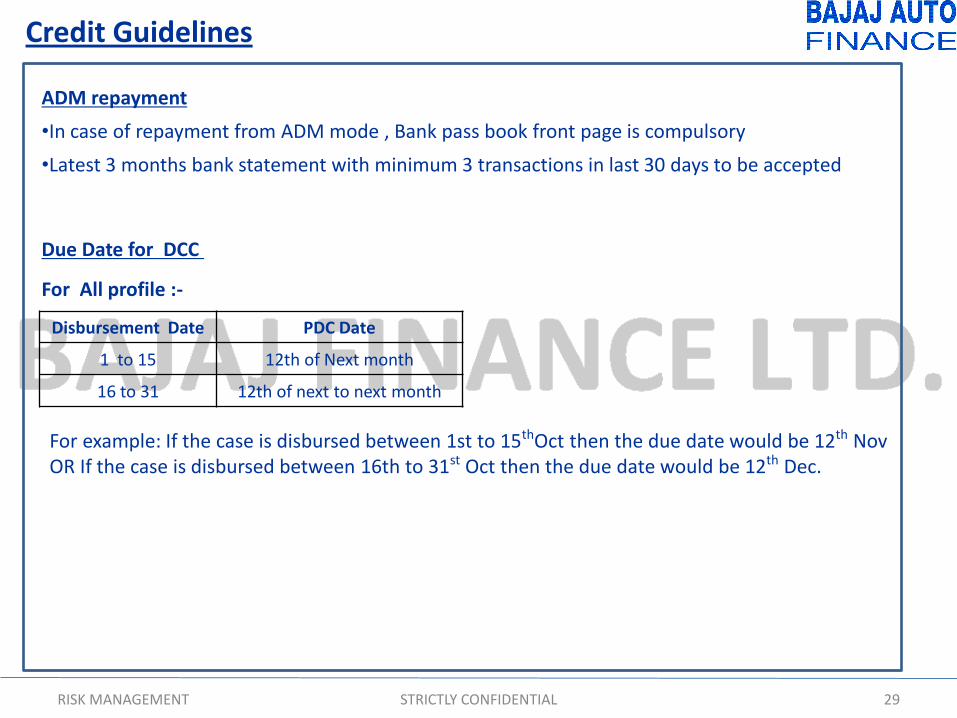

Due Date for DCC

Disbursement Date PDC Date

1 to 15 12th of Next month

16 to 31 12th of next to next month

For example: If the case is disbursed between 1st to 15thOct then the due date would be 12th NovOR If the case is disbursed between 16th to 31st Oct then the due date would be 12th Dec.

For All profile :-

Credit Guidelines

ADM repayment

•In case of repayment from ADM mode , Bank pass book front page is compulsory

•Latest 3 months bank statement with minimum 3 transactions in last 30 days to be accepted

Documentation

KYC Checklist:It is necessary for the CSM/DMA to verify KYC documents as per following :

30STRICTLY CONFIDENTIALRISK MANAGEMENT

LIST OF KYC DOCUMENTS Remarks

ID Proof

Pan CardAny one doc to be provided by customer duly self attested & BAFL sales representative (DMA/CSM /ASM/RSM/permanent employee of bajaj dealership /ASC owner/RSO working with BAFL) to certify the same as original seen and verified (OSV) after verifying from original

Election id

Driving License

Bank pass book with photo and Manager signature & stamp on this(only acceptable in Agri profile)

Govt. and Public Ltd employee ID card

Passport

Address Proof

Electricity bill ( should not be more than 2 months old)

Any one doc to be provided by customer duly self attested & BAFL sales representative (DMA/CSM /ASM/RSM/permanent employee of bajaj dealership /ASC owner/RSO working with BAFL) to certify the same as original seen and verified (OSV) after verifying from original

Passport

Water bill ( Should not be more than 2 months old)

Corporation Tax Receipt

Sale deed /POA

Telephone bill (should not be more than 60 days old and TVR to be conducted on the no.)

Itemized bill of last one month in case of post paid

Govt. and Public Ltd employee ID proof with address

Driving License

Election ID card

Company Lease agreement along with some documentary proof in name of landlord i.e. either light bill, phone bill or water bill or any maintenance receipt from society.

Pre approval Checklist:CSM to verify following documents pre approval :

Documentation

31STRICTLY CONFIDENTIALRISK MANAGEMENT

PRE APPROVAL DOC'S CHECK LIST Remarks

KYC DOCS As per list providedAll docs to be provided by CSM as

Original Seen & Verified

Bank Statement As per credit policy CSM to check BS as per norms

Income Docs Please refer Annexure 4

CIBIL Report CIBIL report to be done by CSM /CPA pre approval

CAM Credit approval Memo as per credit format to be attached in file

Dedupe Check Applicant

To be done for all casesTick the party

Co applicant

Any Other Signatory to the Agreement

Managing Director/Managing Partner of the Company/Partnership

Shareholders having 25%or more Shareholding in the Company-Ltd Company

Partners having 25% or more capital in the partnership firm

Contact Point Verification

Applicant FI

Complete before approvalCo applicant FI

TVR of Applicant/Co-applicant as applicable

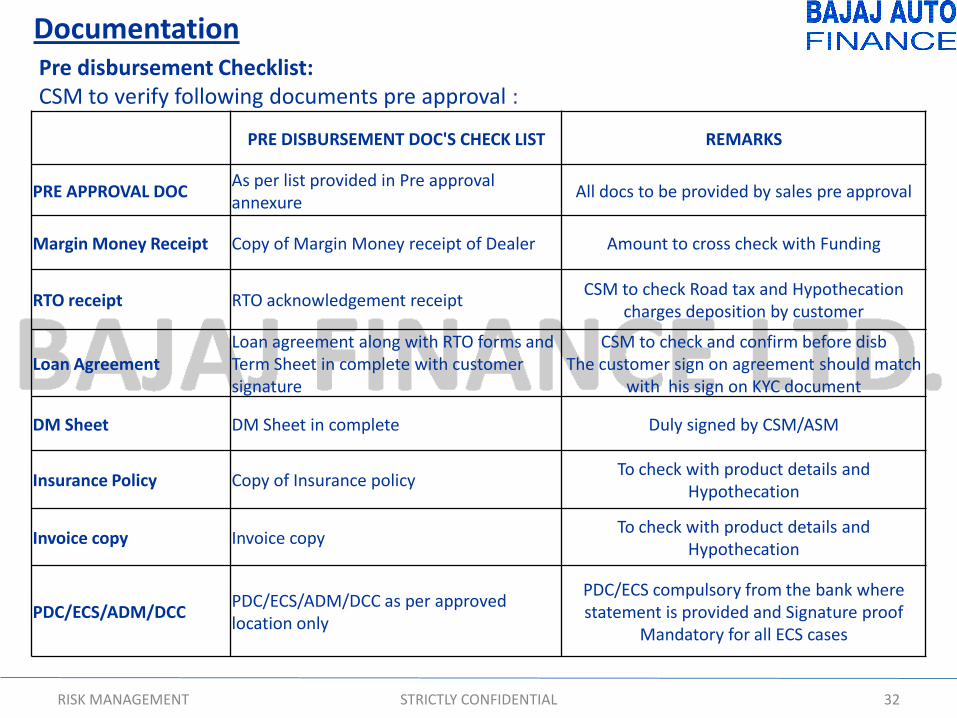

Pre disbursement Checklist:CSM to verify following documents pre approval :

Documentation

32STRICTLY CONFIDENTIALRISK MANAGEMENT

PRE DISBURSEMENT DOC'S CHECK LIST REMARKS

PRE APPROVAL DOCAs per list provided in Pre approval annexure

All docs to be provided by sales pre approval

Margin Money Receipt Copy of Margin Money receipt of Dealer Amount to cross check with Funding

RTO receipt RTO acknowledgement receiptCSM to check Road tax and Hypothecation

charges deposition by customer

Loan AgreementLoan agreement along with RTO forms and Term Sheet in complete with customer signature

CSM to check and confirm before disbThe customer sign on agreement should match

with his sign on KYC document

DM Sheet DM Sheet in complete Duly signed by CSM/ASM

Insurance Policy Copy of Insurance policyTo check with product details and

Hypothecation

Invoice copy Invoice copyTo check with product details and

Hypothecation

PDC/ECS/ADM/DCCPDC/ECS/ADM/DCC as per approved location only

PDC/ECS compulsory from the bank where statement is provided and Signature proof

Mandatory for all ECS cases

33

We thank you for using this manual. This has been designed

with the objective of giving one an insight into Credit as a

function in BAFL. Your suggestions for any improvements

are always welcome.

The Credit team will constantly endeavor at developing a

better and stronger know-how of functional expertise.

Thank You !!

STRICTLY CONFIDENTIALRISK MANAGEMENT

Appendix

RISK MANAGEMENT STRICTLY CONFIDENTIAL 34

35

Appendix -AList of CIBIL Locations

STRICTLY CONFIDENTIALRISK MANAGEMENT

S. No State Locations

1 AP CHITTOOR

2 AP CUDDAPAH

3 AP ELURU

4 AP GUNTUR

5 AP HYDERABAD

6 AP KAKINADA

7 AP KARIMNAGAR

8 AP KURNOOL

9 AP MAHABUBNAGAR

10 AP NELLORE

11 AP ONGOLE

12 AP RAJAHMUNDRY

13 AP SAHIBABAD

14 AP SRIKAKULAM

15 AP TENALI

16 AP TIRUPATI

17 AP VIJAYWADA

18 AP VIZAG

19 AP WARANGAL

20 DL NEW DELHI

21 GJ AHMEDABAD

22 GJ AMRELI

23 GJ ANAND

24 GJ BARDOLI

25 GJ BARODA

26 GJ BHARUCH

27 GJ BHAVNAGAR

28 GJ DABHOI

29 GJ GANDHIDHAM

30 GJ GANDHINAGAR

S.

NoState Locations

31 GJ GODHRA

32 GJ HIMATNAGAR

33 GJ JUNAGARH

34 GJ MEHSANA

35 GJ MORBI

36 GJ NADIAD

37 GJ NAVSARI

38 GJ PALANPUR

39 GJ PATAN

40 GJ PORBANDAR

41 GJ RAJKOT

42 GJ SURAT

43 GJ SURENDRANAGAR

44 GJ VAPI

45 GJ VERAVAL

46 HR AMBALA

47 HR BHIWANI

48 HR FARIDABAD

49 HR GURGAON

50 HR HISSAR

51 HR JAGADHARI

52 HR JIND

53 HR KAITHAL

54 HR KARNAL

55 HR KURUKSHETRA

56 HR NARNAUL

57 HR PALWAL

58 HR PANCHAKULA

59 HR PANIPAT

60 HR REWARI

S. No State Locations

61 HR ROHTAK

62 HR SIRSA

63 HR SONEPAT

64 JH BOKARO

65 JH DEOGHAR

66 JH DHANBAD

67 JH JAMSHEDPUR

68 JH RANCHI

69 KAR BAGALKOT

70 KAR BANGALORE

71 KAR HUBLI

72 KAR MANGALORE

73 KAR MARGAO

74 KAR MYSORE

75 KAR SHIMOGA

76 KAR UDUPI

77 KL CALICUT

78 KL COCHIN

79 KL KANNUR

80 KL KASARGOD

81 KL KOLLAM

82 KL KOTTAYAM

83 KL PERINTHALMANNA

84 KL THIRVANANTHAPURAM

85 KL TRICHUR

86 MH AHMEDNAGAR

87 MH AURANGABAD

88 MH BUTIBORI

89 MH CHIPLUN

90 MH JALGAON

S. No State Locations

91 MH KARAD

92 MH KOLHAPUR

93 MH KOPERGAON

94 MH LATUR

95 MH MALEGAON

96 MH MUMBAI

97 MH NAGPUR

98 MH NASIK

99 MH PANDHARPUR

100 MH PUNE

101 MH SANGLI

102 MH SOLAPUR

103 MH THANE

104 MH ULHASNAGAR

105 MP & CG BHILAI

106 MP & CG BHOPAL

107 MP & CG BILASPUR

108 MP & CG BURHANPUR

109 MP & CG DHAMTARI

110 MP & CG GUNA

111 MP & CG GWALIOR

112 MP & CG INDORE

113 MP & CG JABALPUR

114 MP & CG KHARGONE

115 MP & CG KORBA

116 MP & CG MAHASAMUND

117 MP & CG NARSINGHPUR

118 MP & CG RAIGARH

119 MP & CG RAIPUR

120 MP & CG RAJNANDGAON

RISK MANAGEMENT STRICTLY CONFIDENTIAL 36

S. No State Location

121 MP & CG REWA

122 MP & CG SATNA

123 MP & CG SEONI

124 MP & CG UJJAIN

125 OR BHUBANESHWAR

126 OR SAMBALPUR

127 PB & CH ABOHAR

128 PB & CH AMRITSAR

129 PB & CH BATALA

130 PB & CH BHATINDA

131 PB & CH CHANDIGARH

132 PB & CH FARIDKOT

133 PB & CH GURDASPUR

134 PB & CH HOSHIARPUR

135 PB & CH JAGRAON

136 PB & CH JALANDHAR

137 PB & CH LUDHIANA

138 PB & CH MANDI

139 PB & CH MOGA

140 PB & CH MOHALI

141 PB & CH NALAGARH

142 PB & CH NANGAL

143 PB & CH NAWASHAHAR

144 PB & CH PATHANKOT

145 PB & CH PATIALA

S.

NoState Location

146 PB & CH PHAGWARA

147 PB & CH RAJPURA

148 PB & CH ROPAR

149 PB & CH SANGRUR

150 PB & CH TARN TARAN

151 RJ AJMER

152 RJ ALWAR

153 RJ BANSWARA

154 RJ BHARATPUR

155 RJ BHILWARA

156 RJ BIKANER

157 RJ DAUSA

158 RJ HANUMANGARH

159 RJ JAIPUR

160 RJ JODHPUR

161 RJ KOTA

162 RJ SAWAI MADHOPUR

163 RJ SRIGANGANAGAR

164 RJ SUMERPUR

165 RJ TONK

166 RJ UDAIPUR

167 TN CHENNAI

168 TN COIMBATORE

169 TN CUDDALORE

170 TN ERODE

S.

NoState Location

171 TN KANCHIPURAM

172 TN MADURAI

173 TN PONDICHERRY

174 TN SALEM

175 TN TIRUCHIRAPALLY

176 TN VELLORE

177 UP & UT AGRA

178 UP & UT AKBARPUR

179 UP & UT ALIGARH

180 UP & UT ALLAHABAD

181 UP & UT BAHRAICH

182 UP & UT BARABANKI

183 UP & UT BARAUT

184 UP & UT BAREILLY

185 UP & UT BASTI

186 UP & UT BIJNOR

187 UP & UT BULANDSHAHR

188 UP & UT DEHRADUN

189 UP & UT DEORIA

190 UP & UT FARUKHABAD

191 UP & UT FIROZABAD

192 UP & UT GHAZIABAD

193 UP & UT GONDA

194 UP & UT GORAKHPUR

195 UP & UT HALDWANI

S.

NoState Location

196 UP & UT HARDWAR

197 UP & UT JAUNPUR

198 UP & UT JHANSI

199 UP & UT KANPUR

200 UP & UT KASHIPUR

201 UP & UT LUCKNOW

202 UP & UT MATHURA

203 UP & UT MEERUT

204 UP & UT MIRZAPUR

205 UP & UT MORADABAD

206 UP & UT NOIDA

207 UP & UT PRATAPGARH

208 UP & UT RAMPUR

209 UP & UT ROORKEE

210 UP & UT SAHARANPUR

211 UP & UT SHAHJAHANPUR

212 UP & UT SULTANPUR

213 UP & UT UNNAO

214 UP & UT VARANASI

215 WB DURGAPUR

216 WB GUWAHATI

217 WB HOOGHLY

218 WB HOWRAH

219 WB KOLKATA

220 WB MIDNAPUR

List of CIBIL Locations continues..

Appendix B List of ECS Locations

RISK MANAGEMENT STRICTLY CONFIDENTIAL 37

S. No. Location State S. No. Location State S. No. Location State

1 Hyderabad Andhra Pradesh 29 Gulbarga Karnataka 57 Udaipur Rajasthan

2 Tirupati Andhra Pradesh 30 Davangere Karnataka 58 Jodhpur Rajasthan

3 Nellore Andhra Pradesh 31 Hassan Karnataka 59 Bikaner Rajasthan

4 Vizag Andhra Pradesh 32 Panjim Karnataka 60 Kota Rajasthan

5 Kakinada Andhra Pradesh 33 Calicut Kerala 61 Chennai Tamil Nadu

6 Guntur Andhra Pradesh 34 Trichur Kerala 62 Pondicherry Tamil Nadu

7 Tenali Andhra Pradesh 35 Cochin Kerala 63 Madurai Tamil Nadu

8 Vijaywada Andhra Pradesh 36 Trivandrum Kerala 64 Salem Tamil Nadu

9 Delhi Delhi 37 Mumbai Maharashtra 65 Erode Tamil Nadu

10 Rajkot Gujarat 38 Pune Maharashtra 66 Coimbatore Tamil Nadu

11 Ahmedabad Gujarat 39 Solapur Maharashtra 67 Tirupur Tamil Nadu

12 Baroda Gujarat 40 Kolhapur Maharashtra 68 Tirunelveli Tamil Nadu

13 Surat Gujarat 41 Nasik Maharashtra 83 Trichy Tamil Nadu

14 Jamnagar Gujarat 42 Aurangabad Maharashtra 69 Kanpur Up & Ut

15 Anand Gujarat 43 Nagpur Maharashtra 70 Allahabad Up & Ut

16 Bhavnagar Gujarat 44 Indore Mp & Cg 71 Varanasi Up & Ut

17 Jamshedpur Jharkhand 45 Bhopal Mp & Cg 72 Lucknow Up & Ut

18 Ranchi Jharkhand 46 Gwalior Mp & Cg 73 Dehradun Up & Ut

19 Dhanbad Jharkhand 47 Jabalpur Mp & Cg 74 Gorakhpur Up & Ut

20 Bangalore Karnataka 48 Raipur Mp & Cg 75 Agra Up & Ut

21 Mysore Karnataka 49 Bhubaneshwar Orissa 76 Kolkata West Bengal

22 Mangalore Karnataka 50 Cuttack Orissa 77 Burdwan West Bengal

23 Hubli Karnataka 51 Ludhiana Punjab & Ch 78 Durgapur West Bengal

24 Udupi Karnataka 52 Amritsar Punjab & Ch 79 Siliguri West Bengal

25 Belgaum Karnataka 53 Jalandhar Punjab & Ch 80 Guwahati West Bengal

26 Shimoga Karnataka 54 Chandigarh Punjab & Ch 81 Asansol West Bengal

27 Bijapur Karnataka 55 Jaipur Rajasthan

28 Raichur Karnataka 56 Bhilwara Rajasthan

• Ex-showroom + RTO charges + Insurance = ORP

• 62113 + 5018 + 1498 = 68629 On Road Price

(ORP)

• Initial payment made by customer

• 10295Margin Money

• ORP – Margin Money

• 68629 - 10295 = 58334Loan Amount

• Rate of Interest * Loan Amount *Tenure ( in yrs) = Interest p.a

• 10.30% * 58334 * 1.5 =9013Interest

RISK MANAGEMENT STRICTLY CONFIDENTIAL 38

Customer applies loan Pulsar 150 & the scheme is( scheme Code 9801) with

ROI of 10% p.a. flat with 1 advance EMI for 18 months. The scheme carries

3.5% upfront interest, Rs 100 as service charges.

Appendix C

Continues…

• ( Loan Amount + Total interest ) / tenure (In Mths)

• =(58334 + 9013) / 18 = 3742EMI

• Loan Amount – (No. of Adv EMI * EMI)

• 58334 - (1*3742) = 54592Net Exposure

• (On Road Price – Margin Money – Adv EMI ) *100 / On Road Price

• =68629 - 10295 – 3742 = 80%LTV

• Margin Money +Adv Emi + Processing fees + Upfront Interest +Any other charges

• =10295 + 3742 + 100 + (3.5*58334) = 16179Down Payment

• ORP – Down Payment

• 68629 - 16179 = 52450

Disbursement Amount

Continues..

Field Investigation format:

Credit Approval Memo (CAM) :

Agri Survey Form:

Income Assessment Form

Vernacular Form

RISK MANAGEMENT STRICTLY CONFIDENTIAL 40

Appendix DDocument Template