Embed Size (px)

Citation preview

STRATEGY IN THE DIGITAL ECONOMY

Corigliano – Koslowski – Migliacci – Scemama

PLANI. Market Presentation

II. Market Conduct

III.Firm Focus

IV.Antitrust Activity

1. INTRODUCTION & MARKETPRESENTATION

INTRODUCTION : AMERICAN SKIING COMPANY AND S-K-I DOMINATE THE EASTERN NEW

ENGLAND AND MAINE SKI MARKET

● Situation : Together, the two operators represent 43% of all

skier days (ASC: 17% / S-K-I: 26%) in Eastern New England

and 51% in Maine (ASC: 32% / S-K-I: 19%) across the same

mountains chain, in the middle of the region

● Skiing business definition : “All services related to providing

access to downhill skiing and snowboarding, included but not

limited to providing lifts, ski patrol, snowmaking design,

building, grooming of trails, skiing entertainment and

lodging” - complaint

● The same target set of customers: residents of Eastern

New England and Maine

1994-95

ASC

S-K-I

TargetMarket

1994-95

ASC

S-K-I

TargetMarket

MARKET PARTICULARITIES :

CATCHMENT AREAS OF NEW

ENGLAND’S SKI RESORTS ARE

SIGNIFICANTLY CONDITIONED BY

A GEOGRAPHICAL PROXIMITY

FACTOR AND BARRIERS TO ENTRY

ARE HUGE

● Travel time and expense: important constraint

on available alternatives to a skier

● “Geographic markets for skiing are regional.

Skiers are not willing to travel an unlimited

distance to ski”, “Travelling to distant ski resorts

imposes a burden on the skier, either in the form

of excessive driving time or of a large additional

expense for airfare”

● Barriers to entry are huge and quite

insurmountable because of legal environmental

restrictions and high fixed and sunk costs.

What’s more, Ski Resorts is by nature subject to a

strong climate elasticity.

● Nature and quality of services are homogeneous

and ski resorts remain substitutable when

operating in the same regional geographic area

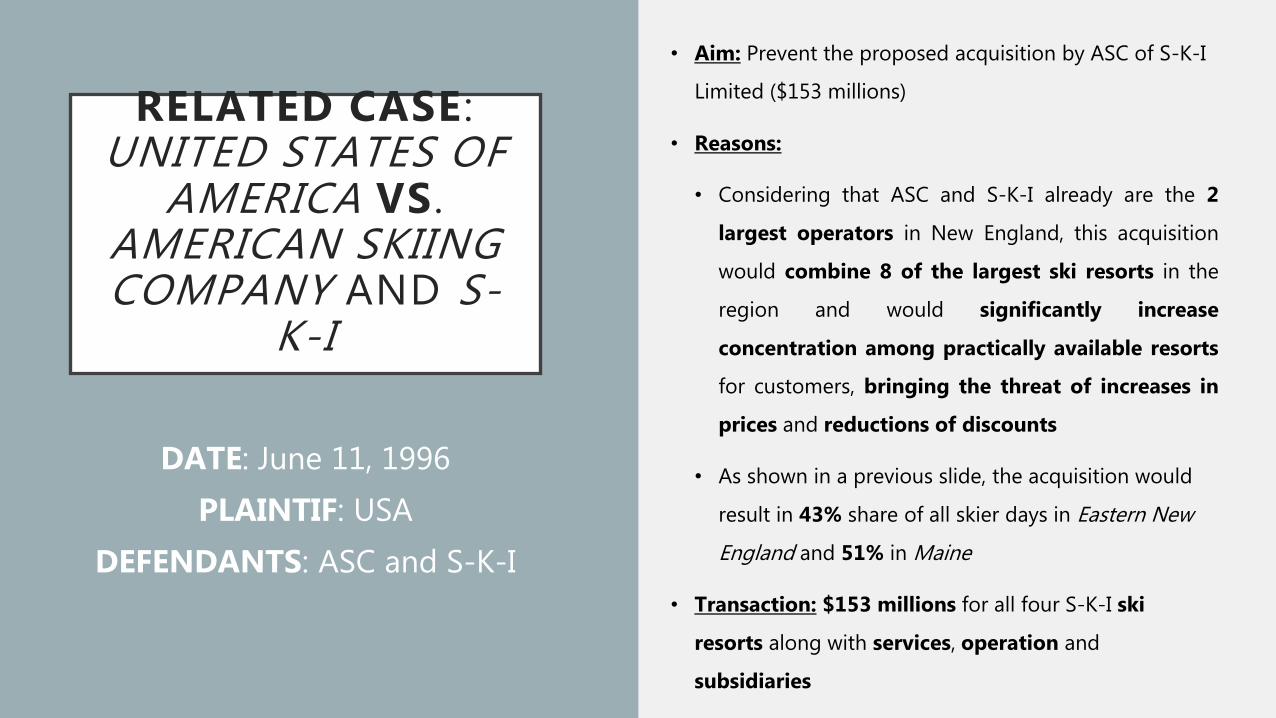

RELATED CASE : UNITED STATES OF

AMERICA VS. AMERICAN SKIING COMPANY AND S-

K-I

• Aim: Prevent the proposed acquisition by ASC of S-K-I

Limited ($153 millions)

• Reasons:

• Considering that ASC and S-K-I already are the 2

largest operators in New England, this acquisition

would combine 8 of the largest ski resorts in the

region and would significantly increase

concentration among practically available resorts

for customers, bringing the threat of increases in

prices and reductions of discounts

• As shown in a previous slide, the acquisition would

result in 43% share of all skier days in Eastern New

England and 51% in Maine

• Transaction: $153 millions for all four S-K-I ski

resorts along with services, operation and

subsidiaries

DATE: June 11, 1996

PLAINTIF: USA

DEFENDANTS: ASC and S-K-I

II. MARKET CONDUCT

NEW ENGLAND SKI MARKET COMPONENTS

• Many ski resorts, few areas managers

A.S.C. S-K-I Ltd.Union

Terminal Piers, Inc.

EndriunasBrothers,

Inc.Intrawest

1994-1996 1984-1996 1977-2007 1987-20071994-

present

Attitash Killington Berkshire eastBlue HillsStrattonmountain

Cranmore Mt. Snow/Haystack CannonsburgRaggedMountain

SugarbushSugarloaf

Sunday river Waterville Valley

Resort Name Base SummitVertical Drop

Longest Run

Snow Making

Attitash, NH 600ft 2350ft 1750ft 3mi 240ac

Cranmore Mountain Resort, NH 600ft 2000ft 1200ft 1mi 192ac

Killington Resort, VT 1165ft 4241ft 3050ft 6mi 500ac

Mount Snow, VT 1900ft 3600ft 1700ft 2mi 480ac

Sugarbush, VT 1483ft 4083ft 2600ft 3mi 356ac

Sugarloaf, ME 1417ft 4237ft 2820ft 3.5mi 618ac

Sunday River, ME 825ft 3150ft 2340ft 3mi 552ac

Waterville Valley, NH 1984ft 4004ft 2020ft 3mi 220ac

PRICES

• Companies’ prices are directly

impacted by the diversity of

alternatives presented to skiers

in these markets. Good

competitors are

• well capitalized,

• well managed

• significant capital

improvement

• real estate development

programs.

• Provision of weekend and day skiing

product market

• Eastern New England and Maine

geographic markets.

• Examples: Skier origin data collected

• Sunday River: approx. 43% of its

weekend skiers reside in

Massachusetts.

• Killington and Mount Snow: approx.

23% and 35%, respectively, of their

weekend skiers reside in New York !

MARKETS

COMPETITION MODEL

Tickets in 95-96 season

BUT…

Skiers do not wish to travel an

unlimited distance to ski.

Burden on the skier

(excessive driving time or large

additional expense for airfare).

However, the longer the ski trip, the

greater a skier's willingness to

travel.

COMPETITION BY COUPONS & DISCOUNTS

• Complete privacy by lack of information• “Ski & Stay”• Price adapted by duration of stay, distance traveled,

hostel choice

PRICE DISCRIMINATION

PRODUCTS & INSTALLATIONS

Lifts: Similar kind of product, few producers Among products a Ski resort can propose to

skier to access to downhill skiing and

snowboarding:

• Providing lifts

• Ski patrol

• Snowmaking,

• Design, building, and grooming of trails

• Skiing lessons

• Ancillary services such as food service

• entertainment, and lodging Innovation are not the leitmotiv for consumer’s choice or competition between ski areas managers

CRANMORE MT. KILLINGTON

PRODUCTS & INSTALLATION (2)

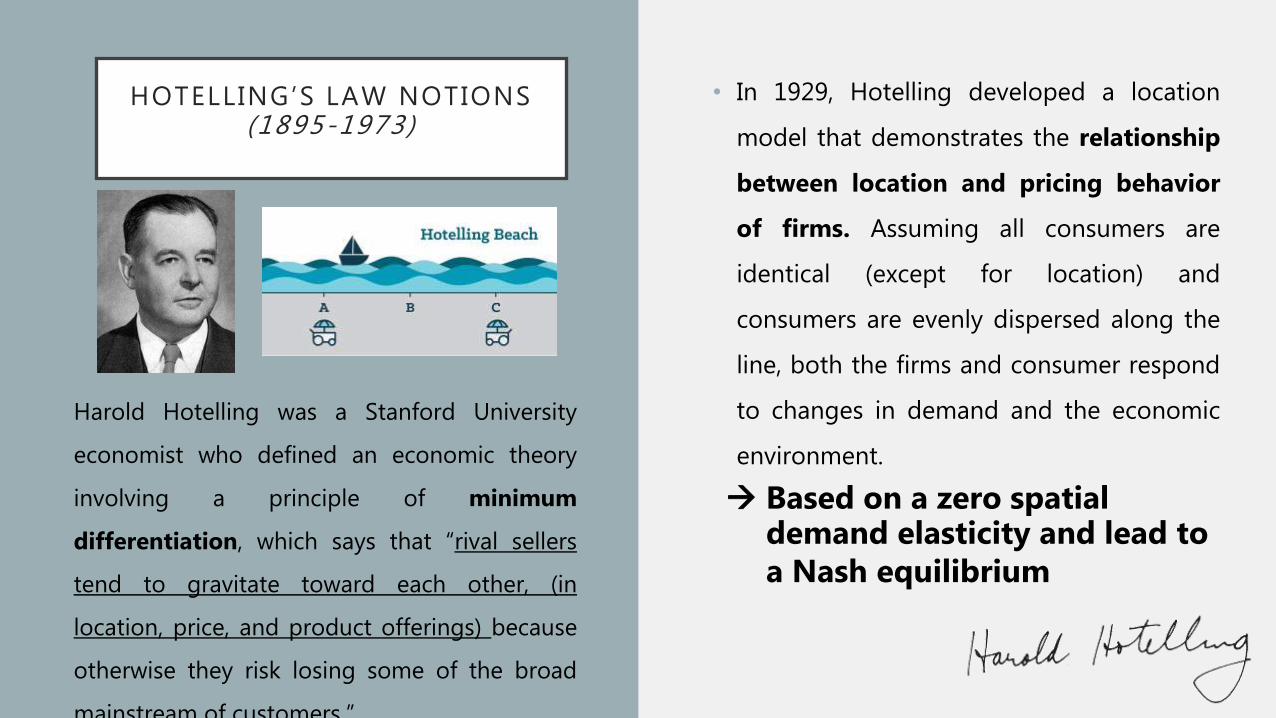

HOTELLING’S LAW NOTIONS(1895-1973)

• In 1929, Hotelling developed a location

model that demonstrates the relationship

between location and pricing behavior

of firms. Assuming all consumers are

identical (except for location) and

consumers are evenly dispersed along the

line, both the firms and consumer respond

to changes in demand and the economic

environment.

Harold Hotelling was a Stanford University

economist who defined an economic theory

involving a principle of minimum

differentiation, which says that “rival sellers

tend to gravitate toward each other, (in

location, price, and product offerings) because

otherwise they risk losing some of the broad

mainstream of customers.”

Based on a zero spatial demand elasticity and lead to a Nash equilibrium

INCUMBENT FIRM REACTION TO ENTRY

• “Finally, the DOJ Complaint alleges that successful

entry or expansion in the skiing business would

be difficult, time consuming, and costly, as well as

extremely unlikely. Entry or expansion therefore

would not be timely, likely, or sufficient to

prevent any harm to competition.”

SKI RESORT MARKET EVOLUTION

1980: A ski resort opened: Beaver Creek (Colorado).

That was the last major ski resort to open in the

United States.

Environmental regulations: huge barrier to building

new ski resorts in North America.

Most investors looking to start a ski resort from scratch are

looking abroad to China, Japan, and South America.

Then, it also takes a long time (decades) to :

• build community support.

• design the ski experience and build the resort

III. FIRM FOCUS AMERICAN SKIING COMPANY

COMPANY PRESENTATION

Description: American Skiing Company (ASC) is a holding company that operates through various subsidiaries in two business segments: ski resorts and real estate.

CEO & Founder:

Leslie B. Otten

STRATEGY: FROM THE FIRST RESORT TO EXPANSION

Sunday River (Maine)

Mutli Resort Company(Multi resort Strategy)

Attitash Bear Peak(New Hampshire)

1980

1994

- Construction- Snowmaking technology=> Biggest resort in the US

- Snowmaking and new chair lifts- Creation: all children's programs, adaptive programs, and snowboarders.=> recognized as a family-oriented resort

1996

Introduction: Edge card program, frequent-skier program and he Magnificent 7 card=> Allowed guests to obtain lift tickets at a reduced rate when they purchased a seven-day package. (Later linked to credit cards)

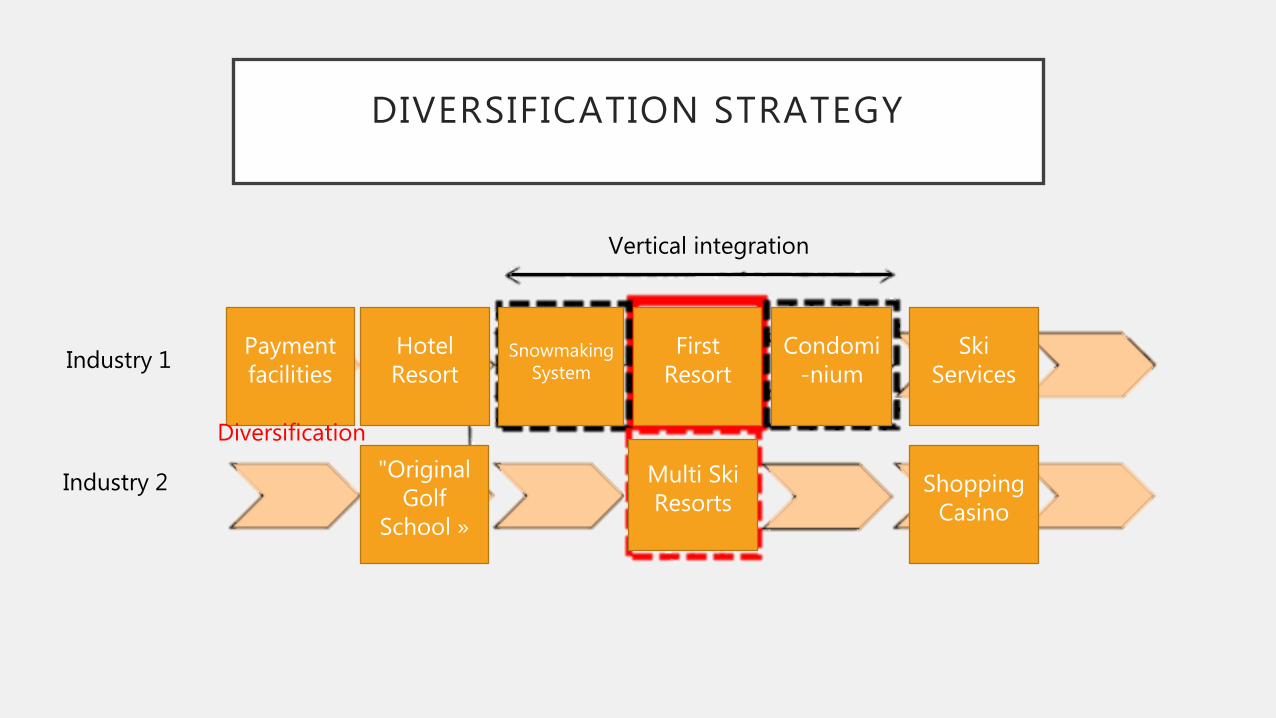

DIVERSIFICATION STRATEGY

Ski Services

"Original Golf

School »

First Resort

HotelResort

Multi Ski Resorts

Shopping Casino

SnowmakingSystem

Condomi-nium

Paymentfacilities

Vertical integration

Industry 1

Industry 2

Diversification

MAJOR COMPETITORS

2 factions

Resort only for Skiing

• Aspen Skiing Company: focus on “purist” customers – Skiers only

Commercial idea of generalized recreation

• Vail (Colorado - biggest competitor to ASC)

• Booth Creek Ski Holdings (New entrant – Can only purchase less fashionable resort)

They are few players. Highly concentrated national market – but each well differentiate by region and specialties

ANTITRUST ACTIVITYIV. ANTITRUST ACTIVITY

ECONOMIC ARGUMENTS

PRESENTED BY THE US GOV

TO INTERFERE IN THE

FIRMS' MERGE

Important information and dates

In February 1996, American Skiing

Company (ASC), formerly known as LBO

Resorts Enterprises Corp. Proposed to

acquire S-K-I Ltd common stock for

approx. 137M$

These merging of the largest

owners/operators of ski resorts caused a

DOJ anti-trust lawsuit in June 1996 right

after S-K-I gave its agreement on the

acquisition operation proposed by ASC

ECONOMIC ARGUMENTS PRESENTED BY THE US GOV TO INTERFERE IN THE FIRMS’ MERGE (2)

Anticompetitive effects (violation of the section 7 of the Clayton act)

- a competition substantially lessened among firms in eastern New England (Vermont, New Hampshire and Maine states) in

providing skiing which could lead to an increase in price and less discounting incentives for customers who go for skiing week-

end trips

- particularly in Maine, where less competition could lead to raise prices and decrease discounts for customers who go for day

skiing trips

Effects fueled by :

- The ski resorts industry is constituted by geographical markets where it is difficult for customers to switch from one to the other

- The DOJ considers that any successful entry in the skiing business would be difficult, costly and time consuming. We will see

that ASC and SKI Ltd competitors are far behind in terms of market shares

=> High risk of « unilateral anticompetitive effects » (US Federal Trade Commission)

ECONOMIC ARGUMENTS OF THE FIRMS

Moreover, the firms argument was prettysimple : dividends !

SHAREHOLDER PRESSURE

S-K-I Ltd. decided the best action for its

shareholders would be to sell its assets.

Meanwhile, LBO Resort Enterprises Corp

(in other words, ASC) was growing and

expanding in the New England market.

Therefore, ASC proposed to acquire SKI

Ldt with a 58.7M$ debt assumption

OUTCOME OF THE INVESTIGATION BY THE DOJ

Final judgment

- The US government allows the firms to merge if they both proceed to divestitures in order to preserve healthy

competition in prices for the customers, under certain conditions

Settlement proposed by the DOJ

- ASC and S-K-I Ltd must sell all their rights, titles, and interests in the Waterville Valley (SKI Ltd) and Mt Cranmore

(ASC) ski resorts in eastern New England, to one or more purchasers, within 180 calendar days after filling the Final

judgment

- These assets and interests have to be sold to one or more purchasers who demonstrate that they will be an effective

competitor to the merged firm

- SKI and ASC must ensure that until the divestitures are completed, Waterville Valley and Mt Cranmore will be held

separate from SKI and ASC other assets and businesses in order to make them as much saleable and economically

viable possible for any prospective buyer

- If the divestitures are not completed before the deadline (180 days) the DOJ will appoint a trustee to complete the

divestitures

WHY IMPOSING DIVESTITURES?

East. New England week-

end tripsHHI Index Change in HHI 2 firms combined market share

Next larger

competitor

market share

If no divestitures 2100 900 ASC 17% + SKI 26% = 43% 7%

If divestitures completed <1800 <40%

Maine day skiing trips

If no divestitures >2900 1200 ASC 32% + 19% = 51% 12%

If divestitures completed 1900 <35%

Market concentration impact

DOJ HHI ’s interpretation rules

The U.S. Department of Justice considers a market with an HHI of less than 1,500 to be a

competitive marketplace, an HHI of 1,500 to 2,500 to be a moderately concentrated

marketplace, and an HHI of 2,500 or greater to be a highly concentrated marketplace.

As a general rule, mergers that increase the HHI by more than 200 points in highly

concentrated markets raise antitrust concerns.

With the divestitures, DOJ will keep the market moderately concentrated andlimit the risk of unilateral anticompetitive effect in the best interest of thecustomers

IMPACT OF THE DOJ INTERVENTION IN THE MARKET

State Vermont

before-acq 1995-1996 S-K-I Ltd Haystack 35$

state prices 1995-1996 38,8$ mean min price 35$ Haystack max price 48$ Stowe

post-acq 1996-1997 ASC Haystack 37$ (+5,7%)

state prices 1996-1997 40,75$ mean (+5%) min price 32$ Mad River max price 49$ Stratton

State Maine

before-acq 1994-1995 S-K-I Ltd Sugarloaf 43$

post-acq 1996-1997 ASC Sugarloaf 46$ (+7%)

state prices 1996-1997 33,5$ mean min price 24$ Camden max price 46$ Sugarloaf

State New Hampshire

before-acq 1994-1995 ASC (LBO) Cranmore 35$

state prices 1994-1995 32,79$ mean min price 22,95$ King Ridge max price 38$ Cannon

post-acq 1997-1998 Sold to Booth Creek Cranmore 39$ (+11%)

state prices 1997-1998 37,15$ mean (+13%) min price 25$ Whaleback max price 46$ Bear Peak

1) Impact on prices

IMPACT OF THE DOJ INTERVENTION IN THE MARKET

Vermont

The ASC resort price price evolution followed the overall state increase tendency but stayed below

the state’s increase mean. The resort’s price became more closer the cheapest ski resort.

Maine

The ASC resort stayed the most expensive in the state (far from its competitors if we look at the

mean price in the whole state), even if its price increased at a reasonable rate.

New Hampshire

The resort’s price is closer to the state mean prices compared to before the divestiture knowing

that the overall price range substantially increased (from approx 23-38$, to 25$-46$ after). So we

could say the divestiture had a positive impact on prices here.

1) Impact on prices (lift prices for the skiier)

IMPACT OF THE DOJ INTERVENTION IN THE MARKET

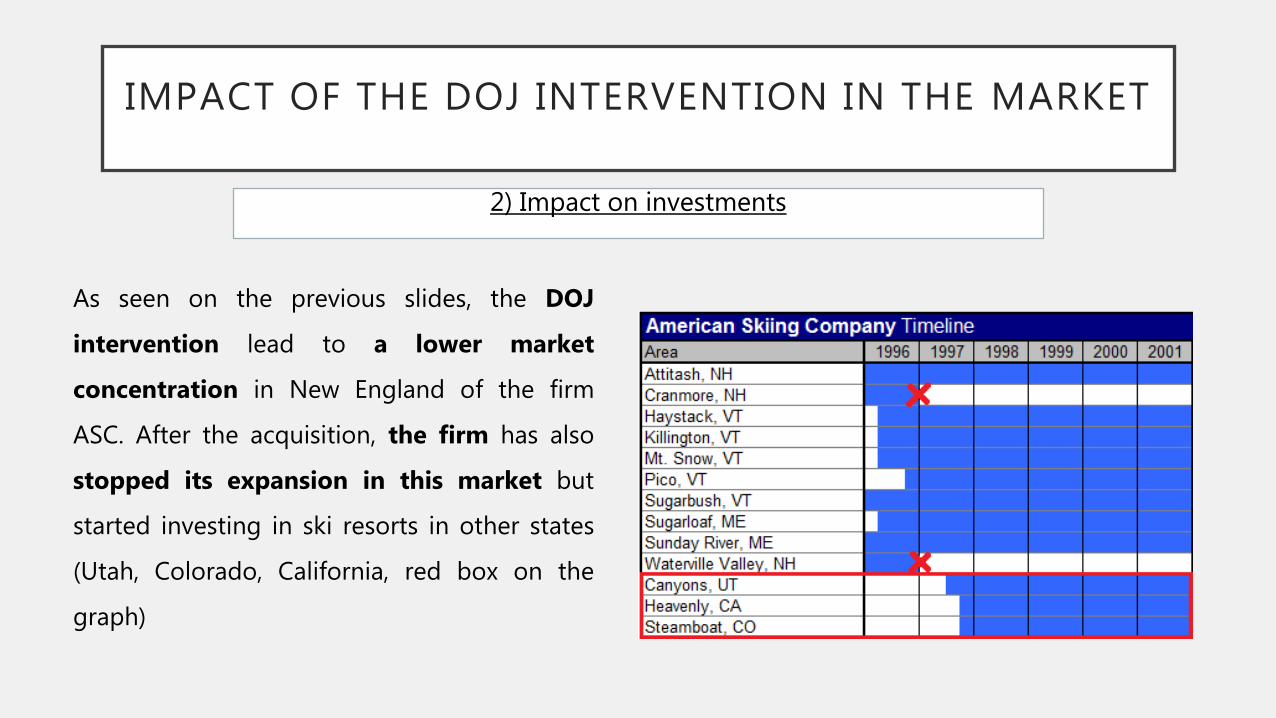

2) Impact on investments

As seen on the previous slides, the DOJ

intervention lead to a lower market

concentration in New England of the firm

ASC. After the acquisition, the firm has also

stopped its expansion in this market but

started investing in ski resorts in other states

(Utah, Colorado, California, red box on the

graph)

IMPACT OF THE DOJ INTERVENTION IN THE MARKET

3) Impact on the market structure – NEW ENTRY !

ASC and S-K-I Ltd respected the DOJ judgement for

the merger to happen. Cranmore and Waterville

Valley were sold to Booth Creek Ski Holdings Inc.

for 17,2$ million on the 27th, November 1996. Booth

Creek was founded on October 8th, 1996 (in other

words, while the divestitures were taking place).

Cranmore and Waterville Valley were the very first

investments of the young firm, which invested in ski

resorts in several states in the same year (1996) and

kept investing in New England with another ski

resort acquisition at the end of 1997 (Loon ski resort).

THANK YOU FOR YOUR ATTENTION

• References

Our Antitrust Case :

https://www.justice.gov/atr/case/us-v-american-skiing-company-and-s-k-i-ltd

Timeline New England ski history 95-96 http://www.newenglandskihistory.com/timeline/timemachine.php?season=1995-96

Maps by countryhttp://www.newenglandtravelplanner.com/outdoors/ski/ne_ski_map.htmlhttp://www.newenglandtravelplanner.com/outdoors/ski/vt/vt_ski_map.htmlhttp://www.newenglandtravelplanner.com/outdoors/ski/nh/nh_ski_map.htmlhttp://www.newenglandtravelplanner.com/outdoors/ski/me/maine_ski_map.html

Gmaps of NE ski resorts https://www.google.com/maps/d/viewer?mid=1zDQpMKkIYdjIpS-KVgXghcEqXYU&ll=43.78053325863693%2C-71.17918186548007&z=7

NE’s ski resorts list with descriptivehttp://www.newenglandtravelplanner.com/outdoors/ski/me/index.htmlhttp://www.newenglandtravelplanner.com/outdoors/ski/nh/index.htmlhttp://www.newenglandtravelplanner.com/outdoors/ski/vt/index.html

History American SkiingCo. http://www.fundinguniverse.com/company-histories/american-skiing-company-history/

ASC Nasdaq homepage http://www.nasdaq.com/markets/ipos/company/american-skiing-co-me-9367-9229

History S-K-I Ltd http://www.newenglandskihistory.com/skiareamanagement/skiltd.php

Bloomberg - American Skiing Co. http://www.bloomberg.com/research/stocks/private/snapshot.asp?privcapId=105872

PR Newswire article on ASChttp://www.prnewswire.com/news-releases/american-skiing-company-announces-comprehensive-plan-to-improve-capital-structure-and-enhance-future-operating-performance-71976377.html

Price evolution through years http://www.newenglandskihistory.com/timeline/vt-ticketprices.php

Ski couponshttps://books.google.fr/books?id=kJcXO3bC82AC&pg=RA1-PA235&lpg=RA1-PA235&dq=ski+coupons+95-96&source=bl&ots=dCIxcPQNdn&sig=siP1V9Ki4lIstq-o7vJNH59r7Xk&hl=fr&sa=X&ved=0ahUKEwi1p5nTmffSAhUOOsAKHZ2eBywQ6AEIJjAC#v=onepage&q=coupon&f=false

NE’s Ski resorts table compare http://www.onthesnow.com/new-england/statistics.html

Explanation HHI index Explanation HHI - anticompetitive

unilateral effects

http://www.investopedia.com/terms/h/hhi.asphttps://www.ftc.gov/tips-advice/competition-guidance/guide-antitrust-laws/mergers/competitive-effects

Economics of big ski resorts https://www.theatlantic.com/business/archive/2012/02/no-business-like-snow-business-the-economics-of-big-ski-resorts/252180/

Hotelling law https://fr.wikipedia.org/wiki/Loi_de_Hotellinghttp://www2.ef.jcu.cz/~klufova/spatial_economy/Palgrave_spatial_economics.pdf

Location model https://en.wikipedia.org/wiki/Location_model#Hotelling.27s_Location_Model

Spatial economicshttps://www.slideshare.net/DISPAR/chapter-3-classical-location-theory-of-the-firm http://www.encyclopedia.com/social-sciences/applied-and-social-sciences-magazines/spatial-economics

Nasdaq IPO full report http://www.nasdaq.com/markets/ipos/filing.ashx?filingid=520682