Embed Size (px)

Citation preview

ASPECTS OF FINANCIAL RISK : CORPORATE GOVERNANCE,

LEADERSHIP & CONTROL

MSC ACCOUNTANCY & FINANCE :CORPORATE GOVERNANCE

& OPERATIONS RISK ANALYSIS AND CONTROL

Stephen Ong BSc(Hons) Econs (LSE),

MBA International Business(Bradford)

Visiting Fellow, Birmingham City UniversityVisiting Professor, Shenzhen University

• Discussion : Forex exposure1

• Corporate Control, M&A, IPO & CEOs

2

• Case Presentation: IBM3

Today’s Overview

1. Open Discussion

• Bartram, S (2008) What lies beneath: foreign exchange rate exposure, hedging and cash flows. Journal of Banking and Finance, 32 (8). pp. 1508-1521

2. CORPORATE CONTROL & POWER OF CEOS

Corporate Governance in Emerging Markets

• What are the challenges that emerging markets face in terms of stepping up their economic development and enhancing the governance of their corporations.

• Such challenges include the institutional design, in particular the role accorded to the stock market, the privatisation of state-owned enterprises (SOEs) as well as social and political barriers to economic development such as crony capitalism.

Learning Outcomes• By the end of this lecture, you should be able to:

1. Critically review whether large equity markets combined with strong investor rights are a necessary and sufficient condition for economic development

2. Comprehend the challenges that emerging markets face in their attempt to improve corporate governance

3. Evaluate corporate governance issues that may arise in privatised or part-privatised SOEs

4. Assess the potential benefits and costs of political connections.

Introduction

• We have seen that there may be a link between a country’s institutional setting, including its legal and financial systems, and the access of its corporations to external capital via well developed stock markets.

• In turn, it is argued that a well developed stock market is a necessary and sufficient driver of economic growth.

• This view is held by a substantial body of the academic literature as well as the World Bank and IMF.

Introduction (Continued)

• However, there are some dissenting voices that argue that some emerging and developed economies have done well despite weak legal institutions and that there substitutes to strong investor protection.

• This lecture will start with a discussion of these two opposing views.

• It will also look at two manifestations of crony capitalism that tend to prevail in developing countries.

• Finally, this lecture will also make some recommendations about how to design corporate governance in formerly state-owned enterprises.

Introduction (Continued)

Large Equity Markets and Strong Property Rights: The Only Way to Achieve Economic Growth?

• The law and finance literature argues that legal and political institutions shape corporate governance and ultimately drive economic growth.

• According to La Porta et al., capital markets will only develop in countries with strong investor rights.

• The absence of liquid capital markets impedes the growth of firms as outside capital is sparse and investment opportunities cannot be taken up.

• Similarly, Mark Roe and Marco Pagano and Paolo Volpin argue that capital markets will only develop and dispersed ownership will only emerge under strong property rights.

• Franklin Allen argues that at the core of the law and finance literature is a narrow view of what the corporation is all about.

• According to this view, the objective of the corporation is to maximise shareholder value.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

• However, this view is based on the assumptions that markets are perfect and complete.

• These assumptions are unlikely to hold, even for the case of highly developed economies.

• For example, markets are not perfect given the existence of negative externalities.

• A negative externality is a cost imposed on others by one’s economic activity.

Large Equity Markets and Strong Property Rights:

The Only Way to Achieve Economic Growth? (Continued)

• For example, in its pursuit of creating shareholder value a firm may end up badly polluting the environment.

• The benefits from polluting the environment, via the cost savings from failing to install pollution-reducing equipment, accrue to the shareholders.

• However, the pollution affects the local community and may result in a substantial reduction in their quality of life.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

• Allen argues that the assumptions behind the law and finance literature are likely to be violated for the case of developed economies and even more likely for emerging economies.

• Allen proposes a much broader view of corporate governance along the lines of how it is typically defined in countries such as Germany and Japan.

• Here, the objective of the firm is to look after all its stakeholders, and not the shareholders.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

• This view is likely to overcome one of the shortcomings of the shareholder-centric view, i.e. the omission of the issue of equitable income distribution.

• This issue is likely a major concern in developing countries where the distributions of wealth and income are highly skewed.

• Given that the assumptions behind the law and finance literature do not hold, the quality of law is neither a necessary nor sufficient condition for economic growth.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

• Allen cites two examples of countries to illustrate the irrelevance of the quality of law in terms of economic growth1. China has experienced remarkable economic

growth since it started opening its economy in 1979, despite weak law and accounting standards

2. The UK experienced a separation of ownership and control before it had strong investor protection.

• The question then arises as to how economic growth could be sustained in each country in the absence of strong law.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

• Allen proposes the four following alternatives to good laws– competition, – trust and reputation,– family ownership, and– foreign ownership.

• There is fierce competition in China from domestic firms and foreign firms.

Large Equity Markets and Strong Property Rights: The Only Way to Achieve Economic Growth? (Continued)

• China has also managed to overcome the weaknesses of its law by developing linkages between social and economic institutions, market and non-market institutions.

• In the UK, trust and information problems were mitigated by floating companies on local stock exchanges with close proximity to their investors.

• Family ownership has also been important across Asia and many successful Chinese firms have ownership by their founders and executives.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

• Joint ventures between domestic and foreign investors are another way of overcoming institutional weaknesses and ensuring access to outside capital.

• Conglomerates may be an additional way of bridging bad laws as they operate internal capital markets whereby affiliated firms with excess funds finance those affiliated firms in need of funding.

• There is support from India that firms affiliated to highly diversified business groups have better accounting and stock performance.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

• Ajit Singh and colleagues also question the role of stock markets as drivers of economic growth.

• Their view of the stock market is much more damning.

• Singh disputes the view that the spectacular economic growth of the USA is mainly due to its large and well developed stock markets.

• He claims the assertion that stock markets are better at allocating economic resources than e.g. banks and the state is wrong for at least two reasons.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

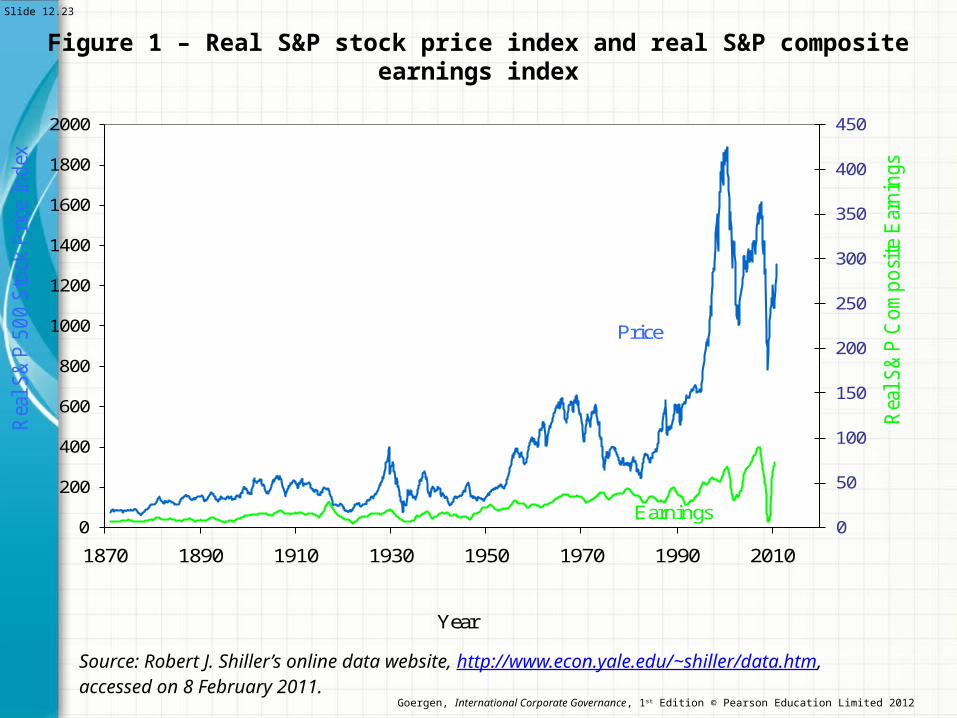

1. Stock markets may suffer from mispricing and investor over-optimism

– The overvaluation of the New Economy stocks and the undervaluation of the Old Economy stocks during the late 1990s is an example of misallocation of resources to firms that were unlikely ever to generate profits

– The work of Robert Shiller supports Singh’s argument– Singh also argues that the widespread use of stock

options in New Economy firms favoured over-reporting of earnings and fuelled the stock market bubble

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

– He also considers the growing use of stock options to have contributed to increasing income inequality in the USA.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

Figure 1 – Real S&P stock price index and real S&P compositeearnings index

0

50

100

150

200

250

300

350

400

450

0

200

400

600

800

1000

1200

1400

1600

1800

2000

1870 1890 1910 1930 1950 1970 1990 2010

Rea

l S

&P

Co

mp

osi

te E

arn

ings

Rea

l S

&P

50

0 S

tock

Pri

ce I

nd

ex

Year

Price

Earnings

Source: Robert J. Shiller’s online data website, http://www.econ.yale.edu/~shiller/data.htm, accessed on 8 February 2011.

Slide 12.23

Goergen, International Corporate Governance, 1st Edition © Pearson Education Limited 2012

2. One of the key mechanisms whereby stock markets reallocate resources is takeovers

– However, Singh claims that this mechanism is not efficient as it does not necessarily favour the survival of the fittest

– Large, but relatively less profitable firms are much more likely to survive than small, profitable firms given that the latter are frequently targeted by the former via mergers and acquisitions.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

• Singh concludes that if stock markets are prone to bubbles in highly developed economies then stock markets in emerging economies are likely to fare even worse.

• The main consequence of policy makers in emerging economies focusing on developing stock markets would then be to increase the volatility of their economy rather than steady economic growth.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

• Singh cites the example of Indonesia– Indonesia experienced a drop of 80% in its stock

market capitalisation during the height of the Asian crisis

– This was followed by an equivalent drop in the value of its currency.

• In contrast, Dennis Mueller argues that the existence of a well developed stock market can only constitute an advantage as it offers firms the option to finance their investments via equity.

Large Equity Markets and Strong Property Rights: The Only Way to

Achieve Economic Growth? (Continued)

Inherited Wealth• Randall Morck, David Stangeland and Bernard

Yeung study the impact of inherited billionaire wealth on economic growth for 42 countries.

• They find that countries, where inherited billionaire wealth is large relative to GDP, have both slower economic growth and technological change.

• In contrast, entrepreneur billionaire wealth is positively correlated with economic growth.

Inherited Wealth (Continued)• They justify the negative effect of inherited

wealth on economic growth by four reasons1. Inherited wealth may keep bad and incompetent

family managers in place2. The highly unequal wealth distribution may create

market power in capital markets, thereby reducing the efficiency of the latter in pricing securities and allocating economic resources

3. Inherited wealth tends to be conservative and opposed to technological change

4. It often has strong ties to politicians further entrenching its position.

The Role of the Government

• Government ownership of large corporations can be substantial in some emerging markets.

• The most extreme example of the importance of government ownership is China.

• In 67% of the firms the government is the largest shareholder.

• Overall, the empirical evidence suggests that the performance of privatised firms improves after the privatisation.

The Role of the Government (Continued)

• However, there are significant differences in the post-privatisation improvements across geographical regions.

• Companies from Africa and the Middle East experience the smallest changes in profitability, efficiency and output.

• Post-privatisation improvements seem to increase with– the degree of trade liberalisation,– stock market liberalisation – and the development and quality of law in

developing countries.• However, the evidence is inconclusive as to

the impact of government ownership after the privatisation.

The Role of the Government (Continued)

• However, the higher the percentage of government ownership post-privatisation the higher is the likelihood that politicians and ex-politicians sit on the firm’s board of directors.

• In contrast, this likelihood decreases with foreign ownership.

• Emerging economies where politically connected firms represent more than 10% of the market capitalisation include Indonesia, Malaysia, the Philippines, Russia and Thailand.

The Role of the Government (Continued)

• Developed economies include Belgium, Ireland, Italy, Taiwan and the UK.

• The question arise whether political connections are good or bad for firm performance.

• There are two views1. The first view is the “grabbing hand” of

government• Politicians on boards pursue their own objectives, in

particular winning votes from their electors• One way to achieve this is to force the firm to

employ more people than is efficient

The Role of the Government (Continued)

• Hence, politicians seeks rents and these are at the expense of the shareholders

• Even if there are benefits from political connections, these will be appropriated by the politicians via bribes and other favours.

2. The second view is the “helping hand” of government• Political connections bring about favours such as

government subsidies and procurement orders.

The Role of the Government (Continued)

• Evidence from Indonesia and Malaysia suggests that political connections are highly valuable.

• In contrast, Mara Faccio finds that political connections are more prevalent in countries believed to be highly corrupt and the market reaction to the appointment of politicians to the board is nil.

• Faccio’s evidence suggests that politicians manage to appropriate all the gains they create.

• However, her results suggest that there is a positive market reaction when a business person becomes a politician.

The Role of the Government (Continued)

• Further evidence by Mara Faccio and David Parsley from geographic ties with politicians suggests that firms that – are family-controlled,– have high growth,– are small,– operate in the industry under the influence

of the politician, and– are from countries with high corruption.

benefit the most from political ties.

The Role of the Government (Continued)

The Design of Corporate Governance in Formerly SOEs

• Ravi Dharwadkar, Gerard George and Pamela Brandes make a series of recommendations on the design of corporate governance in SOEs from emerging markets based on their review of the literature.

• The first set of recommendations consists of three recommendations on the optimal ownership and control of the former SOEs.

The Design of Corporate Governance in Formerly SOEs (Continued)

1. Given that managers and employees with experience of competitive markets are sparse in emerging markets, managerial and employee ownership is not effective.

2. Since investor protection is low, control by a large shareholder rather than dispersed ownership and control will be more effective.

3. Foreign investors are likely to be most effective type of large shareholder.

• The second set of recommendations consists of four recommendations on the types of management, organisational form and managerial contracts as well as capital structure.

1. There needs to be a change of management as – the incumbent management lacks the experience

needed to restructure the firm, and – the government is likely to carry on exercising a

strong influence on the firm if the incumbent management stays in place.

The Design of Corporate Governance inFormerly SOEs (Continued)

2. The optimal organisational structure is a multi-divisional structure as

– they increase the efficiency of the monitoring of the management, and

– also creates internal capital markets substituting for underdeveloped external capital markets.

3. Behaviour-based managerial contracts will be more efficient as outcome-based contracts are more difficult to enforce given the high uncertainty of outcomes due to the weak institutional setup in emerging economies.

The Design of Corporate Governance inFormerly SOEs (Continued)

4. There should be as little debt as possible in the capital structure as

– the disciplinary role of debt is unlikely to work given the weak law enforcement, and

– more debt is likely to increase the agency problem of debt.

The Design of Corporate Governance inFormerly SOEs (Continued)

Conclusions

• Are large stock markets necessary and sufficient condition for economic development?

• Inherited wealth and economic growth.• Political connections.• The design of corporate governance in

former SOEs.

Contractual Corporate Governance• Firms that are highly dependent on equity

financing and are based in economies with underdeveloped capital markets may face financial constraints and a high cost of capital.

• We discuss the ways that enable firms to overcome the absence of highly liquid local capital markets and to tap into more developed foreign capital markets. These ways include foreign cross-listings, reincorporations and cross-border mergers.

• We also discuss whether competition among regulatory systems is good or bad for investors.

Learning Outcomes• By the end of this lecture, you should be able to:

1. Demonstrate how different contractual devices may enable firms from countries with weak corporate governance to improve the level of shareholder protection they offer

2. Assess how firms can reduce their cost of capital by tapping into more developed foreign capital markets

3. Critically review the arguments on both sides of the debate on whether regulatory competition causes a race to the top or a race to the bottom.

Introduction

• The lecture on the taxonomies of corporate governance systems suggests that there is a link between a country’s political and legal setting and the size and development of its capital market.

• In the lecture on corporate governance, types of financial systems and economic growth, we saw that some industries are highly dependent on equity and will only thrive in the presence of a highly developed capital market.

Introduction (Continued)

• Concerning the link between the institutional setting and the size and development of the capital market, a firm’s access to capital may be determined by– the quality of law, in particular investor protection, as

well as the enforcement of law in its home country;– the way social peace is maintained, including the political

orientation of the country’s government; and– the type of electoral system.

• So how can firms in countries with underdeveloped stock markets get better access to capital?

• More generally, how can firms based in countries with weak corporate governance standards exceed those standards credibly?

• Firms can do so by using particular types of contractual devices such as:– cross-border mergers and acquisitions,– (re)incorporations, and– cross-listings.

which enable them to choose their preferred level of investor protection and regulation.

Introduction (Continued)

• Henry Hansmann and Reinier Kraakman argue that firms that do not adopt a shareholder-oriented approach will be punished via a higher cost of capital.

Introduction (Continued)

Cross-Border Mergers and Acquisitions

• Firms may improve their corporate governance and access to capital via cross-border mergers and acquisitions.

• The questions that then arise are as follows – Does the target benefit from the stronger

corporate governance of the bidder or does the bidder benefit from the stronger corporate governance of the target?

– Do bidders with weak corporate governance harm targets with better corporate governance?

Cross-Border Mergers and Acquisitions (Continued)

• Marina Martynova and Luc Renneboog distinguish between three possible effects.– The first two assume that the target adopts the

corporate governance of the bidder • There is a positive spillover effect if a bidder with

better corporate governance improves the corporate governance of the target

• There is a negative spillover effect if a bidder with weaker corporate governance reduces that of the target.

– The third assumes the reverse• The bootstrapping effect consists of a bidder with

weaker corporate governance adopting the stronger corporate governance of the target.

• Bootstrapping is voluntary in the case of a full acquisition, but in the case of a partial acquisition the bidder has to honour the corporate governance regulation that the target is subject to (extraterritoriality principle).

• Stefano Rossi and Paolo Volpin find that, compared to bidders, targets are from countries with weaker shareholder protection.

• They find evidence of a positive spillover effect as bidders with stronger corporate governance have a positive effect on takeover volume and bid premiums.

Cross-Border Mergers and Acquisitions(Continued)

• Laura Starks and Kelsey Wei assume that the target adopts the corporate governance of the bidder.

• They argue that the bid premium should be higher for bidders with lower corporate governance as the target shareholders will be more concerned about the increased risk.

• They find evidence for their hypothesis as US targets of bidders from countries with weaker standards earn higher announcement returns.

Cross-Border Mergers and Acquisitions(Continued)

• Martynova and Renneboog also find that bidders tend to have better corporate governance.

• They find evidence for the positive spillover effect, but no evidence for the negative spillover effect.

• They report that, for bidders with weaker corporate governance, the returns to both the bidder and target are higher.

• This suggests that there is a bootstrapping effect.• The latter is mainly observed for partial acquisitions.

Cross-Border Mergers and Acquisitions(Continued)

• To conclude, the empirical evidence suggests that:– Targets in cross-border acquisitions tend to be

from countries with weak corporate governance– Targets with better shareholder protection

require a higher premium when taken over by bidders with weaker governance

– There is evidence of a positive spillover effect, including evidence suggesting an industry-wide positive spillover effect

Cross-Border Mergers and Acquisitions(Continued)

– There is evidence of a bootstrapping effect whereby bidders with weaker corporate governance adopt the corporate governance of their targets. However in line with the extraterritoritality principle, this effect is mainly found for partial acquisitions

– While targets tend to benefit from being taken over by a bidder with better governance, there is some evidence that bidders lose value when taking over weaker targets.

Cross-Border Mergers and Acquisitions(Continued)

(Re)incorporations• A reincorporation consists of a firm which is already

incorporated in one country moving its legal seat to another country.

• The main motives behind reincorporations are– putting in place takeover defences,– reducing directors’ liability,– the move to a jurisdiction with more flexible corporate

law,– savings on tax or franchise fees,– the reconciliation of the legal and operating domicile of

the firm, and– the facilitation of cross-border mergers and acquisitions.

(Re)incorporations (Continued)• The adoption of takeover defences and

reducing directors’ liability are the most popular motives.

• There are two principles in law applying to incorporations1. The real seat principle2. The incorporation principle.

• According to the real seat principle, the law applying to the firm is that of the location of its headquarters or main activities– Firms are subject to the law of their real seat.

• According to the incorporation principle, the law that applies is that of the country of incorporation.

• Most Continental European countries have adopted the real seat principle whereas Ireland, the UK and USA have adopted the incorporation principle.

• Until recently, only US firms were able to change the state of their incorporation whereas corporate mobility was significantly restricted in Europe.

• However, recent rulings by the European Court of Justice (ECJ) have increased corporate mobility for incorporations, but not for reincorporations.

(Re)incorporations (Continued)

• The question that arises is whether managers choose locations for their (re)incorporations that satisfy shareholder interests rather than their own interests or whether the converse is the case.

• There are two schools of thought on this:1. The first school argues that competition between

jurisdictions leads to better quality corporate lawFirms will choose jurisdictions that provide legal services at the lowest cost and that suit their needs the bestThis is the cost avoidance hypothesis This school argues that there will be a race to the top

(Re)incorporations (Continued)

2. The second school argues that, in order to maximise the revenues from incorporations, jurisdictions will compete to provide laws that cater for managerial rather than shareholder interests

This is the shareholder-exploitation hypothesisThis school predicts that there will be a race to the bottom which will harm economic efficiency.

• Empirical evidence by Stephen Ferris et al. supports the shareholder-exploitation hypothesis

– US managers choose the federal state for the location of their firm based on the discretion they will have in each location.

(Re)incorporations (Continued)

• In turn, the argument about the race to the bottom has been challenged– Jurisdiction shopping is indispensable to guarantee

competition between jurisdictions and is therefore not necessarily against shareholder interests

– Several studies find that firms incorporated in Delaware have higher share prices.

• However, other studies report that the higher share prices cannot be observed after 1996 and that the main reason firms move to Delaware is to set up anti-takeover devices.

(Re)incorporations (Continued)

• The large body of empirical studies documenting a negative market reaction to the adoption of takeover defences supports the shareholder-exploitation hypothesis.

• Hence, it is as yet not clear whether regulatory competition is good or bad.

(Re)incorporations (Continued)

• In recent years, a series of rulings by the ECJ have reaffirmed the principle of freedom of establishment within the EU.

• Some scholars predict lots of incorporations of foreign companies in the UK.

• The recent trends observed by Marco Becht et al. suggest that this prediction is likely to become reality– During 2002-5, the number of new private

limited companies from other EU member states established in the UK was over 55,000.

(Re)incorporations (Continued)

Cross-listings• A cross-listing consists of a firm listing on a

foreign stock exchange at the time of its domestic IPO or thereafter.

• According to the so called bonding hypothesis proposed by John Coffee, firms from weaker corporate governance regimes cross-list on the US market in order to commit not to expropriate their minority shareholders.

• If the bonding hypothesis holds, cross-listed firms trade at a premium.

Cross-listings (Continued)• Virtually all of the finance literature focuses on

firms cross-listing in the USA.• Firms seeking a US cross-listing can do so in two

different ways1. They can cross-list via American Depository Receipts

(ADRs)2. They can cross-list via Global Registered Shares (GRS).

• William Reese and Michael Weisbach find that firms from French civil law countries have more US cross-listings (10.5%) than firms from common law countries (6.7%).

• They also find that cross-listed firms from civil law countries are more likely to issue their equity outside the USA.

• Craig Doidge examines whether the cross-listing has an impact on the voting premium– The ratio of the price of the voting right to the

price of the cash flow right.• He finds that firms with a US cross-listing

have lower voting premiums than those without.

Cross-listings (Continued)

• In another study, Doidge and others examine the valuation effect caused by a US cross-listing.

• They expect a US cross-listing to result in a reduction in the firm’s cost of capital for at least four reasons:– The cross-listing increases the shareholder base and risk

is therefore shared among more shareholders– The cross-listing increases the liquidity of the firm’s

shares– The higher disclosure standards reduce the information

asymmetry between insiders and outsiders– A US cross-listing leads to higher scrutiny and monitoring

by the financial press.

Cross-listings (Continued)

• They argue that the large shareholder faces a trade-off when cross-listing her firm– The reduction in the cost of capital, which increases

the ability to finance growth opportunities, leading to higher future cash flows

– The reduction in her private benefits of control due to improved minority shareholder protection.

• As a result, only firms with significant growth opportunities will cross-list.

• They measure growth opportunities by the Tobin’s q (the ratio of market value to book value).

Cross-listings (Continued)

• As expected, they find that the Tobin’s q of cross-listed firms is higher (by 16.5%) than that of firms from the same country without a cross-listing.

• Wissam Abdallah and Marc Goergen examine the decision about the choice of the host market for a sample of 175 firms cross-listing on 19 different stock exchanges.

Cross-listings (Continued)

• They argue that there are at least three reasons why ownership and control may influence this decision1. The large shareholder faces a trade-off between the

benefits from dispersed ownership (liquidity and risk diversification) and the private benefits from retaining controlThe large shareholder will only be willing to give up control if the benefits from doing so outweigh her private benefits of controlIf this is the case, it makes sense to cross-list on a market with higher shareholder protection bringing about a higher valuation

Cross-listings (Continued)

2. Owners of high-risk firms will prefer to cross-list on a market with higher diversification potential which in turn has been shown to be linked to investor protection

3. While the ownership and control structure itself is likely to have an impact on the decision, the link is not straightforward.

• They find that a firm’s ownership and control structure does indeed have an impact on this decision.

Cross-listings (Continued)

• However, contrary to their expectations, they find that firms with substantial private benefits cross-list on markets with better investor protection.

• This relationship is particularly pronounced for firms where control is concentrated in the hands of a single shareholder.

Cross-listings (Continued)

• Further, firms with significant minority shareholders are more likely to cross-list on a better market whereas those with several large shareholders are more likely to cross-list on a market with similar or worse investor protection.

• To sum up, Abdallah and Goergen find support for the bonding hypothesis.

Cross-listings (Continued)

• To conclude, there is strong empirical support for the bonding hypothesis.

• Firms based in countries with weak investor protection tend to cross-list on better markets to commit themselves not to expropriate their minority shareholders.

• However, the US Sarbanes-Oxley Act of 2002 seems to have changed investors’ and academics’ views on the benefits from cross-listings.

Cross-listings (Continued)

• While the Act may have benefitted some firms, it also seems to have generated significant costs, outweighing in many cases the benefits from a US cross-listing.

Cross-listings (Continued)

Conclusions

• Contractual corporate governance.• Cross-borders mergers.• (Re)incorporations.• Cross-listings.

Corporate Governance in Initial Public Offerings• When a firm goes public, typically there is a

substantial reduction in the entrepreneur’s incentives to maximise shareholder value as he/she no longer owns all of the equity, but still has significant control over the firm. Hence, the initial public offering (IPO) calls for a redesign of the firm’s corporate governance arrangements.

• In addition, IPO firms also frequently suffer from higher asymmetry of information between the insiders and outsiders than more mature firms.

• They also often have financing provided by venture capitalists which comes with its own benefits but may also cause conflicts of interests.

Learning Outcomes• By the end of this lecture, you should be able to:

1. Evaluate the conflicts of interests that may prevail in IPO firms

2. Assess the ways whereby IPO firms can mitigate conflicts of interests between their insiders and outsiders as well as mitigate other problems arising from asymmetric information

3. Explain the benefits from the presence of venture capitalists as well as the conflicts of interests they may cause.

Introduction

• Asymmetric information is about different actors holding different levels of information.

• In corporate governance, asymmetric information typically refers to the management having better information about – the firm, and – their own effort

than outsiders such as shareholders and debtholders.

Introduction (Continued)

• Asymmetric information implies that complete contracts which specify– what the managers have to do in each

contingency of the world, and– the distribution of profits in each contingency

are not possible.• Hence, conflicts of interests cannot be

entirely prevented and corporate governance remains an important issue.

• Corporate governance is an issue for well-established, stock-market trade companies.

• It is even more so for firms going through or having recently gone through their initial public offering (IPO) for at least four reasons1. When it goes public, the firm experiences a

separation of ownership and control2. IPO firms tend to suffer more substantially from

problems of asymmetric information3. The power of the CEO in an IPO is relatively high4. Venture capitalists, with their own benefits and

conflicts of interests, are often involved in IPO firms.

Introduction (Continued)

Asymmetric Information, Pricing Anomalies and the Separation of Ownership and Control in IPOs

• As part of the process of going public, the firm normally appoints an investment bank which will help with the issuing and sale of the equity shares as well as their pricing.

• Broadly speaking, there are two pricing mechanisms– In an offer at a fixed price, the price of the shares,

the so called offer price, is determined by the investment bank

– In a book-building offer, the pricing is more complex and consists of three stages.

Asymmetric Information, Pricing Anomalies and the Separation of Ownership and Control in IPOs (Continued)• The three stages of the book-building are

1. The investment bank asks its major clients for non-binding expressions of interest specifying a price for the shares and a quantity and then determines the price range for the shares

2. During the actual book-building stage, investors are asked to apply for the shares by specifying the quantity and the maximum price (within the price range) they are willing to pay

3. The investment bank goes through the book, determines a strike and all investors that applied at a price equal or higher than the strike price will get shares.

• Three pricing anomalies have been observed for IPOs– the initial underpricing of IPO shares,– their subsequent bad performance over the long term,– and the cycles in the number of IPOs and their initial

returns, i.e. the hot-issue markets.• All three phenomena are pricing anomalies because

they violate the efficient market hypothesis (EMH).• According to the EMH, there should be no

persistent and predictable patterns in securities prices.

Asymmetric Information, Pricing Anomalies and the Separation of Ownership and Control in IPOs (Continued)

• Hot-issue markets are driven by more general cycles in markets.

• However, both IPO underpricing and the bad long-term performance of IPOs have been directly linked to corporate governance.

• Hence, we shall focus on the latter two.• IPO underpricing consists of an IPO being

oversubscribed and its offer price being lower than the closing price on the first day (week) of trading.

Asymmetric Information, Pricing Anomalies and

the Separation of Ownership and Control in IPOs

(Continued)

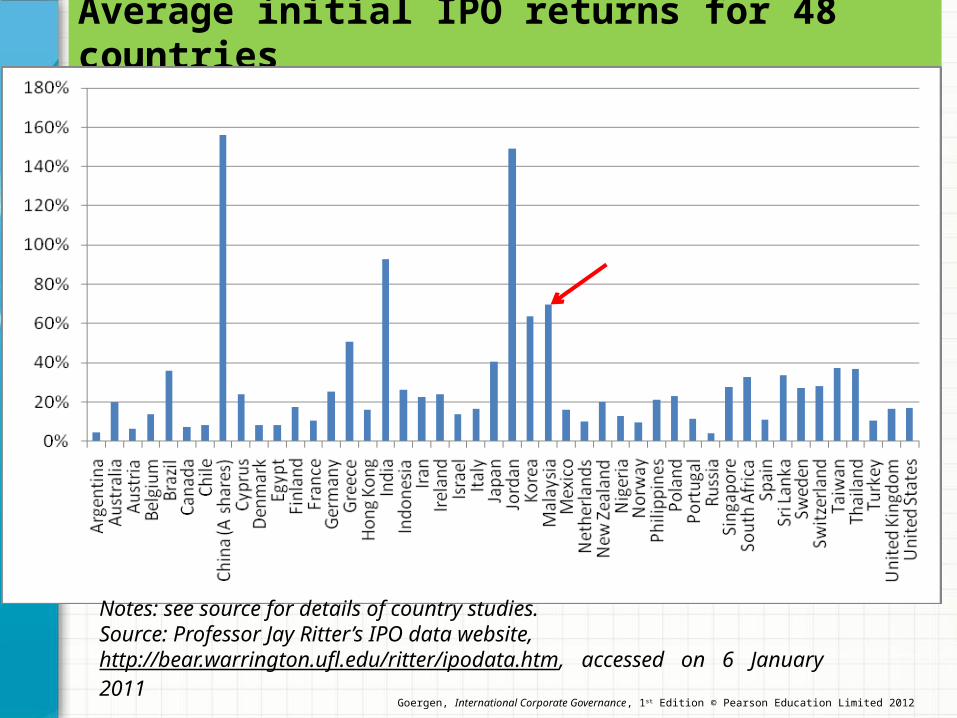

• IPO underpricing has been observed for a large number of countries, including developed as well as emerging economies.

• Average underpricing ranges from 4.2% in Russia to 156.1% in China.

• Although there are many theories on IPO underpricing, there is as yet no single theory that explains all of the IPO underpricing and has empirical support across both different types of firms and markets.

Asymmetric Information, Pricing Anomalies and

the Separation of Ownership and Control in IPOs

(Continued)

Average initial IPO returns for 48 countries

Notes: see source for details of country studies.Source: Professor Jay Ritter’s IPO data website, http://bear.warrington.ufl.edu/ritter/ipodata.htm, accessed on 6 January 2011

Goergen, International Corporate Governance, 1st Edition © Pearson Education Limited 2012

• Michael Brennan and Julian Franks link underpricing to corporate governance, i.e. the allocation of power between insiders and outsiders after the IPO.

• They argue that the incumbent owners of IPO firms deliberately underprice the share to keep control over the firm.

• By underpricing the shares, the IPO will be oversubscribed.

• This then enables the incumbents to discriminate in favour of small investors in the allocation of shares.

Asymmetric Information, Pricing Anomalies and

the Separation of Ownership and Control in IPOs

(Continued)

• This will reduce the concentration of outside ownership.

• While IPOs are initially underpriced, they under-perform over the long term relative to other firms that have been on the stock exchange for a while and are of a similar size.

Asymmetric Information, Pricing Anomalies and

the Separation of Ownership and Control in IPOs

(Continued)

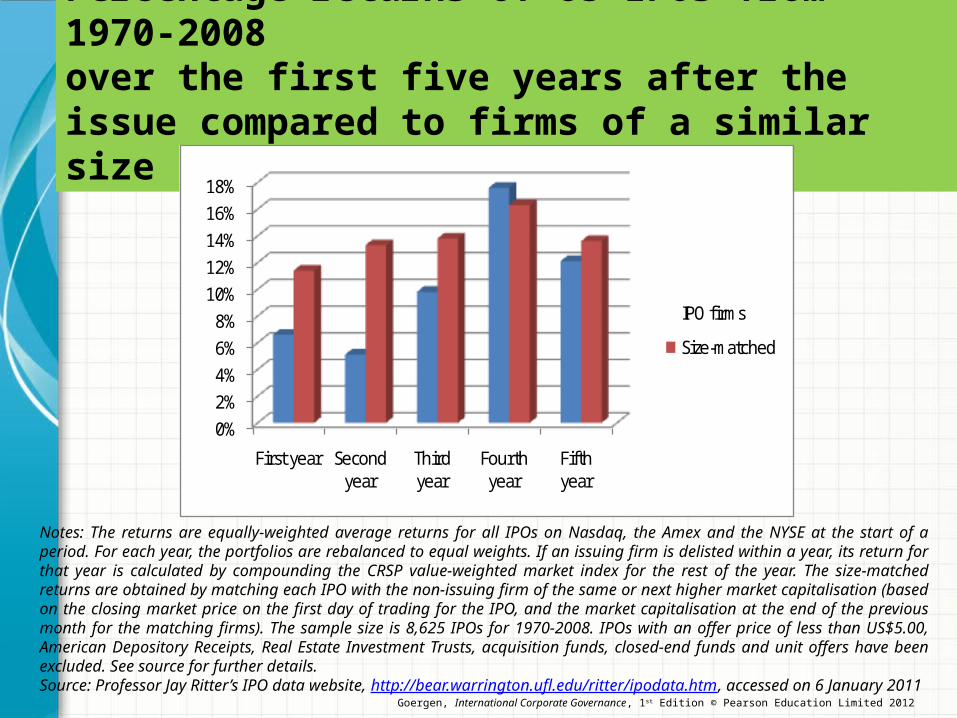

Percentage returns of US IPOs from 1970-2008 over the first five years after the issue compared to firms of a similar size

0%2%4%6%8%

10%12%14%16%18%

First year Second year

Third year

Fourth year

Fifth year

IPO firms

Size-matched

Notes: The returns are equally-weighted average returns for all IPOs on Nasdaq, the Amex and the NYSE at the start of a period. For each year, the portfolios are rebalanced to equal weights. If an issuing firm is delisted within a year, its return for that year is calculated by compounding the CRSP value-weighted market index for the rest of the year. The size-matched returns are obtained by matching each IPO with the non-issuing firm of the same or next higher market capitalisation (based on the closing market price on the first day of trading for the IPO, and the market capitalisation at the end of the previous month for the matching firms). The sample size is 8,625 IPOs for 1970-2008. IPOs with an offer price of less than US$5.00, American Depository Receipts, Real Estate Investment Trusts, acquisition funds, closed-end funds and unit offers have been excluded. See source for further details.Source: Professor Jay Ritter’s IPO data website, http://bear.warrington.ufl.edu/ritter/ipodata.htm, accessed on 6 January 2011 Goergen, International Corporate Governance, 1st Edition © Pearson Education Limited 2012

• Compared to IPO underpricing, there are fewer theoretical explanations of the bad long-term performance of IPOs.

• However, this phenomenon has also been linked to corporate governance.

• As managerial ownership decreases after the IPO, there is a reduction in their incentives.

• The existing empirical evidence suggests that there is no link between firm performance and ownership or control held by the managers post-IPO.

Asymmetric Information, Pricing Anomalies and the Separation of Ownership and Control in IPOs (Continued)

• However, Marc Goergen and Luc Renneboog find that the evolution of ownership and control in British and German IPOs can be explained by firm characteristics such as– risk,– growth,– size, and– performance.

Asymmetric Information, Pricing Anomalies and

the Separation of Ownership and Control in IPOs

(Continued)

Problems of Asymmetric Information and Ways to Mitigate Them

• At the time of the IPO, very little is know about the firm.

• What are the likely consequences of the pronounced asymmetry of information in IPOs?

• George Akerlof studied the consequences of asymmetric information in markets.

• One market he studied is the market for second-hand cars.

• It is very difficult for the buyer to judge the quality of a second-hand car.

Problems of Asymmetric Information and Ways to Mitigate Them (Continued)

• Hence, the danger is high that the buyer may end up with a lemon.

• The main consequence of the difficulty of assessing the quality of a good in a market is that the prices in the market will reflect the average quality of the goods in that market.

• This will have severe consequences for sellers of above-average quality goods in the market as the price they will be able to receive will be too low.

• The quality of firms going public is also difficult to assess.

• The consequence will be that entrepreneurs with above-average quality firms will receive a price for their firm which is too low.

• So how can they credibly signal to the market that their firm is of superior quality?

• They can do so by third-party certification such as via– the use of a highly reputable investment bank, and– venture capital financing.

Problems of Asymmetric Information andWays to Mitigate Them (Continued)

• In addition to third-party certification, entrepreneurs can also signal their superior quality via the ownership they retain in the firm after the IPO.

• Hayne Leland and David Pyle’s model predicts that outside investors perceive the ownership retained by the entrepreneur as a credible signal of firm quality.

• The higher the percentage of ownership retained the higher will be expected firm value.

• The signal is credible as it is costly for the entrepreneur to retain a large stake in the firm.

Problems of Asymmetric Information andWays to Mitigate Them (Continued)

• In addition to retaining a large stake in the IPO, the entrepreneur may also commit himself not to sell his shares after the IPO for a specific period.

• Such a commitment is called a lock-in agreement (lock-up agreement).

• Armando Gomes extends the Leland and Pyle model from a static context to a dynamic one.

• He argues that in countries with weak investor protection the entrepreneur can build up a reputation as a good manager over time by keeping a stake in the firm.

Problems of Asymmetric Information andWays to Mitigate Them (Continued)

• If the manager were to extract private benefits of control from the firm, the minority shareholders would discount the price of the firm.

• The manager would then be punished by a reduction in the value of his stake.

Problems of Asymmetric Information andWays to Mitigate Them (Continued)

The Power of the CEO• The CEO frequently assumes a key position in

the firm.• This is even more so the case in IPO firms.• Sydney Finkelstein proposes the following

four dimensions of CEO power1. structural power,2. ownership power,3. expert power, and 4. prestige power.

The Power of the CEO (Continued)

• Structural power is the power the CEO derives from his position within the firm’s hierarchy or organisational structure.

• It enables the CEO to control the behaviour and actions of his subordinates, thereby reducing uncertainty.

• This power may enable the CEO to push through decisions in case the top management is split.

• A more indirect manifestation of structural power is the superior information the CEO has about the firm.

• Ownership power is derived from the CEO’s ownership stake in the firm.

• It tends to increase with the size of the CEO’s ownership stake.

• If the CEO is the founder or related to the founder this may further amplify his power over subordinates and board members.

The Power of the CEO (Continued)

• The CEO’s expert power stems from – his knowledge of the technologies the firm uses,

and– his ability to deal with the firm’s stakeholders as

well as other environmental factors the firm faces.

• At the extreme, the CEO’s skill set may make him indispensable and put in danger the survival of the firm should he die or leave.

The Power of the CEO (Continued)

• Prestige power is derived from the CEO’s reputation and status within the institutional environment he operates in.

• The CEO’s prestige power increases with his stakeholders’ perception of his influence.

• For example, CEOs who sit on other firms’ boards are likely to have high prestige power.

• CEOs with high prestige power may be part of managerial elites that are admired and whose actions are copied by less prestigious managers.

The Power of the CEO (Continued)

• The firm’s legitimacy is also likely to depend on the CEO’s prestige power.

• The CEO’s prestige power is likely to benefit the firm via the information he is able to collect via his network of contacts.

The Power of the CEO (Continued)

• A fifth dimension of power, in addition to Finkelstein’s four dimensions, is

–5. control power.• Control power measures how pivotal the CEO

is in the voted decision, i.e. how often he will be part of a winning coalition.

• For example, a company has the following three shareholders– shareholder A with 40% of the votes,– shareholder B with 30%, and– the CEO with 25%.

The Power of the CEO (Continued)

• Neither of the three large shareholders has a majority.

• While the CEO is the smallest of the three large shareholders, there are three winning coalitions he can form:– A and CEO (65%),– B and CEO (55%), and– A, B and CEO (95%).

• The only other winning coalition is A and B (70%).

The Power of the CEO (Continued)

• Hence, the CEO is pivotal in three out of four winning coalitions and his control power index is 0.75.

• This is the so called Shapley value which measures the pivotal role of a shareholder.

The Power of the CEO (Continued)

Spinning of IPOs• Jay Ritter discusses the practice in the USA of

“spinning” initial public offerings (IPOs).• IPOs tend to be underpriced, i.e. the shares are

issued at a price which on average is lower that the closing price on the first trading day.

• If there is sufficient competition between investment banks taking companies public, one would expect that underpricing would be much lower or non-existent.

Spinning of IPOs (Continued)

• Ritter found evidence that investment banks used

the underpriced shares as bribes.• The underpriced shares were allocated to customers

of the investment banks to obtain further fee-earning business from them.

• The underpriced shares were also allocated to the executives of the underpriced IPO firms.

• Xiaoding Liu and Jay Ritter found that firms with executives that had been “spun”– Were more underpriced (by 18% (!) on

average)– Were less likely to switch investment banks in

the future.

• Some of the data on “spinning” of IPOs were used to prosecute the executive of Credit Suisse First Boston (CSFB), Frank Quattrone– Accounts of executives who were “spun”

were referred to as “Friend of Frank”.

• Most other major investment banks had been involved in the practice too.

Spinning of IPOs (Continued)

The Role of Venture Capitalists in IPOs

• Venture capitalists (VCs) provide risk capital to young firms that may find it difficult to tap into other sources of finance.

• However, they also provide management guidance as well networking opportunities.

• They also frequently help firms build their management teams, attract key staff, design their organisational structure and establish their market share.

The Role of Venture Capitalists in IPOs (Continued)• VCs frequently call for the replacement of the

entrepreneur by a professional manager thought to add value to the firm.

• However, the entrepreneur is likely to be against her replacement as– she may be personally attached to her firm, and– she may consider her replacement to be humiliating

and to damage her professional reputation.• Nevertheless, the replacement of the founder

CEO is a frequent occurrence, becoming more likely over time.

• So how do VCs manage to replace the entrepreneur?

• They do so via the voting rights they hold and these are frequently amplified by board representation.

• They also often have shareholder agreements and employment contracts which enable them to terminate the founder’s ownership and employment.

• Often, the entrepreneur’s shares are vested.• Vested shares are shares held by the firm on the

behalf of the entrepreneur.

The Role of Venture Capitalists in IPOs (Continued)

• The entrepreneur only obtains legal ownership once specific conditions have been met.

• VCs also typically provide their financing in the form of stage financing.

• Stage financing is financing that is provided gradually as the firm achieves specific performance mile stones.

• The mile stones are typically linked to major stages in the firm’s life cycle such as the development of a prototype.

The Role of Venture Capitalists in IPOs (Continued)

• Hence, VCs create value via the support, the expertise and the networks they offer the firm.

• They are also frequently seeking a successor to the founder who is expected to improve the firm’s value.

• They also tend to be involved in the design of the firm’s governance structure and the improvement of the founder CEO’s incentives.

• However, there is also evidence suggesting that VCs, in particular young VCs, may be subject to conflicts of interests.

The Role of Venture Capitalists in IPOs (Continued)

• Paul Gompers has proposed the grandstanding hypothesis.

• Young VCs, intend on establishing their reputation, take their portfolio firms public early to create a track record of successful investments.

• Venture-capital firms are normally in the form of partnerships with the silent partners, typically institutional investors, providing the funding.

• To guarantee future funding, the VCs will need to have at least one successful IPO.

The Role of Venture Capitalists in IPOs (Continued)

• They may do so by rushing their portfolio firms to the stock exchange.

• The cost from doing so comes in the form of higher underpricing as younger firms have been shown to be more severely underpriced.

• However, this cost is shared by all the shareholders whereas the benefits only accrue to the VC.

• Given that CEOs frequently hold shares in their firm, how do the VCs convince them to take their firm public early?

The Role of Venture Capitalists in IPOs (Continued)

• Michelle Lowry and Kevin Murphy argue that VCs grant CEOs stock options at the IPO with an exercise price equal to the deliberately low offer price.

• Lowry and Murphy do not find a link between IPO underpricing and the expected gains from the CEO’s stock options.

• However, Salim Chahine and Marc Goergen find evidence of such a link when they adjust for the power of the VC and the CEO as well as the power of the board of directors.

The Role of Venture Capitalists in IPOs (Continued)

• Nevertheless, despite these conflicts of interests the evidence suggests that VCs still create value in their portfolio firms.

The Role of Venture Capitalists in IPOs (Continued)

Models of CEO Succession

1. External candidate2. President and/or CEO3. Horse race4. Inside-outside model

Conclusions• The separation of ownership and control in

IPO firms.• Asymmetric information and firm quality.• Finkelstein’s dimensions of CEO power

applied to IPO firms.• Spinning of IPOs.• The role of VCs in IPO firms: value creation

versus conflicts of interests.• Models of CEO succession

Core Readings

• Goergen, M. (2012) International Corporate Governance, Pearson, Ch.12-14;

• David & Tayan, Brian (2011) Corporate Governance Matters, FT Press/Pearson New Jersey, Ch.7-9,11

• Monks & Minow (2011) Corporate Governance, 5th Edition, Wiley. Ch.4

Next Week’s Ideas for Discussion• Petit, Vale´rie and Bollaert, Helen (2012)

Flying Too Close to the Sun? Hubris Among CEOs and How to Prevent it, Journal of Business Ethics, 2012: 108: pp.265–283.

Casestudy 5 : Gertsner’s Pay Package at IBM

Read and prepare the Casestudy on Gertsner’s Pay Package at IBM (Monks & Minow (2011)) for discussion next class. Identify the corporate governance issues faced.

You are required to:

– Map out the stakeholder power/interest issues.

– Evaluate the executive compensation & incentives scheme and model of executive succession planning.

– Propose a more equitable scheme and model to satisfy all stakeholders.

QUESTIONS?