Embed Size (px)

Citation preview

REINSURANCE OF ASSET INTENSIVE PRODUCTS

Amit Ayer, FSA, FRM, MAAA

Head of Willis Re Life Solutions Group (LSG) Analytics / Modeling

Valuation Actuary Symposium

August 31, 2015

2

Table of Contents

A. Risks in “Asset Intensive” products…………………… 3

B. Dynamics of ceding companies and reinsurers……... 6

C. Challenges and considerations with reinsurance…… 9

D. Fixed Annuity reinsurance considerations …………. 10

E. Variable Annuity reinsurance considerations ………. 12

F. Indexed Annuity reinsurance considerations ………. 19

Appendix…………………………………………………….. 23

Risks in “Asset Intensive” Products What does “Asset Intensive” mean?

• Products which, from a risk profile to the insurance company, are affected by “assets” or investments on the company’s balance sheet

• Annuity reinsurance is really the ultimate form of “Asset Intensive” reinsurance, (e.g., reinsurance of liabilities that are heavily weighted toward credit, interest rate and equity risks)

• One major exception to this rule is that variable annuity reinsurance uses a modified coinsurance structure, so assets never leave the cedant’s balance sheet

A B C D E F

3

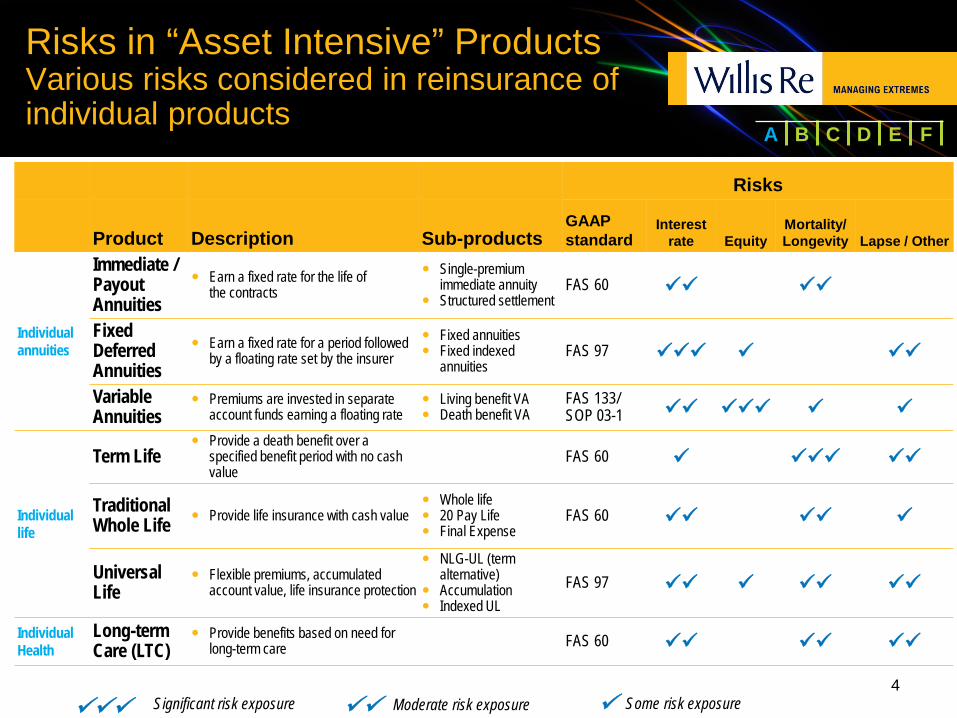

Risks in “Asset Intensive” Products Various risks considered in reinsurance of individual products

4

Risks

Product Description Sub-products GAAP standard

Interest rate Equity

Mortality/ Longevity Lapse / Other

Individual annuities

Immediate / Payout Annuities

Earn a fixed rate for the life of the contracts

Single-premium immediate annuity

Structured settlement FAS 60

Fixed Deferred Annuities

Earn a fixed rate for a period followed by a floating rate set by the insurer

Fixed annuities Fixed indexed

annuities FAS 97

Variable Annuities

Premiums are invested in separate account funds earning a floating rate

Living benefit VA Death benefit VA

FAS 133/ SOP 03-1

Individual life

Term Life Provide a death benefit over a

specified benefit period with no cash value

FAS 60

Traditional Whole Life Provide life insurance with cash value

Whole life 20 Pay Life Final Expense

FAS 60

Universal Life

Flexible premiums, accumulated account value, life insurance protection

NLG-UL (term alternative)

Accumulation Indexed UL

FAS 97

Individual Health

Long-term Care (LTC)

Provide benefits based on need for long-term care

FAS 60

Moderate risk exposure Some risk exposure

Significant risk exposure

A B C D E F

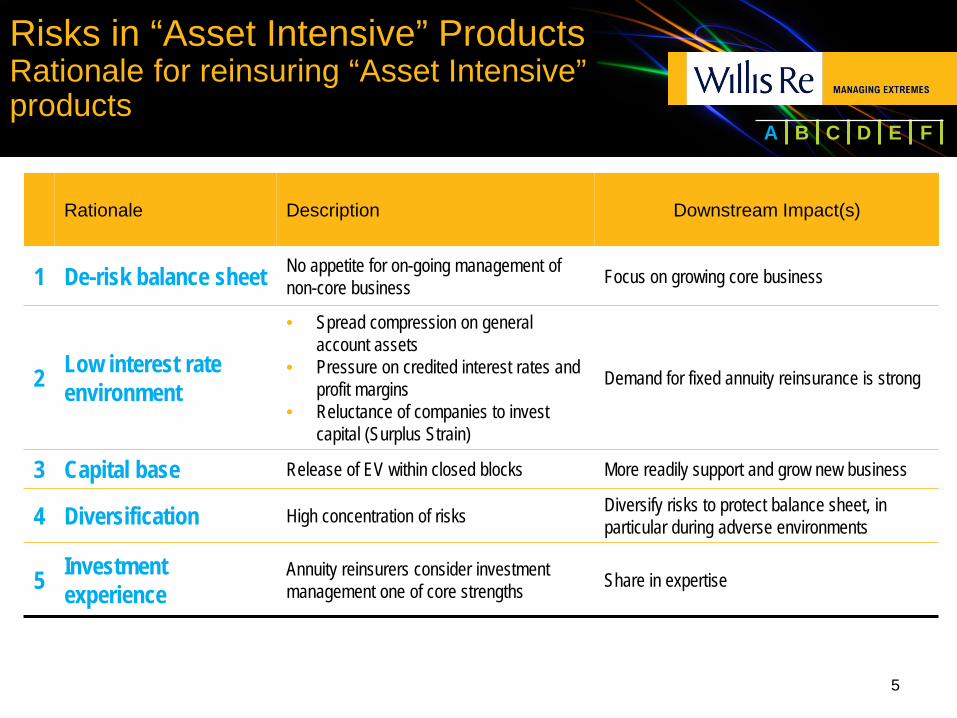

Risks in “Asset Intensive” Products Rationale for reinsuring “Asset Intensive” products

5

Rationale Description Downstream Impact(s)

1 De-risk balance sheet No appetite for on-going management of non-core business Focus on growing core business

2 Low interest rate environment

• Spread compression on general account assets

• Pressure on credited interest rates and profit margins

• Reluctance of companies to invest capital (Surplus Strain)

Demand for fixed annuity reinsurance is strong

3 Capital base Release of EV within closed blocks More readily support and grow new business

4 Diversification High concentration of risks Diversify risks to protect balance sheet, in particular during adverse environments

5 Investment experience

Annuity reinsurers consider investment management one of core strengths Share in expertise

A B C D E F

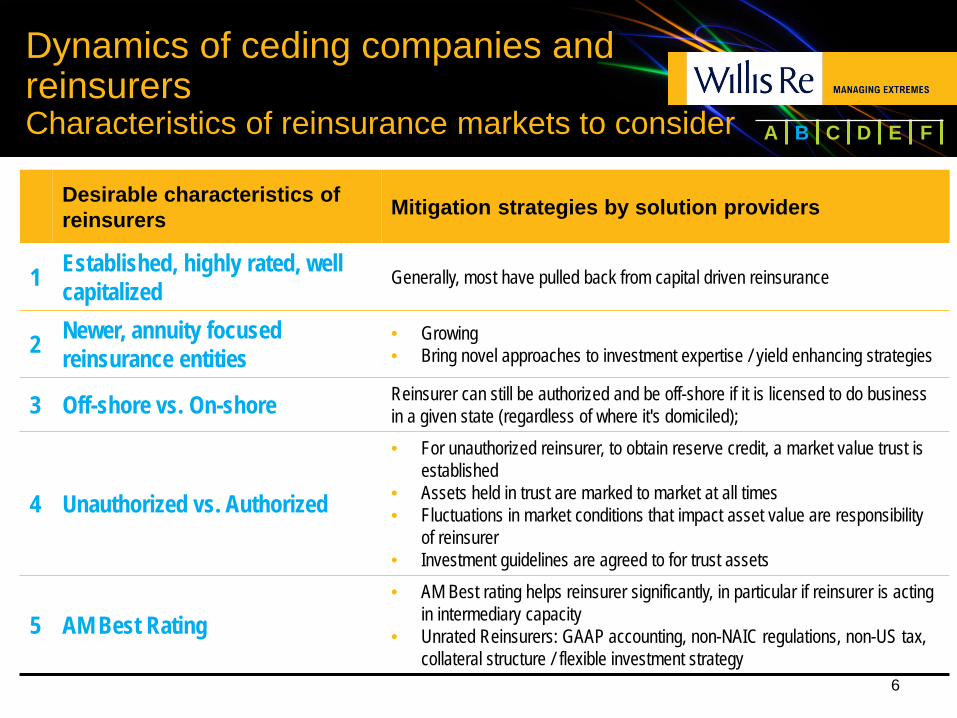

Dynamics of ceding companies and reinsurers Characteristics of reinsurance markets to consider

6

Desirable characteristics of reinsurers Mitigation strategies by solution providers

1 Established, highly rated, well capitalized Generally, most have pulled back from capital driven reinsurance

2 Newer, annuity focused reinsurance entities

• Growing • Bring novel approaches to investment expertise / yield enhancing strategies

3 Off-shore vs. On-shore Reinsurer can still be authorized and be off-shore if it is licensed to do business in a given state (regardless of where it's domiciled);

4 Unauthorized vs. Authorized

• For unauthorized reinsurer, to obtain reserve credit, a market value trust is established

• Assets held in trust are marked to market at all times • Fluctuations in market conditions that impact asset value are responsibility

of reinsurer • Investment guidelines are agreed to for trust assets

5 AM Best Rating • AM Best rating helps reinsurer significantly, in particular if reinsurer is acting

in intermediary capacity • Unrated Reinsurers: GAAP accounting, non-NAIC regulations, non-US tax,

collateral structure / flexible investment strategy

A B C D E F

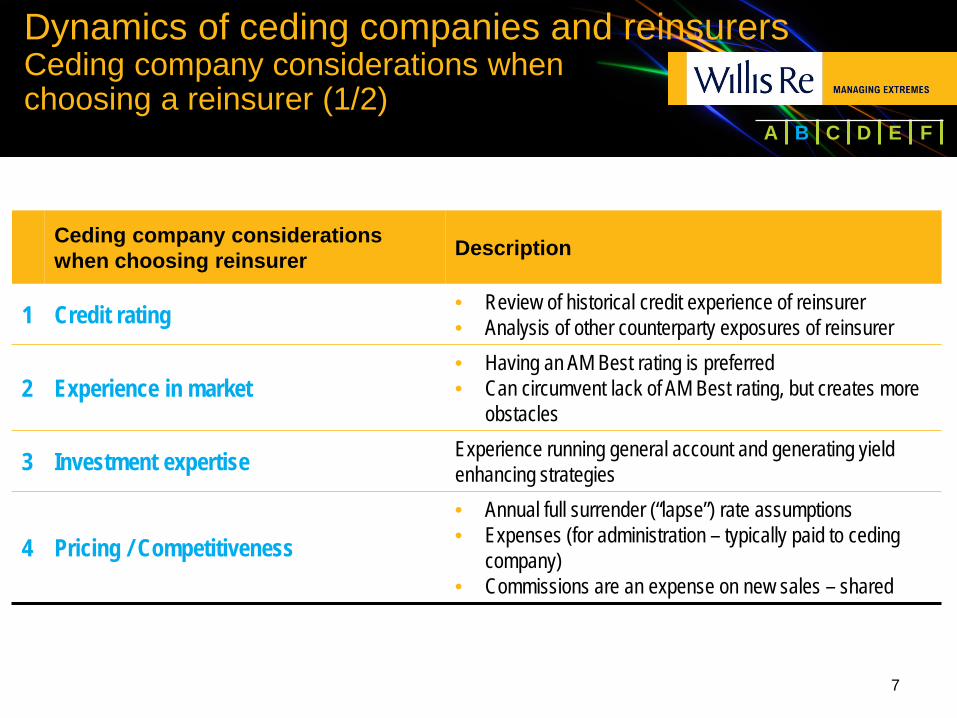

Dynamics of ceding companies and reinsurers Ceding company considerations when choosing a reinsurer (1/2)

7

Ceding company considerations when choosing reinsurer Description

1 Credit rating • Review of historical credit experience of reinsurer • Analysis of other counterparty exposures of reinsurer

2 Experience in market • Having an AM Best rating is preferred • Can circumvent lack of AM Best rating, but creates more

obstacles

3 Investment expertise Experience running general account and generating yield enhancing strategies

4 Pricing / Competitiveness • Annual full surrender (“lapse”) rate assumptions • Expenses (for administration – typically paid to ceding

company) • Commissions are an expense on new sales – shared

A B C D E F

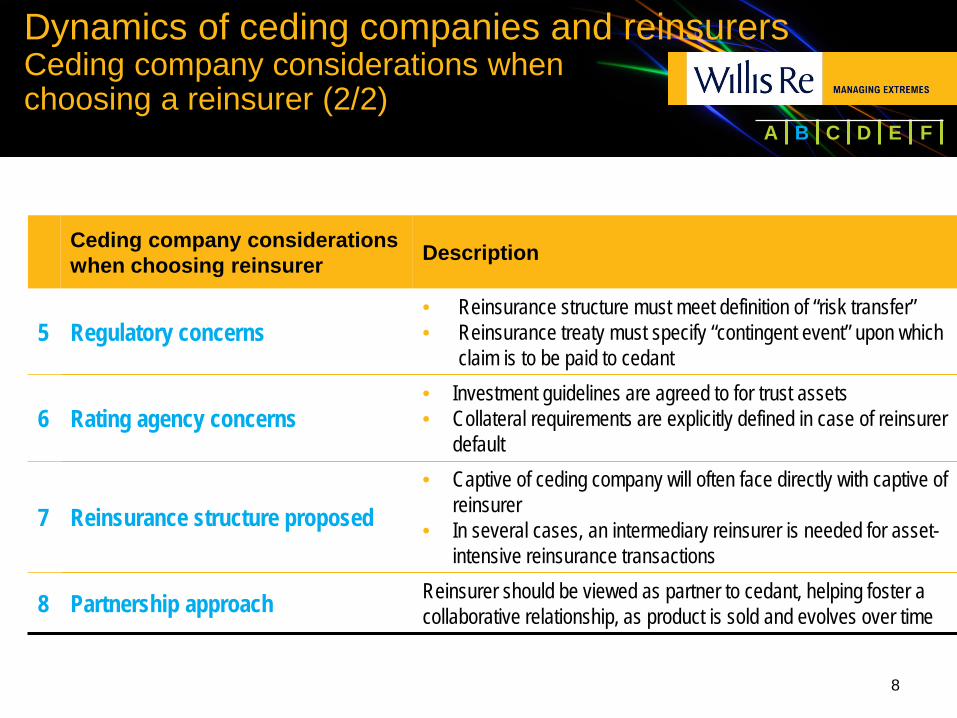

Dynamics of ceding companies and reinsurers Ceding company considerations when choosing a reinsurer (2/2)

8

Ceding company considerations when choosing reinsurer Description

5 Regulatory concerns • Reinsurance structure must meet definition of “risk transfer” • Reinsurance treaty must specify “contingent event” upon which

claim is to be paid to cedant

6 Rating agency concerns • Investment guidelines are agreed to for trust assets • Collateral requirements are explicitly defined in case of reinsurer

default

7 Reinsurance structure proposed • Captive of ceding company will often face directly with captive of

reinsurer • In several cases, an intermediary reinsurer is needed for asset-

intensive reinsurance transactions

8 Partnership approach Reinsurer should be viewed as partner to cedant, helping foster a collaborative relationship, as product is sold and evolves over time

A B C D E F

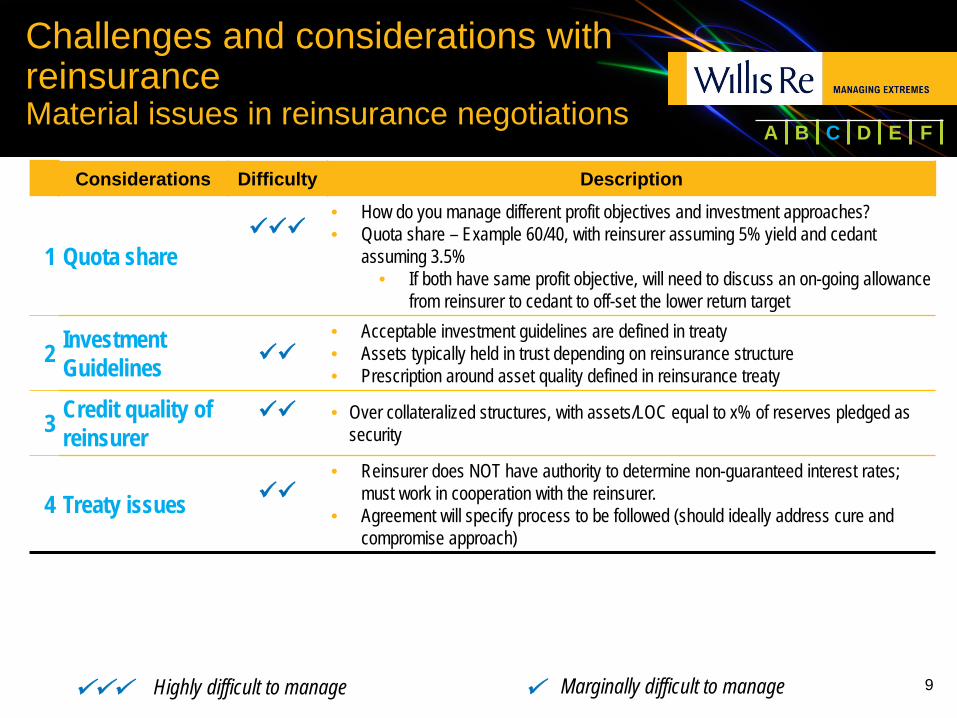

Challenges and considerations with reinsurance Material issues in reinsurance negotiations

9

Considerations Difficulty Description

1 Quota share

• How do you manage different profit objectives and investment approaches? • Quota share – Example 60/40, with reinsurer assuming 5% yield and cedant

assuming 3.5% • If both have same profit objective, will need to discuss an on-going allowance

from reinsurer to cedant to off-set the lower return target

2 Investment Guidelines

• Acceptable investment guidelines are defined in treaty • Assets typically held in trust depending on reinsurance structure • Prescription around asset quality defined in reinsurance treaty

3 Credit quality of reinsurer

• Over collateralized structures, with assets/LOC equal to x% of reserves pledged as security

4 Treaty issues

• Reinsurer does NOT have authority to determine non-guaranteed interest rates; must work in cooperation with the reinsurer.

• Agreement will specify process to be followed (should ideally address cure and compromise approach)

Marginally difficult to manage Highly difficult to manage

A B C D E F

Fixed annuity reinsurance considerations Interest Rates vs. Annuity Sales

• Fixed annuity sales have historically shown a negative correlation with interest rates

• Largest risk is disintermediation, in particular when interest rates rise precipitously

• 2015 sales are an annualized estimate of sales based on one quarter of data from LIMRA

• Baby boomers may be behind increase in fixed annuity sales in 2014/2015 (estimated) (more interested in financial products with guarantees than with equity markets)

10 Source: LIMRA SRI

Fixed Annuity Sales vs. 10-Year Treasury

Commentary

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0

20

40

60

80

100

120

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015(ann)

Fixed Annuity Sales (BN) (left) 10-Year Treasury Rate (right)

A B C D E F

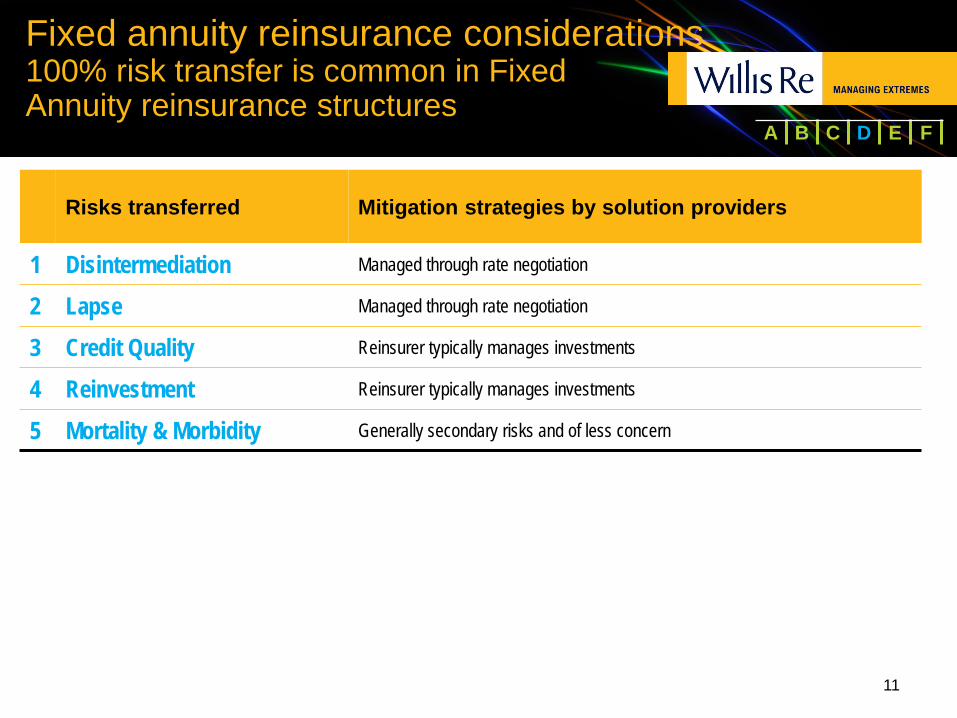

Fixed annuity reinsurance considerations 100% risk transfer is common in Fixed Annuity reinsurance structures

11

Risks transferred Mitigation strategies by solution providers

1 Disintermediation Managed through rate negotiation

2 Lapse Managed through rate negotiation

3 Credit Quality Reinsurer typically manages investments

4 Reinvestment Reinsurer typically manages investments

5 Mortality & Morbidity Generally secondary risks and of less concern

A B C D E F

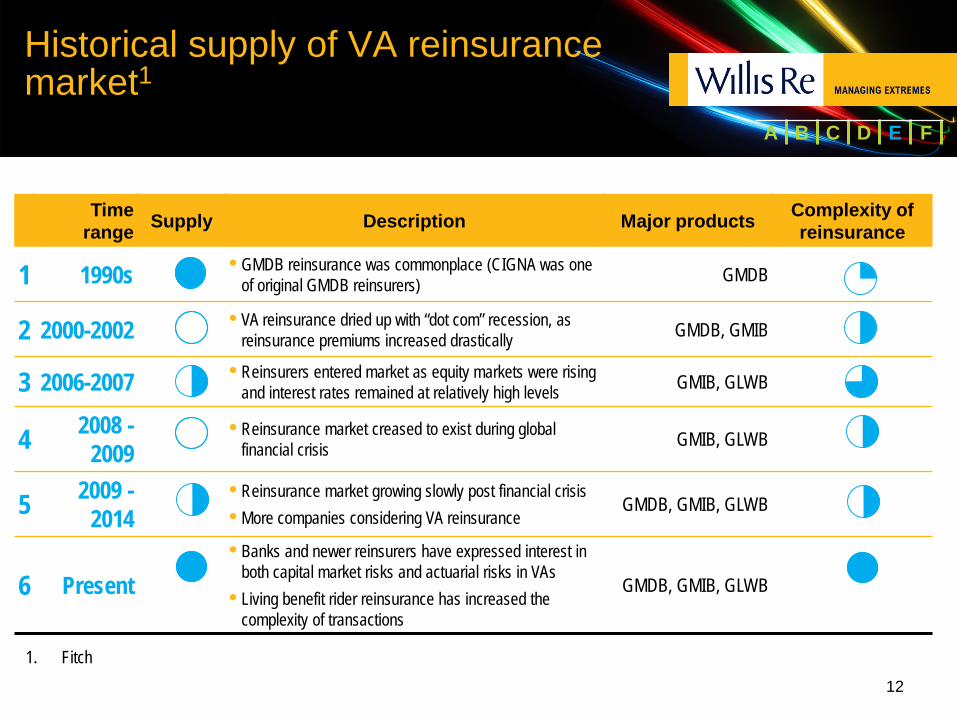

Historical supply of VA reinsurance market1

1. Fitch

Time range Supply Description Major products Complexity of

reinsurance

1 1990s • GMDB reinsurance was commonplace (CIGNA was one of original GMDB reinsurers) GMDB

2 2000-2002 • VA reinsurance dried up with “dot com” recession, as reinsurance premiums increased drastically GMDB, GMIB

3 2006-2007 • Reinsurers entered market as equity markets were rising and interest rates remained at relatively high levels GMIB, GLWB

4 2008 - 2009

• Reinsurance market creased to exist during global financial crisis GMIB, GLWB

5 2009 - 2014

• Reinsurance market growing slowly post financial crisis • More companies considering VA reinsurance

GMDB, GMIB, GLWB

6 Present • Banks and newer reinsurers have expressed interest in

both capital market risks and actuarial risks in VAs • Living benefit rider reinsurance has increased the

complexity of transactions

GMDB, GMIB, GLWB

12

A B C D E F

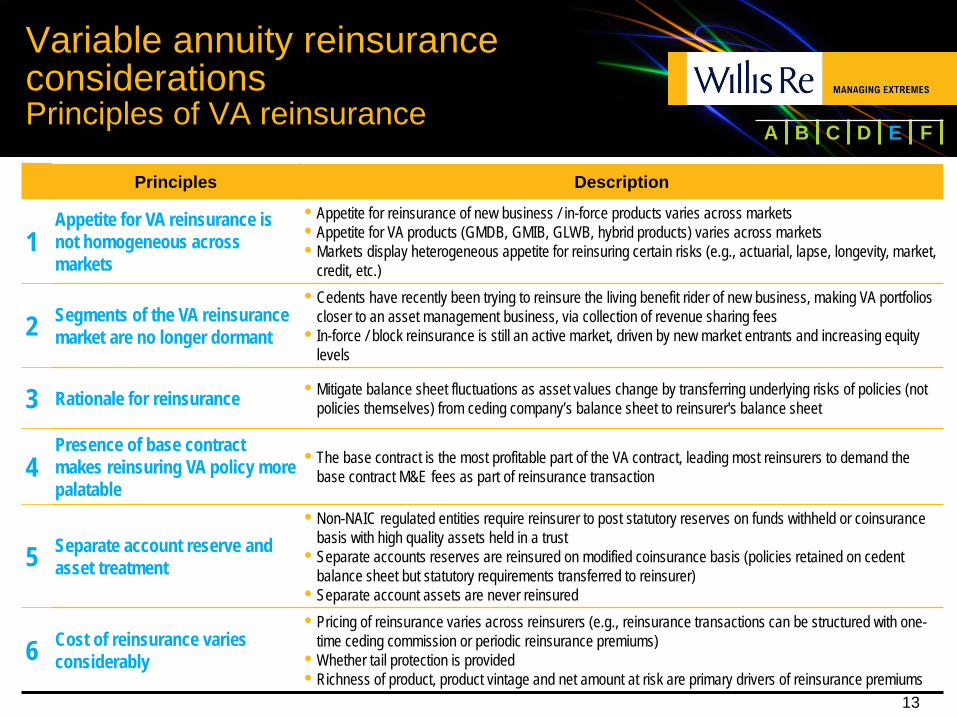

Variable annuity reinsurance considerations Principles of VA reinsurance

Principles Description

1 Appetite for VA reinsurance is not homogeneous across markets

• Appetite for reinsurance of new business / in-force products varies across markets • Appetite for VA products (GMDB, GMIB, GLWB, hybrid products) varies across markets • Markets display heterogeneous appetite for reinsuring certain risks (e.g., actuarial, lapse, longevity, market,

credit, etc.)

2 Segments of the VA reinsurance market are no longer dormant

• Cedents have recently been trying to reinsure the living benefit rider of new business, making VA portfolios closer to an asset management business, via collection of revenue sharing fees

• In-force / block reinsurance is still an active market, driven by new market entrants and increasing equity levels

3 Rationale for reinsurance • Mitigate balance sheet fluctuations as asset values change by transferring underlying risks of policies (not policies themselves) from ceding company’s balance sheet to reinsurer's balance sheet

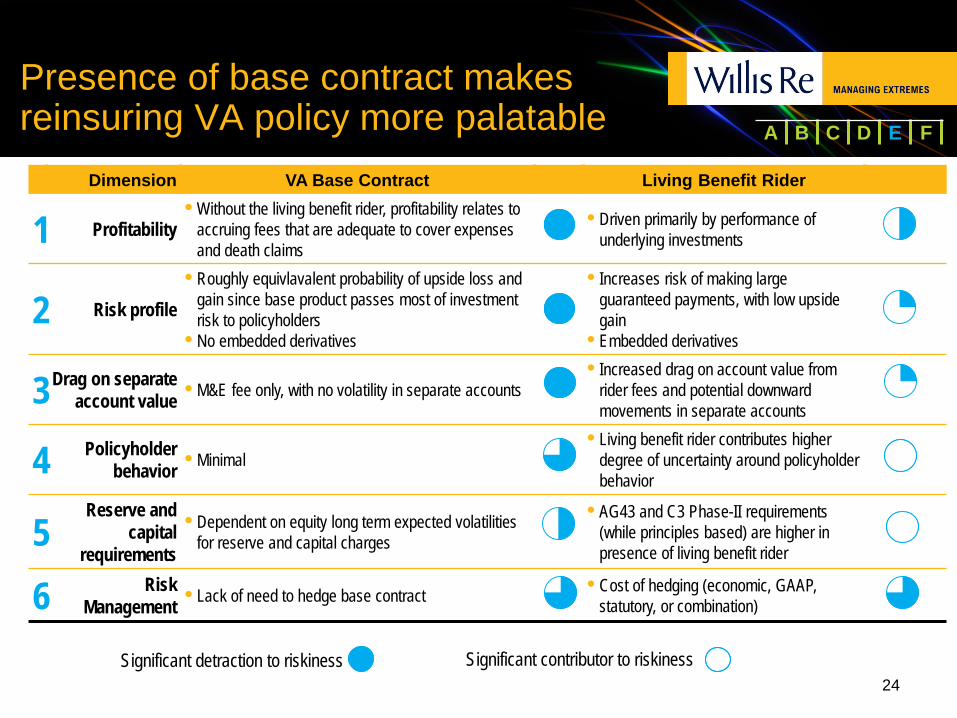

4 Presence of base contract makes reinsuring VA policy more palatable

• The base contract is the most profitable part of the VA contract, leading most reinsurers to demand the base contract M&E fees as part of reinsurance transaction

5 Separate account reserve and asset treatment

• Non-NAIC regulated entities require reinsurer to post statutory reserves on funds withheld or coinsurance basis with high quality assets held in a trust

• Separate accounts reserves are reinsured on modified coinsurance basis (policies retained on cedent balance sheet but statutory requirements transferred to reinsurer)

• Separate account assets are never reinsured

6 Cost of reinsurance varies considerably

• Pricing of reinsurance varies across reinsurers (e.g., reinsurance transactions can be structured with one-time ceding commission or periodic reinsurance premiums)

• Whether tail protection is provided • Richness of product, product vintage and net amount at risk are primary drivers of reinsurance premiums

13

A B C D E F

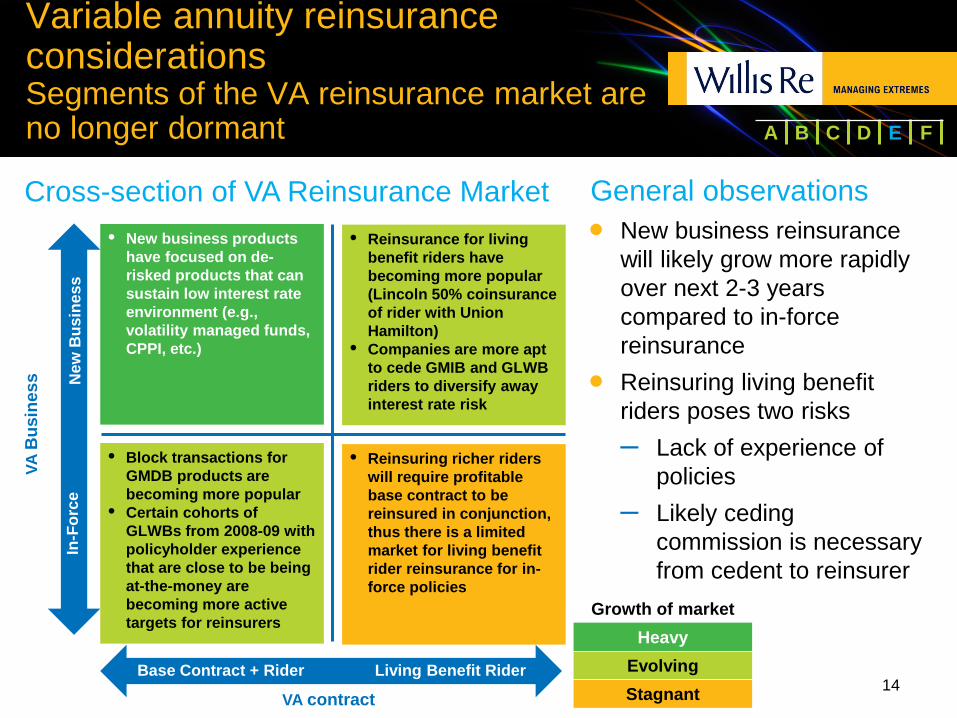

Variable annuity reinsurance considerations Segments of the VA reinsurance market are no longer dormant

General observations • New business reinsurance

will likely grow more rapidly over next 2-3 years compared to in-force reinsurance

• Reinsuring living benefit riders poses two risks – Lack of experience of

policies – Likely ceding

commission is necessary from cedent to reinsurer

14

Cross-section of VA Reinsurance Market

VA B

usin

ess N

ew B

usin

ess

In-F

orce

Base Contract + Rider Living Benefit Rider

• New business products have focused on de-risked products that can sustain low interest rate environment (e.g., volatility managed funds, CPPI, etc.)

VA contract

• Reinsurance for living benefit riders have becoming more popular (Lincoln 50% coinsurance of rider with Union Hamilton)

• Companies are more apt to cede GMIB and GLWB riders to diversify away interest rate risk

• Reinsuring richer riders will require profitable base contract to be reinsured in conjunction, thus there is a limited market for living benefit rider reinsurance for in-force policies

• Block transactions for GMDB products are becoming more popular

• Certain cohorts of GLWBs from 2008-09 with policyholder experience that are close to be being at-the-money are becoming more active targets for reinsurers

Growth of market Heavy

Evolving Stagnant

A B C D E F

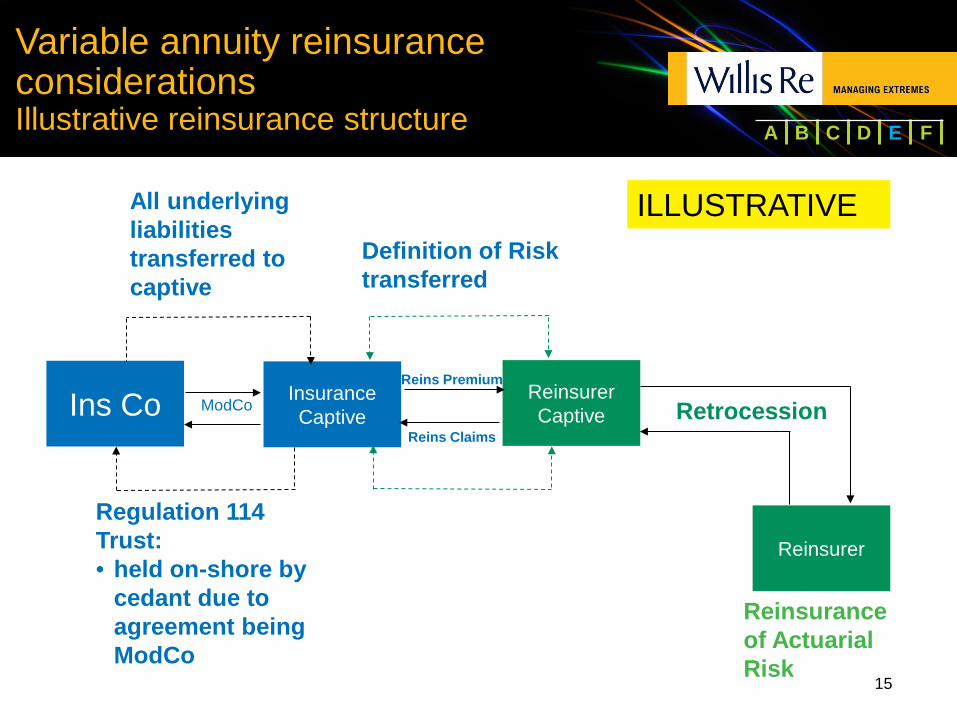

15

Variable annuity reinsurance considerations Illustrative reinsurance structure

Ins Co Insurance Captive

ModCo

Regulation 114 Trust: • held on-shore by

cedant due to agreement being ModCo

Reinsurer Captive

Reins Premium

Reins Claims

Reinsurer

Retrocession

Definition of Risk transferred

All underlying liabilities transferred to captive

Reinsurance of Actuarial Risk

ILLUSTRATIVE

A B C D E F

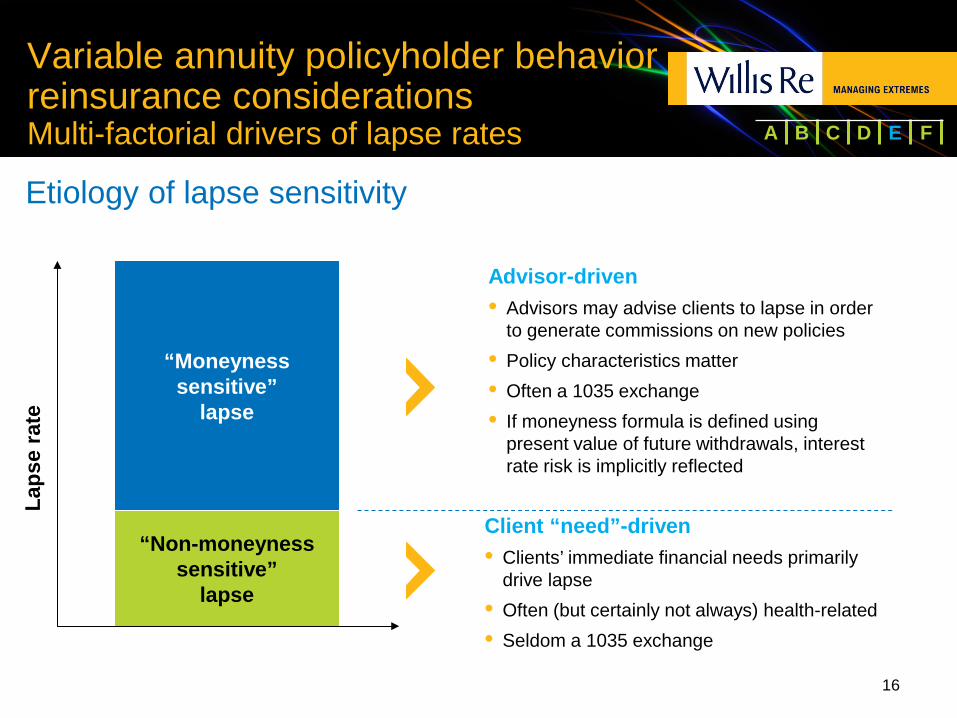

“Non-moneyness sensitive”

lapse

Laps

e ra

te

Variable annuity policyholder behavior reinsurance considerations Multi-factorial drivers of lapse rates

Etiology of lapse sensitivity

“Moneyness sensitive”

lapse

Client “need”-driven • Clients’ immediate financial needs primarily

drive lapse • Often (but certainly not always) health-related • Seldom a 1035 exchange

Advisor-driven • Advisors may advise clients to lapse in order

to generate commissions on new policies • Policy characteristics matter • Often a 1035 exchange • If moneyness formula is defined using

present value of future withdrawals, interest rate risk is implicitly reflected

16

A B C D E F

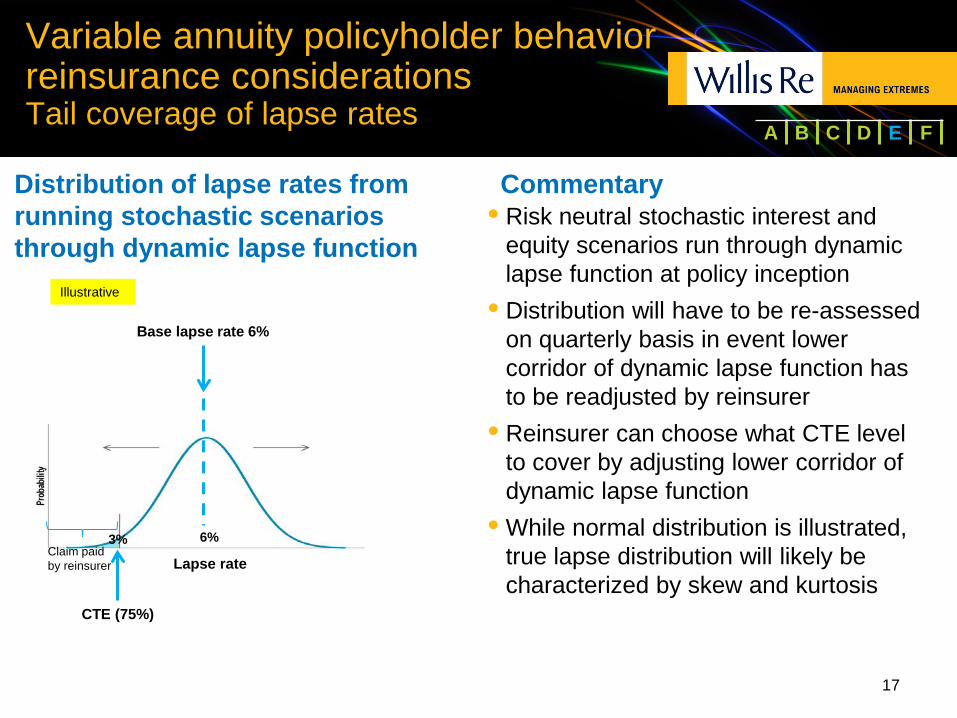

Variable annuity policyholder behavior reinsurance considerations Tail coverage of lapse rates

17

Distribution of lapse rates from running stochastic scenarios through dynamic lapse function

Lapse rate

Commentary • Risk neutral stochastic interest and

equity scenarios run through dynamic lapse function at policy inception

• Distribution will have to be re-assessed on quarterly basis in event lower corridor of dynamic lapse function has to be readjusted by reinsurer

• Reinsurer can choose what CTE level to cover by adjusting lower corridor of dynamic lapse function

• While normal distribution is illustrated, true lapse distribution will likely be characterized by skew and kurtosis

Base lapse rate 6%

6% 3%

CTE (75%)

Claim paid by reinsurer

Illustrative

A B C D E F

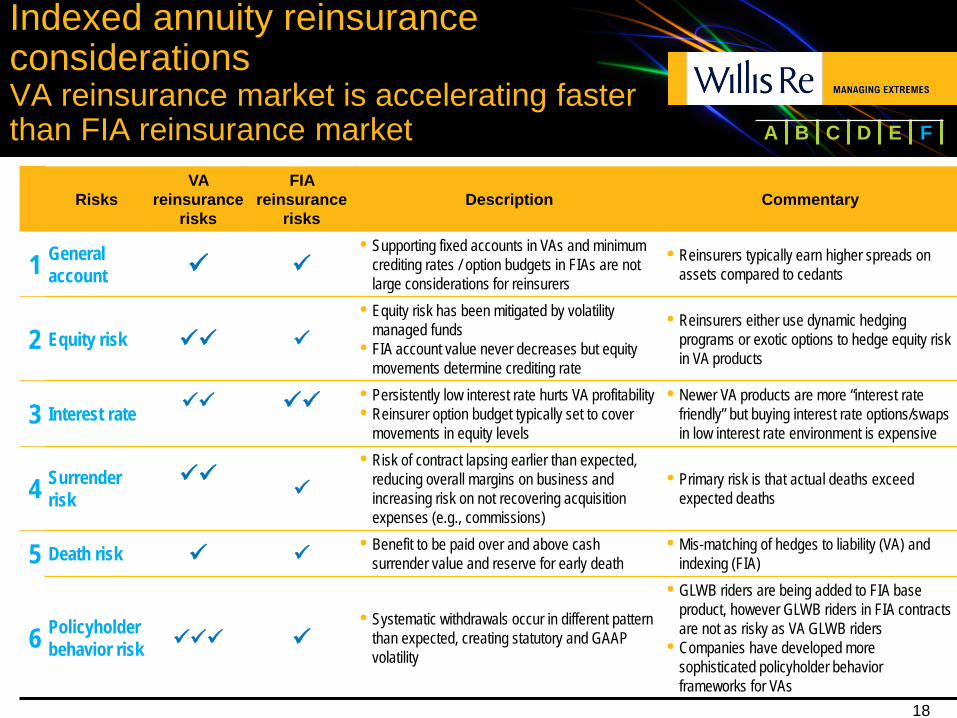

Indexed annuity reinsurance considerations VA reinsurance market is accelerating faster than FIA reinsurance market

18

Risks VA

reinsurance risks

FIA reinsurance

risks Description Commentary

1 General account

• Supporting fixed accounts in VAs and minimum crediting rates / option budgets in FIAs are not large considerations for reinsurers

• Reinsurers typically earn higher spreads on assets compared to cedants

2 Equity risk • Equity risk has been mitigated by volatility

managed funds • FIA account value never decreases but equity

movements determine crediting rate

• Reinsurers either use dynamic hedging programs or exotic options to hedge equity risk in VA products

3 Interest rate

• Persistently low interest rate hurts VA profitability • Reinsurer option budget typically set to cover

movements in equity levels

• Newer VA products are more “interest rate friendly” but buying interest rate options/swaps in low interest rate environment is expensive

4 Surrender risk

• Risk of contract lapsing earlier than expected, reducing overall margins on business and increasing risk on not recovering acquisition expenses (e.g., commissions)

• Primary risk is that actual deaths exceed expected deaths

5 Death risk • Benefit to be paid over and above cash surrender value and reserve for early death

• Mis-matching of hedges to liability (VA) and indexing (FIA)

6 Policyholder behavior risk

• Systematic withdrawals occur in different pattern than expected, creating statutory and GAAP volatility

• GLWB riders are being added to FIA base product, however GLWB riders in FIA contracts are not as risky as VA GLWB riders

• Companies have developed more sophisticated policyholder behavior frameworks for VAs

A B C D E F

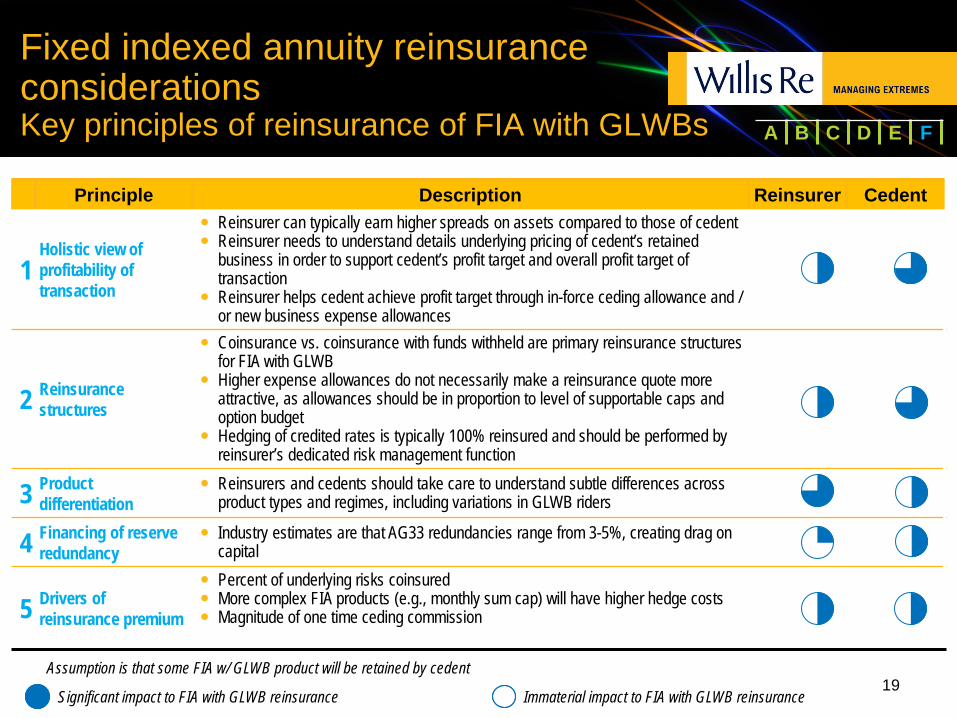

Fixed indexed annuity reinsurance considerations Key principles of reinsurance of FIA with GLWBs

Principle Description Reinsurer Cedent

1 Holistic view of profitability of transaction

Reinsurer can typically earn higher spreads on assets compared to those of cedent Reinsurer needs to understand details underlying pricing of cedent’s retained

business in order to support cedent’s profit target and overall profit target of transaction

Reinsurer helps cedent achieve profit target through in-force ceding allowance and / or new business expense allowances

2 Reinsurance structures

Coinsurance vs. coinsurance with funds withheld are primary reinsurance structures for FIA with GLWB

Higher expense allowances do not necessarily make a reinsurance quote more attractive, as allowances should be in proportion to level of supportable caps and option budget

Hedging of credited rates is typically 100% reinsured and should be performed by reinsurer’s dedicated risk management function

3 Product differentiation

Reinsurers and cedents should take care to understand subtle differences across product types and regimes, including variations in GLWB riders

4 Financing of reserve redundancy

Industry estimates are that AG33 redundancies range from 3-5%, creating drag on capital

5 Drivers of reinsurance premium

Percent of underlying risks coinsured More complex FIA products (e.g., monthly sum cap) will have higher hedge costs Magnitude of one time ceding commission

Significant impact to FIA with GLWB reinsurance Immaterial impact to FIA with GLWB reinsurance 19

Assumption is that some FIA w/ GLWB product will be retained by cedent

A B C D E F

Q&A

Contact information

Amit Ayer, FSA, FRM, MAAA Vice President, Analytics and Modeling Life Solutions Group (E): [email protected] (T): +1 212 915 8310

21

Willis Re Brookfield Place 200 Liberty Street New York, NY 10281

APPENDIX

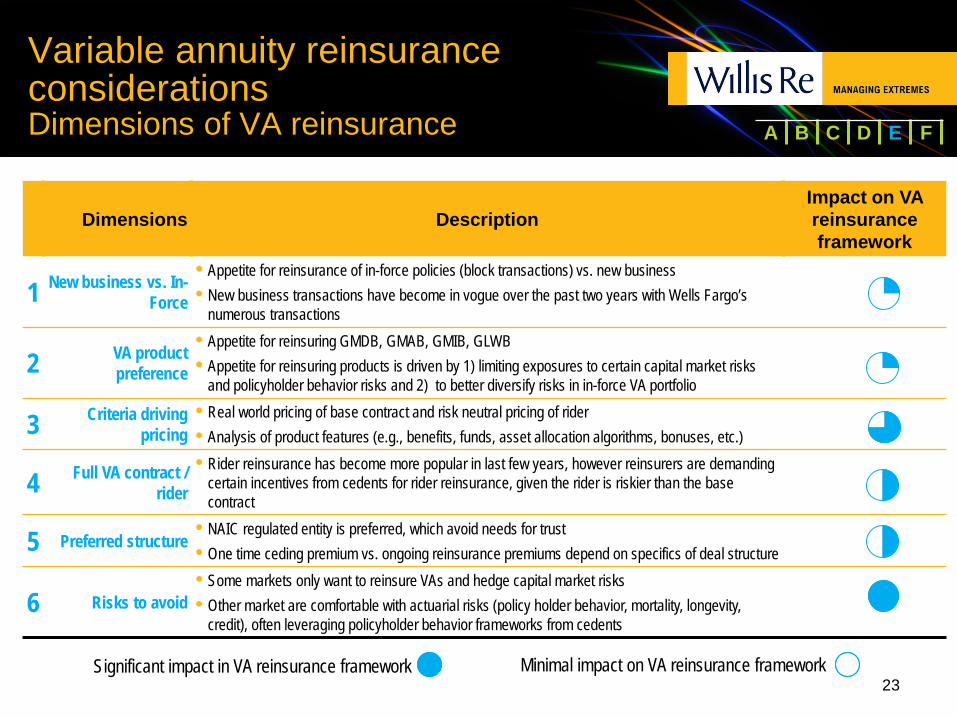

Variable annuity reinsurance considerations Dimensions of VA reinsurance

Dimensions Description Impact on VA reinsurance framework

1 New business vs. In-Force

• Appetite for reinsurance of in-force policies (block transactions) vs. new business • New business transactions have become in vogue over the past two years with Wells Fargo’s

numerous transactions

2 VA product preference

• Appetite for reinsuring GMDB, GMAB, GMIB, GLWB • Appetite for reinsuring products is driven by 1) limiting exposures to certain capital market risks

and policyholder behavior risks and 2) to better diversify risks in in-force VA portfolio

3 Criteria driving pricing

• Real world pricing of base contract and risk neutral pricing of rider • Analysis of product features (e.g., benefits, funds, asset allocation algorithms, bonuses, etc.)

4 Full VA contract / rider

• Rider reinsurance has become more popular in last few years, however reinsurers are demanding certain incentives from cedents for rider reinsurance, given the rider is riskier than the base contract

5 Preferred structure • NAIC regulated entity is preferred, which avoid needs for trust • One time ceding premium vs. ongoing reinsurance premiums depend on specifics of deal structure

6 Risks to avoid • Some markets only want to reinsure VAs and hedge capital market risks • Other market are comfortable with actuarial risks (policy holder behavior, mortality, longevity,

credit), often leveraging policyholder behavior frameworks from cedents

Significant impact in VA reinsurance framework Minimal impact on VA reinsurance framework 23

A B C D E F

Presence of base contract makes reinsuring VA policy more palatable

Dimension VA Base Contract Living Benefit Rider

1 Profitability • Without the living benefit rider, profitability relates to

accruing fees that are adequate to cover expenses and death claims

• Driven primarily by performance of underlying investments

2 Risk profile • Roughly equivlavalent probability of upside loss and

gain since base product passes most of investment risk to policyholders

• No embedded derivatives

• Increases risk of making large

guaranteed payments, with low upside gain

• Embedded derivatives

3 Drag on separate account value • M&E fee only, with no volatility in separate accounts

• Increased drag on account value from rider fees and potential downward movements in separate accounts

4 Policyholder behavior • Minimal

• Living benefit rider contributes higher degree of uncertainty around policyholder behavior

5 Reserve and

capital requirements

• Dependent on equity long term expected volatilities for reserve and capital charges

• AG43 and C3 Phase-II requirements

(while principles based) are higher in presence of living benefit rider

6 Risk Management • Lack of need to hedge base contract • Cost of hedging (economic, GAAP,

statutory, or combination)

Significant detraction to riskiness Significant contributor to riskiness 24

A B C D E F

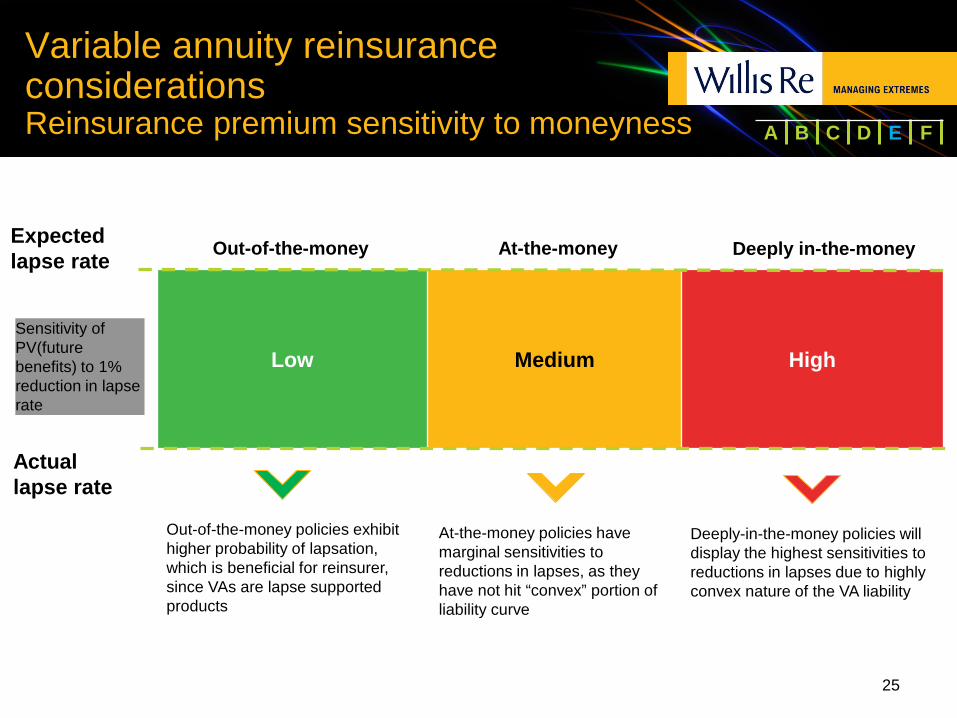

Variable annuity reinsurance considerations Reinsurance premium sensitivity to moneyness

25

Low

Medium

High

Deeply in-the-money At-the-money Out-of-the-money Expected lapse rate

Actual lapse rate

Sensitivity of PV(future benefits) to 1% reduction in lapse rate

Out-of-the-money policies exhibit higher probability of lapsation, which is beneficial for reinsurer, since VAs are lapse supported products

Deeply-in-the-money policies will display the highest sensitivities to reductions in lapses due to highly convex nature of the VA liability

At-the-money policies have marginal sensitivities to reductions in lapses, as they have not hit “convex” portion of liability curve

A B C D E F

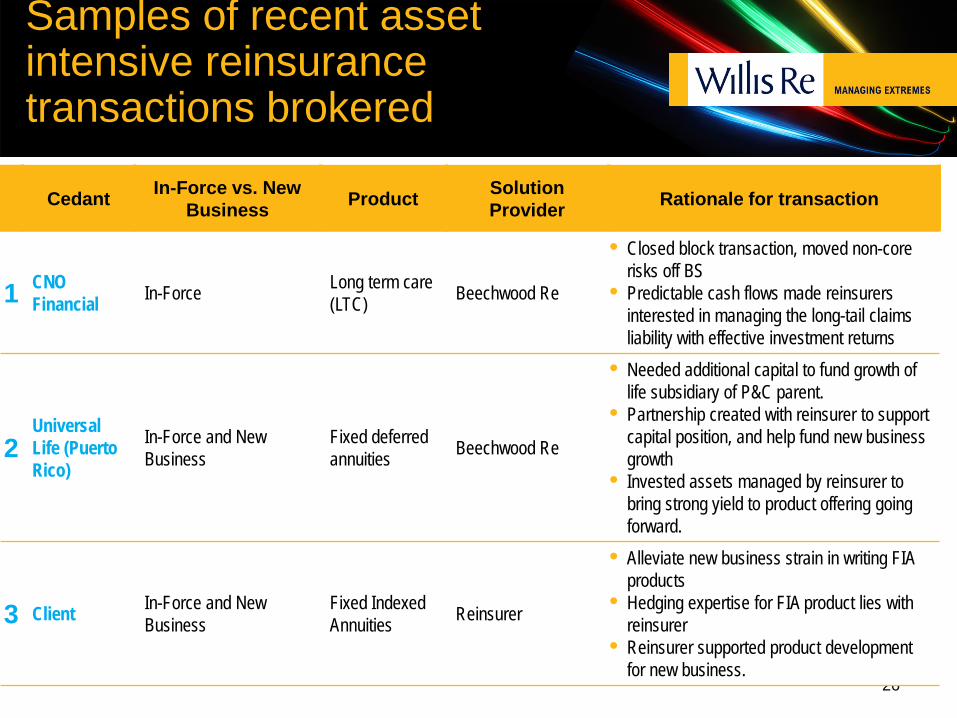

Samples of recent asset intensive reinsurance transactions brokered

26

Cedant In-Force vs. New Business Product Solution

Provider Rationale for transaction

1 CNO Financial In-Force Long term care

(LTC) Beechwood Re

• Closed block transaction, moved non-core risks off BS

• Predictable cash flows made reinsurers interested in managing the long-tail claims liability with effective investment returns

2 Universal Life (Puerto Rico)

In-Force and New Business

Fixed deferred annuities Beechwood Re

• Needed additional capital to fund growth of life subsidiary of P&C parent.

• Partnership created with reinsurer to support capital position, and help fund new business growth

• Invested assets managed by reinsurer to bring strong yield to product offering going forward.

3 Client In-Force and New Business

Fixed Indexed Annuities Reinsurer

• Alleviate new business strain in writing FIA products

• Hedging expertise for FIA product lies with reinsurer

• Reinsurer supported product development for new business.

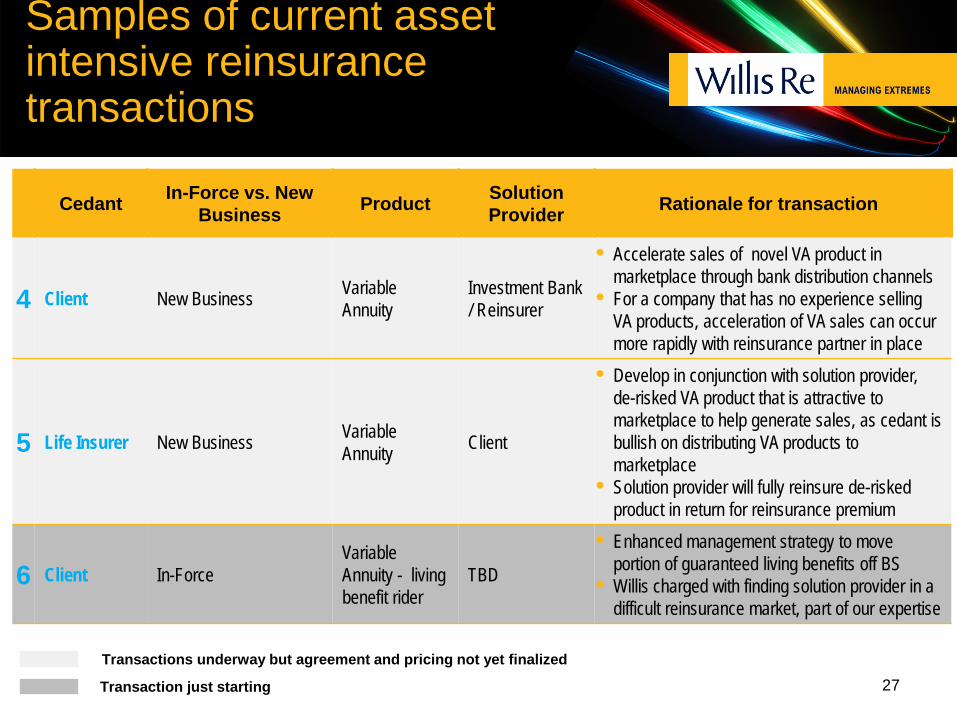

Samples of current asset intensive reinsurance transactions

27

Cedant In-Force vs. New Business Product Solution

Provider Rationale for transaction

4 Client New Business Variable Annuity

Investment Bank / Reinsurer

• Accelerate sales of novel VA product in marketplace through bank distribution channels

• For a company that has no experience selling VA products, acceleration of VA sales can occur more rapidly with reinsurance partner in place

5 Life Insurer New Business Variable Annuity Client

• Develop in conjunction with solution provider, de-risked VA product that is attractive to marketplace to help generate sales, as cedant is bullish on distributing VA products to marketplace

• Solution provider will fully reinsure de-risked product in return for reinsurance premium

6 Client In-Force Variable Annuity - living benefit rider

TBD

• Enhanced management strategy to move portion of guaranteed living benefits off BS

• Willis charged with finding solution provider in a difficult reinsurance market, part of our expertise

Transaction just starting

Transactions underway but agreement and pricing not yet finalized

Surrender Charge

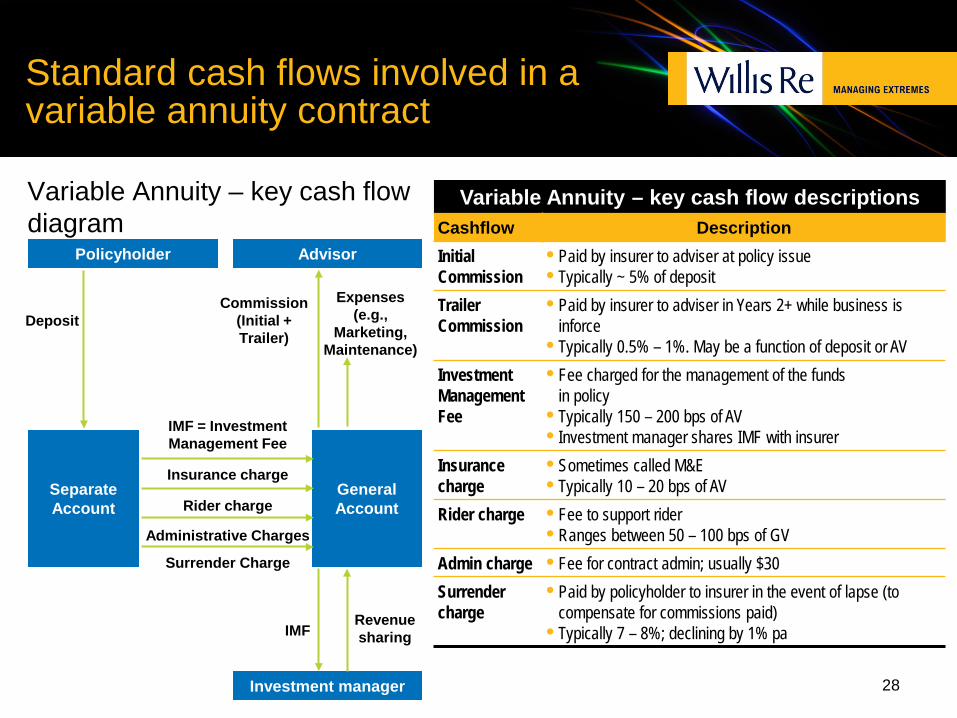

Standard cash flows involved in a variable annuity contract

Variable Annuity – key cash flow diagram

28

Variable Annuity – key cash flow descriptions Cashflow Description Initial Commission

• Paid by insurer to adviser at policy issue • Typically ~ 5% of deposit

Trailer Commission

• Paid by insurer to adviser in Years 2+ while business is inforce

• Typically 0.5% – 1%. May be a function of deposit or AV Investment Management Fee

• Fee charged for the management of the funds in policy

• Typically 150 – 200 bps of AV • Investment manager shares IMF with insurer

Insurance charge

• Sometimes called M&E • Typically 10 – 20 bps of AV

Rider charge • Fee to support rider • Ranges between 50 – 100 bps of GV

Admin charge • Fee for contract admin; usually $30 Surrender charge

• Paid by policyholder to insurer in the event of lapse (to compensate for commissions paid)

• Typically 7 – 8%; declining by 1% pa

Separate Account

Policyholder

Investment manager

Advisor

General Account

Deposit Commission

(Initial + Trailer)

IMF = Investment Management Fee

IMF

Insurance charge

Administrative Charges

Rider charge

Expenses (e.g.,

Marketing, Maintenance)

Revenue sharing

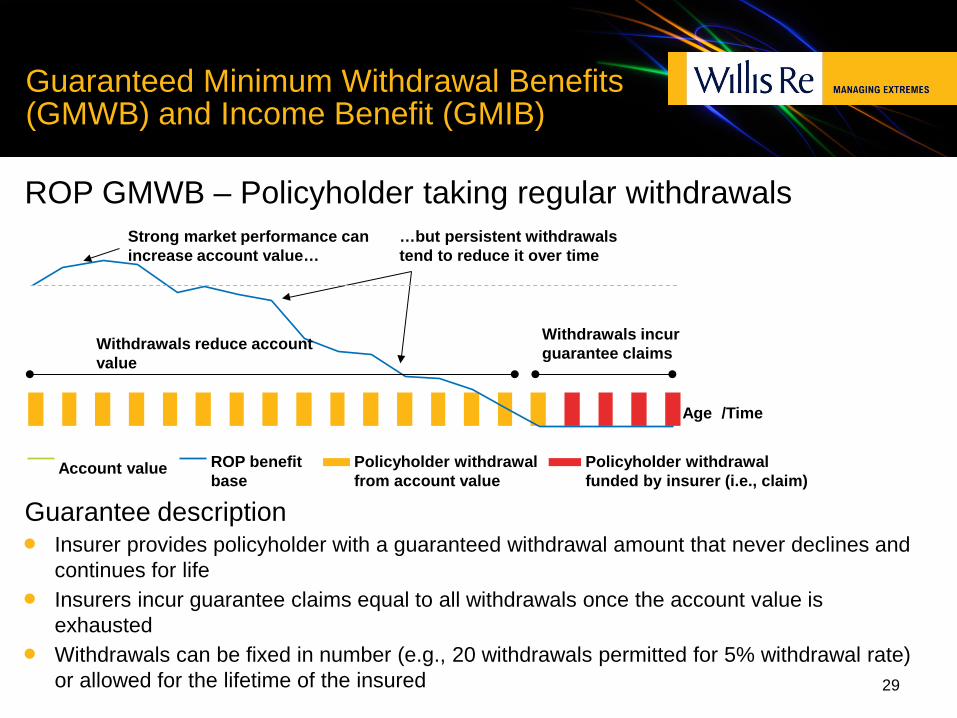

Guaranteed Minimum Withdrawal Benefits (GMWB) and Income Benefit (GMIB)

Guarantee description • Insurer provides policyholder with a guaranteed withdrawal amount that never declines and

continues for life • Insurers incur guarantee claims equal to all withdrawals once the account value is

exhausted • Withdrawals can be fixed in number (e.g., 20 withdrawals permitted for 5% withdrawal rate)

or allowed for the lifetime of the insured

ROP GMWB – Policyholder taking regular withdrawals

Age /Time

Withdrawals incur guarantee claims Withdrawals reduce account

value

Strong market performance can increase account value…

…but persistent withdrawals tend to reduce it over time

Policyholder withdrawal from account value

ROP benefit base

Policyholder withdrawal funded by insurer (i.e., claim)

Account value

29