Embed Size (px)

Citation preview

Banco PINE is specialized in financial services for companies

Institutional

Presentation

3Q09

2/47

Profile

Banco PINE

History of Banco PINE

Macroeconomic Scenario

Strategies for the New Scenario

New Business Opportunities

Companies‟ Profile

Agility in Granting Credit

Companies - Credit Committee

Companies - Credit Systems

Organizational Structure

Strategies for the New Scenario

PINE Investimentos

Cross-Selling

3Q09 Results

Corporate Governance and Shares

Corporate Governance

Main Committees

Shares

Dividends

Social Responsibility

Ratings

Appendix

Agenda

3/47

Profile

Banco PINE

History of Banco PINE

Macroeconomic Scenario

Strategies for the New Scenario

New Business Opportunities

Companies‟ Profile

Agility in Granting Credit

Companies - Credit Committee

Companies – Credit Systems

Organizational Structure

Strategies for the New Scenario

PINE Investimentos

Cross-Selling

3Q09 Results

Corporate Governance and Shares

Corporate Governance

Main Committees

Shares

Dividends

Social Responsibility

Ratings

Appendix

Agenda

Profile

5/47

HIGHLIGHTS – SEPTEMBER 2009

Loan Portfolio: R$4,113 million

ROAE: 11.3%

BIS Ratio: 17.2%

Efficiency Ratio: 44.0%

Clients‟ annual revenues: 87% of the Bank‟s

loan portfolio comprise companies with

revenues of more than R$150 million, while

67% include companies with annual

revenues superior to R$500 million

Banco PINE

Banco PINE's DNA is providing services to Companies

PROFILE

Complete range of services for Companies

Diversified and sophisticated products

Cross-selling opportunities

Financial health based on a prudent strategy

Operating efficiency and good controlling tools

Highly qualified team in all Bank‟s departments

6/47

1939 – Pinheiro Family founds its first bank in Brasil – Banco Central do Nordeste

1975 - Noberto Pinheiro becomes one of the contolling shareholder of Banco BMC

1997 - Noberto and Nelson Pinheiro sell their stake at BMC and found Banco PINE

2005 - Noberto Pinheiro becomes Banco PINE´s sole shareholder

2007 – Start up of Cayman branch

2007 - IPO

History of Banco PINE

Founded in 1997, Banco PINE has been showing a track of resilient development and full use of all

business opportunities

1997Fundation of Banco

PINE

7/47

History of Banco PINE

Growth history boosted by the IPO. Banco PINE was the first Brazilian mid-size bank to go public

1997Foundation of Banco

PINE

2004Opportunity

identified in the

payroll loan

segment

2007

IPO2005Noberto

Pinheiro

becomes Banco

PINE‟s sole

shareholder

782 1,324

2,077

4,325

dec/04 dec/05 dec/06 dec/07

Total Loan Portfolio (R$ Million)

108%

421 553

853

1,951

dec/04 dec/05 dec/06 dec/07

Deposits (R$ Million)

129%

83%

62% 58%66%

17%

38% 42%34%

dec/04 dec/05 dec/06 dec/07

Loan Portfolio Breakdown

Payroll

Corporate

20%

36%

23%

29%

2004 2005 2006 2007

ROAE

8/47

History of Banco PINE

Strategic decision of leaving the payroll-loan business

2008Expanded

focus on the

Corporate

segment

PAYROLL-LOAN

Reduced margins

Increased competition

Excessive regulation

Scale need

Lack of cross-selling opportunities

Excessive lengthening of maturities

Others

CORPORATE

100% focused on the Bank‟s core business

Agile, complete and customized services for

Companies

Cross-Selling: diversified and sophisticated

products

3,067

3,533 3,534

3,070

Mar/08 Jun/08 Sep/08 Dec/08

Corporate Loan Portfolio (R$ Million)

253

127

21 3

1Q08 2Q08 3Q08 4Q08

Payroll Origination (R$ Million)

1997Foundation of Banco

PINE

2004Opportunity

identified in the

payroll loan

segment

2007

IPO2005Noberto

Pinheiro

becomes Banco

PINE‟s sole

shareholder

9/47

History of Banco PINE

Agile and specialized management to overcome the crisis

Banco PINE’s strengths for managing the crisis:

Discontinuity of the payroll-loan business – no dependency upon long-term

funding

Discontinuity of the vehicle financing „pilot project‟ in early 2008

Strict policy of matching assets and liabilities

Agility and efficiency in managing cash position

Focus on robust companies

Close relationship with clients

Ability in credit analyses, structuring and monitoring of collaterized

operations

Strong risk controls and conservative strategy with very low risk exposure

(VaR of 0.26% of Shareholder‟s Equity in December 2008)

Lack of leveraged derivatives

2008Global

Financial

Crisis

1997Foundation of Banco

PINE

2004Opportunity

identified in the

payroll loan

segment

2007

IPO2005Noberto

Pinheiro

becomes Banco

PINE‟s sole

shareholder

2008Expanded

focus on the

Corporate

segment

31%37% 33%

40%

51%45% 47%

Mar/08 Jun/08 Sep/08 Dec/08 Mar/09 Jun/09 Sep/09

Cash Position x Time Deposits

10/47

Macroeconomic Scenario

Brazil: Main Economic Indicators - Banco Pine

ECONOMIC INDICATORS (basis scenario: 75% of probability) 2002 2003 2004 2005 2006 2007 2008 2009F 2010F2011-15 (F)

Real GDP growth rate (%) 2.7% 1.1% 5.7% 3.2% 4.0% 5.4% 5.1% 0.2% 4.8% 4.7%

R$:US$ end of the period (nominal) 3.54 2.91 2.67 2.34 2.14 1.79 2.40 1.70 1.63 1.47

R$:US$ average (nominal) 2.99 3.06 2.92 2.44 2.18 1.95 1.84 1.99 1.79 1.54

BR inflation (IPC / IPCA) 12.5% 9.3% 7.6% 5.7% 3.1% 4.5% 5.9% 4.3% 4.7% 4.5%

BR inflation (IGP-M) 25.3% 8.7% 12.5% 1.3% 3.8% 7.7% 9.8% -1.5% 5.6% 6.5%

BR interest rate (Selic, end of the period) 25.0% 16.5% 17.8% 18.00% 13.25% 11.25% 13.75% 8.75% 11.75% 10.50%

BR interest rate (Selic, average) 19.5% 23.1% 16.4% 19.15% 15.06% 11.98% 12.54% 9.92% 10.23% 11.13%

Total external debt (US$bn) 196.0 200.0 185.0 154.0 156.0 166.0 170.0 169.9 174.5 188.0

Private(US$bn) 85.0 80.0 70.0 66.0 80.0 96.0 103.0 105.6 114.0 131.1

Public (US$bn) 111.0 120.0 115.0 88.0 76.0 70.0 67.0 64.3 60.5 56.8

External Reserves (US$bn) 38.0 49.0 53.0 54.0 86.0 180.0 207.0 250.0 322.0 502.0

Total external debt (% of reserves) 516% 408% 349% 285% 181% 92% 82% 68% 54% 37%

Private (% of reserves) 224% 163% 132% 122% 93% 53% 50% 42% 35% 26%

Public (% of reserves) 292% 245% 217% 163% 88% 39% 32% 26% 19% 11%

Commercial balance (US$bn) 13.2 24.8 33.8 44.8 46.2 40.0 25.0 33.0 21.5 15.0

Current Account (US$bn) -7.6 4.2 11.7 14.0 13.6 1.5 -35.0 -12.0 -25.0 -35.0

Current Account (% of GDP) -1.5% 0.8% 1.8% 1.6% 1.3% 0.1% -3.1% -1.2% -2.1% -2.6%

Primary Surplus (% of GDP) 3.5% 3.9% 4.2% 4.4% 3.9% 4.0% 4.3% 1.5% 2.0% 3.3%

Public sector net debt/GDP 55.5% 57.2% 51.8% 51.5% 45.0% 42.7% 37.0% 42.5% 39.0% 36.0%

Brazil Risk (bps, end of period) 1,439 463 383 311 194 221 450 200 150 80

Challenge for the new scenario: economic growth and interest rate below historic rates.

11/47

Profile

Banco PINE

History of Banco PINE

Macroeconomic Scenario

Strategies for the New Scenario

New Business Opportunities

Companies‟ Profile

Agility in Granting Credit

Companies - Credit Committee

Companies – Credit Systems

Organizational Structure

Strategies for the New Scenario

PINE Investimentos

Cross-Selling

3Q09 Results

Corporate Governance and Shares

Corporate Governance

Main Committees

Shares

Dividends

Social Responsibility

Ratings

Appendix

Agenda

Strategies for the

New Scenario

13/47

New Business Opportunities

Banco PINE has the opportunity of getting into a segment poorly served in the local market,

expanding its operations

Large multiple banks

Wholesale

mid-size banks

Poorly served segment

Banco PINE: focused on corporate loan, offering

taylor-made sophisticated products with

transparency and agility.

Mid-size banks

Fore

ign b

anks

14/47

Company‟s Profile

Strong penetration in the Upper Middle

and Low Corporate segments (annual

revenues)

Present in the main

economic Sectors

30%35% 37%

22%

28%30%

29%

20%20%

19% 17% 13%

Mar-09 Jun-09 Sep-09

Up to R$ 150 million

R$ 150 to R$ 500 million

R$ 500 million to R$ 1 billion

> R$ 1 billion

Sugar and Ethanol

17%

Infrastructure15%

Vehicles and Autoparts

11%

Specialized Services

7%

Energy7%

Agriculture6%

Construction6%

Financial Institutions

4%

Logistics3%

Meat Processing3%

Food2%

Construction and

DecorationMaterial

2%Metallurgy

1%

Other16%

Banco PINE thoroughly understands the needs of its clients

15/47

Agility in Granting Credit

72-hour process in average; credit analysis may be concluded within 1 business day in special cases

Reports on credit visits and loan

transactions structuring

Credit analysis, visits to

clients, data update,

interaction with internal

research team and issue of

opinion

Issue of opinion

Presentation of

proposals to the

Committee

Sales Officer

Credit Analyst

Platform and

Regional

Superintendents

Chief Credit Officer

and Credit Analysts

CREDIT COMMITTEE

16/47

CREDIT COMMITTEE

Twice a week

Minimum quorum: 4 members

(attendance of CEO or Chairman is mandatory)

Members:

Chairman of the Board

CEO

Corporate Vice-President

Corporate Processing, Formalization and Legal

Vice President

Chief Credit Officer

The credit analysts present their research on the company and the transaction

The relationship department defend the credit proposal

Committee members present their opinions and votes

The last one to express their opinion and vote are the CEO or Chairman

Approval Model

Companies - Credit Committee

The approval must be unanimous

Participants:

Credit Analysts

Other members of the Corporate Commercial

17/47

Information available on the systems:

Visits to clients

Revenue, Balance Sheet, Income Statement and other financial information

Company‟s debt information, provided by the Central Bank: type, institution, amounts, terms and amounts overdue

Restrictions (such as at Serasa, a consumer-credit rating service)

Recommendations from all parties involved (regional platform, superintendents, credit department, etc.)

Characteristics of transactions

Companies‟ import and export information, provided by Central Bank

Companies - Credit Systems

Advanced credit systems, with record keeping and regular updating

18/47

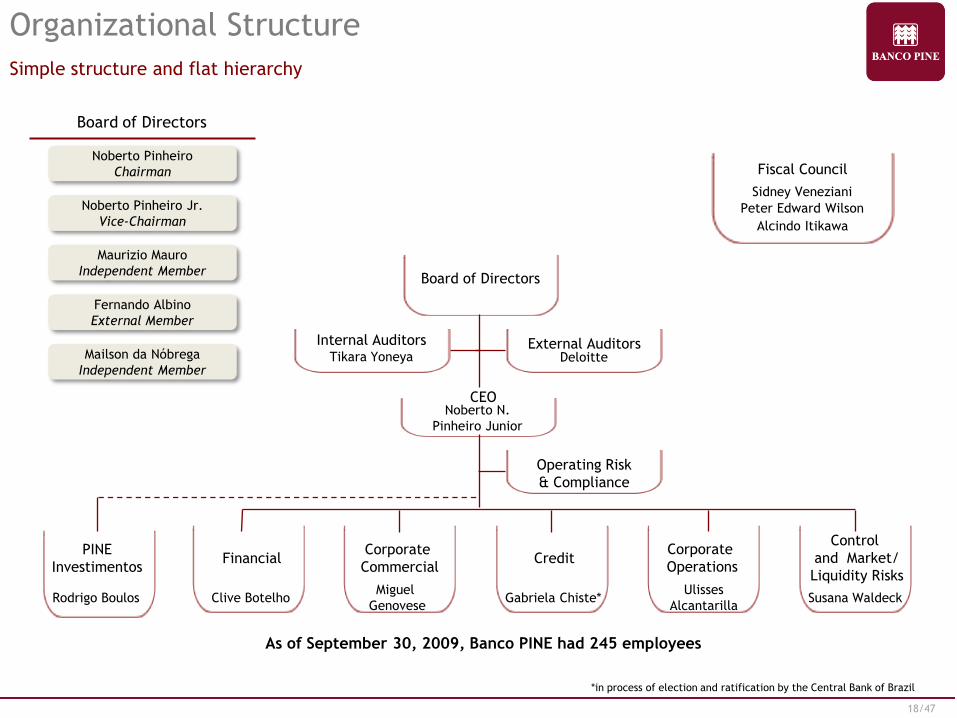

Organizational Structure

Simple structure and flat hierarchy

Internal AuditorsTikara Yoneya

CEONoberto N.

Pinheiro Junior

Board of Directors

Fiscal Council

Sidney Veneziani

Alcindo Itikawa

Peter Edward Wilson

External AuditorsDeloitte

Noberto Pinheiro

Chairman

Maurizio Mauro

Independent Member

Fernando Albino

External Member

Mailson da Nóbrega

Independent Member

Noberto Pinheiro Jr.

Vice-Chairman

Board of Directors

Credit

Gabriela Chiste*

Financial

Clive Botelho

Corporate

Commercial

Miguel

Genovese

Control

and Market/

Liquidity Risks

Susana Waldeck

Corporate

Operations

Ulisses

Alcantarilla

PINE

Investimentos

Rodrigo Boulos

As of September 30, 2009, Banco PINE had 245 employees

Operating Risk

& Compliance

*in process of election and ratification by the Central Bank of Brazil

19/47

Strategies for the New Scenario

Criterious portfolio growth and Cross-Selling opportunities

Challenges for the New Scenario:

Interest rate reduction

Banking industry consolidation

Capital optimization:

Stronger leveraging

Cross-selling:

More products per client

Corporate

Loans

Loans

Overdraft accounts

Discounts

Compror/Vendor

Linked Collection

Foreign Exchange

/ Trade Finance

Exports

ACC/ACE

Letter of Credit

Documentary

Collection

Prepayment

Imports

Letter of Credit

Advance Payments

Documentary

Collection

Spot Foreign

Exchange

Foreign currency

loans and

investments

Loans (2,770)

Foreign Lending

Foreign

Investments

Onlending

FINAME

Automatic

Manufacturer

Agribusiness

Others

EXIM

Pre-shipping

Special Pre-

shipping

Post-shipping

Automatic BNDES

FINEM

Guarantees

Bidding

Public tenders

Performance

Credit/Financial

Institutions

Treasury

Currencies

Interests

Commodities

Equities

Indexes

Macro Advisory

Investments

Local Currency

CDB/ RDB

Government Bonds

FIDC (Receivables

Investment Funds)

CDI (Interbank

Deposit

Certificate)

LCA (Agribusiness)

Credit Funds

Foreign Currency

CD -Certificate of

Deposit

Demand Deposit

Accounts

Eurobonds

Custody Account

Money Market

Accounts

Time Deposit

Private Equity

PINE

Investimentos

Financial Advisory

Strategic Advisory

Mergers &

Acquisitions

Underwriting and

Syndicated Loans

Private Equity

Credit Funds

20/47

Third-parties Asset Management

Credit Funds

Private Equity Funds

Corporate Services

Mergers & Acquisitions

Financial Advisory

Credit Structuring

Syndicated Loans

PINE Investimentos

PINE Investimentos setup: creation of new values for clients and optimization of the Bank's capital

usage

Banco PINE’s current partnerships include:

Private Equity Fund in association with the American Global Emerging Market Fund (GEM)

Financial advisory services provided together with Pátria Investimentos

Exclusive credit funds in the amount of R$ 350 million

21/47

Positioning of our business:

“More than selling products, our mission is to understand the needs of our

clients in order to provide solutions for their businesses,

strengthening the relationship”

Client Selection

Business Analysis

Visits Strategies

Sharing of Information

Visits

Information Analysis

Planning of actions

and executions

Offer to Client

Cross-selling

Strategy for creation of a cross-selling culture.

22/47

Profile

Banco PINE

History of Banco PINE

Macroeconomic Scenario

Strategies for the New Scenario

New Business Opportunities

Companies‟ Profile

Agility in Granting Credit

Companies - Credit Committee

Companies – Credit Systems

Organizational Structure

Strategies for the New Scenario

PINE Investimentos

Cross-Selling

3Q09 Results

Corporate Governance and Shares

Corporate Governance

Main Committees

Shares

Dividends

Social Responsibility

Ratings

Appendix

Agenda

3Q09 Results

24/47

HighlightsIn light of the gradual improvement in the economic scenario, Banco PINE expanded its loan

portfolio and deposits.

17.1%

11.1%11.3%

3Q08 2Q09 3Q09

ROAE

20 bps-600 bps

1.0%

1.7%

1.3%

Sep-08 Jun-09 Sep-09

NON-PERFORMING LOANS

-40 bps

70 bps

47.1%

44.8%44.0%

3Q08 2Q09 3Q09

EFFICIENCY RATIO

- 80 bps

- 230 bps

3,534

3,068

3,416

Sep-08 Jun-09 Sep-09

CORPORATE LOAN PORTFOLIO (R$ Million)

11.3%-13.2%

50,935

34,502 37,639

3Q08 2Q09 3Q09

OPERATING INCOME(R$ Thousand)

9.1%

-32.3%

2,148

1,917

2,302

Sep-08 Jun-09 Sep-09

TOTAL DEPOSITS(R$ Million)

20.1%-10.8%

25/47

Balance SheetOn book loan portfolio increased 8.8% in the quarter

R$ million

Sep-09 Jun-09 Sep-08

Assets 7,200 6,275 4,741

Securities and derivative financial instruments 3,578 2,791 542

Lending operations 3,210 2,951 3,541

(-) Allowance for loan losses (105) (107) (71)

Net lending operations 3,105 2,844 3,470

Other 517 640 729

Liabilities 6,385 5,464 3,910

Deposits 2,201 1,849 2,062

Money market funding 2,585 1,915 37

Funds from acceptance and securities issued 718 769 576

Other 881 931 1,235

Shareholders' equity 815 811 831

Liabilities and Shareholders' equity 7,200 6,275 4,741

26/47

ResultsThe operating Income increased 9.1% in the quarter.

R$ thousand

3Q09 2Q09 3Q08

Gross income from financial intermediation 50,594 43,922 103,319

Fee Income 21,678 29,498 3,892

Personnel and Administrative Expenses (28,525) (30,021) (36,667)

Commissions (873) (1,050) (5,335)

Tax Expenses (6,286) (7,716) (12,190)

Other Operating (expenses) income 1,051 (131) (2,084)

Operating Income 37,639 34,502 50,935

Non-operating income (1) 886 (1,806)

Income before taxes 37,638 35,388 49,129

Income and social contribution taxes (9,566) (9,056) (10,667)

Profit Sharing (6,004) (4,532) (5,033)

Net Income 22,068 21,800 33,429

ROAE 11.3% 11.1% 17.1%

27/47

Loan PortfolioIn the corporate loan portfolio, working capital loans recorded a 15.7% growth in the quarter.

4,885 3,922 4,113

Sep-08 Jun-09 Sep-09

Loan Portfolio (R$ Million)

-19.7%

4.9%

72% 78% 83%

28% 22% 17%

Sep-08 Jun-09 Sep-09

Portfolio Breakdown

Individuals

Corporate

2,709

1,940 2,244

486

836 822

339

292 350

Sep-08 Jun-09 Sep-09

Corporate Portfolio Breakdown (R$ Million)

Guarantees

Onlending and Trade Finance

Working Capital

-13.2%3,534

3,0683,41611.3%

1,005

679 552

217

79 66

129

95

79

Sep-08 Jun-09 Sep-09

Individuals Portfolio Breakdown (R$ Million)

Third-parties portfolio

Own portfolio

Off book portfolio

-36.8%

1,351

854697

-18.4%

28/47

Loan Portfolio - CorporateBanco PINE offers a complete range of loan products in both local and foreign currency. 110% of

the corporate loan portfolio is covered by guarantees

Receivables31%

Product Fiduciary Alienation

22%

Investments9%

Property Fiduciary Alienation

10%

Promissory Notes24%

Payroll4%

Loan Portfolio by Product Guarantees

Working Capital66%

FX17% Financing in

Foreing Currency

3%

Onlendings (Instr. 2770)

1%

Guarantees10%

BNDES Onlendings

3%

29/47

0.00%

1.95%

0.30%

0.91%

0.11%

0.65%

0.96% 1.00%

0.60%

0.90%

1.69%

1.28%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Jun/09 Sep/09

Real Devaluation

Nasdaq WTC Brazilian Elections

Banco Santos Liquidity Crisis

Global Financial

Crisis

Loan Portfolio Quality and NPL Historical Data

Overdue D-H Portfolio / Total PortfolioLoan portfolio quality

Strict quality control of the loan portfolio. The coverage of the D-H portfolio was 100.2% in

September.

AA; 23.6%

A; 45.0%

B; 24.7%

C; 3.5%

D-E; 1.1%

F-H; 2.1%

30/47

Funding

Medium Term Note

Joint Lead Managers

Public Offering - MTN

2008

Foreign Funding – Private Placements

US$ 33.6 Million

US$ 35.5 MillionUS$ 52.8 Million

US$ 39.9 Million

US$ 150 Million

1,841 1,756

2,154

Sep-08 Jun-09 Sep-09

Time Deposits + Agribusiness Letter of Credit (R$ Million)

-4.6% 22.7%

2,148 1,917 2,302

1,005

679 553

429

642 576

554

306 275

147

128 142

Sep-08 Jun-09 Sep-09

Funding Mix (R$ Million)

Borrowings and Onlendings

Funds from Acceptance and Securities Issued

Trade Finance / Cayman

Loan Assigments

Deposits

3,672 3,848

4,283

-14.34.8%

Average funding maturity in 3Q09 was 10 months.

31/47

Financial MarginFinancial Margin in 3Q09 would be 80 bps higher than the figure delivered excluding early

settlements in the payroll loan business.

Main factors impacting 3Q09 financial margin:

• Deleveraging of the loan portfolio, specially between September 2008 and March 2009, due to the

international financial crisis;

• Focus on large companies in 3Q09;

• No payroll loan assignments;

• Absorption of early settlements in the payroll loan business;

• Reduced interest rates in the quarter, leading to an impact if 10 bps on return on free capital.

3Q09 9M09

Margin before provision for

loan losses (excluding repo) 7.1% 7.4%

7.0% 7.1%

2Q09 3Q09

10 bps

32/47

Profile

Banco PINE

History of Banco PINE

Macroeconomic Scenario

Strategies for the New Scenario

New Business Opportunities

Companies‟ Profile

Agility in Granting Credit

Companies - Credit Committee

Companies - Credit Systems

Organizational Structure

Strategies for the New Scenario

PINE Investimentos

Cross-Selling

3Q09 Results

Corporate Governance and Shares

Corporate Governance

Main Committees

Shares

Dividends

Social Responsibility

Ratings

Appendix

Agenda

Corporate

Governance and

Shares

34/47

Corporate Governance

Banco PINE adopts the best corporate governance practices

Clear PoliciesPerformance

Monitoring

Risk Management

Settlement of

Responsibilities

Alignment of

Internal Policies

Compliance with

Legislation and

interests

Three independent members in the Board of Directors

Mailson Ferreira da Nóbrega: Finance Minister of Brazil

from 1988 to 1990

Maurizio Mauro: CEO of Booz Allen Hamilton and Grupo

Abril

Fernando Albino de Oliveira: ex-director of CVM and

partner of Albino Advogados Associados

São Paulo Stock Exchange Level 1 of Corporate Governance

Fiscal Council

100% tag along rights for all shareholders, including non-

voting shares

Arbitration procedures for fast settlement of litigation

35/47

Main decisions are taken by committees: Board of Directors and a structure of specific committees

Non-stop exchange of knowledge and information

Transparency

Main Committees

Banco PINE believes that the use of the best corporate governance practices substantially enhances

its business‟ outcome

Board of

Directors

Fiscal

Council Audit

Support

Committee

Treasury

Committee

(ALCO)

National and

Foreign Funding

Products

Committee

Credit

Committee

Retail

Committee

Delinquency

Committee

Compliance

and Basel Risk

Committee

Executive

Committee

Performance

Evaluation

Committee

Ethics

CommitteeIT Committee

Human

Resources

Committee

PINE

Investimentos

Committee

36/47

Shares

Shareholders' structure breakdown

2007

IPO

78.4%

8.7%

12.9%

11.1%

13.8%12.9%

20.4%19.0%

20.6% 20.9% 20.9%20.2% 19.6% 19.5% 20.1% 19.7%

37.3%38.5%

41.7%

31.1%

37.2%

32.3%

38.3%39.7%

41.9%

43.6%44.9% 45.1%

43.6%

51.6%

47.7%

45.5%

48.5%

43.8%

47.1%

40.8%39.4%

37.9%

36.7%35.7%

34.8%

36.6%

Sep-08 Oct-08 Nov-08 Dec-08 Jan-09 Feb-09 Mar-09 Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09

Institutional

Investors

Individuals

Foreign

Investors

37/47

Basis Price100: 08/01/08

Final Date: 10/31/09

Shares

Evolution of PINE4 and IBOVESPA (São Paulo Stock Exchange Index)

40

50

60

70

80

90

100

110

120

130

140

5/2008

6/2008

7/2008

8/2008

9/2008

10/2008

11/2008

12/2008

1/2009

2/2009

3/2009

4/2009

5/2009

6/2009

7/2009

8/2009

9/2009

10/2009

PINE4 IBOVESPA09/15/08

Lehman Brothers bankruptcy

D 14.8%R$ 10.33

D 6.8%61,545

R$ 9.00

57,630Withdrawal of foreign

Investors

38/47

Dividends and Interest on Own Capital

Dividends

Since 2008, Banco PINE pays dividends/interest on own capital on a quarterly basis

16 25 25

33

45

15

1H07 2H07 1H08 2H08 1H09 3Q09

Gross Dividend and Interest on Own Capital (R$ million)

R$ Million R$

Gross Amount Total Amount Value per Share

1Q09 25.0 0.2955

2Q09 20.0 0.2391

3Q09 15.0 0.1800

Total paid in 9M09 60.0 0.7146

39/47

Social

Casa Hope

Instituto Alfabetização Solidária.

Sports

Fortalecimento do Hipismo (Strengthening Equestrian

Sports): dissemination of equestrian sports as a healthy

activity that is accessible to various social segments.

Crianças e Jovens que Brilham (Children and Youth that

Shine): tennis training workshops in state and municipal

schools

Responsible Credit

“Lists of Exceptions”: the Bank does not finance projects

or those organizations that damage the environment, are

involved in illegal labor practices or produce, sell or use

products, substances or activities considered prejudicial to

society.

System of environmental monitoring, financed by the IADB

and coordinated by FGV, and internally-produced

sustainability reports for corporate loans.

Social Responsibility

Banco PINE supports and promotes the Brazilian culture

Culture

Paisagem e Olhar: watercolor pictures showing the

biodiversity of the Atlantic Rainforest

Embarcações: historic record of typical Brazilian boats

Revoluções Brasileiras:

reports about the bravery

of Brazilian ancestors

Museus Brasileiros: a collection of

the country‟s leading museums

Anita Malfatti: retrospective of works

and biography

Green Building

40/47

Global

Foreign Currency

Long Term

Outlook

Local Currency

Long Term

Outlook

National

Long Term

Short Term

Outlook

Bank Financial Strength

Ba2

Stable

Ba2

Stable

A1.br

Br-1

Stable

D

A

Ratings

BB-

B

Stable

BB-

B

Stable

br A-

Stable

Global

Foreign Currency

Long Term

Short Term

Outlook

Local Currency

Long Term

Short Term

Outlook

National

Long Term

Outlook

10.54

Global

Foreign Currency

Long Term

Short Term

Outlook

Local Currency

Long Term

Short Term

Outlook

National

Long Term

Short Term

Outlook

Individual

Support

B+

B

Stable

B+

B

Stable

A-(bra)

F2(bra)

Stable

D

5

Appendix

42/47

Financial Statements Highlights

R$ million

* Excludes Extraordinary Expenses

** Excludes IPO expenses in 2007

84

197269

545 517

220

2004 2005 2006 2007 2008 9M09

Gross Income from Financial Intermediation before Provision

43 49

86

124

151

88

2004 2005 2006 2007 2008 9M09

Personnel and Administrative Expenses (excludes commissions)**

6 6

26

50

6657

2004 2005 2006 2007 2008 9M09

Provision for Loan Losses

(expenses)

32

68 63

166 158

64

2004 2005 2006 2007 2008 9M09

Net Income*

43/47

Balance Sheet Highlights

R$ million

1,3861,991

3,215

5,700 6,1767,200

Dec/04 Dec/05 Dec/06 Dec/07 Dec/08 Sep/09

Total Assets

171 209335

800 827 815

Dec/04 Dec/05 Dec/06 Dec/07 Dec/08 Sep/09

Shareholders' Equity

421 553853

1,951

1,462

2,302

Dec/04 Dec/05 Dec/06 Dec/07 Dec/08 Sep/09

Deposits

19.8%

35.7%

23.0%

29.2%

19.4%

10.5%

2004 2005 2006 2007 2008 9M09

ROAE

44/47

Loan Portfolio

R$ million

7821,324

2,077

4,325 4,264 4,113

Dec/04 Dec/05 Dec/06 Dec/07 Dec/08 Sep/09

Total Loan Portfolio

45/47

Funding

R$ million

759

1,341

2,085

3,623 3,737 3,848

Dec/04 Dec/05 Dec/06 Dec/07 Dec/08 Sep/09

Total Funding

54%41% 40%

54%39%

60%

2% 28% 32%

28%

26%

14%8%

6%11%

7%

13%7%

36%25%

17% 11%18% 15%

4%4% 4%

Dec/04 Dec/05 Dec/06 Dec/07 Dec/08 Sep/09

Funding Breakdown (%)

Deposits Loan Assignments Securities Issued Other Funding Borrowings and Onlendings

46/47

Efficiency Ratio and BIS

68.1%

51.5% 50.3%

37.3%42.6% 45.7%

2004 2005 2006 2007 2008 9M09

Efficiency Ratio

18.2%20.7% 19.2% 18.3% 19.3%

17.2%

Dec/04 Dec/05 Dec/06 Dec/07 Dec/08 Sep/09

BIS Ratio

47/47

Clive Botelho

CFO

Nira Bessler

Head of Investor Relations

Alejandra Hidalgo

Investor Relations Analyst

Phone: +55-11-3372-5553

www.bancopine.com.br/ir

Investor Relations

This presentation contains forward-looking statements relating to the prospects of the business, estimates for operating and financial results, and those related to growth prospects of Banco PINE. These are

merely projections and, as such, are based exclusively on the expectations of Banco PINE’s management concerning the future of the business and its continued access to capital to fund the Company’s

business plan. Such forward-looking statements depend, substantially, on changes in market conditions, government regulations, competitive pressures, the performance of the Brazilian economy and the

industry, among other factors and risks disclosed in Banco PINE’s filed disclosure documents and are, therefore, subject to change without prior notice.